Chapter 09 – Long-Term Liabilities

9-1

Chapter 9

Long-Term Liabilities

INSTRUCTOR’S MANUAL

Learning Objectives

LO9-1 Explain financing alternatives.

LO9-2 Account for installment notes payable.

LO9-3 Understand the balance sheet effects of operating and capital leases.

LO9-4 Identify the characteristics of bonds.

LO9-5 Determine the price of a bond issue.

LO9-6 Account for the issuance of bonds.

LO9-7 Record the retirement of bonds.

Analysis

LO9-8 Make financial decisions using long-term liability ratios.

Chapter 09 – Long-Term Liabilities

9-2

Teaching Suggestions

Historically, long-term liabilities, especially bonds, are one of the toughest topics in a financial

accounting course. Some financial accounting textbooks combine current and long-term

liabilities into one chapter, opting to skim over the topics related to long-term liabilities. We

redesigned the chapter to provide instructors flexibility in the coverage of long-term liabilities.

Instructors who prefer an overview of long-term liabilities including installment notes, leases,

and bonds can just cover Part A. Instructors who prefer more detailed coverage of bonds can also

cover Part B (Pricing a Bond) and/or Part C (Recording Bonds Payable).

Chapters 4–12 focus on a separate underlying industry theme. Chapter 9 focuses on

amusement parks as these companies tend to carry a very high level of debt. References to Six

Flags and Cedar Fair are made in the feature story and continue periodically throughout the

chapter. The end-of-chapter material and supplements continue the amusement park theme.

Chapter 9 starts with the basic accounting equation to contrast debt financing with equity

financing. Students need to understand the advantages and disadvantages of borrowing money

(debt financing) in comparison to obtaining additional investment from stockholders (equity

financing). Part A provides an overview of long-term debt including coverage of installment

notes (car loans and home loans), leases, and bonds.

Part B is a stand-alone section explaining how bond prices are determined. As a separate

section, Part B allows instructors flexibility to choose whether to include the topic of bond

pricing in reading and homework assignments. Some instructors feel strongly that students need

to understand how to price a bond and that pricing a bond provides a key example of present

value concepts. Other instructors feel equally strong that bond pricing is better left for finance

and intermediate accounting courses. The chapter is designed to leave the choice up to you. Bond

pricing is shown using a financial calculator, Excel spreadsheets, and present value tables, as

instructors use all three methods.

Part C illustrates the recording of bonds issued at face value, at a discount, and at a premium.

Interest expense is calculated based on the effective interest method, as this is GAAP. We do not

cover the straight-line interest method, as this method is not true GAAP, and introducing

multiple methods adds confusion for students. Part C concludes with recording the retirement of

bonds, including a decision maker’s perspective explaining why a company may choose to buy

back debt early.

The chapter concludes with a debt analysis using the actual financial statements of Coca-

Cola and PepsiCo. PepsiCo’s higher leverage increases risk. In good times, PepsiCo’s higher

leverage results in a higher return to investors. However, in down times, their higher leverage

results in a lower overall return to investors.

Chapter 09 – Long-Term Liabilities

9-3

A

As

ss

si

ig

gn

nm

me

en

nt

t

C

Ch

ha

ar

rt

ts

s

Questions

Learning

Objective(s)

Topic

Time

(Min.)

