CHAPTER 23 (FIN MAN); CHAPTER 9 (MAN) Evaluating Variances from Standard Costs

COMPREHENSIVE PROBLEM 5 (Continued)

Part B

5.

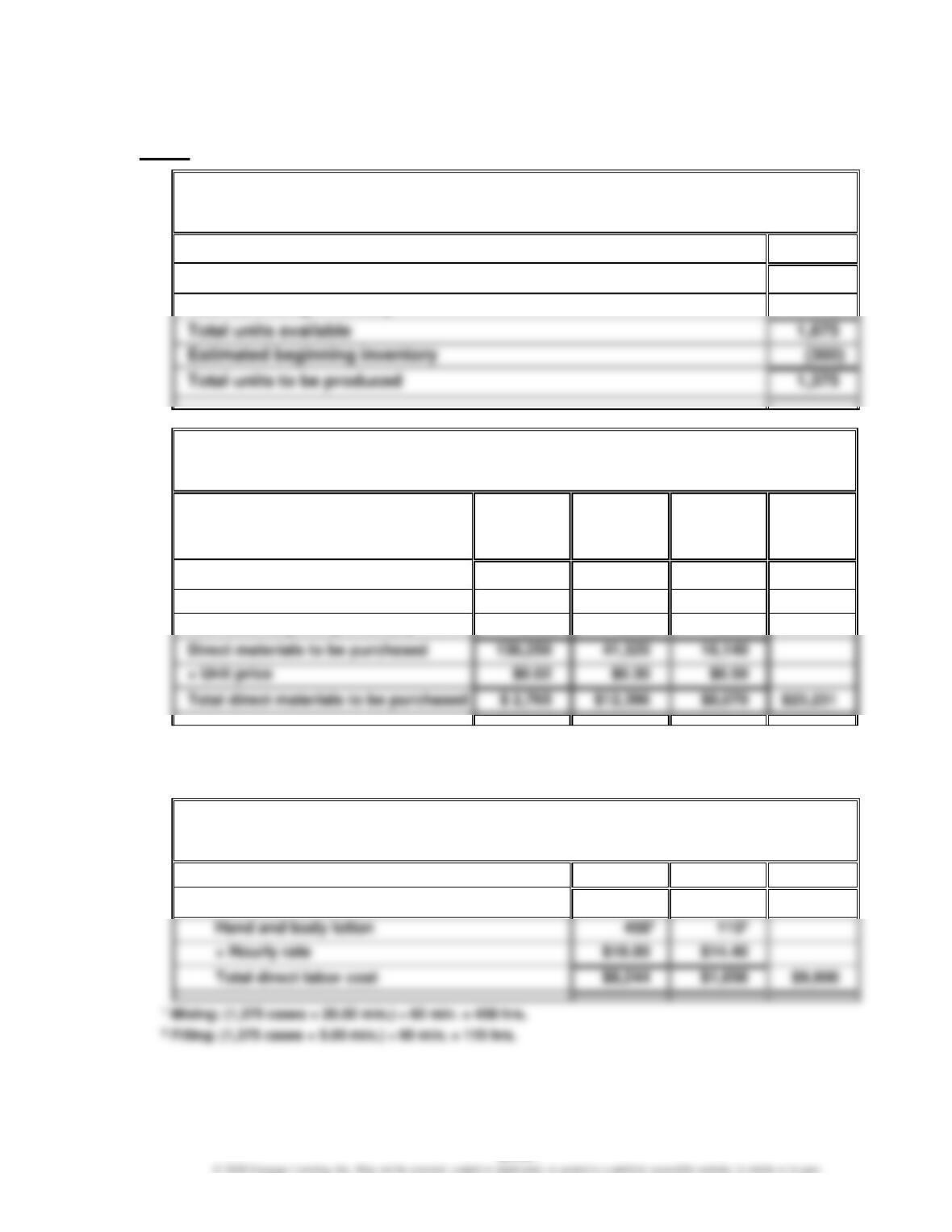

Genuine Spice Inc.

Production Budget

For the Month Ended August 31

Cases

Expected cases to be sold

1,500

Desired ending inventory

175

Total units available

Estimated beginning inventory

6.

Genuine Spice Inc.

Direct Materials Purchases Budget

For the Month Ended August 31

Cream

Base

(ozs.)

Natural

Oils

(ozs.)

Bottles

(bottles)

Total

Units required for production

137,5001

41,2502

16,5003

Desired ending inventory

1,000

360

240

Direct materials to be purchased

$12,396

Estimated beginning inventory

(250)

(290)

(600)

1 Cream base: 1,375 cases × 100 ozs. = 137,500 ozs.

2 Natural oils: 1,375 cases × 30 ozs. = 41,250 ozs.

3 Bottles: 1,375 cases × 12 bottles = 16,500 bottles

7.

