CHAPTER 9

Budgetary Planning

ASSIGNMENT CLASSIFICATION TABLE

Learning Objectives

Questions

Brief

Exercises

Do It!

Exercises

A

Problems

1. State the essentials of effective

budgeting and the components of

the master budget.

1, 2, 3, 4, 5,

6, 7, 8, 9,

10

1

1

1

2. Prepare budgets for sales,

production, and direct materials.

11, 12, 13

2, 3, 4,

2

2, 3, 4, 5, 6,

7, 8, 10

1A, 2A, 3A

3. Prepare budgets for direct labor,

manufacturing overhead, and

selling and administrative

expenses, and a budgeted

income statement.

14, 15, 16,

17, 18

5, 6, 7, 8

3

9, 10, 11,

12, 13

1A, 2A, 6A

4. Prepare a cash budget and a

budgeted balance sheet.

19, 20

9

4

14, 15, 16,

17, 18, 19

4A, 6A

5. Apply budgeting principles to

nonmanufacturing companies.

21, 22

10

5

19, 20, 21

5A

ASSIGNMENT CHARACTERISTICS TABLE

Problem

Number

Description

Difficulty

Level

Time

Allotted (min.)

1A

Prepare budgeted income statement and supporting

budgets.

Simple

30–40

2A

Prepare sales, production, direct materials, direct labor,

and income statement budgets.

Simple

40–50

3A

Prepare sales and production budgets and compute cost

per unit under two plans.

30–40

Prepare cash budget for two months.

merchandiser.

retained earnings and balance sheet.

BLOOM’ S TAXONOMY TABLE

Correlation Chart between Bloom’s Taxonomy, Learning Objectives and End–of-Chapter Exercises and Problems

Learning Objective

Knowledge

Comprehension

Application

Analysis

Synthesis

Evaluation

1. State the essentials of

effective budgeting and

the components of the

master budget.

DI9-1

Q9-1

Q9-2

Q9-3

Q9-4

Q9-5

Q9-6

Q9-7

Q9-8

Q9-9

Q9–10

E9-1

BE9-1

2. Prepare budgets for sales,

production, and direct

materials.

Q9–11

Q9–12

Q9–13

BE9-2

BE9-3

BE9-4

DI9-2

E9-2

E9-3

E9-4

E9-5

E9-6

E9-7

E9-8

E9–10

P9–1A

P9–2A

P9–3A

3. Prepare budgets for direct

labor, manufacturing

overhead, and selling and

administrative expenses,

and a budgeted income

statement.

Q9–14

Q9–15

Q9–16

Q9–18

Q9–17

BE9-5

BE9-6

BE9-7

BE9-8

DI9-3

E9-9

E9–10

E9–11

E9–12

E9–13

P9–1A

P9-2A

P9–6A

4. Prepare a cash budget and

a budgeted balance sheet.

Q9–19

Q9–20

BE9-9

DI9-4

E9–14

E9–15

E9–17

E9–18

E9–19

P9–4A

P9–6A

E9–16

5. Apply budgeting

principles to

nonmanufacturing

companies.

Q9–21

Q9–22

BE9-10

DI9-5

E9–19

E9–20

E9–21

P9–5A

Broadening Your Perspective

BYP9-2

BYP9-3

BYP9-4

BYP9-1

BYP9-5

BYP9-6

BYP9-7

ANSWERS TO QUESTIONS

1. (a) A budget is a formal written statement of management’s plans for a specified future time period,

expressed in financial terms.

2. The primary benefits of budgeting are:

(1) It requires all levels of management to plan ahead and to formalize goals on a recurring basis.

(2) It provides definite objectives for evaluating performance at each level of responsibility.

3. The essentials of effective budgeting are: (1) a sound organizational structure, (2) research and

analysis, and (3) acceptance by all levels of management.

4. (a) Disagree. Accounting information makes major contributions to the budgeting process. Accounting

provides the starting point of budgeting by providing historical data on revenues, costs, and

5. The budget period should be long enough to provide an attainable goal under normal business

conditions. The budget period should minimize the impact of seasonal and cyclical business

fluctuations, but it should not be so long that reliable estimates are impossible. The most common

budget period is one year.

6. Disagree. Long-range planning usually encompasses a period of at least five years. It involves

the selection of strategies to achieve long-term goals and the development of policies and plans to

be able to provide better budgetary estimates. In addition, by involving lower-level managers in

the process, it is more likely that they will perceive the budget as being fair and reasonable. One

disadvantage of participative budgeting is that it takes more time, and thus costs more. Another

disadvantage of participative budgeting is that it may enable managers to game the system

through such practices as budgetary slack.

Questions Chapter 9 (Continued)

8. Budgetary slack is the amount by which a manager intentionally underestimates budgeted

revenues or overestimates budgeted expenses in order to make it easier to achieve budgetary

goals. Managers may have an incentive to create budgetary slack in order to increase the likelihood of

receiving a bonus, or decrease the likelihood of losing their job.

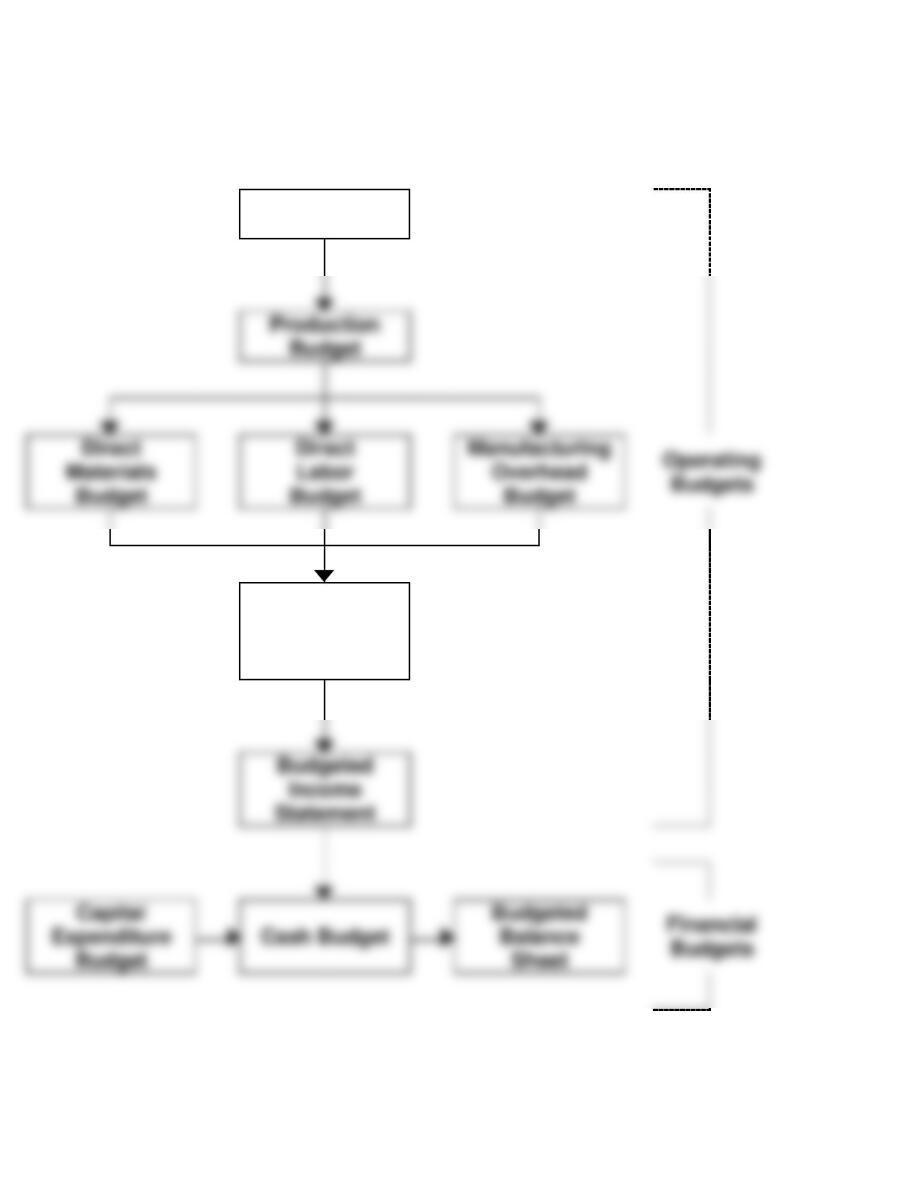

9. A master budget is a set of interrelated budgets that constitutes a plan of action for a specified

time period. The master budget is developed within the framework of a sales forecast.

10. The sales budget is the starting point in preparing the master budget. An inaccurate sales budget

may adversely affect net income. An overly optimistic sales budget may result in excessive

inventories and a very conservative sales budget may lead to inventory shortages.

16. The first quarter budgeted selling and administrative expenses are $74,000 [(12% X $200,000) +

$50,000]. The second quarter total is $78,800 [(12% X $240,000) + $50,000].

17. The budgeted cost per unit of product is $46 ($10 + $20 + $16). Gross profit per unit is $19 ($65 – $46).

Total budgeted gross profit is $475,000 (25,000 X $19).

18. The supporting schedules are the budgets for sales, direct materials, direct labor, and manufacturing

overhead.

SOLUTIONS TO BRIEF EXERCISES

BRIEF EXERCISE 9-1

Sales

Budget

Selling and

Administrative

Expense

Budget

BRIEF EXERCISE 9-2

PAIGE COMPANY

Sales Budget

For the Year Ending December 31, 2017

Quarter

1

2

3

4

Year

Expected

unit

10,000

14,000

15,000

18,000

57,000

BRIEF EXERCISE 9-3

PAIGE COMPANY

Production Budget

For the Six Months Ending June 30, 2017

Quarter

Six

Months

1

2

Expected unit sales

Add: Desired ending finished goods

10,000

3,500

a

14,000

3,750

c

BRIEF EXERCISE 9-4

PERINE COMPANY

Direct Materials Budget

For the Month Ending January 31, 2017

Units to be produced ………………………………………………. 4,000

Direct materials per unit …………………………………………. X 2

Total pounds required for production………………………. 8,000

Add: Desired ending inventory (25% X 5,000 X 2) …… 2,500

BRIEF EXERCISE 9-5

GUNDY COMPANY

Direct Labor Budget

For the Six Months Ending June 30, 2017

Quarter

Six

Months

1

2

Units to be produced

5,000

7,000

BRIEF EXERCISE 9-6

ROCHE INC.

Manufacturing Overhead Budget

For the Year Ending December 31, 2017

Quarter

1

2

3

4

Year

Variable costs

$20,000

$25,000

$30,000

$35,000

$110,000

BRIEF EXERCISE 9-7

ELBERT COMPANY

Selling and Administrative Expense Budget

For the Year Ending December 31, 2017

Quarter

1

2

3

4

Year

Variable expenses

expenses

$24,000

$28,000

$32,000

$36,000

$120,000

BRIEF EXERCISE 9-8

NORTH COMPANY

Budgeted Income Statement

For the Year Ending December 31, 2017

Sales ………………………………………………………………………. $2,250,000

Cost of goods sold (50,000 X $25) ……………………………. 1,250,000

Gross profit …………………………………………………………….. 1,000,000

Total manufacturing overhead

BRIEF EXERCISE 9-9

Collections from Customers

Credit Sales

January

February

March

January, $220,000

February, $260,000

$165,000

$ 55,000

195,000

$ 65,000

BRIEF EXERCISE 9-10

Budgeted cost of goods sold ($400,000 X 65%) …………………… $260,000

Add: Desired ending inventory ($480,000 X 65% X 20%) ……. 62,400

SOLUTIONS FOR DO IT! REVIEW EXERCISES

DO IT! 9-1

1. Operating budgets

2. Master budget

3. Participative budgeting

DO IT! 9-2

PARGO COMPANY

Sales Budget

For the Year Ending December 31, 2017

Quarter

1

2

3

4

Year

Total sales

Expected unit

200,000

250,000

250,000

300,000

1,000,000

DO IT! 9-2 (Continued)

PARGO COMPANY

Production Budget

For the Year Ending December 31, 2017

Quarter

1

2

3

4

Year

Required production units

Expected unit sales

Add: Desired ending finished

200,000

250,000

250,000

300,000

PARGO COMPANY

Direct Materials Budget

For the Year Ending December 31, 2017

Quarter

1

2

3

4

Year

Units to be produced

Direct materials per unit

Total pounds needed for

production

Add: Desired ending

212,500

X 2

425,000

250,000

X 2

500,000

262,500

X 2

525,000

285,000

X 2

570,000

materials purchases

DO IT! 9-3

(a) Total unit cost:

Cost Element

Quantity

Unit Cost

Total

Direct materials …………………………

2 pounds

$12.00

$24.00

(b) PARGO COMPANY

Budgeted Income Statement

For the Year Ending December 31, 2017

Sales (1,000,000) units from sales budget, page 9-10 ……. $41,500,000

Cost of goods sold (1,000,000 X $34.50/unit) ……………… 34,500,000

DO IT! 9-4

BATISTA COMPANY

Cash Budget

April

Beginning cash balance…………………………………………………….. $ 25,000

Add: Cash receipts for April ……………………………………………… 245,000

Total available cash …………………………………………………………… 270,000

DO IT! 9-5

Zeller COMPANY

Merchandise Purchases Budget

For the Six Months Ending June 30, 2017

Quarter

Six

1

2

Months

Budgeted cost of goods sold

(Sales .50)

$20,000

$24,000

Add: Desired ending merchandise

inventory (10% of next

Total

Required merchandise purchases

SOLUTIONS TO EXERCISES

EXERCISE 9-1

MEMO

To Jim Dixon

From: Student

Re: Budgeting

I am glad Trusler Company is considering preparing a formal budget. There are

many benefits derived from budgeting, as I will discuss later in this memo.

A budget is a formal written statement of management’s plans for a specified

future time period, expressed in financial terms. The master budget gener–

ally consists of operating budgets such as the sales budget, production

The primary benefits of budgeting are:

1. It requires all levels of management to plan ahead and to formalize

goals on a recurring basis.

2. It provides definite objectives for evaluating performance at each

level of responsibility.

In order to maximize these benefits, it is essential that budgeting take place

within a sound organizational structure, so authority and responsibility for all

phases of operations are clearly defined. Also, the budget should be based on

EXERCISE 9-2

EDINGTON ELECTRONICS INC.

Sales Budget

For the Six Months Ending June 30, 2017

Quarter 1

Quarter 2

Six Months

Product

Units

Selling

Price

Total

Sales

Units

Selling

Price

Total

Sales

Units

Selling

Price

Total

Sales

Totals

300,000

15,000

375,000

27,000

THOME AND CREDE, CPAs

Sales Revenue Budget

For the Year Ending December 31, 2017

Quarter 1

Quarter 2

Quarter 3

Quarter 4

Billable

Billable

Total

Billable

Billable

Total

Billable

Billable

Total

Billable

Billable

Total

Dept.

Hours

Rate

Rev.

Hours

Rate

Rev.

Hours

Rate

Rev.

Hours

Rate

Rev.

