Chapter 9

Plant Assets, Natural Resources, and Intangibles

Review Questions

1. Define property, plant, and equipment. Provide some examples.

Property, plant, and equipment are long-lived, tangible assets used in the operation of a business.

2. Plant assets are recorded at historical cost. What does the historical cost of a plant asset include?

3. How do land improvements differ from land?

4. What does the word capitalize mean?

Capitalize means that an asset account was debited (increased) because the company acquired an

asset. Capitalized assets, except for land, are depreciated over their useful lives.

5. What is a lump-sum purchase, and how is it accounted for?

6. What is the difference between a capital expenditure and a revenue expenditure? Give an example

of each.

A capital expenditure is debited to an asset account because it increases the asset’s capacity or

9-2

7. What is depreciation? Define useful life, residual value, and depreciable cost.

Depreciation is the allocation of a plant asset’s cost to expense over its useful life. Depreciation

8. Which depreciation method ignores residual value until the last year of depreciation? Why?

9. How does a business decide which depreciation method is best to use?

A business should match an asset’s expense against the revenue that the asset produces when

10. What is the depreciation method that is used for tax accounting purposes? How is it different than

the methods that are required by GAAP to be used for financial accounting purposes?

11. If a business changes the estimated useful life or estimated residual value of a plant asset, what must

the business do in regard to depreciation expense?

When a company makes an accounting change in estimate, generally accepted accounting principles

12. What financial statement are property, plant, and equipment reported on, and how?

Property, plant and equipment are reported at book value on the balance sheet. Companies may

9-3

13. How is discarding of a plant asset different from selling a plant asset?

14. How is gain or loss determined when disposing of plant assets? What situation constitutes a gain?

What situation constitutes a loss?

Gain or loss is determined by comparing the cash received and the market value of any other assets

15. What is a natural resource? What is the process by which businesses spread the allocation of a

natural resource’s cost over its usage?

16. What is an intangible asset? Provide some examples.

Intangible assets are assets that have no physical form. Instead, these assets convey special rights

17. What is the process by which businesses spread the allocation of an intangible asset’s cost over its

useful life?

18. What is goodwill? Is goodwill amortized? What happens if the value of goodwill has decreased at

the end of the year?

Goodwill is the excess of the cost of an acquired company over the sum of the market values of its

19. What does the asset turnover ratio measure, and how is it calculated?

20A. What does it mean if an exchange of plant assets has commercial substance? Are gains and losses

recorded on the books because of the exchange?

An exchange has commercial substance if the future cash flows change as a result of the

9-5

Short Exercises

S9-1 Determining the cost of an asset

Learning Objective 1

Highland Clothing purchased land, paying $96,000 cash and signing a $300,000 note payable. In

addition, Highland paid delinquent property tax of $1,100, title insurance costing $600, and $4,600 to

level the land and remove an unwanted building. Record the journal entry for purchase of the land.

SOLUTION

Purchase price of land

$ 396,000

Add related costs:

Property taxes in arrears

Title insurance

Removal of building

Total cost of land

$ 402,300

9-6

S9-2 Making a lump-sum asset purchase

Learning Objective 1

Concord Pet Care Clinic paid $210,000 for a group purchase of land, building, and equipment. At the

time of the acquisition, the land had a market value of $110,000, the building $88,000, and the

equipment $22,000. Journalize the lump-sum purchase of the three assets for a total cost of $210,000,

the amount for which the business signed a note payable.

SOLUTION

Asset

Market

Value

Percentage of Total Value

× Total

Purchase

Price

= Assigned

Cost of

Each Asset

Land

$ 110,000

$110,000 / $220,000 = 50%

× $210,000

= $ 105,000

S9-3 Computing first-year depreciation and book value

Learning Objective 2

On January 1, 2018, Air Canadians purchased a used airplane for $37,000,000. Air Canadians expects

the plane to remain useful for five years (4,000,000 miles) and to have a residual value of $5,000,000.

The company expects the plane to be flown 1,400,000 miles during the first year.

Requirements

1. Compute Air Canadians’s first-year depreciation expense on the plane using the following

methods:

a. Straight-line

b. Units-of-production

c. Double-declining-balance

2. Show the airplane’s book value at the end of the first year for all three methods.

Building

× $210,000

Equipment

× $210,000

Total

$ 220,000

Debit

9-7

SOLUTION

Requirement 1

a.

Straight-line

=

(Cost − Residual value) / Useful life

=

($37,000,000 ̶ $5,000,000) / 5 years

=

$6,400,000 per year

Requirement 2

Straight-line

Units-of-production

Double-declining-

balance

Cost

Less: Accumulated Depreciation

Book value

S9-4 Computing second-year depreciation and accumulated depreciation

Learning Objective 2

On January 1, 2018, Advanced Airline purchased a used airplane at a cost of $60,500,000. Advanced

Airline expects the plane to remain useful for eight years (5,000,000 miles) and to have a residual value

of $5,500,000. Advanced Airline expects the plane to be flown 1,100,000 miles the first year and

1,200,000 miles the second year.

Requirements

1. Compute second-year (2019) depreciation expense on the plane using the following methods:

a. Straight-line

b. Units-of-production

c. Double-declining-balance

2. Calculate the balance in Accumulated Depreciation at the end of the second year for all three

methods.

b.

Depreciation per unit

=

(Cost – Residual value) / Useful life in units

($37,000,000 ̶ $5,000,000) / 4,000,000 miles

=

$8 per mile

Units-of-production

=

Depreciation per unit × Current year usage

=

$8 per mile × 1,400,000 miles

=

$11,200,000 for year 1

c.

Double-declining-balance

=

(Cost – Accumulated depreciation) × 2 × (1 / Useful life)

=

($37,000,000 ̶ $0) × 2 × (1/ 5 years)

=

$14,800,000 for year 1

9-8

SOLUTION

Requirement 1

a.

Straight-line

=

(Cost − Residual value) / Useful life

=

($60,500,000 ̶ $5,500,000) / 8 years

Requirement 2

Straight-line

Units-of-

production

Double-declining-

balance

Depreciation Expense – Year 1

$ 6,875,000

$ 12,100,000

$ 15,125,000

Depreciation Expense – Year 2

Total Accumulated Depreciation

$ 25,300,000

$ 26,468,750

S9-5 Calculating partial-year depreciation

Learning Objective 2

On February 28, 2017, Rural Tech Support purchased a copy machine for $53,400. Rural Tech Support

expects the machine to last for six years and have a residual value of $3,000. Compute depreciation

expense on the machine for the year ended December 31, 2017, using the straight-line method.

=

b.

Depreciation per unit

=

(Cost – Residual value) / Useful life in units

($60,500,000 ̶ $5,500,000) / 5,000,000 miles

=

$11 per mile

Units-of-production

=

Depreciation per unit × Current year usage

=

$11 per mile × 1,100,000 miles

=

$12,100,000 in Year 1

=

Depreciation per unit × Current year usage

=

$11 per mile × 1,200,000 miles

=

c.

Double-declining-balance

=

(Cost – Accumulated depreciation) × 2 × (1 / Useful life)

=

($60,500,000 ̶ $0) × 2 × (1/ 8 years)

=

$15,125,000 in Year 1

=

(Cost – Accumulated depreciation) × 2 × (1 / Useful life)

=

($60,500,000 ̶ $15,125,000) × 2 × (1/ 8 years)

=

9-9

SOLUTION

Straight-line

=

(Cost − Residual value) / Useful life × (Number of Months / 12)

S9-6 Changing the estimated life of an asset

Learning Objective 2

Assume that Smith’s Auto Sales paid $45,000 for equipment with a 15-year life and zero expected

residual value. After using the equipment for six years, the company determines that the asset will

remain useful for only five more years.

Requirements

1. Record depreciation expense on the equipment for Year 7 by the straight-line method.

2. What is accumulated depreciation at the end of Year 7?

SOLUTION

Requirement 1

Straight-line

=

(Cost − Residual value) / Useful life

=

($45,000 ̶ $0) / 15 years

=

$3,000 per year

Accumulated depreciation after 6 years

=

$3,000 per year × 6 years

=

$18,000

Book value after 6 years

=

(Cost – Accumulated Depreciation)

=

$45,000 ̶ $18,000

=

$27,000

Revised depreciation

=

(Book value − Revised residual value) / Revised useful life remaining

($27,000 ̶ $0) / 5 years

=

$5,400 per year

=

($53,400 ̶ $3,000) / 6 years × (10/12)

=

$7,000

9-10

Requirement 2

Straight-line

Depreciation Expense – Years 1– 6

$ 18,000

S9-7 Discarding of a fully depreciated asset

Learning Objective 3

On June 15, 2017, Family Furniture discarded equipment that had a cost of $27,000, a residual value of

$0, and was fully depreciated. Journalize the disposal of the equipment.

SOLUTION

Date

Accounts and Explanation

Debit

Credit

June 15

Accumulated Depreciation—Equipment

27,000

27,000

S9-8 Discarding an asset

Learning Objective 3

On October 31, 2018, Alternative Landscapes discarded equipment that had a cost of $26,920.

Accumulated Depreciation as of December 31, 2017, was $25,000. Assume annual depreciation on the

equipment is $1,920. Journalize the partial-year depreciation expense and disposal of the equipment.

SOLUTION

Partial year depreciation = $1,920 × 10/12 = $1,600

Market value of assets received

Less: Book value of asset disposed of

Less: Accumulated Depreciation ($25,000 + $1,600)

Gain or (Loss)

Depreciation Expense – Year 7

Total Accumulated Depreciation

$ 23,400

9-11

Date

Accounts and Explanation

Debit

Credit

Oct. 31

Depreciation Expense—Equipment

1,600

Accumulated Depreciation—Equipment

1,600

S9-9 Selling an asset at gain or loss

Learning Objective 3

Alpha Communication purchased equipment on January 1, 2018, for $27,500. Suppose Alpha

Communication sold the equipment for $20,000 on December 31, 2020. Accumulated Depreciation as of

December 31, 2020, was $10,000. Journalize the sale of the equipment, assuming straight-line

depreciation was used.

SOLUTION

Market value of assets received

$ 20,000

Less: Book value of asset disposed of

Cost

Less: Accumulated Depreciation

17,500

Gain or (Loss)

Date

Debit

Credit

Dec. 31

Cash

Accumulated Depreciation—Equipment

Equipment

Gain on Disposal

2,500

S9-10 Selling an asset at gain or loss

Learning Objective 3

Peter Company purchased equipment on January 1, 2018, for $28,000. Suppose Peter Company sold the

equipment for $4,000 on December 31, 2019. Accumulated Depreciation as of December 31, 2019, was

$11,000. Journalize the sale of the equipment, assuming straight-line depreciation was used.

Accumulated Depreciation—Equipment

Loss on Disposal

Equipment

9-12

SOLUTION

Market value of assets received

$ 4,000

S9-11 Accounting for depletion of natural resources

Learning Objective 4

Ajax Petroleum holds huge reserves of oil assets. Assume that at the end of 2018, Ajax Petroleum’s cost

of oil reserves totaled $27,000,000, representing 3,000,000 barrels of oil.

Requirements

1. Which method does Ajax Petroleum use to compute depletion?

2. Suppose Ajax Petroleum removed and sold 500,000 barrels of oil during 2019. Journalize depletion

expense for 2019.

SOLUTION

Requirement 1

Requirement 2

Depletion per unit

=

(Cost – Residual value) / Estimated total units

=

$9 per barrel

Depletion expense

=

Depletion per unit × Number of units extracted

=

$9 per barrel × 500,000 barrels

=

$4,500,000

Less: Book value of asset disposed of

Cost

$ 28,000

Less: Accumulated Depreciation

17,000

Gain or (Loss)

Date

Accounts and Explanation

Debit

Credit

S9-12 Accounting for an intangible asset

Learning Objective 5

On October 1, 2018, Modern Company purchased a patent for $153,600 cash. Although the patent gives

legal protection for 20 years, the patent is expected to be used for only eight years.

Requirements

1. Journalize the purchase of the patent.

2. Journalize the amortization expense for the year ended December 31, 2018. Assume straight-line

amortization.

