DM–1

DERIVATIVES MODULE

UNDERSTANDING THE ISSUES

1. The intrinsic value of a forward contract to

sell a commodity or currency is determined

by comparing the spot rate/price at the date

of inception of the forward to the spot

rate/price at a later valuation date. At date

of inception of the forward, the difference

between the forward rate and spot

the current spot price. The difference be-

tween these two values times the notional

amount represents the total intrinsic value.

The time value of an option is measured by

subtracting the intrinsic value from the total

value of the option.

2. A firm commitment to sell inventory is fixed

in terms of the quantity, price, and delivery

ment.

3. A cash flow hedge of a forecasted transac-

tion affects both current and future operat-

ue increases $700, then the time value has

decreased by $200. This $200 change

would be recognized in current income.

Changes in the intrinsic value over time are

initially recorded as a component of other

comprehensive income and therefore do

not currently impact operating income.

4. Unlike a futures contract, an option contract

represents a right, rather than an obliga-

tion. While the option contract requires the

holder to make an initial nonrefundable

cash outlay, the holder can allow the option

to expire in unfavorable conditions. In the

case of a futures contract, the contract

6.5% fixed in exchange for receipt of a

variable rate of LIBOR plus 2%. If LIBOR is

greater than 4.5%, the borrower will gain

Derivatives Module—Exercises DM–2

EXERCISES

EXERCISE 1

Because the option hedges a forecasted transaction, the only impact on earnings prior to the

transaction actually taking place and then, in turn, affecting earnings itself will be changes in the

time value of the option.

The impact on earnings for the first and second 30-day period is a charge against earnings of

$2,000 and $2,500, respectively, to be recognized as an unrealized loss on the hedge.

30 Days Expiration

Beginning Later Date

Notional amount in tons ……………………….. 500 500 500

Strike price …………………………………………. $1,200 $1,200 $1,200

First Next

30 Days 30 Days

Fixed interest ($3 million × 8% × 1/12 year) ………………… $20,000 $20,000

Settlement of rate differences:

(8.1% vs. 8% on $3 million × 1/12 year) ………………… 250

(7.8% vs. 8% on $3 million × 1/12 year) ………………… (500)

Net interest expense ………………………………………………… $20,250 $19,500

DM–3 Derivatives Module—Exercises

EXERCISE 2

Corn Futures

June 1 June 30 July 31

Number of bushels ………………………………. 150,000 150,000 150,000

Spot price/bushel ………………………………… $3.42 $3.41 $3.43

Future price/bushel ……………………………… $3.56 $3.53 $3.54

Fair value of contract:

(original futures price vs. current

Time value (spot-forward difference)

Note A: Because the July 31 spot rate is greater than the June 30 spot rate, the contract has no in-

trinsic value. Therefore, the value of the contract must be traceable to time value.

As a result of the above hedging activity, the following changes would occur:

June

July

Increase (decrease) in value of inventory …. $ (1,500) $ 1,500

Gain (loss) on futures contract:

Exercise 2, Concluded

Wheat Futures

June 1 June 30 July 31

Number of bushels ………………………………. 150,000 150,000 150,000

Spot price/bushel ………………………………… $6.20 $6.19 $6.175

Future price/bushel ……………………………… $6.35 $6.33 $6.32

Fair value of contract:

(original futures price vs. current

As a result of the above hedging activity, the following changes would occur:

June

July

Increase (decrease) in value of inventory …. $(1,500) $(2,250)

Gain (loss) on futures contract:

EXERCISE 3

June 30

December 31

(1) Net interest expense:

(8.75% vs. 9% on $4,000,000 × ½ year) ………. (5,000)

(2) Carrying value of note payable:

(3) Net unrealized gain (loss) on the swap …………………… $ 0 $ 0

EXERCISE 4

(1) Critical criteria that must be satisfied in order to justify classification as a fair value hedge

include the following:

a. At inception, the hedging relationship is identified and documented.

b. There is an expectation that the hedge will be highly effective. Effectiveness of the

hedge must be assessed at inception and on an ongoing basis.

(2) Several factors that could suggest that the hedge is highly effective include the following:

a. The option is for the same notional amount (100,000 bushels) as is the commitment.