Auditing

2,300

$ 80

$184,000

1,600

$ 80

128,000

2,000

$ 80

$160,000

2,400

$ 80

$192,000

Year

Billable

Billable

Total

Dept.

Hours

Rate

Rev.

Auditing

$ 80

$2,197,000

EXERCISE 9-3

Tax

3,000

270,000

2,200

198,000

2,000

180,000

2,500

225,000

1,500

1,500

1,500

1,500

$619,000

$491,000

$505,000

$582,000

EXERCISE 9-4

TURNEY COMPANY

Production Budget

For the Year Ending December 31, 2017

Product HD-240

Quarter

1

2

3

4

Year

Expected unit sales

Add: Desired ending

5,000

7,000

8,000

10,000

EXERCISE 9-5

DEWITT INDUSTRIES

Direct Materials Purchases Budget

For the Quarter Ending March 31, 2017

January

February

March

Units to be produced

Direct materials per unit

Total pounds needed for production

Add: Desired ending direct materials

10,000

X 2

20,000

8,000

X 2

16,000

5,000

X 2

10,000

EXERCISE 9-6

(a) HARDIN COMPANY

Production Budget

For the Six Months Ending June 30, 2017

Quarter

Six

Months

1

2

Expected unit sales

Add: Desired ending finished goods

units

5,000

1,500

(1)

6,000

1,750

(2)

EXERCISE 9-6 (Continued)

(b) HARDIN COMPANY

Direct Materials Budget

For the Six Months Ending June 30, 2017

Quarter

Six

Months

1

2

Units to be produced

Direct materials per unit

Total pounds needed for production

Add: Desired ending direct

5,250

X 3

15,750

6,250

X 3

18,750

EXERCISE 9-7

Finished goods:

Sales ……………………………………………………………… 2,675

Plus: Ending inventory ……………………………………. 2,200

Total required …………………………………………………….. 4,875

Less: beginning inventory ……………………………… 2,230

Production required ……………………………………………. 2,645

$67,800

EXERCISE 9-8

(a) FUQUA COMPANY

Production Budget

For the Two Months Ending February 28, 2017

_____________________________________________________________

January

February

Expected unit sales ……………………………………..

10,000

12,000

Add: desired ending finished goods

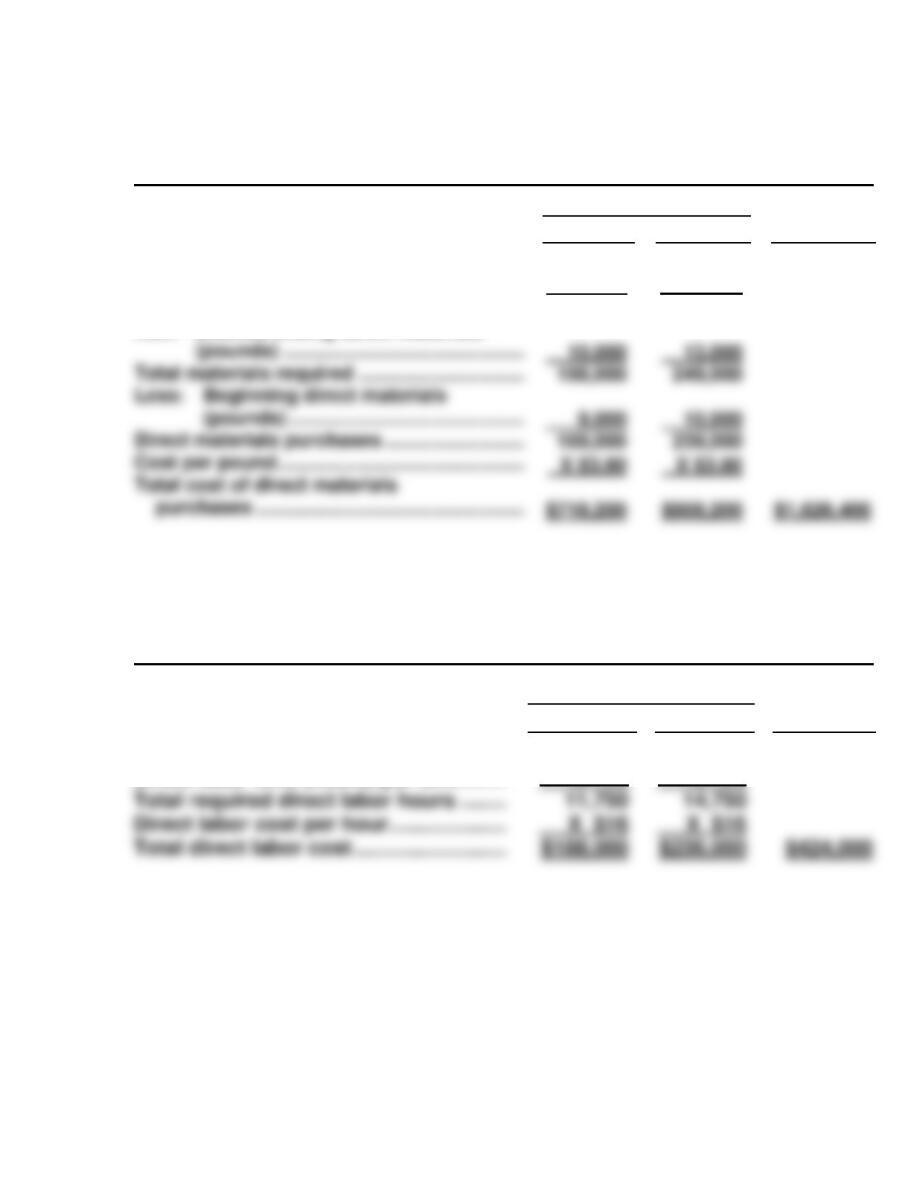

(b) FUQUA COMPANY

Direct Materials Budget

For the Month Ending January 31, 2017

_____________________________________________________________

January

Units to be produced ……………………………………………………

10,400

Direct material pounds per unit …………………………………….

X 4

Total pounds needed for production ……………………………..

41,600

Add: desired pounds in ending materials inventory ………

19,520*

Total materials required ……………………………………………….

61,120

Less: beginning direct materials (pounds) …………………….

Direct materials purchases …………………………………………..

44,480

Cost per pound ……………………………………………………………

X $2

Total cost of direct materials purchases ………………………..

$88,960

Total required units ……………………………………..

12,400

14,600

10,400

12,200

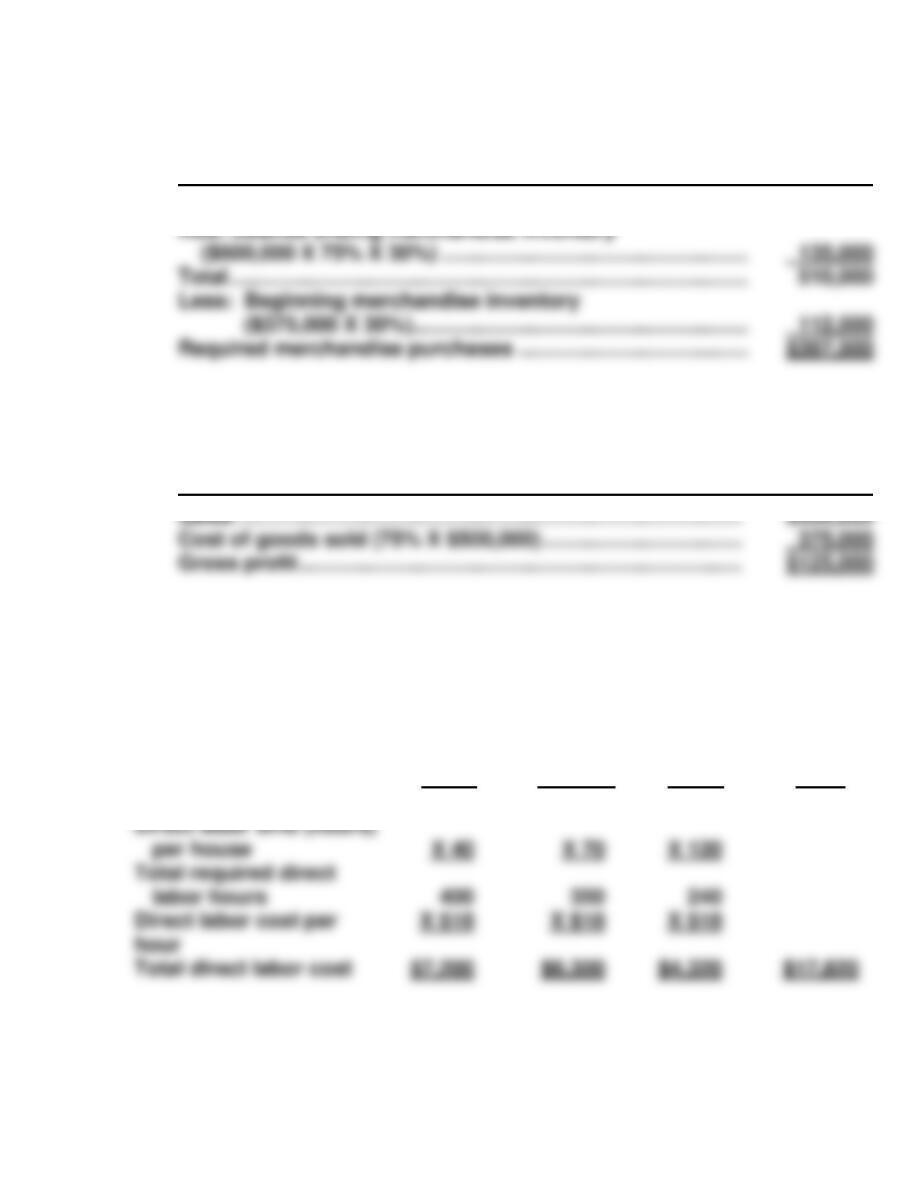

EXERCISE 9-9

RODRIQUEZ, INC.

Direct Labor Budget

For the Year Ending December 31, 2017

Quarter

1

2

3

4

Year

Units to be produced

Direct labor time

20,000

25,000

35,000

30,000

110,000

EXERCISE 9-10

LOWELL COMPANY

Production Budget

For the Quarter Ending March 31, 2017

Jan Feb Mar Total

Sales in units 12,000 14,000 13,000 39,000

Plus: desired ending inventory 19,200(1) 17,400(2) 15,400(3) 15,400

EXERCISE 9-10 (Continued)

LOWELL COMPANY

Direct Labor Budget

For the Quarter Ending March 31, 2017

Jan Feb Mar Total

Production in units 13,600 12,200 11,000

EXERCISE 9-11

ATLANTA COMPANY

Manufacturing Overhead Budget

For the Year Ending December 31, 2017

Quarter

1

2

3

4

Year

($443,000 ÷ 78,000)

Variable costs

Indirect materials ($.80/hour)

Indirect labor ($1.20/hour)

Maintenance ($.50/hour)

Total variable

Fixed costs

Supervisory salaries

$12,000

18,000

7,500

37,500

35,000

$ 14,400

21,600

9,000

45,000

35,000

$ 16,800

25,200

10,500

52,500

35,000

$ 19,200

28,800

12,000

60,000

35,000

$ 62,400

93,600

39,000

195,000

140,000

EXERCISE 9-12

KIRKLAND COMPANY

Selling and Administrative Expense Budget

For the Six Months Ending June 30, 2017

Quarter

Six

Months

1

2

Budgeted sales in units

Variable expenses (1)

Sales commissions

20,000

$20,000*

22,000

$22,000

$ 42,000

Fixed expenses

Sales salaries

Office salaries

Depreciation

Insurance

Utilities

12,000

8,000

4,200

1,500

800

12,000

8,000

4,200

1,500

800

24,000

16,000

8,400

3,000

1,600

(1) Variable costs per dollar of sales are: Sales commissions (5%), Delivery

expense (2%), and Advertising (3%).

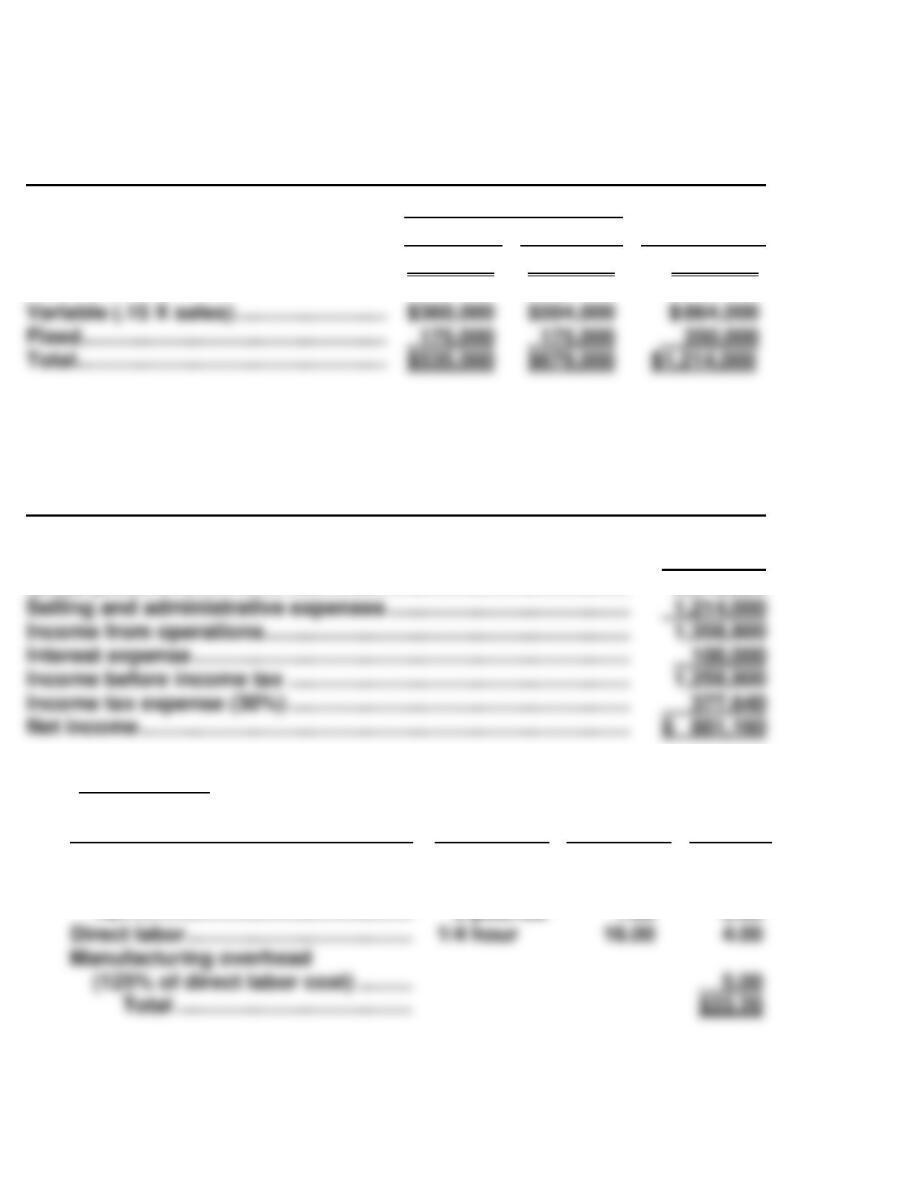

EXERCISE 9-13

(a) FULTZ COMPANY

Computation of Cost of Goods Sold

For the Year Ending December 31, 2017

Cost of one unit of finished goods:

Direct materials (1 X $5) …………………………..…………………………. $ 5

Direct labor (3 X $15) ………………………………………………………….. 45

(b) FULTZ COMPANY

Budgeted Income Statement

For the Year Ending December 31, 2017

Sales (30,000 X $85) …………………………………………………… $2,550,000

Cost of goods sold (see part (a)) ………………………………… 1,950,000

Gross profit ………………………………………………………………. 600,000

EXERCISE 9-14

DANNER COMPANY

Cash Budget

For the Two Months Ending February 28, 2017

January

February

Beginning cash balance ……………………………………

Add: Receipts

Collections from customers …………………..

