255

CHAPTER 9

FINANCIAL STATEMENT ANALYSIS

CLASS DISCUSSION QUESTIONS

1. Horizontal analysis is the percentage analy-

sis of increases and decreases in compara-

tive financial statements. Each item on the

most recent statement is compared with the

related item on one or more earlier state-

ments in terms of the following:

a. Amount of increase or decrease.

2. Comparative statements provide information

as to changes between dates or periods.

Trends indicated by comparisons may be far

more significant than the data for a single

date or period.

3. Before this question can be answered, the

increase in net income should be compared

4. You should first determine if the expense

amount in the base year (denominator) is

significant. A 70% or more increase of a

very small expense item may be of little

concern. However, if the expense amount in

the base year is significant, then over a 70%

increase may require further investigation.

5. Generally, the two ratios would be very

capital, gives a better analysis of the current

position. Such a comparison shows:

Current Preceding

Year Year

Working capital ……. $162,000 $138,000

Current ratio ……….. 2.8 3.3

Walmart. Such sales are “on account,” and

thus create accounts receivable that must

be collected. A recent financial statement

showed Walmart’s accounts receivable turn-

ing 64 times, while Procter & Gamble’s

turned only 6 times.

8. No, an accounts receivable turnover of 9

with sales on an n/30 basis is not satisfacto-

collectibility on the books.

9. a. A high inventory turnover minimizes the

amount invested in inventories, thus

freeing funds for more advantageous

use. Storage costs, administrative ex-

penses, and losses caused by obsoles-

cence and adverse changes in prices

c. No. The inventory turnover ratio and the

number of days’ sales in inventory ratio

are interrelated. Both ratios are comput-

ed using the average inventory [(Begin-

ning Inventory + Ending Inventory) ÷ 2]

and the cost of goods sold. Specifically,

365 days divided by the inventory turn-

over ratio equals the number of days’

sales in inventory.

10. The ratio of fixed assets to long-term liabilities

increased from 3.6 ($1,260,000 ÷ $350,000)

11. a. The rate earned on total assets adds

interest expense to the net income,

holders’ investment.

b. The rate earned on stockholders’ equity

is normally higher than the rate earned

on total assets. This is because of lev-

erage, which compensates stockholders

for the higher risk of their investments.

12. a. Due to leverage, the rate on stockhold-

ers’ equity will often be greater than

b. Higher. The concept of leverage applies

to preferred stock as well as debt. The

rate earned on common stockholders’

equity ordinarily exceeds the rate

earned on total stockholders’ equity

because the amount earned on assets

acquired through the use of funds pro-

vided by preferred stockholders normal-

ly exceeds the dividends paid to pre-

ferred stockholders.

13. The earnings per share in the preceding

14. A share of common stock is currently selling

15. The dividend yield on common stock is a

measure of the rate of return to common

stockholders in terms of cash dividend dis-

16. During periods when sales are increasing, it

is likely that a company will increase its

inventories and expand its plant. Such situa-

tions frequently result in an increase in

current liabilities out of proportion to the

increase in current assets and thus lower

the current ratio.

17. One report is the Report on Internal Control,

which verifies management’s conclusions on

257

EXERCISES

E9–1

a.

SEARLE TECHNOLOGIES CO.

Comparative Income Statement

For the Years Ended December 31, 20Y8 and 20Y7

20Y8 20Y7

Amount Percent Amount Percent

Sales …………………………………….. $ 900,000 100.0% $ 725,000 100.0%

Cost of goods sold ………………… 558,000 62.0 435,000 60.0

Gross profit …………………………... $ 342,000 38.0% $ 290,000 40.0%

b. The vertical analysis indicates that the cost of goods sold as a percent of sales

increased by 2 percentage points (62.0% – 60.0%), while selling expenses de-

E9–2

a.

SPEEDWAY MOTORSPORTS, INC.

Comparative Income Statement (in thousands of dollars)

Year 2 Year 1

Revenues:

Admissions ………………………………. $130,239 25.7% $139,125 27.7%

Event-related revenue ……………….. 163,621 32.3 156,691 31.2

NASCAR broadcasting revenue …. 185,394 36.7 178,722 35.6

Other operating revenue ……………. 26,591 5.3 27,705 5.5

Total revenue ……………………….. $505,845 100.0% $502,243 100.0%

b. Overall revenue remained approximately the same for Years 1 and 2. However,

the total expenses as a percent of total revenue increased by 10.7% (96.5% –

85.8%), which resulted in income from continuing operations before taxes as a

percent of revenue decreasing by 10.7% (14.2% – 3.5%). The largest increase in

expenses occurred in other expenses. The notes to the financial statements in-

E9–3

a.

