CHAPTER 9

Financing Activities

THINKING BEYOND THE QUESTION

What are the fundamental accounting issues associated with financing activities?

Debt increases a company’s financial risk. The debt and interest on the

debt have to be paid by the borrower. If a company fails to make these

QUESTIONS

Q9-1 Liabilities are sometimes liquidated with resources other than cash, but it

is cash that is most often used. Therefore, separation of liabilities into

Q9-2 Debentures are unsecured bonds. This means there is no specific collat-

eral backing for the bonds. Specific assets are not pledged as security.

Instead, bondholders rely on the general credit worthiness of the compa-

234 Chapter 9

Q9-3 The stated rate (nominal rate) is the interest rate that is printed on the

face of the bond. When multiplied by the face value of the bond, it deter-

Q9-4 A capital lease is simply a means of financing the acquisition of assets.

For example, a capital lease has the same economic effects as if a com-

pany borrowed money from a bank and then used that money to pur-

chase a resource outright from a seller. First, in both a purchase and a

Q9-5 A contingency is an existing condition that may result in an economic ef-

fect if a future event occurs. A liability, on the other hand, is an existing

Q9-6 A contingency arises from a possibility that some future event might take

place. Whether the future event will occur or not is uncertain. A commit-

Q9-7 I do not agree. Contributed capital includes only those items of stock-

holders’ equity that resulted from a direct contribution by the owners to

Financing Activities 235

Q9-8 Yes, I agree. Most, but not all, current liabilities arise from operating activ-

(1) Accounts payable generally arise from purchasing inventory on

credit. This is an operating activity because it deals with providing

goods and services to customers. (2) Income taxes payable arise

from providing goods and services to customers profitably. There-

Q9-9 Beach Club Inc. should increase its cash account by $200,000, increase

Q9–10 Most companies report the detailed changes in stockholders’ equity ac-

counts in a financial statement titled Statement of Stockholders’ Equity

Q9–11 The difference is that the purchase and sale of widgets involves an exter-

nal party—a customer. Revenues are generated from selling goods and

Q9–12 The three terms concern the distribution of dividends. The date of decla-

ration is the date that the board of directors announce that a dividend will

be paid. The date of record establishes who will receive the dividend.

236 Chapter 9

Q9–13 Instead of voting rights, the preferred stockholders generally have a divi-

dend preference and a liquidation preference over common stockholders.

That is, if dividends are to be paid in any given period, the preferred divi-

Q9–14 The dividend preference only protects preferred shareholders during the

current period. If preferred stock is not cumulative, a choice by the Board

of Directors to bypass dividends in a given year means the preferred div-

Q9–15 This is the risk-return trade-off at work. Investors are rewarded for taking

on risk. The more risk an investor is willing to accept, the greater are the

potential rewards. If an investor desires to limit risk, the investor automat-

Q9–16 Contributed capital is the term that describes direct stockholder invest-

ments in a corporation. When an investor purchases stock from a corpora-

tion, the funds collected by the corporation are called contributed capital.

Common stock is that category of stock that controls the corporation

Financing Activities 237

have voting rights.

EXERCISES

E9-1 Definitions of all terms are listed in the glossary.

0.64993 (5 periods, 9%)

PV of bonds = $311,172 + $649,930

0.78353 (5 periods, 5%)

E9-3 a. The bonds sold at a discount. Buyers paid less than the face value of

the bonds so they could earn a higher return on the bonds than the

stated rate. Therefore, interest expense recognized by the issuer

238 Chapter 9

E9-4 a. $746,320 Interest expense would be the effective rate times the

present value of the bonds at the beginning of the 2008

fiscal year: 0.08 × $9,329,000 = $746,320.

b. $9,375,320 The net liability is the present value of the bonds on

E9-5 a. Income statement: The income statement would report a gain on ex-

tinguishment of debt of $11,400 ($186,400 − $175,000). This would

raise net income by the same amount (ignoring taxes).