(3) An option may provide more flexibility than a futures contract because an option does not

have to be exercised if it is out-of-the-money, unlike a future. Therefore, if corn prices in-

(4) The value of an option consists of two components: intrinsic value and time value. The for-

mer represents the extent to which the current spot price compares favorably to the strike

(5) Granted, with an option you are either in-the-money or you are not. Therefore, an option

(6) The initial time value component of an option’s value is allocated to earnings over the pe-

riod of the term of the option. The amount of time value allocated to each period is deter-

EXERCISE 5

30 Days 60 Days

Later

Later

Option A: Call Option

Investment in option (equal to fair value of option) …….. $ 700 $ 2,500

Other comprehensive income Dr (Cr):

Intrinsic value at inception out-of-the-money ……….. $ 0 $ 0

Current intrinsic value out-of-the-money ……………… 0

Current intrinsic value [200 × ($1,510 – $1,500)] ….. 2,000

Change in intrinsic value ……………………………… $ 0 $(2,000)

EXERCISE 6

(1) Analysis of changes in the value of the call option:

February 20 February 28 March 31 April 20

Notional amount in pounds …….. 300,000 300,000 300,000 300,000

Strike price …………………………… $1.60 $1.60 $1.60 $1.60

28 Other Comprehensive Income………………………………………. 3,000

Investment in Option ……………………………………………….. 3,000

To record change in intrinsic value of option.

Investment in Option …………………………………………………… 400

Unrealized Gain on Option ……………………………………….. 400

To record change in time value of option

($800 on February 20 vs. $1,200 on February 28).

Mar. 31 Investment in Option …………………………………………………… 6,000

Other Comprehensive Income ………………………………….. 6,000

To record change in intrinsic value of option.

Apr. 20 Investment in Option …………………………………………………… 6,000

Other Comprehensive Income ………………………………….. 6,000

To record change in intrinsic value of option.

Unrealized Loss on Option …………………………………………… 300

Investment in Option ……………………………………………….. 300

Exercise 6, Concluded

May 3 Inventory of Soybean Meal …………………………………………… 489,000

Cash ……………………………………………………………………… 489,000

To record purchase at $1.63 per pound.

(2) The net effect on earnings with and without the cash flow hedge is as follows:

Without the With the

Hedge

Hedge

Assumed sales value ………………………………………………………. $ 300,000 $ 300,000

EXERCISE 7

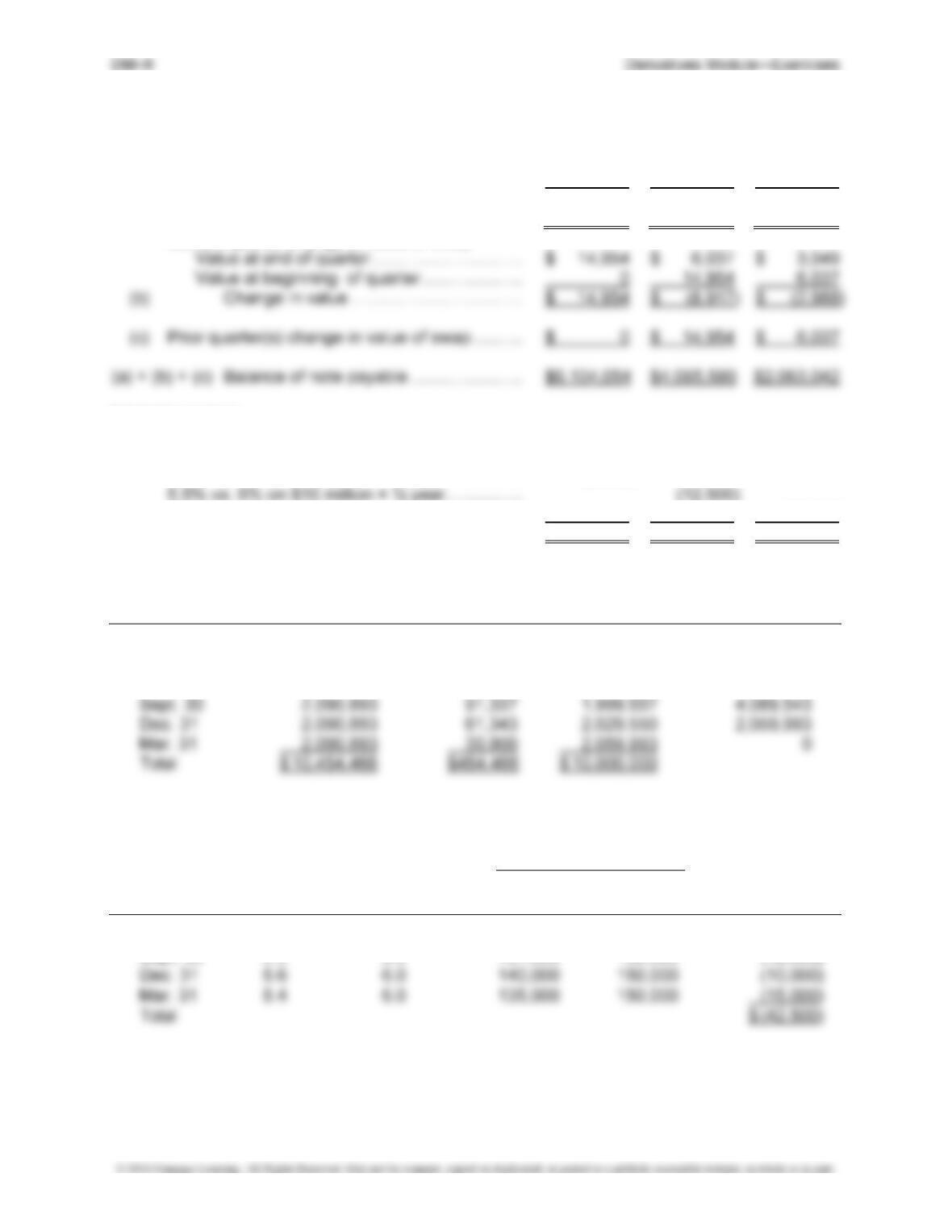

September December

June 30

30 31

Basis of 6% note payable:

(a) Balance per Schedule A ……………………………… $6,089,100 $4,089,543 $2,059,993

Current quarter change in value of swap:

Interest expense:

Amount per Schedule A …………………………………… $ 120,887 $ 91,337 $ 61,343

Settlement of rate difference:

5.8% vs. 6% on $10 million × ¼ year ……………. (5,000)

5.6 % vs. 6% on $10 million × ¼ year …………… (10,000)

Net interest expense ……………………………………….. $ 115,887 $ 78,837 $ 51,343

Schedule A: Amortization of Note Payable Without Swap

Quarter Payment Interest Principal Balance

$ 10,000,000

Mar. 31 $ 2,090,893 $150,000 $ 1,940,893 8,059,107

June 30 2,090,893 120,887 1,970,007 6,089,100

Schedule B: Quarterly Variable versus Fixed Rate Differences

Quarterly Interest at

Variable Variable Quarterly

Quarter Rate Fixed Rate Rate Fixed Rate Difference

June 30 5.80% 6.00% $145,000 $150,000 $ (5,000)

Sept. 30 5.5 6.0 137,500 150,000 (12,500)

