CHAPTER 9 Receivables

Prob. 9-2B (Concluded)

4. Bad Debt Expense 115,860

Allowance for Doubtful Accounts 115,860

Uncollectible accounts estimate

($123,235 – $7,375).

5. On the balance sheet, assets would be overstated by $115,860 because the

allowance for doubtful accounts would be understated by $115,860. In addition,

Prob. 9-3B

1.

Increase Balance of

Expense Expense (Decrease) Allowance

Actually Based on in Amount Account,

Reported Estimate of Expense End of Year

$18,000 $31,250 $13,250 $13,250

2. Yes. The actual write-offs of accounts originating in the first two years are

reasonably close to the expense that would have been charged to those years on

the basis of 1/4% of sales. The total write-off of receivables originating in the first

Bad Debt Expense

Year

1st

CHAPTER 9 Receivables

Prob. 9-4B

1.

Note

1. $110

2. 525

3. 600

2. Oct. 10 Accounts Receivable 48,600

Notes Receivable 48,000

Interest Revenue 600

3. Dec. 31 Interest Receivable 452

4. Jan. 14 Cash 36,480

Notes Receivable 36,000

Interest Receivable 368

Interest Revenue 112

($36,000 × 8% × 14 ÷ 360).

Feb. 8 Cash 24,240

Notes Receivable 24,000

Feb. 13

Due Date

(a)

Apr. 23

Oct. 10

Interest Due at Maturity

(b)

($33,000 × 4% × 30 ÷ 360)

($60,000 × 7% × 45 ÷ 360)

($48,000 × 5% × 90 ÷ 360)

