DM–13 Derivatives Module—Problems

PROBLEM M-2

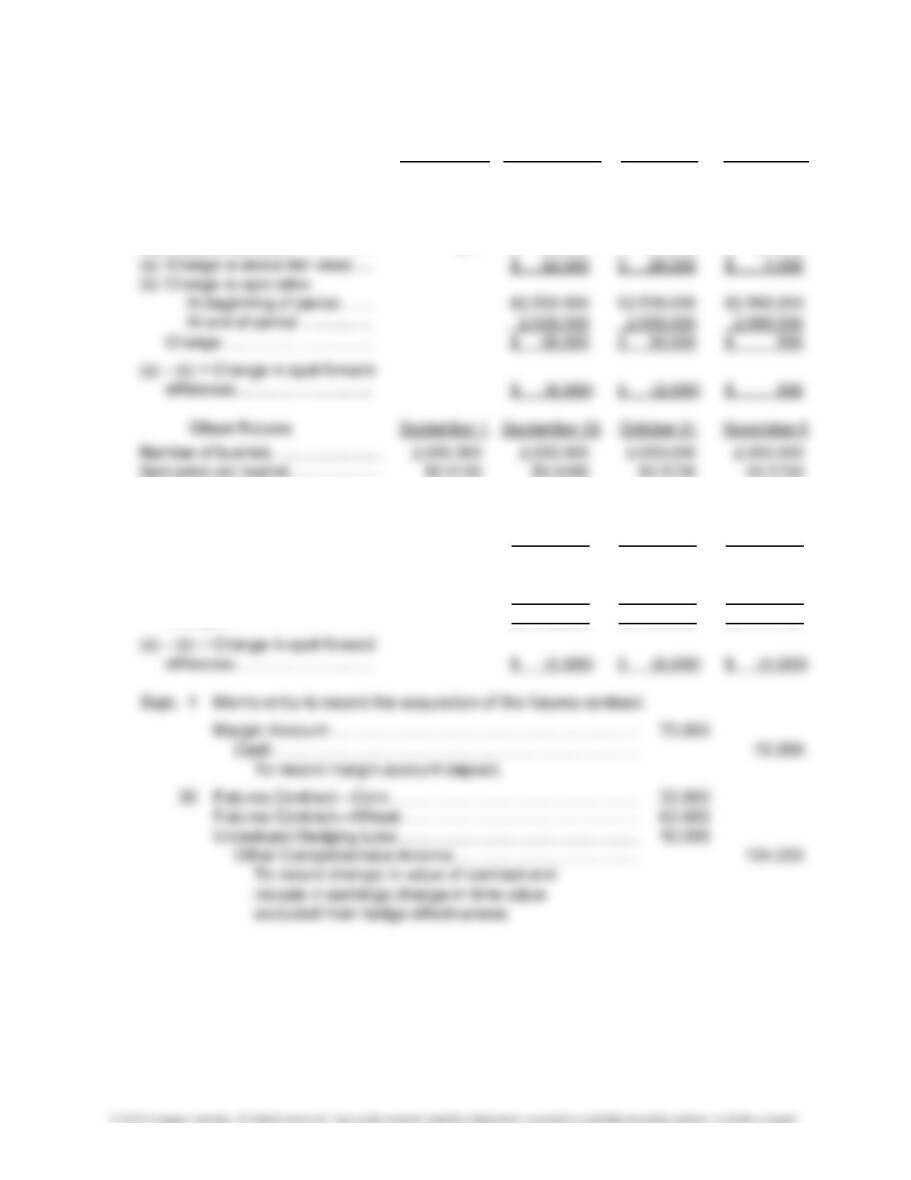

(1) Corn Futures September 1 September 30 October 31 November 5

Number of bushels. …………………… 1,000,000 1,000,000 1,000,000 1,000,000

Spot price per bushel …………………. $2.5000 $2.5380 $2.5680 $2.5685

Futures price per bushel …………….. $2.5100 $2.5420 $2.5700 $2.5710

Fair value of contract ………………. $— $ 32,000 $ 60,000 $ 61,000

Futures price per bushel …………….. $3.5210 $3.5520 $3.5710 $3.5705

Fair value of contract ………………. $— $ 62,000 $ 100,000 $ 99,000

(a) Change in above fair value …. $ 62,000 $ 38,000 $ (1,000)

(b) Change in spot rates:

At beginning of period ……. $7,030,000 $7,096,000 $7,140,000

At end of period ……………. 7,096,000 7,140,000 7,140,000

Change ……………………………. $ 66,000 $ 44,000 $ —

Problem M-2, Concluded

Oct. 31 Futures Contract—Corn ………………………………………………. 28,000

Futures Contract—Wheat …………………………………………….. 38,000

Unrealized Hedging Loss …………………………………………….. 8,000

Other Comprehensive Income ………………………………….. 74,000

Nov. 5 Futures Contract—Corn ………………………………………………. 1,000

Unrealized Hedging Loss …………………………………………….. 500

Futures Contract—Wheat ………………………………………… 1,000

Other Comprehensive Income ………………………………….. 500

To record change in value of contract and

include in earnings change in time value

excluded from hedge effectiveness.

