b.

c.

29,000$

2. 200% Declining-Balance:

29,000$

Book value at the end of the fourth year

Gain on disposal

3. 150% Declining-Balance:

29,000$

Book value at the end of the fourth year

Loss on disposal

PROBLEM 9.2A

SWANSON & HILLER, INC. (concluded)

Computation of gains or losses upon disposal:

Cash proceeds

Swanson & Hiller will probably use the straight-line method for financial reporting

purposes, as this method results in the least amount of depreciation expense in the

early years of the asset’s useful life.

1. Straight-Line

Cash proceeds

Cash proceeds

Loss on disposal

Book value at the end of the fourth year

12,000$

Book

Value

$600 $600 $15,400

16,000 x 1/20

16,000 x 1/20

2019

2020

2021

16,000 x 1/20

Accumulated Book

Depreciation Value

$800 $800 $15,200

2020

2021

2019

Accumulated Book

Depreciation Value

$600 $600 $15,400

2019

2020

2021

Year

2018

Depreciation

Expense

(2) 200% Declining-Balance (half-year convention):

Computation

(3) 150% Declining-Balance (half-year convention):

$16,000 x 10% x 1/2

Year

2018

PROBLEM 9.3A

50 Minutes, Strong

Accumulated

Depreciation

Depreciation

Expense

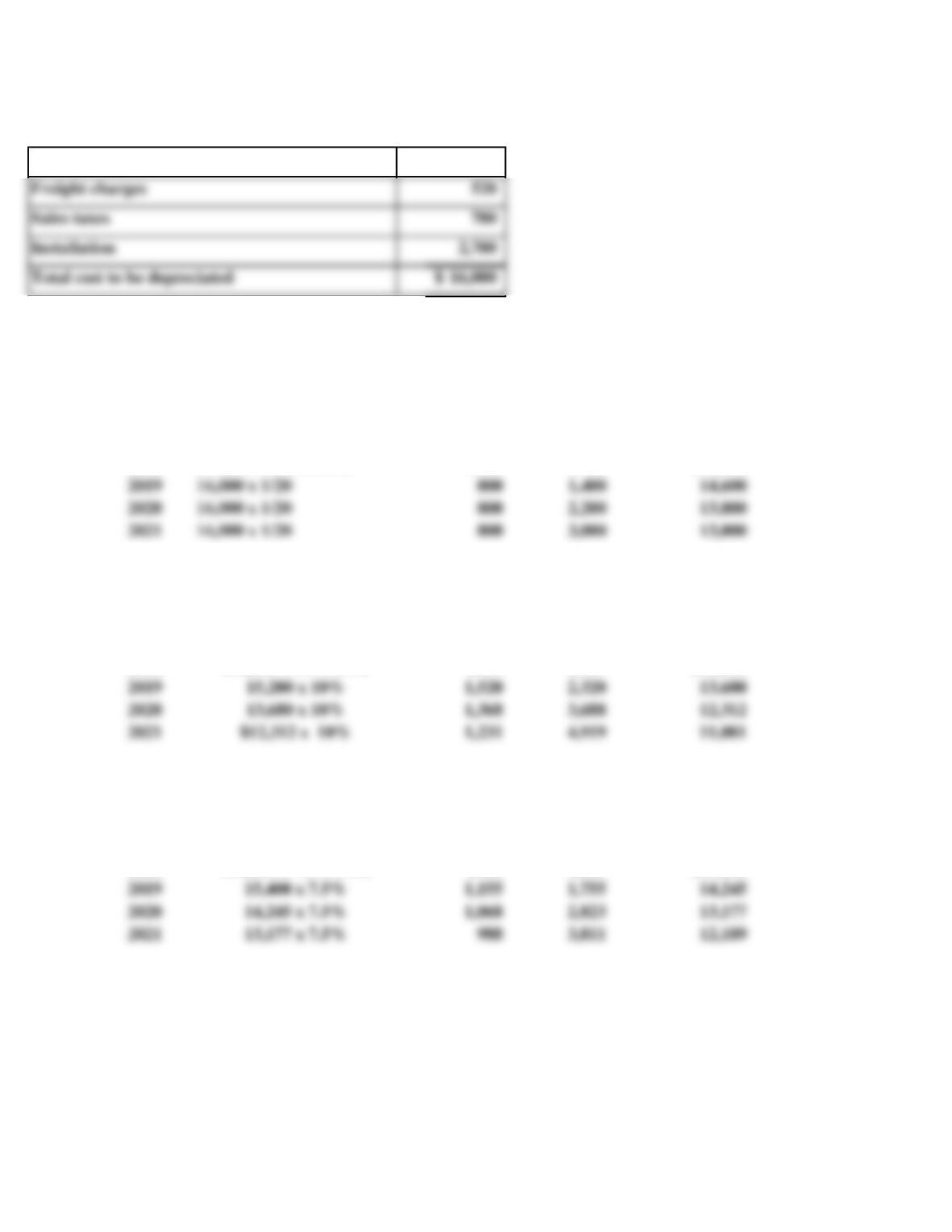

a. Costs to be depreciated include:

Cost of shelving

$16,000 x 7.5% x 1/2

HILLS HARDWARE

(1) Straight-Line Schedule (nearest whole month):

Depreciation

Expense

Computation

Computation

$16,000 x 1/20 x 9/12

Year

2018

Total cost to be depreciated

Freight charges

Sales taxes

b.

c.