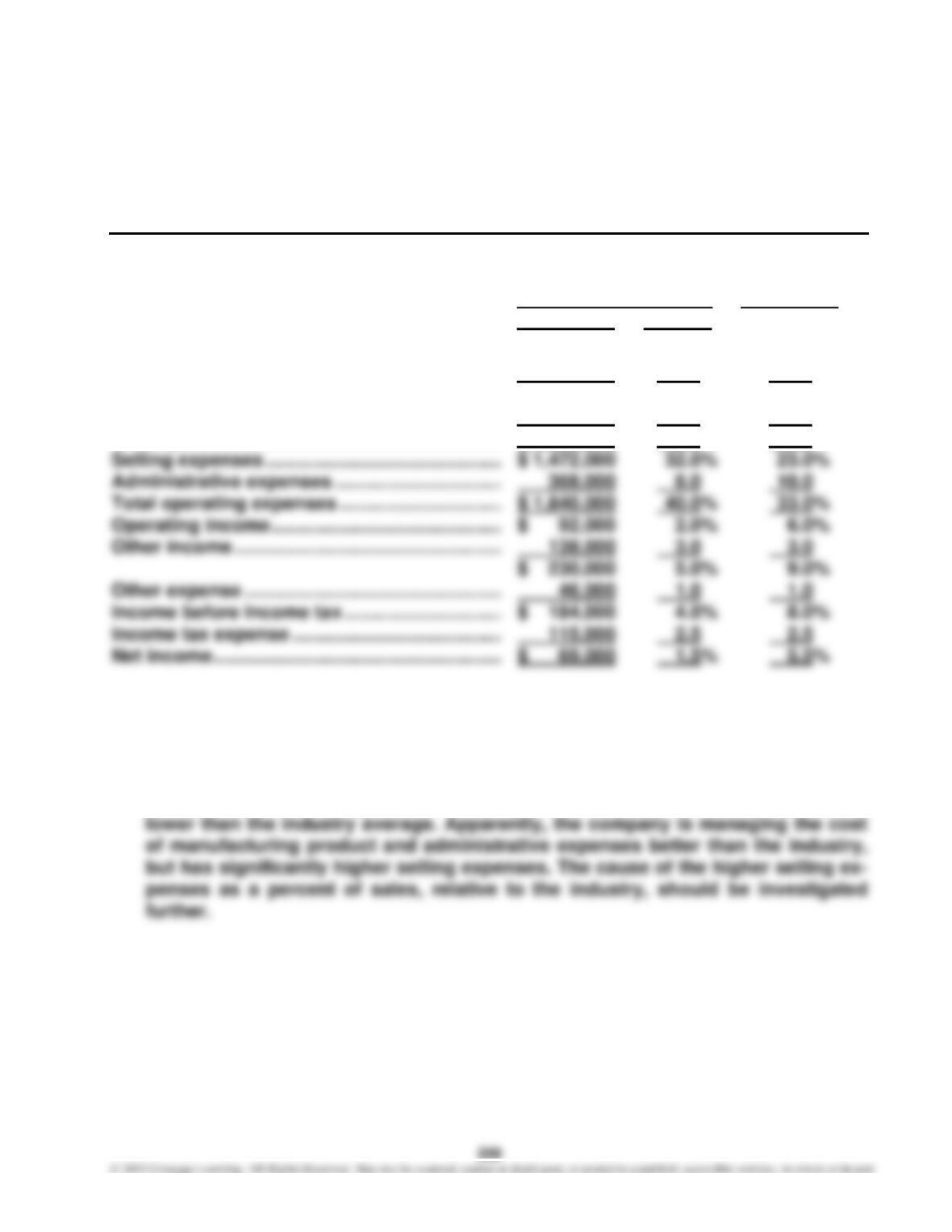

GARRITY ELECTRONICS COMPANY

Common-Sized Income Statement

Garrity Electronics

Electronics Industry

Company Average

Amount Percent

Sales ……………………………………………………….. $ 4,728,800 102.8% 102.5%

Sales returns and allowances …………………… 128,800 2.8 2.5

Net sales …………………………………………………. $ 4,600,000 100.0% 100.0%

Cost of goods sold …………………………………… 2,668,000 58.0 61.0

Gross profit ……………………………………………… $ 1,932,000 42.0% 39.0%

b. The cost of goods sold is 3 percentage points (61.0% – 58.0%) lower than the

industry average, but the selling expenses are 9 percentage points (32.0% –

23.0%) higher than the industry average. Administrative expenses are 2 percent-

age points (10.0% – 8.0%) lower than the industry average. The combined impact

is for net income as a percent of sales to be 4 percentage points (5.5% – 1.5%)

