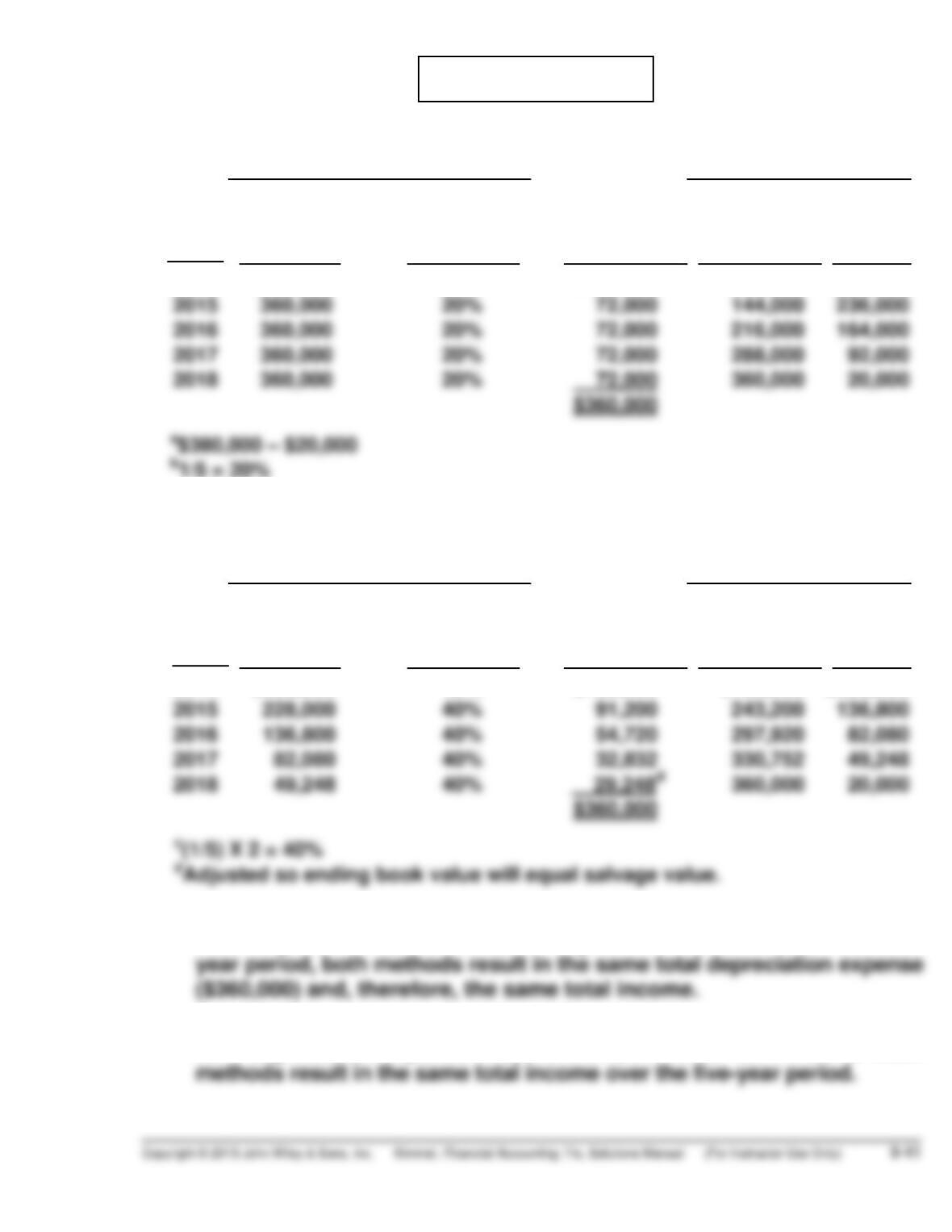

(a) STRAIGHT-LINE DEPRECIATION

Computation End of Year

Annual

Depreciable Depreciation Depreciation Accumulated Book

Years Cost X Rate = Expense Depreciation Value

2014 $360,000a 20%b $ 72,000 $ 72,000 $308,000

DOUBLE-DECLINING-BALANCE DEPRECIATION

Computation End of Year

Book Value Annual

Beginning Depreciation Depreciation Accumulated Book

Years of Year X Rate = Expense Depreciation Value

2014 $380,000 40%c $152,000 $152,000 $228,000

(b) Straight-line depreciation provides the lower amount for 2014 depreci-

ation expense and, therefore, the higher 2014 income. Over the five-

(c) Double-declining-balance depreciation provides the higher amount for

2014 depreciation expense and, therefore, the lower 2014 income. Both

*PROBLEM 9-8B

CHAPTER 9 COMPREHENSIVE PROBLEM SOLUTION

(a) Dec. 2 Equipment ……………………………………………. 16,800

Cash ……………………………………………….. 16,800

Cash …………………………………………………….. 3,500

Accumulated Depreciation—Equipment … 2,625

Equipment ………………………………………. 5,000

15 Accounts Receivable ……………………………. 5,000

Sales Revenue …………………………………. 5,000

23 Salaries and Wages Expense ………………… 6,600

Cash ……………………………………………….. 6,600

31 Bad Debt Expense ($4,000 – $500) …………. 3,500

