Chapter 9 – Long-Term Liabilities

Exercise 9-9 (LO 9-5)

Requirement 1

(1)

Date

(2)

Cash

Paid

(3)

Interest

Expense

(4)

Decrease in

Carrying

Value

(5)

Carrying

Value

Face Amount

x 4.5% Stated

Rate

Carrying Value

x 4% Market

Rate

(2) – (3)

Prior Carrying

Value – (4)

548,419

Requirement 2

January 1, 2021

Cash

549,482

Bonds Payable

500,000

June 30, 2021

Interest Expense

21,979

December 31, 2021

Interest Expense

21,958

Chapter 9 – Long-Term Liabilities

Exercise 9-10 (LO 9-5)

January 1, 2021

Cash

600,000

Bonds Payable

600,000

(Issue bonds at face amount)

June 30, 2021

Interest Expense

(Pay semiannual interest)

December 31, 2021

Interest Expense

(Pay semiannual interest)

Chapter 9 – Long-Term Liabilities

Exercise 9-11 (LO 9-5)

Requirement 1

(1)

Date

(2)

Cash

Paid

(3)

Interest

Expense

(4)

Increase in

Carrying

Value

(5)

Carrying

Value

Face Amount

x 3.5% Stated

Rate

Carrying Value

x 4% Market

Rate

(3) – (2)

Prior Carrying

Value + (4)

562,022

Requirement 2

January 1, 2021

Cash

559,229

Discount on Bonds Payable

40,771

June 30, 2021

Interest Expense

22,369

December 31, 2021

Interest Expense

22,424

Chapter 9 – Long-Term Liabilities

9-24 Financial Accounting, 5e

Exercise 9-12 (LO 9-5)

Requirement 1

(1)

Date

(2)

Cash

Paid

(3)

Interest

Expense

(4)

Decrease in

Carrying

Value

(5)

Carrying

Value

Face Amount

Carrying Value

Prior Carrying

Requirement 2

January 1, 2021

Cash

644,632

Bonds Payable

600,000

Premium on Bonds Payable

44,632

(Issue bonds at a premium)

June 30, 2021

Interest Expense

(Pay semi-annual interest)

December 31, 2021

(Pay semi-annual interest)

Chapter 9 – Long-Term Liabilities

Exercise 9-13 (LO 9-5)

January 1, 2021

Cash

600,000

Bonds Payable

600,000

(Issue bonds at face amount)

Interest Expense

(Pay annual interest)

Interest Expense

(Pay annual interest)

Chapter 9 – Long-Term Liabilities

9-26 Financial Accounting, 5e

Exercise 9-14 (LO 9-5)

Requirement 1

(1)

Date

(2)

Cash

Paid

(3)

Interest

Expense

(4)

Increase in

Carrying

Value

(5)

Carrying

Value

Requirement 2

January 1, 2021

Cash

559,740

Discount on Bonds Payable

40,260

Bonds Payable

600,000

(Issue bonds at a discount)

December 31, 2021

Interest Expense

44,779

(Pay annual interest)

December 31, 2022

(Pay annual interest)

Chapter 9 – Long-Term Liabilities

Exercise 9-15 (LO 9-5)

Requirement 1

(1)

Date

(2)

Cash

Paid

(3)

Interest

Expense

(4)

Decrease in

Carrying

Value

(5)

Carrying

Value

Face Amount

Carrying Value

Prior Carrying

Requirement 2

January 1, 2021

Cash

644,161

Bonds Payable

600,000

Premium on Bonds Payable

44,161

(Issue bonds at a premium)

December 31, 2021

Interest Expense

(Pay annual interest)

December 31, 2022

(Pay annual interest)

9-28 Financial Accounting, 5e

Exercise 9-16 (LO 9-6)

Requirement 1

(1)

Date

(2)

Cash

Paid

(3)

Interest

Expense

(4)

Increase in

Carrying

Value

(5)

Carrying

Value

Face Amount

Carrying Value

Prior Carrying

Requirement 2

If the market rate drops to 7%, it will cost $601,452 to retire the bonds.

