9-21

PROBLEM 9-33 (CONTINUED)

3. Since the 20×1 usage of Islin is 200,000 gallons, the firm’s raw-material purchases

budget (in dollars) for Islin for 20×2 is as follows:

Quantity of Islin required for production in 20×2 (in gallons):

Yarex (120,800 × 1) ………………………………………………………….

Darol (79,200 × .7) …………………………………………………………..

120,800

55,440

4. The company should continue using Islin, because the cost of using Philin is

$152,632 greater than using Islin, calculated as follows:

Change in material cost from substituting Philin for Islin:

9-22

PROBLEM 9-34 (25 MINUTES)

1. Tuition revenue budget:

Current student enrollment…………………….

12,000

Add: 5% increase in student body……………

600

Total student body……………………………….

12,600

180

12,420

Credit hours per student per year…………….

x 30

Total credit hours………………………………..

Tuition rate per hour…………………………….

x $75

2. Faculty needed to cover classes:

Total student body…………………………………….

12,600

Total student class enrollments to be covered….

Students per class…………………………………….

Classes to be taught………………………………….

Classes taught per professor……………………….

Faculty needed…………………………………………

Classes per student per year [(15 credit hours ÷

3. Possible actions might include:

• Hire part-time instructors

9-23

PROBLEM 9-35 (25 MINUTES)