Allowance for Doubtful Accounts …….. 3,500

Interest Receivable

Depreciation Expense …………………………… 4,000

Accumulated Depreciation—Building

COMPREHENSIVE PROBLEM (Continued)

Depreciation Expense ……………………………… 250

Accumulated Depreciation—Equipment

[($16,800 – $1,800) ÷ 5] X 1/12 …………… 250

COMPREHENSIVE PROBLEM (Continued)

(b) KENSETH CORPORATION

Adjusted Trial Balance

December 31, 2014

Debits Credits

Cash …………………………………………………………

Accounts Receivable …………………………………

Allowance for Doubtful Accounts ………………

Accumulated Depreciation—Buildings ……….

Accumulated Depreciation—Equipment …….

Sales Revenue ………………………………………….

Interest Revenue ……………………………………….

Gain on Disposal of Plant Assets……………….

$ 2,100

41,800

$ 4,000

54,000

32,350

905,000

600

1,125

COMPREHENSIVE PROBLEM (Continued)

(c) KENSETH CORPORATION

Income Statement

For the Year Ended December 31, 2014

Sales revenue ………………………………….

Cost of goods sold …………………………..

Total operating expenses …………………

Income from operations ……………………

Other revenues and gains

$905,000

633,500

202,475

69,025

KENSETH CORPORATION

Retained Earnings Statement

For the Year Ending December 31, 2014

Retained earnings, 1/1/14 ……………………………………

$ 63,600

COMPREHENSIVE PROBLEM (Continued)

