Financing Activities 251

D. As each payment is made, the amount owed decreases. As the unpaid

E.

ASSETS

=

LIABILITIES

+

OWNERS’ EQUITY

Date

Accounts

Cash

Other

Assets

Contributed

Capital

Retained

Earnings

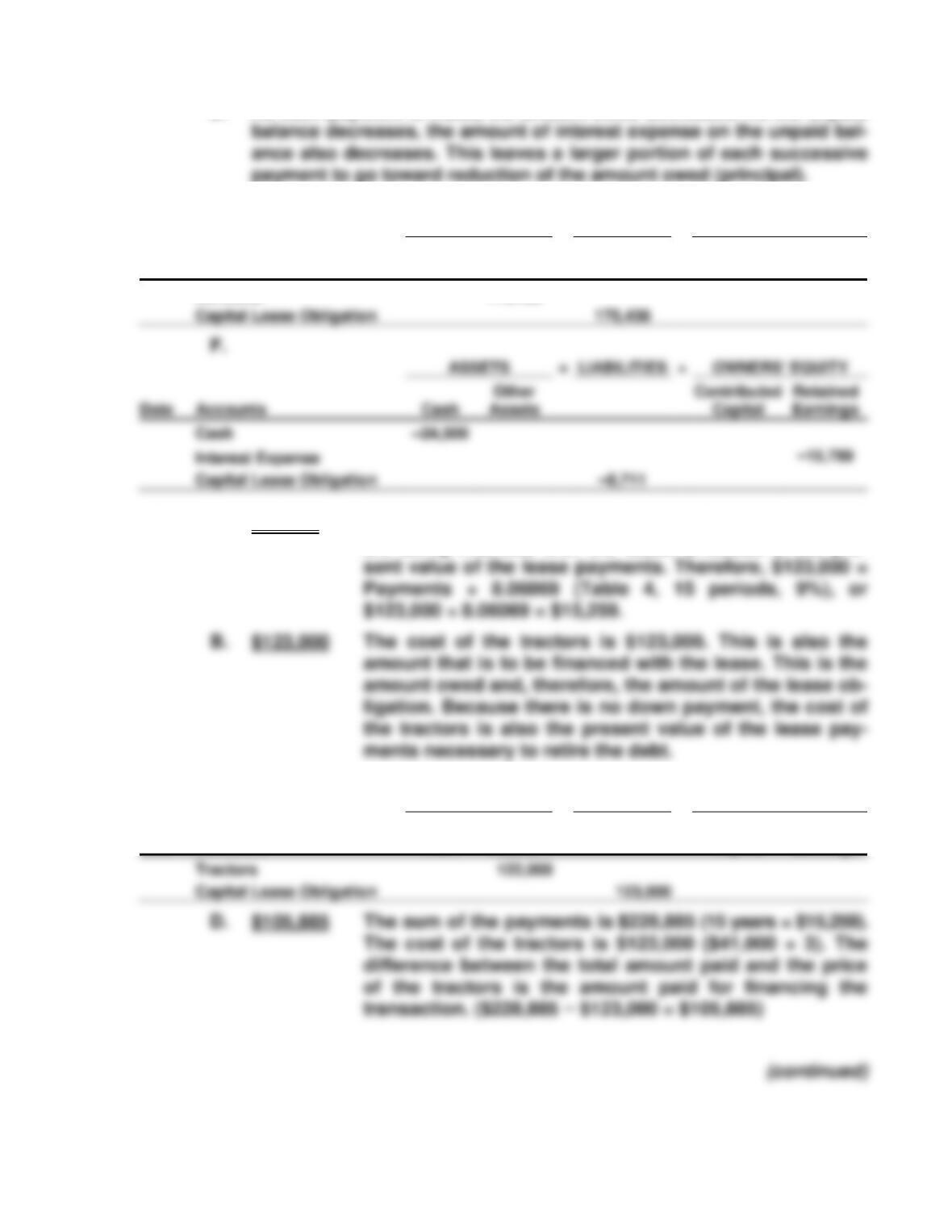

Bulldozer

175,438

Capital Lease Obligation

ASSETS

=

LIABILITIES

+

OWNERS’ EQUITY

Date

Accounts

Cash

Other

Contributed

Capital

Retained

P9-9 A. $15,259 Three tractors with a total cost of $123,000 ($41,000 × 3)

are being financed with the lease. $123,000 is the pre-

C.