E9-6

ASSETS

=

LIABILITIES

+

OWNERS’ EQUITY

Date

Accounts

Cash

Other

Assets

Contributed

Capital

Retained

Earnings

a.

Cash

360,728

Bonds Payable

360,728

Cash

Interest Expense

Bonds Payable

c.

Cash

Financing Activities 239

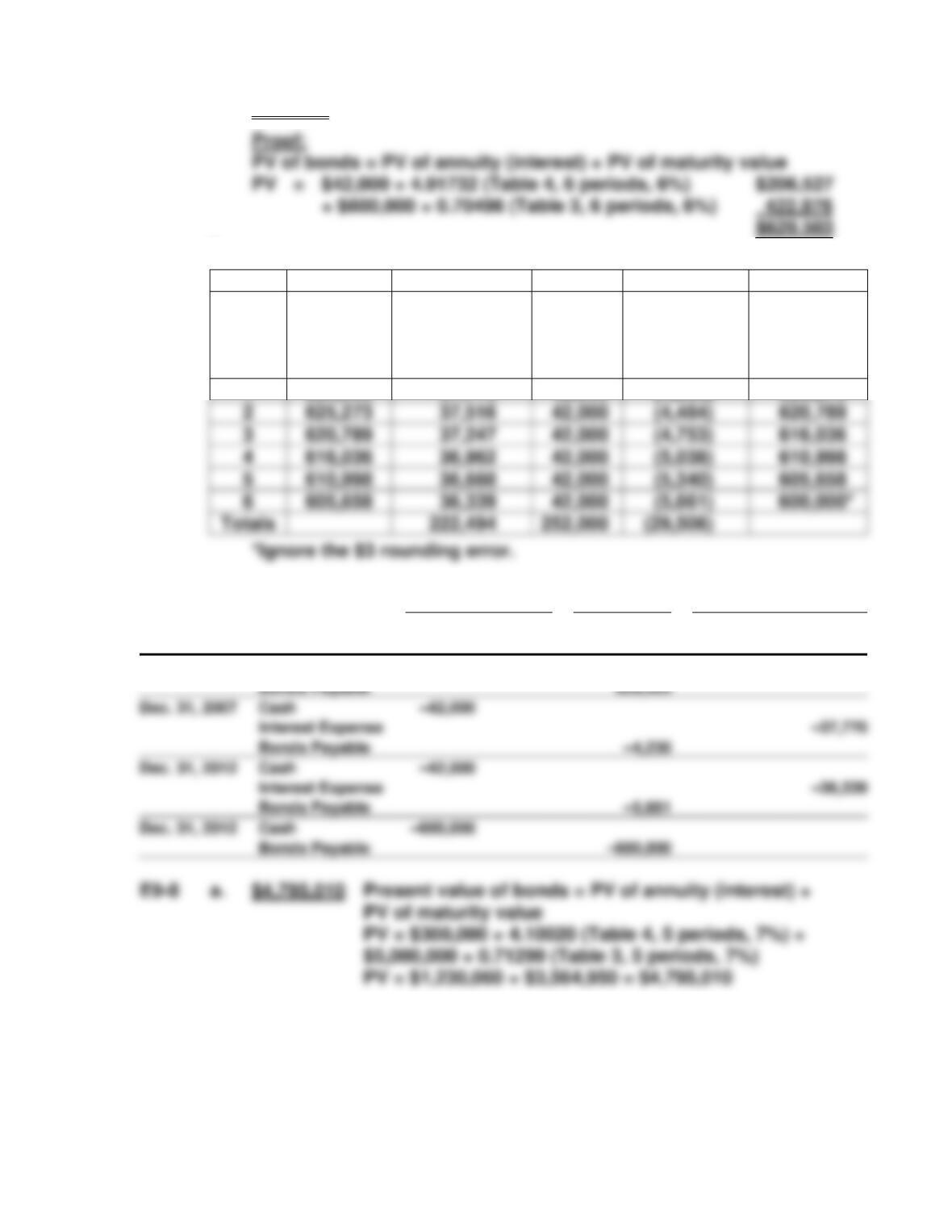

E9-7 a. $629,503

b.

