275

E9–19, Concluded

f. Return on Stockholders’ Equity = Net Income

Average Total Stockholders’ Equity

$500,000

$11,150,000 * = 4.48%

*[($8,000,000 + $1,000,000 + $2,000,000) + $11,300,000] ÷ 2

276

E9–20

a. Times Interest Earned =

Income Before Income Tax + Interest Expense

Interest Expense

$400,000

$400,000 + $3,400,000 = 9.5

c. Earnings per Share on Common Stock = Net Income –– Preferred Dividends

Common Shares Outstandin

g

$2,400,000 –– $800,000

500,000 * shares = $3.20

*$3,500,000 ÷ $7 = 500,000

e. Dividends per Share of Common Stock = gOutstandin Shares Common

Dividends Common

shares 500,000

$100,000 = $0.20

277

E9–21

a. Earnings per Share =

Net Income –– Preferred Dividends

Common Shares Outstanding

$1,300,000 –– $150,000*

100,000** shares

= $11.50

*($2,250,000 ÷ $90) × $6 = $150,000

**$12,500,000 ÷ $125 = 100,000 shares

b. Price-Earnings Ratio =

$11.50

$92.00

= 8.0

278

E9–22

a. Price-Earnings Ratio = Share per Earnings

Share per PriceMarket

Dividend Yield = Share per PriceMarket

Share per Dividends

Amazon.com:

$0.00

$1,855.32 = 0%

McDonald’s:

$3.83

$169.96 = 2.3%

Microsoft:

$1.84

$138.06 = 1.3%

Appendix E9–23

a. NR d. NR

a.

LEADBETTER INC.

Partial Income Statement

For the Year Ended December 31, 20Y3

Income from continuing operations before income tax …………….. $766,250

b.

LEADBETTER INC.

Partial Income Statement

For the Year Ended December 31, 20Y3

Earnings per common share:

Income from continuing operations …………………………………….. $6.131

Gain from discontinued operations ……………………………………… 2.402

280

PROBLEMS

P9–1

1.

