Chapter 09 – Financial Planning and Analysis: The Master Budget

9-1

CHAPTER 9

Financial Planning and Analysis:

The Master Budget

ANSWERS TO REVIEW QUESTIONS

9-1 A budget facilitates communication and coordination by making each manager

9-2 An example of using the budget to allocate resources in a university is found in the

area of research funds and grants. Universities typically have a limited amount of

9-3 A master budget, or profit plan, is a comprehensive set of budgets covering all

phases of an organization’s operations for a specified period of time. The master

9-5 General economic trends are important in forecasting sales in the airline industry.

The overall health of the economy is an important factor affecting the extent of

9-6 Operational budgets specify how an organization’s operations will be carried out to

meet the demand for its goods and services. The operational budgets prepared in a

Chapter 09 – Financial Planning and Analysis: The Master Budget

9-2

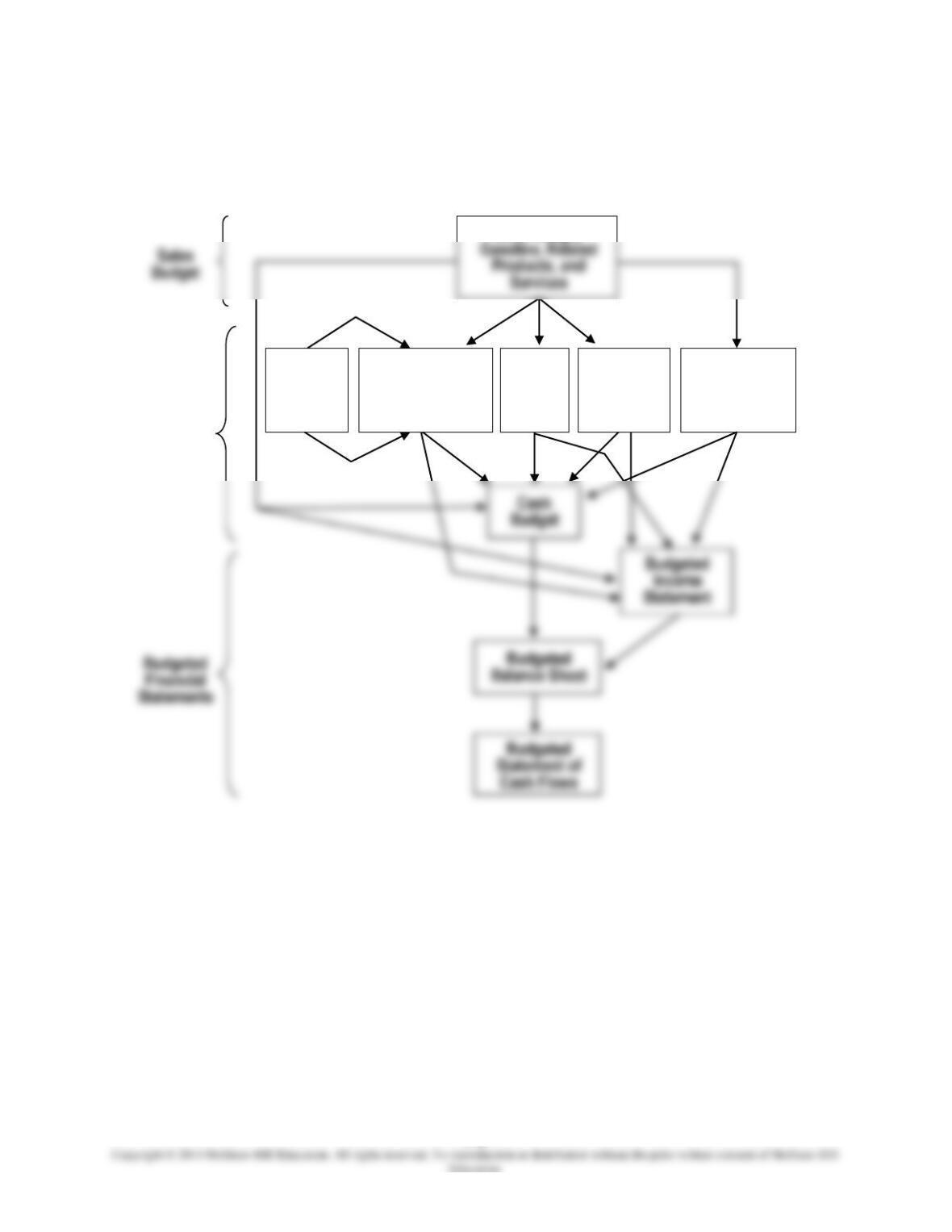

Flowchart for Review Question 9-4

Operational

Budgets

Ending

Inventory

Budget:

Gasoline

Materials Budget:

Gasoline and

Related Products

Labor

Budget

Overhead

Budget

Selling and

Administrative

Expense

Budget

Sales Budget:

Chapter 09 – Financial Planning and Analysis: The Master Budget

9-3

9-7 Application of activity-based costing to the budgeting process yields activity-based

budgeting (ABB). In the logic of activity-based costing, the company engages in a

9-8 E-budgeting stands for an electronic and enterprise-wide budgeting process. Under

this approach the information needed to construct a budget is gathered via the

9-9 The city of Boston could use budgeting for planning purposes in many ways. For

example, the city’s personnel budget would be important in planning for required

9-10 The budget director, or chief budget officer, specifies the process by which budget

data will be gathered, collects the information, and prepares the master budget. To

9-11 The budget manual says who is responsible for providing various types of

information, when the information is required, and what form the information is to

9-12 A company’s board of directors generally has final approval over the master budget.

By exercising its authority to make changes in the budget and grant final approval,

Chapter 09 – Financial Planning and Analysis: The Master Budget

9-4

9-13 A master budget is based on many assumptions and predictions of unknown