Genuine Spice Inc.

Direct Labor Budget

For the Month Ended August 31

Mixing

Filling

Total

Hours required for production of:

4581

CHAPTER 23 (FIN MAN); CHAPTER 9 (MAN) Evaluating Variances from Standard Costs

COMPREHENSIVE PROBLEM 5 (Continued)

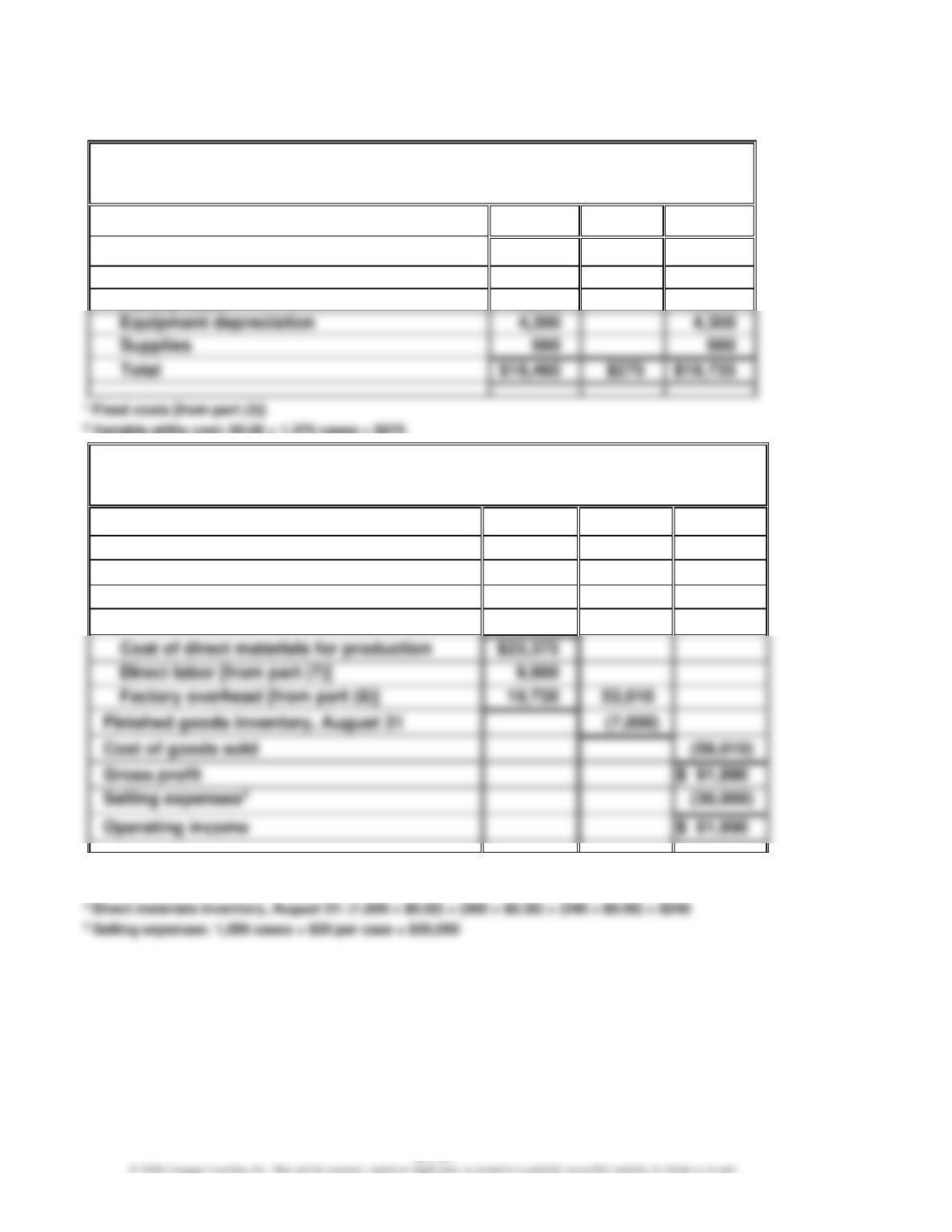

8.

Genuine Spice Inc.

Factory Overhead Budget

For the Month Ended August 31

Fixed1

Variable2

Total

Factory overhead:

Utilities

$ 500

$275

$ 775

Equipment depreciation

Supplies

Facility lease

14,000

14,000

9.

Genuine Spice Inc.

