Chapter 9 – Long-Term Liabilities

9-60 Financial Accounting, 5e

Requirement 3

Premium. The issue price is $916,254.

Calculator Input

Bond

Characteristics

Key

Amount

1. Face amount

FV

$850,000

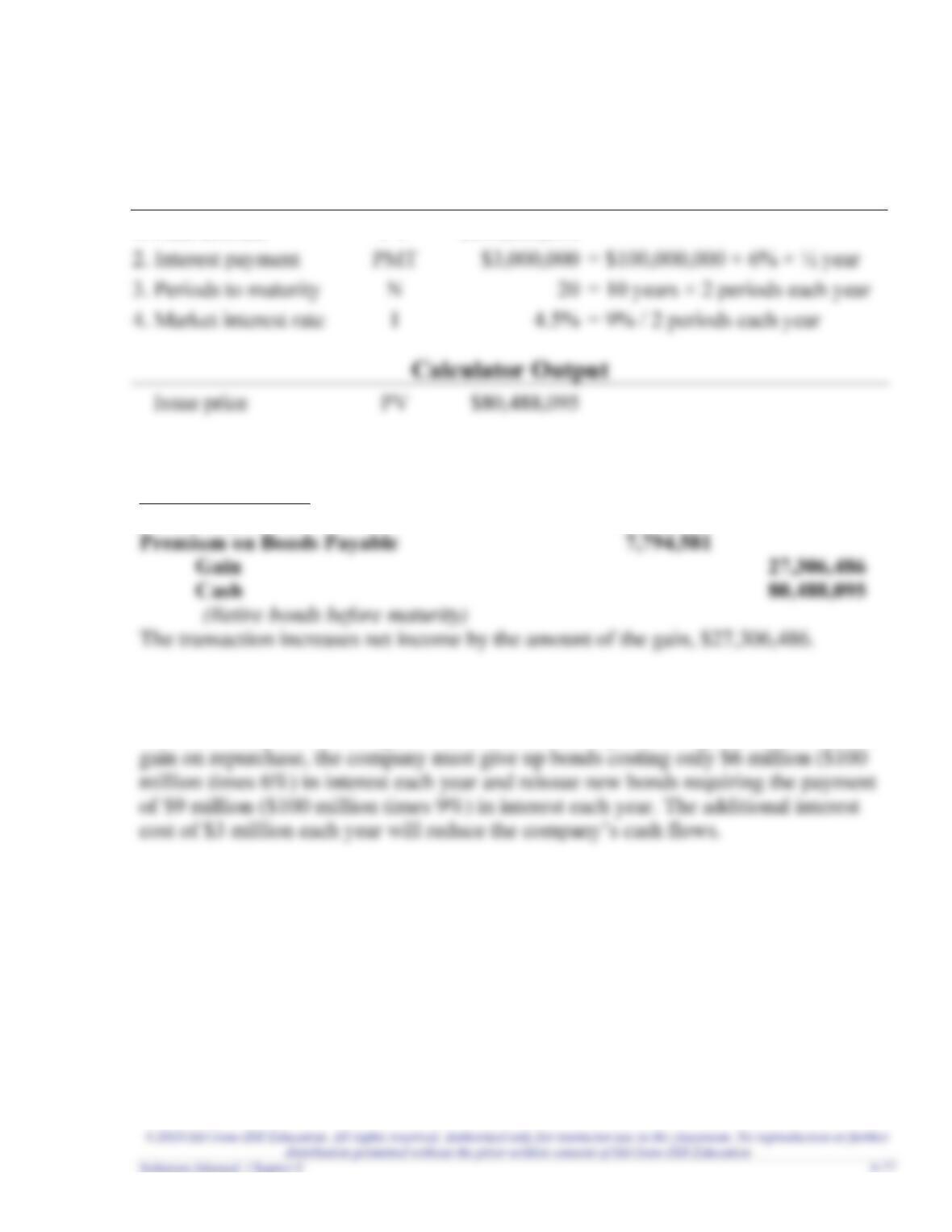

2. Interest payment

3. Periods to maturity

4. Market interest rate

PV

(1)

Date

(2)

Cash

Paid

(3)

Interest

Expense

(4)

Decrease in

Carrying

Value

(5)

