255

CHAPTER 9

METRIC ANALYSIS OF FINANCIAL STATEMENTS

CLASS DISCUSSION QUESTIONS

1. Horizontal analysis is the percentage analy-

sis of increases and decreases in compara-

tive financial statements. Each item on the

most recent statement is compared with the

related item on one or more earlier state-

ments in terms of the following:

a. Amount of increase or decrease.

b. Percent of increase or decrease.

The percent change in the cash balances at

the end of the preceding year from the end

2. Comparative statements provide information

as to changes between dates or periods.

Trends indicated by comparisons may be far

more significant than the data for a single

date or period.

3. Before this question can be answered, the

increase in net income should be compared

with changes in sales, expenses, and assets

4. You should first determine if the expense

amount in the base year (denominator) is

significant. A 70% or more increase of a

small expense item may be of little concern.

However, if the expense amount in the base

year is significant, then over a 70% increase

may require further investigation.

quick ratio, along with the amount of working

capital, gives a better analysis of the current

position. Such a comparison shows the

following:

Current Preceding

Year Year

Working capital ……. $162,000 $138,000

Current ratio ………… 2.8 3.3

Quick ratio …………… 0.9 1.2

Procter & Gamble, in contrast, sells almost

exclusively to other businesses, such as

Walmart. Such sales are “on account,” and

thus create accounts receivable that must

be collected. A recent financial statement

showed Walmart’s accounts receivable turn-

ing 64 times, while Procter & Gamble’s

turned only 6 times.

8. No, an accounts receivable turnover of 9

are running beyond 40 days. A substantial

amount of past-due accounts of doubtful

collectibility may be on the books.

9. a. A high inventory turnover minimizes the

amount invested in inventories, thus

freeing funds for more advantageous

use. Storage costs, administrative ex-

256

10. The ratio of fixed assets to long-term liabilities

increased from 3.6 ($1,260,000 ÷ $350,000)

for the preceding year to 4.0 ($1,800,000 ÷

$450,000) for the current year, indicating that

the company is in a stronger position now than

in the preceding year to borrow additional

funds on a long-term basis.

11. a. The return on total assets adds interest

expense to the net income, which is

divided by average total assets. It

measures the profitability of total assets

b. The return on stockholders’ equity is

normally higher than the return on total

assets. This is because of leverage,

which compensates stockholders for the

higher risk of their investments.

12. a. Due to leverage, the return on stock-

holders’ equity will often be greater than

dends paid to preferred stockholders.

13. The earnings per share in the preceding

year were $3.75 per share ($7.50 ÷ 2),

adjusted for the stock split in the latest year.

14. A share of common stock is currently selling

at 15 times current annual earnings per share.

15. The dividend yield on common stock is a

measure of the rate of return to common

stockholders in terms of cash dividend dis-

tributions. Companies in growth industries

typically reinvest a significant portion of the

is likely a company will increase its inventories

and expand its operations. Such situations

frequently result in an increase in current

liabilities out of proportion to the increase in

current assets and thus lower the current

ratio.

17. One report is the Report on Internal Control,

which verifies management’s conclusions on

257

EXERCISES

E9–1

a.

TRIBAL TECHNOLOGIES CO.

Comparative Income Statement

For the Years Ended December 31, 20Y8 and 20Y7

20Y8 20Y7

Amount Percent Amount Percent

Sales …………………………………….. $ 450,000 100.0% $ 362,500 100.0%

Cost of goods sold ………………… (279,000) (62.0) (217,500) (60.0)

Gross profit …………………………… $ 171,000 38.0% $ 145,000 40.0%

b. The vertical analysis indicates the cost of goods sold as a percent of sales

increased by 2 percentage points (62.0% – 60.0%), selling expenses decreased

by 3 percentage points (16.0% – 13.0%), administrative expenses decreased

258

E9–2

a.

SPEEDWAY MOTORSPORTS, INC.