SOLUTION

Requirement 1

Date

Accounts and Explanation

Debit

Credit

Requirement 2

Date

Accounts and Explanation

Debit

Credit

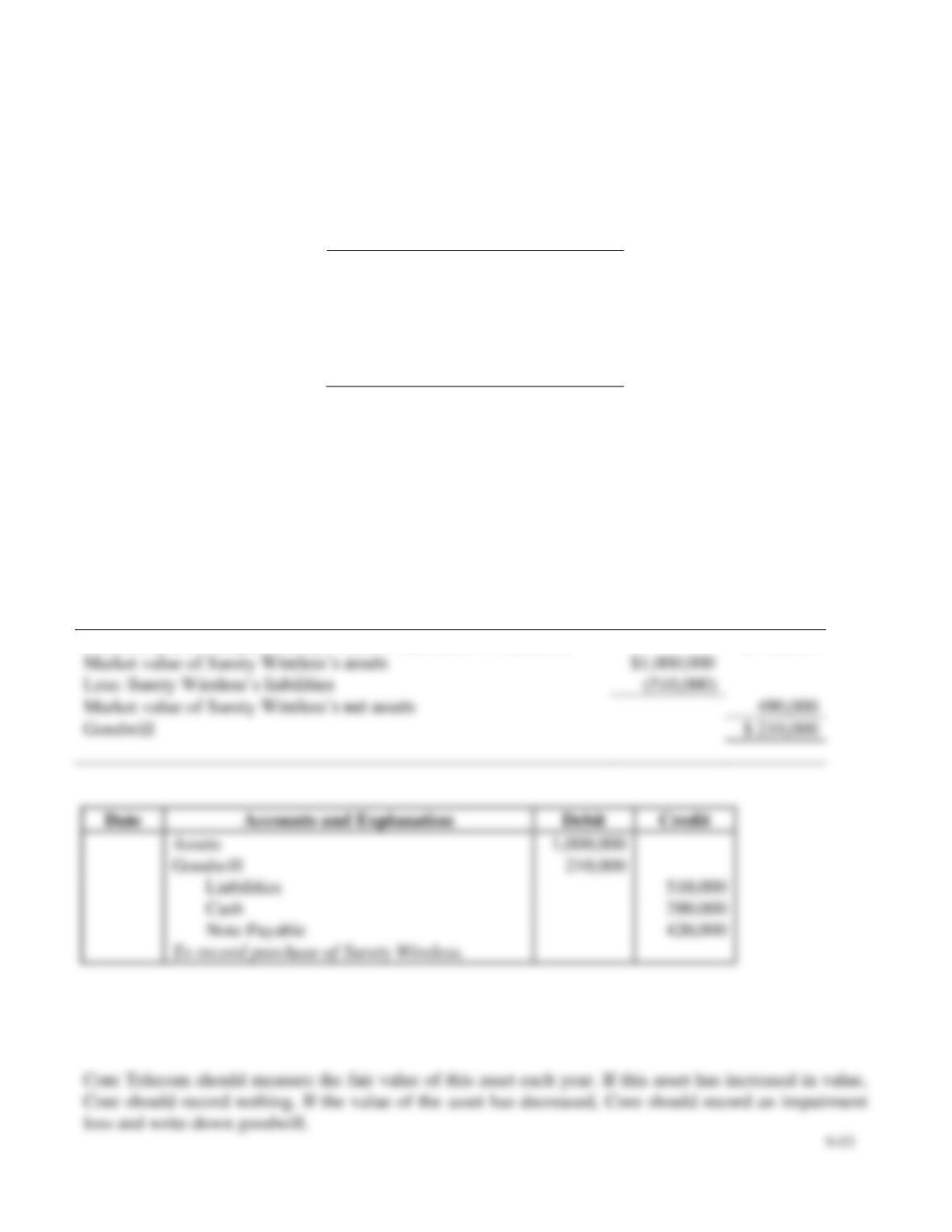

S9-13 Accounting for goodwill

Learning Objective 5

Decca Publishing paid $230,000 to acquire Thrifty Nickel, a weekly advertising paper. At the time of the

acquisition, Thrifty Nickel’s balance sheet reported total assets of $130,000 and liabilities of $70,000.

The fair market value of Thrifty Nickel’s assets was $100,000. The fair market value of Thrifty Nickel’s

liabilities was $70,000.

9-14

Requirements

1. How much goodwill did Decca Publishing purchase as part of the acquisition of Thrifty Nickel?

2. Journalize Decca Publishing’s acquisition of Thrifty Nickel.

SOLUTION

Requirement 1

Purchase price to acquire Thrifty Nickel

$ 230,000

Requirement 2

Date

Accounts and Explanation

Debit

Credit

Assets

100,000

Goodwill

200,000

230,000

S9-14 Computing the asset turnover ratio

Learning Objective 6

Biagas, Inc. had net sales of $55,600,000 for the year ended May 31, 2018. Its beginning and ending

total assets were $52,800,000 and $98,500,000, respectively. Determine Biagas’s asset turnover ratio for

year ended May 31, 2018.

SOLUTION:

Asset turnover ratio

=

Net sales / Average total assets

=

$55,600,000 / [($52,800,000 + $98,500,000) / 2]

=

$55,600,000 / $75,650,000

=

0.73 times (rounded)

Market value of Thrifty Nickel’s assets

Less: Thrifty Nickel’s liabilities

Market value of Thrifty Nickel’s net assets

Goodwill

$ 200,000

9-15

S9A-15 Exchanging plant assets

Learning Objective 7 Appendix 9A

Micron Precision, Inc. purchased a computer for $2,500, debiting Computer Equipment. During 2016

and 2017, Micron Precision, Inc. recorded total depreciation of $1,600 on the computer. On January 1,

2018, Micron Precision, Inc. traded in the computer for a new one, paying $2,100 cash. The fair market

value of the new computer is $3,900. Journalize Micron Precision, Inc.’s exchange of computers.

Assume the exchange had commercial substance.

SOLUTION

Market value of assets received

$ 3,900

Less:

Date

Accounts and Explanation

Debit

Credit

Jan. 1

Computer Equipment (new)

3,900

Accumulated Depreciation—Computer Equipment

1,600

2,500

2,100

S9A-16 Exchanging plant assets

Learning Objective 7 Appendix 9A

White Corporation purchased equipment for $22,000. White recorded total depreciation of $19,000 on

the equipment. On January 1, 2018, White traded in the equipment for new equipment, paying $23,200

cash. The fair market value of the new equipment is $25,100. Journalize White Corporation’s exchange

of equipment. Assume the exchange had commercial substance.

Cash paid

Gain or (Loss)

$ 900

SOLUTION

Market value of assets received

$ 25,100

Less:

Book value of asset exchanged

(19,000)

Cash paid

Gain or (Loss)

9-17

Exercises

E9-17 Determining the cost of assets

Learning Objective 1

1. Land $333,000

Lawson Furniture purchased land, paying $65,000 cash and signing a $250,000 note payable. In

addition, Lawson paid delinquent property tax of $5,000, title insurance costing $4,000, and $9,000 to

level the land and remove an unwanted building. The company then constructed an office building at a

cost of $400,000. It also paid $54,000 for a fence around the property, $12,000 for a sign near the

entrance, and $8,000 for special lighting of the grounds.

Requirements

1. Determine the cost of the land, land improvements, and building.

2. Which of these assets will Lawson depreciate?

SOLUTION

Requirement 1

Land

Requirement 2

E9-18 Making a lump-sum purchase of assets

Learning Objective 1

Lot 3 $177,500

Maplewood Properties bought three lots in a subdivision for a lump-sum price. An independent

appraiser valued the lots as follows:

Lot

Appraised

Value

1

$ 144,000

2

96,000

3

240,000

Maplewood paid $355,000 in cash. Record the purchase in the journal, identifying each lot’s cost in a

separate Land account. Round decimals to two places, and use the computed percentages throughout.

SOLUTION

Asset

Market

Value

Percentage of Total Value

× Total

Purchase

Price

= Assigned

Cost of

Each Asset

Lot 1

$ 144,000

$144,000 / $480,000 = 30%

× $355,000

= $ 106,500

Lot 2

× $355,000

= 71,000

Lot 3

$240,000 / $480,000 = 50%

× $355,000

Total

$ 480,000

E9-19 Distinguishing capital expenditures from revenue expenditures

Learning Objective 1

Consider the following expenditures:

a. Purchase price.

b. Ordinary recurring repairs to keep the machinery in good

working order.

c. Lubrication before machinery is placed in service.

d. Periodic lubrication after machinery is placed in service.

e. Major overhaul to extend useful life by three years.

f. Sales tax paid on the purchase price.

g. Transportation and insurance while machinery is in transit from

seller to buyer.

h. Installation.

i. Training of personnel for initial operation of the machinery.

Classify each of the expenditures as a capital expenditure or a revenue expenditure related to machinery.

SOLUTION

a.

Capital expenditure

Revenue expenditure

c.

Capital expenditure

Revenue expenditure

e.

Capital expenditure

Capital expenditure

Capital expenditure

Capital expenditure

Capital expenditure

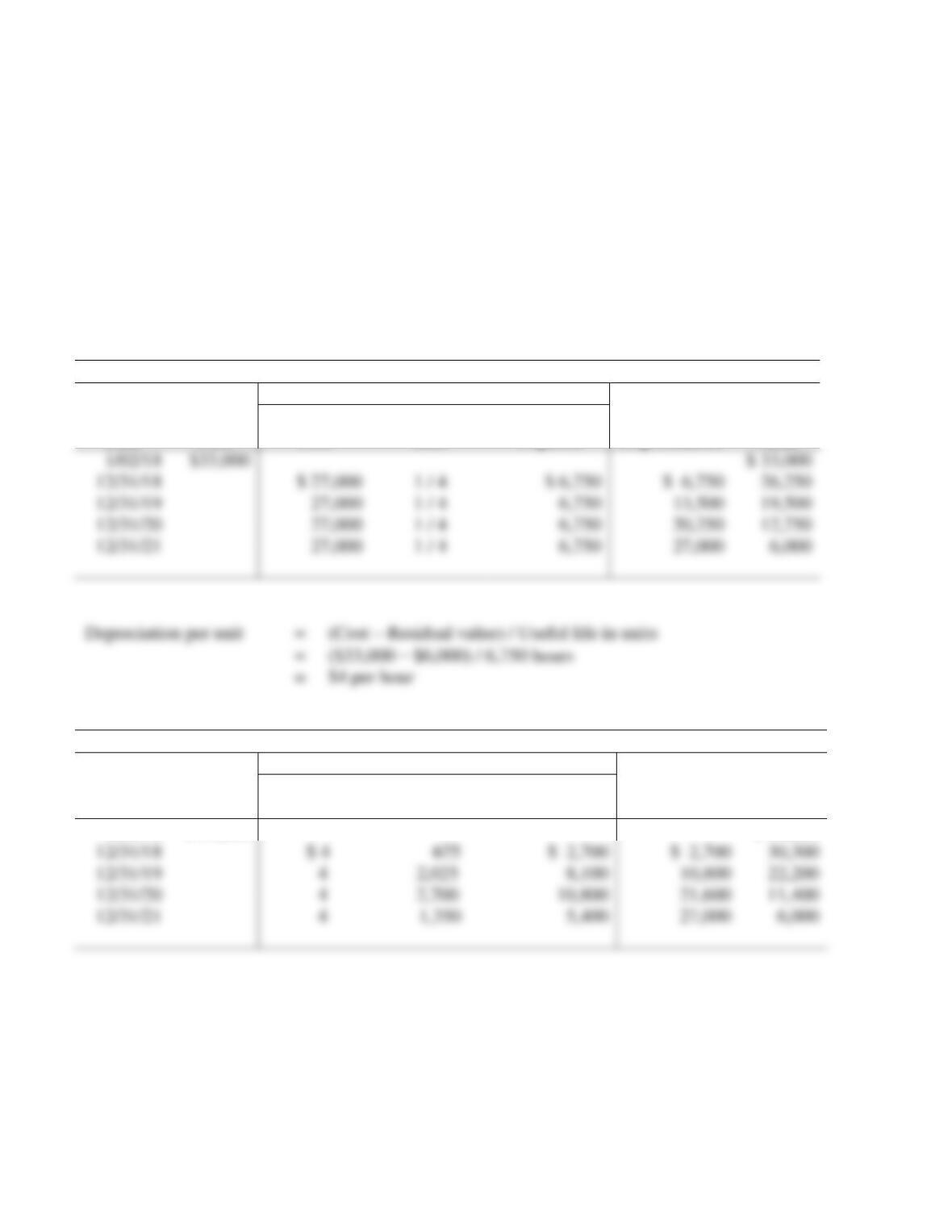

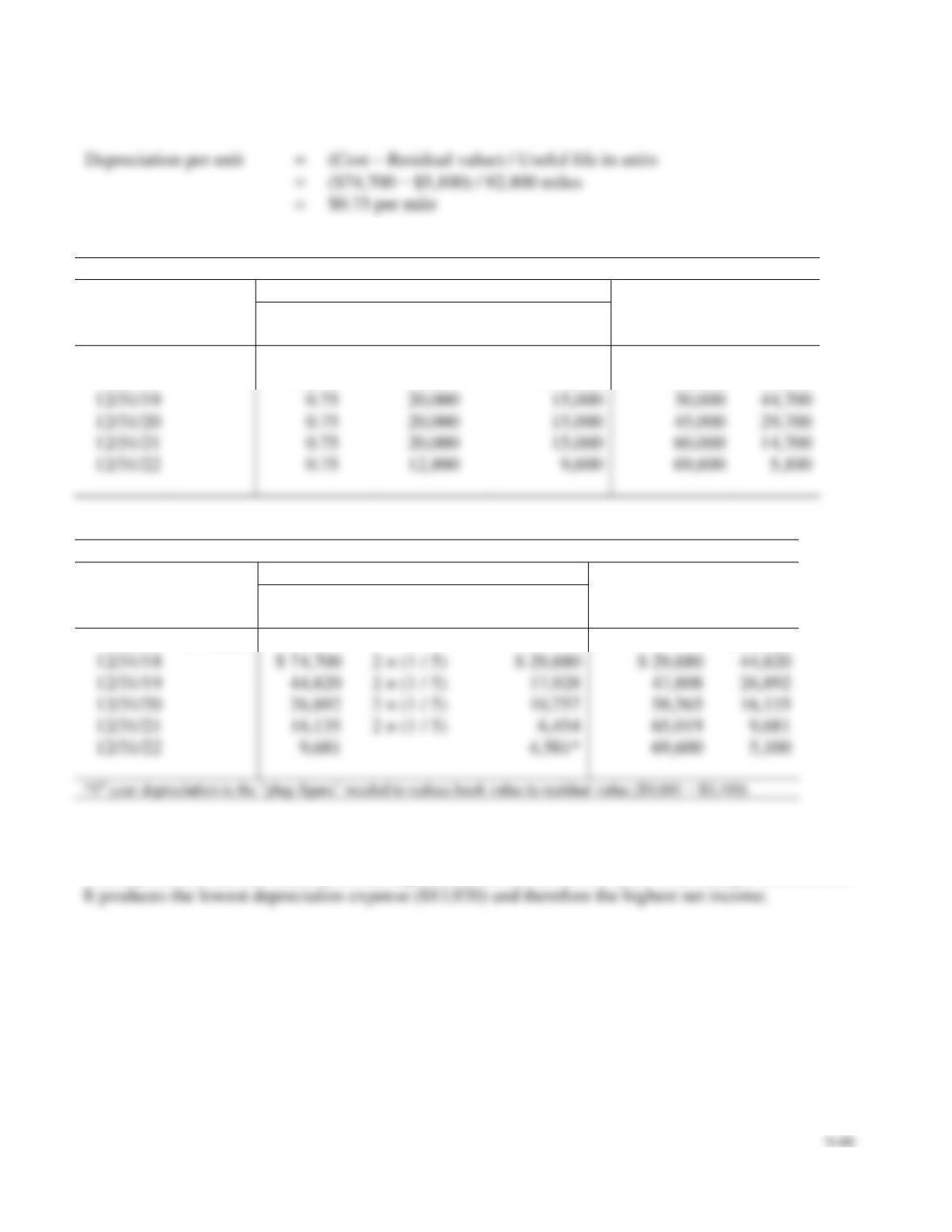

E9-20 Computing depreciation—three methods

Learning Objective 2

1. Double-declining-balance, 12/31/19, Exp. $8,250

Crispy Fried Chicken bought equipment on January 2, 2018, for $33,000. The equipment was expected

9-20

Requirements

1. Prepare a schedule of depreciation expense, accumulated depreciation, and book value per year for

the equipment under the three depreciation methods: straight-line, units-of-production, and double-

declining-balance. Show your computations. Note: Three depreciation schedules must be prepared.