parameters. For example, the sales budget is built on an assumption about the

9-14 The difference between the revenue or cost projection that a person provides in the

budgeting process and a realistic estimate of the revenue or cost is called budgetary

9-15 An organization can reduce the problem of budgetary slack in several ways. First, it

9-16 The idea of participative budgeting is to involve employees throughout an

organization in the budgetary process. Such participation can give employees the

9-17 This comment is occasionally heard from people who have started and run their own

small business for a long period of time. These individuals have great knowledge in

9-5

9-18 In developing a budget to meet your college expenses, the primary steps would be to

project your cash receipts and your cash disbursements. Your cash receipts could

9-19 Firms with international operations face a variety of additional challenges in

preparing their budgets.

• A multinational firm’s budget must reflect the translation of foreign currencies

9-20 Most of the differences in budgeting between manufacturing and non-manufacturing

firms derive from the need for inventories in manufacturing. Because of this,

additional budget schedules are generally required in manufacturing firms. These

often include:

(a) Production budget

Chapter 09 – Financial Planning and Analysis: The Master Budget

9-6

SOLUTIONS TO EXERCISES

EXERCISE 9-21 (20 MINUTES)

1.

The total required production is 131,144 units, computed as follows:

Budgeted Sales

(in units)

Planned Ending Inventory

(in units)

June

32,000 (40,000 80%)

July

40,000 (given)

August

October

Sales in units:

July ………………………………………………………………………………………………….

August ……………………………………………………………………………………………..

September ………………………………………………………………………………………..

44,100

Total for third quarter ………………………………………………………………………..

126,100

Add: Desired ending inventory, September 30 ……………………………………

Subtotal ……………………………………………………………………………………………

163,144

Total required production ………………………………………………………………….

131,144

2.

Assumed production during third quarter (in units) …………………………...

120,000

Raw-material requirements per unit of product (in pounds) ………………..

4

Raw material required for production in third quarter (in pounds) ……….

480,000

Subtotal ……………………………………………………………………………………………

600,000

Deduct: Ending raw-material inventory, June 30 …………………………………

Raw material to be purchased during third quarter (in pounds) …………..