Budgeted Income Statement

For the Month Ended August 31

Sales1

$150,000

Finished goods inventory, August 1

$12,000

Direct materials inventory, August 12

$ 392

Direct materials purchases [from part (6)]

23,231

Direct materials inventory, August 313

(248)

Cost of direct materials for production

Direct labor [from part (7)]

Finished goods inventory, August 31

Cost of goods sold

1 Sales: 1,500 cases × $100 per case = $150,000

2 Direct materials inventory, August 1: (250 × $0.02) + (290 × $0.30) + (600 × $0.50) = $392

CHAPTER 23 (FIN MAN); CHAPTER 9 (MAN) Evaluating Variances from Standard Costs

COMPREHENSIVE PROBLEM 5 (Continued)

Part C

10.

Direct materials price variance:

Cream

Base

Natural

Oils

Bottles

Actual price ………………………

$ 0.016

$ 0.32

$ 0.42

Standard price…………………..

(0.020)

(0.30)

(0.50)

Difference …………………………

$ (0.004)

$ 0.02

$ (0.08)

× Actual quantity (units)* …..

Direct materials price variance

$ (1,500)

CHAPTER 23 (FIN MAN); CHAPTER 9 (MAN) Evaluating Variances from Standard Costs

COMPREHENSIVE PROBLEM 5 (Continued)

Direct materials quantity variance:

Cream

Base

Natural

Oils

Bottles

Actual quantity1 …………………….

153,000

ozs

46,500

ozs.

18,750

btls.

Standard quantity2 ………………..

(150,000)

ozs.

(45,000)

ozs.

(18,000)

btls.

Difference …………………………....

3,000

ozs.

1,500

ozs.

750

btls.

Thus, only unfavorable variances were possible. The standard quantities were

1 Actual quantity:

Cream base: 1,500 cases × 102 ozs. = 153,000 ozs.

Natural oils: 1,500 cases × 31 ozs. = 46,500 ozs.

Bottles: 1,500 cases × 12.5 bottles = 18,750 bottles

CHAPTER 23 (FIN MAN); CHAPTER 9 (MAN) Evaluating Variances from Standard Costs

COMPREHENSIVE PROBLEM 5 (Continued)

11.

Direct labor rate variance:

Mixing

Department

Filling

Department

Actual rate ………………………………………………….

$ 18.20

$ 14.00

Standard rate ………………………………………………

(18.00)

(14.40)

Difference …………………………..………………………

$ 0.20

$ (0.40)

× Actual time (hours)1 ………………………………….

Direct labor rate variance …………………………….

Direct labor time variance:

Mixing

Department

Filling

Department

Actual time (hours)1 ………………………………

487.5

hrs.

140.0

hrs.

Standard time (hours)2 …………………………..

(500.0)

hrs.

(125.0)

hrs.

Difference ……………………………………………..

(12.5)

hrs.

15.0

hrs.

2 Standard time:

Mixing: (1,500 units × 20.00 min.) ÷ 60 min. = 500 hrs.

Filling: (1,500 units × 5.00 min.) ÷ 60 min. = 125 hrs.

The Mixing Department is producing at a labor time that is slightly better than

standard, thus producing a favorable direct labor time variance. This may be the

CHAPTER 23 (FIN MAN); CHAPTER 9 (MAN) Evaluating Variances from Standard Costs

COMPREHENSIVE PROBLEM 5 (Continued)