2. Which method tracks the wear and tear on the equipment most closely?

SOLUTION

Requirement 1

Depreciable cost = Cost − Residual value = $33,000 − $6,000 = $27,000

Straight-Line Depreciation Schedule

Depreciation for the Year

Date

Asset

Cost

Depreciable

Cost

Depreciation

Rate

Depreciation

Expense

Accumulated

Depreciation

Book

Value

Depreciation per unit

=

(Cost – Residual value) / Useful life in units

=

$4 per hour

Units-of-Production Depreciation Schedule

Depreciation for the Year

Date

Asset

Cost

Depreciation

per Unit

Number

of Units

Depreciation

Expense

Accumulated

Depreciation

Book

Value

1/02/18

$ 33,000

$ 33,000

1/02/18

$33,000

$ 33,000

E9-20, cont.

Requirement 1, cont.

Double-Declining-Balance Depreciation Schedule

Depreciation for the Year

Date

Asset

Cost

Book

Value

DDB

Rate

Depreciation

Expense

Accumulated

Depreciation

Book

Value

1/02/18

$ 33,000

$ 33,000

Requirement 2

E9-21 Changing an asset’s useful life and residual value

Learning Objective 2

Yr. 16 $14,350

Salem Hardware Consultants purchased a building for $540,000 and depreciated it on a straight-line

basis over a 40-year period. The estimated residual value is $100,000. After using the building for 15

years, Salem realized that wear and tear on the building would wear it out before 40 years and that the

estimated residual value should be $88,000. Starting with the 16th year, Salem began depreciating the

building over a revised total life of 35 years using the new residual value. Journalize depreciation

expense on the building for years 15 and 16.

SOLUTION

Straight-line depreciation

=

(Cost − Residual value) / Useful life

=

Accumulated depreciation after 15 years

=

$11,000 per year × 15 years

=

$165,000

Book value after 15 years

=

(Cost – Accumulated Depreciation)

$540,000 ̶ $165,000

=

$375,000

Revised depreciation

=

(Book value − Revised residual value) / Revised useful life remaining

=

9-22

Date

Accounts and Explanation

Debit

Credit

Year 15

Depreciation Expense—Building

11,000

E9-22 Recording partial-year depreciation and sale of an asset

Learning Objectives 2, 3

Depr. Exp. $3,400

On January 2, 2017, Comfy Clothing Consignments purchased showroom fixtures for $17,000 cash,

expecting the fixtures to remain in service for five years. Comfy has depreciated the fixtures on a

double-declining-balance basis, with zero residual value. On October 31, 2018, Comfy sold the fixtures

for $7,600 cash. Record both depreciation expense for 2018 and sale of the fixtures on October 31,

2018.

SOLUTION

Double-declining-balance

=

(Cost – Accumulated depreciation) × 2 × (1 / Useful life)

($17,000 ̶ $0) × 2 × (1/5 years)

=

$6,800 in year 1

=

(Cost – Accumulated depreciation) × 2 × (1 / Useful life)

($17,000 ̶ $6,800) × 2 × (1/ 5 years) × 10/12

=

Market value of assets received

Less: Book value of asset disposed of

Cost

$ 17,000

Less: Accumulated Depreciation ($6,800 + $3,400)

Gain or (Loss)

Date

Accounts and Explanation

Debit

Credit

9-23

E9-23 Recording partial-year depreciation and sale of an asset

Learning Objectives 2, 3

Loss $(2,000)

On January 2, 2016, Pet Spa purchased fixtures for $37,800 cash, expecting the fixtures to remain in

service for six years. Pet Spa has depreciated the fixtures on a straight-line basis, with $9,000 residual

value. On May 31, 2018, Pet Spa sold the fixtures for $24,200 cash. Record both depreciation expense

for 2018 and sale of the fixtures on May 31, 2018.

SOLUTION

Straight-line depreciation

=

(Cost − Residual value) / Useful life

=

($37,800 ̶ $9,000) / 6 years

=

$4,800 per year (2016 and 2017)

Date

Accounts and Explanation

Debit

Credit

May 31

Depreciation Expense—Fixtures

2,000

Accumulated Depreciation—Fixtures

2,000

Cash

Accumulated Depreciation—Fixtures

Loss on Disposal

2,000

Fixtures

=

(Cost − Residual value) / Useful life

($37,800 ̶ $9,000) / 6 years × 5/12

=

Market value of assets received

Less: Book value of asset disposed of

Cost

$ 37,800

Less: Accumulated Depreciation ($4,800 + $4,800 + $2,000)

Gain or (Loss)

E9–24 Journalizing natural resource depletion

Learning Objective 4

$1.30 per ton

Cannon Mountain Mining paid $462,300 for the right to extract mineral assets from a 400,000-ton

deposit. In addition to the purchase price, Cannon also paid a $900 filing fee, a $1,800 license fee to the

state of Nevada, and $55,000 for a geological survey of the property. Because Cannon purchased the

rights to the minerals only and did not purchase the land, it expects the asset to have zero residual value.

During the first year, Cannon removed and sold 50,000 tons of the minerals. Make journal entries to

record (a) purchase of the minerals (debit Minerals), (b) payment of fees and other costs, and (c)

depletion for the first year.

SOLUTION

Purchase price of minerals

$ 462,300

Add related costs:

Filing fee

License

Geological survey

Total cost of minerals

$ 520,000

Depletion per unit

=

(Cost – Residual value) / Estimated total units

=

($520,000 ̶ $0) / 400,000 tons

=

$1.30 per ton

Depletion expense

=

Depletion per unit × Number of units extracted

=

$1.30 per ton × 50,000 tons

=

$65,000

9-25

E9-25 Handling acquisition of patent, amortization, and change in useful life

Learning Objectives 2, 5

2. Amort. Exp. $50,000

Melbourn Printers (MP) manufactures printers. Assume that MP recently paid $200,000 for a patent on a

new laser printer. Although it gives legal protection for 20 years, the patent is expected to provide a

competitive advantage for only eight years.

Requirements

1. Assuming the straight-line method of amortization, make journal entries to record (a) the purchase

of the patent and (b) amortization for the first full year.

2. After using the patent for four years, MP learns at an industry trade show that another company is

designing a more efficient printer. On the basis of this new information, MP decides, starting with

Year 5, to amortize the remaining cost of the patent over two remaining years, giving the patent a

total useful life of six years. Record amortization for Year 5.

SOLUTION

Requirement 1

Amortization expense

=

(Cost – Residual value) / Useful life

=

($200,000 ̶ $0) / 8 years

=

$25,000

9-26

Requirement 2

Accumulated amortization after 4 years

=

$25,000 per year × 4 years

=

$100,000

E9-26 Measuring and recording goodwill

Learning Objective 5

1. Goodwill $1,000,000

Princeton has acquired several other companies. Assume that Princeton purchased Kelleher for

$9,000,000 cash. The book value of Kelleher’s assets is $19,000,000 (market value, $20,000,000), and it

has liabilities of $12,000,000 (market value, $12,000,000).

Requirements

1. Compute the cost of the goodwill purchased by Princeton.

2. Record the purchase of Kelleher by Princeton.

SOLUTION

Requirement 1

Purchase price to acquire Kelleher

$ 9,000,000

Market value of Kelleher’s assets

$ 20,000,000

Less: Kelleher’s liabilities

Market value of Kelleher’s net assets

Goodwill

Book value after 4 years

=

(Cost – Accumulated Amortization)

$200,000 ̶ $100,000

=

$100,000

Revised amortization

=

(Book value − Revised residual value) / Revised useful life remaining

=

9-27

Requirement 2

Date

Accounts and Explanation

Debit

Credit

Assets

20,000,000

E9-27 Computing asset turnover ratio

Learning Objective 6

Blackerby Photo reported the following figures on its December 31, 2018, income statement and balance

sheet:

Net sales

$ 441,000

Dec. 31,

2018

Dec. 31,

2017

Cash

$ 31,000

$ 30,000

Accounts Receivable

68,000

65,000

Merchandise Inventory

80,000

79,000

Prepaid Expenses

16,000

5,000

Property, plant, and equipment,

net

175,000

18,000

Compute the asset turnover ratio for 2018 Round to two decimal places.

SOLUTION

Dec. 31, 2018

Dec. 31, 2017

Cash

$ 31,000

$ 30,000

Accounts Receivable

Merchandise Inventory

Prepaid Expenses

Property, plant, and equipment, net

Total Assets

Asset turnover ratio

Net sales / Average total assets

$441,000 / [($370,000 + $197,000) / 2]

$441,000 / $283,500

1.56 times (rounded)

Goodwill

12,000,000

9-28

E9A-28 Exchanging assets—two situations

Learning Objective 7 Appendix 9A

2. Loss $(7,000)

Partner Bank recently traded in office fixtures. Here are the facts:

Old fixtures:

New fixtures:

Cost, $91,000

Cash paid, $110,000

Accumulated depreciation,

$68,000

Market value,

$133,000

Requirements

1. Record Partner Bank’s trade-in of old fixtures for new ones. Assume the exchange had commercial

substance.

2. Now let’s change one fact. Partner Bank feels compelled to do business with Elm Furniture, a bank

customer, even though the bank can get the fixtures elsewhere at a better price. Partner Bank is

aware that the new fixtures’ market value is only $126,000. Record the trade-in. Assume the

exchange had commercial substance.

SOLUTION

Requirement 1

Market value of assets received

$133,000

Less:

Book value of asset exchanged

Cash paid

Gain or (Loss)

$ 0

9-29

Requirement 2

Market value of assets received

$ 126,000

Less:

E9A-29 Measuring asset cost, units-of-production depreciation, and asset trade

Learning Objectives 1, 2, 7 Appendix 9A

1. $11,880

Wimot Trucking Corporation uses the units-of-production depreciation method because units-of-

production best measures wear and tear on the trucks. Consider these facts about one Mack truck in the

company’s fleet.

When acquired in 2015, the rig cost $360,000 and was expected to remain in service for 10 years or

1,000,000 miles. Estimated residual value was $90,000. The truck was driven 80,000 miles in 2015,

120,000 miles in 2016, and 160,000 miles in 2017. After 44,000 miles, on March 15, 2018, the company

traded in the Mack truck for a less expensive Freightliner. Wimot also paid cash of $20,000. Fair market

value of the Mack truck was equal to its net book value on the date of the trade.

Requirements

1. Record the journal entry for depreciation expense in 2018.

2. Determine Wimot’s cost of the new truck.

3. Record the journal entry for the exchange of assets on March 15, 2018. Assume the exchange had

commercial substance.

Book value of asset exchanged

Cash paid

(133,000)

Gain or (Loss)

$ (7,000)

9-30

SOLUTION

Requirement 1

Depreciation per unit

=

(Cost – Residual value) / Useful life in units

=

$0.27 per mile

Units-of-production

=

Depreciation per unit × Current year usage

=

$0.27 per mile × 80,000 miles

=

$21,600 in 2015

=

Depreciation per unit × Current year usage

=

$0.27 per mile × 120,000 miles

=

$32,400 in 2016

=

Depreciation per unit × Current year usage

=

$0.27 per mile × 160,000 miles

=

$43,200 in 2017

=

Depreciation per unit × Current year usage

=

$0.27 per mile × 44,000 miles

=

$11,880 in 2018

Total accumulated depreciation

=

$21,600 + $32,400 + $43,200 + $11,880

=

$109,080

9-31

E9A-29, cont.

Requirement 2

Market value of assets received

$270,920

Requirement 3

Date

Accounts and Explanation

Debit

Credit

Mar. 15

Truck (new)

270,920

Accumulated Depreciation—Truck

109,080

360,000

Less:

Book value of asset exchanged

$ 360,000

Cash paid

Gain or (Loss)

9-32

Problems (Group A)

P9-30A Determining asset cost and recording partial-year depreciation, straight-line

Learning Objectives 1, 2

1. Bldg. $461,100

Discount Parking, near an airport, incurred the following costs to acquire land, make land

improvements, and construct and furnish a small building:

a. Purchase price of three acres of land

$

80,000

b. Delinquent real estate taxes on the land to be paid by Discount Parking

6,300

c. Additional dirt and earthmoving

9,000

d. Title insurance on the land acquisition

3,200

e. Fence around the boundary of the property

9,600

f. Building permit for the building

1,000

g. Architect’s fee for the design of the building

20,700

h. Signs near the front of the property

9,300

i. Materials used to construct the building

215,000

j. Labor to construct the building

175,000

k. Interest cost on construction loan for the building

9,400

l. Parking lots on the property

28,500

m. Lights for the parking lots

11,200

n. Salary of construction supervisor (80% to building; 20% to parking lot and concrete

walks)

50,000

o. Furniture

11,200

p. Transportation of furniture from seller to the building

2,200

q. Additional fencing

6,600

Discount Parking depreciates land improvements over 15 years, buildings over 40 years, and furniture

over 10 years, all on a straight-line basis with zero residual value.