Comparative Income Statement (in thousands of dollars)

Year 2 Year 1

Amount Percent Amount Percent

Revenues:

Admissions ……………………………….. $ 100,694 20.3% $ 100,798 20.8%

Event-related revenue ………………… 146,980 29.6 146,849 30.3

NASCAR® broadcasting revenue … 217,469 43.8 207,369 42.8

Other operating revenue …………….. 31,320 6.3 29,293 6.1

Total revenue ……………………….. $ 496,463 100.0% $ 484,309 100.0%

Expenses and other:

b. Overall revenue increased in Year 2 primarily due to the increase in NASCAR

broadcasting revenue of 1.0% (43.8% – 42.8%). The total expenses as a percent

of total revenue increased in Year 2 by 17.8% (109.3% – 91.5%), which resulted

in operating income before taxes as a percent of revenue decreasing by

17.8% [8.5% – (9.3%)].

The major increase in expenses in Year 2 was in general and administrative

expenses, which increased 17.3% (57.4% – 40.1%). This increase was related

to the recording of an impairment of goodwill of $98,868 in Year 2, which was

259

E9–3

a.

DAWG ELECTRONICS COMPANY

Common-Sized Income Statement

Dawg Electronics

Electronics Industry

Company Average

Amount Percent

Sales ………………………………………………………. $ 3,750,000 100.0% 100.0%

Cost of goods sold ………………………………….. (2,062,500) (55.0) (61.0)

Gross profit …………………………………………….. $ 1,687,500 45.0% 39.0%

Selling expenses ……………………………………… $(1,125,000) (30.0)% (23.0)%

Administrative expenses ………………………….. (262,500) (7.0) (10.0)

b. The cost of goods sold is 6 percentage points (61.0% – 55.0%) lower than the

industry average, but the selling expenses are 7 percentage points (30.0% –

23.0%) higher than the industry average. Administrative expenses are 3

percentage points (10.0% – 7.0%) lower than the industry average. Operating

income is 2 percentage points higher (8.0% – 6.0%). Other revenue is 2.6 per-

260

E9–4

20Y2 Percent 20Y1 Percent

Current assets $ 752,000 9.4% $ 602,000 8.6%

Propert

y

, plant, and equipment 6,248,000 78.1 5,397,000 77.1

Intan

g

ible assets 1,000,000 12.5 1,001,000 14.3

Total assets $8,000,000 100.0% $7,000,000 100.0%

Current liabilities $ 504,000 6.3% $ 427,000 6.1%

Lon

g

-term liabilities 1,504,000 18.8 1,197,000 17.1

Total liabilities $2,008,000 25.1% $1,624,000 23.2%

261

E9–5

a. CASCADE IMAGES INC.

Comparative Income Statement

For the Years Ended December 31, 20Y5 and 20Y4

Increase (Decrease)

20Y5 20Y4 Amount Percent

Sales ……………………………………. $ 500,000 $ 400,000 $100,000 25.0%

Cost of goods sold ……………….. (320,000) (250,000) (70,000) 28.0%

Gross profit ………………………….. $ 180,000 $ 150,000 $ 30,000 20.0%

Selling expenses …………………… $ (35,000) $ (30,000) $ (5,000) 16.7%

262

E9–6

a. (1) Working Capital = Current Assets – Current Liabilities

20Y9: $525,000 = $900,000 – $375,000

20Y8: $400,000 = $650,000 – $250,000

b. The liquidity of Icon Living, Inc., appears to have improved between 20Y8 and

20Y9 since the company’s working capital increased. However, given that the

current ratio and quick ratio decreased, it should be concluded that the

company’s liquidity declined from 20Y8 to 20Y9. These changes are the result

of an increase in current liabilities and change in the mix of current assets.

E9–7

a. (1) Current Ratio = sLiabilitieCurrent

setsCurrent As

b. The liquidity of PepsiCo has increased some over this time period. Both the

current and quick ratios have increased. The current ratio increased from 1.3

to 1.5, and the quick ratio increased from 1.1 to 1.3. PepsiCo is a strong

company with ample resources for meeting its short-term obligations.

263

E9–8

a. The working capital, current ratio, and quick ratio are calculated incorrectly.