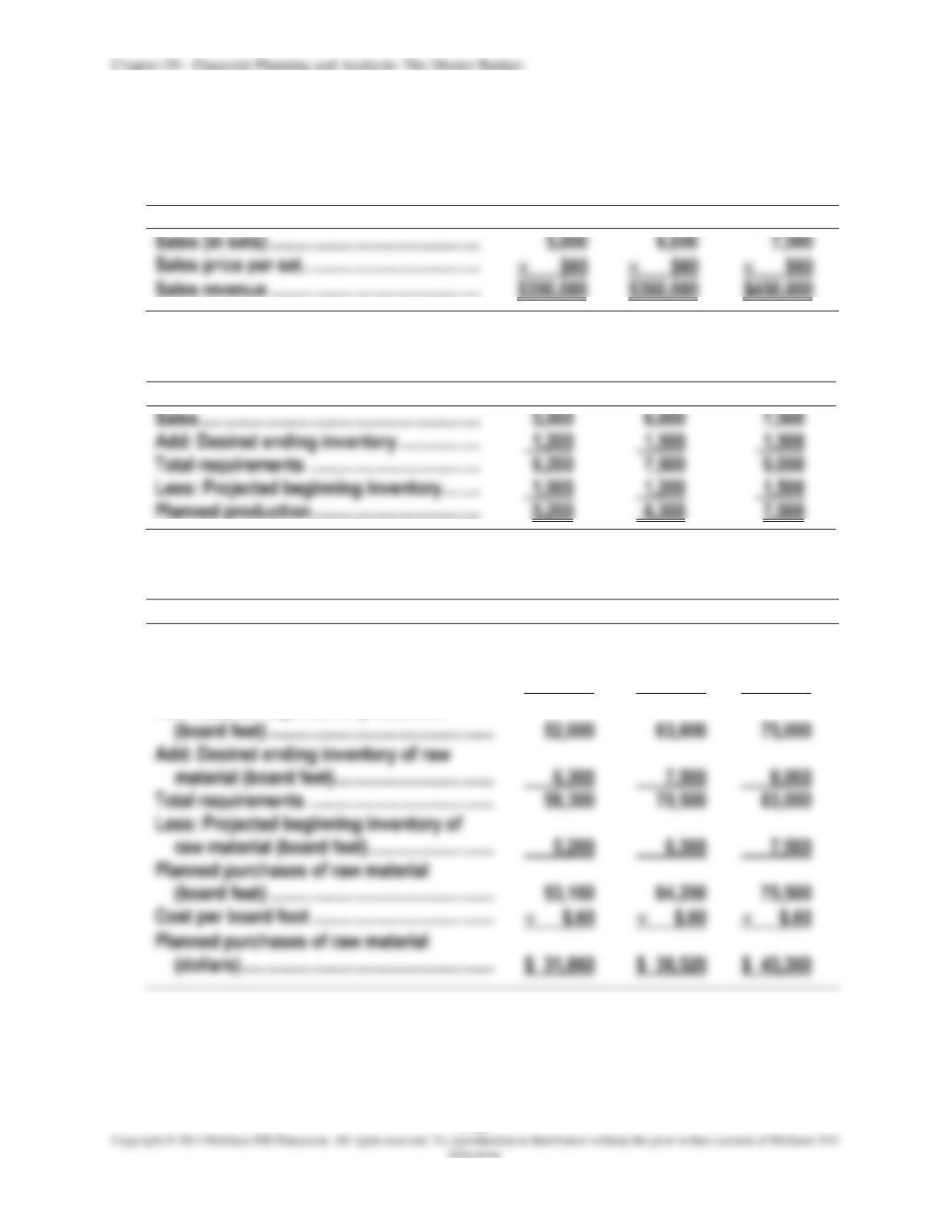

1.

Sales budget

July

August

September

Sales (in sets) ………………………………………

5,000

6,000

7,500

2.

Production budget (in sets)

July

August

September

Sales ……………………………………………………

5,000

6,000

7,500

Add: Desired ending inventory ……………..

1,200

1,500

1,500

Total requirements ……………………………….

6,200

7,500

9,000

Less: Projected beginning inventory ……..

1,000

1,200

1,500

3.

Raw-material purchases

July

August

September

Planned production (sets) ……………………….

5,200

6,300

7,500

Raw material required per set

(board feet) …………………………………………

10

10

10

Total requirements ………………………………….

58,300

70,500

83,000

Less: Projected beginning inventory of

Raw material required for production

9-24

PROBLEM 9-35 (CONTINUED)

4.

Direct-labor budget

July

August

September

Planned production (sets) ……………………….

5,200

6,300

7,500

Direct-labor hours required ……………………..

7,800

9,450

11,250

Chapter 09 – Financial Planning and Analysis: The Master Budget

9-25

PROBLEM 9-36 (30 MINUTES)

