11,000$

375

Book

Value

$800 $800 $11,200

2020

2021

2019

Accumulated Book

Depreciation Value

$1,200 $1,200 $10,800

2021

2019

2020

Accumulated Book

Depreciation Value

$900 $900 $11,100

2020

2021

2019

DAVIDSON, DDS

(1) Straight-Line (nearest whole month):

Depreciation

Expense

Computation

Year

2018

Computation

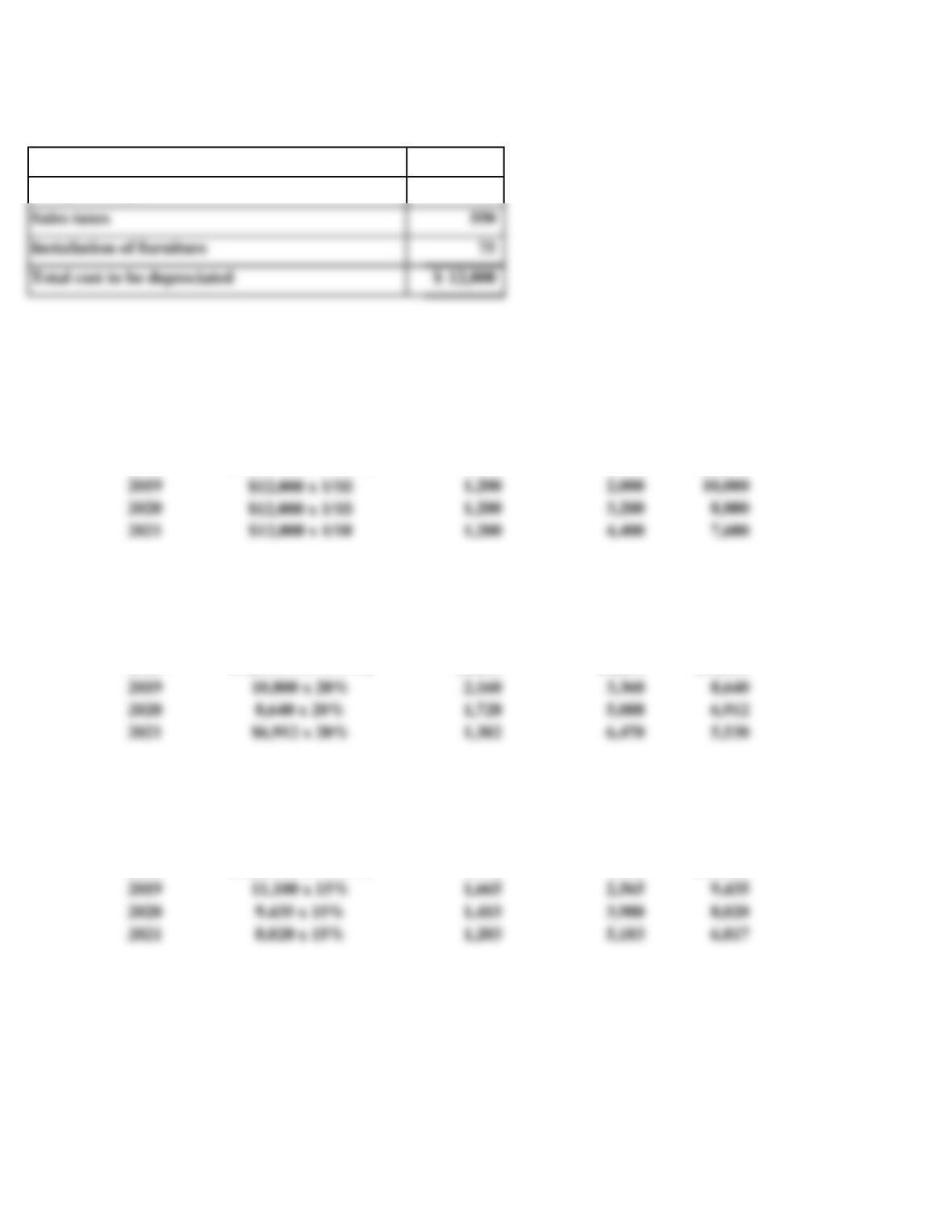

$12,000 x 1/10 x 8/12

$12,000 x 15% x 1/2

PROBLEM 9.3B

50 Minutes, Strong

a. Costs to be depreciated include:

Cost of furniture

Freight charges

Accumulated

Depreciation

Year

2018

Depreciation

Expense

Depreciation

Expense

(2) 200% Declining-Balance (half-year convention):

Computation

(3) 150% Declining-Balance (half-year convention):

$12,000 x 20% x 1/2

Year

2018

Sales taxes

Installation of furniture

Total cost to be depreciated

b.

c.

1. Journal entry assuming that the furniture was sold for $780:

780

2,600

Gain on Disposal of Assets

Loss on Sale of Asset

2. Journal entry assuming that the furniture was sold for $250:

250

2,600

Davidson may use the straight-line method in its financial statements to achieve the

least amount of depreciation expense in the early years of the furniture’s useful life.