CHAPTER 9 Receivables

Prob. 9-5B

Mar. 8 Notes Receivable 33,000

Accounts Receivable 33,000

16 Notes Receivable 72,000

Accounts Receivable 72,000

June 11 Notes Receivable 36,000

Accounts Receivable 36,000

July 26 Cash 36,270

Notes Receivable 36,000

Interest Revenue 270

Aug. 4 Notes Receivable 48,000

Accounts Receivable 48,000

CHAPTER 9 Receivables

Prob. 9-6B

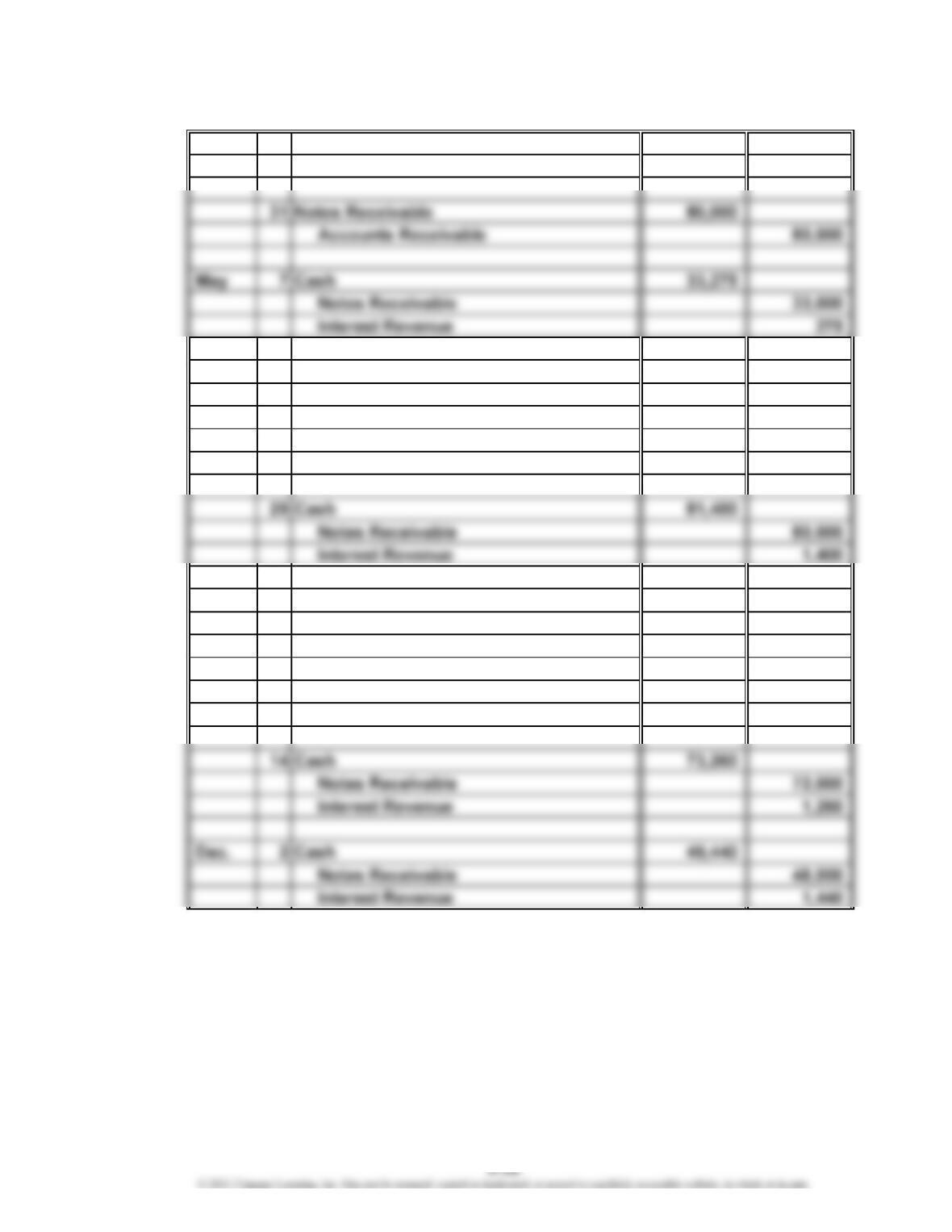

Jan. 21 Accounts Receivable—Black Tie Co. 28,000

Sales 28,000

May 17 Cash 28,280

Notes Receivable 28,000

Interest Revenue 280

($28,000 × 6% × 60 ÷ 360).