A

B

C

D

E

F

Year

PV at

Beginning

of Year

Interest

Incurred

(Column B ×

Interest Rate)

Amount

Paid

Amortization

of Principal

(Column C –

Column D)

Value at End

of Year

(Column B +

Column E)

1

629,503

37,770

42,000

(4,230)

625,273

2

625,273

37,516

42,000

(4,484)

620,789

3

620,789

37,247

42,000

(4,753)

616,036

4

616,036

36,962

42,000

(5,038)

610,998

5

610,998

36,660

(5,340)

605,658

6

605,658

36,339

42,000

(5,661)

600,000*

c.

ASSETS

=

LIABILITIES

+

OWNERS’ EQUITY

Date

Accounts

Cash

Other

Assets

Contributed

Capital

Retained

Earnings

Jan. 1, 2007

Cash

629,503

Bonds Payable

629,503

Dec. 31, 2007

Cash

Interest Expense

Bonds Payable

Dec. 31, 2012

Cash

Interest Expense

Bonds Payable

Dec. 31, 2012

Cash

Bonds Payable

The bonds sold for an amount less than the face amount; i.e., at a dis-

count. This occurred because the bonds will pay interest at a lesser rate

than the market rate.

(continued)

240 Chapter 9

The bonds sold for an amount greater than the face amount; i.e., at a

premium. This occurred because the bonds will pay interest at a greater

rate than the market rate.

$1,283,506 For the bonds in part (b), those sold at a premium, the

interest expense over the five-year period would be the

E9-9 This exercise requires students to determine the present value of lease

payments and to separate the first lease payment into its interest compo-

nent and its reduction of liability component. Entries are required (a) at

the beginning of the lease and (b) at the date of the first lease payment.

ASSETS

=

LIABILITIES

+

OWNERS’ EQUITY

Accounts

Cash

Other

Assets

Contributed

Capital

Retained

Earnings

Diagnostic Equipment

Capital Lease Obligation

Financing Activities 241

ASSETS

=

LIABILITIES

+

OWNERS’ EQUITY

Accounts

Cash

Other

Assets

Contributed

Capital

Retained

Earnings

E9–10 a. Liability; Notes Payable; current

E9–11 1. f 5. g 9. n 13. d

E9–12 a. A charter is the legal document granted by a state government that

d. 79,000 Outstanding shares is the number of shares held by

stockholders. In this case, 80,000 were initially sold, but

1,000 have been reacquired.

Cash

Capital Lease Obligation

Interest Expense

242 Chapter 9

E9–13 a. 1 million Authorized shares is the number permitted by the com-

pany’s charter.

E9–14

Quick Chips Company

Stockholders’ Equity

Stockholders’ Equity: 2009 2008

Common stock, $0.25 par value,

600,000 shares authorized,

E9–15 a. Date of declaration: January 27

c. There are only two choices that a board of directors can make re-

garding profits. It can pay them out as dividends, or it can retain

profits for reinvestment in the company (hence the term retained

Financing Activities 243

E9–16 a. Cash dividend: There is no effect on the income statement (divi-

b. Stock dividend: There is no effect on the income statement. On the

balance sheet, Retained Earnings decreases by $21,000 and Contrib-

c. Stock split: There is no effect on the income statement. The only

f. Cash flow: Paid for dividends $(335,000)

Purchases of stock (220,000)

create net income.

E9–18 a. The increase in Retained Earnings was caused by the transfer of net

income to Retained Earnings when the revenue and expense ac-

counts were closed.

