Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

2. Real estate acquired as speculation should be listed in the balance sheet under the caption

“Investments,” below the Current Assets section.

4. Capital expenditures include the cost of acquiring fixed assets and the cost of improving an

asset. These costs are recorded by increasing (debiting) a fixed asset account. Capital

5. Capital expenditure

7. a. No

b. No

8. a. An accelerated depreciation method is most appropriate for situations in which the decline

in productivity or earning power of the asset is proportionately greater in the early years of

9. a. No, the accumulated depreciation for an asset cannot exceed the cost of the asset. To do so

would create a negative book value, which is meaningless.

10. a. Over the shorter of its legal life or years of usefulness.

CHAPTER 9

FIXED ASSETS AND INTANGIBLE ASSETS

DISCUSSION QUESTIONS

9-1

CHAPTER 9 Fixed Assets and Intangible Assets

PE 9–1A

7 Delivery Truck 1,675

PE 9–1B

14 Accumulated Depreciation—Delivery Van 2,300

PE 9–2A

a. $295,000 ($340,000 – $45,000)

PE 9–2B

PE 9–3A

PE 9–3B

Feb.

PRACTICE EXERCISES

Aug.

CHAPTER 9 Fixed Assets and Intangible Assets

PE 9–4A

PE 9–4B

PE 9–5A

PE 9–5B

PE 9–6A

a. $28,000 [($465,000 – $45,000) ÷ 15]

9-3

CHAPTER 9 Fixed Assets and Intangible Assets

PE 9–6B

a. $75,000 = $600,000 × [(1 ÷ 16) × 2)] = $600,000 × 12.5%

b. $20,625 gain, computed as follows:

Cost……………………………………………

…

$600,000

PE 9–7A

a. $0.30 per ton = $127,500,000 ÷ 425,000,000 tons

PE 9–7B

a. $1.04 per ton = $494,000,000 ÷ 475,000,000 tons

CHAPTER 9 Fixed Assets and Intangible Assets

PE 9–8A

a. Dec. 31 Loss from Impaired Goodwill 4,000,000

Goodwill 4,000,000

Impaired goodwill.

PE 9–8B

a. Dec. 31 Loss from Impaired Goodwill 6,000,000

Goodwill 6,000,000

Impaired goodwill.

PE 9–9A

a. Fixed Asset Turnover:

Sales……………………………

…

Fixed assets:

Beginning of year…………

…

2016 2015

$5,510,000 $4,880,000

$1,600,000 $1,450,000

9-5

CHAPTER 9 Fixed Assets and Intangible Assets

PE 9–9B

a. Fixed Asset Turnover:

Revenue………………………

…

Fixed assets:

Beginning of year………

…

2016 2015

$1,668,000 $1,125,000

$ 670,000 $ 580,000

9-6

CHAPTER 9 Fixed Assets and Intangible Assets

Ex. 9–1

a. New printing press: 1, 2, 3, 5, 6

b. Used printing press: 7, 8, 9, 11

Ex. 9–2

Ex. 9–3

Initial cost of land ($75,000 + $90,000)………………………

…

$165,000

Plus: Legal fees………………………………………………

…

$ 2,500

Ex. 9–4

Capital expenditures: 3, 4, 5, 6, 7, 9, 10

EXERCISES

9-7

CHAPTER 9 Fixed Assets and Intangible Assets

Ex. 9–6

Mar. 20 Accumulated Depreciation—Delivery Truck 1,890

Cash 1,890

June 11 Delivery Truck 1,350

Ex. 9–7

a. No. The $44,500,000 represents the original cost of the equipment. Its

replacement cost, which may be more or less than $44,500,000, is not

Ex. 9–8

(a) 25% (1 ÷ 4), (b) 12.5% (1 ÷ 8), (c) 10% (1 ÷ 10), (d) 6.25% (1 ÷ 16), (e) 4% (1 ÷ 25),

Ex. 9–9

$2,600 [($48,000 – $9,000) ÷ 15]

9-8

CHAPTER 9 Fixed Assets and Intangible Assets

Ex. 9–11

a. Depreciation Rate per Mile:

Miles Operated

21,000

Ex. 9–12

a.

