*EXERCISE 9-19

(a) Declining-balance method:

(b) Units-of-activity method:

SOLUTIONS TO PROBLEMS

Item Land Building Other Accounts

1 $280,000

PROBLEM 9-1A

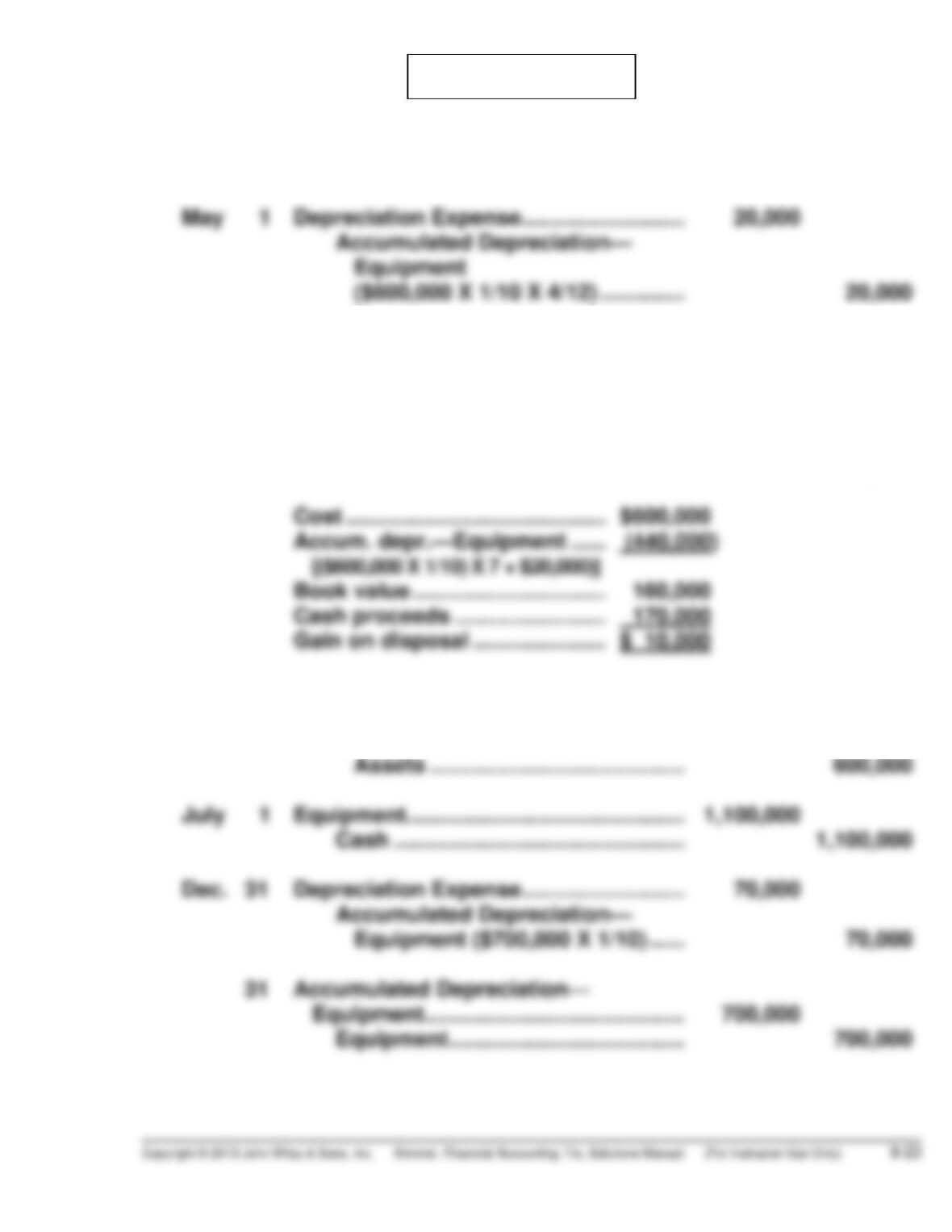

(a) April 1 Land ………………………………………………. 2,200,000

Cash ………………………………………… 2,200,000

1 Accumulated Depreciation—

Equipment ……………………………………. 440,000

Cash ………………………………………………. 170,000

Equipment ………………………………… 600,000

Gain on Disposal of Plant

Assets …………………………………… 10,000

June 1 Cash ………………………………………………. 1,600,000

Land …………………………………………. 1,000,000

Gain on Disposal of Plant

PROBLEM 9-2A

PROBLEM 9-2A (Continued)