1

LO9-1

Define capital structure

5

2

LO9-1

Compare borrowing with issuing stock

5

3

LO9-2

Relate interest expense to the carrying value of an

installment note with fixed monthly payments

5

4

LO9-3

Explain the difference between an operating lease

and a capital lease

5

5

LO9-4

Describe bond issue costs

5

6

LO9-4

Compare borrowing from a bank to issuing bonds

5

7

LO9-4

Contrast bond characteristics

5

8

LO9-4

Define convertible bonds and explain how they

might benefit the investor and the issuer

5

9

LO9-5

Explain how to calculate the issue price of bonds

5

10

LO9-5

Describe the difference in bond terms

5

11

LO9-5

Explain the relationship between the stated interest

rate and the market interest rate for bonds issued at

a discount

5

12

LO9-5

Explain the relationship between the stated interest

rate and the market interest rate for bonds issued at

a premium

5

13

LO9-5

Calculate the interest payment for a bond issue

5

14

LO9-5

Calculate the issue price of bonds

5

15

LO9-6

Explain the relationship between the carrying value

of bonds payable and the amount recorded for

interest expense for bonds issued at a discount

5

16

LO9-6

Explain the relationship between the carrying value

of bonds payable and the amount recorded for

interest expense for bonds issued at a premium

5

17

LO9-6

Describe how the columns in an amortization

schedule are calculated

5

18

LO9-7

Explain why a company would choose to buy back

bonds before their maturity date

5

19

LO9-7

Describe the entry to record the early retirement of

bonds

5

20

LO9-8

Describe the potential risks and rewards of carrying

additional debt

5

Chapter 09 – Long-Term Liabilities

9-4

Brief

Exercises

Learning

Objective(s)

Topic

Time

(Min.)

BE9-1

LO9-2

Record installment notes

10

BE9-2

LO9-4

Explain the conversion feature of bonds

5

BE9-3

LO9-5

Calculate the issue price of bonds

5

BE9-4

LO9-5

Calculate the issue price of bonds

5

BE9-5

LO9-5

Calculate the issue price of bonds

5

BE9-6

LO9-6

Record bond issue and related semiannual interest

10

BE9-7

LO9-6

Record bond issue and related semiannual interest

10

BE9-8

LO9-6

Record bond issue and related semiannual interest

10

BE9-9

LO9-6

Record bond issue and related annual interest

10

BE9-10

LO9-6

Record bond issue and related annual interest

10

BE9-11

LO9-6

Record bond issue and related annual interest

10

BE9-12

LO9-6

Calculate interest expense

5

BE9-13

LO9-6

Calculate interest expense

5

BE9-14

LO9-6

Interpret a bond amortization schedule

5

BE9-15

LO9-6

Interpret a bond amortization schedule

5

BE9-16

LO9-7

Record early retirement of bonds issued at a

discount

5

BE9-17

LO9-7

Record early retirement of bonds issued at a

premium

5

BE9-18

LO9-8

Calculate ratios

15

Exercises

Learning

Objective(s)

Topic

Time

(Min.)

E9-1

LO9-1

Compare financing alternatives

10

E9-2

LO9-2

Record installment notes

15

E9-3

LO9-3

Compare operating and capital leases

20

E9-4

LO9-4

Match bond terms with their definitions

10

E9-5

LO9-5

Calculate the issue price of bonds

15

E9-6

LO9-5

Calculate the issue price of bonds

15

E9-7

LO9-6

Record bonds issued at face amount

10

E9-8

LO9-6

Record bonds issued at a discount

20

E9-9

LO9-6

Record bonds issued at a premium

20

E9-10

LO9-6

Record bonds issued at face amount

10

E9-11

LO9-6

Record bonds issued at a discount

20

E9-12

LO9-6

Record bonds issued at a premium

20

E9-13

LO9-6

Record bonds issued at face amount with interest

payable annually

20

E9-14

LO9-6

Record bonds issued at a discount with interest

payable annually

20

E9-15

LO9-6

Record bonds issued at a premium with interest

payable annually

20

E9-16

LO9-7

Record the retirement of bonds

20

E9-17

LO9-7

Record the retirement of bonds

20

9-5

E9-18

LO9-8

Calculate and analyze ratios

20

E9-19

LO9-2, 9-8

Complete the accounting cycle using long-term

liability transactions

60

Problems

Learning

Objective(s)

Topic

Time

(Min.)

P9-1A

LO9-2

Record and analyze installment notes

25

P9-2A

LO9-3, 9-8

Explore the impact of leases on the debt to equity

ratio

25

P9-3A

LO9-5, 9-6

Calculate the issue price of a bond and prepare

amortization schedules

30

P9-4A

LO9-6

Record bond issue and related interest

30

P9-5A

LO9-6

Understand a bond amortization schedule

15

P9-6A

LO9-6

Prepare a bond amortization schedule and record

transactions for the bond issuer

20

P9-7A

LO9-8

Calculate and analyze ratios

30

P9-1B

LO9-2

Record and analyze installment notes

25

P9-2B

LO9-3, 9-8

Explore the impact of leases on the debt to equity

ratio

25

P9-3B

LO9-5, 9-6

Calculate the issue price of a bond and prepare

amortization schedules

30

P9-4B

LO9-6

Record bond issue and related interest

30

P9-5B

LO9-6

Understand a bond amortization schedule

15

P9-6B

LO9-6

Prepare a bond amortization schedule and record

transactions for the bond issuer

20

P9-7B

LO9-8

Calculate and analyze ratios

30

Additional

Perspectives

Topic

Time

(Min.)