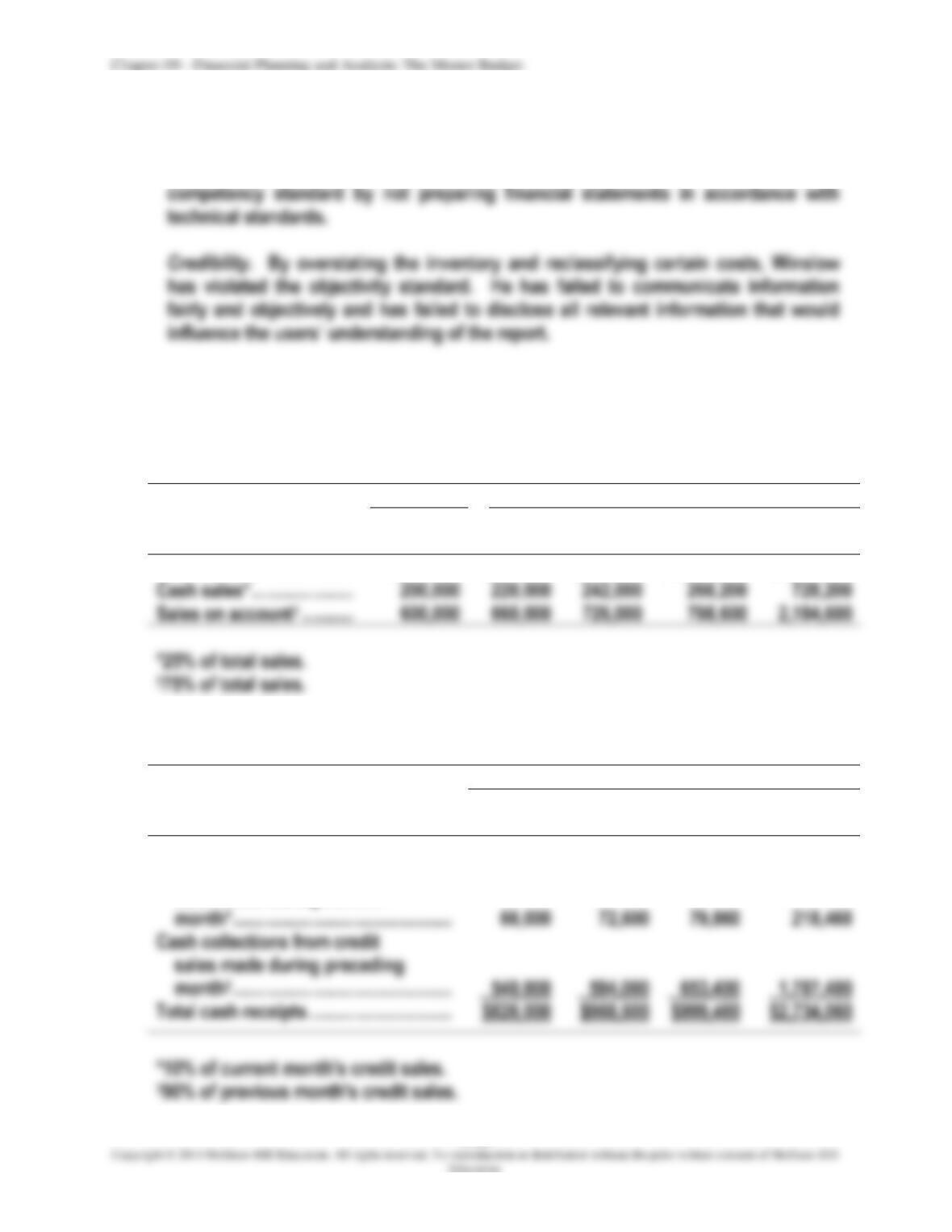

1. Sales are collected over a two-month period, 40% in the month of sale and 60% in the

3. Dakota Fan collected 40% of February’s sales during February, or $78,400. Thus,

7. Financing required is $3,500 ($15,000 minimum balance less ending cash balance of

Chapter 09 – Financial Planning and Analysis: The Master Budget

9-26

PROBLEM 9-37 (45 MINUTES)

1.

The benefits that can be derived from implementing a budgeting system include the

following:

Chapter 09 – Financial Planning and Analysis: The Master Budget

9-27

PROBLEM 9-37 (CONTINUED)

2.

a. Schedule

b. Subsequent Schedule

Sales Budget

Production Budget

Selling Expense Budget

Budgeted Income Statement

Ending Inventory Budget (units)

Production Budget

Production Budget (units)

Direct-Material Budget

Direct-Labor Budget

Production-Overhead Budget

Direct-Material Budget

Direct-Labor Budget

Production-Overhead Budget

Selling Expense Budget

Budgeted Income Statement

Research and Development Budget

Budgeted Income Statement

Administrative Expense Budget

Budgeted Income Statement

Budgeted Income Statement

Budgeted Balance Sheet

Capital Expenditures Budget

Cash Receipts and Disbursements Budget

Budgeted Balance Sheet

Budgeted Statement of Cash Flows

Budgeted Balance Sheet

Budgeted Statement of Cash Flows

Budgeted Statement of Cash Flows

Chapter 09 – Financial Planning and Analysis: The Master Budget

9-28

PROBLEM 9-38 (60 MINUTES)

1. Sales budget for 20×3:

Units

Price

Total

Light coils ……………………………………………………….

$ 14,400,000

Heavy coils ……………………………………………………..

13,600,000

2.

Production budget (in units) for 20x3:

Light

Coils

Heavy

Coils

Projected sales ……………………………………………………………………

Add: Desired inventories,

Total requirements ……………………………………………………………….

Deduct: Expected inventories, January 1, 20×3 ……………………..

3.

Raw-material purchases budget (in quantities) for 20×3:

Raw Material

Sheet

Metal

Copper

Wire

Platforms

Light coils (65,000 units projected

Heavy coils (41,000 units projected

Production requirements …………………………………

Add: Desired inventories, December 31, 20×3 …..

Total requirements …………………………………………..

Deduct: Expected inventories,

January 1, 20×3 ………………………………………….

Chapter 09 – Financial Planning and Analysis: The Master Budget

9-29

PROBLEM 9-38 (CONTINUED)

4.

Raw-material purchases budget for 20×3:

Raw Material

Raw Material

Required

(units)

Anticipated

Purchase

Price

Total

Sheet metal …………………………………………………….

Copper wire ……………………………………………………

5.

Direct-labor budget for 20×3:

Projected

Production

(units)

Hours

per

Unit

Total

Hours

Rate

Total

Cost

Light coils ……………………………….

$3,900,000

Heavy coils ……………………………..

6. Production overhead budget for 20×3:

Cost Driver

Quantity

Cost

Driver

Rate

Budgeted

Cost

Purchasing and material handling …………………..

725,000 lb.a

$.50

$362,500

Depreciation, utilities, and inspection ………………

106,000 coils b

Shipping ………………………………………………………..