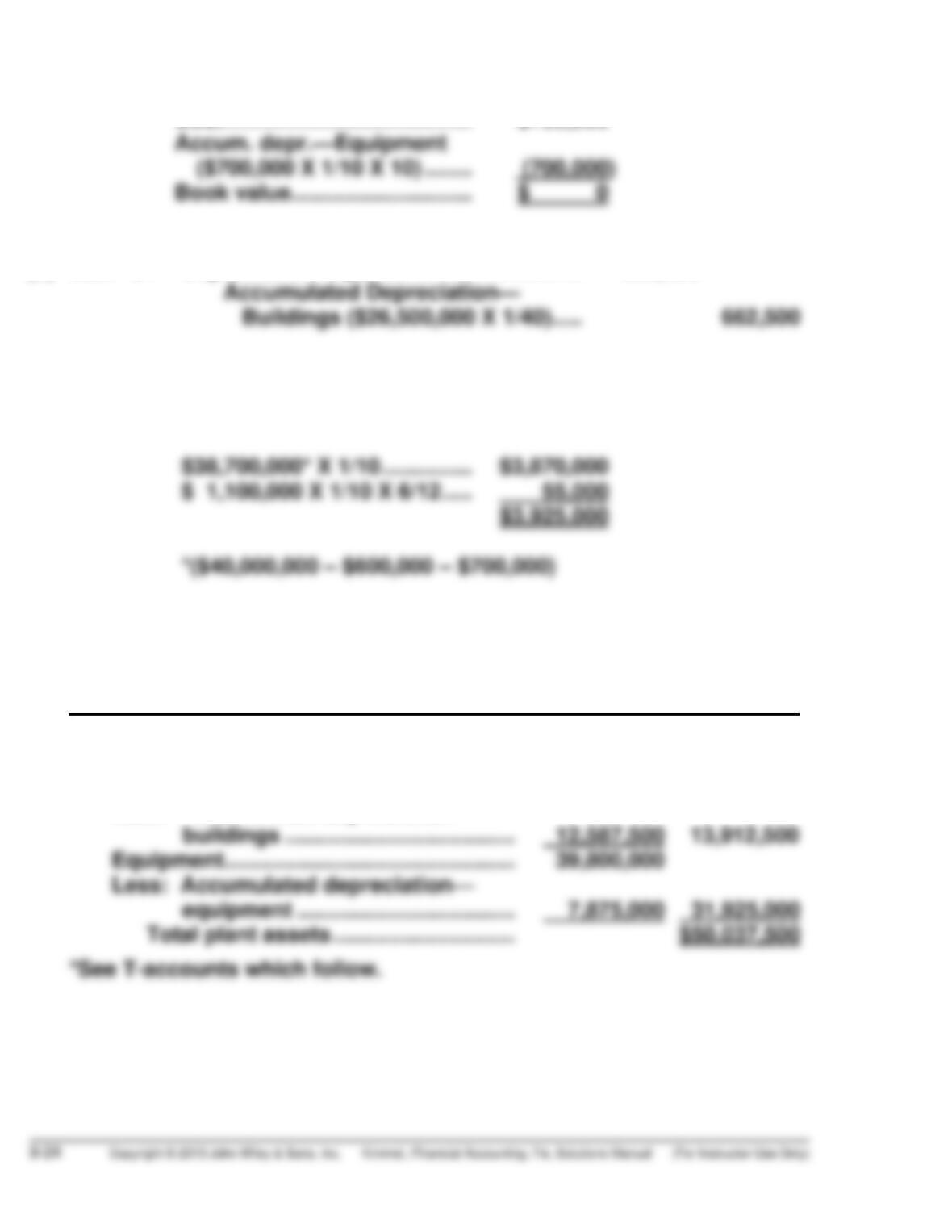

Cost ………………………………….. $700,000

(b) Dec. 31 Depreciation Expense ………………………. 662,500

31 Depreciation Expense ………………………. 3,925,000

Accumulated Depreciation—

Equipment ………………………………. 3,925,000

(c) NAVARO CORPORATION

Partial Balance Sheet

December 31, 2015

Plant Assets*

Land ………………………………………………… $ 4,200,000

Buildings ………………………………………….. $26,500,000

Less: Accumulated depreciation—

PROBLEM 9-2A (Continued)