Requirements

1. Set up columns for Land, Land Improvements, Building, and Furniture. Show how to account for

each cost by listing the cost under the correct account. Determine the total cost of each asset.

2. All construction was complete and the assets were placed in service on October 1. Record partial-

year depreciation expense for the year ended December 31. Round to the nearest dollar.

9-33

SOLUTION

Requirement 1

Land

Land

Improvements

Building

Furniture

Purchase price

$ 80,000

Real estate taxes

6,300

Requirement 2

Straight-line

=

(Cost − Residual value) / Useful life × (Number of Months / 12)

Land Improvements

=

($75,200 ̶ $0) / 15 years × (3/12)

=

$1,253 (rounded)

($461,100 ̶ $0) / 40 years × (3/12)

=

$2,882 (rounded)

Furniture

=

($13,400 ̶ $0) / 10 years × (3/12)

=

$335

Dirt and earthmoving

9,000

Title insurance

3,200

Fence

Building permit

$ 1,000

Architect’s fee

Signs

Building materials

Building labor

Interest on construction loan

Parking lots

Lights for parking lots

Salary of construction supervisor

Furniture

Transportation of furniture

Additional fencing

Totals

$ 461,100

9-34

P9-30A, cont.

Requirement 2, cont.

Date

Accounts and Explanation

Debit

Credit

Dec. 31

Depreciation Expense—Land Improvements

1,253

Accumulated Depreciation—Land Improvements

1,253

To record depreciation on land improvements.

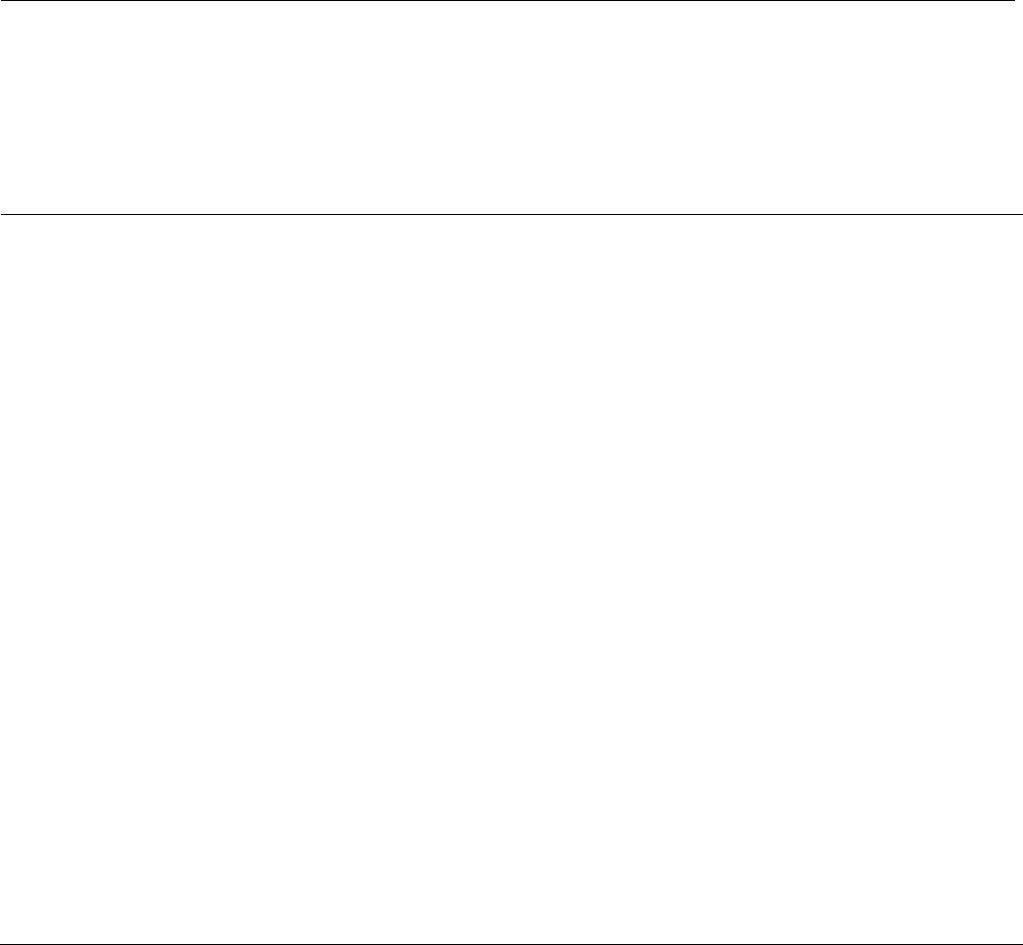

P9-31A Determining asset cost, preparing depreciation schedules (3 methods), and identifying

depreciation results that meet management objectives

Learning Objectives 1, 2

1. Units-of-production, 12/31/18, Dep. Exp. $24,000

On January 3, 2018, Rapid Delivery Service purchased a truck at a cost of $100,000. Before placing the

truck in service, Rapid spent $3,000 painting it, $600 replacing tires, and $10,400 overhauling the

engine. The truck should remain in service for five years and have a residual value of $12,000. The

truck’s annual mileage is expected to be 32,000 miles in each of the first four years and 8,000 miles in

the fifth year—136,000 miles in total. In deciding which depreciation method to use, Andy Sargeant, the

general manager, requests a depreciation schedule for each of the depreciation methods (straight-line,

units-of-production, and double-declining-balance).

Requirements

1. Prepare a depreciation schedule for each depreciation method, showing asset cost, depreciation

expense, accumulated depreciation, and asset book value.

2. Rapid prepares financial statements using the depreciation method that reports the highest net

income in the early years of asset use. Consider the first year that Rapid uses the truck. Identify the

depreciation method that meets the company’s objectives.

Depreciation Expense—Building

2,882

Accumulated Depreciation—Building

2,882

To record depreciation on building.

Depreciation Expense—Furniture

Accumulated Depreciation—Furniture

To record depreciation on furniture.

9-35

SOLUTION

Requirement 1

Purchase price of truck

$ 100,000

Depreciable cost = Cost − Residual value = $114,000 − $12,000 = $102,000

Straight-Line Depreciation Schedule

Depreciation for the Year

Date

Asset

Cost

Depreciable

Cost

Depreciation

Rate

Depreciation

Expense

Accumulated

Depreciation

Book

Value

1/03/18

$ 114,000

$ 114,000

Add related costs:

Painting

Tires

Engine overhaul

Total cost of truck

$ 114,000

Depreciation per unit

(Cost – Residual value) / Useful life in units

$0.75 per mile

P9-31A, cont.

Requirement 1, cont.

Units-of-Production Depreciation Schedule

Depreciation for the Year

Date

Asset

Cost

Depreciation

per Unit

Number

of Units

Depreciation

Expense

Accumulated

Depreciation

Book

Value

1/03/18

$ 114,000

$ 114,000

12/31/18

$ 0.75

32,000

$ 24,000

$ 24,000

90,000

12/31/19

0.75

32,000

66,000

12/31/20

0.75

32,000

42,000

12/31/21

0.75

32,000

18,000

12/31/22

0.75

8,000

12,000

Double-Declining-Balance Depreciation Schedule

Depreciation for the Year

Date

Asset

Cost

Book

Value

DDB

Rate

Depreciation

Expense

Accumulated

Depreciation

Book

Value

1/03/18

$ 114,000

$ 114,000

$ 114,000

$ 45,600

68,400

41,040

24,624

14,774

12,000

Requirement 2

The depreciation method that reports the highest net income in the first year is the straight-line method.

It produces the lowest depreciation expense ($20,400) and therefore the highest net income.

9-37

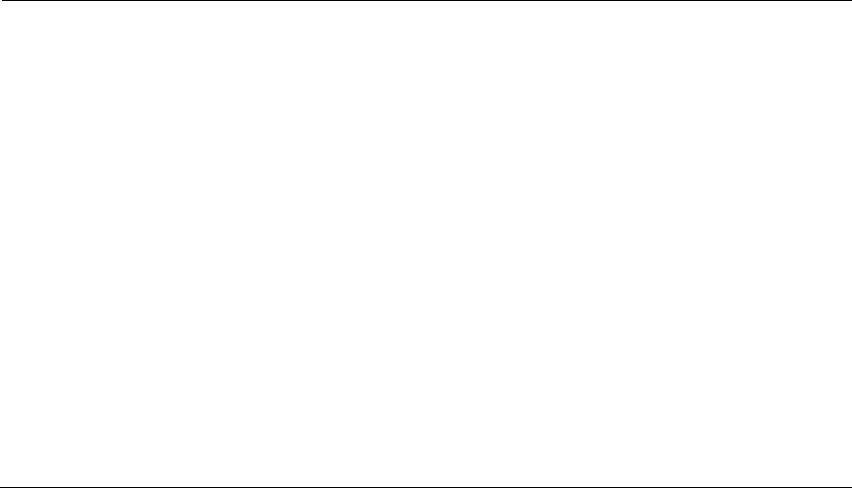

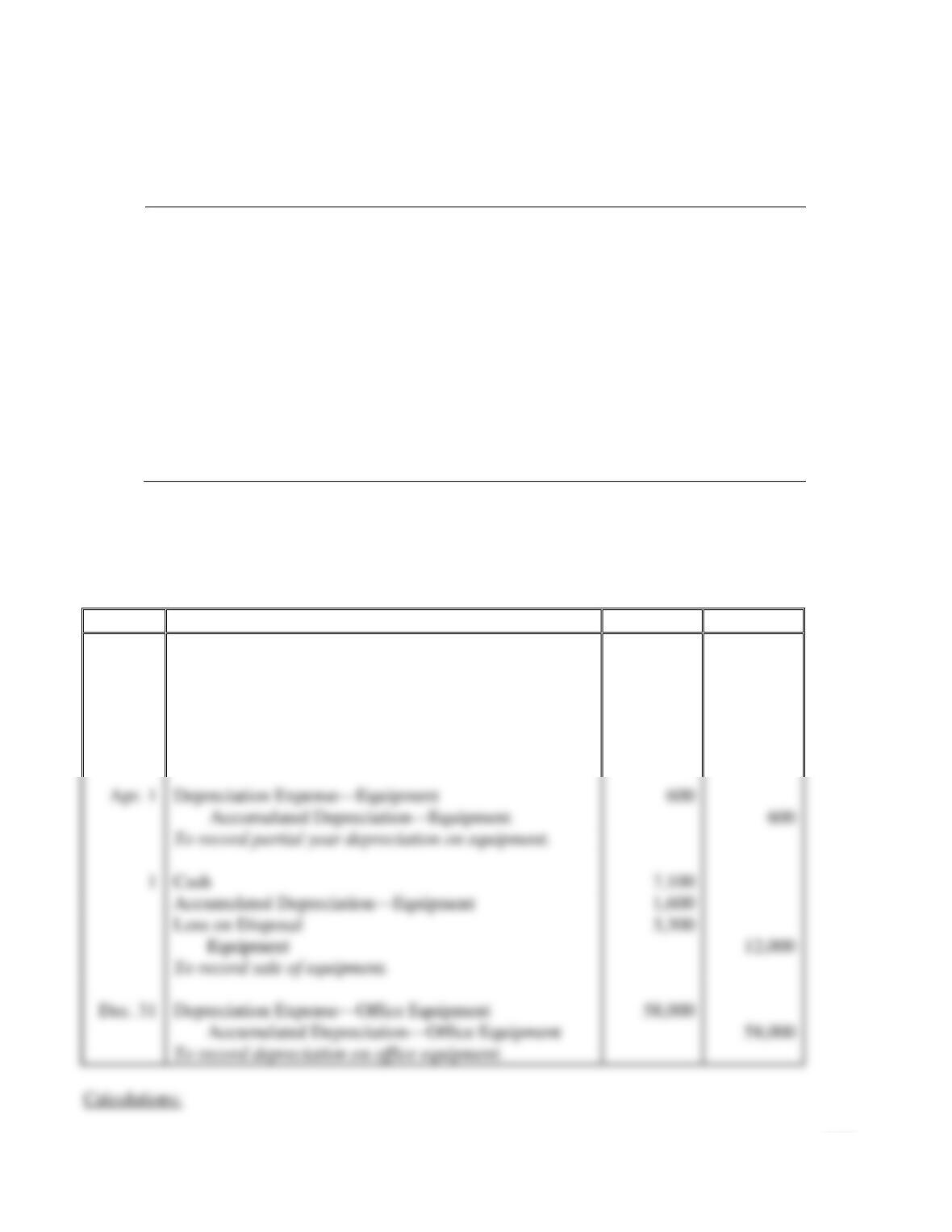

P9-32A Recording lump-sum asset purchases, depreciation, and disposals

Learning Objectives 1, 2, 3

Sep. 1 Gain $193,250

Ellie Johnson Associates surveys American eating habits. The company’s accounts include Land,

Buildings, Office Equipment, and Communication Equipment, with a separate Accumulated

Depreciation account for each depreciable asset. During 2018, Ellie Johnson Associates completed the

following transactions:

Jan. 1

Purchased office equipment, $113,000. Paid $80,000 cash and

financed the remainder with a note payable.

Apr. 1

Acquired land and communication equipment in a lump-sum purchase.

Total cost was $310,000 paid in cash. An independent appraisal valued

the land at $244,125 and the communication equipment at $81,375.

Sep. 1

Sold a building that cost $520,000 (accumulated depreciation of

$285,000 through December 31 of the preceding year). Ellie Johnson

Associates received $420,000 cash from the sale of the building.

Depreciation is computed on a straight-line basis. The building has a

40-year useful life and a residual value of $25,000.

Dec.

31

Recorded depreciation as follows:

Communication equipment is depreciated by the straight-line method

over a five-year life with zero residual value.

Office equipment is depreciated using the double-declining-balance

method over five years with a $1,000 residual value.