1. Journal entry assuming that the shelving was sold for $1,100:

1,100

8,600

Shelving

Gain on Disposal of Assets

Accumulated Depreciation: Shelving

Loss on Sale of Asset

Shelving

2. Journal entry assuming that the shelving was sold for $175:

175

PROBLEM 9.3A

HILLS HARDWARE (concluded)

Hills Hardware may use the straight-line method in its financial statements to

The 200% declining-balance method results in the lowest reported book value at

Cash

Accumulated Depreciation: Shelving

Cash

d.

25 Minutes, Medium

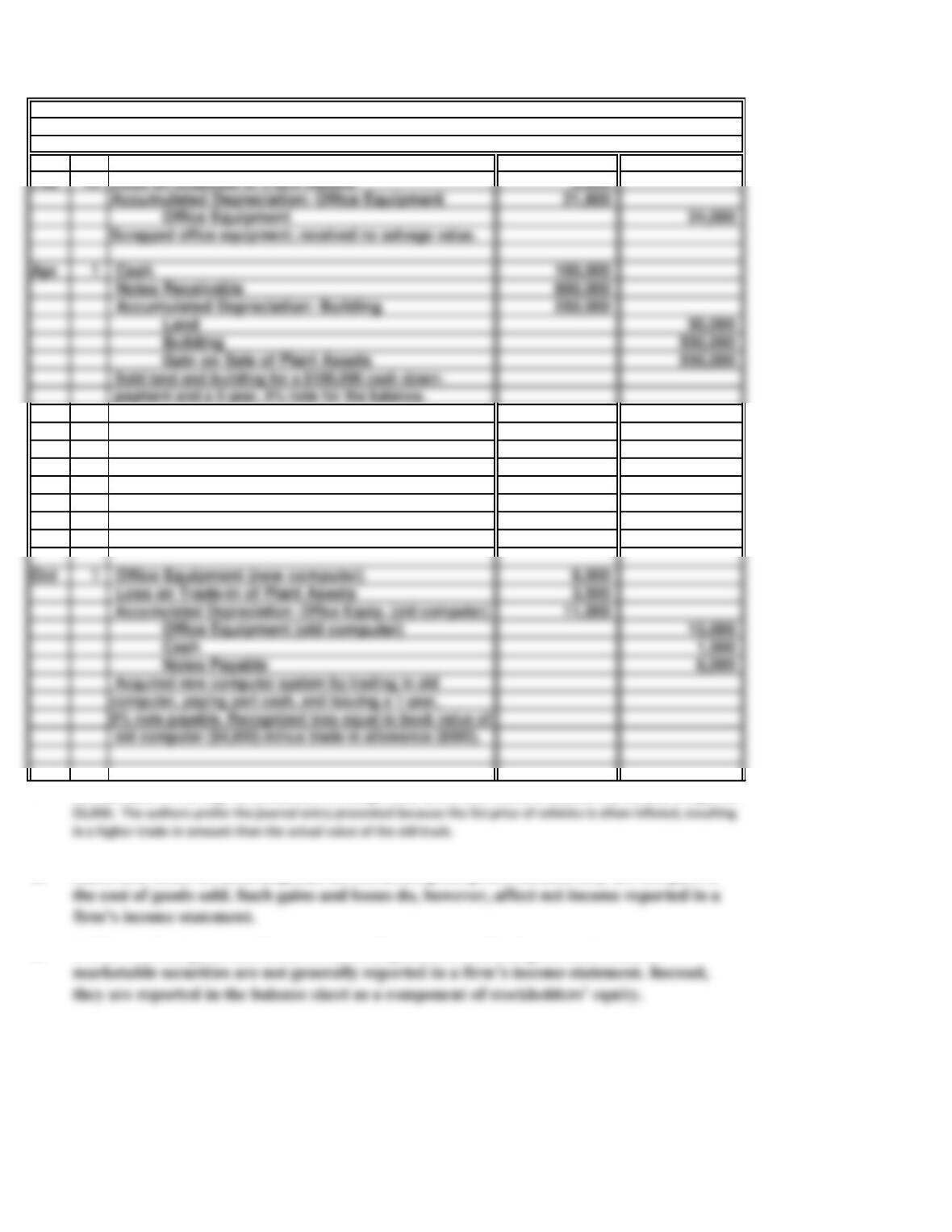

Aug 15* Vehicles (new truck) 38,000

Accumulated Depreciation: Vehicles (old truck) 18,000

Vehicles (old truck) 26,000

Gain on Disposal of Plant Assets 2,000

Cash 28,000

To record trade-in of old truck on new; trade-in

allowance exceeded book value by $2,000.