Sale of marketable securities …………………

Total receipts ………………………………………..

$ 45,000

85,000

12,000

97,000

$ 27,500

150,000

0

150,000

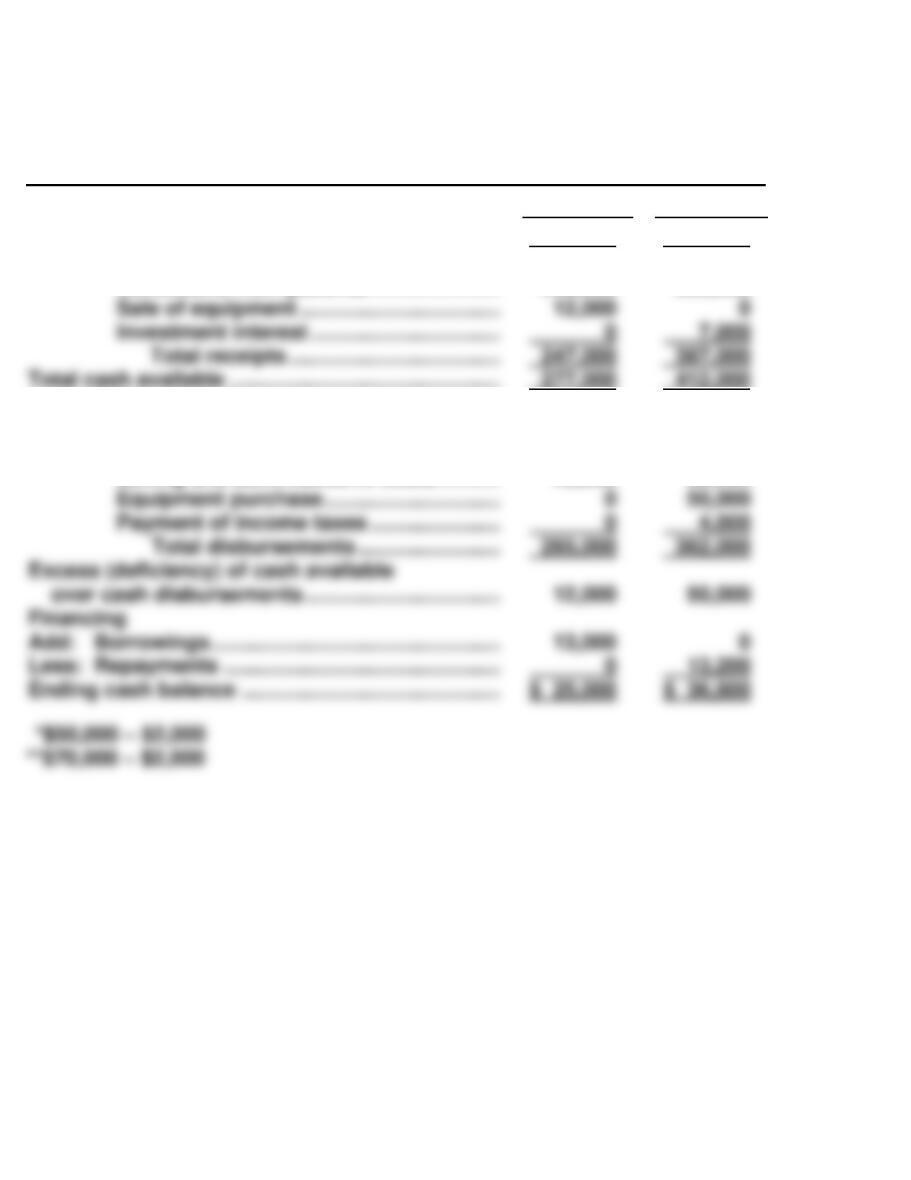

EXERCISE 9-15

DEITZ CORPORATION

Cash Budget

For the Quarter Ended March 31, 2017

Beginning cash balance …………………………………………………..

Add: Receipts

Collections from customers …………………………………..

Sale of equipment …………………………………………………

Total receipts ………………………………………………….

Total available cash …………………………………………………………

$ 30,000

185,000

3,000

188,000

218,000

EXERCISE 9-16

(a) TRENSHAW COMPANY

Cash Budget

For the Month Ended July 31, 2017

Beginning cash balance ………………………. $45,000

Add: Cash collections ………………………… 90,000

Total cash available …………………………….. $135,000

Less: Cash disbursements

Merchandise purchases ……… $56,200

Operating expenses ……………. 40,800

(b) An advantage of cash budgeting is that it allows cash shortfalls to be

predicted. If the timing of future cash shortfalls is known, arrange–

EXERCISE 9-17

(a) NEITO COMPANY

Expected Collections from Customers

March

March cash sales (30% X $250,000) ……………………………….

$ 75,000

Collection of March credit sales

[(70% X $250,000) X 10%] …………………………………………..

17,500

(b) NEITO COMPANY

Expected Payments for Direct Materials

March

March cash purchases (50% X $38,000) …………………………

$19,000

[(50% X $38,000) X 40%] …………………………………………….

[(50% X $36,000) X 60%] …………………………………………….

Total payments ………………………………………………….

Payment of March credit purchases

[(70% X $220,000) X 50%] …………………………………………..

[(70% X $200,000) X 36%] …………………………………………..

50,400

Total collections ………………………………………………..

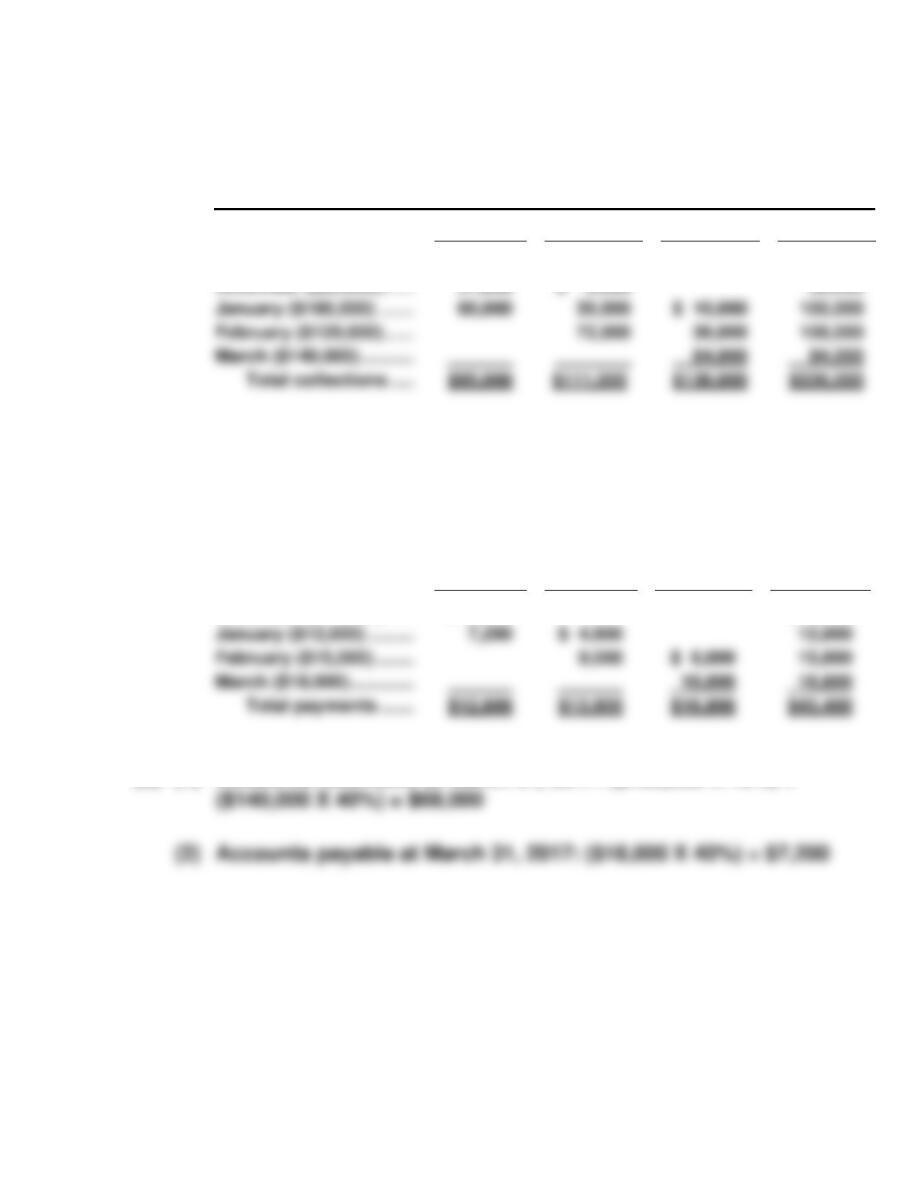

EXERCISE 9-18

(a) (1)

GREEN LANDSCAPING INC.

Schedule of Expected Collections From Clients

For the Quarter Ending March 31, 2017

January

February

March

Quarter

November ($80,000) ……………………………………….

December ($90,000) ……………………………………….

$ 8,000

27,000

$ 9,000

$ 8,000

36,000

(2)

GREEN LANDSCAPING INC.

Schedule of Expected Payments for Landscaping Supplies

For the Quarter Ending March 31, 2017

________________________________________________________

January

February

March

Quarter

December ($14,000) ……………………………………….

$ 5,600

$ 5,600

(b)

(1)

Accounts receivable at March 31, 2017: ($120,000 X 10%) +

EXERCISE 9-19

PLETCHER DENTAL CLINIC

Cash Budget

For the Two Quarters Ending June 30, 2017

1st Quarter

2nd Quarter

Beginning cash balance …………………………………..

Add: Receipts

Collections from patients ……………………

Less: Disbursements

Professional salaries ………………………….

Overhead costs ………………………………….

Selling and administrative costs ………….

$ 30,000

235,000

140,000

77,000

48,000*

$ 25,000

380,000

140,000

100,000

68,000**

EXERCISE 9-20

(a) GRAND STORES

Merchandise Purchases Budget

For the Month Ending June 30, 2017

Budgeted cost of goods sold ($500,000 X 75%) ……………… $375,000

(b) GRAND STORES

Budgeted Income Statement

For the Month Ending June 30, 2017

EXERCISE 9-21

Emeric and Ellie’s Painting Service

Direct Labor Budget

For the Month Ending June 30, 2017

Small

Medium

Large

Total

Home to be painted

10

5

2

per house

hour

Total direct labor cost

SOLUTIONS TO PROBLEMS

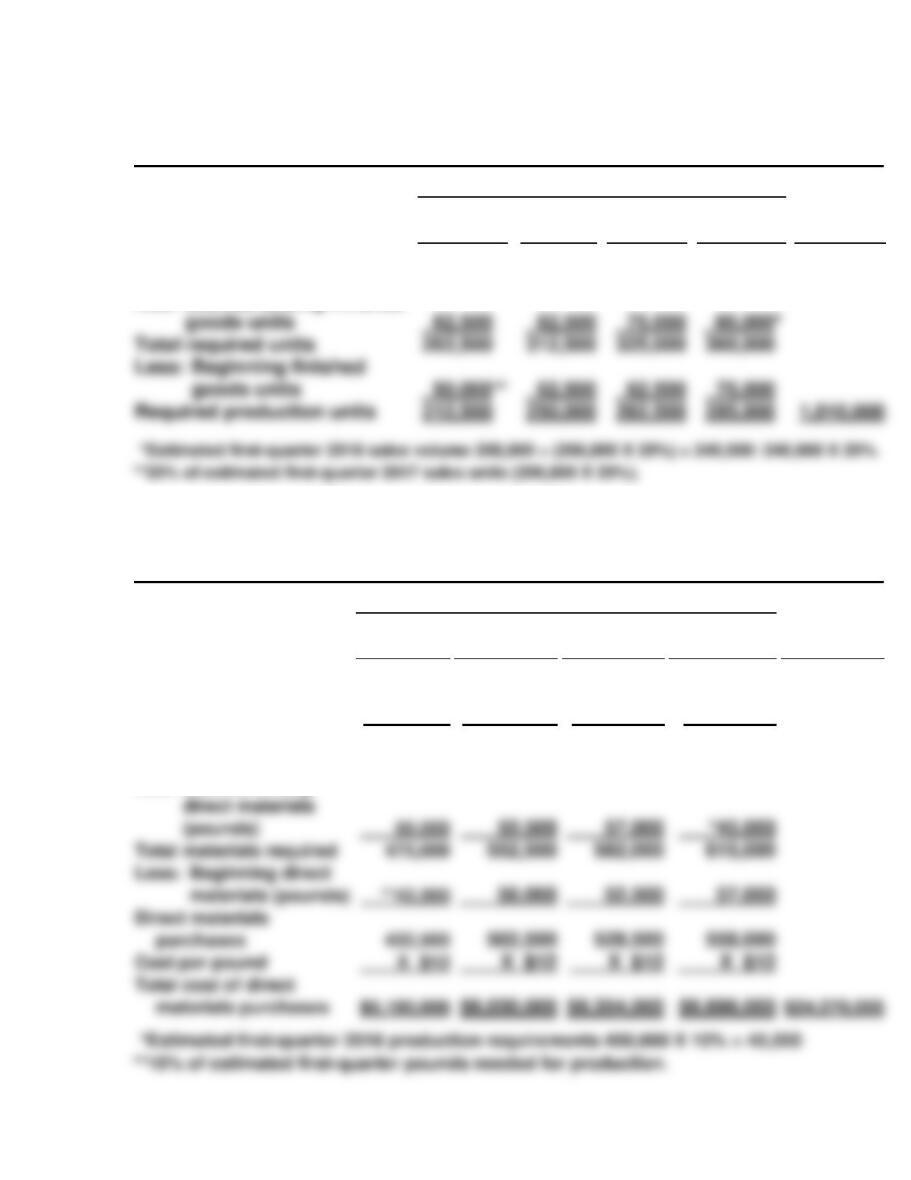

PROBLEM 9-1A

COOK FARM SUPPLY COMPANY

Sales Budget

For the Six Months Ending June 30, 2017

Quarter

Six

Months

1

2

Expected unit sales …………………

40,000

56,000

96,000

COOK FARM SUPPLY COMPANY

Production Budget

For the Six Months Ending June 30, 2017

Quarter

Six

Months

1

2

Required production units …………………………...