AP9-1

Continuing Problem: Great Adventures

20

AP9-2

Financial Analysis: American Eagle Outfitters, Inc.

25

AP9-3

Financial Analysis: The Buckle, Inc.

25

AP9-4

Comparative Analysis: American Eagle Outfitters, Inc. vs. The

Buckle, Inc.

25

AP9-5

Ethics

25

AP9-6

Internet Research

20

AP9-7

Written Communication

15

AP9-8

Earnings Management

30

Chapter 09 – Long-Term Liabilities

9-6

Chapter Quiz Questions

The following multiple-choice questions are 10 unique quiz questions that correspond to the 10

questions at the end of each chapter. Each question covers the same learning objective but with a

little different twist. The correct answer is highlighted in bold for each item.

LO9-1

1. Which of the following is not a common long-term debt?

LO9-3

2. Which of the following leases is simply a rental?

LO9-4

3. Bonds can be secured or unsecured. Likewise, bonds can be term or serial bonds. Which is

more common?

LO9-4

4. Convertible bonds:

a. Provide potential benefits only to the lender.

LO9-5

5. Bonds issued at a discount are:

a. Issued above face value.

9-7

LO9-6

6. Which of the following is true for bonds issued at a premium?

LO9-6

7. The cash paid for interest on bonds payable is calculated as:

a. Face amount times the stated interest rate.

LO9-6

8. When bonds are issued at a premium, what happens to the carrying value and interest

expense over the life of the bonds?

LO9-7

9. Douglas County Fairgrounds retires a $50 million bond issue when the carrying value of the

bonds is $52 million, but the market value of the bonds is only $47 million. The entry to

LO9-8

10. Financial leverage is best measured by which of the following ratios?

Chapter 09 – Long-Term Liabilities

9-8

Alternate Let’s Review

Problem #1

Assume that on January 1, 2018, Adventure Island issues $500,000 of 8% bonds, due in 10

years, with interest payable semi-annually on June 30 and December 31 each year.

Required:

1. If the market rate is 8%, will the bonds issue at face amount, a discount, or a premium?

Calculate the issue price.

2. If the market rate is 9%, will the bonds issue at face amount, a discount, or a premium?

Calculate the issue price.

3. If the market rate is 7%, will the bonds issue at face amount, a discount, or a premium?

Calculate the issue price.

Solution:

1. If the market rate is 8%, the bonds will issue at face amount.

Calculator Input

Bond

Characteristics

Key

Amount

Calculator Output

$228,195

Chapter 09 – Long-Term Liabilities

9-9

Calculator Input

Bond

characteristics

Key

Amount

1. Face amount

FV

$500,000

2. Interest payment each period

3. Market interest rate each period

4. Periods to maturity

N

Calculator Output

Issue price

PV

$467,480

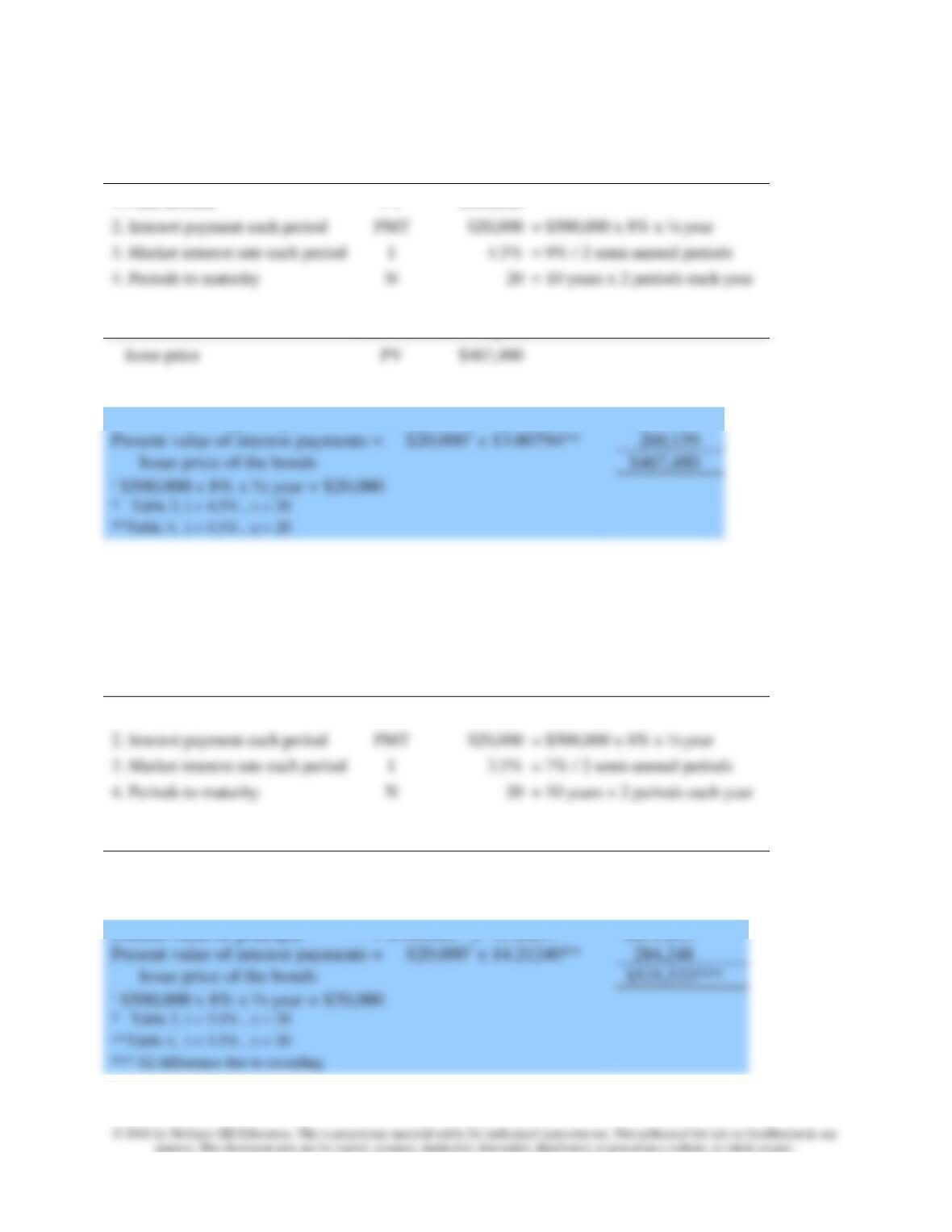

Present value of principal = $500,000 x 0.41464*

$207,321

Present value of interest payments = $20,0001 x 13.00794**

$467,480

3. If the market rate is 7%, the bonds will issue at a premium. The only change we make is that

now I = 3.5%.

Calculator Input

Bond

characteristics

Key

Amount

1. Face amount

FV

$500,000

2. Interest payment each period

3. Market interest rate each period

4. Periods to maturity

N

Calculator Output

Issue price

PV

$535,531

Present value of principal = $500,000 x 0.50257*

$251,285

Present value of interest payments = $20,0001 x 14.21240**

9-10

Problem #2

Assume that on January 1, 2018, Adventure Island issues $500,000 of 8% bonds, due in 10

years, with interest payable semi-annually on June 30 and December 31 each year.

Required:

1. If the market rate is 8%, the bonds will issue at $500,000. Record the bond issue on January

1, 2018, and the first two semi-annual interest payments on June 30, 2018, and December 31,

2018.

2. If the market rate is 9%, the bonds will issue at $467,480. Record the bond issue on January

1, 2018, and the first two semi-annual interest payments on June 30, 2018, and December 31,

2018.

3. If the market rate is 7%, the bonds will issue at $535,531. Record the bond issue on January

1, 2018, and the first two semi-annual interest payments on June 30, 2018, and December 31,

2018.

Solution:

1.

January 1, 2018

Debit

Credit

Cash

June 30, 2018

Interest Expense

20,000

20,000

December 31, 2018

Interest Expense

20,000

20,000

2.