The working capital and current ratio incorrectly include intangible assets

and property, plant, and equipment as a part of current assets. Both are

The correct calculations are as follows:

Working Capital = Current Assets – Current Liabilities

$150,000 = $750,000 – $600,000

Current Ratio = sLiabilitieCurrent

setsCurrent As = $600,000

$750,000 = 1.25

264

E9–9

a. (1) Accounts Receivable Turnover = Sales

Average Accounts Receivable

Year 3: 1

$2,640,000

$412,500 = 6.4 Year 2: 3

$1,957,500

$337,500 = 5.8

(2) Days’ Sales in Receivables = Accounton Sales Daily Average

Receivable AccountsAverage

Year 3:

1

2

$412,500

$7,233 = 57.0 days

Note: The days’ sales in receivables can also be computed by dividing

365 days by the accounts receivable turnover as shown below.

Year 3: 365 days

6.4 = 57.0 days

b. The collection of accounts receivable has improved from Year 2 to Year 3.

This can be seen in the increase in accounts receivable turnover and the re-

265

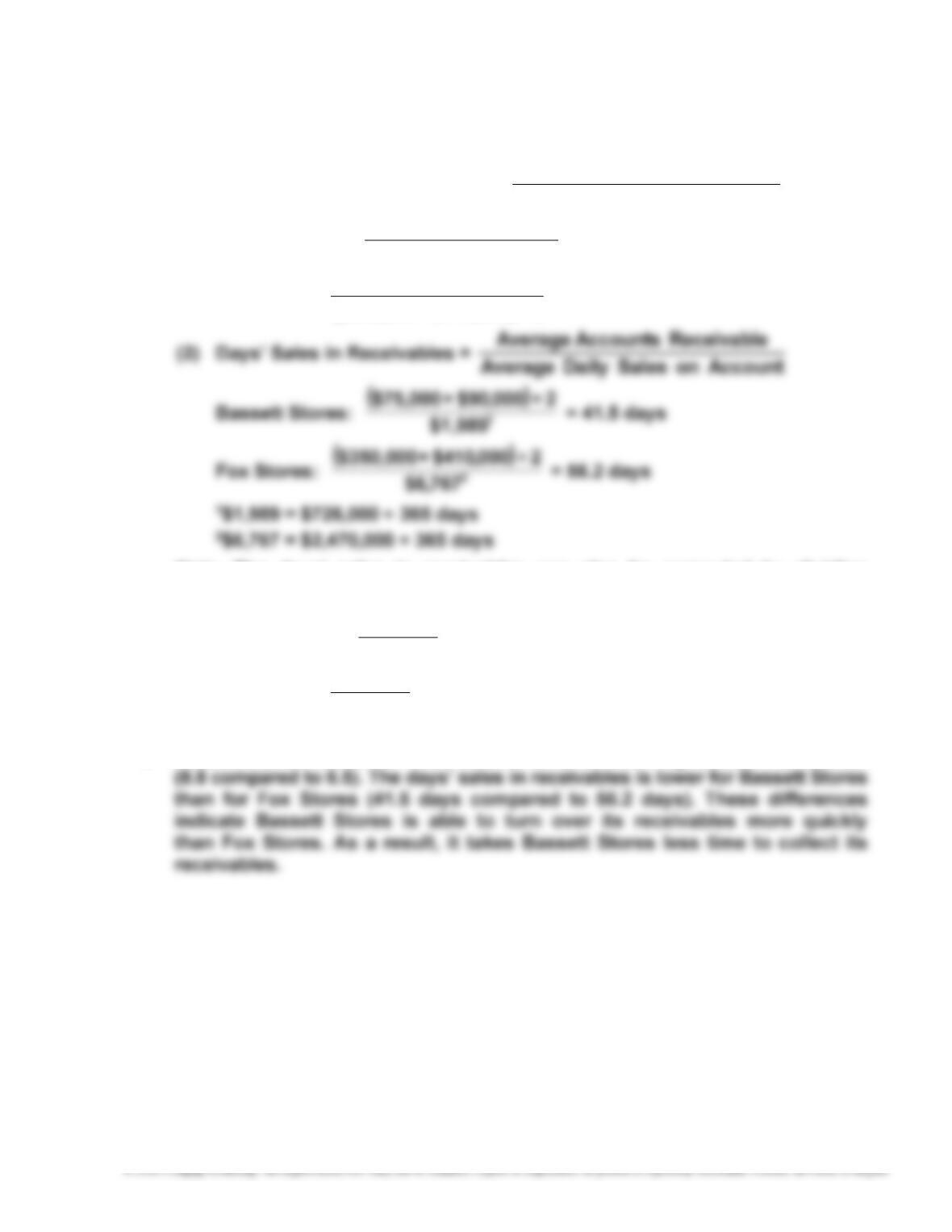

E9–10

a. (1) Accounts Receivable Turnover = Sales

Avera

g

e Accounts Receivable

Bassett Stores: 2÷)000,90$+000,75($

000,726$ = 8.8

Fox Stores: 2÷)000,410$+000,350($

000,470,2$ = 6.5

Note: The days’ sales in receivables can also be computed by dividing

365 days by the accounts receivable turnover as shown below.