244 Chapter 9

E9–19

Year

Total

Dividends Paid

Dividends

to Preferred

Dividends

to Common

Unpaid Dividends

to Preferred

2007

$50,000

$28,000a

$22,000b

$ 0

2008

2010

0

E9–20 1. r 5. g 9. l 13. q 17. e

E9–21 a. 50,000 $2,500,000 preferred stock balance ÷ $50 par value per

share

Financing Activities 245

PROBLEMS

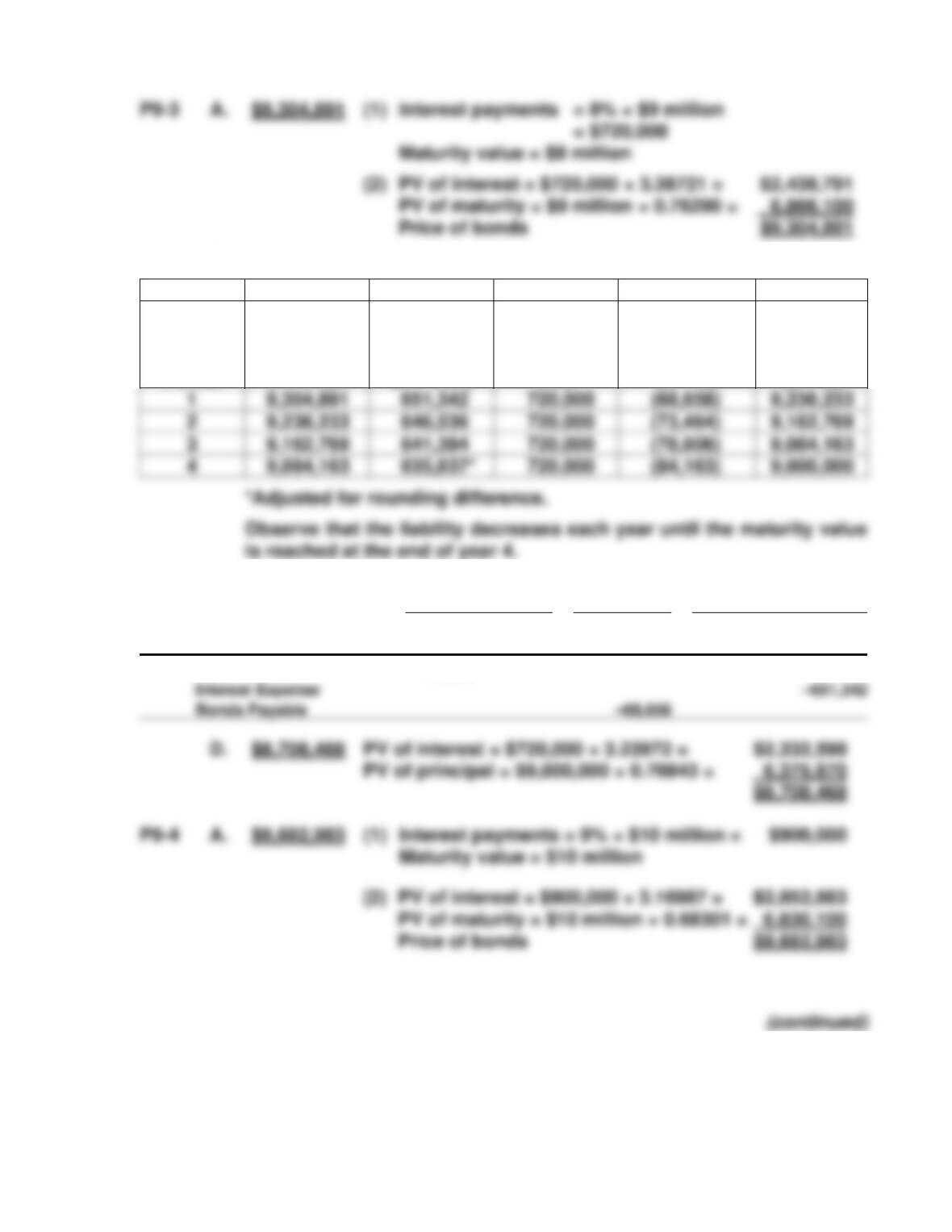

D. 9% The amount of interest incurred in any year divided by