Expected unit sales ……………………………………..

Add: Desired ending finished goods

units …………………………………………………

40,000

15,000

56,000

18,000

Total sales ……………………………..

PROBLEM 9-1A (Continued)

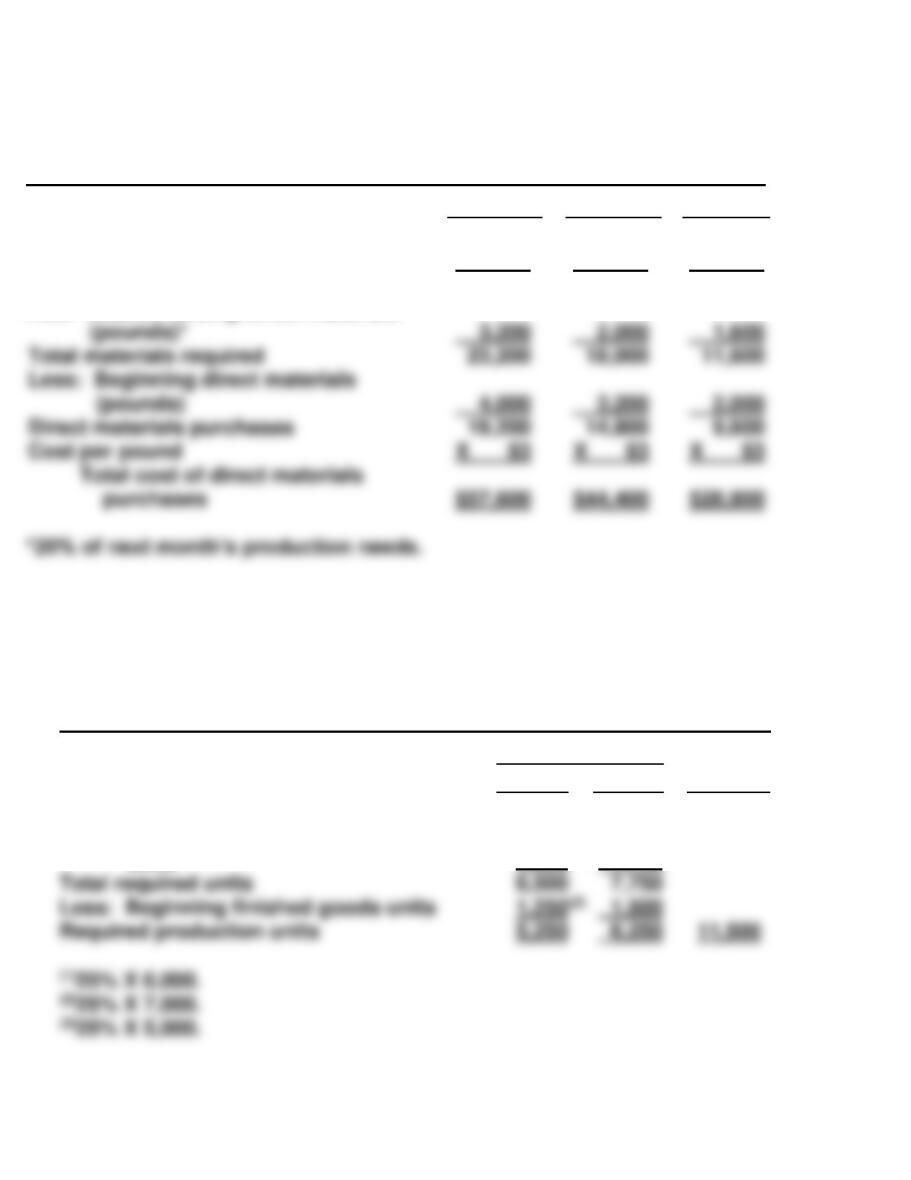

COOK FARM SUPPLY COMPANY

Direct Materials Budget—Gumm

For the Six Months Ending June 30, 2017

Quarter

Six

Months

1

2

Units to be produced ………………………………

Direct materials per unit ………………………….

Total pounds needed for production ……….

Add: Desired ending direct materials

47,000

X 4

188,000

59,000

X 4

236,000

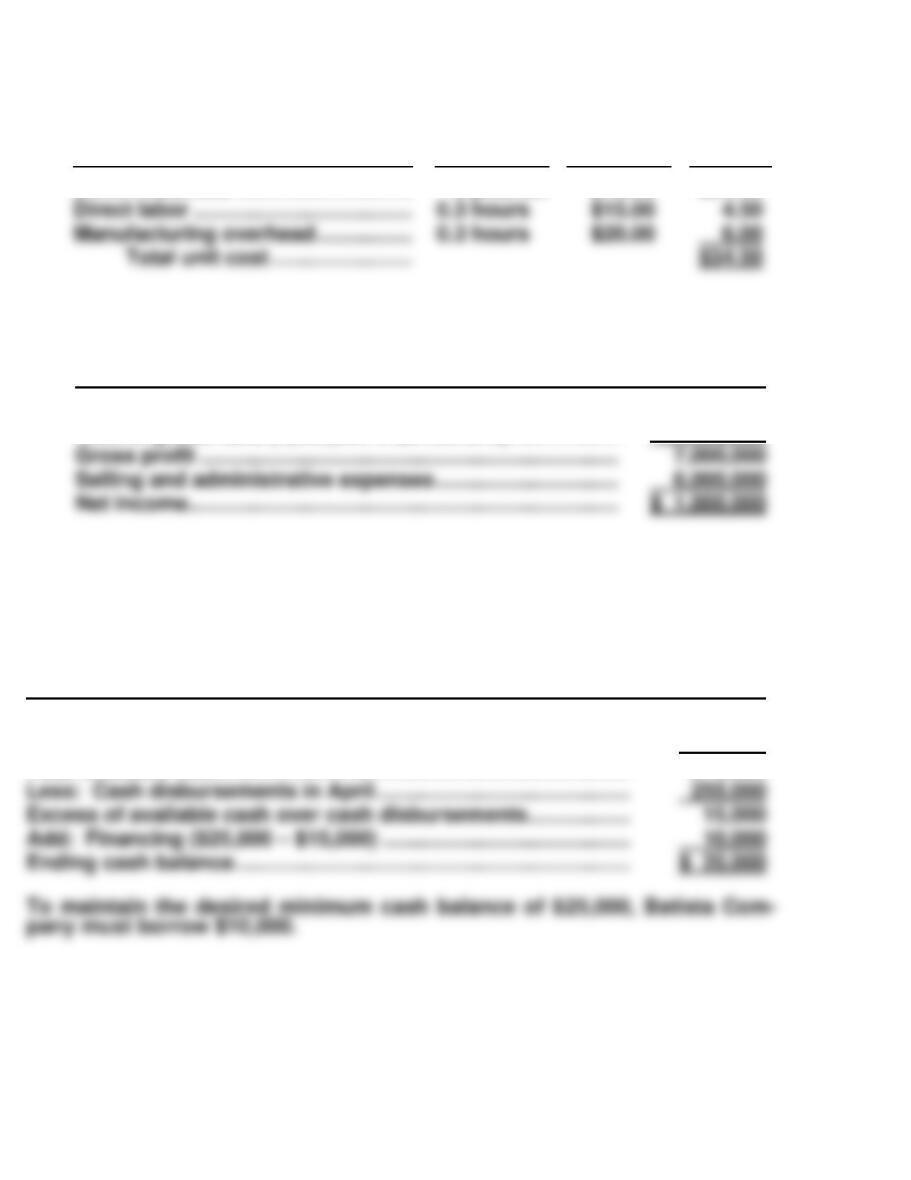

COOK FARM SUPPLY COMPANY

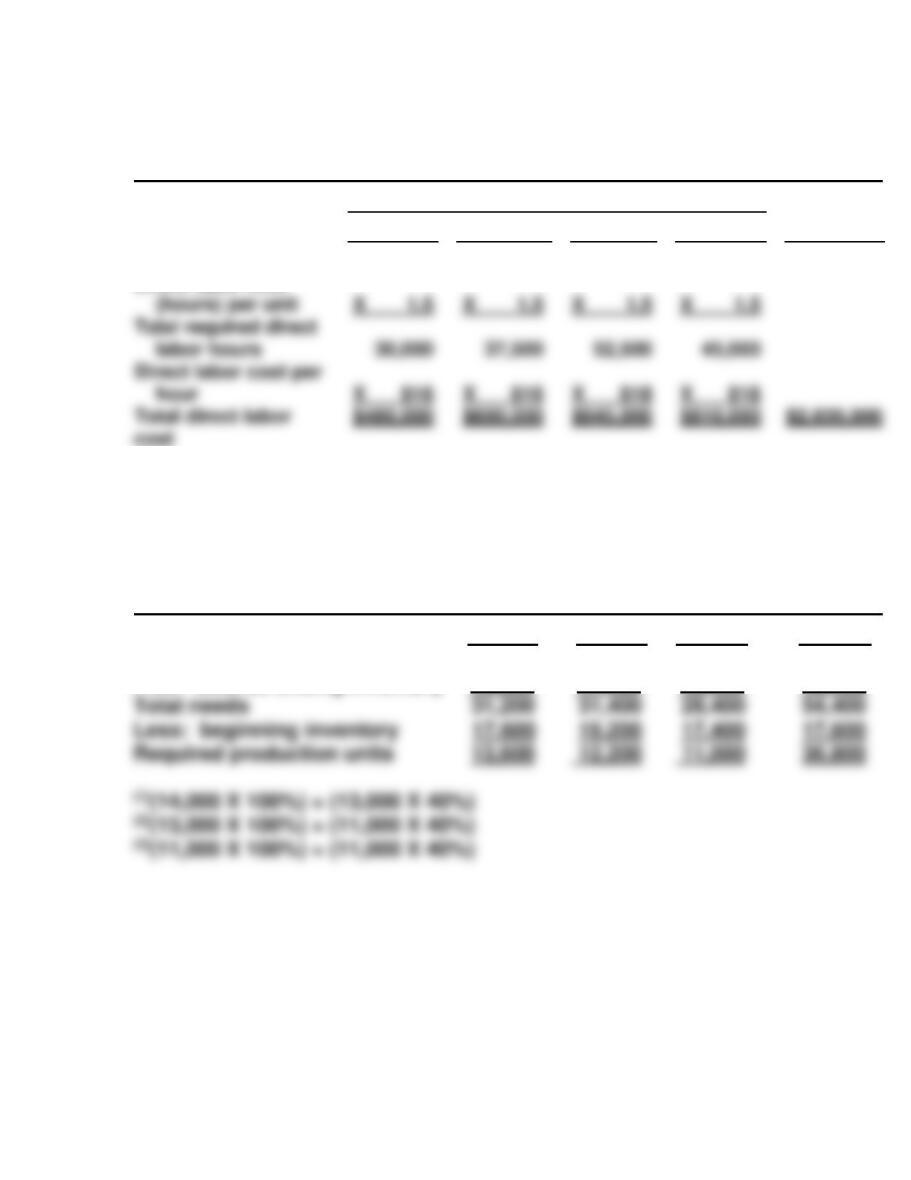

Direct Labor Budget

For the Six Months Ending June 30, 2017

Quarter

Six

Months

1

2

Units to be produced ………………………

Direct labor time (hours) per unit ……..

47,000

X 1/4

59,000

X 1/4

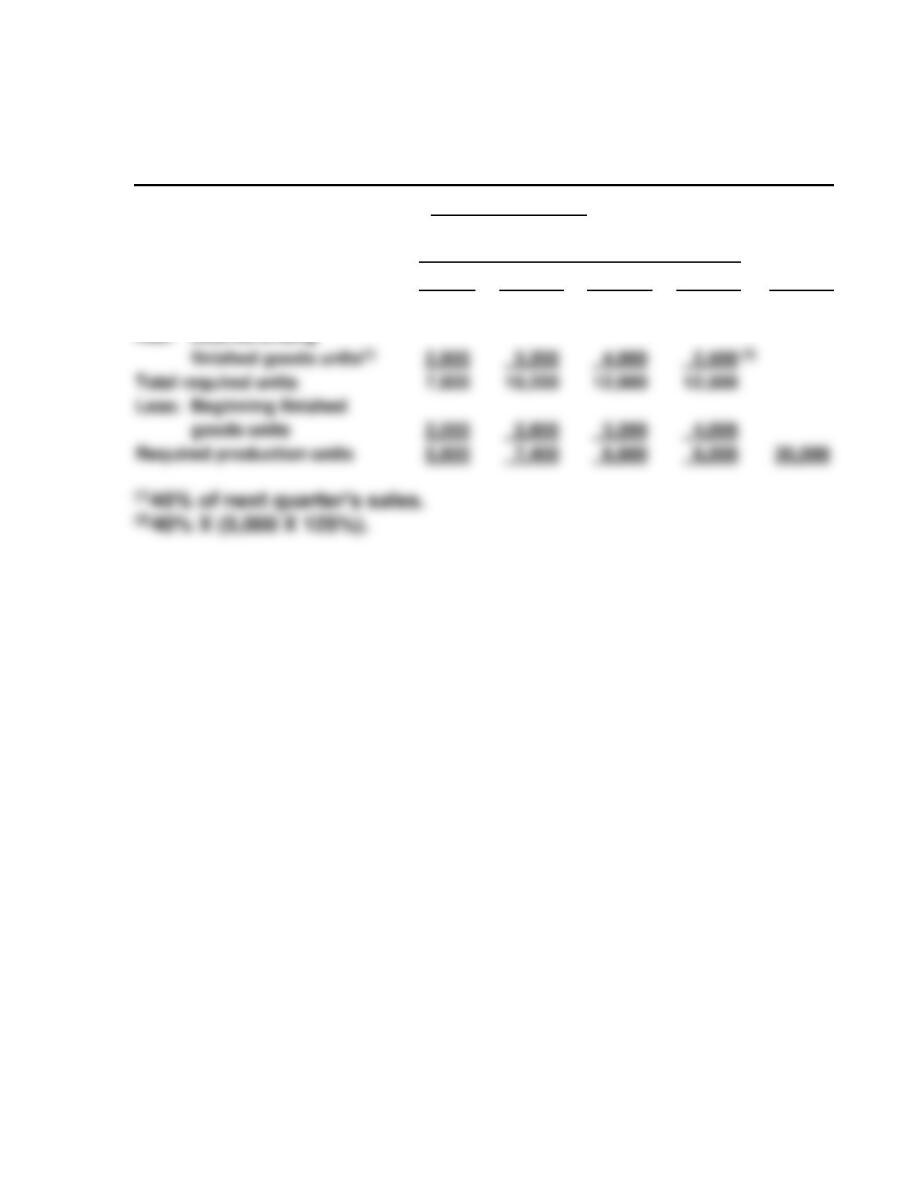

PROBLEM 9-1A (Continued)