460,000

Total raw-material purchases during third quarter ………………………………

9-7

EXERCISE 9-22 (25 MINUTES)

1.

Cash collections in October:

Month of Sale

Amount Collected in October

July ……………………………………………………..

$150,000 4%

$ 6,000

August …………………………………………………

17,500

October ………………………………………………..

225,000 70%

157,500

2.

Cash collections in fourth quarter from credit sales in fourth quarter.

Amount Collected

Month of Sale

Credit

Sales

October

November

December

October ……………………………………..

$225,000

$157,500

$ 33,750

$ 22,500

November ………………………………….

–

December ………………………………….

–

Total ………………………………………….

$157,500

$208,750

Chapter 09 – Financial Planning and Analysis: The Master Budget

9-8

EXERCISE 9-23 (20 MINUTES)

1.

July

August

September

Sales …………………………………………………..

$240,000

$180,000

$270,000a

Cash receipts:

From cash sales ………………………………

$ 120,000b

$ 90,000c

$135,000

From sales on account …………………….

108,000d

102,000

117,000e

2.

Accounts payable, 12/31/x0 ……………………………………………………….

€ 600,000

Purchases of goods and services on account during 20×1 ………….

2,400,000

Payments of accounts payable during 20×1 ……………………………….

Accounts payable, 12/31/x1 ……………………………………………………….

3.

Accounts receivable, 12/31/x0 ……………………………………………………

¥ 1,700,000

Sales on account during 20×1 ……………………………………………………

4,500,000

Collections of accounts receivable during 20×1 ………………………….

4.

Accumulated depreciation, 12/31/x0 …………………………………………..

$ 405,000

Depreciation expense during 20×1 …………………………………………….

75,000

Accumulated depreciation, 12/31/x1 …………………………………………..

$ 480,000

5.

Retained earnings, 12/31/x0 ………………………………………………………

$1,537,500

Net income for 20×1 ……………………………………………………….…………

Dividends paid in 20×1 ………………………………………………………………

0

Retained earnings, 12/31/x1 ………………………………………………………

$1,837,500

Chapter 09 – Financial Planning and Analysis: The Master Budget

9-9

EXERCISE 9-24 (15 MINUTES)

1.

Production (in units) required for the year:

Sales for the year ………………………………………………………………………………

3,360,000

Add: Desired ending finished-goods inventory on December 31 ………….

Deduct: Beginning finished-goods inventory on January 1 ………………….

560,000

Required production during the year ………………………………………………….

3,150,000

2.

Purchases of raw material (in units), assuming production of 3,500,000 finished units:

Add: Desired ending inventory on December 31 ………………………………….

Deduct: Beginning inventory on January 1 …………………………………………

245,000

Required raw-material purchases during the year ……………………………….

7,070,000

Chapter 09 – Financial Planning and Analysis: The Master Budget

9-10

EXERCISE 9-25 (20 MINUTES)

1.

WHITE MOUNTAIN FURNITURE SHOWROOM

EXPECTED CASH COLLECTIONS

NOVEMBER

Month

Sales

Percent

Expected

Collections

September ………………………………….

$150,000

9%

$ 13,500

October ………………………………………

195,000

November …………………………………..

165,000

2.

WHITE MOUNTAIN FURNITURE SHOWROOM

EXPECTED CASH DISBURSEMENTS

NOVEMBER

October purchases to be paid in November …………………………………………

$135,000

Less: 2% cash discount ……………………………………………………………………..

2,700

Net …………………………………………………………………………………………………

$132,300

Cash disbursements for expenses ………………………………………………………

3.

WHITE MOUNTAIN FURNITURE SHOWROOM

EXPECTED CASH BALANCE

NOVEMBER 30

Balance, November 1 ………………………………………………………………………….

$ 55,000

Add: Expected collections ………………………………………………………………….

168,000

Less: Expected disbursements …………………………………………………………..