ASSETS

=

LIABILITIES

+

OWNERS’ EQUITY

Date

Accounts

Cash

Other

Assets

Contributed

Capital

Retained

Earnings

Tractors

Capital Lease Obligation

252 Chapter 9

E.

ASSETS

=

LIABILITIES

+

OWNERS’ EQUITY

Date

Accounts

Cash

Other

Assets

Contributed

Capital

Retained

Earnings

B.

ASSETS

=

LIABILITIES

+

OWNERS’ EQUITY

Date

Accounts

Cash

Other

Assets

Contributed

Capital

Retained

Earnings

C.

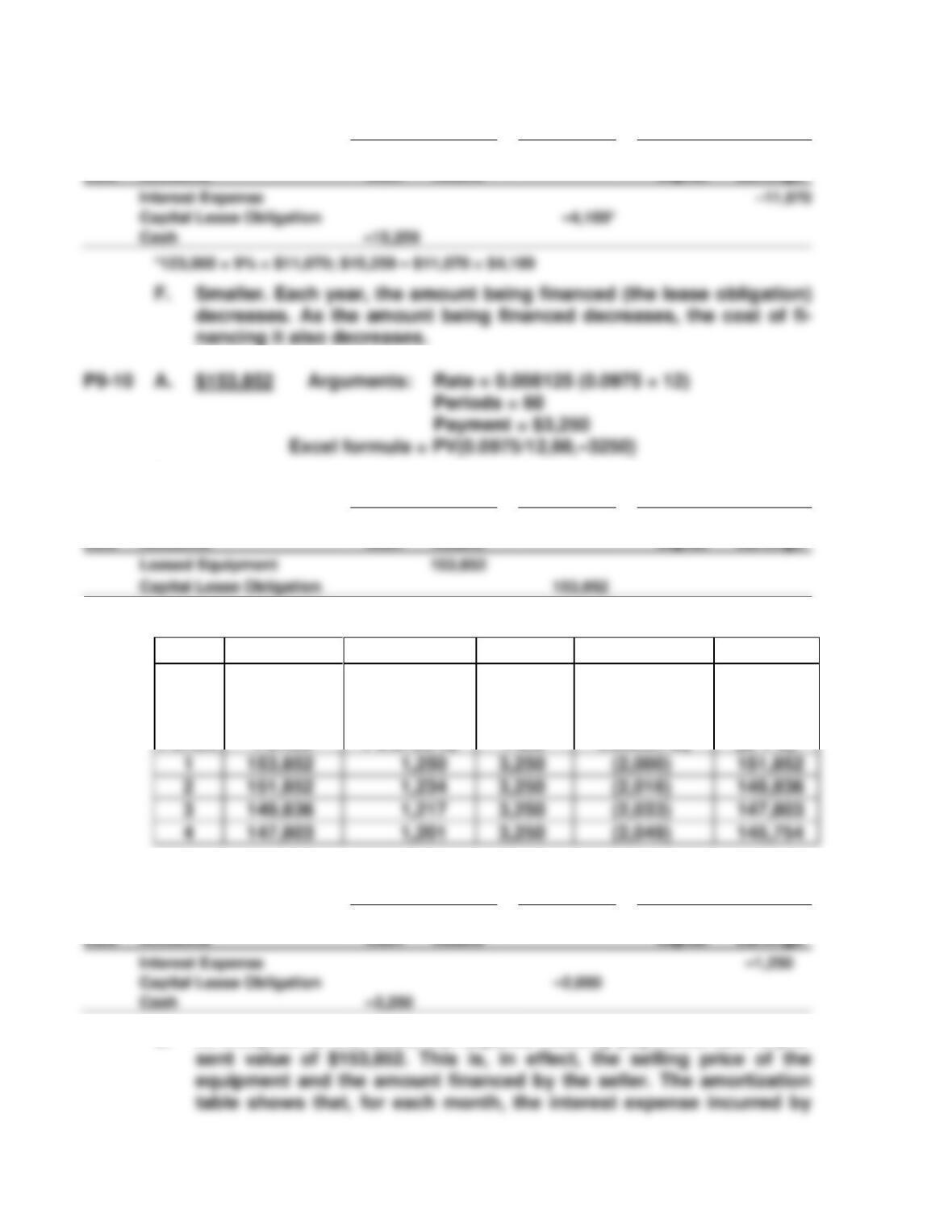

A

B

C

D

E

F

Period

Present

Value at

Beginning of

Period

Interest

Incurred

(Column B

× 0.8125%)

Amount

Paid

Amortization

of Principal

(Column C −

Column D)

Value At

End of

Period

(B + E)

D.