Record the transactions in the journal of Ellie Johnson Associates.

SOLUTION

9-38

Date

Accounts and Explanation

Debit

Credit

Jan. 1

Office Equipment

113,000

Cash

80,000

Note Payable

33,000

To record purchase of office equipment.

Calculations:

Apr. 1 – Acquisition of land and communication equipment:

Asset

Market

Value

Percentage of Total Value

× Total

Purchase

Price

= Assigned

Cost of

Each Asset

Land

$ 244,125

$244,125 / $325,500 = 75%

× $310,000

= $ 232,500

Comm. Equip.

$81,375 / $325,500 = 25%

× $310,000

= 77,500

Total

$ 325,500

Land

232,500

Communication Equipment

77,500

Cash

310,000

To record purchase of land and comm. equipment.

Depreciation Expense—Building

Accumulated Depreciation—Building

To record depreciation on building.

Cash

420,000

Accumulated Depreciation—Building

293,250

Building

520,000

Gain on Disposal

193,250

To record sale of building.

Dec. 31

Depreciation Expense—Communication Equipment

11,625

Accumulated Depreciation—Comm. Equipment

11,625

To record depreciation on communication equipment.

Depreciation Expense—Office Equipment

45,200

Accumulated Depreciation—Office Equipment

45,200

To record depreciation on office equipment.

P9-32A, cont.

Sep. 1 – Sale of building

Straight-line depreciation

=

(Cost − Residual value) / Useful life × (Number of Months / 12)

=

($520,000 ̶ $25,000) / 40 years × 8/12

=

$8,250 per partial year (2018)

Market value of assets received

$ 420,000

Less: Book value of asset disposed of

Cost

$ 520,000

Less: Accumulated Depreciation ($285,000 + $8,250)

(293,250)

226,750

Gain or (Loss)

$ 193,250

Dec. 31 – Depreciation on communication equipment

Straight-line depreciation

=

(Cost − Residual value) / Useful life × (Number of Months / 12)

=

($77,500 ̶ $0) / 5 years × 9/12

=

$11,625 per partial year (2018)

Dec. 31 – Depreciation on office equipment

Double-declining-balance depreciation

=

(Cost – Accumulated depreciation) × 2 × (1 / Useful life)

=

($113,000 ̶ $0) × 2 × (1/5 years)

=

$45,200 in 2018

P9-33A Accounting for natural resources

Learning Objective 4

Depl. Exp. $548,640

Conseco Oil, Inc. has an account titled Oil and Gas Properties. Conseco paid $6,600,000 for oil reserves

holding an estimated 1,000,000 barrels of oil. Assume the company paid $570,000 for additional

geological tests of the property and $450,000 to prepare for drilling. During the first year, Conseco

removed and sold 72,000 barrels of oil. Record all of Conseco’s transactions, including depletion for the

first year.

SOLUTION

Purchase price of oil reserves

$ 6,600,000

Add related costs:

Geological tests

Drilling preparation

Total cost of oil reserves

$ 7,620,000

Depletion per unit

=

(Cost – Residual value) / Estimated total units

=

($7,620,000 ̶ $0) / 1,000,000 barrels

=

$7.62 per barrel

Depletion expense

=

Depletion per unit × Number of units extracted

=

$7.62 per barrel × 72,000 barrels

=

$548,640

Date

Accounts and Explanation

Debit

Credit

Oil and Gas Properties

6,600,000

Cash

6,600,000

To record purchase of oil reserves.

Oil and Gas Properties

1,020,000

Cash

1,020,000

oil reserves.

Depletion Expense—Oil and Gas Properties

Accumulated Depletion—Oil and Gas Properties

To record depletion.

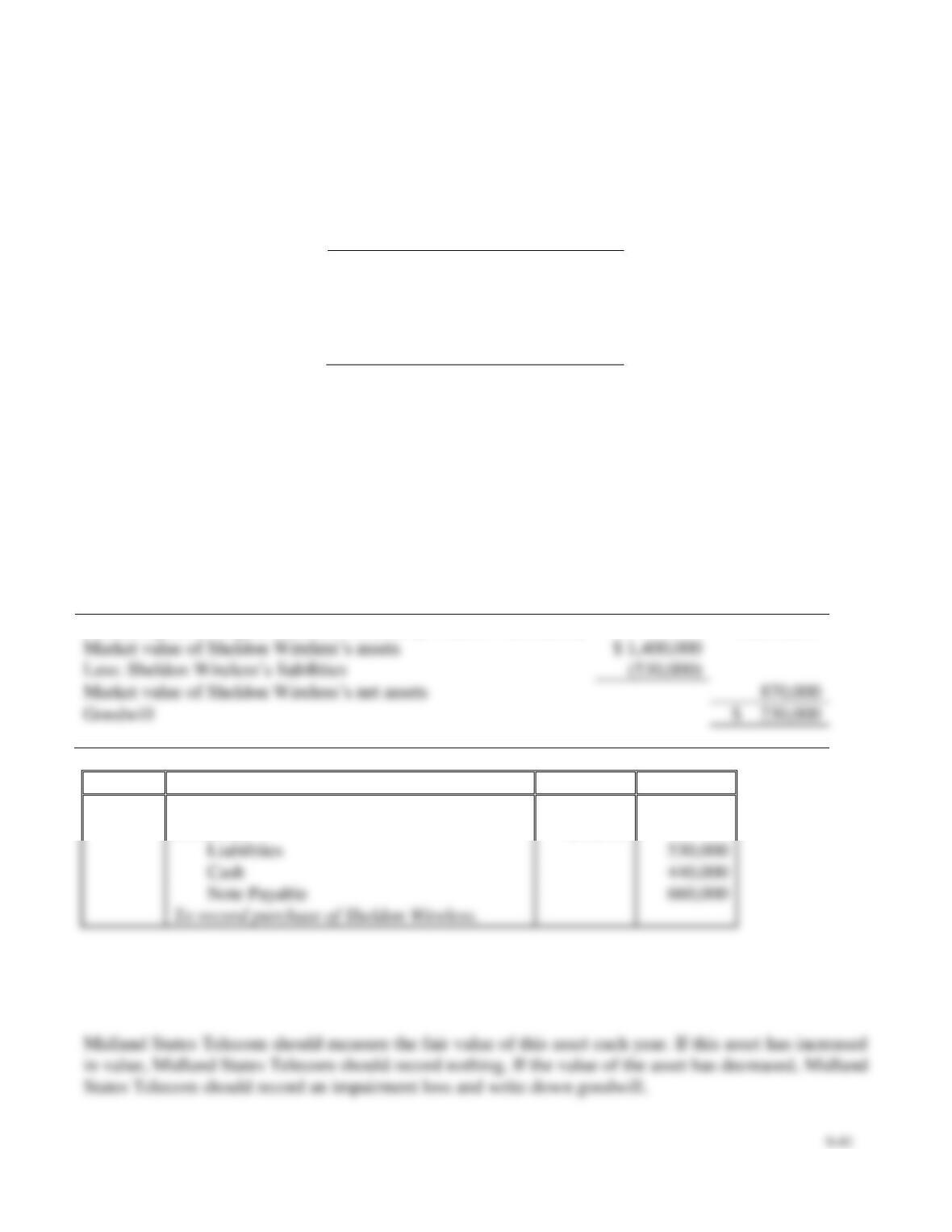

P9-34A Accounting for intangibles

Learning Objective 5

1. Goodwill $230,000

Midland States Telecom provides communication services in Iowa, Nebraska, the Dakotas, and

Montana. Midland States Telecom purchased goodwill as part of the acquisition of Sheldon Wireless

Enterprises, which had the following figures:

Book value of assets

$ 900,000

Market value of assets

1,400,000

Market value of

liabilities

530,000

Requirements

1. Journalize the entry to record Midland States Telecom’s purchase of Sheldon Wireless for

$440,000 cash plus a $660,000 note payable.

2. What special asset does Midland States Telecom’s acquisition of Sheldon Wireless identify? How

should Midland States Telecom account for this asset after acquiring Sheldon Wireless? Explain in

detail.

SOLUTION

Requirement 1

Purchase price to acquire Sheldon Wireless ($440,000 + $660,000)

$1,100,000

Market value of Sheldon Wireless’s assets

$ 1,400,000

Less: Sheldon Wireless’s liabilities

Market value of Sheldon Wireless’s net assets

Goodwill

Date

Accounts and Explanation

Debit

Credit

Assets

1,400,000

Goodwill

230,000

530,000

440,000

660,000

Requirement 2

The acquisition identifies the asset goodwill.

9-42

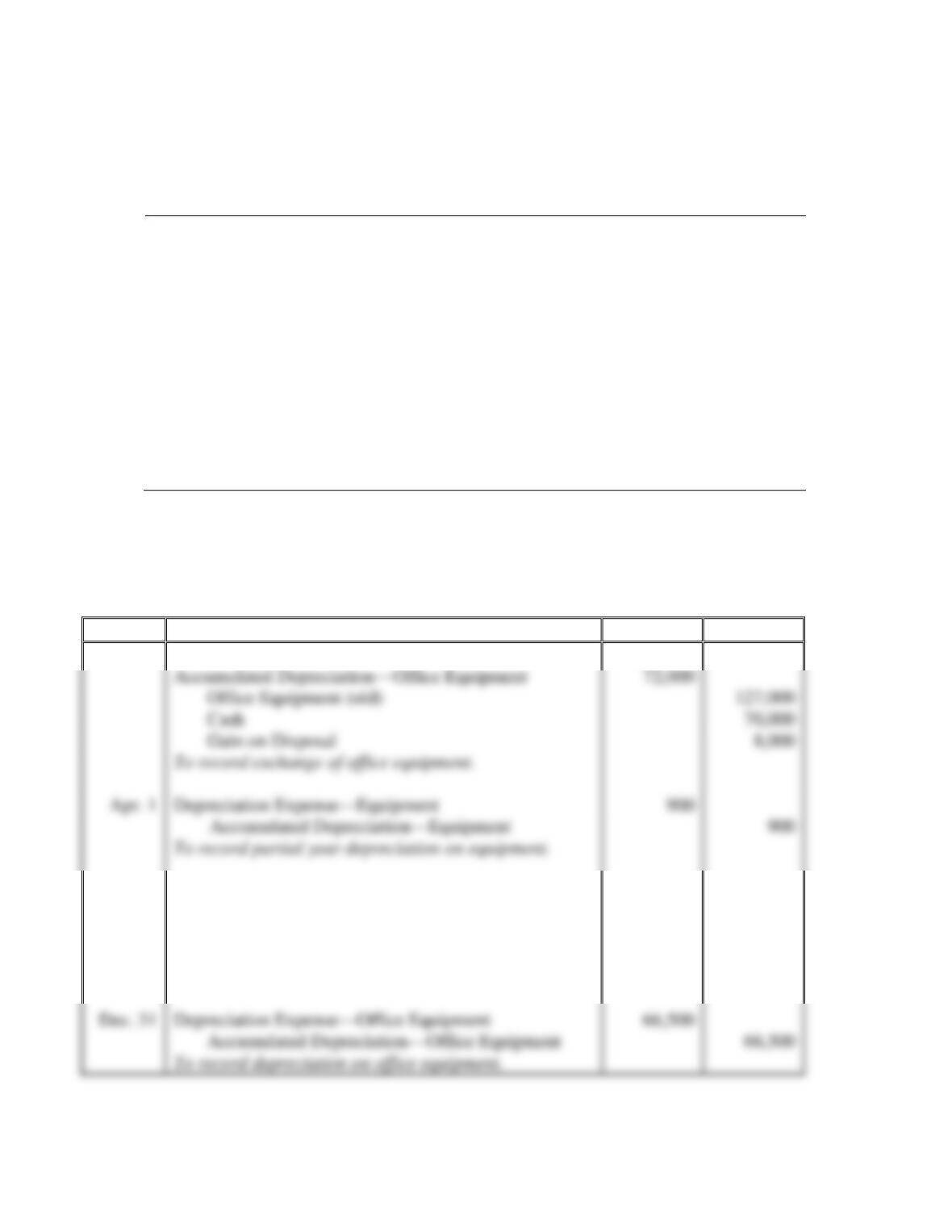

P9A-35A Journalizing partial-year depreciation and asset disposals and exchanges

Learning Objectives 2, 3, 7 Appendix 9A

Jan. 1 Gain $8,000

During 2018, Mora Corporation completed the following transactions:

Jan. 1

Traded in old office equipment with book value of $55,000 (cost of

$127,000 and accumulated depreciation of $72,000) for new equipment.

Mora also paid $70,000 in cash. Fair value of new equipment is $133,000.

Assume the exchange had commercial substance.

Apr. 1

Sold equipment that cost $18,000 (accumulated depreciation of $8,000

through December 31 of the preceding year). Mora received $6,100 cash

from the sale of the equipment. Depreciation is computed on a straight-line

basis. The equipment has a five-year useful life and a residual value of $0.

Dec.

31

Recorded depreciation as follows:

Office equipment is depreciated using the double-declining-balance method

over four years with a $9,000 residual value.

Record the transactions in the journal of Mora Corporation.

SOLUTION

Date

Accounts and Explanation

Debit

Credit

Jan. 1

Office Equipment (new)

133,000

1

Cash

6,100

Accumulated Depreciation—Equipment

8,900

Loss on Disposal

3,000

Equipment

18,000

To record sale of equipment.

Depreciation Expense—Office Equipment

66,500

Accumulated Depreciation—Office Equipment

66,500

To record depreciation on office equipment.

Accumulated Depreciation—Office Equipment

72,000

Office Equipment (old)

127,000

Cash

70,000

Gain on Disposal

8,000

To record exchange of office equipment.