COOK FARM SUPPLY COMPANY

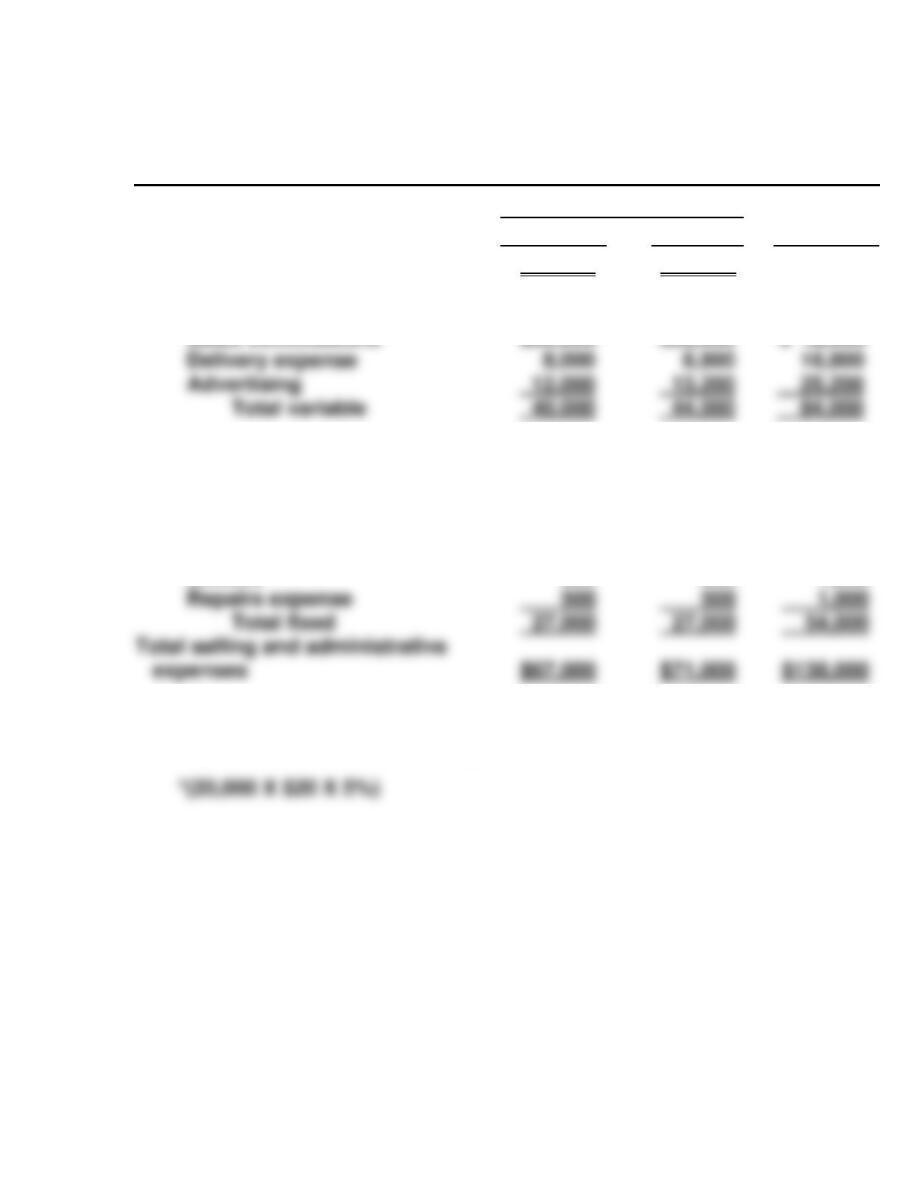

Selling and Administrative Expense Budget

For the Six Months Ending June 30, 2017

Quarter

Six

Months

1

2

Budgeted sales in units

40,000

56,000

96,000

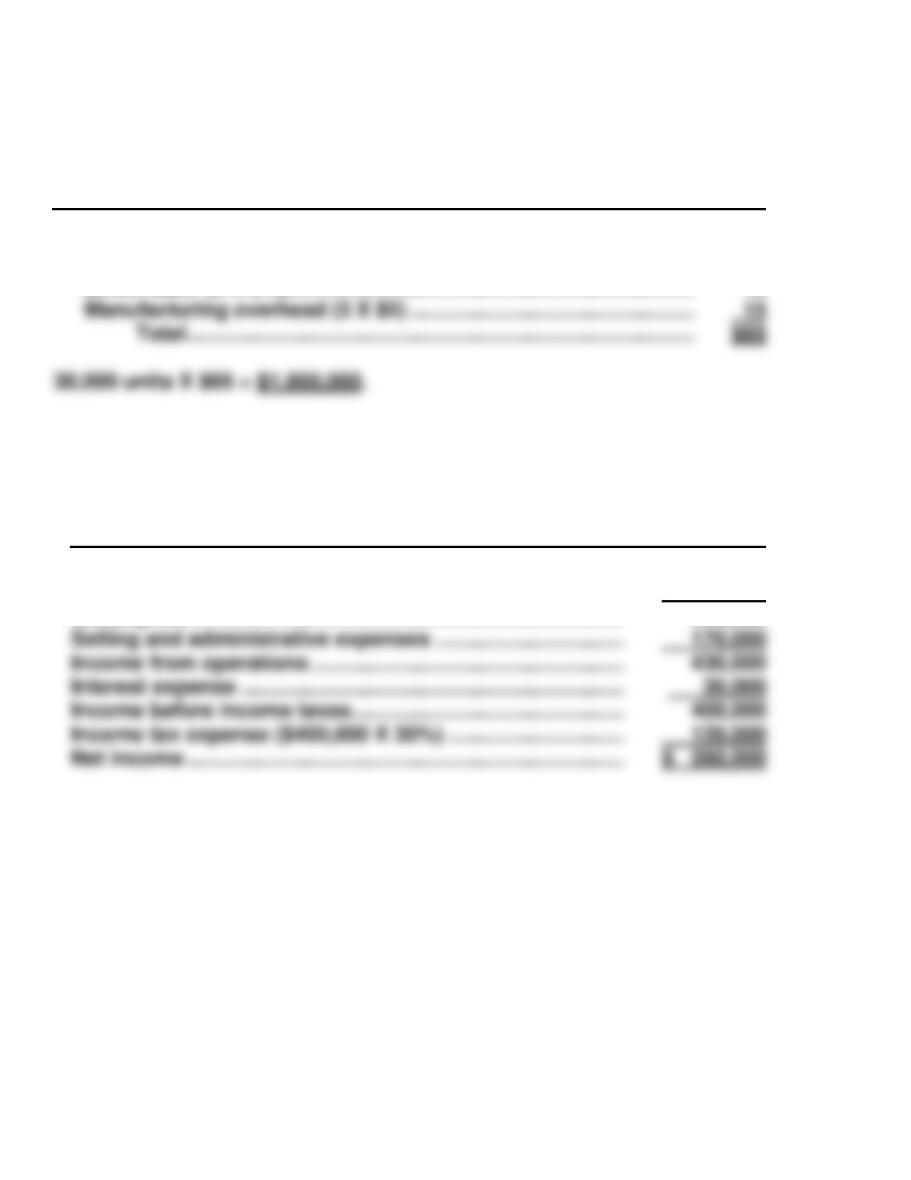

COOK FARM SUPPLY COMPANY

Budgeted Income Statement

For the Six Months Ending June 30, 2017

Sales ………………………………………………………………………………… $5,760,000

Cost of goods sold (96,000 X $33.20)* ………………………………… 3,187,200

Gross profit ………………………………………………………………………. 2,572,800

*Cost Per Bag

Cost Element

Quantity

Unit Cost

Total

Direct materials

Gumm ……………………………………

Tarr ………………………………………..

4 pounds

6 pounds

$ 3.80

1.50

$15.20

9.00

PROBLEM 9-2A

(a) DELEON INC.

Sales Budget

For the Year Ending December 31, 2017

JB 50

JB 60

Total

Expected unit sales …………..

400,000

200,000

(b) DELEON INC.

Production Budget

For the Year Ending December 31, 2017

JB 50

JB 60

Expected unit sales …………………………

400,000

200,000

PROBLEM 9-2A (Continued)

(c) DELEON INC.

Direct Materials Budget

For the Year Ending December 31, 2017

JB 50

JB 60

Total

Units to be produced ………………….

Direct materials per unit ……………..

Total pounds needed for

405,000

X 2

205,000

X 3

(d) DELEON INC.

Direct Labor Budget

For the Year Ending December 31, 2017

JB 50

JB 60

Total

Units to be produced ………………….

405,000

205,000

650,000

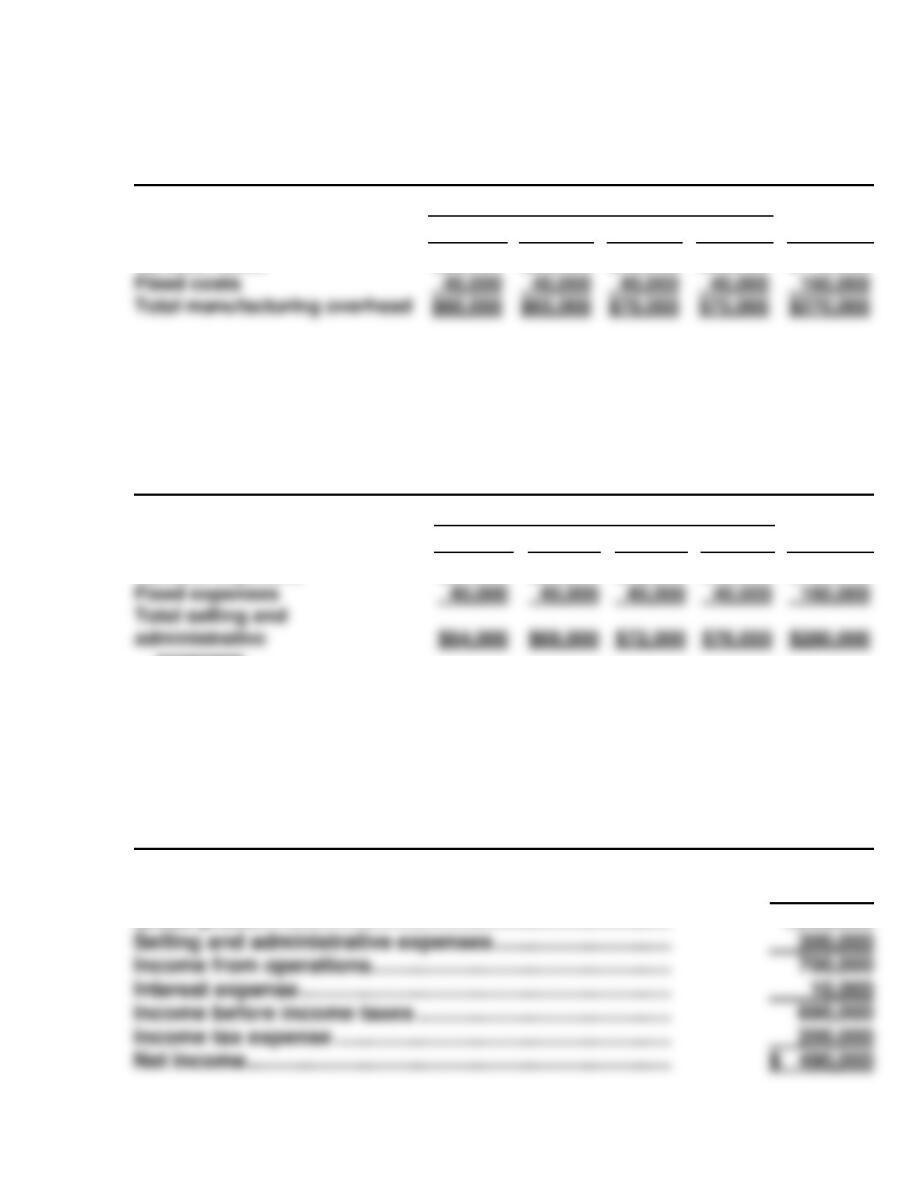

$2,440,000

PROBLEM 9-2A (Continued)

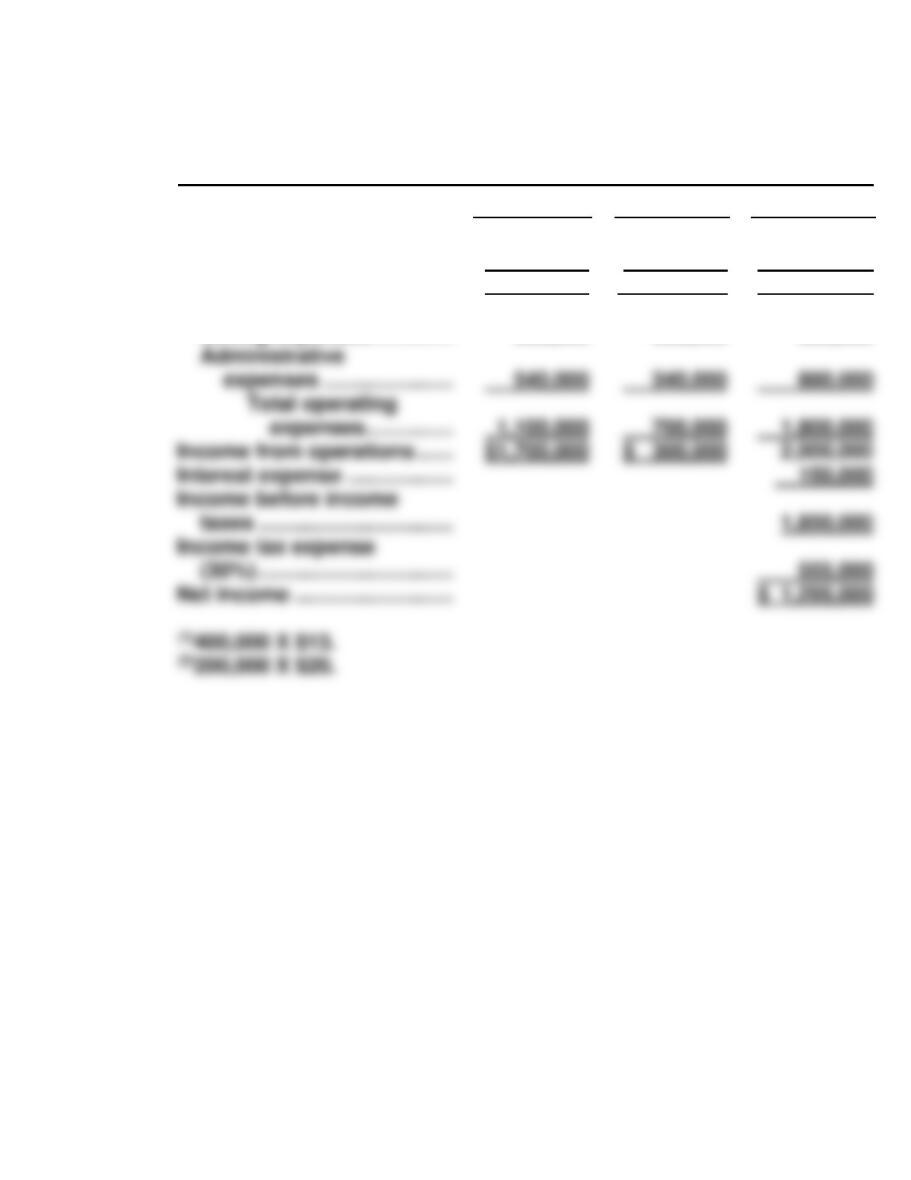

(e) DELEON INC.