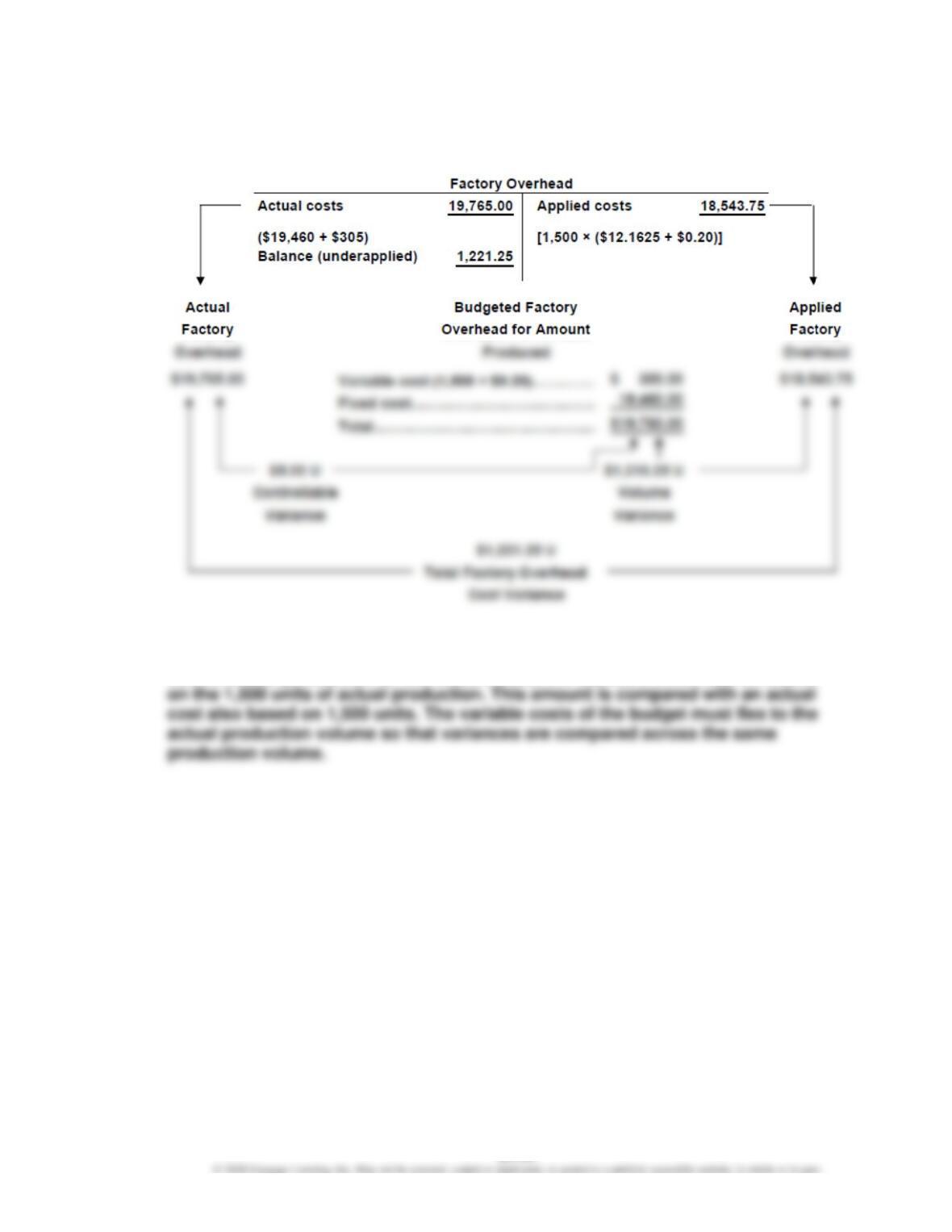

12.

Factory overhead controllable variance:

Actual variable overhead ……………………………………………………

$ 305

*

13.

Factory overhead volume variance:

Normal volume ………………………………………………………………….

1,600

cases

Actual volume ……………………………………………………………………

(1,500)

cases

Difference …………………………………………………………………………

cases

× Fixed factory overhead rate* ……………………………………………

CHAPTER 23 (FIN MAN); CHAPTER 9 (MAN) Evaluating Variances from Standard Costs

COMPREHENSIVE PROBLEM 5 (Concluded)

Alternative Computation of Overhead Variances

14. The production volume of 1,375 cases determined in part (5) was planned at the

beginning of August. The variances compare the actual cost and the standard

cost of actual production for the month. Thus, the standard cost must be based

CHAPTER 23 (FIN MAN); CHAPTER 9 (MAN) Evaluating Variances from Standard Costs

MAKE A DECISION

MAD 23–1 (FIN MAN); MAD 9–1 (MAN)

a.

Standard hours for coding:

Lines of code

1,400

÷ Level 2 standard lines per hour

÷ 50

Note that the standard rate per hour is set at the Level 2 rate for this Level 2 project.

We are comparing the Level 1 performance to the Level 2 standard.

b.

Direct Labor Rate Variance

=

(Actual Rate per Hour – Standard Rate per Hour) ×

Actual Hours

=

($25 – $35) × 40 hrs.

=

$(400) Favorable

MAD 23–2 (FIN MAN); MAD 9–2 (MAN)

a.

Number of employees

4

Hours per week

× 40

Total actual hours for the week

160

Labor rate per hour

× $15

Actual staff cost

$ 2,400

b.

Unscheduled

Scheduled

Total

Standard time (in minutes)

30

15

CHAPTER 23 (FIN MAN); CHAPTER 9 (MAN) Evaluating Variances from Standard Costs

MAD 23–2 (FIN MAN); MAD 9–2 (MAN) (Concluded)

c.