Depreciation Expense—Equipment

9-43

Calculations:

Jan. 1 – Exchange of office equipment

Apr. 1 – Sale of equipment

Straight-line depreciation

=

(Cost − Residual value) / Useful life × (Number of Months / 12)

=

($18,000 ̶ $0) / 5 years × 3/12

=

$900 per partial year (2018)

Market value of assets received

Less: Book value of asset disposed of

Cost

$ 18,000

Less: Accumulated Depreciation ($8,000 + $900)

Gain or (Loss)

Double-declining-balance depreciation

=

(Cost – Accumulated depreciation) × 2 × (1 / Useful life)

=

($133,000 – $0) × 2 × (1/4 years)

=

$66,500

Dec. 31 – Depreciation on office equipment

Market value of assets received

Less:

Book value of asset exchanged

$ 127,000

Cash paid

Gain or (Loss)

9-44

Problems (Group B)

P9-36B Determining asset cost and recording partial-year depreciation

Learning Objectives 1, 2

1. Bldg. $483,500

Safe Parking, near an airport, incurred the following costs to acquire land, make land improvements, and

construct and furnish a small building:

a. Purchase price of three acres of land

$

86,000

b. Delinquent real estate taxes on the land to be paid by Safe Parking

6,300

c. Additional dirt and earthmoving

8,400

d. Title insurance on the land acquisition

3,400

e. Fence around the boundary of the property

9,600

f. Building permit for the building

900

g. Architect’s fee for the design of the building

20,100

h. Signs near the front of the property

9,000

i. Materials used to construct the building

217,000

j. Labor to construct the building

172,000

k. Interest cost on construction loan for the building

9,500

l. Parking lots on the property

29,400

m. Lights for the parking lots

11,600

n. Salary of construction supervisor (80% to building; 20% to parking lot and concrete

walks)

80,000

o. Furniture

11,700

p. Transportation of furniture from seller to the building

1,900

q. Additional fencing

6,900

Safe Parking depreciates land improvements over 15 years, buildings over 40 years, and furniture over

10 years, all on a straight-line basis with zero residual value.

Requirements

1. Set up columns for Land, Land Improvements, Building, and Furniture. Show how to account for

each cost by listing the cost under the correct account. Determine the total cost of each asset.

2. All construction was complete and the assets were placed in service on September 1. Record

partial-year depreciation expense for the year ended December 31. Round to the nearest dollar.

9-45

SOLUTION

Requirement 1

Land

Land

Improvements

Building

Furniture

Purchase price

$ 86,000

Requirement 2

Straight-line

=

(Cost − Residual value) / Useful life × (Number of Months / 12)

Land Improvements

=

($82,500 ̶ $0) / 15 years × (4/12)

=

$1,833 (rounded)

($483,500 ̶ $0) / 40 years × (4/12)

=

$4,029 (rounded)

Furniture

=

($13,600 ̶ $0) / 10 years × (4/12)

=

$453 (rounded)

Real estate taxes

Dirt and earthmoving

Title insurance

Fence

Building permit

Architect’s fee

Signs

Building materials

Building labor

Interest on construction loan

Parking lots

Lights for parking lots

Salary of construction supervisor

Furniture

Transportation of furniture

Additional fencing

Totals

$ 104,100

$ 483,500

9-46

P9-36B, cont.

Requirement 2, cont.

Date

Accounts and Explanation

Debit

Credit

Dec. 31

Depreciation Expense—Land Improvements

1,833

Accumulated Depreciation—Land Improvements

1,833

To record depreciation on land improvements.

P9-37B Determining asset cost, preparing depreciation schedules (3 methods), and identifying

depreciation results that meet management objectives

Learning Objectives 1, 2

1. Units-of-production, 12/31/18, Dep. Exp. $15,000

On January 3, 2018, Speedy Delivery Service purchased a truck at a cost of $67,000. Before placing the

truck in service, Speedy spent $3,000 painting it, $1,200 replacing tires, and $3,500 overhauling the

engine. The truck should remain in service for five years and have a residual value of $5,100. The

truck’s annual mileage is expected to be 20,000 miles in each of the first four years and 12,800 miles in

the fifth year—92,800 miles in total. In deciding which depreciation method to use, Alec Rivera, the

general manager, requests a depreciation schedule for each of the depreciation methods (straight-line,

units-of-production, and double-declining-balance).

Requirements

1. Prepare a depreciation schedule for each depreciation method, showing asset cost, depreciation

expense, accumulated depreciation, and asset book value.

2. Speedy prepares financial statements using the depreciation method that reports the highest net

income in the early years of asset use. Consider the first year that Speedy uses the truck. Identify

the depreciation method that meets the company’s objectives.

Depreciation Expense—Building

4,029

Accumulated Depreciation—Building

4,029

To record depreciation on building.

Depreciation Expense—Furniture

Accumulated Depreciation—Furniture

To record depreciation on furniture.

9-47

SOLUTION

Requirement 1

Purchase price of truck

$ 67,000

Depreciable cost = Cost − Residual value = $74,700 − $5,100 = $69,600

Straight-Line Depreciation Schedule

Depreciation for the Year

Date

Asset

Cost

Depreciable

Cost

Depreciation

Rate

Depreciation

Expense

Accumulated

Depreciation

Book

Value

1/03/18

$ 74,700

$ 74,700

Add related costs:

Painting

Tires

Engine overhaul

Total cost of truck

$ 74,700

Depreciation per unit

=

(Cost – Residual value) / Useful life in units

=

$0.75 per mile

P9-37B, cont.

Requirement 1, cont.

Units-of-Production Depreciation Schedule

Depreciation for the Year

Date

Asset

Cost

Depreciation

per Unit

Number

of Units

Depreciation

Expense

Accumulated

Depreciation

Book

Value

1/03/18

$ 74,700

$ 74,700

12/31/18

$ 0.75

20,000

$ 15,000

15,000

59,700

12/31/19

0.75

20,000

30,000

44,700

12/31/20

0.75

20,000

45,000

29,700

12/31/21

0.75

20,000

60,000

14,700

12/31/22

0.75

12,800

69,600

5,100

Double-Declining-Balance Depreciation Schedule

Depreciation for the Year

Date

Asset

Cost

Book

Value

DDB

Rate

Depreciation

Expense

Accumulated

Depreciation

Book

Value

1/03/18

$ 74,700

$ 74,700

$ 29,880

47,808

58,565

65,019

69,600

Requirement 2

The depreciation method that reports the highest net income in the first year is the straight-line method.

9-49

P9-38B Recording lump-sum asset purchases, depreciation, and disposals

Learning Objectives 1, 2, 3

Sep. 1 Gain $163,250

Whitney Plumb Associates surveys American eating habits. The company’s accounts include Land,

Buildings, Office Equipment, and Communication Equipment, with a separate Accumulated

Depreciation account for each asset. During 2018, Whitney Plumb completed the following transactions:

Jan. 1

Purchased office equipment, $117,000. Paid $77,000 cash and financed the

remainder with a note payable.

Apr. 1

Acquired land and communication equipment in a lump-sum purchase.

Total cost was $350,000 paid in cash. An independent appraisal valued the

land at $275,625 and the communication equipment at $91,875.

Sep. 1

Sold a building that cost $520,000 (accumulated depreciation of $285,000

through December 31 of the preceding year). Whitney Plumb received

$390,000 cash from the sale of the building. Depreciation is computed on a

straight-line basis. The building has a 40-year useful life and a residual

value of $25,000.

Dec.

31

Recorded depreciation as follows:

Communication equipment is depreciated by the straight-line method over a

five-year life with zero residual value.

Office equipment is depreciated using the double-declining-balance method

over five years with a $2,000 residual value.

Record the transactions in the journal of Whitney Plumb Associates.

9-50

SOLUTION

Date

Accounts and Explanation

Debit

Credit

Jan. 1

Office Equipment

117,000

Cash

77,000

Note Payable

40,000

To record purchase of office equipment.

Calculations:

Apr. 1 – Acquisition of land and communication equipment:

Asset

Market

Value

Percentage of Total Value

× Total

Purchase

Price

= Assigned

Cost of

Each Asset

$91,875 / $367,500 = 25%

Land

262,500

Communication Equipment

87,500

Cash

350,000

To record purchase of land and comm. equipment.

Depreciation Expense—Building

Accumulated Depreciation—Building

To record depreciation on building.

Cash

390,000

Accumulated Depreciation—Building

293,250

Building

520,000

Gain on Disposal

163,250

To record sale of building.

Depreciation Expense—Communication Equipment

13,125

Accumulated Depreciation—Comm. Equipment

13,125

To record depreciation on communication equipment.

Depreciation Expense—Office Equipment

46,800

Accumulated Depreciation—Office Equipment

46,800

To record depreciation on office equipment.

P9-38B, cont.

Sep. 1 – Sale of building

Straight-line depreciation

=

(Cost − Residual value) / Useful life × (Number of Months / 12)

=

($520,000 ̶ $25,000) / 40 years × 8/12

=

$8,250 per partial year (2018)

Market value of assets received

$ 390,000

Less: Book value of asset disposed of

Cost

$ 520,000

Less: Accumulated Depreciation ($285,000 + $8,250)

(293,250)

226,750

Gain or (Loss)

$ 163,250

Dec. 31 – Depreciation on communication equipment

Straight-line depreciation

=

(Cost − Residual value) / Useful life × (Number of Months / 12)

=

($87,500 ̶ $0) / 5 years × 9/12

=

$13,125 per partial year (2018)

Dec. 31 – Depreciation on office equipment

Double-declining-balance depreciation

=

(Cost – Accumulated depreciation) × 2 × (1 / Useful life)

=

($117,000 ̶ $0) × 2 × (1/5 years)

=

$46,800 in 2018

P9-39B Accounting for natural resources

Learning Objective 4

Depl. Exp. $1,383,750

Donahue Oil Incorporated has an account titled Oil and Gas Properties. Donahue paid $6,400,000 for oil

reserves holding an estimated 400,000 barrels of oil. Assume the company paid $510,000 for additional

geological tests of the property and $470,000 to prepare for drilling. During the first year, Donahue

removed and sold 75,000 barrels of oil. Record all of Donahue’s transactions, including depletion for the

first year.

SOLUTION

Purchase price of oil reserves

$ 6,400,000

Add related costs:

Geological tests

Drilling preparation

Total cost of oil reserves

$ 7,380,000

Depletion per unit

(Cost – Residual value) / Estimated total units

($7,380,000 ̶ $0) / 400,000 barrels

$18.45 per barrel

Depletion expense

Depletion per unit × Number of units extracted

$18.45 per barrel × 75,000 barrels

$1,383,750

Date

Accounts and Explanation

Debit

Credit

Oil and Gas Properties

6,400,000

Cash

6,400,000

To record purchase of oil reserves.

Oil and Gas Properties

Cash

oil reserves.

Depletion Expense—Oil and Gas Properties

1,383,750

Accumulated Depletion—Oil and Gas Properties

1,383,750

To record depletion.

P9-40B Accounting for intangibles

Learning Objective 5

1. Goodwill $210,000

Core Telecom provides communication services in Iowa, Nebraska, the Dakotas, and Montana. Core

purchased goodwill as part of the acquisition of Surety Wireless Company, which had the following

figures:

Book value of assets

$

700,000

Market value of assets

1,000,000

Market value of

liabilities

510,000

Requirements

1. Journalize the entry to record Core’s purchase of Surety Wireless for $280,000 cash plus a

$420,000 note payable.

2. What special asset does Core’s acquisition of Surety Wireless identify? How should Core

Telecom account for this asset after acquiring Surety Wireless? Explain in detail.

SOLUTION

Requirement 1

Purchase price to acquire Surety Wireless ($280,000 + $420,000)

$ 700,000

Requirement 2

The acquisition identifies the asset goodwill.

9-54

P9A-41B Journalizing partial-year depreciation and asset disposals and exchanges

Learning Objectives 2, 3, 7 Appendix 9

Jan. 1 Gain $6,000

During 2018, Lora Company completed the following transactions:

Jan. 1

Traded in old office equipment with book value of $55,000 (cost of

$129,000 and accumulated depreciation of $74,000) for new equipment.

Lora also paid $55,000 in cash. Fair value of new equipment is $116,000.

Assume the exchange had commercial substance.

Apr. 1

Sold equipment that cost $12,000 (accumulated depreciation of $1,000

through December 31 of the preceding year). Lora received $7,100 cash

from the sale of the equipment. Depreciation is computed on a straight-line

basis. The equipment has a five-year useful life and a residual value of $0.

Dec.

31

Recorded depreciation as follows:

Office equipment is depreciated using the double-declining-balance method

over four years with a $7,000 residual value.

Record the transactions in the journal of Lora Company.

SOLUTION

Date

Accounts and Explanation

Debit

Credit

Jan. 1

Office Equipment (new)

116,000

Accumulated Depreciation—Office Equipment

74,000

Office Equipment (old)

129,000

Cash

55,000

Gain on Disposal

6,000

To record exchange of office equipment.

Depreciation Expense—Equipment

Cash

7,100

Loss on Disposal

3,300

Equipment

12,000

To record sale of equipment.

Depreciation Expense—Office Equipment

58,000

Accumulated Depreciation—Office Equipment

58,000

To record depreciation on office equipment.

9-55

Jan. 1 – Exchange of office equipment

P9-41B, cont.

Apr. 1 – Sale of equipment

Straight-line depreciation

=

(Cost − Residual value) / Useful life × (Number of Months / 12)

=

($12,000 ̶ $0) / 5 years × 3/12

=

$600 per partial year (2018)

Market value of assets received

Less: Book value of asset disposed of

Cost

$ 12,000

Less: Accumulated Depreciation ($1,000 + $600)

Gain or (Loss)

Double-declining-balance depreciation

=

(Cost – Accumulated depreciation) × 2 × (1 / Useful life)

=

($116,000 – $0) × 2 × (1/4 years)

=

$58,000

Excel Skill Problem

P9-42 Using Excel to prepare depreciation schedules

Download an Excel template for this problem online in MyAccountingLab or at http://www.pearsonhighered.com/Horngren.

The Fraser River Corporation has purchased a new piece of factory equipment on January 1, 2018, and wishes to compare

three depreciation methods: straight-line, double-declining-balance, and units-of-production.