PROBLEM 9.3B

DAVIDSON, DDS (concluded)

Cash

The 200% declining-balance method results in the lowest reported book value at

Cash

Accumulated Depreciation: Furniture

Accumulated Depreciation: Furniture

d.

25 Minutes, Medium

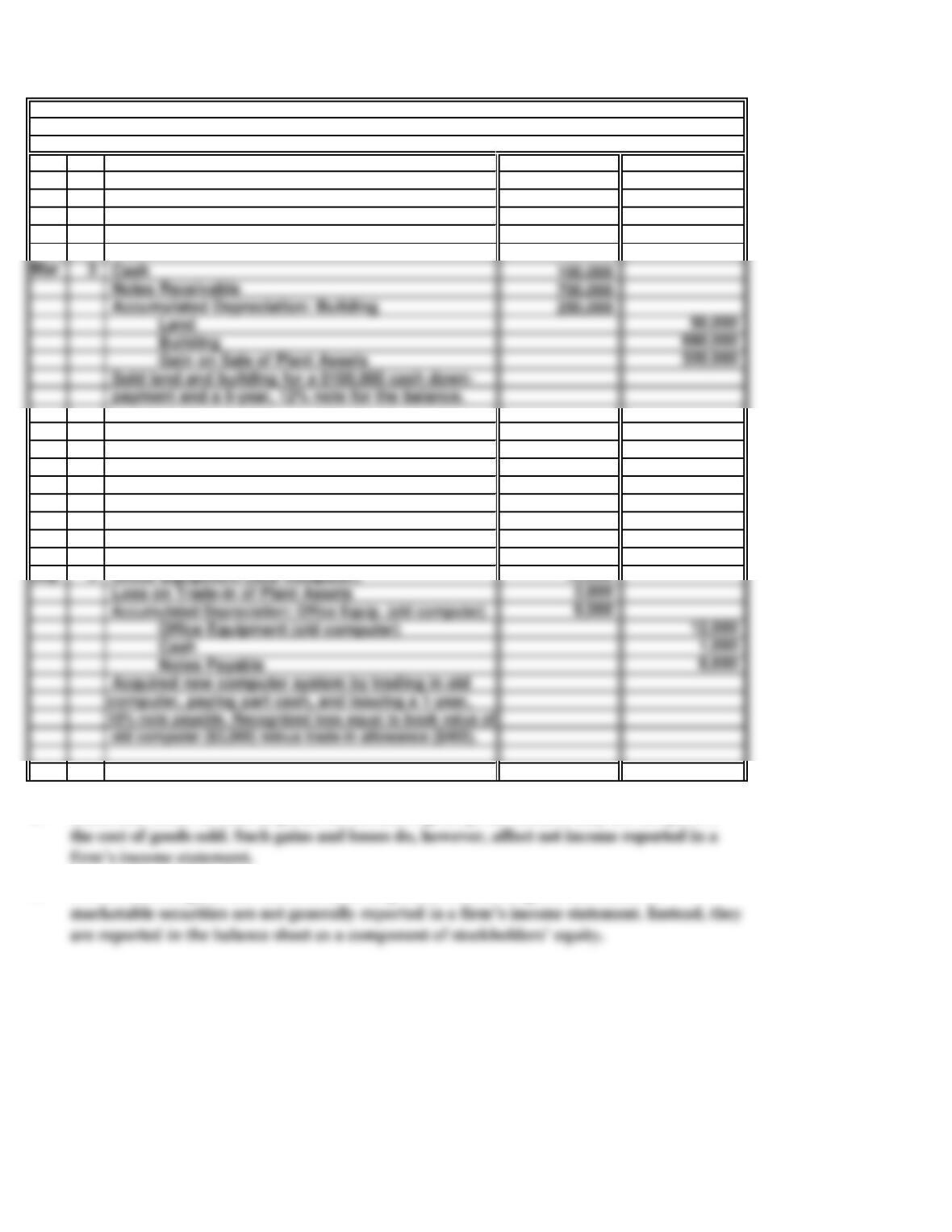

Jan 6 Loss on Disposal of Plant Assets 1,200

Accumulated Depreciation: Office Equipment 16,800

Office Equipment 18,000

Scrapped equipment; received no salvage value.

Jul 10 Vehicles (new truck) 37,000

Accumulated Depreciation: Vehicles (old truck) 22,000

Vehicles (old truck) 26,000

Gain on Disposal of Plant Assets 8,000

Cash 25,000

To record trade-in of old truck on new; trade-in

allowance exceeded book value by $8,000.

Sep 3 Office Equipment (new computer) 10,000

Loss on Trade-in of Plant Assets 2,600

Office Equipment (old computer) 12,000

Cash 1,000

Notes Payable 8,600

b.

c.

Gains and losses on asset disposals do not affect gross profit because they are not part of

Unlike realized gains and losses on asset disposals, unrealized gains and losses on

PROBLEM 9.4B

a.

General Journal

BLAKE CONSTRUCTION

Land 50,000

Building 680,000

Gain on Sale of Plant Assets 320,000

Sold land and building for a $100,000 cash down-

payment and a 5-year, 12% note for the balance.