June 15 Accounts Receivable—Pioneer Co. 17,700

Sales 17,700

25 Cash 17,700

Accounts Receivable—Pioneer Co. 17,700

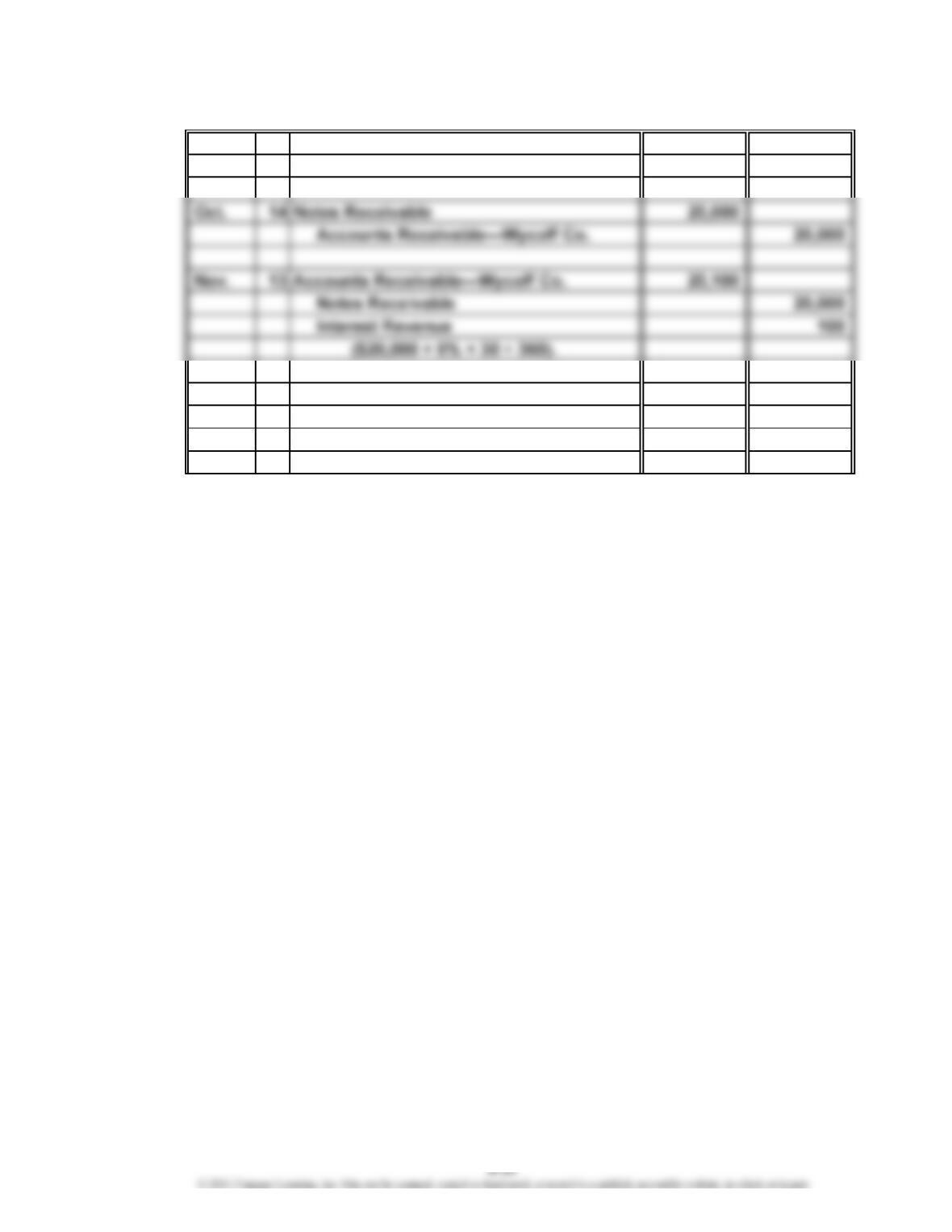

July 21 Notes Receivable 18,000

Cash 120

Notes Receivable 18,000

Interest Revenue 120

($18,000 × 8% × 30 ÷ 360).

CHAPTER 9 Receivables

Prob. 9-6B (Concluded)