The equipment costs $400,000 and has an estimated useful life of four years, or 8,000 hours. At the end of four years, the

equipment is estimated to have a residual value of $20,000.

Requirements

1. Use Excel to prepare depreciation schedules for straight-line, double-declining-balance, and units-of-

production methods. Use cell references from the Data table.

2. Prepare a second depreciation schedule for double-declining-balance method, using the Excel function DDB.

The DDB function cannot be used in the last year of the asset’s useful life.

3. At December 31, 2018, Fraser River is trying to determine if it should sell the factory equipment. Fraser River

will only sell the factory equipment if the company earns a gain of at least $6,000. For each of the three

depreciation methods, what is the minimum amount that Fraser River will sell the factory equipment for in

order to have a gain of $6,000?

SOLUTION

The student templates for Using Excel are available online in MyAccountingLab in the Multimedia Library or at

tbd

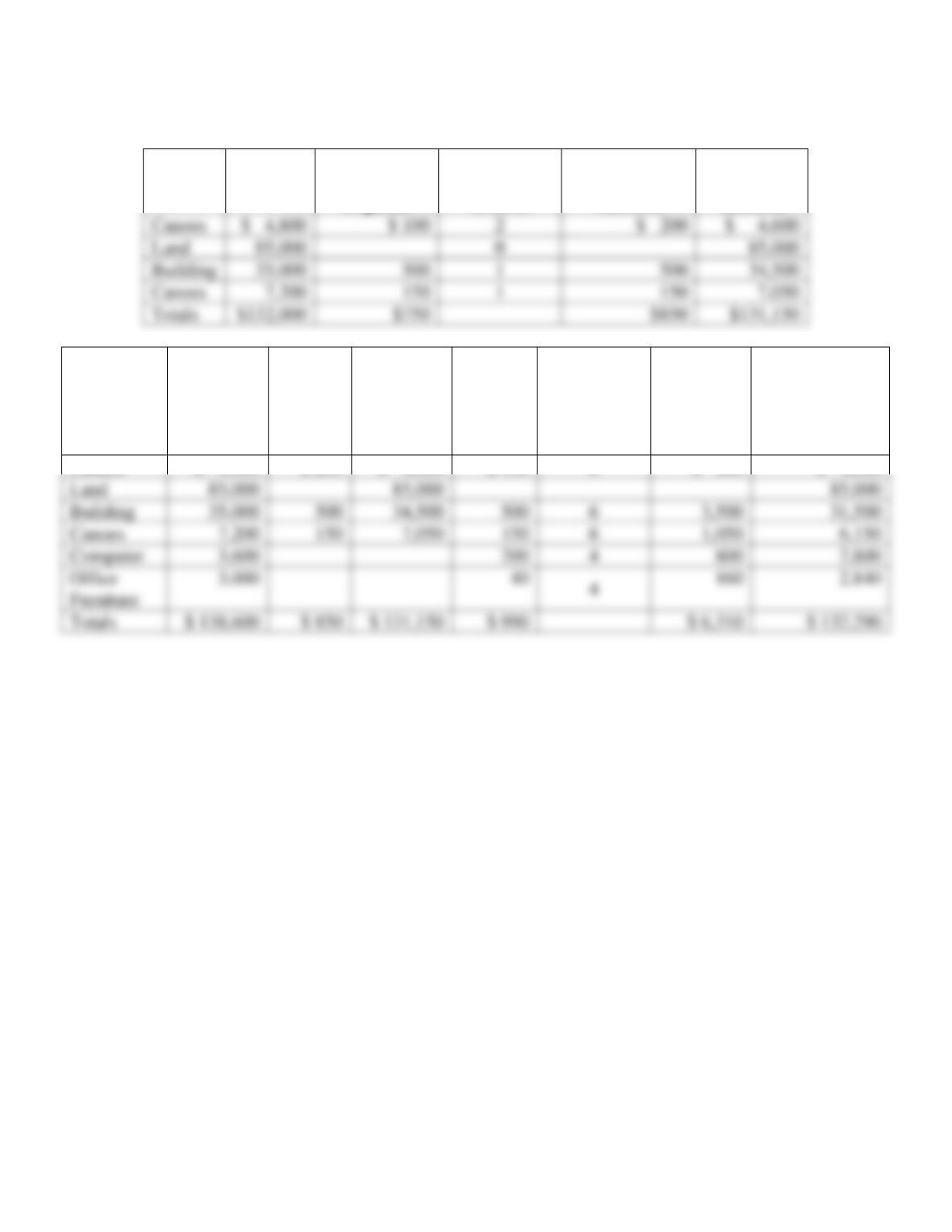

Continuing Problem

P9-43 Calculating and journalizing partial-year depreciation

This problem continues the Canyon Canoe Company situation from Chapter 8. Amber and Zack Wilson are

continuing to review business practices. Currently, they are reviewing the company’s property, plant, and

equipment and have gathered the following information:

Asset

Acquisition

Date

Cost

Estimated

Life

Estimated

Residual Value

Depreciation

Method*

Monthly

Depreciation

Expense

Canoes

Nov. 3, 2018

$

4,800

4 years

$ 0

SL

$ 100

Land

Dec. 1, 2018

85,000

n/a

Building

Dec. 1, 2018

35,000

5 years

5,000

SL

500

Canoes

Dec. 2, 2018

7,200

4 years

0

SL

150

Computer

Mar. 2, 2019

3,600

3 years

300

DDB

Office

Furniture

Mar. 3, 2019

3,000

5 years

600

SL

*

SL Straight-line; DDB Double-declining-balance==

Requirements

1. Calculate the amount of monthly depreciation expense for the computer and office furniture for 2019.

2. For each asset, determine the book value as of December 31, 2018. Then, calculate the depreciation expense

for the first six months of 2019 and the book value as of June 30, 2019.

3. Prepare a partial balance sheet showing Property, Plant, and Equipment as of June 30, 2019.

SOLUTION

Requirement 1

Monthly depreciation expense on Computer:

9-59

Requirement 2

Asset

Cost

Monthly

Depreciation

Expense

Months

Depreciated

in 2018

Accumulated

Depreciation

12/31/18

Book

Value

12/31/18

Asset

Cost

Accum.

Deprn.

12/31/18

Book

Value

12/31/18

Monthly

Deprn.

Expense

2019

Months

Depreciated

in 2019

(Jan. –

Jun.)

Accum.

Deprn.

6/30/19

Book

Value

6/30/19

Canoes

$ 4,800

$ 200

$ 4,600

$ 100

6

$ 800

$ 4,000

Land

85,000

85,000

Building

35,000

34,500

6

Canoes

6

Computer

4

800

Furniture

Totals

$ 850

$ 990

Canoes

Land

85,000

Building

34,500

Canoes

Totals

$131,150

9-60

P9-43, cont.

Requirement 3

CANYON CANOE COMPANY

Balance Sheet – Partial

June 30, 2019

Assets

Property, Plant, and Equipment:

Land

85,000

Building

Less: Accu. Depr.—Building

31,500

Canoes

12,000

Less: Accu. Depr.—Canoes

10,150

Computer

Less: Accu. Depr.—Computer

Office Furniture

Less: Accu. Depr.—Offc. Furn.

Total Property, Plant, and Equipment

9-61

Comprehensive Problem for Chapters 7-9

Top Quality Appliance—Long Beach has just purchased a franchise from Top Quality Appliance (TQA). TQA is

a manufacturer of kitchen appliances. TQA markets its products via retail stores that are operated as franchises.

As a TQA franchisee, Top Quality Appliance—Long Beach will receive many benefits, including having the

exclusive right to sell TQA brand appliances in Long Beach. TQA appliances have an excellent reputation and the

TQA name and logo are readily recognized by consumers. TQA also manages national television advertising

campaigns that benefit the franchisees. In exchange for these benefits, Top Quality Appliance—Long Beach will

pay an annual franchise fee to TQA based on a percentage of sales. The annual franchise fee is a separate cost and

in addition to the purchase of the franchise.

Top Quality Appliance—Long Beach

Chart of Accounts

Cash

Common Stock

Petty Cash

Retained Earnings

Accounts Receivable

Dividends

Allowance for Bad Debts

Sales Revenue

Merchandise Inventory

Interest Revenue

Office Supplies

Cost of Goods Sold

Prepaid Insurance

Franchise Fee Expense

Interest Receivable

Salaries Expense

Notes Receivable

Utilities Expense

Land

Insurance Expense

Building

Supplies Expense

Accumulated Depreciation—Building

Bad Debt Expense

Store Fixtures

Bank Expense

Accumulated Depreciation—Store Fixtures

Credit Card Expense

Office Equipment

Depreciation Expense—Building

Equipment

Franchise

Depreciation Expense—Office Equipment

Accounts Payable

Amortization Expense—Franchise

Interest Payable

Interest Expense

Notes Payable

Cash Short and Over

Top Quality Appliance—Long Beach completed the following transactions during 2018, its first year of

operations:

9-62

h.

Purchased appliances from TQA (merchandise inventory) on account for $425,000.

i.

Established a petty cash fund for $150.

j.

Sold appliances on account to B&B Contractors for $215,000, terms n/30 (cost, $86,000).

k.

Sold appliances to Davis Contracting for $150,000 (cost, $65,000), receiving a 6-month, 8% note.

l.

Recorded credit card sales of $80,000 (cost, $35,000), net of processor fee of 2%.

m.

Received payment in full from B&B Contractors.

n.

Purchased appliances from TQA on account for $650,000.

o.

Made payment on account to TQA, $300,000.

p.

Sold appliances for cash to LB Home Builders for $350,000 (cost, $175,000).

q.

Received payment in full on the maturity date from Davis Contracting for the note.

Sold appliances to Leard Contracting for $265,000 (cost, $130,000), receiving a 9–month, 8% note.

Made payment on account to TQA, $500,000.

Sold appliances on account to various businesses for $985,000, terms n/30 (cost, $395,000).

u.

Collected $715,000 cash on account.

v.

Paid cash for expenses: Salaries, $180,000; Utilities, $12,650

Replenished the petty cash fund when the fund had $62 in cash and petty cash tickets for $85 for office supplies.

x.

Paid dividends, $5,000.

Paid the franchise fee to TQA of 5% of total sales of $2,045,000.

Requirements

1. Record the transactions in the general journal. Omit explanations.

2. Post to the general ledger.

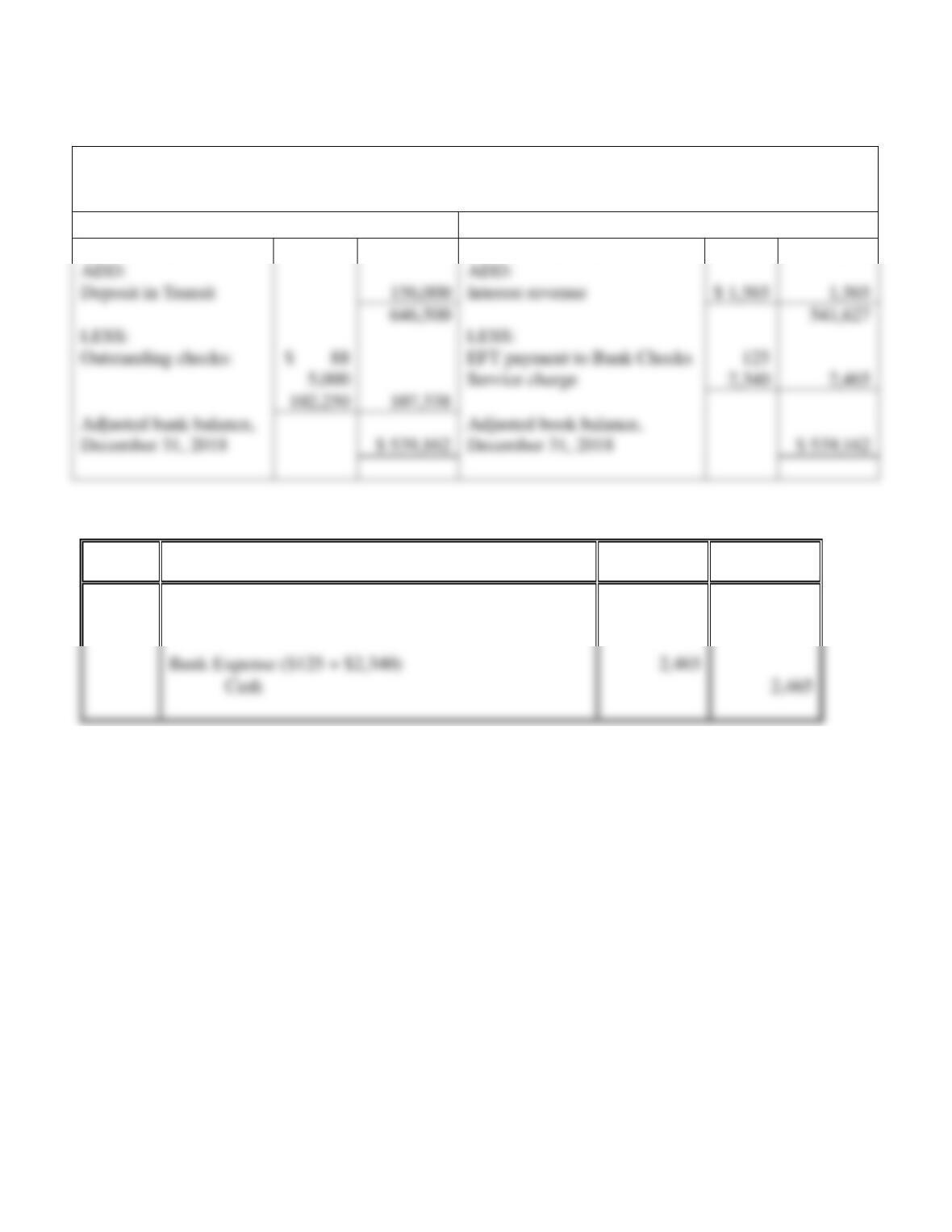

3. It is a common business practice to reconcile the bank accounts on a monthly basis. However, in this problem,

the reconciliation of the company’s checking account will be done at the end of the year, based on an annual

summary.