260

E9–4

OTTER CREEK COMPANY

Comparative Balance Sheet

December 31, 20Y2 and 20Y1

20Y2 20Y1

Amount Percent Amount Percent

Current assets ……………………….. $ 700,000 40% $ 504,000 36%

Property, plant, and equipment 945,000 54 770,000 55

Intangible assets ……………………. 105,000 6 126,000 9

E9–5

a. MONTANA IMAGES COMPANY

Comparative Income Statement

For the Years Ended December 31, 20Y5 and 20Y4

20Y5 20Y4 Increase (Decrease)

Amount Amount Amount Percent

Sales …………………………………….. $ 579,000 $ 500,000 $ 79,000 15.8%

Cost of goods sold ………………… 343,500 300,000 43,500 14.5

Gross profit …………………………... $ 235,500 $ 200,000 $ 35,500 17.8

E9–6

a. (1) Working Capital = Current Assets – Current Liabilities

20Y9: $700,000 = $1,200,000 – $500,000

20Y8: $480,000 = $880,000 – $400,000

b. The liquidity of Tiger Shapes has improved from the preceding year to the cur-

rent year. The working capital, current ratio, and quick ratio have all increased.

Most of these changes are the result of an increase in current assets.

E9–7

a. (1) Current Ratio =

sLiabilitieCurrent

setsCurrent As

b. The liquidity of PepsiCo has decreased some over this time period. Both the cur-

rent and quick ratios have decreased. The current ratio decreased from 1.1 to

1.0, and the quick ratio decreased from 0.8 to 0.6. Despite these decreases, how-

262

E9–8

a. The working capital, current ratio, and quick ratio are calculated incorrectly. The

working capital and current ratio incorrectly include intangible assets and prop-

erty, plant, and equipment as a part of current assets. Both are noncurrent. The

quick ratio has an incorrect denominator in that it does not include accrued

liabilities. The denominator of the quick ratio should be total current liabilities.

b. Unfortunately, the working capital, current ratio, and quick ratio are all below the

minimum threshold required by the bond indenture. This may require the com-

263

E9–9

a. (1) Accounts Receivable Turnover =

Accounton SalesNet

(2) Number of Days’ Sales in Receivables =

Accounton Sales Daily Average

Receivable AccountsAverage

Year 3:

2

1

$11,573

$320,000

= 27.7 days

Year 2:

4

3

$9,468

$270,000

= 28.5 days

b. The collection of accounts receivable has improved. This can be seen in both the

increase in accounts receivable turnover from 12.8 to 13.2 and the reduction in

the collection period from 28.5 days to 27.7 days. The credit terms require pay–

ment in 30 days.