Cash ……………………………………………………………………. 230,000

Futures Contract—Corn …………………………………………… 61,000

(2) Factors that might cause the futures contracts to not be highly effective include the following:

a. Changes in the price of wheat and corn may not correlate as highly with the change in

the price of flour due to costs associated with producing flour.

DM–15 Derivatives Module—Problems

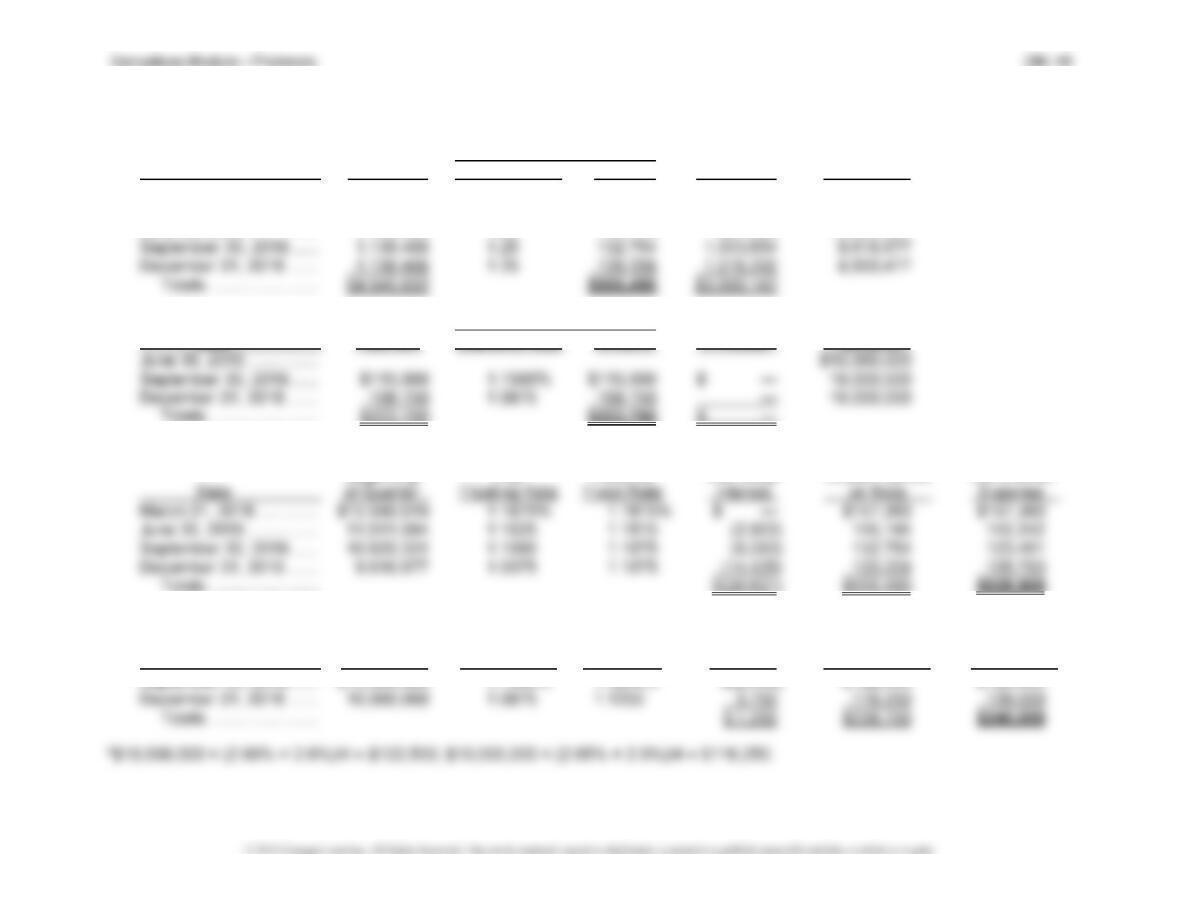

PROBLEM M-3

Futures Contract To Sell

Key Variables January February March

Number of units per contract ……………. 10,000 10,000

Spot price per unit ………………………….. $3.45 $3.40

Futures price per unit ……………………… $3.50 $3.44

Problem M-3, Continued

Forward Contract To Buy

Key Variables January February March

Number of units per contract ……………………. 5,000 5,000 5,000

Spot price per unit ………………………………….. $90.20 $90.50 $90.60

Forward rate per unit ………………………………. $91.50 $91.20 $90.60

Original forward rate per unit …………………… $92.00 $92.00 $92.00

Fair value of forward in future $s:

Discount rate …………………………………………. 6% 6%

Present value of the above fair value:

FV = –$2,500, n = 1.5, I = 0.25% ………… (2,491)

FV = –$4,000, n = 0.5, I = 0.25% ………… (3,995)

FV = –$7,000, n = 0.0, I = 0.25% ………… (7,000)

Current present value …………………………….. (2,491) (3,995) (7,000)

Problem M-3, Concluded

Call Option

Key Variables January February March

Number of units per option ………………. 100,000 100,000 100,000

Spot price per unit ………………………….. $8.05 $8.02 $7.95

Effect on Earnings—Gain (Loss)

Change in time value—gain (loss):

Original value of $1,000 vs. $400 . $ (600)

$400 vs. $0………………………………. $ (400)

Change in intrinsic value—gain (loss):

Original value of $5,000 vs. $2,000 In OCI

$2,000 vs. $0……………………………. In OCI

Sales revenue (100,000 × $12)………… $1,200,000

PROBLEM M-4

(1) Interest

Date Payment Quarterly Rate Amount Principal Balance

December 31, 2017 ……. $12,590,619

March 31, 2018 ………….. $1,136,408 1.25% $157,383 $ 979,025 11,611,594

June 30, 2018 ……………. 1,136,408 1.25 145,145 991,263 10,620,331

(2) Interest

Date Payment Quarterly Rate Amount Principal Balance

(3) Balance at

Beginning Pay Receive Net Swap Stated Interest Net Interest

(4) Balance at

Beginning Pay Receive Net Swap Stated Interest Net Interest

Date of Quarter Floating Rate Fixed Rate Interest on Note* Income

September 30, 2018 …… $10,000,000 1.1500% 1.1250% $(2,500) $122,500 $120,000

Problem M-4, Concluded

(5) Pay floating rate interest per quarter ($10,000,000 × 1.0875%) ………….. $108,750

Receive fixed rate interest per quarter ($10,000,000 × 1.1250%) ……….. 112,500

(6) In addition to the risk that the interest income on the note would decline due to falling varia-

ble interest rates, there is now a concern due to changing currency exchange rates. If the