Carrying

Value

Face Amount

Carrying Value

Prior Carrying

Chapter 9 – Long-Term Liabilities

Problem 9-8B (LO 9-8)

Requirement 1

($ in millions)

Total

Liabilities

÷

Stockholders’

Equity

=

Debt to Equity

Ratio

Surf City

÷

=

Paradise Falls

÷

=

Requirement 2

($ in millions)

Net

Income

÷

Average

Total Assets

=

Return on

Assets Ratio

Surf City

$18

÷

$19,816*

=

0.1%

Paradise Falls

÷

=

3.3%

Requirement 3

($ in millions)

Net Income +

Interest + Taxes

÷

Interest

=

Times Interest

Earned Ratio

Surf City

÷

=

Paradise Falls

÷

=

Chapter 9 – Long-Term Liabilities

9-62 Financial Accounting, 5e

ADDITIONAL PERSPECTIVES

Continuing Problem: Great Adventures

AP9-1

Requirement 1

(1)

Date

(2)

Cash

Paid

(3)

Interest

Expense

(4)

Decrease in

Carrying

Value

(5)

Carrying

Value

Monthly

Carrying Value

Prior Carrying

Chapter 9 – Long-Term Liabilities

Requirement 2

November 1, 2022

Land

500,000

Notes Payable (long-term)