ASSETS

=

LIABILITIES

+

OWNERS’ EQUITY

Date

Accounts

Cash

Other

Assets

Contributed

Capital

Retained

Earnings

Interest Expense

Capital Lease Obligation

Cash

E. At inception of the lease, the required monthly payments have a pre-

Interest Expense

Capital Lease Obligation

Cash

Financing Activities 253

the purchaser is exactly equal to 0.8125% of the amount owed (9¾%

interest ÷ 12 months = 0.8125%). For example, in period one, the pur-

chaser owes a balance of $153,852 for the entire month. At 9¾% an-

B.

ASSETS

=

LIABILITIES

+

OWNERS’ EQUITY

Date

Accounts

Cash

Other

Assets

Contributed

Capital

Retained

Earnings

C.

A

B

C

D

E

F

Period

Present

Value at

Beginning

of Period

Interest

Incurred

(Column B ×

11.35%)

Amount

Paid

Amortization

of Principal

(Column C −

Column D)

Value At

End of

Period

(B + E)

1

350,000

39,725

95,535

(55,810)

294,190

2

294,190

33,391

95,535

(62,144)

232,046

3

232,046

26,337

95,535

(69,198)

162,848

4

162,848

18,483

95,535

(77,052)

5

85,796

95,535

(85,797)

D. The interest expense (column C above) decreases each year because

E.

ASSETS

=

LIABILITIES

+

OWNERS’ EQUITY

Date

Accounts

Cash

Other

Assets

Contributed

Capital

Retained

Earnings

Interest Expense

Capital Lease Obligation

Cash

254 Chapter 9

interest expense incurred by the purchaser is exactly 11.35%. For ex-

P9–12 A. The Stockholders’ Equity section at December 31, 2008, would re-

port:

1The number of shares outstanding after the preceding transactions

would be:

Number at beginning of year 2,200,000

2The value of Retained Earnings after these transactions is:

Beginning balance $46,000,000

B. The financing section of the Statement of Cash Flows would report

the following:

Financing Activities 255

P9–13 A. The Stockholders’ Equity section of the Balance Sheet after the stock

split would be:

B. The Stockholders’ Equity section of the Balance Sheet after the 100%

stock dividend would be:

C. The total of stockholders’ equity is the same whether the company

carries out a split or a dividend. For the split, par is decreased from

P9–14 A. Net income = $26,182. Net income is reported on the bottom of the

256 Chapter 9

B. Dividends = $14,300. The dividends reported here must be cash divi-

C. Treasury stock increase = $1,263. The acquisition of treasury stock is

E. Common stock = $14,000. The cumulative par value of all common

P9–15 A. Stockholders’ Equity Before Conversion

Preferred stock, $5 par, 4,000 shares outstanding $ 20,000

Total $4,598,000

B. Stockholders’ Equity After Conversion

Common stock, $1 par, 57,000 shares outstanding $ 57,000

C. There is no effect on the financing section of the Statement of Cash

Flows.

Financing Activities 257

D. Shareholders are often attracted by convertible preferred stock. So,

they may be willing to accept a lower dividend rate than other, simi-

P9–16 The complete stockholders’ equity section is as follows:

December 31

2008

2007

Stockholders’ Equity

Paid-in capital in excess of par value

Retained earnings

Total Stockholders’ Equity

$1,411,750

8.5% Preferred stock, $10 par value, 10,000

The individual items can be determined as follows:

a. 10,000 preferred shares × $10 par value

b. 10,000 preferred shares × $10 par value

h. Equal to the sum of both years’ net income ($75,000 + $125,000 =

$200,000) minus the dividend paid on April 1, 2008 ($75,000 × 10% =

258 Chapter 9

P9–17 A. 3,000 $300,000 ÷ $100 par value = 3,000 preferred

shares issued; same answer for both years

D. 57,550 (2007) 60,000 shares issued − 2,450 treasury

shares = 57,550

73,600 (2008) 75,000 shares issued − 1,400 treasury

shares = 73,600

$16.00

G. $157,500 (2007) The company was started during 2007. Div-

idends are declared 30 days after the end of

the year. Therefore, no dividends have yet

been declared at December 31, 2007. The

Financing Activities 259

H. $5.25 The preferred stock earns a dividend of

($15,750 ÷ 3,000 shares).