Budgeted Income Statement

For the Year Ending December 31, 2017

JB 50

JB 60

Total

Sales ………………………………..

Cost of goods sold ……………

Gross profit ………………………

Operating expenses

Selling expenses ……………

$8,000,000

5,200,000

2,800,000

560,000

(1)

$5,000,000

4,000,000

1,000,000

360,000

(2)

$13,000,000

9,200,000

3,800,000

920,000

$ 1,295,000

PROBLEM 9-3A

(a) HILL INDUSTRIES

Sales Budget

For the Year Ending December 31, 2017

Plan A

Plan B

Expected unit sales ……………………………..

765,000

(1)

950,000

(2)

(b) HILL INDUSTRIES

Production Budget

For the Year Ending December 31, 2017

Plan A

Plan B

Total required units ……………………………………….

Expected unit sales ……………………………………….

Add: Desired ending finished goods units ……

765,000

38,250

(1)

950,000

60,000

(c) Variable costs = $4.40 per unit ($1.80 + $1.40 + $1.20) for both plans.

Plan A

Plan B

$6.88

$6.35

PROBLEM 9-3A (Continued)

(d) Gross Profit

Plan A

Plan B

Sales

$6,426,000

$7,125,000

PROBLEM 9-4A

(a) (1) Expected Collections from Customers

January

February

November ($250,000) …………………………..

December ($320,000) …………………………..

$ 50,000

96,000

$ 0

64,000

(2) Expected Payments for Direct Materials

January

February

December ($100,000) …………………………..

$ 40,000

$ 0

PROBLEM 9-4A (Continued)

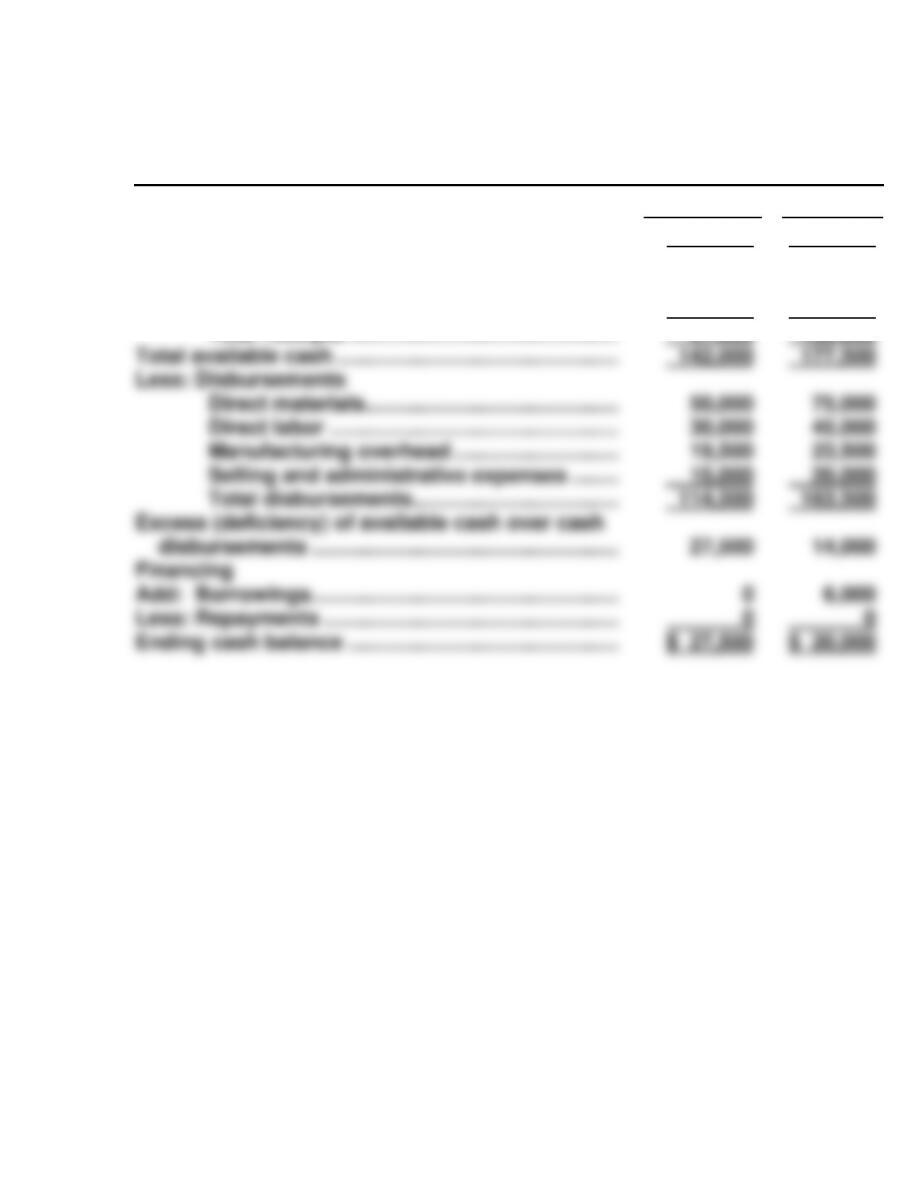

(b) COLTER COMPANY

Cash Budget

For the Two Months Ending February 28, 2017

January

February

Beginning cash balance …………………………….

Add: Receipts

Collections from customers …………

[See Schedule (1)]

Notes receivable ………………………….

Sale of securities …………………………

Total receipts ……………………….

Total available cash …………………………………..

$ 60,000

326,000

15,000

341,000

401,000

$ 51,000

372,000

6,000

378,000

429,000

Less: Repayments ……………………………………

Ending cash balance …………………………………

0

$ 51,000

0

$ 50,000

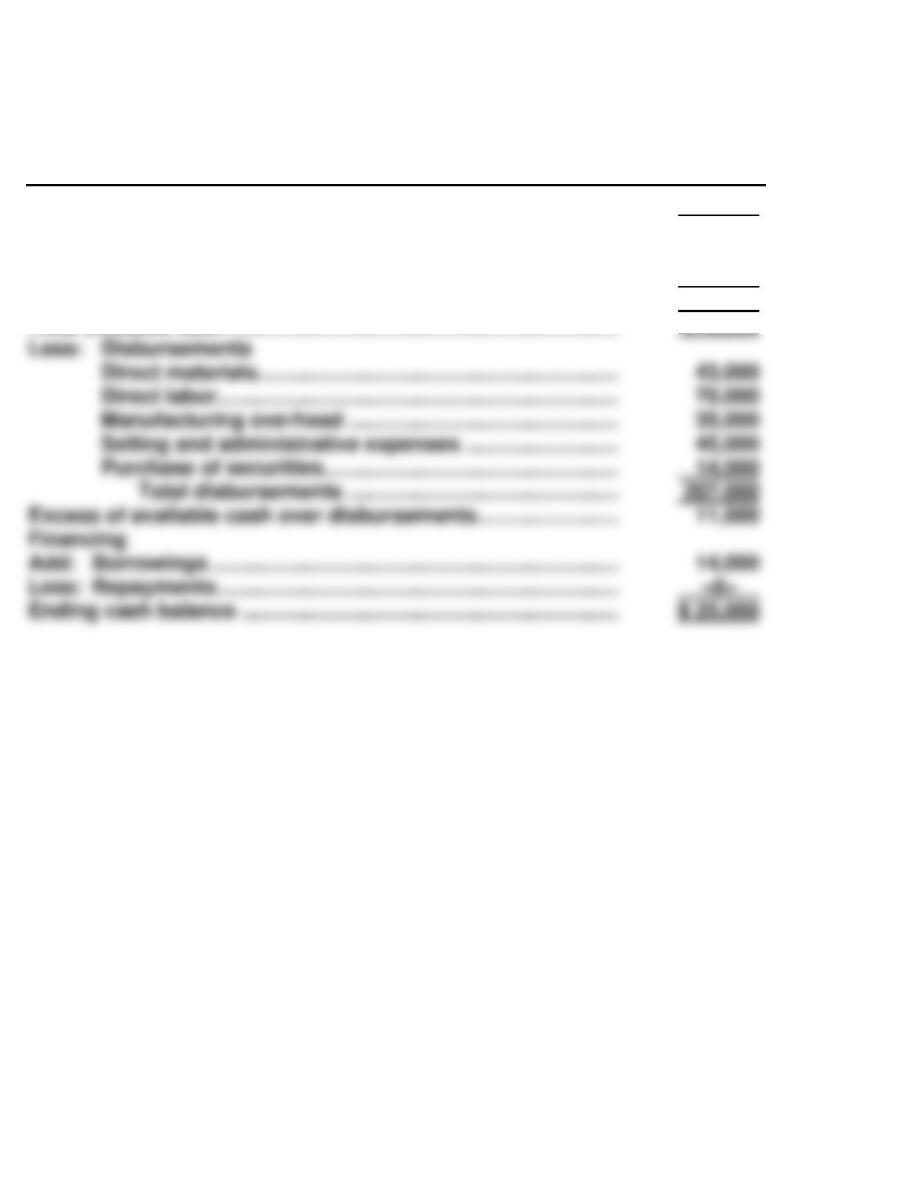

PROBLEM 9-5A

(a) SUPPAR COMPANY

San Miguel Store

Merchandise Purchases Budget

For the Months of May and June, 2017

May

June

Budgeted cost of goods sold ………………………

Add: Desired ending merchandise inventory …..

$600,000

63,000

(2)

$630,000

66,150

(1)

(3)

PROBLEM 9-5A (Continued)

(b) SUPPAR COMPANY

San Miguel Store

Budgeted Income Statement

For the Months of May and June, 2017

May

June

Sales …………………………………………………………

Cost of goods sold

Beginning inventory …………………………….

Purchases …………………………………………..

Cost of goods available for sale …………..

$800,000

60,000

603,000

663,000

$840,000

63,000

633,150

696,150

Net income ………………………………………………..

Income from operations ……………………………..

Interest expense ………………………………………..

Income before income taxes ……………………….

54,100

2,000

52,100

58,900

2,000

56,900

Less: Ending inventory ……………………….

Gross profit ……………………………………………….

PROBLEM 9-6A

KRAUSE INDUSTRIES

Budgeted Cost of Goods Sold

For the Year Ending December 31, 2017

Finished goods inventory, 1/1/17 ……………………… $ 24,000

Cost of goods manufactured

Direct materials used ………………………………… $62,500

KRAUSE INDUSTRIES

Budgeted Income Statement

For the Year Ending December 31, 2017

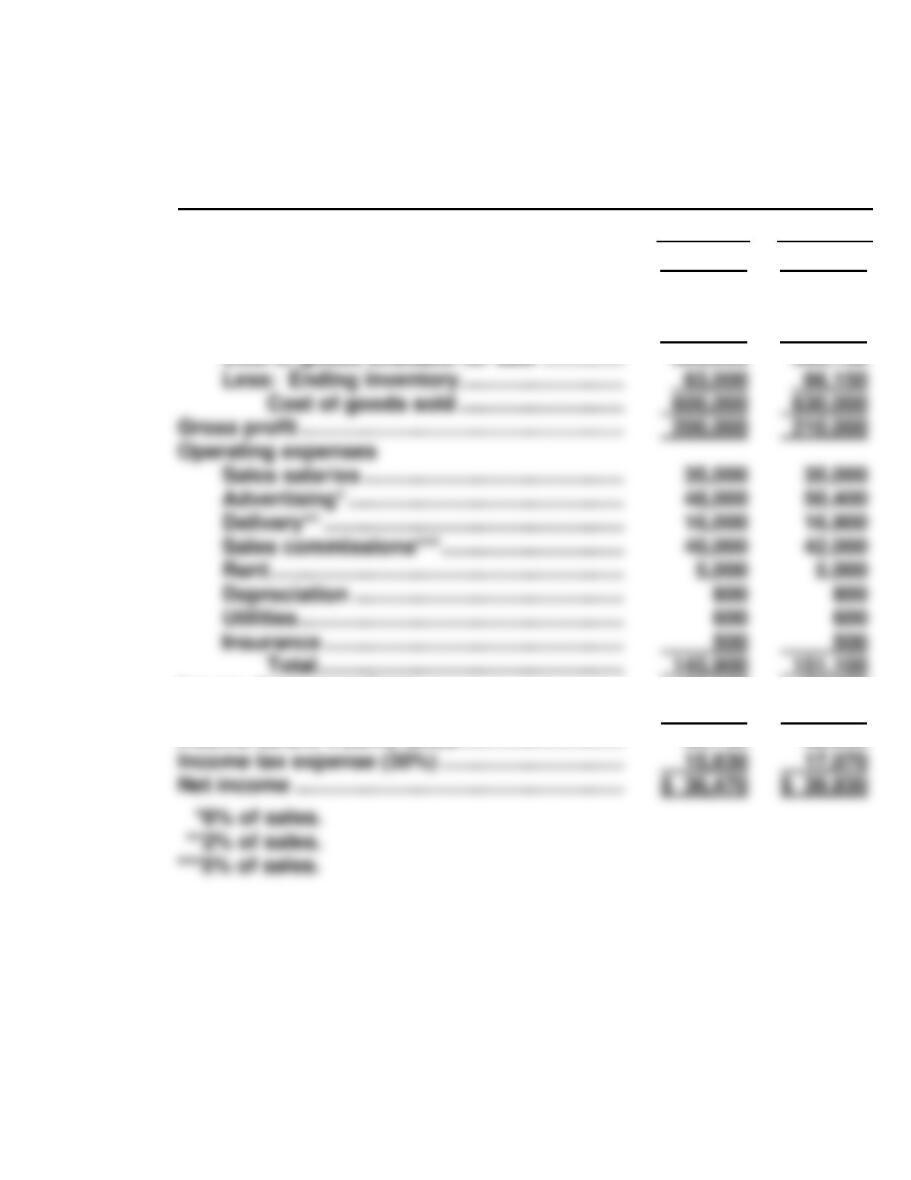

Sales revenue (8,000 $32) …………………………..…. $256,000

Cost of goods sold ………………………………………….. 141,000

Gross profit …………………………………………………….. 115,000

KRAUSE INDUSTRIES

Budgeted Retained Earnings Statement

For the Year Ending December 31, 2017

Retained earnings, 1/1/17 …………………………………. $25,000

Add: Net income ……………………………………………… 21,900

PROBLEM 9-6A (Continued)