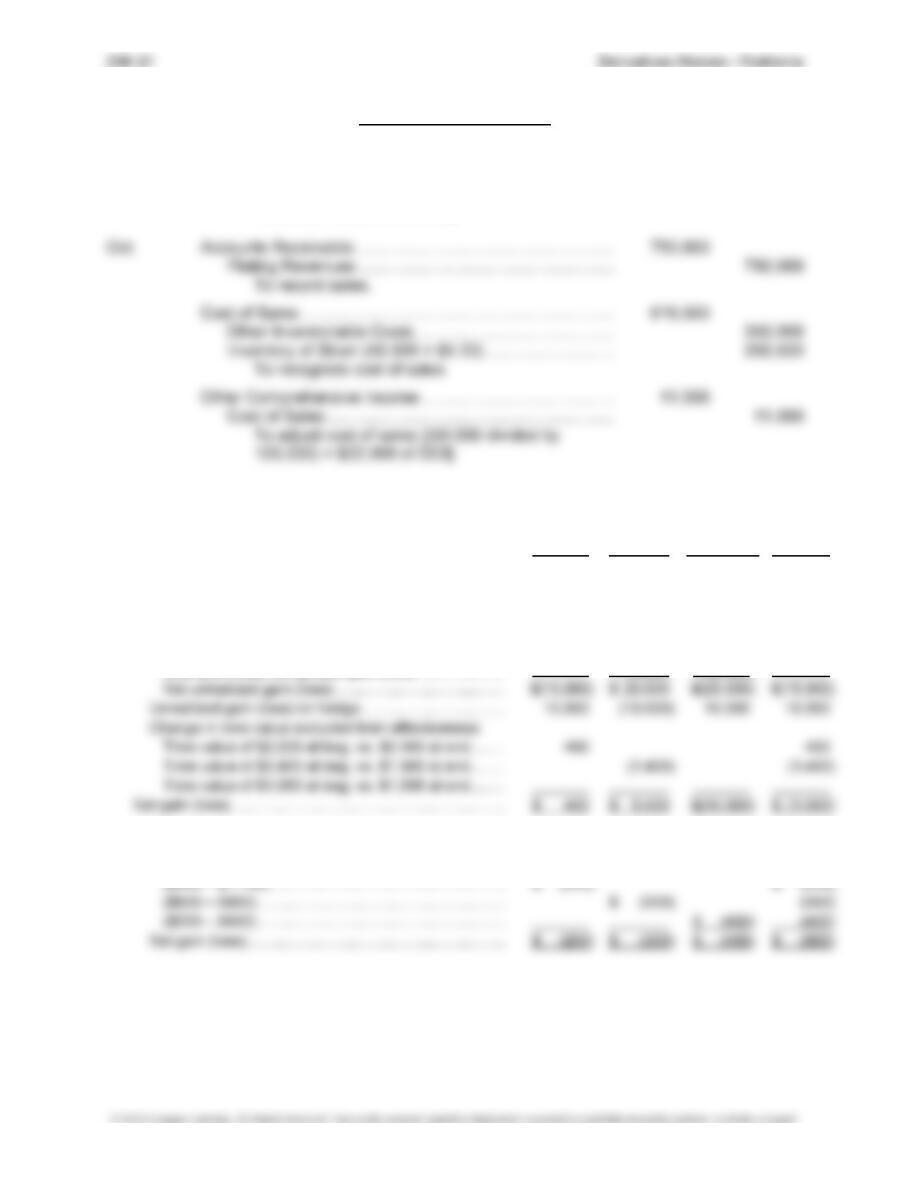

PROBLEM M-5

July 10 July 31 August 31 September 10

Notional amount in troy ounces. ………. 100,000 100,000 100,000 100,000

Strike price ……………………………………. $5.00 $5.00 $5.00 $5.00

July 10 Investment in Call Option ………………………………………….. 20,000

Cash …………………………………………………………………. 20,000

To record payment of option premium

(100,000 × $0.20).

31 Investment in Call Option ………………………………………….. 3,000

Unrealized Loss on Hedge ($10,000 – $9,000) …………….. 1,000

Other Comprehensive Income ($10,000 – $14,000) … 4,000

Aug. 31 Investment in Call Option ………………………………………….. 14,000

Unrealized Loss on Hedge ………………………………………… 7,000

Sept. 10 Unrealized Loss on Hedge ………………………………………… 1,000

Other Comprehensive Income …………………………………… 3,000

Investment in Call Option …………………………………….. 4,000

To record change in value of the option.

Sept. Accounts Receivable ………………………………………………… 225,000

Plating Revenues ……………………………………………….. 225,000

To record sales.

Problem M-5, Concluded

Sept. Other Comprehensive Income …………………………………… 3,300

Cost of Sales ……………………………………………………… 3,300

To adjust cost of sales [(15,000 divided by

100,000) × $22,000 of OCI].