its corresponding “beginning–of–year present value.” In

G. The total interest incurred, $175,560, is the total amount paid to cred-

itors for the use of their funds over the five years. That total amount

is paid out in pieces. First, an interest check is sent to creditors at

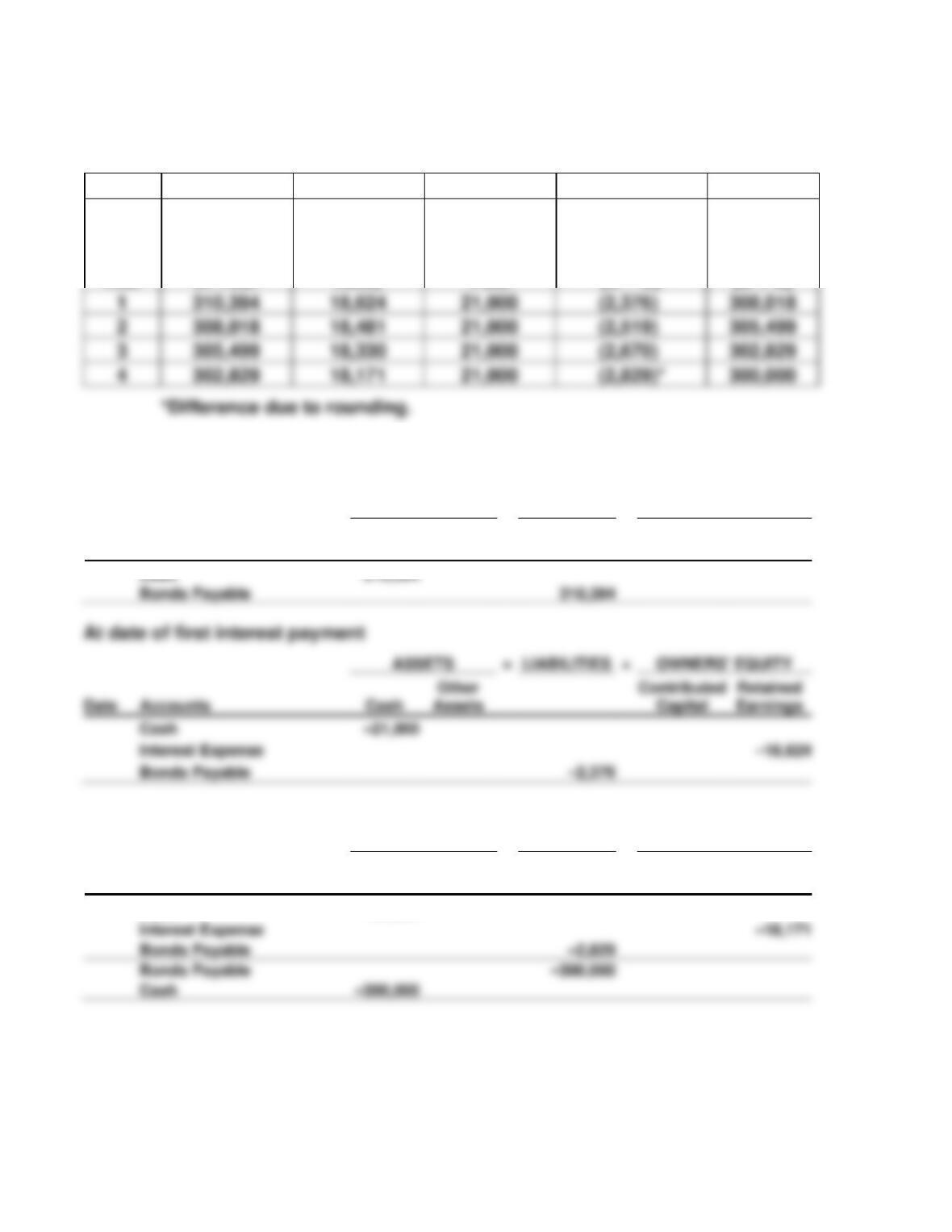

P9-2 A. 7% The bonds sold at a price of $310,394. This is a price above

face value, so the stated rate is greater than the 6% effective

rate.

