9-1

CHAPTER 9

Reporting and Analyzing Long-Lived Assets

Learning Objectives

1. Describe how the cost principle applies to plant assets.

2. Explain the concept of depreciation.

3. Compute periodic depreciation using the straight-line method, and contrast its

expense pattern with those of other methods.

9-2

Chapter Outline

Learning Objective 1 – Describe how the Cost Principle Applies to Plant

Assets

Plant Assets (also called property, plant, and equipment) are resources that have

physical substance (a definite size and shape), are used in the operations of a

business, and are not intended for sale to customers.

▪ It is important for companies to (1) keep assets in good operating condition, (2)

replace worn-out or outdated assets, and (3) expand its productive assets as

needed.

Determining The Cost of Plant Assts—The historical cost principle requires that

companies record plant assets at cost.

Land – Land is often used as a building site for a manufacturing plant or office. The

cost of land includes:

▪ The cash purchase price.

Land improvements – Land improvements are structural additions made to land

such as driveways, parking lots, fences, landscaping, and underground sprinklers.

▪ The cost of land improvements includes all expenditures necessary to make the

improvements ready for their intended use.

Buildings – Buildings are facilities used in operations, such as stores, offices,

factories, warehouses, and airplane hangars.

▪ All necessary expenditures relating to the purchase or construction of a building

are charged to the Buildings account.

9-3

▪ When a building is purchased, such costs include the purchase price, closing

costs (attorney’s fees, title insurance, etc.), and real estate broker’s

Equipment – Equipment includes assets used in operations, such as store check–

out counters, office furniture, factory machinery, delivery trucks, and airplanes.

▪ The cost of equipment consists of the cash purchase price, sales taxes, freight

charges, and insurance during transit paid by the purchaser, as well as

expenditures required in assembling, installing, and testing the unit.

▪ Two criteria apply in determining the cost of equipment:

(1) The frequency of the cost – one time or recurring

(2) The benefit period – the life of the asset or one year.

▪ To illustrate, assume that Lenard Company purchases a delivery truck at a cash

price of $22,000. Related expenditures are for sales taxes $1,320, painting and

lettering $500, motor vehicle license $80, and a three-year accident insurance

policy $1,600. The cost of the motor vehicle license is treated as an expense,

and the cost of an insurance policy is considered a prepaid asset. Thus the

entry to record the purchase of the truck and related expenditures is as follows:

Equipment ………………………………………………… 23,820

To Buy or Lease – An alternative to purchasing an asset is leasing. In a lease,

the owner of an asset (the lessor) allows another party (the lessee) to use the

asset for period of time at an agreed price.

▪ Some advantages of leasing an asset versus purchasing it are:

o reduced risk of obsolescence

9-4

TEACHING TIP

Ask students to name some companies with which they are familiar. Now ask them what

types of long-lived assets they would expect to see on the balance sheets of these companies.

Discuss the differences between operating and capital leases. Explain why certain leases

are capitalized for accounting purposes.

Learning Objective 2 – Explain the Concept of Depreciation

Accounting for Plant Assets—Depreciation is the process of allocating to expense

the cost of a plant asset over its useful (service) life in a rational and systemic manner.

▪ Such cost allocation is designed to properly match expenses with revenues.

▪ Depreciation affects the balance sheet through accumulated depreciation, which

▪ Depreciation applies to three classes of plant assets:

o Land improvements

o Buildings

o Equipment

▪ Land is not a depreciable asset.

▪ The revenue-producing ability of a depreciable asset declines during its useful life

TEACHING TIP

Reinforce the idea that depreciation is simply a systematic way of allocating the cost of the

asset over its life. Depreciation does not attempt to bring the asset to fair value. Think of

buildings that are very old and have been owned by an individual or a company for a long

time. The book value of these assets (cost less accumulated depreciation) is probably small.

The buildings have probably not depreciated at all. Rather, they have probably appreciated.

Factors In Computing Depreciation:

▪ Cost—Plant assets are recorded at cost, in accordance with the historical cost

principle.

9-5

TEACHING TIP

Explain that management is responsible for determining useful life and salvage, as well as

selecting the depreciation method. Discuss ways to estimate the useful life and salvage

value.

Learning Objective 3 – Compute Periodic Depreciation Using the Straight–

line. Method, and Contrast its Expense Pattern with

those of Other Methods

Depreciation Methods—Depreciation is generally computed using one of three

methods:

1. Straight-line

2. Declining-balance

3. Units-of-activity

▪ Each of these depreciation methods is acceptable under generally accepted

accounting principles.

▪ Once a method is chosen, it should be applied consistently over the useful life of

the asset.

▪ Management selects the method it believes best measures an asset’s

contribution to revenue over its useful life.

▪ Straight-line depreciation is the most widely used method. It is used for some or

all of the depreciation by more than 95% of U.S. companies.

expense using a constant rate applied to a declining book value.

▪ This method is called an accelerated depreciation method because it results

in more depreciation in the early years of an asset’s life and less depreciation in

the later years of an asset’s life than does the straight-line approach.