Loss on Trade-in of Plant Assets 3,500

*

b.

c.

Gains and losses on asset disposals do not affect gross profit because they are not part of

Unlike realized gains and losses on asset disposals, unrealized gains and losses on

PROBLEM 9.4A

a.

General Journal

HITCHCOCK DEVELOPERS

An alternative for the Aug. 15 transaction is to assign a cost to the new vehicle of $39,000 and increase the gain to

Accumulated Depreciation: Office Equipment 21,800

Office Equipment 24,000

Scrapped office equipment; received no salvage value.

Notes Receivable 800,000

Accumulated Depreciation: Building 250,000

Land 50,000

Building 550,000

Gain on Sale of Plant Assets 550,000

Sold land and building for a $100,000 cash down-

payment and a 5-year, 9% note for the balance.

25 Minutes, Medium

a.

b.

c.

d.

PROBLEM 9.5A

REDDICK CORPORATION

Intangible asset. A patent grants its owner the exclusive right to produce a particular

Operating expense. Although the training of employees probably has some benefit

Intangible asset. Goodwill represents the expected value of future earnings in excess of

Operating expense. Because of the uncertainty surrounding the potential benefits of R&D

programs, research and development costs are charged to expense in the period in which

20 Minutes, Medium

220,000$

9.25

Actual average net income per year

Management assumption of four years excess earnings

c.

PROBLEM 9.6A

KIVI SERVICE STATIONS

b. Estimated goodwill associated with the purchase of Gas N’Go:

a. Estimated goodwill associated with the purchase of Joe’s Garage:

Actual average net income per year

Typical sales multiplier

Due to the difficulties in objectively estimating the value of goodwill, it is recorded only when

it is purchased. Kivi may actually have generated internally a significant amount of goodwill

30 Minutes, Medium

a.

b. $20,000

c.

PROBLEM 9.7A

THAXTON, INC.

Depreciation expense for the first two years under the three depreciation methods is

determined as follows:

Straight-line:

Units-of-Output:

The units of output method is directly tied to the miles driven rather than calendar time

Truck

30 Minutes, Medium

a.

$275,000

75,000

c.

$350,000

(52,500) $297,500

Less: Accumulated depreciation

*$75,000 – $15,000 = $60,000

Year 2

Book value

Sales price

Loss on sale

Less: Accumulated depreciation

Plant and intangible asset sections of the balance sheet:

PROBLEM 9.8A

ROTHCHILD, INC.

Depreciation is calculated on the following amount:

Purchase price

Plus: Expenditures to prepare asset for use

Year 1:

Equipment

$350,000

($350,000 – $52,500) x 15% = $44,625

Depreciation expense for Year 3:

($350,000 – $52,500 – $44,625) x 15% = $37,931

The declining balance rate at 150% of the straight-line is:

100%/10 years = 10%; 10% x 1.5 = 15%

Depreciation expense for Year 1:

Depreciation expense for Year 2:

$350,000 x 15% = $52,500

a.

b. (1)

(4)

(5)

(6)

SOLUTIONS TO PROBLEMS SET B

PROBLEM 9.1B

SMITHFIELD HOTEL

The accidental damage to the equipment was not a “reasonable and necessary” part of

the installation process and, therefore, should not be included in the cost of the