E9–10

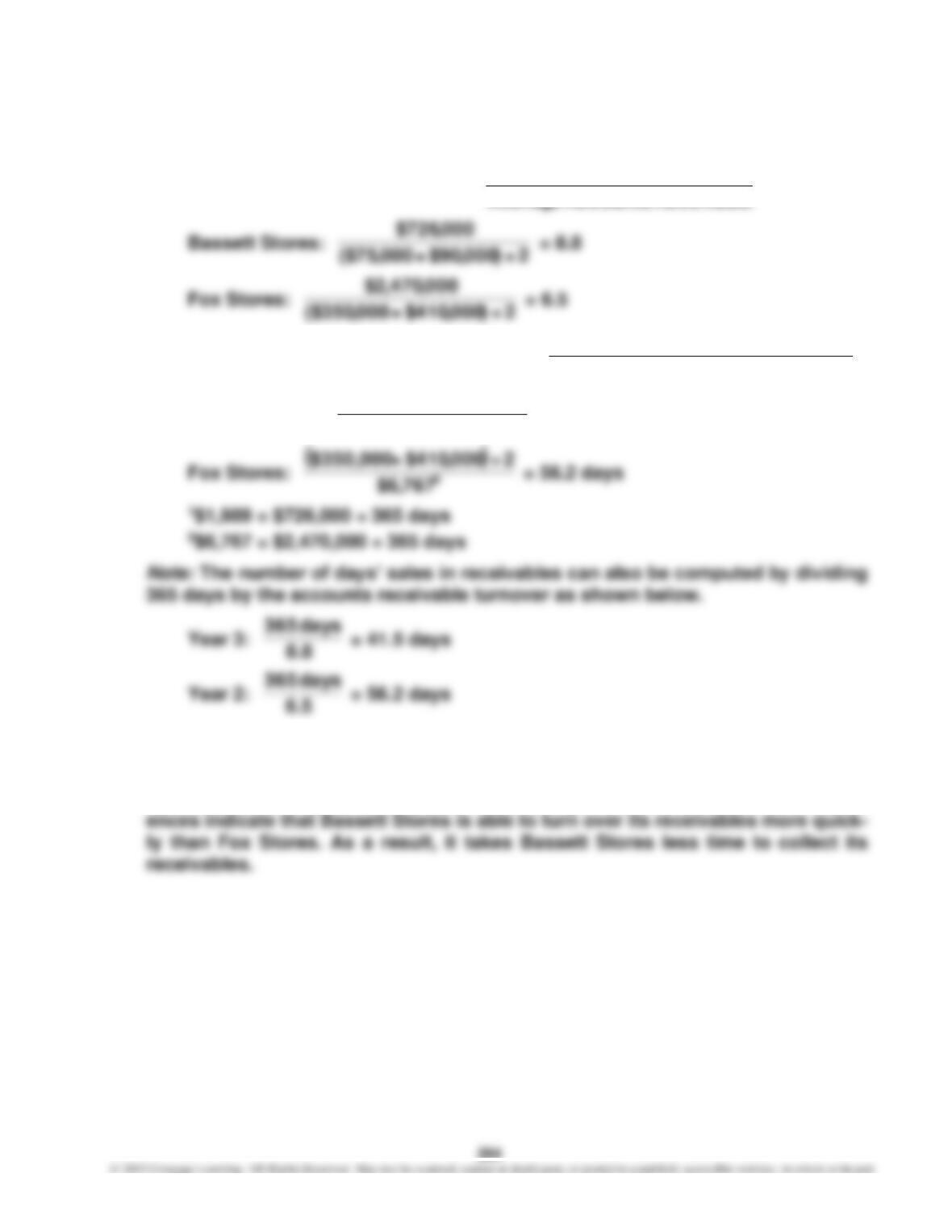

a. (1) Accounts Receivable Turnover =

Receivable AccountsAverage

Accounton SalesNet

(2) Number of Days’ Sales in Receivables =

Accounton Sales Daily Average

Receivable Accounts

Bassett Stores:

( )

1

$1,989

2÷000,90$ + $75,000

= 41.5 days

b. Bassett Stores’ accounts receivable turnover is much higher than Fox Stores

(8.8 compared to 6.5). The number of days’ sales in receivables is lower for Bas-

sett Stores than for Fox Stores (41.5 days compared to 56.2 days). These differ-

265

E9–11

a. (1) Inventory Turnover =

Inventory Average

Sold Goods ofCost

(2) Number of Days’ Sales in Inventory =

Sold Goods ofCost Daily Average

Inventory Average

Current Year:

1

$15,945

2÷)000,550$+000,420($

= 30.4 days

Preceding Year:

2

$11,795

2÷)000,420$+000,400($

= 34.8 days

b. The inventory position of the business has improved. The inventory turnover has

increased, while the number of days’ sales in inventory has decreased. The sales

volume has increased faster than the inventory has increased, thus resulting in

the improving inventory position.