Calculator Input

Bond

characteristics

Key

Amount

1. Face amount

FV

2. Interest payment each period

3. Periods to maturity

4. Market interest rate each period

Calculator Output

Issue price

PV

$601,452

December 31, 2022

Chapter 9 – Long-Term Liabilities

Exercise 9-17 (LO 9-6)

Requirement 1

(1)

Date

(2)

Cash

Paid

(3)

Interest

Expense

(4)

Decrease in

Carrying

Value

(5)

Carrying

Value

Face Amount

Carrying Value

Prior Carrying

Requirement 2

If the market rate increases to 8%, it will cost $568,311 to retire the bonds.

Calculator Input

Bond

Characteristics

Key

Amount

1. Face amount

FV

$600,000

2. Interest payment each period

3. Periods to maturity

4. Market interest rate each period

Calculator Output

Issue price

PV

$568,311

December 31, 2023

Bonds Payable

600,000

Chapter 9 – Long-Term Liabilities

9-30 Financial Accounting, 5e

Exercise 9-18 (LO 9-7)

Requirement 1

Premium. The issue price is $45,057,519

Calculator Input

Bond

Characteristics

Key

Amount

1. Face amount

FV

$41,000,000

2. Interest payment

3. Periods to maturity

Calculator Output

Issue price

PV

$45,057,519

Requirement 2

Face amount. The issue price is $41,000,000.

Calculator Input

Bond

Characteristics

Key

Amount

1. Face amount

FV

$41,000,000

2. Interest payment

3. Periods to maturity

4. Market interest rate

Calculator Output

Issue price

PV

$41,000,000

Chapter 9 – Long-Term Liabilities

Requirement 3

Discount. The issue price is $37,482,387

Calculator Input

Bond

Characteristics

Key

Amount

1. Face amount

FV

$41,000,000

2. Interest payment

3. Periods to maturity

4. Market interest rate

PV

Chapter 9 – Long-Term Liabilities

9-32 Financial Accounting, 5e

Exercise 9-19 (LO 9-7)

Requirement 1

Premium. The issue price is $27,934,072.

Calculator Input

Bond

Characteristics

Key

Amount

1. Face amount

FV

$26,000,000

2. Interest payment

3. Periods to maturity

Calculator Output

PV

Requirement 2

Face amount. The issue price is $26,000,000.

Calculator Input

Bond

Characteristics

Key

Amount

1. Face amount

FV

$26,000,000

2. Interest payment

3. Periods to maturity

4. Market interest rate

Calculator Output

PV

Chapter 9 – Long-Term Liabilities

Requirement 3

Discount. The issue price is $24,233,258.

Calculator Input

Bond

Characteristics

Key

Amount

1. Face amount

FV

$26,000,000

2. Interest payment

3. Periods to maturity

4. Market interest rate

PV

Chapter 9 – Long-Term Liabilities

Exercise 9-20 (LO 9-8)

Requirement 1

Total

Liabilities

÷

Stockholders’

Equity

=

Debt to Equity

Ratio

E-Travel

÷

=

Pricecheck

÷

=

Requirement 2

Net Income +

Interest + Taxes

÷

Interest

=

Times Interest

Earned Ratio

E-Travel

$588,159

÷

$94,233

=

6.2

Pricecheck

$600,724

÷

$34,084

=

Chapter 9 – Long-Term Liabilities

Exercise 9-21 (LO 9-2, LO 9-8)

Requirement 1

January 1

Debit

Credit

Cash

100,000

Notes Payable (Long-term)

100,000

(Issue a long-term note payable)

January 4

Debit

Credit

Cash

31,000

Accounts Receivable

31,000

(Receive cash on account)

January 11

Debit

Credit

Accounts Payable

11,000

(Pay cash on account)

January 15

Debit

Credit

Salaries Expense

28,900

Cash

28,900

(Pay for salaries)

January 30

Debit

Credit

Cash

65,000

130,000

Accounts Receivable

Sales Revenue

(Sell inventory for cash and on account)

Cost of Goods Sold

112,500

Inventory

(Record cost of inventory sold)

January 31

Debit

Credit

Interest Expense

Notes Payable (Long-term)