25 Minutes, Easy

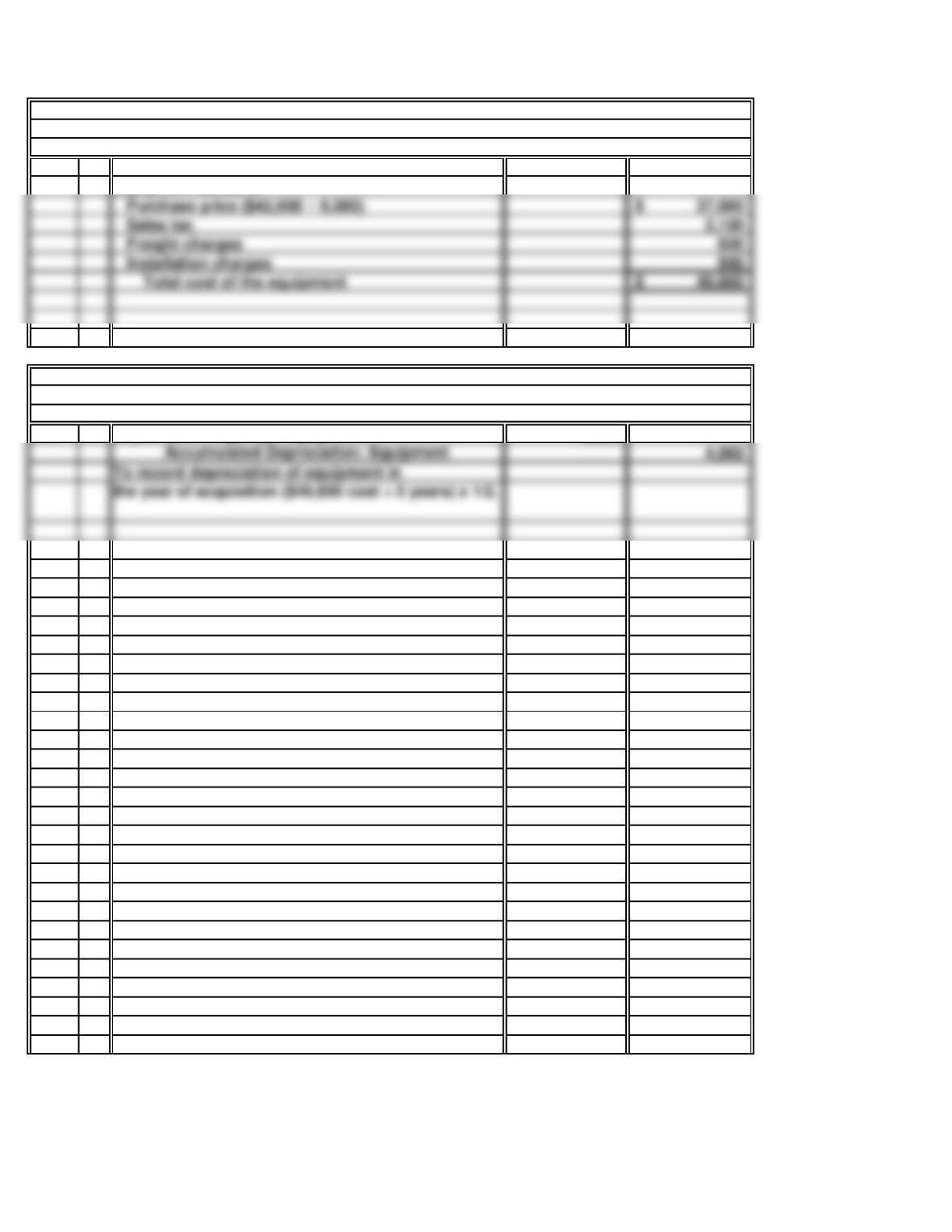

The cost of plant and equipment includes all expenditures that are reasonable and necessary

The purchase price of $37,000 ($42,000 – $5,000) is part of the cost of the equipment.

To be used in hotel operations, the equipment must first be installed. Thus,

(2)

(3)

c.

Equipment account:

Dec 31 4,060

Accumulated Depreciation: Equipment 4,060

To record depreciation of equipment in

PROBLEM 9.1B

SMITHFIELD HOTEL (concluded)

Expenditures that should be debited to the

d.

Depreciation Expense: Equipment

Installation charges

Sales tax

Freight charges

Book

Year Value

1 $17,000 $17,000 $163,000

Accumulated Book

Year Depreciation Value

1 $36,000 $36,000 $144,000

Accumulated Book

Year Depreciation Value

1 $27,000 $27,000 $153,000

2 45,900 72,900 107,100

107,100 x 30%

153,000 x 30%

Depreciation

Expense

$180,000 x 30% x 1/2

Depreciation

Expense

Computation

$180,000 x 40% x 1/2

(3) 150% Declining-Balance Schedule:

Computation

(2) 200% Declining-Balance Schedule:

Depreciation

Expense

Computation

PROBLEM 9.2B

45 Minutes, Medium

R & R, INC.

a. (1) Straight-Line Schedule:

Accumulated

Depreciation

$170,000 x 1/5 x 1/2

b.

c.

$ 58,000

2. 200% Declining-Balance:

$ 58,000

31,104

$ 26,896

Book value at the end of the fourth year

Gain on disposal

3. 150% Declining-Balance:

$ 58,000

52,479

$ 5,521

Book value at the end of the fourth year

Gain on disposal

R & R, Inc. will probably use the straight-line method for financial reporting

1. Straight-Line

Cash proceeds

Cash proceeds

PROBLEM 9.2B

R & R, INC. (concluded)

Computation of gains or losses upon disposal:

Cash proceeds

61,000

Loss on disposal

Book value at the end of the fourth year