E9–12

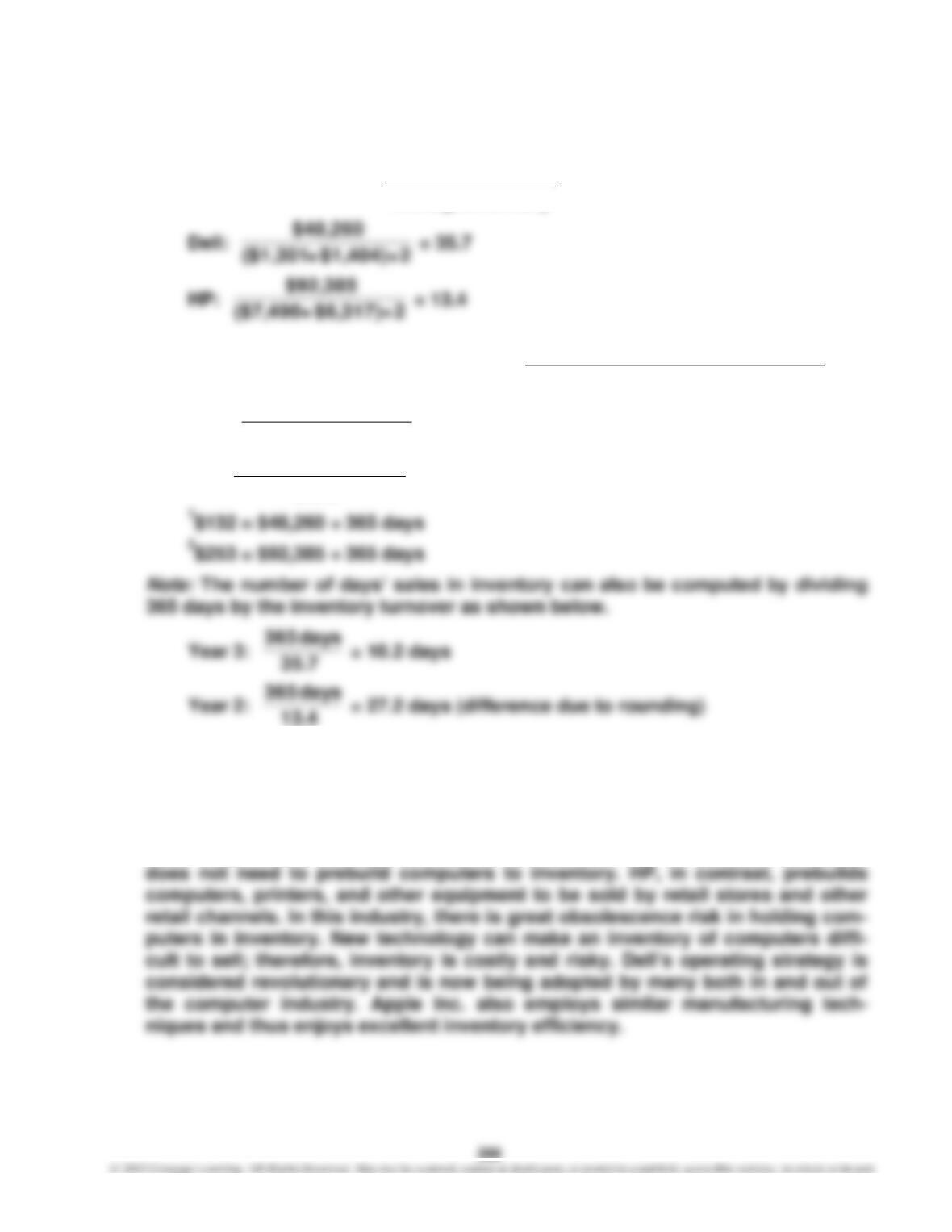

a. (1) Inventory Turnover =

Inventory Average

Sold Goods ofCost

(2) Number of Days’ Sales in Inventory =

Sold Goods ofCost Daily Average

Inventory Average

Dell:

1

$132

2÷$1,404)+($1,301

= 10.2 days

HP:

2

$253

2÷$6,317)+($7,490

= 27.3 days

b. Dell has a much higher inventory turnover ratio than does HP (35.7 for Dell vs.

13.4 for HP). Likewise, Dell has a much smaller number of days’ sales in invent-

tory (10.2 days for Dell vs. 27.3 days for HP). These significant differences are a

result of Dell’s make-to-order strategy. Dell has successfully developed a manu-

facturing process that is able to fill a customer order quickly. As a result, Dell