Land

12/31/14 3,000,000 6/1/14 1,000,000

Buildings

12/31/14 26,500,000

Equipment

12/31/14 40,000,000 05/01/15 600,000

Accumulated Depreciation—Buildings

12/31/14 11,925,000

Accumulated Depreciation—Equipment

05/01/15 440,000 12/31/14 5,000,000

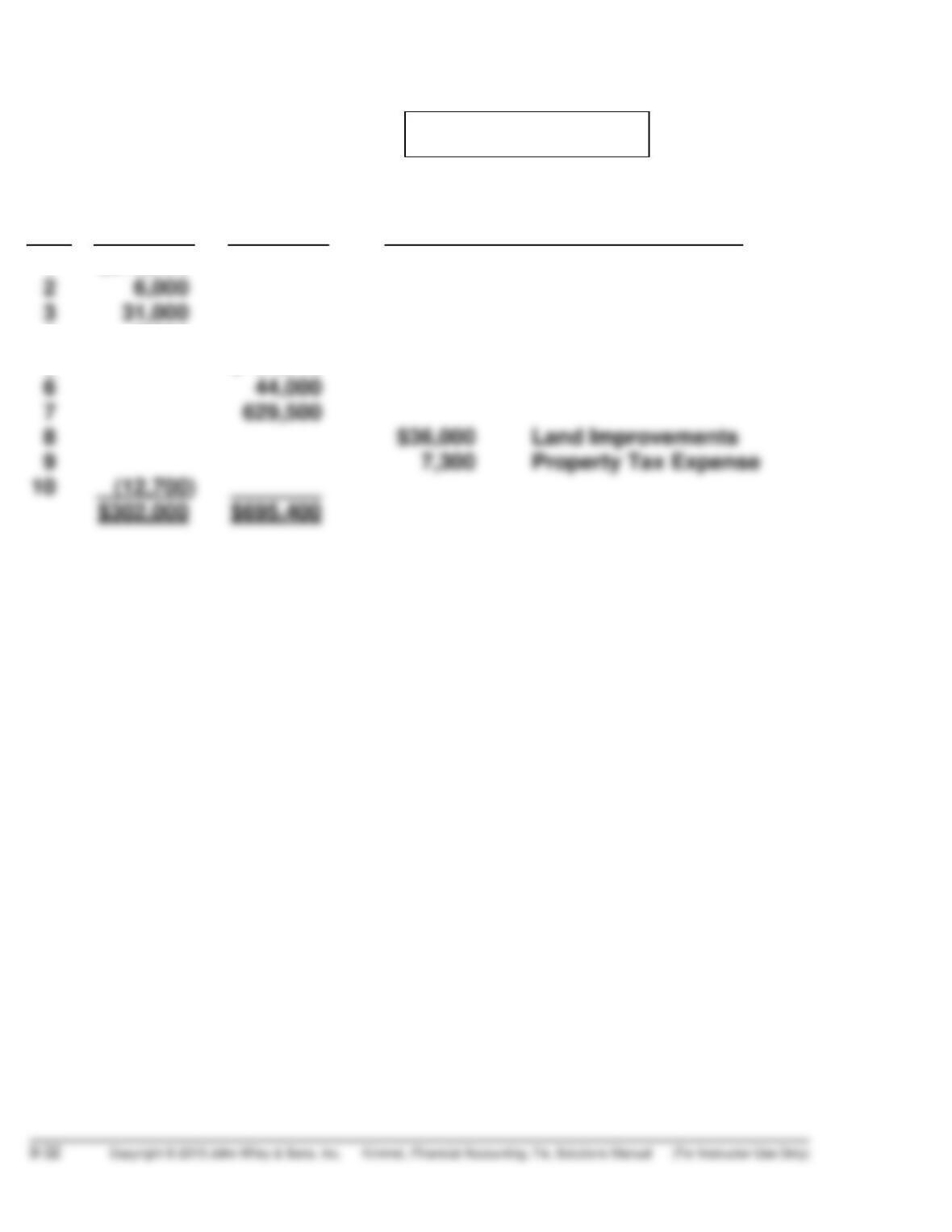

Jan. 1 Accumulated Depreciation—Equipment …… 71,000

June 30 Depreciation Expense ……………………………… 3,000

June 30 Cash ……………………………………………………….. 12,000

Accumulated Depreciation—Equipment …… 21,000

Equipment ………………………………………… 30,000

Dec. 31 Depreciation Expense ……………………………… 3,800

31 Loss on Disposal of Plant Assets …………….. 10,600

Accumulated Depreciation—Equipment …… 22,800

Equipment ………………………………………… 33,400

Cost ………………………………………………………… $33,400

Accumulated Depreciation—Equipment

[($33,400 – $3,000) X 1/8 X 6] …………………. (22,800)

PROBLEM 9-3A

(a) Jan. 2 Patents ………………………………………………… 46,800

Cash ………………………………………………. 46,800

Jan.– Research and Development Expense ……. 230,000

June Cash ………………………………………………. 230,000

Sept. 1 Advertising Expense …………………………….. 40,000

Cash ………………………………………………. 40,000

(b) Dec. 31 Amortization Expense ………………………….. 11,700

Patents …………………………………………… 11,700

[($60,000 X 1/10) + ($46,800 X 1/9) +

($20,000 X 1/20 X 6/12)]

(c) Intangible Assets

Patents ($126,800 cost less $17,700 amortization) (1) ……… $109,100

(d) The intangible assets of Cedeno Corporation consist of two patents

and two copyrights. One patent with a cost of $60,000 is being amor-

tized over 10 years. In addition, legal costs of $46,800 incurred in the suc-

PROBLEM 9-4A

1. Research and Development Expense …………………… 160,000

Patents ………………………………………………………… 160,000

Patents ……………………………………………………………….. 8,000

Amortization Expense

[$10,000 – ($40,000 X 1/20)] ………………………… 8,000

PROBLEM 9-5A

(a) Danner London

1. $240,000 $300,000

Return on assets = 7.5% = 10.0%

$3,200,000 $3,000,000

(b) Based on the asset turnover, London Corp. is more effective in using

assets to generate sales. Its asset turnover is 11% higher than

Danner’s ratio.