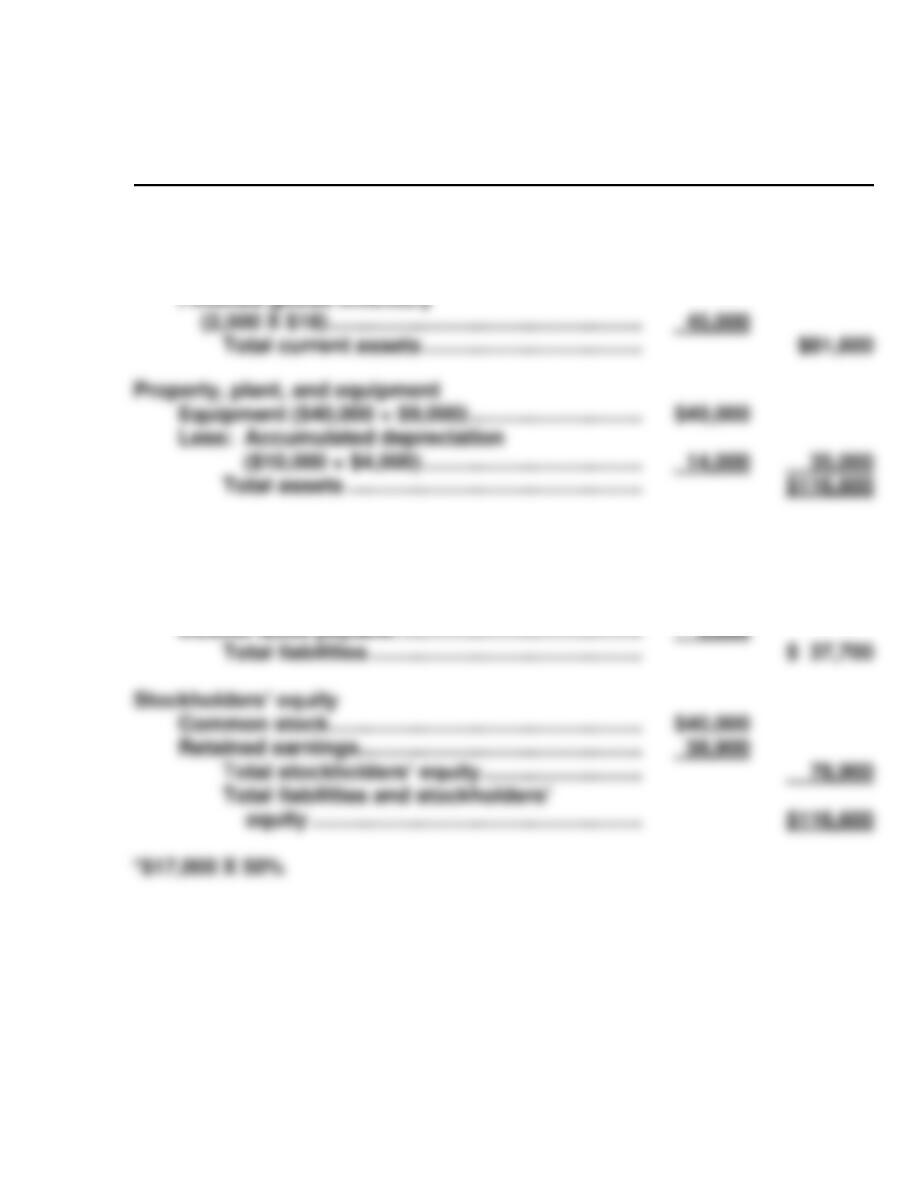

KRAUSE INDUSTRIES

Budgeted Balance Sheet

December 31, 2017

Assets

Current assets

Cash ……………………………………………………….…… $ 5,880

Accounts receivable ($76,800 X 40%) ……………. 30,720

Liabilities and Stockholders’ Equity

Liabilities

Notes payable ($25,000 – $8,000) ………………….. $17,000

Accounts payable ($8,500* + $7,200) ……………… 15,700

PROBLEM 9-6A (Continued)

Proof of budgeted cash balance December 31, 2017

Beginning Cash ………………………………………………. $ 7,500

Collections

Beginning accounts receivable ………………………… $ 73,500

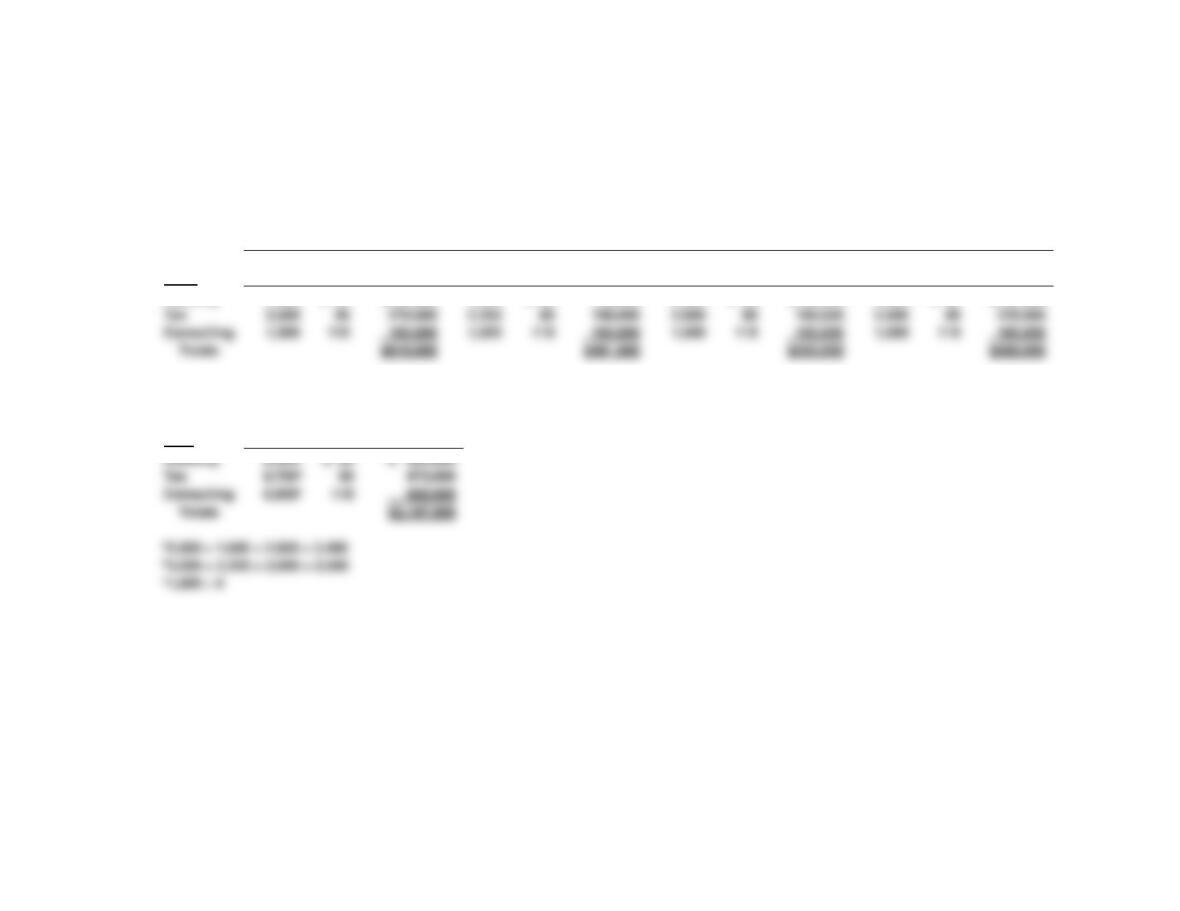

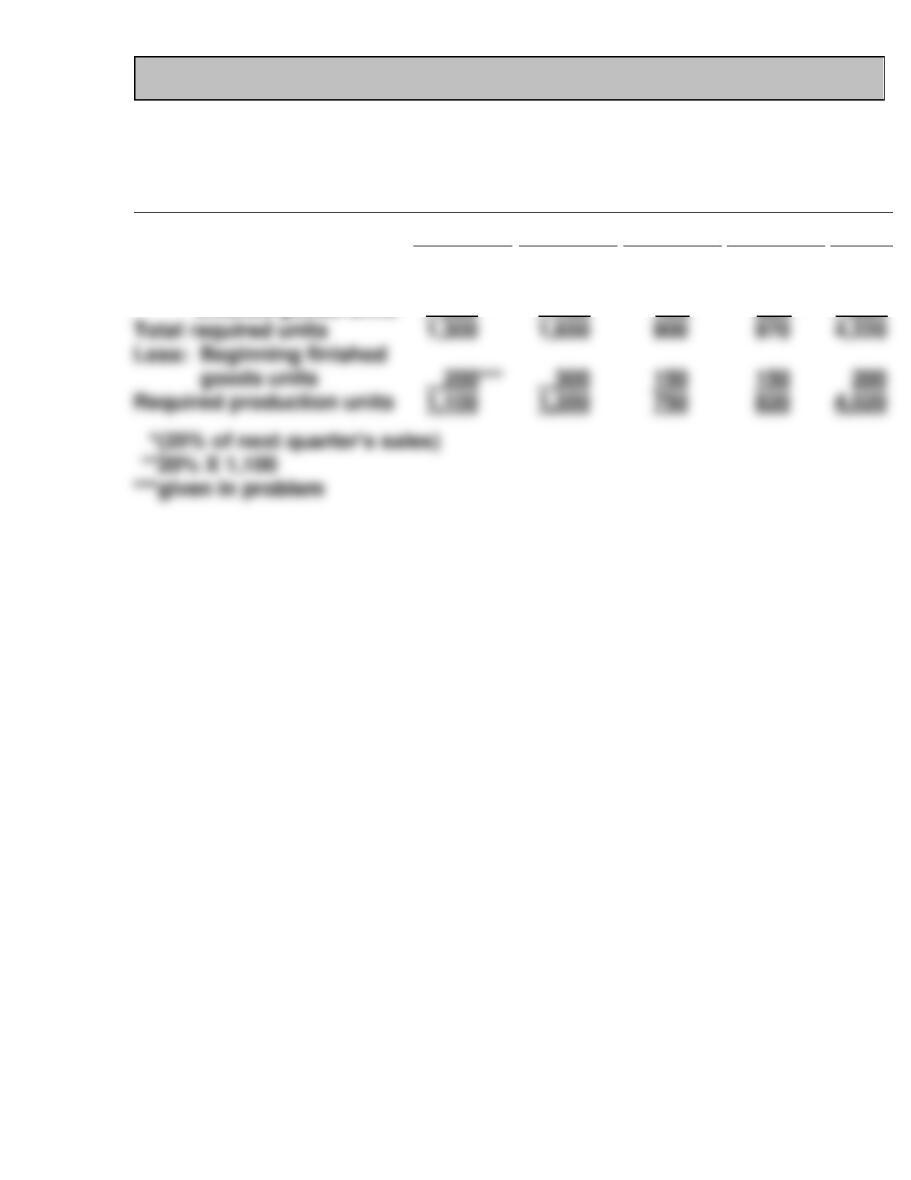

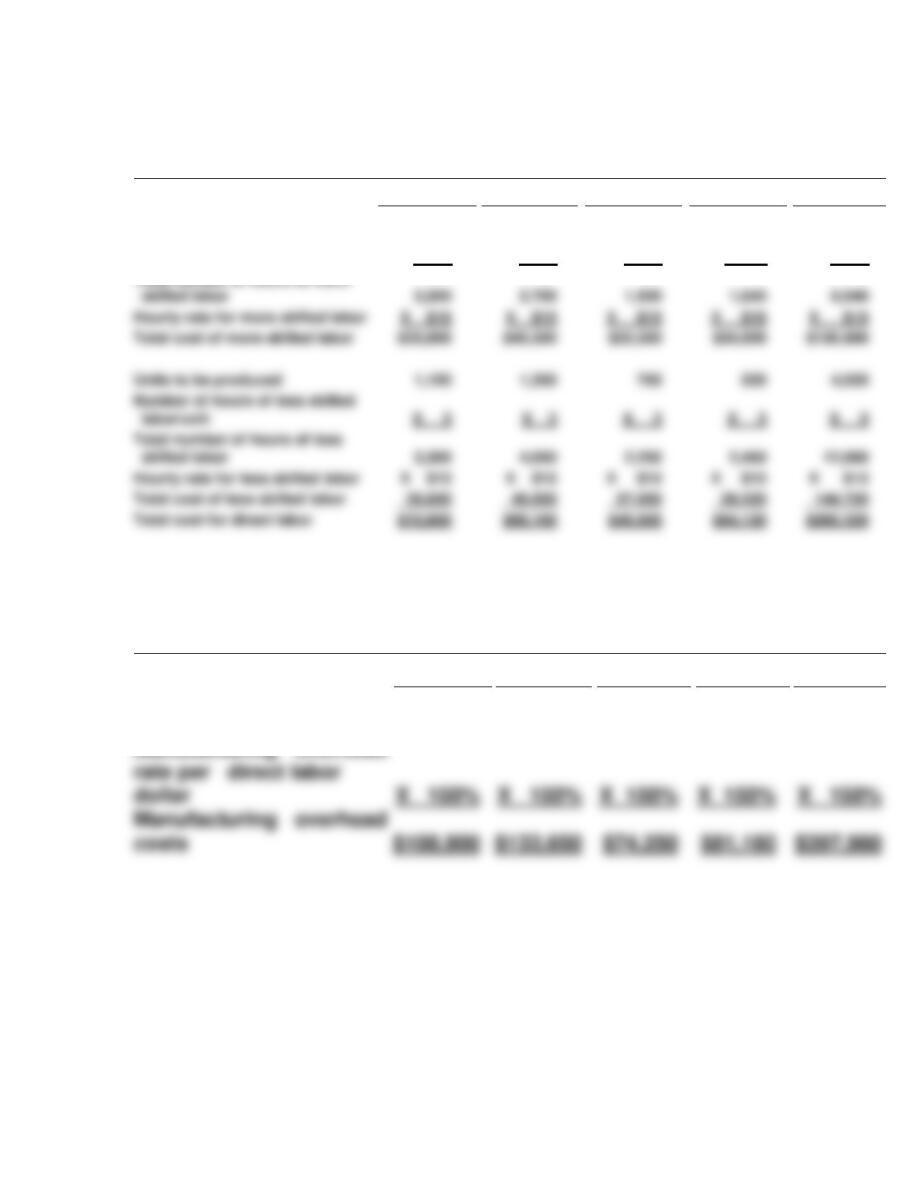

CD9 CURRENT DESIGNS

CURRENT DESIGNS

Production Budget

For the Year Ending December 31, 2017

Quarter 1

Quarter 2

Quarter 3

Quarter 4

Total

Expected unit sales

1,000

1,500

750

750

4,000

Add: desired ending

finished goods units

300*

150*

150*

220**

220

Total required units

1,300

1,650

900

970

4,220

goods units

300

150

Required production units

1,100

1,350

750

820

4,020

CD9 (Continued)