Ex. 9–13

a. 5% of ($75,000 – $10,000) = $3,250 or [($75,000 – $10,000) ÷ 20]

$0.26

First Year

4% of $120,000 = $4,800

Credit to

$ 5,460

5,360

Rate per Mile Depreciation

Accumulated

Truck No.

1

Second Year

4% of $120,000 = $4,800

9-9

CHAPTER 9 Fixed Assets and Intangible Assets

Ex. 9–14

a. Year 1: 9 ÷ 12 × [($40,000 – $8,000) ÷ 8] = $3,000

Year 2: ($40,000 – $8,000) ÷ 8 = $4,000

Ex. 9–16

a. Apr. 30 Carpet 18,000

Cash 18,000

Ex. 9–17

a. Cost of equipment…………………………………………………………………

…

$140,000

Accumulated depreciation at December 31, 2016

9-10

CHAPTER 9 Fixed Assets and Intangible Assets

Ex. 9–18

a. 2013 depreciation expense: $22,500 [($425,000 – $65,000) ÷ 16]

b. $357,500 [$425,000 – ($22,500 × 3)]

c. Cash 340,000

Accumulated Depreciation—Equipment 67,500

9-11

CHAPTER 9 Fixed Assets and Intangible Assets

Ex. 9–21

a. Property, Plant, and Equipment (in millions):

Current Preceding

Year Year

Land and buildings………………………………………………

…

$ 2,439 $ 2,059

Machinery, equipment, and internal-use software…………

…

15,743 6,926

b. We would expect Apple’s book value of fixed assets to increase during the

year as its sales increase. Although additional depreciation expense will

reduce the book value, most companies, such as Apple, invest in new assets

Ex. 9–22

2. Land does not depreciate.

3. Patents and goodwill are intangible assets that should be listed in a separate

9-12

CHAPTER 9 Fixed Assets and Intangible Assets

Ex. 9–23

Ex. 9–24

a. Best Buy: 13.90 ($50,705 ÷ $3,647)