Chapter 09 – Financial Planning and Analysis: The Master Budget

9-11

EXERCISE 9-26 (30 MINUTES)

Answers will vary widely, depending on the governmental unit selected and the budgetary

EXERCISE 9-27 (30 MINUTES)

1.

Budgeted cash collections for December:

Month of Sale

Collections in December

2.

Budgeted income (loss) for December:

Sales revenue ……………………………………………………………..

$440,000

Less: Cost of goods sold (75% of sales) ……………………….

330,000

Gross margin (25% of sales) ………………………………………..

$110,000

Less: Operating expenses: ………………………………………….

Bad debts expense (2% of sales) ………………………..

Depreciation ($432,000/12) ………………………………….

Other expenses ………………………………………………….

Total operating expenses ……………………………………

Chapter 09 – Financial Planning and Analysis: The Master Budget

9-12

EXERCISE 9-27 (CONTINUED)

3.

Projected balance in accounts payable on December 31:

The December 31 balance in accounts payable will be equal to December’s purchases of

merchandise. Since the store’s gross margin is 25 percent of sales, its cost of goods

sold must be 75 percent of sales.

Month

Sales

Cost of

Goods

Sold

Amount Purchased in December

December ………………..

$440,000

$330,000

$330,000 20%

$ 66,000

January …………………..

240,000

Therefore, the December 31 balance in accounts payable will be $306,000.

Chapter 09 – Financial Planning and Analysis: The Master Budget

9-13

EXERCISE 9-28 (20 MINUTES)

Memorandum

Date:

Today

To:

President, East Bank of Mississippi

From:

I.M. Student and Associates

Subject:

Budgetary slack

Budgetary slack is the difference between a budget estimate that a person provides

and a realistic estimate. The practice of creating budgetary slack is called padding the

budget. The primary negative consequence of slack is that it undermines the credibility

9-14

EXERCISE 9-29 (20 MINUTES)

1.

Total Sales in January 20×5

$200,000

$260,000

$320,000

Cash receipts in January, 20×5

From December sales on account …………

$ 14,250*

$ 14,250

$ 14,250

From January cash sales ……………………..

150,000†

From January sales on account ……………

*$14,250 = $380,000 .25 .15

**$40,000 = $200,000 .25 .80

2.

Operational plans depend on various assumptions. Usually there is uncertainty about

EXERCISE 9-30 (25 MINUTES)

1.

Direct professional labor budget for the month of June:

Professional services in June:

Total direct professional labor ……………………………………….

hours

Total direct professional labor cost ……………………………….

Chapter 09 – Financial Planning and Analysis: The Master Budget

9-15

EXERCISE 9-30 (CONTINUED)

2.

Cash collections during June:

May

June

Half-hour visits (4,000 80%) ………………………………………..

3,200

3,200

Billing rate ……………………………………………………………………

$60

$60

Total billings for half-hour visits …………………………………….

$192,000

$192,000

800

800

Billing rate ……………………………………………………………………

Total billings for one-hour visits …………………………………….

$ 84,000

$ 84,000

Total billings during month ……………………………………………

$276,000

$276,000

Collections during June ………………………………………………..

$ 27,600

$248,400

3. Overhead and administrative expense budget for June:

Patient registration and records (4,000 visits $3.00 per visit) …. $12,000

Chapter 09 – Financial Planning and Analysis: The Master Budget

9-16

SOLUTIONS TO PROBLEMS

PROBLEM 9-31 (30 MINUTES)

1. Schedule of cash collections:

January

February

March

Collection of accounts receivable:

$165,000 x 20% …………………………………..

$ 33,000

Collection of January sales ($450,000):

60% in January; 35% in February ………..

$157,500

Collection of February sales ($540,000):

60% in February; 35% in March …………..

$189,000

Collection of March sales ($555,000):

60% in March ……………………………………..

Sale of equipment ……………………………………

15,000

Total cash collections ………………………..

$303,000

$481,500

$537,000

2. Schedule of cash disbursements:

January

February

March

Payment of accounts payable ………………….