I. zero All dividends due to preferred stock must

be paid before any dividends may be paid

to common. No dividends could be paid to

common stockholders in 2008.

J. zero The preferred stock is cumulative. No divi-

to preferred shareholders.

P9–18 A. 2008: 18,000 preferred shares $450,000 ÷ $25 par value

2007: 15,000 preferred shares $375,000 ÷ $25 par value

B. 2008: 136,000 common shares $680,000 ÷ $5 par value

2007: 115,000 common shares $575,000 ÷ $5 par value

260 Chapter 9

G. $2,599,500 Net income is the change in Retained Earnings

I. $8.46 Total dividends in 2008 $500,000

Less: preferred dividends

P9–19 A. Yes; generally companies will record an estimate of the liability to

repair potential defective products.

E. Yes; as long as the bonds have not been redeemed, they should be

shown as a liability. This would be a current liability, so the company

would be required to transfer the amount from the long-term section

Financing Activities 261

G. No; stock dividends do not require the use of a company’s assets, so

no liability should be recorded.

sheet.

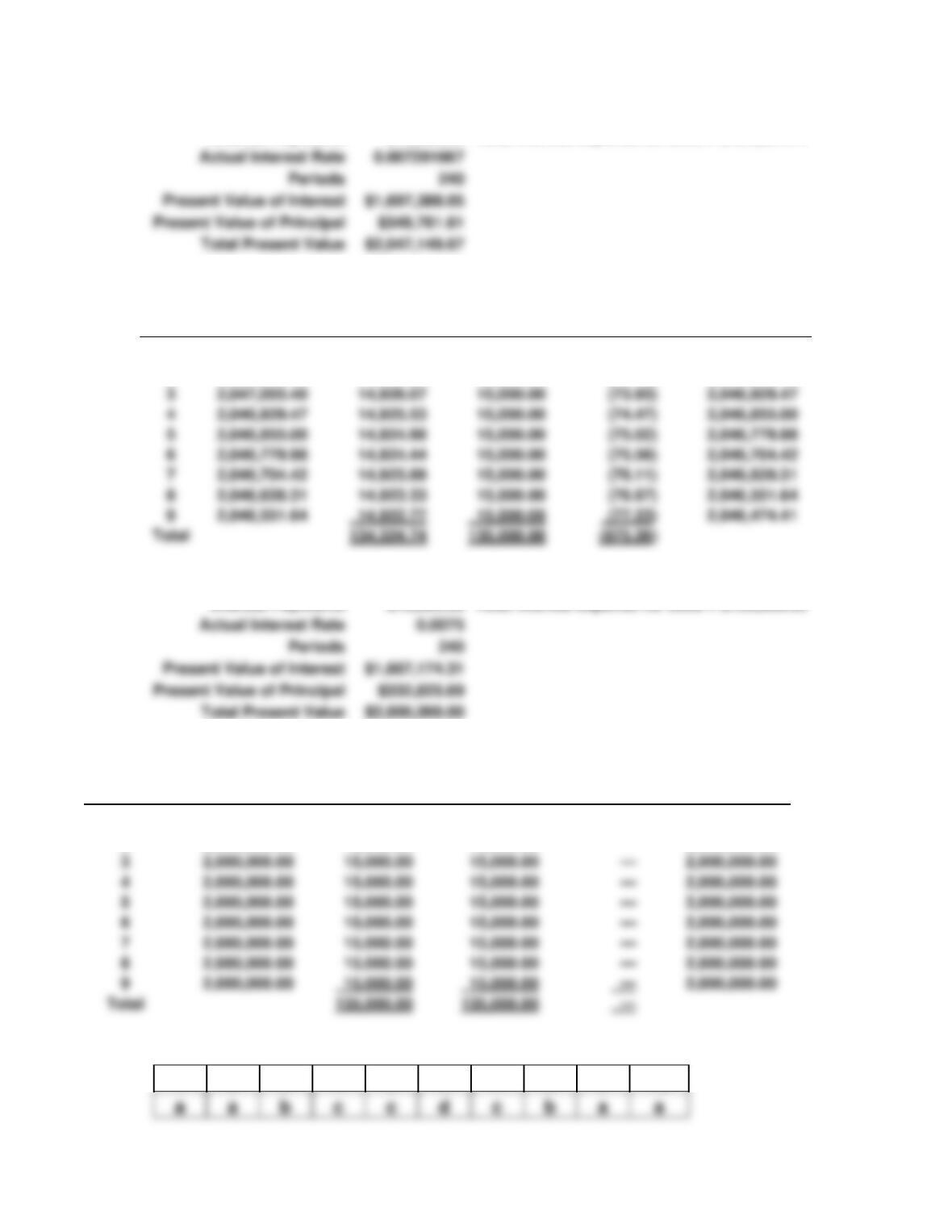

P9–20

Maturity

$2,000,000

Total interest expense in 2008 = $135,612.47

Interest Payments

$15,000.00

Total interest paid in 2008 = $135,000.00

Month

Present Value

at Beginning

of Month

Interest

Incurred

Amount

Paid

Amortization

of Principal

Value at End

of Month

1

1,954,505.76

15,065.98

15,000.00

65.98

1,954,571.74

2

1,954,571.74

15,066.49

15,000.00

66.49

1,954,638.23

3

1,954,638.23

15,067.00

15,000.00

67.00

1,954,705.23

5

1,954,772.75

15,068.04

15,000.00

68.04

1,954,840.79

6

15,068.56

15,000.00

68.56

1,954,909.35

8

15,069.63

15,000.00

69.63

1,955,048.07

9

15,000.00

1,955,118.23

262 Chapter 9

Maturity

$2,000,000

If the effective interest rate were 8.75%:

Interest Payments

$15,000.00

Total interest expense for 2008 = $134,324.74

Month

Present Value

at Beginning

of Month

Interest

Incurred

Amount

Paid

Amortization

of Principal

Value at End

of Month

1

2,047,149.67

14,927.13

15,000.00

(72.87)

2,047,076.80

2

2,047,076.80

14,926.60

15,000.00

(73.40)

2,047,003.40

2,047,003.40