PROBLEM 9-6A

(a) Accumulated

Depreciation

Year Computation 12/31

MACHINE 1

2012 $84,000* X 1/8 = $10,500 $10,500

MACHINE 2

2013 $85,000 X 40%* X 6/12 = $17,000 $17,000

*(1/5) X 2

MACHINE 3

2013 800 X $2.00a = $ 1,600 $ 1,600

(b) Year Depreciation Expense

MACHINE 2

PROBLEM 9-7A

(a) STRAIGHT-LINE DEPRECIATION

Computation End of Year

Annual

Depreciable Depreciation Depreciation Accumulated Book

Years Cost X Rate = Expense Depreciation Value

2014 $220,000* 25%** $ 55,000 $ 55,000 $195,000

DOUBLE-DECLINING-BALANCE DEPRECIATION

Computation End of Year

Book Value Annual

Beginning Depreciation Depreciation Accumulated Book

Years of Year X Rate = Expense Depreciation Value

2014 $250,000 50%* $125,000 $125,000 $125,000

2015 125,000 50% 62,500 187,500 62,500

(b) Straight-line depreciation provides the lower amount for 2014 deprecia-

tion expense ($55,000) and, therefore, the higher 2014 income. Over the

(c) Double-declining-balance depreciation provides the higher amount

*PROBLEM 9-8A

Item Land Building Other Accounts

1 $270,000

4 7,700

5 $ 21,900

PROBLEM 9-1B

(a) April 1 Land ……………………………………………….. 2,600,000

Cash …………………………………………. 2,600,000

May 1 Depreciation Expense ………………………. 25,000

Accumulated Depreciation—

Equipment …………………………………. 750,000

Gain on Disposal of Plant

Assets ……………………………………. 17,000

Cost ………………………………………. $750,000

June 1 Cash ………………………………………………. 2,000,000

Gain on Disposal of Plant

Dec. 31 Depreciation Expense ……………………… 47,000

Accumulated Depreciation—

PROBLEM 9-2B

PROBLEM 9-2B (Continued)