$ 66,000

Payment of January purchases ($270,000):

70% in January; 30% in February ………..

$ 81,000

Payment of February purchases ($300,000):

70% in February; 30% in March …………..

$ 90,000

Payment of March purchases ($420,000):

70% in March ……………………………………..

Cash operating costs ………………………………

93,000

72,000

Total cash disbursements …………………..

$348,000

$363,000

$519,000

Chapter 09 – Financial Planning and Analysis: The Master Budget

9-17

PROBLEM 9-31 (CONTINUED)

3. Schedule of cash needs:

January

February

March

Beginning cash balance……………………….

$ 60,000

$ 60,000

$132,900

Total receipts…………………………………….

303,000

481,500

537,000

$541,500

$669,900

Less: Total disbursements……………………

348,000

363,000

519,000

$ 15,000

$178,500

$150,900

Financing:

45,000

(600)*

$ 60,000

$132,900

$150,900

Chapter 09 – Financial Planning and Analysis: The Master Budget

9-18

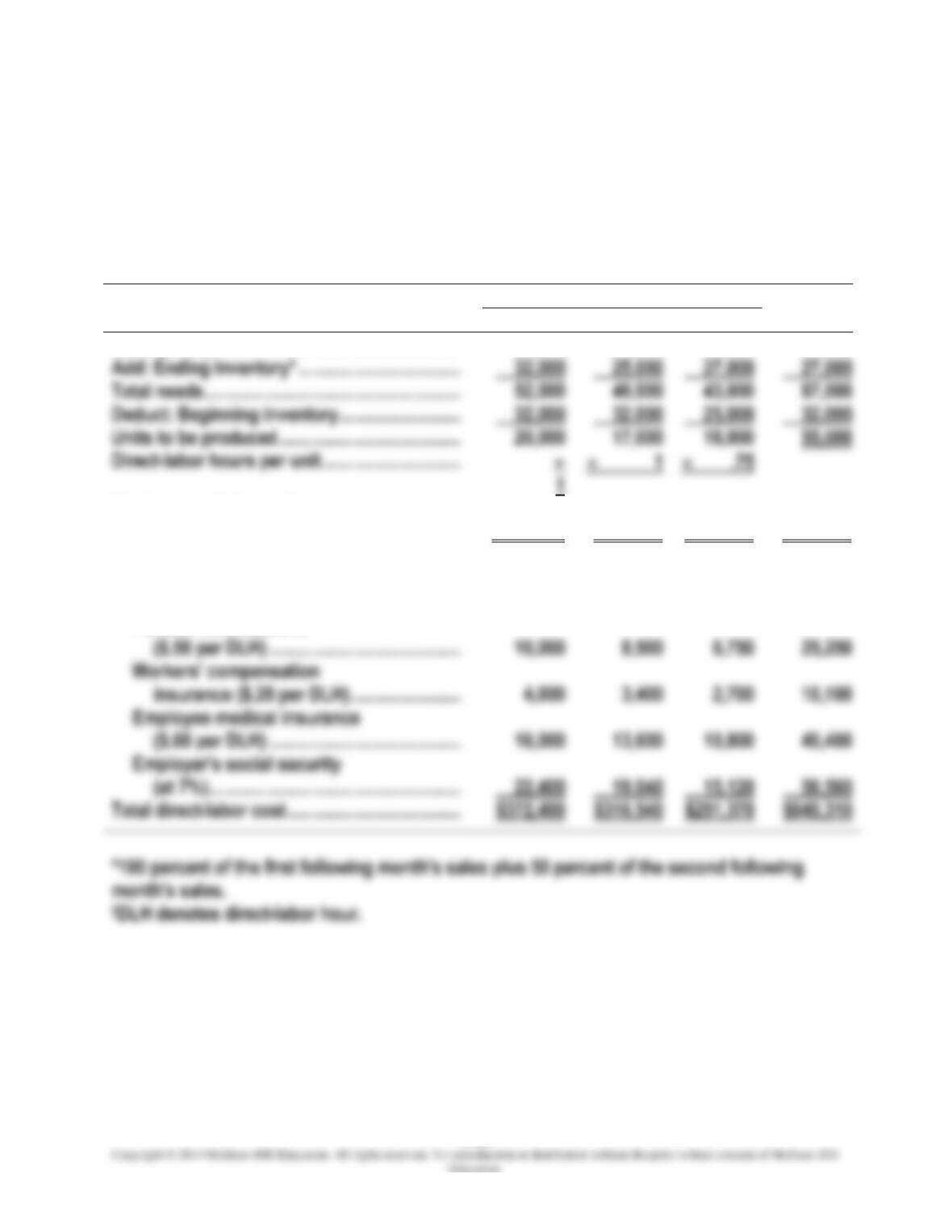

PROBLEM 9-32 (40 MINUTES)

1.

Production and direct-labor budgets

SHADY SHADES, INC.

BUDGET FOR PRODUCTION AND DIRECT LABOR

FOR THE FIRST QUARTER OF 20X1

Month

January

February

March

Quarter

Sales (units) ……………………………………………..

20,000

24,000

16,000

60,000

Add: Ending inventory* ……………………………..

32,000

25,000

27,000

27,000

Total needs ……………………………………………….

52,000

49,000

43,000

87,000

Deduct: Beginning inventory ……………………..

32,000

32,000

25,000

32,000

Units to be produced …………………………………

20,000

17,000

18,000

55,000

Total hours of direct labor

time needed ………………………………………….

20,000

17,000

13,500

50,500

Direct-labor costs:

Wages ($16.00 per DLH)† ……………………….

$320,000

$272,000

$216,000

$808,000

($.50 per DLH) …………………………………..

Workers’ compensation

insurance ($.20 per DLH) ……………………

Employer’s social security

(at 7%) ………………………………………………

22,400

19,040

15,120

56,560

Pension contributions

Chapter 09 – Financial Planning and Analysis: The Master Budget

9-19

PROBLEM 9-32 (CONTINUED)

2.

Use of data throughout the master budget (excluding financial statement budgets):