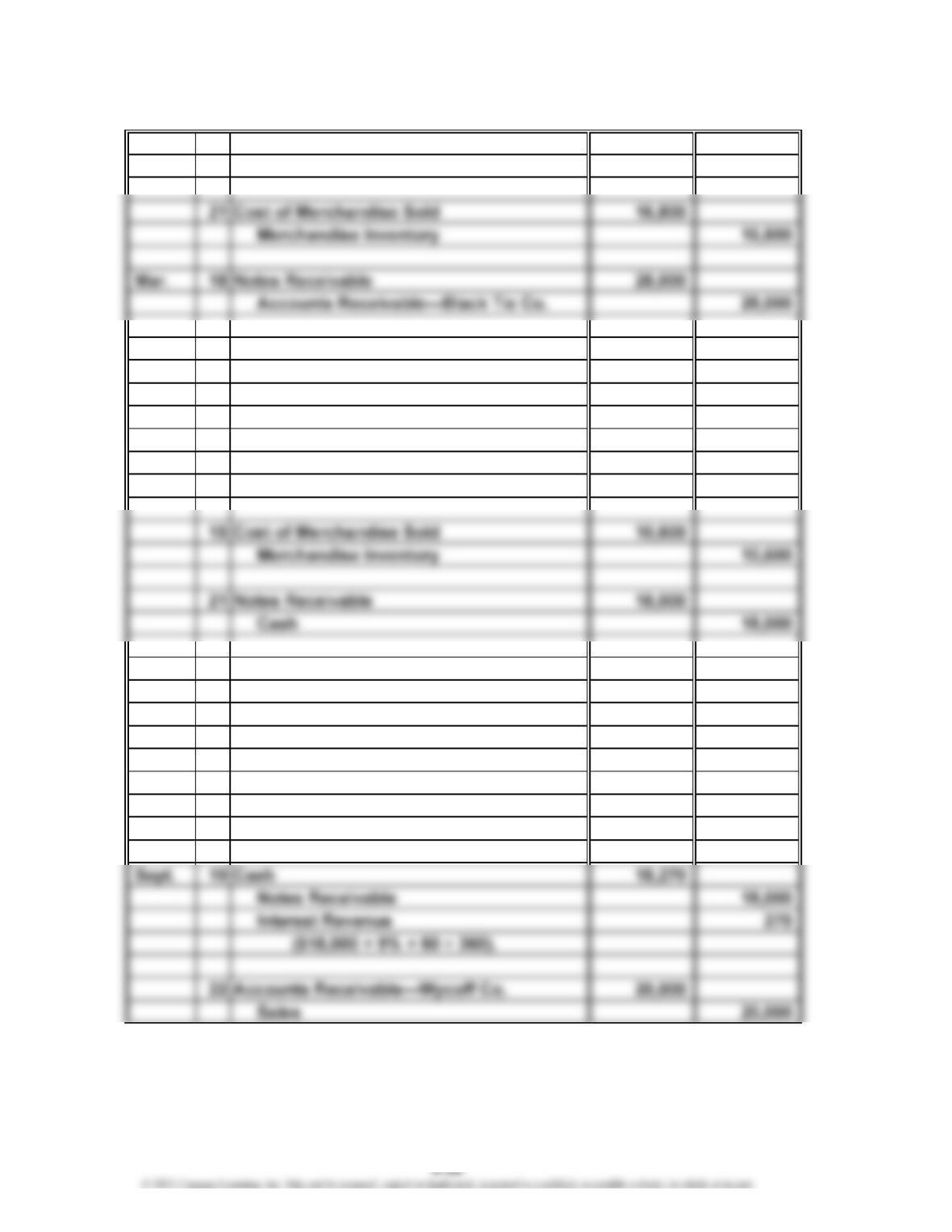

Sept. 22 Cost of Merchandise Sold 12,000

Merchandise Inventory 12,000

Dec. 28 Cash 20,301

Accounts Receivable—Wycoff Co. 20,100

Interest Revenue 201

($20,100 × 8% × 45 ÷ 360).

CHAPTER 9 Receivables

CP 9-1

Estimates of uncollectible accounts receivable create a unique financial reporting

challenge. Because the company does not know with certainty the amount of accounts

receivable that will be uncollectible, there is no “correct” estimate. The company must

use its judgment along with historical data to develop an estimate that fairly presents the

portion of credit sales that will become uncollectible. These estimates are required

under GAAP and should be representationally faithful and accurately match bad debt

expense to revenues generated from credit sales.

CP 9-2

By computing interest using a 365-day year for depository accounts (liabilities), Bev is

minimizing interest expense to the bank. By computing interest using a 360-day year

CP 9-3

A sample solution based on Nike Inc.’s Form 10-K for the fiscal year ended May 31, 2018,

follows:

1. a. $3,498 million (from balance sheet)

b. $30 million (Note 1)

2. The company’s receivables turnover has improved from 9.9 in 2017 to 10.1 in 2018,

as shown below.

2018 2017

Sales……………………………………………………

…

$ 36,397 $ 34,350

Beginning accounts receivable……………………

…

$ 3,677 $ 3,241

Ending accounts receivable………………………

…

3,498 3,677

CASES & PROJECTS

CHAPTER 9 Receivables

CP 9-4

To: Todd Hurley, CEO

From: A+ Student

Re: Allowance Method for Uncollectible Accounts

Accounts receivable result from the sale of goods to customers on account. Because

payment is received from customers after goods are delivered, there is a risk that

customers will default on their accounts. While the company does not know which

customers will default, it does have historical information on the portion of accounts

receivable that has become uncollectible in the past. The allowance method uses this

Bad Debt Expense XXX

Allowance for Doubtful Accounts XXX

This adjusting entry affects both the income statement and balance sheet. On the

income statement, bad debt expense is matched against the revenues generated

by the accounts receivable. On the balance sheet, the accounts receivable balance is

reduced by the allowance for doubtful accounts, which is the portion of the accounts

receivable that the company does not expect to collect. This resulting number is the

amount of accounts receivable that the company expects to collect, called the net

realizable value of the receivables.

CHAPTER 9 Receivables

CP 9-5

1. a.