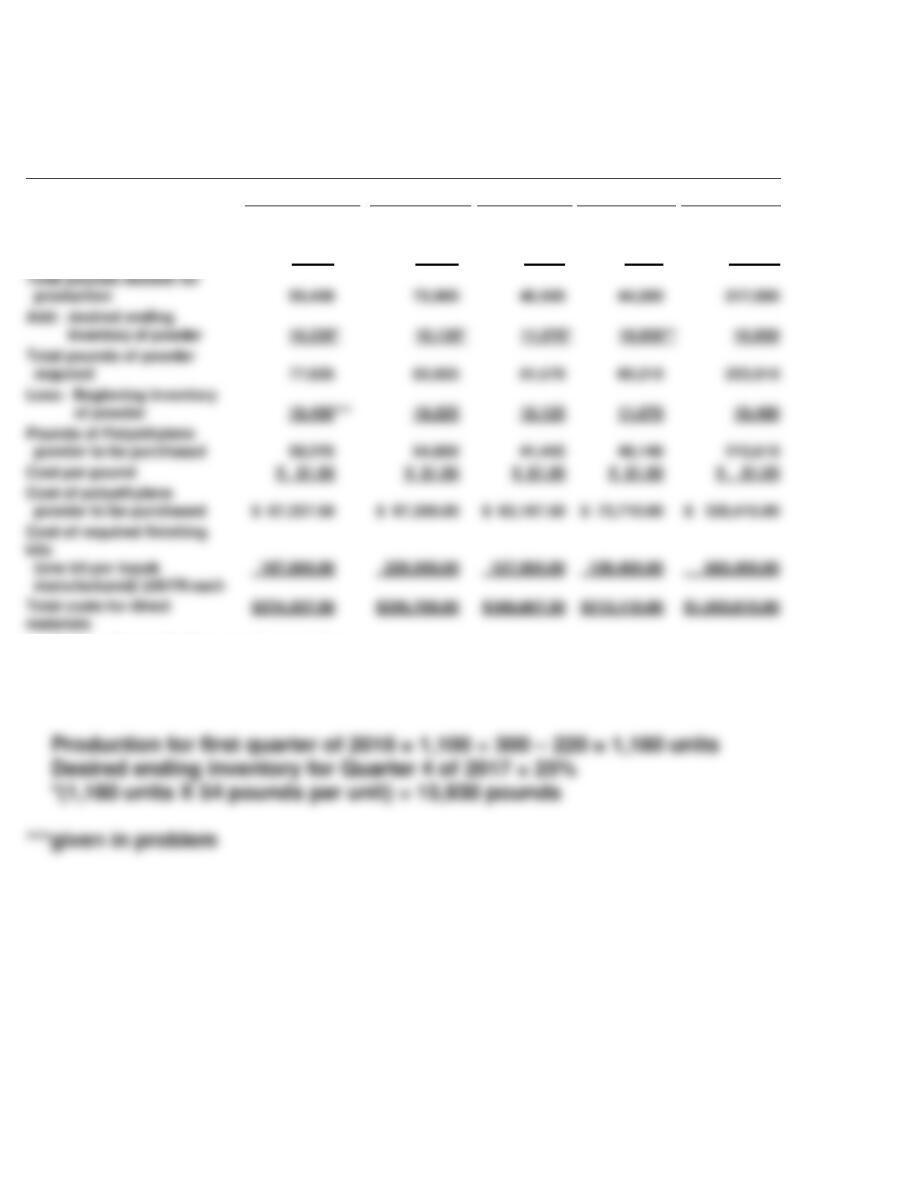

CURRENT DESIGNS

Direct materials Budget

For the Year Ending December 31, 2017

Quarter 1

Quarter 2

Quarter 3

Quarter 4

Total

Units to be produced

1,100

1,350

750

820

4,020

Pounds of polyethylene

powder per unit

X 54

X 54

X 54

X 54

X 54

*25% of needs for next quarter

**Desired ending inventory for Quarter 4 = 25% of amount needed for first

quarter of 2018 production.

Total pounds needed for

Add: desired ending

inventory of powder

10,125*

15,930

required

Less: Beginning inventory

Pounds of Polyethylene

powder to be purchased

Cost per pound

Cost of polyethylene

manufactured) @$170 each

materials

CD9 (Continued)

CURRENT DESIGNS

Direct labor Budget

For the Year Ending December 31, 2017

Quarter 1

Quarter 2

Quarter 3

Quarter 4

Total

Units to be produced

1,100

1,350

750

820

4,020

Number of hours of more skilled

labor/unit

X 2

X 2

X 2

X 2

X 2

Total number of hours of more

CURRENT DESIGNS

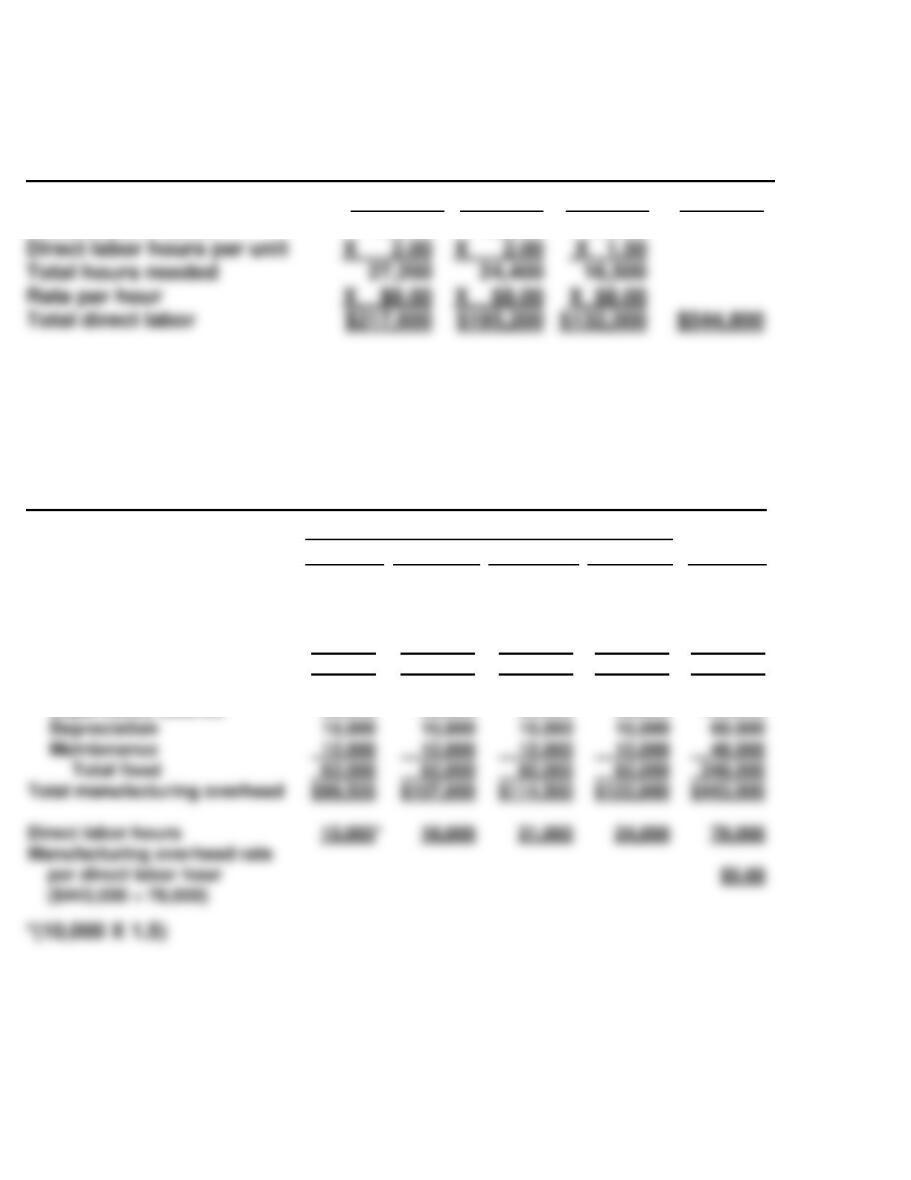

Manufacturing Overhead Budget

For the Year Ending December 31, 2017

Quarter 1

Quarter 2

Quarter 3

Quarter 4

Total

Total costs for direct

labor

$72,600

$89,100

$49,500

$54,120

$265,320

rate per direct labor

X 150%

X 150%

$74,250

$81,180

$397,980

Manufacturing overhead

Total cost of more skilled labor

Number of hours of less skilled

labor/unit

X 3

X 3

X 3

X 3

Total number of hours of less

Total cost of less skilled labor

Total cost for direct labor

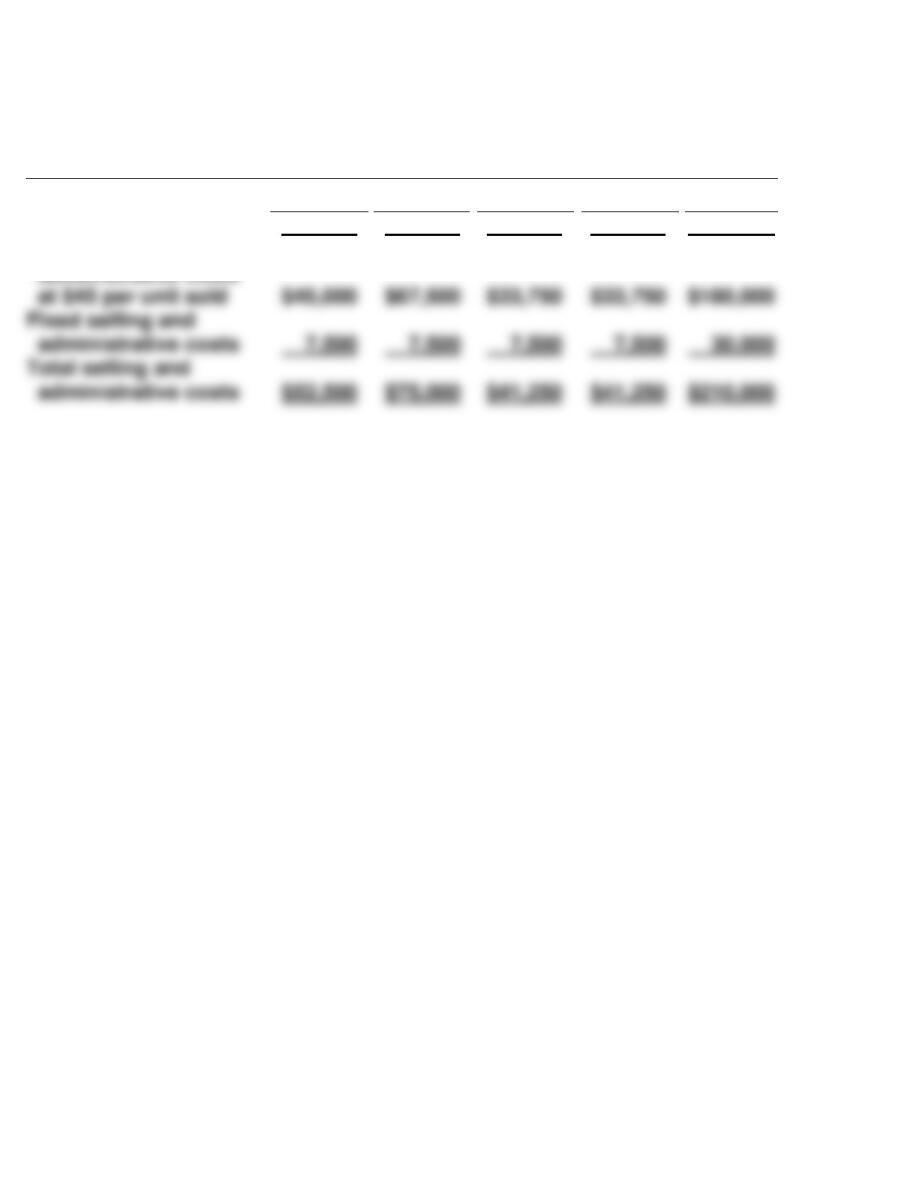

CD9 (Continued)

CURRENT DESIGNS

Selling and Administrative Expense Budget

For the Year Ending December 31, 2017

Quarter 1

Quarter 2

Quarter 3

Quarter 4

Total

Expected unit sales

1,000

1,500

750

750

4,000

Variable selling and

administrative costs

BYP 9-1 DECISION-MAKING ACROSS THE ORGANIZATION

(a) The budget at Palmer Corporation is an imposed “top–down” budget

which fails to consider both the need for realistic data and the human

interaction essential to an effective budgeting/control process. The

president has not given any basis for his goals, so one cannot know

whether they are realistic for the company. True participation of company

employees in preparation of the budget is minimal and limited to mechani–

cal gathering and manipulation of data. This suggests there will be little

enthusiasm for implementing the budget.

The budget process is the merging of the requirements of all facets of

the company on a basis of sound judgment and equity. Specific instances

of poor procedures other than the approach and goals include the

following:

1. The sales by product line should be based upon an accurate sales

forecast of potential market. Therefore, the sales by product line

(b) Palmer Corporation should consider the adoption of a “bottom to top”

(participative) budget process. This means that the people responsible

for performance under the budget would participate in the decisions

by which the budget is established. In addition, this approach requires

BYP 9-1 (Continued)

The sales forecast should be developed considering internal sales

(c) The functional areas should not necessarily be expected to cut costs

when sales volume falls below budget. The time frame of the budget

(one year) is short enough so that many costs are relatively fixed in

BYP 9-2 MANAGERIAL ANALYSIS

(a) Direct materials Either lower quality materials resulting in an inferior

product and possible lost sales, or fewer units

produced resulting in lost sales.

Direct labor Reduced production resulting in lost sales, or

reduction in quality of product resulting in lost sales.

(b) Given the nature of their product, a decline in quality should be

avoided, since this could result in lower future sales. Direct materials

represent the largest single cost, and thus perhaps the greatest

potential savings. Perhaps substitute materials of similar quality can

BYP 9-3 REAL-WORLD FOCUS

(a) According to Mr. LaFaive, zero-based budgeting requires that the

existence of a government program or programs be justified in each

(b) In addition to saving money and improving services, zero-based

budgeting may:

• Increase restraint in developing budgets;

(c) On the cost side of the equation, zero-based budgeting:

• May increase the time and expense of preparing a budget;

(d) In Oklahoma, which has recently adopted zero-based budgeting, officials

BYP 9-4 COMMUNICATION ACTIVITY

Date 2017

Mrs. Megan Parcells, CEO

Life Protection Products

Dear Mrs. Parcells:

Allow me to congratulate you on the success of your new venture! The

growth in sales you have experienced is phenomenal. You have managed the

business side of the venture very well also. At the same time, I understand

your concern about cash flow. You are selling these kits as fast as you can

make them, and yet you are running out of cash.

There is a solution to your problem. Before describing that, it may be

helpful for you to understand why this situation occurred. The primary

reason is that you are purchasing kit supplies at least two months in advance

BYP 9-4 (Continued)

However, even if you raised prices, you will find that you need additional

cash as long as the business continues to expand. It certainly does not

mean that you and Sue are doing anything wrong. It just means that you

will be investing additional funds as long as you continue to grow.

BYP 9-5 ETHICS CASE

(a) At best, if you disclose the errors in your calculations, you will be

embarrassed. At worst, you will be dismissed without a recommendation

for another job.

BYP 9-6 ALL ABOUT YOU

Personal Budget

Typical Month

Income:

Wages earned ………………………………………….. $2,500

Expenses:

Rent ………………………………………………………………….. 500

Utilities

Electricity ………………………………………………… 85

Telephone and Internet …………………………….. 125

BYP 9-7 CONSIDERING YOUR COSTS AND BENEFITS

We are concerned that the personal budgets presented on websites and in

financial planning textbooks often list student loans among the sources of

income. This type of thinking can lead to an overreliance on debt during