14,926.07

(73.93)

2,046,929.47

14,925.53

(74.47)

2,046,779.98

14,924.44

(75.56)

2,046,704.42

14,923.89

(76.11)

2,046,551.64

Maturity

$2,000,000

If the effective interest rate were 9%:

Interest Payments

$15,000.00

Total interest expense for 2008 = $135,000.00

Month

Present Value

at Beginning

of Month

Interest

Incurred

Amount Paid

Amortization

of Principal

Value at End

of Month

1

2,000,000.00

15,000.00

15,000.00

—

2,000,000.00

2

2,000,000.00

15,000.00

15,000.00

—

2,000,000.00

3

2,000,000.00

15,000.00

—

2,000,000.00

5

2,000,000.00

15,000.00

15,000.00

—

2,000,000.00

6

2,000,000.00

15,000.00

15,000.00

—

2,000,000.00

8

2,000,000.00

15,000.00

15,000.00

—

2,000,000.00

9

2,000,000.00

2,000,000.00

P9–21

1

2

3

4

5

6

7

8

9

10

Financing Activities 263

CASES

C9-1 Information that might be helpful in making a loan decision would include

the following:

A description of the company: A borrower should describe the busi-

Financial statements for the business for the past several years: A

creditor is interested in whether a borrower is likely to pay interest and

principal at the agreed times. The ability of a borrower to make these

date.

A plan describing future activities and use of borrowed funds: In addi-

tion to historical statements, information about expected future activities

C9-2 A. The par value of a company’s stock represents the portion of con-

tributed capital that may be legally restricted. In some states, corpo-

264 Chapter 9

B. Preferred stock typically has a fixed dividend rate. If the stock is cu-

mulative, dividends in arrears must be paid before dividends can be

C. Suspension of preferred dividends has no effect on the financial

statements. No account balances are affected directly by the deci-

December 31 (Millions) 2007 2006

Total assets $3,759.7 $3,774.4

D. The common stockholders have only a small claim to the company’s

future cash flows and earnings. This claim increased in 2007, how-

Financing Activities 265

C9-3 A. At year-end 2004, liabilities are a primary source of financing for as-

sets. At that date, 70% of the company’s assets were financed with

liabilities.