To determine the stated rate:

246 Chapter 9

B. An amortization table was not part of the requirements but is helpful

to answer part B.

A

B

C

D

E

F

Year

Present

Value at

Beginning

of Year

Interest

Incurred

(B × Interest

Rate)

Amount

Paid

Amortization

of Principal

(C − D)

Value

at End of

the Year

(B + E)

The necessary entries to the accounting system are as follows:

At date of issuance

ASSETS

=

LIABILITIES

+

OWNERS’ EQUITY

Date

Accounts

Cash

Other

Assets

Contributed

Capital

Retained

Earnings

Cash

310,394

Bonds Payable

ASSETS

=

LIABILITIES

+

OWNERS’ EQUITY

Date

Accounts

Cash

Other

Assets

Contributed

Capital

Retained

Earnings

At date of last interest payment

ASSETS

=

LIABILITIES

+

OWNERS’ EQUITY

Date

Accounts

Cash

Other

Assets

Contributed

Capital

Retained

Earnings

Cash

–21,000

Interest Expense

Bonds Payable

Bonds Payable

Cash

(2,376)

(2,519)

(2,670)

Financing Activities 247

B.

A

B

C

D

E

F

Period

Present

Value at

Beginning

of Period

Effective

Interest

(B × 0.07)

Interest

Payment @

0.08

Amortization

of Principal

(C – D)

Value

At End of

Period

(B + E)

C.

ASSETS

=

LIABILITIES

+

OWNERS’ EQUITY

Date

Accounts

Cash

Other

Assets

Contributed

Capital

Retained

Earnings

Cash

–720,000

Interest Expense

Bonds Payable

248 Chapter 9

B. The amortization schedule would show the following:

A

B

C

D

E

F

Period

Present

Value at

Beginning

of Period

Effective

Interest

(B × 0.10)

Interest

Payment

@ 0.09

Amortization

of Principal

(C − D)

Value

at End of

Period

(B + E)

1

9,682,983

968,298

900,000

68,298

9,751,281

C.

ASSETS

=

LIABILITIES

+

OWNERS’ EQUITY

Date

Accounts

Cash

Other

Assets

Contributed

Capital

Retained

Earnings

P9-5 The price of a 10-year bond paying 8% interest, with semiannual pay-

ments, and yielding a 6% market rate would be $1,149 [($40 × 14.87747) +

2

9,751,281

975,128

900,000

75,128

9,826,409

3

9,826,409

982,641

900,000

82,641

9,909,050

4

9,909,050

990,950*

900,000

90,950

Financing Activities 249

P9-6 A. Option #1 annual payment is $14,761

B.

Total Cash

Outflow

Total Interest

Expense

C. The firm would pay more under option 2 because no principal is re-

paid until the end of the four years. Hence, the entire balance is out-

each year.

D. The better choice would depend on the firm’s cash position. If there

P9-7 A. Dealer A: Because the present value of an annuity is known

250 Chapter 9

B. Dealer A Dealer B

C. Total of payments $2,717,360 $ 2,682,530

D. If the company will finance the equipment, it should accept Dealer

E. A cash outflow will appear in the financing section each year for 10

B.

A

B

C

D

E

F

Year

Present

Value at

Beginning

of Year

Interest

Incurred

(B × Interest

Rate)

Amount

Paid

Amortization

of Principal

(C − D)

Value

at End of

the Year

(B + E)

(8,711)

(9,495)

C. The lease transaction is being used as a method of financing acqui-

sition of the asset. Therefore, every lease payment is part interest