General production overhead ………………………….

Chapter 09 – Financial Planning and Analysis: The Master Budget

9-30

PROBLEM 9-39 (60 MINUTES)

1.

Sales budget:

Box C

Box P

Total

Sales (in units)

500,000

500,000

2.

Production budget (in units):

Box C

Box P

Sales …………………………………………………………………………..

500,000

500,000

Add: Desired ending inventory …………………………..………..

Total units needed……………………………………………………….

505,000

515,000

Deduct: Beginning Inventory ……………………………………….

3.

Raw-material budget:

CORRUGATING MEDIUM

Box C

Box P

Total

Production requirements (number of boxes) ………

495,000

495,000

Raw material required per box (pounds) …………….

.2

.3

production (pounds) ……………………………………..

Add: Desired ending

raw-material inventory …………………………………..

Total raw-material needs …………………………………..

257,500

Deduct: Beginning raw-material inventory …………

Raw material to be purchased …………………………...

252,500

Cost of purchases (corrugating medium) …………..

$ 37,875

Raw material required for

9-31

PROBLEM 9-39 (CONTINUED)

PAPERBOARD

Box C

Box P

Total

Production requirement (number of boxes) ………..

495,000

495,000

Raw material required per box (pounds) …………….

.3

.7

Add: Desired ending

raw-material inventory …………………………………..

Total raw-material needs …………………………………..

500,000

Deduct: Beginning raw-material inventory …………

Raw material to be purchased …………………………...

485,000

Price (per pound) ……………………………………………..

Raw material required for

4.

Direct-labor budget:

Box C

Box P

Total

Production requirements (number of boxes)

495,000

495,000

Direct labor required per box (hours) …………………

Direct labor required for production (hours)

1,237.5

Direct-labor rate ……………………………………………….

5.

Production-overhead budget:

Indirect material ……………………………………………………………………………….

$ 15,750

Indirect labor ……………………………………………………………………………………

Utilities …………………………………………………………………………………………….

Property taxes ………………………………………………………………………………….

Insurance ……………………………………………………….………………………………..

Depreciation …………………………………………………………………………………….

43,500

Total overhead ………………………………………………………………………………….

$222,750

Chapter 09 – Financial Planning and Analysis: The Master Budget

9-32

PROBLEM 9-39 (CONTINUED)

6.

Selling and administrative expense budget:

Salaries and fringe benefits of sales personnel ………………………………….

$112,500

Advertising ………………………………………………………………………………………

Management salaries and fringe benefits …………………………………………..

Clerical wages and fringe benefits …………………………………………………….

Miscellaneous administrative expenses …………………………………………….

Total selling and administrative expenses ………………………………………….

$315,000

7.

Budgeted income statement:

Sales revenue [from sales budget, req. (1)] ………………………………………..

$1,650,000

Less: Cost of goods sold:

Gross margin ……………………………………………………………………………………

$1,170,000

Selling and administrative expenses ………………………………………………….

315,000

Income before taxes ………………………………………………………………………….

$ 855,000

Income tax expense (35%) …………………………………………………………………

299,250

Net income ……………………………………………………………………………………….

$ 555,750

*Calculation of production cost per unit:

(a)

Predetermined overhead rate

=

hours labor–direct of volume

overhead ingmanufactur budgeted

Chapter 09 – Financial Planning and Analysis: The Master Budget

9-33

PROBLEM 9-39 (CONTINUED)

(b)

Calculation of production cost per unit:

Box C

Box P

Direct material:

Paperboard

Corrugating medium

Direct labor:

Applied production overhead:

9-34

PROBLEM 9-40 (45 MINUTES)

1.

The revised operating budget for Vancouver Consulting Associates for

the fourth quarter is presented below. Supporting calculations follow:

VANCOUVER CONSULTING ASSOCIATES

REVISED OPERATING BUDGET

FOR THE FOURTH QUARTER OF 20X4

Revenue:

Consulting fees:

Computer system consulting …………………………………………………

$ 956,250

Management consulting ………………………………………………………..

936,000

Total consulting fees ……………………………………………………..

$1,892,250

Other revenue ……………………………………………………………………………..

20,000

Total revenue ……………………………………………………………………….

$1,912,250

Expenses:

Consultant salary expenses* …………………………..…………………………...

$1,021,300

Travel and related expenses ………………………………………………………..

General and administrative expenses …………………………………………..