267

E9–13

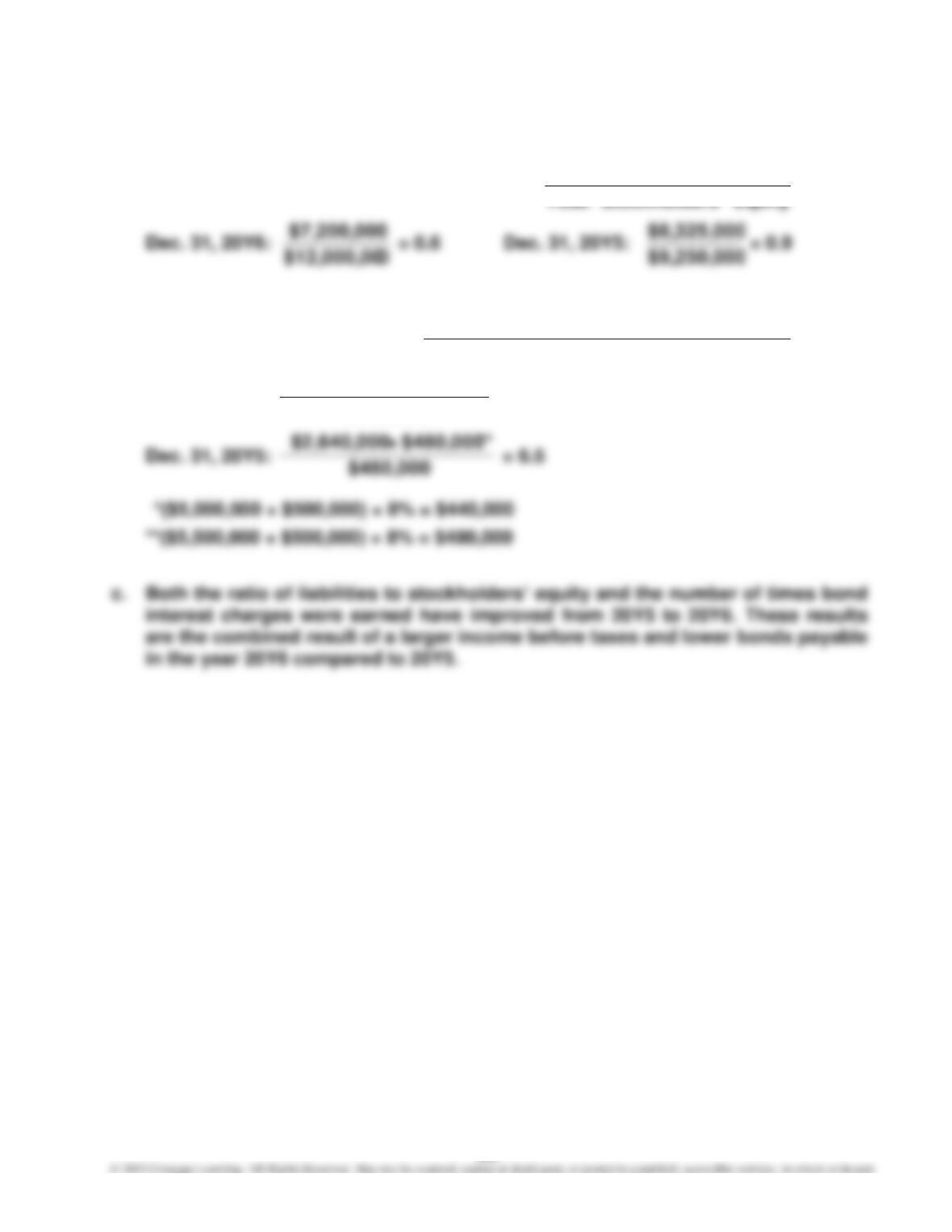

a. Ratio of Liabilities to Stockholders’ Equity =

Total Liabilities

Total Stockholders’ Equity

b.

Earned AreChargesInterest

Bond Times of Number

=

ExpenseInterest

ExpenseInterest + Tax Before Income

Dec. 31, 20Y6:

$440,000

000$440 + $2,816,000 *,

= 7.4

268

E9–14

a. Ratio of Liabilities to Stockholders’ Equity =

Equity rs’Stockholde Total

sLiabilitie Total

Hasbro:

$2,713

= 1.9

b.

Earned AreChargesInterest

Times of Number

=

ExpenseInterest

ExpenseInterest + Tax Before Income

Hasbro:

$89

$89 + $486

= 6.5

269

E9–15

a. Ratio of Liabilities to Stockholders’ Equity =

Equity rs‘Stockholde Total

sLiabilitie Total

H.J. Heinz:

$2,759

$1,683 + $4,780 + $2,648

= 3.3

b. Ratio of Fixed Assets to Long-Term Liabilities =

Fixed Assets (net)

Long–Term Liabilities

H.J. Heinz:

$6,463

$2,484

=

$1,683 + $4,780

$2,484

= 0.38

c. H.J. Heinz uses more debt than does Hershey, but the ratio of total liabilities to

stockholders’ equity ratio is similar for both companies (3.3 vs. 4.2), the ratio of

fixed assets is very different. H.J. Heinz has a much lower ratio of fixed assets to