25 Minutes, Medium

a.

b.

c.

d.

PROBLEM 9.5B

DELTA PRODUCTS CORPORATION

Intangible asset. A patent grants its owner the exclusive right to produce a particular

product. If the patent has significant cost, this cost is regarded as an intangible asset and

Operating expense. Although the training of employees probably has some benefit

Intangible asset. Goodwill represents the present value of future earnings in excess of

Operating expense. Because of the great uncertainty surrounding the potential benefits of

R&D programs, the FASB has ruled that research and development costs should be

e.

20 Minutes, Medium

250,000$

10

280,000$

196,000

240,000$

Estimated goodwill of Mell’s

Estimated excess earnings of Mell’s

Divided by management’s desired return on investments

c.

Due to the difficulties in objectively estimating the value of goodwill, it is recorded only when

Actual average net income per year

Normal earnings for Mell’s ($980,000 x 20% = $196,000)

PROBLEM 9.6B

JELL STORES

b. Estimated goodwill associated with the purchase of Mell’s:

a. Estimated goodwill associated with the purchase of Missy’s:

Actual average net income per year

Typical sales multiplier

Estimated goodwill of Missy’s

Estimated fair value of Missy’s

Fair value of identifiable assets of Missy’s

30 Minutes, Medium

a.

b. $24,000

c.

The units of output method is tied to the miles driven rather than calendar time and, as a

Units-of-Output:

Straight-line:

Truck

PROBLEM 9.7B

HAYWOOD, INC.

Depreciation expense for the first two years under the three depreciation methods is

determined as follows:

30 Minutes, Medium

a.

c.

$670,000

$670,000

Loss on sale

Less: Accumulated depreciation

Book value

Sales price

Year 2

Equipment

*$80,000 – $13,333 = $66,667

Less: Accumulated depreciation

Year 1:

Equipment

Plant and intangible asset sections of the balance sheet:

PROBLEM 9.8B

RODGERS COMPANY

Depreciation is calculated on the following amount:

Depreciation expense for Year 1:

Depreciation expense for Year 2:

Depreciation expense for Year 3:

($670,000 – $134,000) x 20% = $107,200

($670,000 – $134,000 – $107,200) x 20% = $85,760

Plus: Expenditures to prepare asset for use

$670,000 x 20% = $134,000

Purchase price

The declining balance rate at 200% of the straight-line is:

100%/10 years = 10%; 10% x 2 = 20%

20 Minutes, Strong

a.

b.

c.

SOLUTIONS TO CRITICAL THINKING CASES

ARE USEFUL LIVES “FLEXIBLE”?

CASE 9.1

AN ETHICS CASE

The ethical issue confronting Gillespie is whether the change in estimated useful lives is

reasonable, or whether it will cause the company’s financial statements to be misleading. On

Lengthening the period over which assets are depreciated for financial statement purposes

will reduce the annual charges to depreciation expense. This will reduce expenses in the

Management is responsible for establishing the estimated useful lives of assets for purposes

of calculating depreciation and preparing financial statements. Those lives must be

consistent with the actual expected use of the assets. To arbitrarily lengthen the estimated

a.

b.

c.

CASE 9.2

DEPARTURES FROM GAAP—ARE THEY ETHICAL?

20 Minutes, Strong

No. Miller Construction Co. is not a publicly owned company and has no external reporting

The question facing Max O’Shaughnessey is whether users of the company’s balance sheet

might assume that it was prepared in conformity with generally accepted accounting

Showing plant assets at current market values is not in conformity with generally accepted

20 Minutes, Easy

b.

c. (1)

d.

CASE 9.3

Accelerated depreciation methods transfer the costs of plant assets to expense more quickly

than does the straight-line method. These larger charges to depreciation expense reduce the

No—different depreciation methods may be used for different assets. The principle of

20 years (a 5% straight-line depreciation rate is equivalent to writing off 1/20 of the

DEPRECIATION POLICIES IN ANNUAL REPORTS

The depreciation methods used in financial statements are determined by management, not

15 Minutes, Medium

a.

b.

1.

2.

3.

4.

As a supervisor yourself, find ways to recognize individual and/or group

There are a number of steps that you might take, including the following:

Meet with employees periodically to remind them of company policy, including the

Work with your superiors to develop more specific policies, with examples,

CASE 9.4

CAPITALIZATION VS. EXPENSE

Employees, including yourself, may be applying the generally stated policies in a manner

that improves the appearance of your division’s performance. They (and you) may not

even realize this is being done, or it may be intentional. A consistent pattern of

capitalizing costs that should be expensed, or costs that are in a “gray area” between

Develop more specific materiality guidelines for applying capitalization and

ETHICS, FRAUD & CORPORATE GOVERNANCE

No time estimate

R & D EXPENDITURES

CASE 9.5

A keyword search of Pharmaceutical Companies will result in an extensive list of firms. The list

will include extremely profitable industry giants whose R&D expenditures typically amount to

15% to 25% of total costs and expenses. In addition, many smaller companies whose primary

INTERNET