Cash

($583 = $100,000 × 7% × 1/12)

Chapter 9 – Long-Term Liabilities

9-36 Financial Accounting, 5e

Exercise 9-21 (continued)

Requirement 2

(a) January 31

Debit

Credit

Depreciation Expense

800

Accumulated Depreciation

800

(Record depreciation for January)

($800 = [$120,000−$24,000] / 120 months)

(b) January 31

Debit

Credit

Bad Debt Expense

Allowance for Uncollectible Accounts

(c) January 31

Debit

Credit

Salaries Expense

26,100

Salaries Payable

26,100

(Adjust salaries payable)

(d) January 31

Debit

Credit

Income Tax Expense

Income Tax Payable

(Adjust income taxes)

Notes Payable (Long-term)

17,411

Notes Payable (Current)

17,411

(Reclassify current portion of note payable)

Chapter 9 – Long-Term Liabilities

Exercise 9-21 (continued)

Requirement 3

Freedom Fireworks

Adjusted Trial Balance

January 31, 2021

Accounts

Debit

Credit

Cash

$165,320

Accounts Receivable

133,000

Allowance for Uncollectible Accounts

$ 4,100

Inventory

39,500

Land

67,300

Buildings

120,000

Accumulated Depreciation

10,400

Accounts Payable

Salaries Payable

26,100

Income Tax Payable

Notes Payable (Current)

17,411

Notes Payable (Long-term)