Exercise 7, Concluded

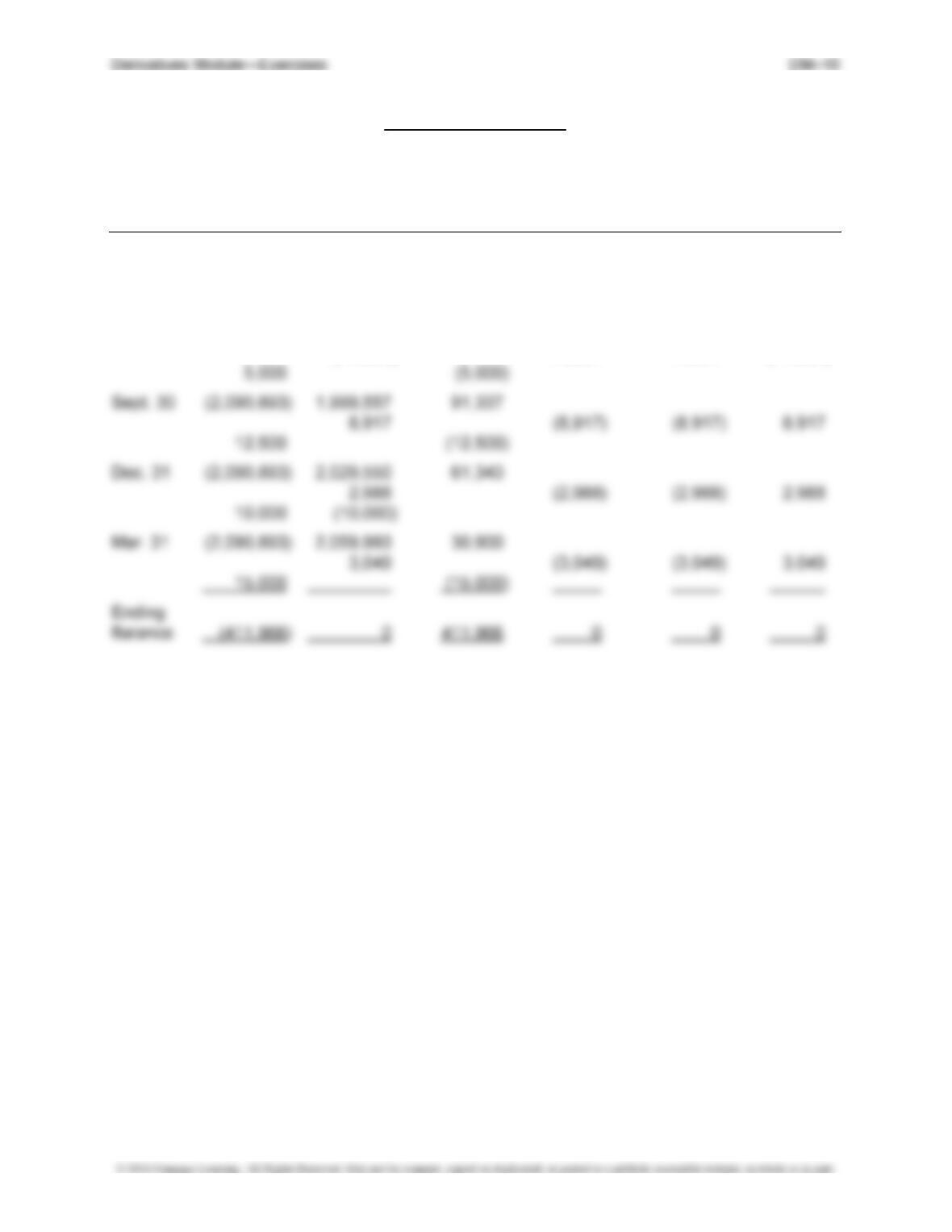

Summary of Entries Dr (Cr) over the Life of the Note Payable

Note Gain (Loss) Swap Gain (Loss)

Cash Payable Interest On Debt Asset on Swap

Beginning

Balance 10,000,000 (10,000,000)

Mar. 31 (2,090,893) 1,940,893 150,000

June 30 (2,090,893) 1,970,007 120,887

(14,954) 14,954 14,954 (14,954)

DM–11 Derivatives Module—Problems

PROBLEMS

PROBLEM M-1

(1) Value of Option March 29 March 31 April 30 May 18

Intrinsic value ……………………. $1,000 $1,000 $3,000 $4,000

Time value ………………………… 1,400 1,200 300 0

Total value ………………………… $2,400 $2,200 $3,300 $4,000

Mar. 29 Investment in Put Option …………………………………….. 2,400

Cash …………………………………………………………… 2,400

To record purchase of option.

Apr. 30 Investment in Put Option …………………………………….. 1,100

Loss on Option (Time Value) ………………………………. 900

Gain on Option (Intrinsic Value) ……………………… 2,000

PROBLEM M-1, Concluded

May 18 Investment in Put Option …………………………………….. 700

Loss on Option (Time Value) ………………………………. 300

Gain on Option (Intrinsic Value) ……………………… 1,000

Inventory of Commodity A …………………………………… 115,000

Firm Commitment ……………………………………………… 3,000

Cash …………………………………………………………… 118,000

To record purchase of inventory.

Cash ………………………………………………………………… 4,000

Investment in Put Option ……………………………….. 4,000

June 16 Cash ………………………………………………………………… 90,000

Sales Revenue …………………………………………….. 90,000

To record sale of one-half of the inventory.

Cost of Sales …………………………………………………….. 70,000

(2) Desired Without the With the

Position Option Option