Requirement 3

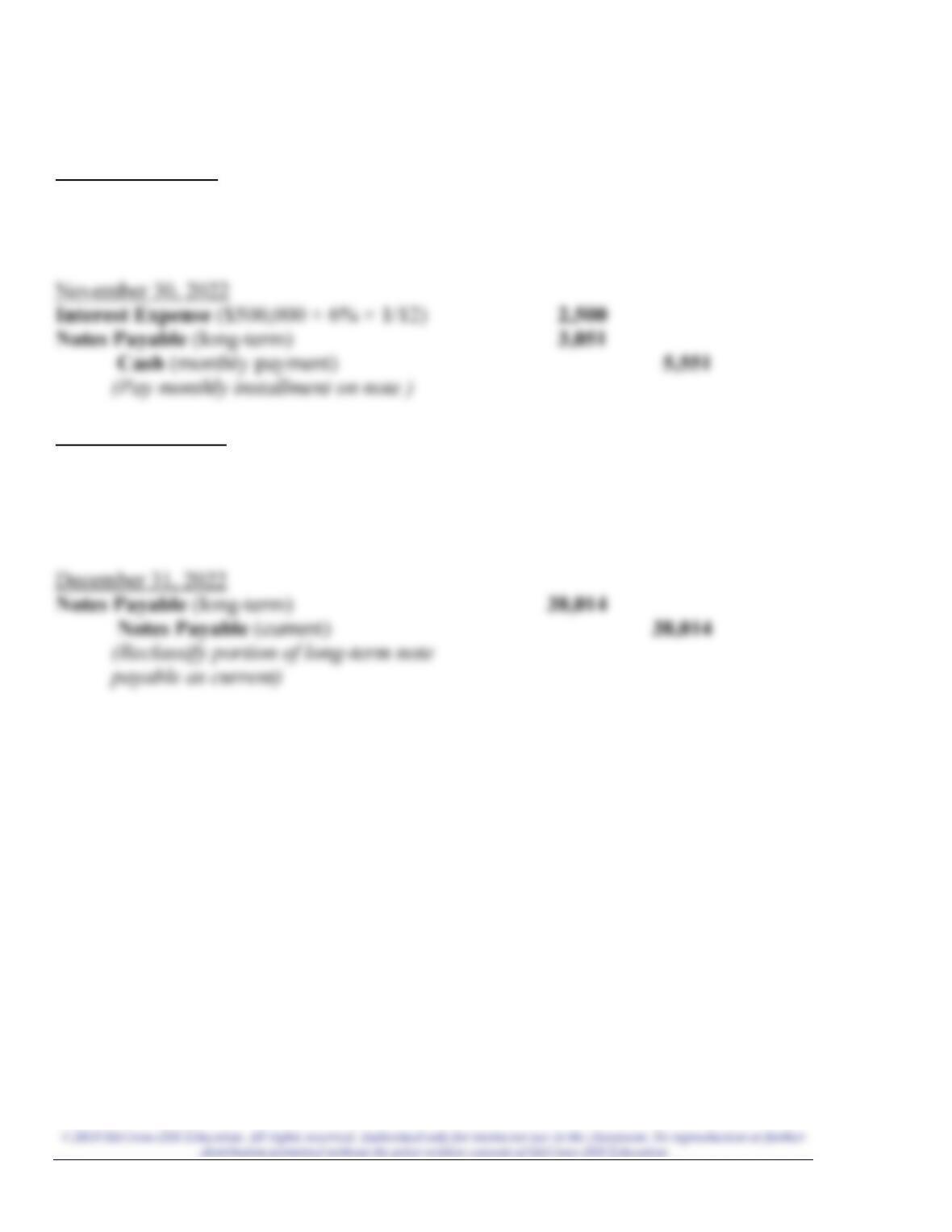

November 30, 2022

Interest Expense ($500,000 × 6% × 1/12)

2,500

Notes Payable (difference)

3,051

5,551

December 31, 2022

Interest Expense ($496,949 × 6% × 1/12)

2,485

Notes Payable (difference)

3,066

Cash (monthly payment)

5,551

Requirement 4

* Portion of note that will be paid within one year of the balance sheet date.

Chapter 9 – Long-Term Liabilities

9-64 Financial Accounting, 5e

Additional Perspective 9-1 (in General Ledger)

Students will be given the following existing trial balance.

Great Adventures, Inc.

Trial Balance

December 31, 2022

(Prior to transactions in AP9-1)

Accounts

Debit

Credit

Cash

$ 89,070

Accounts Receivable

50,000

Allowance for Uncollectible Accounts

$ 2,400

Inventory

Prepaid Insurance

Land

Equipment

62,000

Accumulated Depreciation

25,250

Accounts Payable

Deferred Revenue

Warranty Liability

Contingent Liability

12,000

Income Tax Payable

14,500

Interest Payable

750

Notes Payable (current)

10,000

Notes Payable (long-term)

20,000

Common Stock

20,000

Retained Earnings

33,450

Service Revenue

44,500

Sales Revenue

120,000

Interest Revenue

Sales Discounts

Depreciation Expense

Insurance Expense

Rent Expense

Salaries Expense

24,000

Supplies Expense

Bad Debt Expense

Repairs and Maintenance Expense

Warranty Expense

Chapter 9 – Long-Term Liabilities

Chapter 9 – Long-Term Liabilities

9-66 Financial Accounting, 5e

Additional Perspective 9-1 (in General Ledger, continued)

November 1, 2022

Land

500,000

Notes Payable (long-term)

500,000

(Purchase land by issuing a note payable)

November 30, 2022

Interest Expense ($500,000 × 6% × 1/12)

Notes Payable (long-term)

5,551

December 31, 2022

Interest Expense ($496,949 × 6% × 1/12)

2,485

Notes Payable (long-term)

3,066

Cash (monthly payment)

5,551

(Pay monthly installment on note )

December 31, 2022

Notes Payable (long-term)

Notes Payable (current)

Chapter 9 – Long-Term Liabilities

Additional Perspective 9-1 (in General Ledger, continued)

Great Adventures, Inc.

Income Statement

For the period ended December 31, 2022

Service revenue

$ 44,500

Sales revenue

Sales discounts

Cost of goods sold

38,500

Gross profit

$125,650

Depreciation Expense

17,250

Insurance Expense

5,700

Rent Expense

2,400

Salaries Expense

24,000

Supplies Expense

Bad Debt Expense

Repairs and Maintenance Expense

Warranty Expense

Loss

Operating income (loss)

57,000

Interest revenue

120

Interest expense

(6,785)

Income before income taxes

50,335

Income tax expense

Chapter 9 – Long-Term Liabilities

9-68 Financial Accounting, 5e

Additional Perspective 9-1 (in General Ledger, continued)

Great Adventures, Inc.