Direct Labor Time Variance

=

(Actual Staff Hours – Standard Staff Hours) ×

Standard Rate per Hour

=

(160 hrs. – 155 hrs.) × $15 per hour

=

$75 Unfavorable

The actual hours exceeded the standard hours; thus, the variance is unfavorable.

d. The first, and most obvious, factor is the mix of admissions. If the mix of

admissions becomes more heavily weighted toward unscheduled admissions,

MAD 23–3 (FIN MAN); MAD 9–3 (MAN)

a.

Standard Sorts per Minute ×

Standard Minutes per Hour

=

Standard Sorts per Hour

(per employee)

90 sorts per min. × 60 min. per hr.

=

5,400 standard sorts per hr.

Pieces of Mail ÷

Standard Sorts per Hour

=

Number of Hours Planned

24,192,000 letters ÷ 5,400 sorts per hr.

=

4,480 hrs. planned

Number of Hours Planned ÷ Hours per

Temporary Employee per Month

=

Number of Hires

28 temporary hires for December

Actual pieces sorted = 23,895,000

=

CHAPTER 23 (FIN MAN); CHAPTER 9 (MAN) Evaluating Variances from Standard Costs

MAD 23–4 (FIN MAN); MAD 9–4 (MAN)

a. 33,900 hours × $25 per hour = $847,500 total budgeted cost

b.

Police Activity

Actual Hours

per Activity

Actual Activities

for Year

Total

Employee

Hours

Theft

0.75

7,000

5,250

Arrest

2.00

18,000

36,000

c

Direct labor time variance

Actual cost

$1,121,250

Budgeted cost

(847,500)

Time variance (unfavorable)

$ 273,750

d. All three police activities are consuming more time per activity than planned. This

CHAPTER 23 (FIN MAN); CHAPTER 9 (MAN) Evaluating Variances from Standard Costs

TAKE IT FURTHER

TIF 23–1 (FIN MAN); TIF 9–1 (MAN)

The use of ideal standards is a legitimate concern for Henry. It is likely that such

standards are too tight and do not include the necessary fatigue factors that are

typical in this type of operation. It seems as though Henry is arguing for practical

standards that can be attained if the operation is running well. Maybe some standard

CHAPTER 23 (FIN MAN); CHAPTER 9 (MAN) Evaluating Variances from Standard Costs

TIF 23–2 (FIN MAN); TIF 9–2 (MAN)

This is a case where there is strong evidence that the poor performance that is

occurring inside the Assembly Department may be the result of behaviors outside

of the department. This is one of the classic problems with variance analysis. Often,

the variances reflect causes outside of the responsibility center manager’s control.

That is what appears to be happening here. The Assembly supervisor complains

that both the purchased parts and incoming material from the Fabrication

Department have been giving them trouble. A review of performance reports reveals

CHAPTER 23 (FIN MAN); CHAPTER 9 (MAN) Evaluating Variances from Standard Costs

TIF 23–3 (FIN MAN); TIF 9–3 (MAN)

To: Plant Manager

From: Controller

Re: Variable Factory Overhead Variances

I have reviewed your concerns related to the recent variable overhead cost variance

report that indicates the plant incurred a total variable factory overhead unfavorable

variance of $12,320. My analysis of the variable nature of the three costs covered in the

report follows.

The major cause of the unfavorable variance appears to originate with indirect factory

wages. Indirect factory wages generated $8,500 of the $12,320 unfavorable variance,

which is almost 70% of the total variance. The variance of $8,500 is 28% ($8,500 ÷

$30,600) higher than the standard. This is much greater than the 10% difference between

the existing production volume and full capacity. In other words, more is being spent on

CHAPTER 23 (FIN MAN); CHAPTER 9 (MAN) Evaluating Variances from Standard Costs

CERTIFIED MANAGEMENT ACCOUNTANT (CMA®)

EXAMINATION QUESTIONS (ADAPTED)

1. d. The actual wage rate per hour is $7.50 and the actual hours worked equal 38,

computed as follows:

Actual hours:

(X – 40 hours) × $7.00

=

$(14.00)

X – 40 hours

(2)

X

=

38

hours

2. b. The materials variance of $11,000 should be investigated, because it exceeds

10% of the budgeted amount ($100,000 × 0.1). The direct labor variance is $4,000,

which is less than 10% of budget ($50,000 × 0.1), so it would not be investigated

under the company policy.

3. d. Frisco’s direct materials price variance is $10,800 favorable, computed as

follows:

4. b. JoyT’s variable factory overhead controllable variance is $2,000 unfavorable,

computed as follows:

Variable Factory Overhead

Controllable Variance

=

Actual Variable

Factory Overhead

–

Budgeted Variable

Factory Overhead