Basset Stores: 8.8

days 365 = 41.5 days

Fox Stores: 6.5

days 365 = 56.2 days

b. Bassett Stores’ accounts receivable turnover is much higher than Fox Stores’

266

E9–11

a. (1) Inventory Turnover = Inventory Average

Sold Goods ofCost

(2) Days’ Sales in Inventory = Sold Goods ofCost Daily Average

Inventory Average

Current Year: 1

$15,945

2÷)000,550$+000,420($ = 30.4 days

Preceding Year: 2

$11,795

2÷)000,420$+000,400($ = 34.8 days

1$15,945 = $5,820,000 ÷ 365 days

2$11,795 = $4,305,000 ÷ 365 days

b. The inventory position of the business has improved. The inventory turnover

has increased even as the days’ sales in inventory has decreased. The sales

volume has increased faster than the inventory has increased, thus resulting

in an improved inventory position.

267

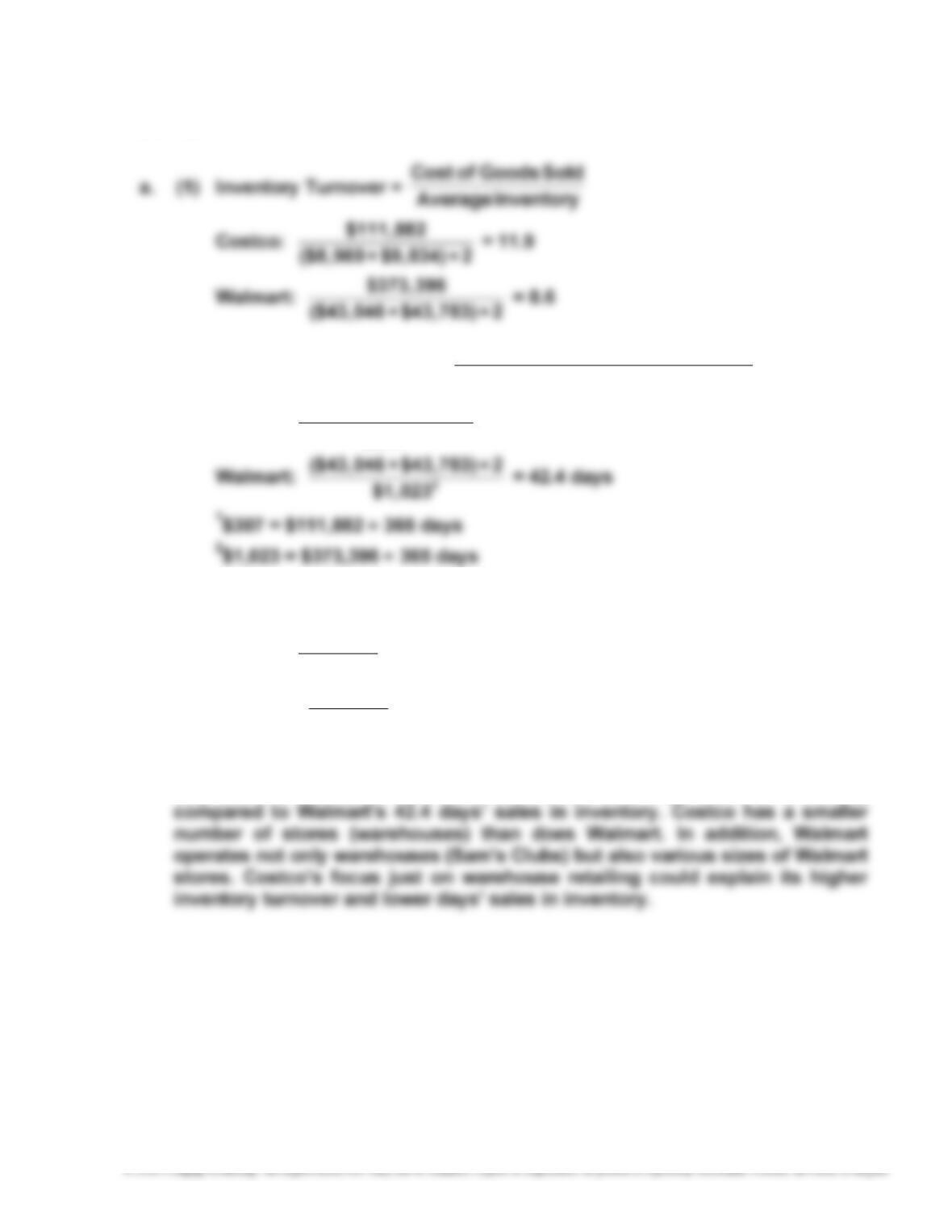

E9–12

(2) Days’ Sales in Inventory = Sold Goods ofCost Daily Average

Inventory Average

Costco: 1

($8,969 + $9,834) ÷ 2

$307 = 30.6 days

Note: The days’ sales in inventory can also be computed by dividing 365 days

by the inventory turnover as shown below.

Costco:

365 days

11.9 = 30.7 days (difference due to rounding)

Walmart:

365 days

8.6 = 42.4 days

b. Costco has a higher inventory turnover of 11.9 compared to Walmart’s inven-

tory turnover of 8.6. As a result, Costco has 30.6 days’ sales in inventory

268

E9–13

a. Ratio of Liabilities to Stockholders’ Equity =

Total Liabilities

Total Stockholders’ Equity

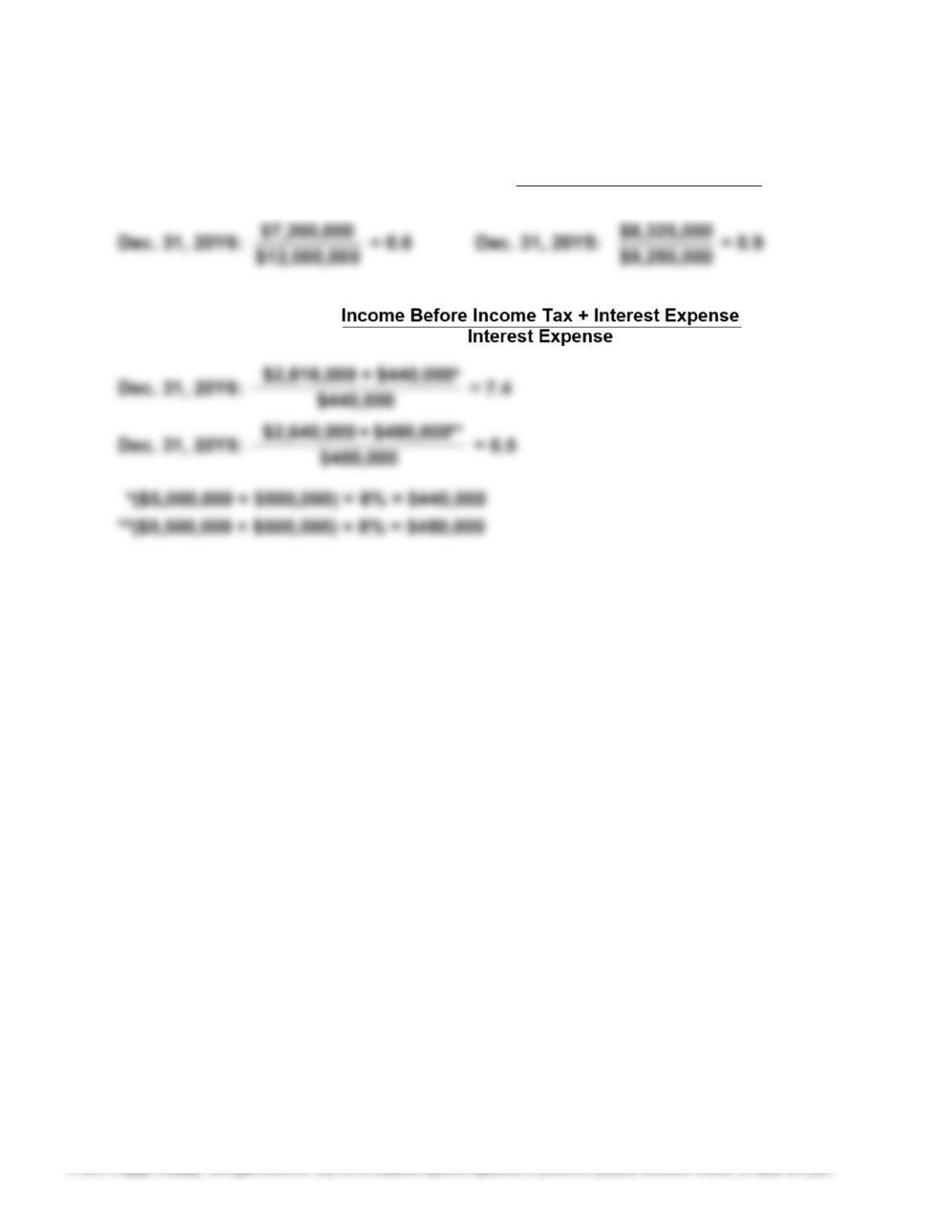

b.

Times Interest Earned

=

c. Both the ratio of liabilities to stockholders’ equity and that of the times interest

earned have improved from 20Y5 to 20Y6. These results are the combined re-

sult of a larger income before taxes and lower bonds payable in the year 20Y6

compared to 20Y5 and indicate an improvement in the company’s ability to

meet its currently maturing debt.

269

E9–14

a. Debt Ratio = Total Liabilities

Total Assets *

Hasbro:

$3,460

$5,290 = 65.4%

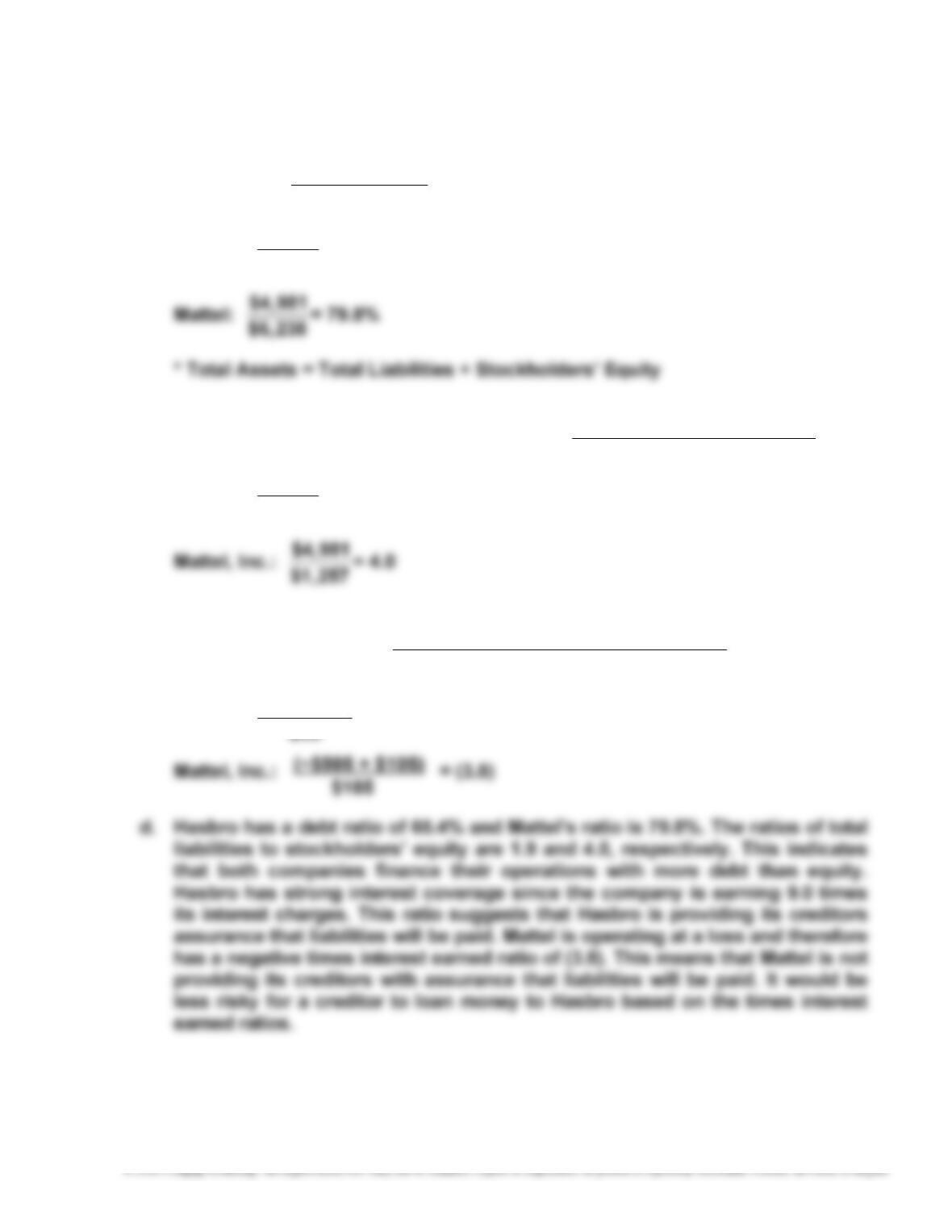

b. Ratio of Liabilities to Stockholders’ Equity = Equity rs’Stockholde Total

sLiabilitie Total

Hasbro:

$3,460

$1,830 = 1.9

c. Times Interest Earned = ExpenseInterest

ExpenseInterest + Tax Before Income

Hasbro:

$786 + $98

270

E9–15

a. Debt Ratio = Total Liabilities

Total Assets *

Hershey:

$4,622

$5,554 = 83.2%

b. Ratio of Liabilities to Stockholders’ Equity = Equity rs’Stockholde Total

sLiabilitie Total

Hershey:

$4,622

$932 = 5.0

Mondelez:

$36,918

$26,191 = 1.4

c. Ratio of Fixed Assets to Long-Term Liabilities = Fixed Assets (net)

Long-Term Liabilities

d. Hershey uses more debt than Mondelez given a debt ratio of 83.2% for Hershey

and a debt ratio of 58.5% for Mondelez. The ratio of total liabilities to stock-

holders’ equity ratio is 5.0 for Hershey and 1.4 for Mondelez. The ratio of fixed

271

E9–16

a. Asset Turnover = Sales

Average Long–Term Operating Assets

YRC Worldwide:

$4,891

$842 = 5.81

b. The asset turnover measures the number of sales dollars earned for each dol-

lar of long-term operating assets. The greater the number of sales dollars

earned for every dollar of assets, the more efficient a firm is in using assets.

Thus, the ratio is a measure of the efficiency in using assets. The three

companies are different in their efficiency in using assets because they are

different in the nature of their operations. Union Pacific earns only 42 cents

for every dollar of assets. This is because Union Pacific is asset intensive.

That is, Union Pacific must invest in locomotives, railcars, terminals, tracks,

right-of-way, and information systems to earn revenues. These investments

272

E9–16, Concluded

Note to Instructors: Students may wonder how asset-intensive companies

overcome their asset efficiency disadvantages relative to competitors with

better asset efficiencies. Asset efficiency is part of the financial equation; the