long-term liabilities than Hershey. This ratio divides the property, plant, and

E9–16

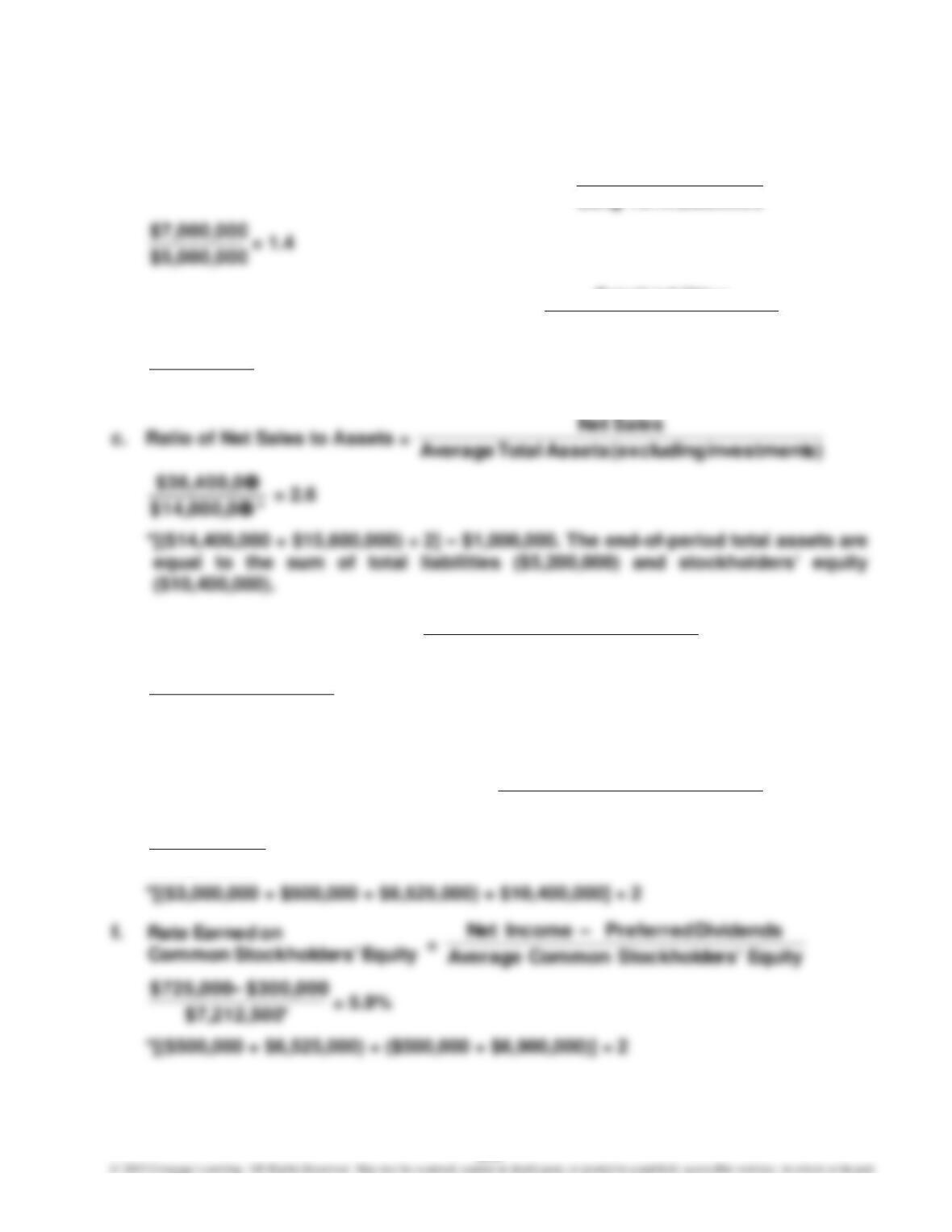

a. Ratio of Net Sales to Total Assets:

AssetsTotal Average

Sales Net

YRC Worldwide:

$2,529

$4,869

= 1.9

b. The ratio of net sales to assets measures the number of sales dollars earned for

each dollar of assets. The greater the number of sales dollars earned for every

dollar of assets, the more efficient a firm is in using assets. Thus, the ratio is a

measure of the efficiency in using assets. The three companies are different in

their efficiency in using assets, because they are different in the nature of their

operations. Union Pacific earns only 40 cents for every dollar of assets. This is

because Union Pacific is very asset intensive. That is, Union Pacific must invest

271

E9–16, Concluded

Note to Instructors: Students may wonder how asset-intensive companies over-

come their asset efficiency disadvantages relative to competitors with better

asset efficiencies, as in the case between railroads and motor carriers. Asset

efficiency is part of the financial equation; the other part is the profit margin

E9–17

a. Rate Earned on Total Assets =

AssetsTotal Average

ExpenseInterest + IncomeNet

20Y5:

*$2,650,000

$40,000 + $530,000

= 21.5% 20Y4:

**$2,200,000

$40,000 + $430,000

= 21.4%

*($2,900,000 + $2,400,000) ÷ 2 **($2,400,000 + $2,000,000) ÷ 2

Rate Earned on Stockholders’ Equity =

Equity rs‘Stockholde Average

IncomeNet

b. The profitability ratios indicate that The O’Malley Group’s profitability has

declined slightly. Most of this change is due to net income not increasing as rap-