Ex. 9–25

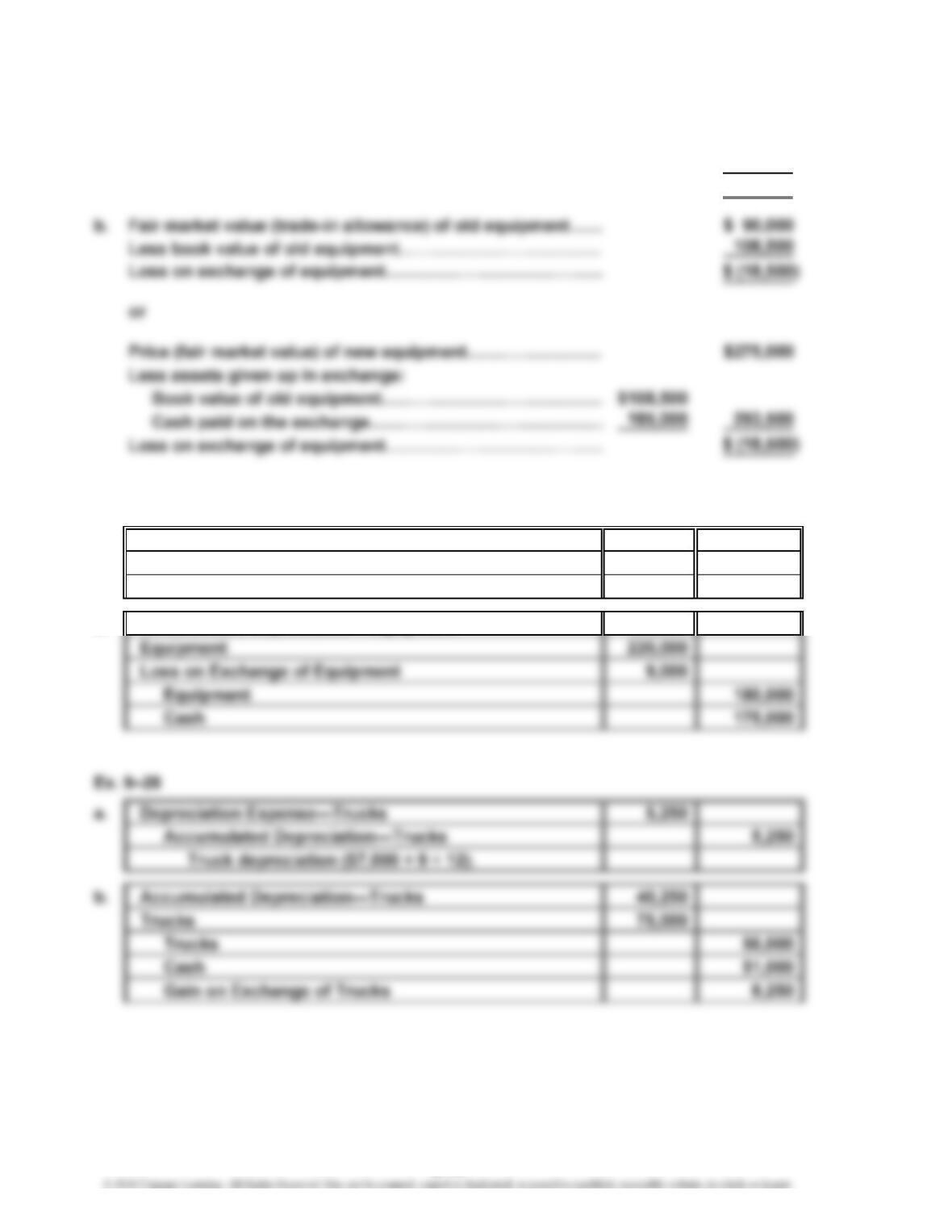

a. Price (fair market value) of new equipment……………………

…

$275,000

Trade-in allowance of old equipment…………………………… 90,000

Cash paid on the date of exchange……………………………

…

$185,000

a.

Revenue

Average Book Value of Fixed Assets

=Fixed Asset Turnover Ratio

9-13

CHAPTER 9 Fixed Assets and Intangible Assets

Ex. 9–26

a. Price (fair market value) of new equipment……………………

…

$275,000

Trade-in allowance of old equipment…………………………… 90,000

Cash paid on the date of exchange……………………………

…

$185,000

Ex. 9–27

a. Depreciation Expense—Equipment 6,000

Accumulated Depreciation—Equipment 6,000

Equipment depreciation ($12,000 × 6 ÷ 12).

b. Accumulated Depreciation—Equipment 126,000

9-14

CHAPTER 9 Fixed Assets and Intangible Assets

Prob. 9–1A

1. Land Other

Item Land Improvements Building Accounts

a. $ 2,500

b. 340,000

c. 15,500

n. 2,000

o. 2,500

p.* (7,500)

q. 800,000

* Receipt.

3. Because land used as a plant site does not lose its ability to provide services,

4. Because Land Improvements are depreciated, depreciation expense of $1,200

($12,000 × 1 ÷ 20 × 2) would be overstated, and net income would be understated

PROBLEMS

9-15

CHAPTER 9 Fixed Assets and Intangible Assets

Prob. 9–2A

1.

a. Straight- b. Units-of- c. Double-

Line Output Declining-Balance

Year Method Method Method

2014 $28,000 $37,380 $60,000

Calculations:

Straight-line method:

($90,000 – $6,000) ÷ 3 = $28,000 each year

Units-of-output method:

Double-declining-balance method:

2014: $90,000 × 2 ÷ 3 = $60,000

2. The double-declining-balance method yields the most depreciation expense in

2014 of $60,000.

3. Over the three-year life of the equipment, all three depreciation methods yield

Depreciation Expense

9-16

CHAPTER 9 Fixed Assets and Intangible Assets

Prob. 9–3A

a. Straight-line method:

2014: [($270,000 – $9,000) ÷ 3] × 9 ÷ 12…………………………………

…

$65,250

2015: ($270,000 – $9,000) ÷ 3………………………………………………

…

87,000

b. Units-of-output method:

2014: 7,500 hours × $14.50*………………………………………………

…

$108,750

c. Double-declining-balance method:

2014: $270,000 × 2 ÷ 3 × 9 ÷ 12…………...………………………………

…

$135,000