Balance Sheet

December 31, 2022

Assets

Liabilities

Current assets:

Current liabilities:

Cash

$ 77,968

Accounts payable

$ 20,800

Accounts receivable

50,000

Deferred Revenue

Allow for Uncoll Accts

Warranty Liability

Inventory

Prepaid Insurance

Income tax payable

Total current assets

Interest payable

Notes Payable (current)

Total liabilities

Long-term assets:

Land

500,000

Stockholders’ Equity

Equipment

62,000

Common stock

20,000

Accumulated depreciation

(25,250)

Retained earnings

69,285

Total stockholders’ equity

89,285

$670,218

Total assets

$670,218

Chapter 9 – Long-Term Liabilities

Additional Perspective 9-1 (in General Ledger, concluded)

Dec. 31, 2022

Debit

Credit

Service Revenue

44,500

Sales Revenue

Dec. 31, 2022

Retained Earnings

128,435

Cost of Goods Sold

38,500

Depreciation Expense

17,250

Insurance Expense

Salaries Expense

24,000

Supplies Expense

Bad Debt Expense

Repairs and Maintenance Expense

Loss

Interest Expense

Chapter 9 – Long-Term Liabilities

9-70 Financial Accounting, 5e

Financial Analysis: American Eagle

AP9-2

($ in thousands)

Requirement 1

Total

Liabilities

÷

Stockholders’

Equity

=

Debt to

Equity Ratio

Requirement 2

Net

Income

÷

Average

Total Assets

=

Return on

Assets

Requirement 3

The bankruptcy risk of American Eagle is low. The company carries very little debt

Chapter 9 – Long-Term Liabilities

Financial Analysis: Buckle

AP9-3

($ in thousands)

Requirement 1

Total

Liabilities

÷

Stockholders’

Equity

=

Debt to

Equity Ratio

$149,308

Requirement 2

Net

Income

÷

Average

Total Assets

=

Return on

Assets

Requirement 3

The bankruptcy risk of The Buckle is low. The company carries no bank borrowings

Chapter 9 – Long-Term Liabilities

9-72 Financial Accounting, 5e

Comparative Analysis: American Eagle vs. Buckle

AP9-4

($ in thousands)

Requirement 1

Total

Liabilities

÷

Stockholders’

Equity

=

Debt to

Equity Ratio

Requirement 2

Net

Income

÷

Average Total

Assets

=

Return on

Assets Ratio

$89,707

Chapter 9 – Long-Term Liabilities

Ethics

AP9-5

1. Current liabilities are understated and long-term liabilities are overstated by

$447,116.

2.

Current

Ratio

Debt to Equity

Ratio

Current Assets/

Current Liabilities

Total Liabilities /

Total Equity

= 1.15

= 1.32

= 0.99

= 1.32

3. Yes.

By misclassifying the current portion of the note as part of long-term liabilities, the

current ratio is overstated. Thus, the company’s ability to pay its debt in the following

4. No.

The portion of the note that is due within one year of the balance sheet date

Chapter 9 – Long-Term Liabilities

9-74 Financial Accounting, 5e

Internet Research

AP9-6

This case provides an opportunity for students to learn more about credit ratings at

Chapter 9 – Long-Term Liabilities

Written Communication

AP9-7

Requirement 1

A company that borrows by issuing bonds is effectively by-passing the bank and

borrowing directly from the investing public, usually at a lower interest rate than it

Requirement 2

One of the primary reasons for issuing bonds over issuing common stock relates to

Requirement 3

The price of a bond is calculated as the present value of the principal (the face amount

Chapter 9 – Long-Term Liabilities

9-76 Financial Accounting, 5e

Earnings Management

AP9-8

Requirement 1

Calculator Input

Bond

Characteristics

Key

Amount

1. Face amount

FV

$100,000,000

2. Interest payment

3. Periods to maturity

4. Market interest rate

PV

$110,465,146

Requirement 2

Calculator Input

Bond

Characteristics

Key

Amount

1. Face amount

FV

$100,000,000

2. Interest payment

3. Periods to maturity

4. Market interest rate

Chapter 9 – Long-Term Liabilities

Requirement 3

Calculator Input

Bond

Characteristics

Key

Amount

1. Face amount

FV

$100,000,000

2. Interest payment

3. Periods to maturity

PV

Requirement 4

December 31, 2021

Bonds Payable

100,000,000

Premium on Bonds Payable

Requirement 5

No.

Investors likely would not agree with David Plesko’s plan. To report the $27 million