other part is the profit margin made on each dollar of sales. Thus, companies

E9–17

a. Return on Total Assets = AssetsTotal Average

ExpenseInterest + IncomeNet

*($2,100,000 + $1,600,000) ÷ 2 **($1,600,000 + $1,200,000) ÷ 2

Return on Common

Stockholders’ Equity = Equity rs’Stockholde Common Average

Dividends Preferred––IncomeNet

20Y5: *$1,450,000

$32,000–– $530,000 = 34.3% 20Y4: **$1,000,000

$32,000–– $430,000 = 39.8%

*($1,700,000 + $1,200,000) ÷ 2 **($1,200,000 + $800,000) ÷ 2

b. The profitability ratios indicate The O’Malley Group’s profitability has

273

E9–18

a. Return on Total Assets = AssetsTotal Average

ExpenseInterest + IncomeNet

b. Return on Stockholders’ Equity = Equity rs’Stockholde Total Average

IncomeNet

Year 3: $1,536

($5,661 + $4,322) ÷ 2 = 30.8%

Year 2: $611

($4,322 + $4,253) ÷ 2 = 14.3%

274

E9–19

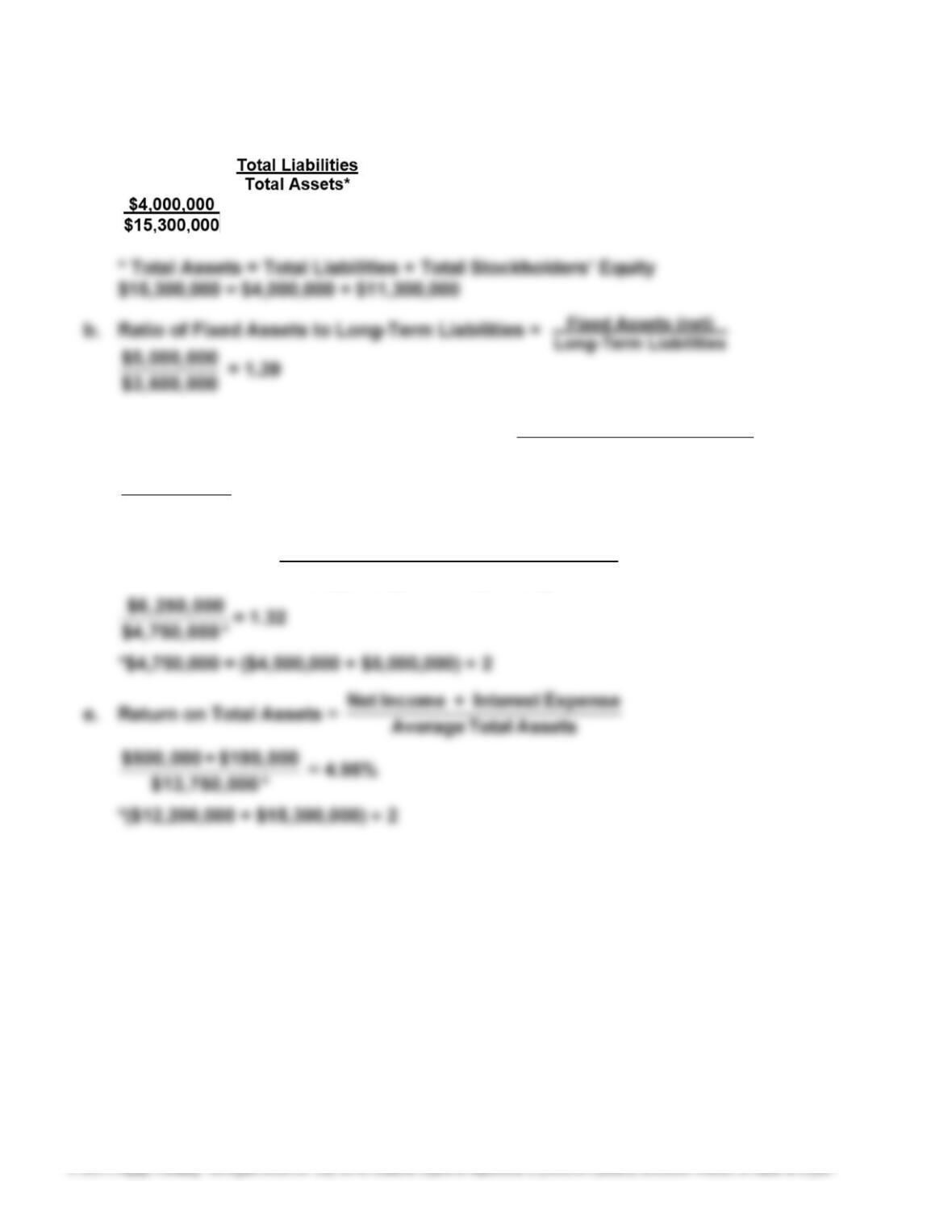

a. Debt ratio =

= 26.14%

c. Ratio of Liabilities to Stockholders’ Equity =

Equity rs’Stockholde Total

sLiabilitie Total

$4,000,000

$11,300,000

= 0.35

d. Asset Turnover =

Sales

Average Long– Term Operating Assets