Addition to Allowance

for Doubtful Accounts

$20,000 $15,000 ($20,000 – $5,000)

22,000 18,750 ($5,000 + $22,000 – $8,250)

2. a. The estimate of 1/2 of 1% of credit sales may be too large because the allowance

for doubtful accounts has steadily increased each year. The increasing balance

of the allowance for doubtful accounts may also be due to the failure to write

off a large number of uncollectible accounts. These possibilities could be

evaluated by examining the accounts in the accounts receivable subsidiary

ledger for collectibility and comparing the result with the balance in the

allowance for doubtful accounts.

b. The balance of Allowance for Doubtful Accounts that should exist at

December 31, 20Y7, can only be determined after all attempts have been

made to collect the receivables on hand at December 31, 20Y7. However,

the account balances at December 31, 20Y7, could be analyzed, perhaps

using an aging schedule, to determine a reasonable amount of allowance

and to determine accounts that should be written off. Also, past write-offs

of uncollectible accounts could be analyzed in depth in order to develop a

reasonable percentage for future adjusting entries, based on past history.

Caution, however, must be exercised in using historical percentages.

20Y5

b.

Accounts Written

Year Off During Year

20Y4

CHAPTER 9 Receivables

CP 9-6

1. and 2.

Sales…………………………………

Average accts. receivable………

…

Accts. receivable turnover………

…

The days’ sales in receivables could also be computed by dividing 365 days by

the accounts receivable turnover as follows:

Year 2: 8.8 (365 days ÷ 41.55)

Year 1: 10.4 (365 days ÷ 35.18)

3. The accounts receivable turnover indicates an increase in the efficiency of

collecting accounts receivable by increasing from 35.18 to 41.55, a favorable

4. We assumed that the percentage of credit sales to total sales remains constant

from one period to the next and no major changes in operations occurred

between years. For example, if the percentage of credit sales to total sales is

$ 1,198$ 1,032

[($1,015 + $1,049) ÷ 2] [($1,049 + $1,347) ÷ 2]

35.1841.55

($42,879 ÷ $1,032) ($42,151 ÷ $1,198)

Year 2 Year 1

$42,879 $42,151

…

CP 9-7

1. and 2.

Sales…………………………………

Average accts. receivable………

…

…

The days’ sales in receivables could also be computed by dividing 365 days by

the accounts receivable turnover as follows:

Year 2: 28.2 (365 days ÷ 12.94)

Year 1: 26.8 (365 days ÷ 13.63)

3. The accounts receivable turnover indicates a decline in the efficiency of

collecting accounts receivable by decreasing from 13.63 to 12.94, an unfavorable

Year 2 Year 1

$265,595 $229,234

$ 20,530 $ 16,814

CHAPTER 9 Receivables

CP 9-8

1. and 2.

Sales…………………………………

Average accts. receivable………

…

The days’ sales in receivables could also be computed by dividing 365 days by

the accounts receivable turnover as follows:

Year 2: 4.1 (365 days ÷ 89.28)

Year 1: 3.9 (365 days ÷ 94.02)

3. The accounts receivable turnover indicates a slight decrease in the efficiency of

collecting accounts receivable by decreasing from 94.02 to 89.28, an unfavorable

4. Costco’s accounts receivable turnover would normally be higher than that of a

typical manufacturing company such as the Campbell Soup Company. This is

because many of Costco’s customers charge their purchases to credit cards

Year 2 Year 1

$138,434 $126,172

$ 1,550.5 $ 1,342.0

[($1,669 + $1,432) ÷ 2]

[($1,432 + $1,252) ÷ 2]

…

CP 9-9

1. Note to Instructors: The turnover ratios will vary over time. Recently, the various

turnover ratios (rounded to one decimal place) were as follows:

Alcoa Corp. …………………………

…

12.2

AutoZone, Inc. ………………………

…

40.6

Barnes & Noble, Inc. ………………

…

55.8

…

…

…

IBM ……………………………………

…

9.8

Kroger …………………………………

…

79.6

Procter & Gamble …………………… 13.8

Wal-Mart ………………………………

…

95.1

Whirlpool Corporation ……………

…

8.5

Based on the above ratios, the companies can be categorized as follows:

Alcoa Inc. AutoZone, Inc.

Caterpillar Barnes & Noble, Inc.

The Coca-Cola Company Delta Air Lines

2. The companies with accounts receivable turnover ratios above 15 are all companies

selling primarily to individual consumers. In contrast, companies with turnover

ratios below 15 are companies selling primarily to other businesses. Generally, we

would expect companies selling to individual consumers to have higher turnover

Below 15 Above 15

Accounts Receivable Turnover Ratio