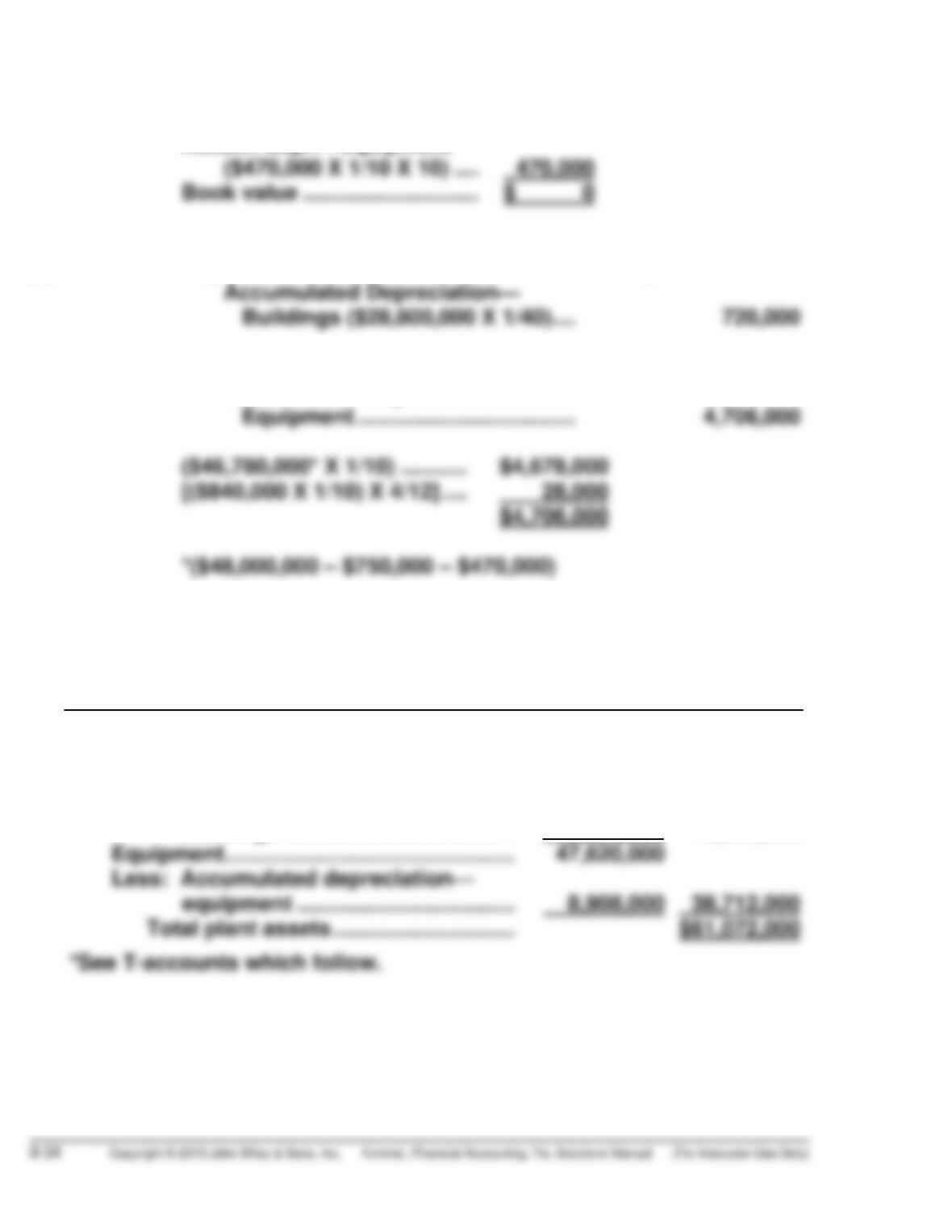

Cost ………………………………….. $470,000

Accum. depr.—equipment

(b) Dec. 31 Depreciation Expense ……………………… 720,000

31 Depreciation Expense ……………………… 4,706,000

Accumulated Depreciation—

(c) TONG CORPORATION

Partial Balance Sheet

December 31, 2014

Plant Assets*

Land ………………………………………………… $ 5,800,000

Buildings ………………………………………….. $28,800,000

Less: Accumulated depreciation—

buildings ……………………………….. 12,240,000 16,560,000

PROBLEM 9-2B (Continued)