Components of the master budget, other than the production budget and the direct-

labor budget, that would also directly or indirectly use the sales data include the

following:

• Sales budget

• Cost-of-goods-sold budget

• Selling and administrative expense budget

Components of the master budget, other than the production budget and the direct-

labor budget, that would also directly or indirectly use the production data include the

following:

• Direct-material budget

• Production-overhead budget

Components of the master budget, other than the production budget and the direct-

labor budget, that would also directly or indirectly use the direct-labor-hour data

include the following:

• Production-overhead budget (for determining the overhead application rate)

• Cash budget

Components of the master budget, other than the production budget and the direct-

labor budget, that would also directly or indirectly use the direct-labor cost data

include the following:

• Production-overhead budget (for determining the overhead application rate)

• Cost-of-goods-sold budget

• Cash budget

Chapter 09 – Financial Planning and Analysis: The Master Budget

9-20

PROBLEM 9-32 (CONTINUED)

3. Production overhead budget:

SHADY SHADES, INC.

PRODUCTION OVERHEAD BUDGET

FOR THE FIRST QUARTER OF 20X1

Month

January

February

March

Quarter

Shipping and handling ……………

$ 60,000

$ 72,000

$48,000

$180,000

Total production overhead ………

$360,000

$327,000

$957,750

PROBLEM 9-33 (40 MINUTES)

1. Niagra Chemical Company’s production budget (in gallons) for the three products for

20×2 is calculated as follows:

Yarex

Darol

Norex

Sales for 20×2 ………………………………………

Total required ………………………………………

Deduct: Inventory, 12/31/x1

Required production in 20×2 …………………

2. The company’s conversion cost budget for 20×2 is shown in the following schedule:

Conversion hours required:

Yarex (120,800 × .07) …………………………….

Darol (79,200 × .10) ………………………………

Norex (50,800 × .16) ……………………………..

Total hours ………………………………………….