January 1, 2018

Debit

Credit

Cash

Discount on Bonds Payable

32,520

June 30, 2018

Interest Expense ($467,480 x 9% x ½)

21,037

December 31, 2018

Chapter 09 – Long-Term Liabilities

9-11

Interest Expense ([$467,480 + 1,037] x 9% x ½)

21,083

Discount on Bonds Payable (difference)

3.

January 1, 2018

Debit

Credit

Cash

535,531

Bonds Payable

500,000

Premium on Bonds Payable

Interest Expense ($535,531 x 7% x ½)

Premium on Bonds Payable (difference)

December 31, 2018

Interest Expense ([$535,531 – 1,256] x 7% x ½)

Premium on Bonds Payable (difference)

Chapter 09 – Long-Term Liabilities

9-12

Key Points by Learning Objective

LO9-1 Explain financing alternatives.

LO9-2 Account for installment notes payable.

LO9-3 Understand the balance sheet effects of operating and capital leases.

LO9-4 Identify the characteristics of bonds.

The distinguishing characteristics of bonds include whether they are backed by collateral

LO9-5 Determine the price of a bond issue.

LO9-6 Account for the issuance of bonds.

When bonds issue at face amount, the carrying value and the corresponding interest expense

LO9-7 Record the retirement of bonds.

Chapter 09 – Long-Term Liabilities

9-13

Analysis

LO9-8 Make financial decisions using long-term liability ratios.

The debt to equity ratio is a measure of financial leverage. Assuming more debt (higher leverage)

Chapter 09 – Long-Term Liabilities

9-14

Common Mistakes

Common Mistake

The interest rate we use to calculate the bond issue price is always the market rate, never the

stated rate. Some students get confused and incorrectly use the stated rate to calculate present

Common Mistake

Students sometimes incorrectly record interest expense using the stated rate rather than the

Chapter 09 – Long-Term Liabilities

9-15

Decision Points

Question

Accounting Information

Analysis

How do you

determine a

company’s capital

Balance sheet

A debt capital structure would have a

higher portion of liabilities relative to

stockholders’ equity. An equity

Question

Accounting Information

Analysis

obligations related to

the financial statements

sheet but are disclosed in the notes to

Does the company

have significant

Disclosure of lease

commitments in the notes to

Operating lease commitments are not

reported as liabilities on the balance

Question

Accounting Information

Analysis

Which company has

higher leverage?

Debt to equity ratio

Question

Accounting Information

Analysis

Debt to equity is a measure of

financial leverage. Companies with

Chapter 09 – Long-Term Liabilities

9-16

Career Corner

Career Corner

Financing alternatives, capital structure, notes, leases, and bonds are topics covered in both

accounting and finance. How do you decide whether to major in accounting or finance? Some

Chapter 09 – Long-Term Liabilities

9-17

Ethical Dilemma

Ethical Dilemma

On January 1, 2017, West-Tex Oil issued $50 million of 8% bonds maturing in 10 years. The

market interest rate on the issue date was 9%, which resulted in the bonds being issued at a

discount. In December 2018, Tex Winters, the company CFO, notes that in the two years since

the bonds were issued, interest rates have fallen almost 3%. Tex suggests that West-Tex might

consider repurchasing the 8% bonds and reissuing new bonds at the lower current interest rates.

Another executive, Will Bright, asks, “Won’t the repurchase result in a large loss to our

financial statements?” Tex agrees, indicating that West-Tex is likely to just meet earnings targets

for 2018. The company would probably not meet its targets with a multimillion-dollar loss on a

bond repurchase. However, 2019 looks to be a record-breaking year. They decide that maybe

they should wait until 2019 to repurchase the bonds.

How could the repurchase of debt cause a loss to be reported in net income? Explain how the

repurchase of debt might be timed to manage reported earnings. Is it ethical to time the

repurchase of bonds to help meet earnings targets?

Bond prices move in the opposite direction of interest rates. When interest rates decrease, bond

prices increase. This makes the debt more expensive, resulting in a loss on repurchase equal to

the difference between the higher repurchase price and the current carrying value of the bonds.

Key Issues

• Is it ethical to time the repurchase of bonds to help meet earnings targets?

• More broadly, when is it acceptable and when is it not acceptable to time accounting

practices to meet earnings targets?