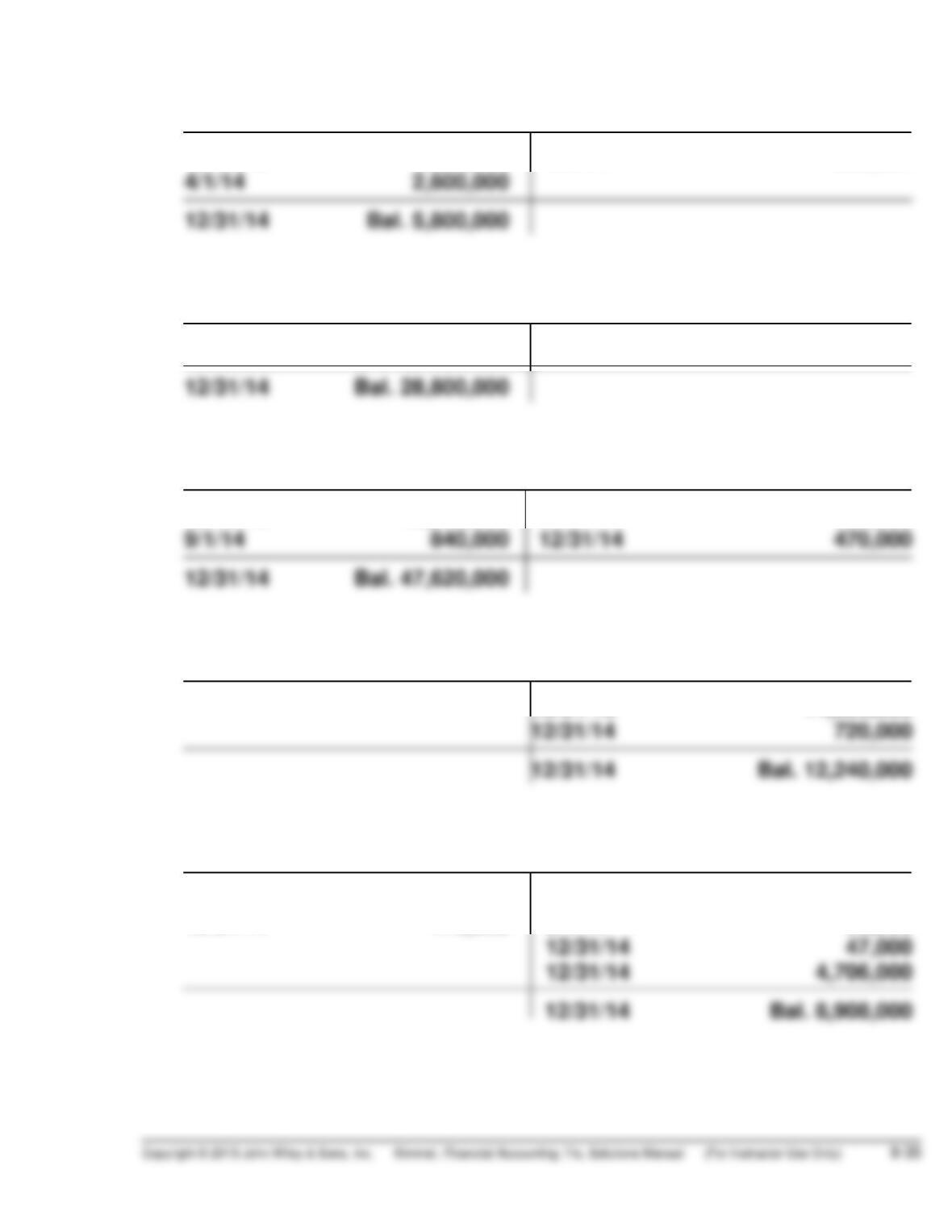

Land

12/31/13 4,000,000 6/1/14 800,000

Buildings

12/31/13 28,800,000

Equipment

12/31/13 48,000,000 5/1/14 750,000

Accumulated Depreciation—Buildings

12/31/13 11,520,000

Accumulated Depreciation—Equipment

5/1/14 400,000 12/31/13 5,000,000

12/31/14 470,000 5/1/14 25,000

Jan. 1 Accumulated Depreciation—

Equipment

Mar. 31 Depreciation Expense ………………………… 1,550

Cash ………………………………………………….. 25,000

Accumulated Depreciation—

Cost …………………………………………………… $43,400

Accumulated Depreciation—Equipment

Dec. 31 Depreciation Expense ………………………… 4,500

Accumulated Depreciation—

Dec. 31 Accumulated Depreciation—

Equipment

PROBLEM 9-3B

(a) Jan. 2 Patents …………………………………………………. 45,000

Cash ………………………………………………… 45,000

Jan.- Research and Development Expense …….. 220,000

June Cash ………………………………………………… 220,000

(b) Dec. 31 Amortization Expense …………………………… 12,550

Patents …………………………………………….. 12,550

(c) Intangible Assets

Patents ($137,000 cost less $19,550 amortization) (1) ……… $117,450

Copyrights ($168,000 cost less $24,600 amortization) (2) … 143,400

(d) The intangible assets of Venable Company consist of two patents and

two copyrights. One patent with a cost of $70,000 is being amortized

PROBLEM 9-4B

1. Research and Development Expense ………………… 225,000

Patents ……………………………………………………… 225,000

PROBLEM 9-5B

(a) Quiver Swaze

1. $800,000 $920,000

Return on assets = 26.7% = 34.1%

$3,000,000 $2,700,000

(b) Based on the asset turnover, Swaze Corp. is more effective in using

assets to generate sales. Its asset turnover is 16% higher than

Quiver’s ratio.

PROBLEM 9-6B

(a) Accumulated

Depreciation

Year Computation 12/31

MACHINE 1

2012 $63,000* X 1/7 X 6/12 = $4,500 $ 4,500

MACHINE 2

2013 $64,000 X 50%* X 9/12 = $24,000 $24,000

2014 $40,000 X 50% = $20,000 44,000

Depreciation

(b) Year Expense

MACHINE 2

*PROBLEM 9-7B