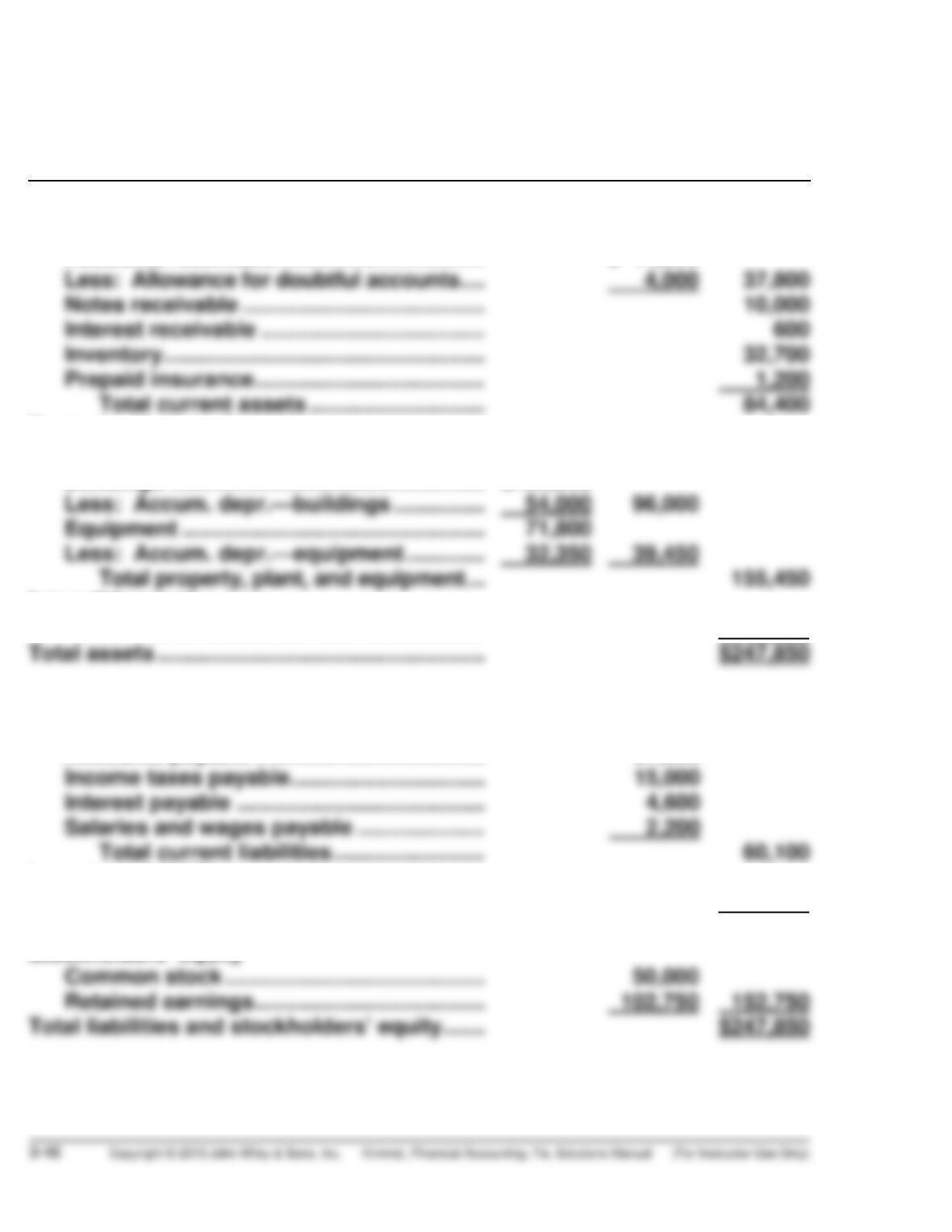

(d) KENSETH CORPORATION

Balance Sheet

December 31, 2014

Current assets

Cash ……………………………………………………

Accounts receivable …………………………….

Property, plant, and equipment

Land ……………………………………………………

Buildings …………………………………………….

Intangible assets

Patent ………………………………………………….

T

Current liabilities

Notes payable (due April 30, 2015) ………..

Accounts payable ………………………………..

Long-term liabilities

Notes payable (due in 2020)………………….

T

otal liabilities …………………………………………..

Stockholders’ equity

T

$150,000

$ 41,800

20,000

$ 11,000

27,300

$ 2,100

8,000

35,000

95,100

(a) At December 31, 2011, total cost of property, plant and equipment was

$455,097,000; book value was $212,162,000.

(e) Goodwill and intangible assets with indefinite lives are not amortized,

but rather tested for impairment at least annually. The company tested

goodwill and trademarks during the fourth quarter of each year. It

recorded an impairment in 2009 but none in 2010 or 2011.

BYP 9-1 FINANCIAL REPORTING PROBLEM

(a) Tootsie Roll Hershey Company

$43,938 $628,962

The asset turnover measures how efficiently a company uses its assets

to generate sales. It shows the dollars of sales generated by each dollar

invested in assets. Hershey Company’s asset turnover (1.40) was 126%

higher than Tootsie Roll’s (.62) in 2011. Therefore, it can be concluded

BYP 9-2 COMPARATIVE ANALYSIS PROBLEM

1. Return on assets

(a) All of the companies have market values (that is, the total market price of

all of their shares) that is less than the shareholders’ equity on their

(b) In most instances, when a company’s market value is less than its book

value, the company needs to consider writing down its goodwill. It is

(c) In order for goodwill to be present on a company’s balance sheet, that

company must have purchased another business. If the amount paid for

BYP 9-3 RESEARCH CASE

(a) Online retailers, such as Amazon, have large investments in

sophisticated warehouses, but they have no money tied up in massive

stores, such as those of Best Buy. This is would mean that, all else equal,

an online retailer would have lower total assets, which would increase

the asset turnover as well as the return on assets. We would also expect

that the online retailer’s operating costs would be lower since it doesn’t

incur salary and other costs of running a store. This should increase its

net income, which would increase the profit margin ratio.

2011 2006

(b) Profit Margin $1,277 =2.5%

$50,272 $1,140 =3.7%

$30,848

(c) Profit Margin × Asset Turnover = Return on Assets

(d) It is interesting to note that the asset turnover stayed the same, at 2.78

times between 2006 and 2011. This means that the company generates

the same amount of sales per dollar invested in assets. However, the

BYP 9-4 INTERPRETING FINANCIAL STATEMENTS

Answers will vary depending on the company chosen by student.