Reconcile the bank account by comparing the following annual summary statement from Long Beach National

Bank to the Cash account in the general ledger. Record journal entries as needed and post to the general ledger.

Use transaction z as the posting reference.

Beginning Balance, January 1, 2018

$ 0

Deposits and other credits:

$ 500,000

deposited the cash received from the stockholders.

b.

Paid $50,000 cash for a TQA franchise.

the following market values: Land, $100,000; Building, $500,000.

d.

Paid $75,000 for store fixtures.

Paid $45,000 for office equipment.

Paid $600 for office supplies.

g.

Paid $3,600 for a two-year insurance policy.

78,400

350,000

715,000

Interest Revenue

1,859,965

Checks and other debits:

125

Checks:

50,000

200,000

45,000

75,000

150

3,600

600

300,000

500,000

192,650

Bank service charge

2,340

(1,369,465)

Ending balance, December 31, 2018

$ 490,500

(1) Bank Checks is a company that prints business checks (considered a bank expense) for Top Quality Appliance—Long

Beach

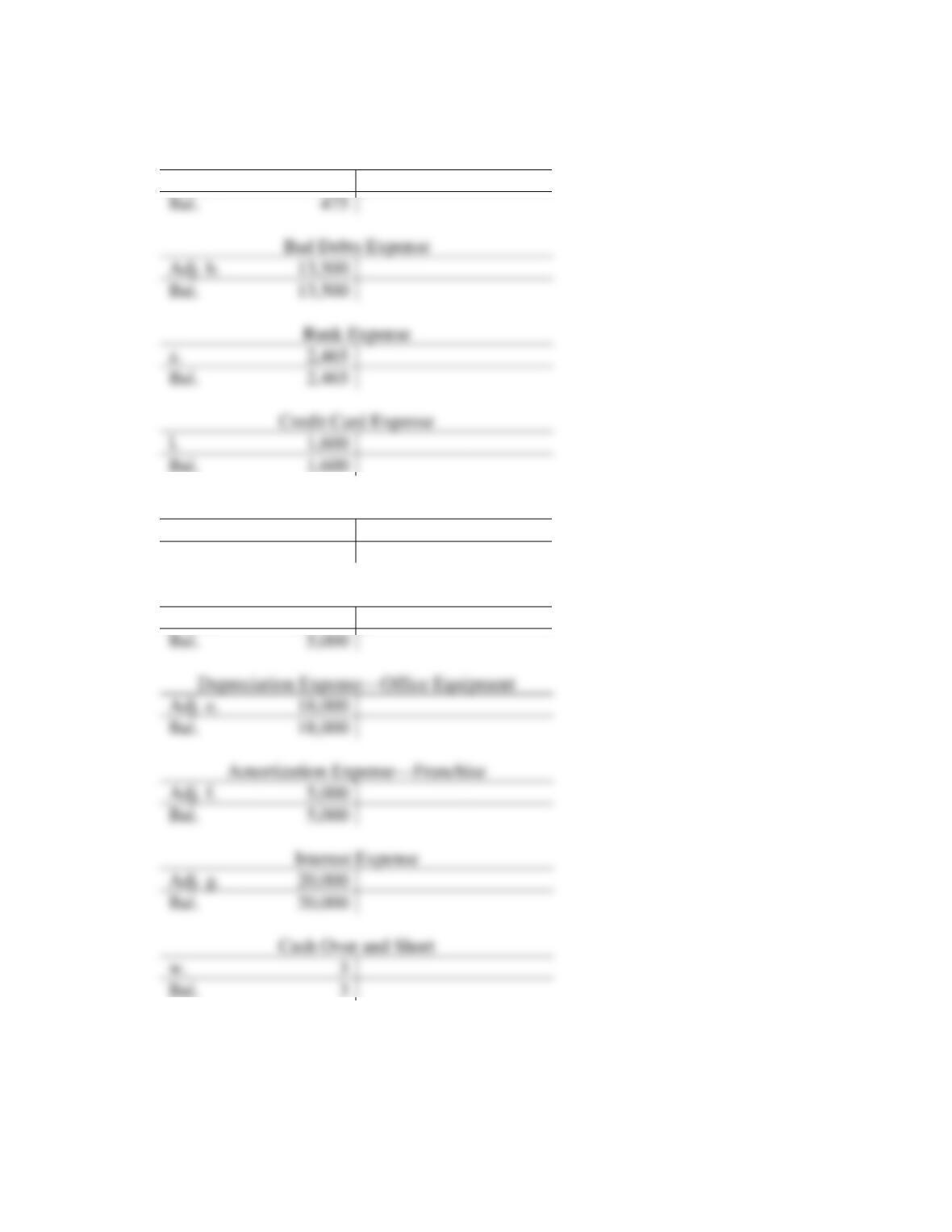

4. In preparation for preparing the adjusting entries, complete depreciation schedules for the first five years

for the depreciable plant assets, assuming the assets were purchased on January 2, 2018:

5. Record adjusting entries for the year ended December 31, 2018:

a. One year of the prepaid insurance has expired.

b. Management estimates that 5% of Accounts Receivable will be uncollectible.

c. An inventory of office supplies indicates $475 of supplies have been used.

6. Post adjusting entries and prepare an adjusted trial balance.

7. Prepare a multi-step income statement and statement of retained earnings for the year ended December

8. Evaluate the company’s success for the first year of operations by calculating the following ratios. Round

to two decimal places. Comment on the results.

a. Liquidity:

i. Current ratio

ii. Acid-test ratio

iii. Cash ratio

b. Efficiency:

i. Accounts receivable turnover

ii. Day’s sales in receivables

iii. Asset turnover

iv. Rate of return on total assets

SOLUTION

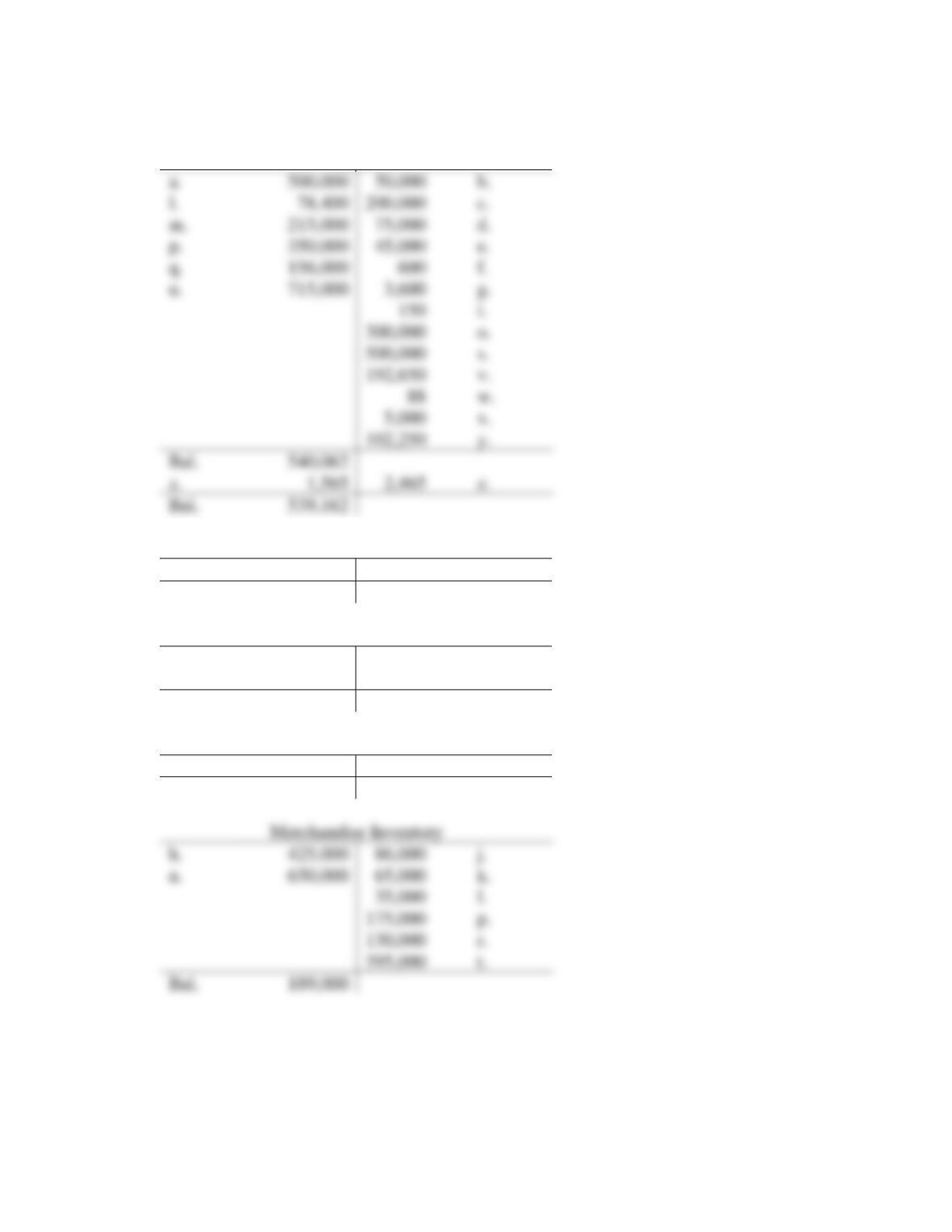

Requirement 1

Date

Accounts

Debit

Credit

a.

Cash

500,000

Common Stock

500,000

Franchise

Cash

c.

Cash

200,000

Notes Payable

400,000

e.

Office Equipment

f.

Office Supplies

600

Cash

600

Prepaid Insurance

Cash

425,000

425,000

9-65

i.

Petty Cash

150

Cash

150

j.

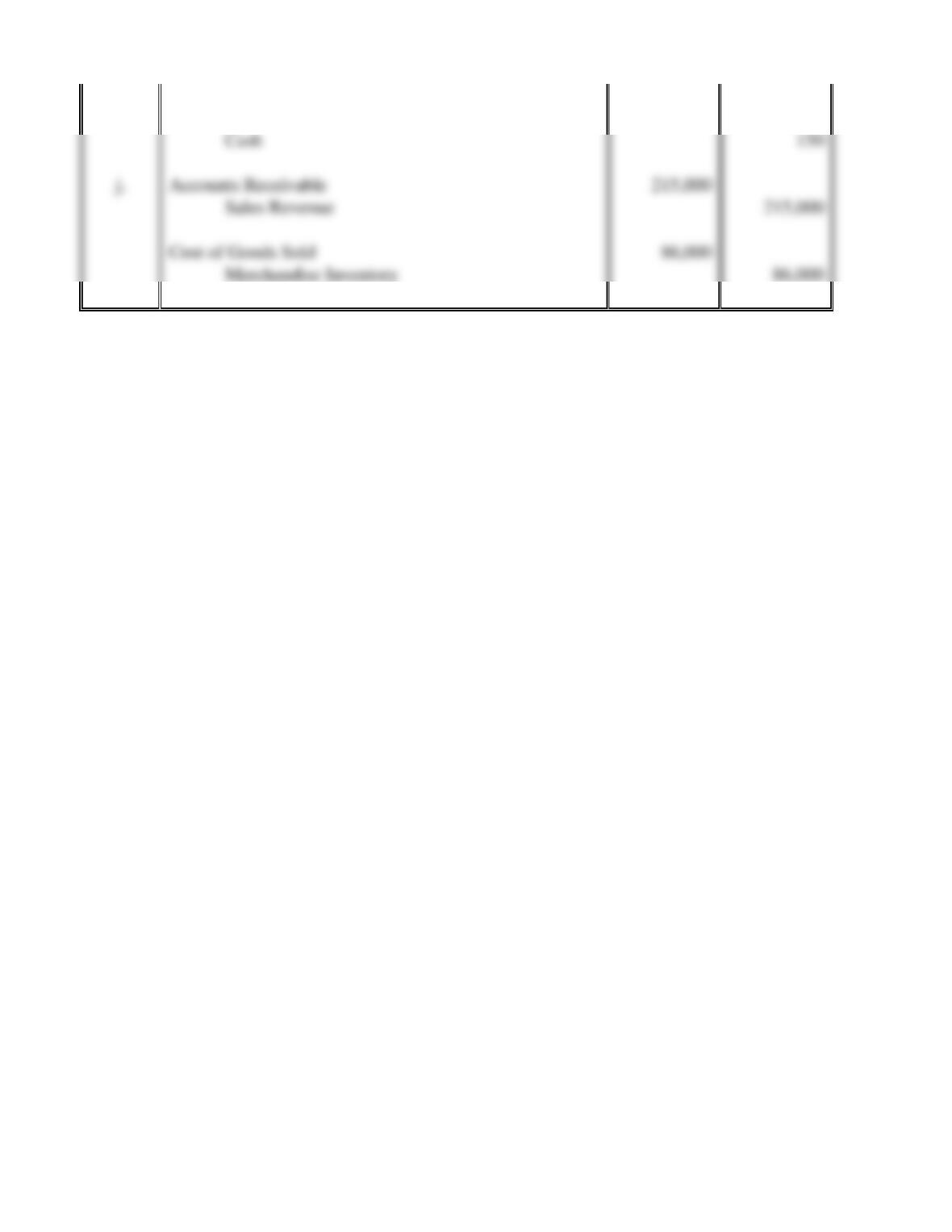

Accounts Receivable

Sales Revenue

Cost of Goods Sold

Merchandise Inventory

9-66

Comprehensive Problem, cont.

Requirement 1, cont.

Date

Accounts

Debit

Credit

k.

Note Receivable—Davis Contracting

150,000

Sales Revenue

150,000

m.

Cash