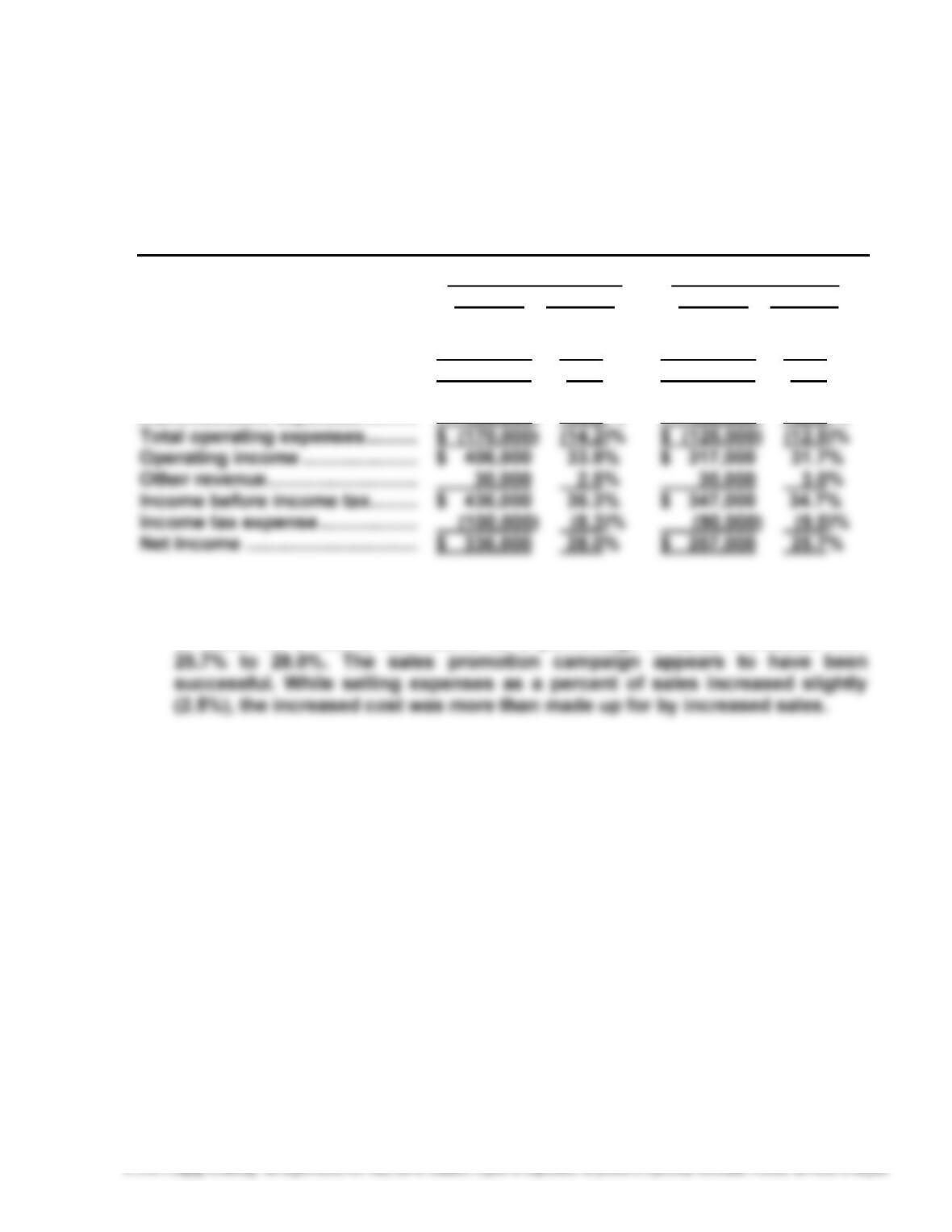

GREYHOUND TECHNOLOGY COMPANY

Comparative Income Statement

For the Years Ended December 31, 20Y3 and 20Y2

Increase (Decrease)

20Y3 20Y2 Amount Percent

Sales ………………………………………. $862,000 $785,000 $ 77,000 9.8%

Cost of goods sold ………………….. (650,000) (500,000) 150,000 30.0%

Gross profit …………………………….. $212,000 $285,000 $ (73,000) (25.6)%

Selling expenses …………………….. $ (44,000) $ (40,000) $ 4,000 10.0%

Administrative expenses …………. (27,000) (25,000) 2,000 8.0%

2. Net income declined from $202,000 in 20Y2 to $130,300 in 20Y3. Sales

increased by 9.8%; cost of goods sold increased by 30.0%, causing the gross

profit to decline by 25.6%. Selling expenses increased slightly more than

sales (10.0% compared to 9.8%), and administrative expenses increased by

281

P9–2

1.

FISHING EXPERIENCES INC.

Comparative Income Statement

For the Years Ended December 31, 20Y6 and 20Y5

20Y6 20Y5

Amount Percent Amount Percent

Sales ……………………………………. $ 1,200,000 100.0% $ 1,000,000 100.0%

Cost of goods sold ……………….. (624,000) (52.0)% (558,000) (55.8)%

Gross profit ………………………….. $ 576,000 48.0% $ 442,000 44.2%

Selling expenses …………………... $ (120,000) (10.0)% $ (75,000) (7.5)%

2. The vertical analysis indicates that the costs other than selling expenses

(cost of goods sold and administrative expenses) improved as a percentage

of sales. As a result, net income as a percentage of sales increased from

282

P9–3

1. a. Working Capital = Current Assets – Current Liabilities

$675,000 – $250,000 = $425,000

b. Current Ratio = sLiabilitieCurrent

setsCurrent As

2.

Supporting Calculations

Working Current Quick Current Quick Current

Transaction Capital Ratio Ratio Assets Assets Liabilities

a. $ 425,000 2.7 1.9 $675,000 $ 475,000 $250,000

b. 425,000 3.0 2.1 635,000 435,000 210,000

c. 425,000 2.3 1.5 750,000 475,000 325,000

d. 425,000 2.9 2.0 645,000 445,000 220,000

283

P9–4

1. Working capital: $2,790,000

$3,690,000 – $900,000

4. Accounts receivable turnover: 16.0

$10,000,000 ÷ [($740,000 + $510,000) ÷ 2]

5. Day’s sales in receivables: 22.8

$10,000,000 ÷ 365 = $27,397

[($740,000 + $510,000) ÷2] ÷ $27,397

8. Debt ratio: 26.6%

$2,600,000 ÷ $9,780,000

9. Ratio of liabilities to stockholders’ equity: 0.4

$2,600,000 ÷ $7,180,000

10. Ratio of fixed assets to long-term liabilities: 2.2

$3,740,000 ÷ $1,700,000

11. Times interest earned: 7.6

($1,130,000 + $170,000) ÷ $170,000

284

P9–4, Concluded

17. Earnings per share: $8.55

($900,000 – $45,000) ÷ 100,000 shares

18. Price-earnings ratio: 14.0

$119.70 ÷ $8.55

285

P9–5

1. a.

15%

20%

25%

Return on Total Assets = AssetsTotal Average

ExpenseInterest +IncomeNet

Year 5:

$9,500,000

$2,185,000 = 23.0% Year 2: $5,200,000

$1,008,800 = 19.4%