idly from 20Y4 to 20Y5 as net income increased from 20Y3 to 20Y4. Specifically,

net income increased 23.3% [($530,000 – $430,000) ÷ $430,000] from 20Y4 to

272

E9–18

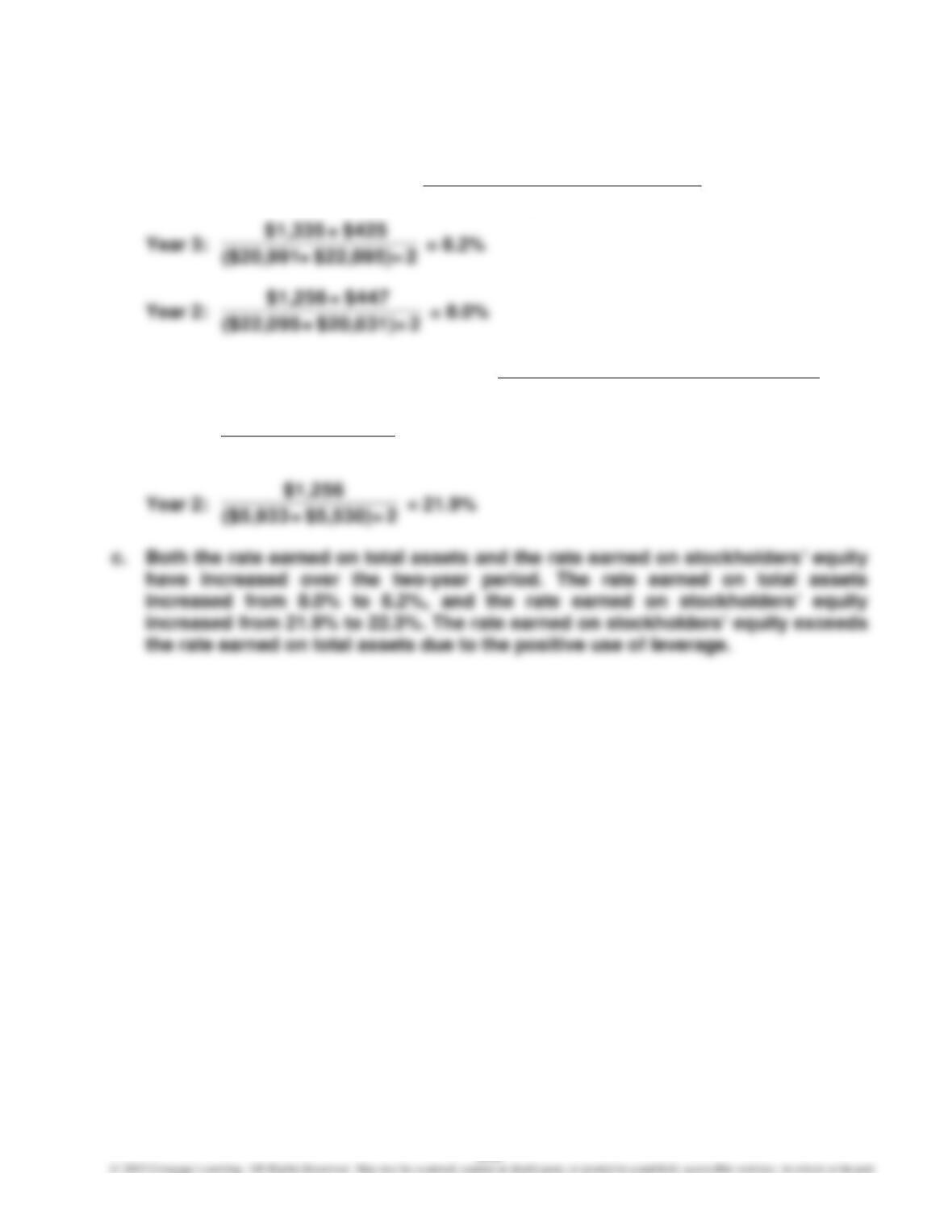

a. Rate Earned on Total Assets =

AssetsTotal Average

ExpenseInterest + IncomeNet

b. Rate Earned on Stockholders’ Equity =

Equity rs‘Stockholde Total Average

IncomeNet

Year 3:

2 ÷ $5,933) + ($6,051

$1,335

= 22.3%

273

E9–19

a. Ratio of Fixed Assets to Long-Term Liabilities =

sLiabilitie ermT–Long

AssetsFixed

b. Ratio of Liabilities to Stockholders’ Equity =

Equity rs‘Stockholde Total

sLiabilitie Total

0$10,400,00

$5,200,000

= 0.5

d. Rate Earned on Total Assets =

AssetsTotal Average

Expense Interest + Income Net

*0$15,000,00

$400,000 + $725,000

= 7.5%

*($14,400,000 + $15,600,000) ÷ 2

e. Rate Earned on Stockholders’ Equity =

Equity rs‘Stockholde Average

IncomeNet

*0$10,212,50

$725,000

= 7.1%

274

E9–20

a.

Earned AreChargesInterest

Bond Times of Number

=

ExpenseInterest

ExpenseInterest + Tax Before Income

$400,000

$400,000 + $3,400,000

= 9.5

c. Earnings per Share on Common Stock =

gOutstandin Shares Common

Dividends Preferred –– Income Net

shares 500,000

$800,000 –– $2,400,000

= $3.20

e. Dividends per Share of Common Stock =

gOutstandin Shares Common

Dividends Common

shares 500,000

$100,000

= $0.20