81,192

Common Stock

200,000

Retained Earnings

155,400

Sales Revenue

195,000

Cost of Goods Sold

112,500

Salaries Expense

55,000

Bad Debt Expense

Depreciation Expense

Interest Expense

Income Tax Expense

$704,303

$704,303

Chapter 9 – Long-Term Liabilities

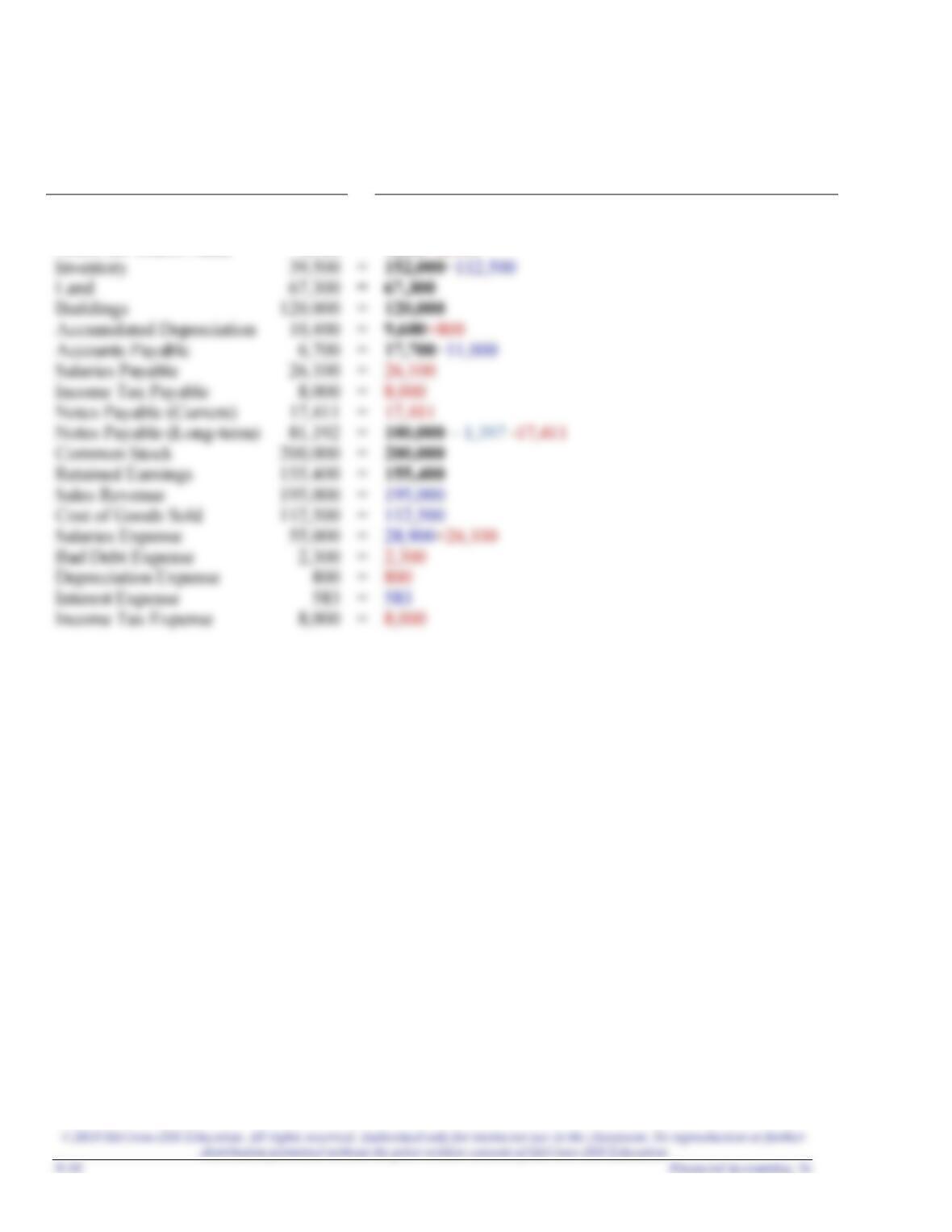

Exercise 9-21 (continued)

Requirement 3 (continued)

Accounts

Ending

Balance

Beginning balance in bold, entries during January in blue,

and adjusting entries in red.

Cash

$165,320

=

11,200+100,000+31,000−11,000−28,900+65,000−1,980

Accounts Receivable

133,000

=

34,000−31,000+130,000

Allow for Uncoll Accts

4,100

=

1,800+2,300

Inventory

=

152,000−112,500

Land

=

67,300

Buildings

120,000

=

Accumulated Depreciation

=

9,600+800

Accounts Payable

6,700

=

17,700−11,000

Salaries Payable

=

Income Tax Payable

8,000

=

Notes Payable (Current)

=

Notes Payable (Long-term)

=

100,000 – 1,397 -17,411

Common Stock

200,000

=

Retained Earnings

155,400

=

Sales Revenue

195,000

=

Cost of Goods Sold

112,500

=

Salaries Expense

=

Bad Debt Expense

2,300

=

Depreciation Expense

=

Interest Expense

=

Income Tax Expense

8,000

=

Chapter 9 – Long-Term Liabilities

Exercise 9-21 (continued)

Requirement 4

Freedom Fireworks

Multiple-Step Income Statement

For the year month ended January 31, 2021

Sales revenue

$195,000

Cost of goods sold

112,500

Gross profit

$ 82,500

Bad debt expense

Depreciation expense

Total operating expenses

Interest expense

Income tax expense

Requirement 5

Freedom Fireworks

Classified Balance Sheet

January 31, 2021

Assets

Liabilities

Cash

$165,320

Accounts payable

$ 6,700

Accounts receivable

133,000

Salaries payable

26,100

Less: Allowance

Income tax payable

Inventory

Notes payable (Current)

17,411

Total current liabilities

58,211

Notes payable (Long-term)

81,192

Total liabilities

Land

Buildings

Common stock

Less: Accumulated Depreciation

Retained earnings

*

Total assets

$510,620

$510,620

Chapter 9 – Long-Term Liabilities

9-40 Financial Accounting, 5e

Exercise 9-21 (concluded)

Requirement 6

January 31, 2021

Debit

Credit

Sales Revenue

195,000

Retained Earnings

195,000

(Close revenue accounts)

Retained Earnings

179,183

Cost of Goods Sold

112,500

Salaries Expense

Bad Debt Expense

Depreciation Expense

Interest Expense

Income Tax Expense

(Close expense accounts)

Requirement 7

(a) The debt to equity ratio is:

$139,403

$371,217

(b) The times interest earned ratio is:

(c) Based on the debt to equity ratio and the times interest earned ratio, ratio, Freedom Fireworks