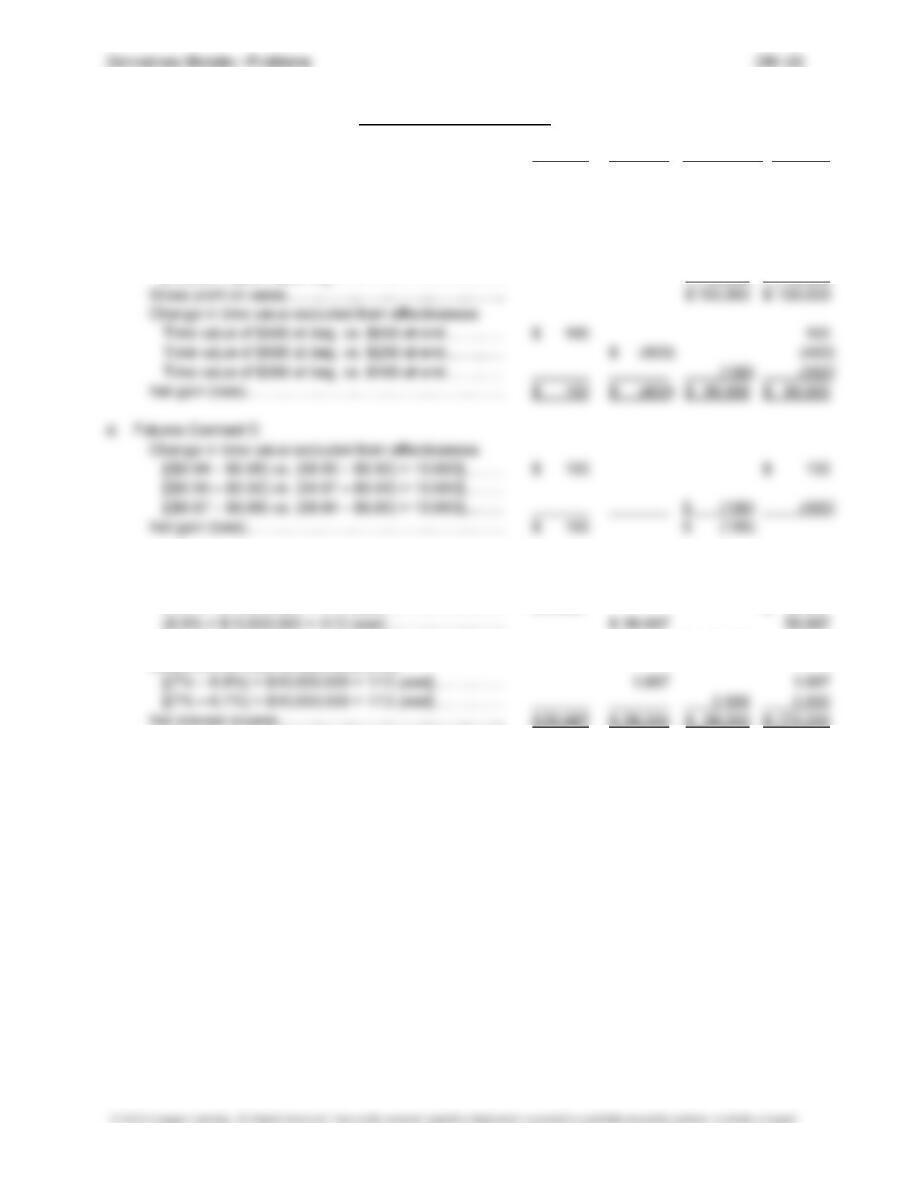

PROBLEM M-6

July

August September Total

a. Call Option A

Unrealized gain (loss) on commitment:

10,000 × ($45 – $46) …………………………………………. $(10,000) $(10,000)

10,000 × ($45 – $44) …………………………………………. $ 10,000 10,000

10,000 × ($45 – $46.50) …………………………………….. $(15,000) (15,000)

Less previously recognized gain (loss) ………………… 10,000 (10,000)

b. Call Option B (hedge not effective—does not qualify for special hedge accounting)

Unrealized gain (loss) on option:

Problem M-6, Concluded

July

August September Total

c. Put Option C

Sales revenue ……………………………………………………… $ 287,500 $ 287,500

Cost of sales ……………………………………………………….. (200,000) (200,000)

Adjustment to cost of sales—Intrinsic value at July 1 of

$0 versus intrinsic value at 9/10 of $12,500

[10,000 × ($30 – $28.75)] …………………………………… 12,500 12,500

e. Interest Rate Swap

Variable interest income:

(6.8% × $10,000,000 × 1/12 year) ………………………. $ 56,667 $ 56,667

(6.7% × $10,000,000 × 1/12 year) ………………………. $ 55,833 55,833

Settlement of fixed variable difference:

DM–23 Derivatives Module—Problems

PROBLEM M-7

(1) 2016

Dec. 31 Interest Expense ………………………………………………………… 800,000

Cash ……………………………………………………………………… 800,000

To record interest expense

[(7% + 1%) × $20,000,000 × ½ year].

Interest Rate Swap Asset ………………………………………… 47,001

To record settlement of the swap [(7.1% – 7.0%) ×

$20,000,000 × ½ year] and the change in the value

of the swap.

Other Comprehensive Income………………………………………. 10,000

To record settlement of the swap [(6.9% – 7.0%) ×

$20,000,000 × ½ year] and the change in value

of the swap.

Interest Expense ………………………………………………………… 10,000

Other Comprehensive Income ………………………………….. 10,000

Problem M-7, Concluded

2018

June 30 Interest Expense ………………………………………………………… 780,000

Cash ……………………………………………………………………… 780,000

To record interest expense [(6.8% + 1%) ×

$20,000,000 × ½ year].

(2) Impact on Earnings of the Interest Rate Swap

6-Month Period Ending

Dec. 31, June 30, Dec. 31, June 30,

2016

2017 2017 2018 Total

Effective interest rate:

Without a hedge ……….. 8.0% 8.1% 7.9% 7.8%

Unfortunately, in retrospect, the company would have been better off not to have engaged

in an interest rate swap. The swap resulted in an additional decrease in earnings of

$20,000.

(3) The LIBOR rate on December 31, 2017, would have had to be 7%. This would have re-