Depreciation expense …………………………..……………………………………..

Corporate expense allocation ………………………………………………………

150,000

Total expenses ……………………………………………………………………..

$1,553,050

*$1,021,300 = $490,000 + $531,300. (See supporting calculations.)

9-35

PROBLEM 9-40 (CONTINUED)

Supporting calculations:

• Schedule of projected revenues for the fourth quarter of 20×4:

Computer

System

Consulting

Management

Consulting

Third Quarter:

Revenue ………………………………………………………………….

$843,750

$630,000

Hourly billing rate ……………………………………………………

÷ $150

÷ $180

Billable hours ………………………………………………………….

Number of consultants …………………………………………….

Hours per consultant ……………………………………………….

Fourth-quarter planned increase …………………………………..

Billable hours per consultant ………………………………………..

Billable hours ………………………………………………………………

Chapter 09 – Financial Planning and Analysis: The Master Budget

9-36

PROBLEM 9-40 (CONTINUED)

• Schedules of projected salaries, travel, general and administrative, and allocated

corporate expenses:

Computer

System

Consulting

Management

Consulting

Compensation:

Existing consultants:

Annual salary …………………………………………………..

$ 92,000

$100,000

Quarterly salary ……………………………………………….

$ 23,000

$ 25,000

Planned increase (10%) ……………………………………

Total fourth-quarter salary per consultant …………

Number of consultants …………………………………….

Total ………………………………………………………………………

$379,500

$275,000

New consultants at old salary (3 $25,000) ……………..

Total salary …………………………………………………………….

$379,500

$350,000

Benefits (40%) ………………………………………………………..

Total compensation …………………………………………

$531,300

Travel expenses:

Computer system consultants (425 hrs. 15) ………….

6,375

Management consultants (400 hrs. 13) ………………….

5,200

Total hours ………………………………………………………

11,575

Rate per hour* ……………………………………………………….

Total travel expense …………………………………………

$115,750

General and administrative ($200,000 93%) ………………..

Corporate expense allocation ($100,000 150%) …………..

*Third-quarter travel expense

÷

hours

=

rate

2.

An organization would prepare a revised operating budget when the assumptions

underlying the original budget are no longer valid. The assumptions may involve

9-37

PROBLEM 9-41 (40 MINUTES)

1. Strategic planning identifies the overall objective of an organization and generally

considers the impact of external factors such as competitive forces, market demand,

2. For each of the financial objectives established by the board of directors and

president of Fit-for-Life Foods, Inc., the calculations to determine whether John

Winslow’s budget attains these objectives are presented in the following table.

CALCULATION OF FINANCIAL OBJECTIVES: FIT-FOR-LIFE FOODS, INC.

Objective

Attained/

Not Attained

Calculations

Maintain cost of goods sold at or

Not attained

$1,339,000*/$1,895,500 = 70.6% (rounded)

Increase sales by 12%

($1,700,000 × 1.12 = $1,904,000)

Not attained

($1,895,500 – $1,700,000)/$1,700,000 = 11.5%

3. The accounting adjustments contemplated by John Winslow are unethical because

they will result in intentionally overstating income by understating the cost of goods

sold. The specific standards of ethical conduct for management accountants

violated by Winslow are as follows:

9-38

PROBLEM 9-41 (CONTINUED)

Competence. By making the accounting adjustments, Winslow violated the

PROBLEM 9-42 (120 MINUTES)

1.

Sales budget:

20×0

20×1

December

January

February

March

First

Quarter

Total sales ……………………

$800,000

$880,000

$968,000

$1,064,800

$2,912,800

Cash sales* ………………….

Sales on account† ………..

*25% of total sales.

2.

Cash receipts budget:

20×1

January

February

March

First

Quarter

Cash sales ……………………………………..

$220,000

$242,000

$266,200

$ 728,200

Cash collections from credit

*10% of current month’s credit sales.

Cash collections from credit

sales made during current

9-39

PROBLEM 9-42 (CONTINUED)

3.

Purchases budget:

20×0

20×1

December

January

February

March

First

Quarter

Budgeted cost of

goods sold ………………

$560,000

$616,000

$677,600

$745,360

$2,038,960

Total goods

$954,800

inventory…………………

Add: Desired

†The desired ending inventory for the quarter is equal to the desired ending inventory

on March 31, 20×1.

**The beginning inventory for the quarter is equal to the December ending inventory.