BYP 9-5 REAL-WORLD FOCUS

(a)

(in thousands) Current results

Proposed results

without cannibalization

Proposed results

with cannibalization

Return on assets $12,000 = .12 $13,500 = .135 $12,000 = .12

$100,000 $100,000 $100,000

(b) If there is no cannibalization, return on assets increases from 12% to

13.5%. This occurs even though the profit margin decreases from 27%

to 22.5% because the asset turnover increases significantly, from .45

(c) Yes, there are other alternatives. Here are some examples.

1. Increase spending on marketing in an effort to increase sales of

high end product, without offering the new, low-end product line.

2. Consider marketing the new line under a different name, so as to

minimize the cannibalization. This might substantially increase

3. If neither of 1. or 2. seems feasible, they should consider closing

a plant. This would increase the asset turnover and return on

assets.

BYP 9-6 DECISION MAKING ACROSS THE ORGANIZATION

Answers will depend on the position selected by the student. Some points

that should be considered include:

1. Some relatively small companies may spend less on R&D because they

must expense these costs. However, the vast majority of companies

2. The tangible future benefits of R&D costs may not be realized for

several years, if ever. Conversely, the purchase of a long-lived asset

BYP 9-7 COMMUNICATION ACTIVITY

(a) The stakeholders in this situation are:

Tyler Weber, president of Fresh Air Anti-Pollution Company.

Robin Cain, controller.

(b) The intentional misstatement of the life of an asset or the amount of the

salvage value is unethical for whatever the reason. There is nothing

unethical per se about changing the estimates used for the life of an

asset or of an asset’s salvage value if the change is an attempt to better

(c) Income before income taxes in the year of change is increased $155,000

($387,500 – $232,500) by implementing the president’s proposed changes.

Old Estimates

Asset cost…………………………………………………….. $3,500,000

Revised Estimates

Asset cost…………………………………………………….. $3,500,000

Estimated salvage ………………………………………… 400,000

BYP 9-8 ETHICS CASE

BYP 9-9 ALL ABOUT YOU

(b) For the most part, the value of a brand is not reported on a company’s

balance sheet. Most companies are required to expense all costs related

to the maintenance of a brand name. Also any research and development

that went into the development of the related product is generally

BYP 9-10 FASB CODIFICATION ACTIVITY

(a) Capitalize is a term used to indicate that the cost would be recorded as

(b) Intangible assets are assets that lack physical substance. (The term

intangible asset is used to refer to intangible assets other than

goodwill.)

(c) Codification reference 360-10-35-2 addresses the concept of deprecia-

tion accounting and the various factors to consider in selecting the

BYP 9-11 CONSIDERING PEOPLE, PLANET AND PROFIT

(a) Airbus developed a wing attachment called a Sharklet that is designed to

reduce fuel consumption. It is quite similar to a device that is sold by

(b) Aviation Partners says that its Winglets will reduce fuel consumption by

5 to 7 percent. It says that the total amount of jet fuel that its device has

saved is approximately 3 billion gallons.

(c) Airbus and Aviation Partners were involved in discussions for about

(d) If Aviation Partners loses the lawsuit it would have expense the cost

of the lawsuit. It would also have to review the recorded value of its

IFRS CONCEPTS AND APPLICATION

IFRS9-1

Component depreciation is a method of allocating the cost of a plant asset

into separate parts based on the estimated useful lives of each component.

IFRS9-2

Revaluation is an accounting procedure that adjusts plant assets to fair value

at the reporting date. Revaluation must be applied annually to assets that are

experiencing rapid price changes.

IFRS9-3

Both types of development expenditures relate to the creation of new products

but one is expensed and the other is capitalized. Development costs incurred

IFRS9-4

Warehouse component: ($280,000 – $40,000)/20 = $12,000

IFRS9-5

(a) Accumulated Depreciation—Plant Assets …………….. 60,000

Revaluation Surplus ………………………………….. 40,000

IFRS9-6

Development Expense ………………………………………………… 400,000

IFRS9-7 INTERNATIONAL FINANCIAL STATEMENT ANALYSIS

(a) Zetar uses straight line and reducing-balance depreciation methods.

The depreciation rates range from 10–33%.