▪ The declining-balance approach can be applied at different rates, which result in

varying speeds of depreciation.

Units-Of-Activity— Under the units-of-activity method, the life of an asset is

expressed in terms of the total units of production or the use expected from the

asset.

9-6

▪ The units-of-activity method is suited to factory machinery and such items as

delivery equipment and airplanes.

▪ This method is generally not suitable for such assets as buildings or furniture

TEACHING TIP

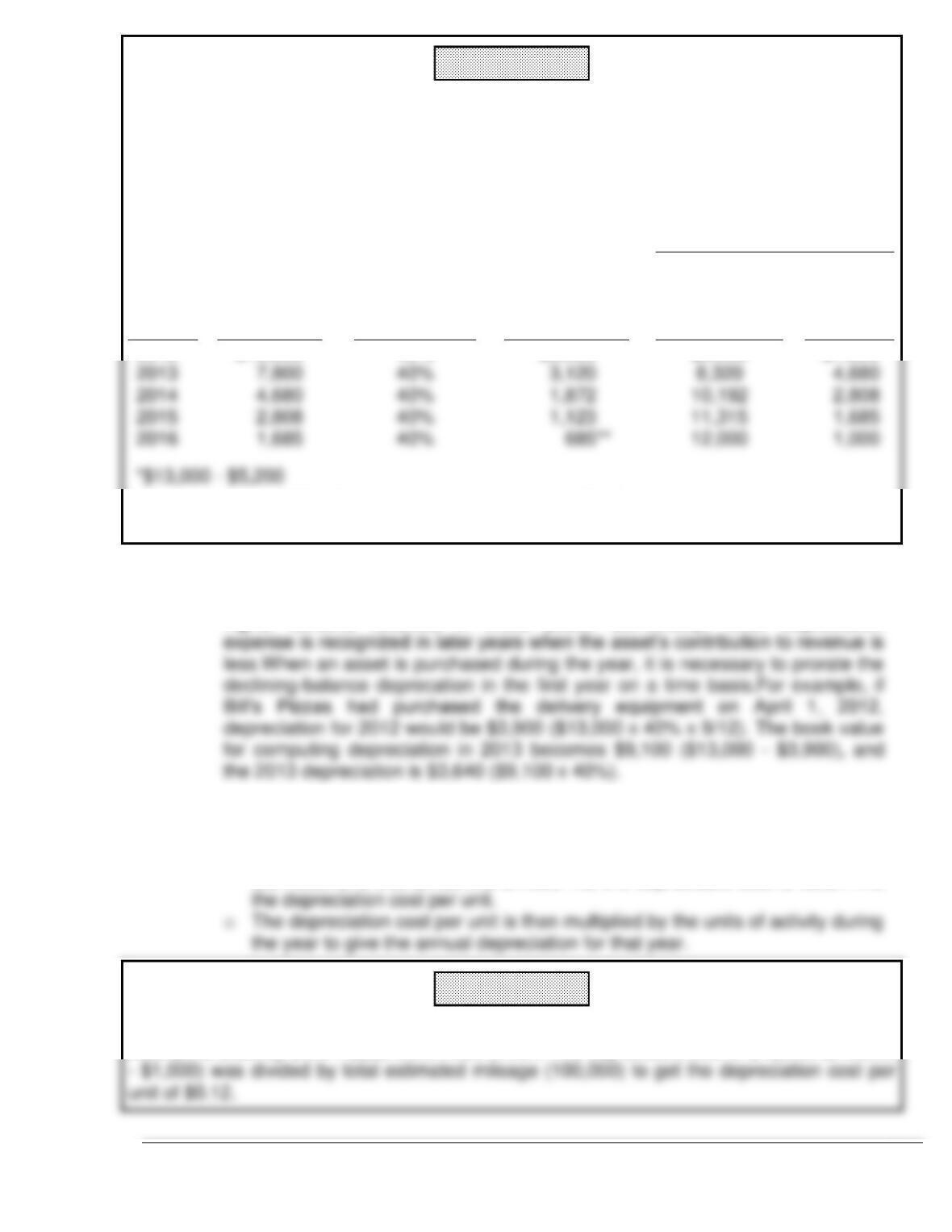

Using the example in the book of the small delivery truck purchased by Bill’s Pizzas on

January 1, 2012:

Cost $13,000

Expected salvage value $1,000

Computation of straight-line depreciation:

($13,000 – $1,000) 5 years = $2,400 per year

Rate: 100% 5 years = 20% per year

Depreciation Schedule Assuming Straight-Line Depreciation

Depreciable Value

Annual

Depreciation

End of Year

Accumulated

Book

Year

Cost

Rate

Expense

Depreciation

Value

2012

$12,000

20%

$2,400

$ 2,400

$10,600

9-7

TEACHING TIP

Go over the example in the book of the delivery truck purchased by Bill’s Pizzas on January 1,

2012, using the double-declining-balance method. The Appendix expands the example to

show that when using the declining-balance method, the salvage value is ignored in the

beginning. However, the asset cannot be depreciated below its salvage value.

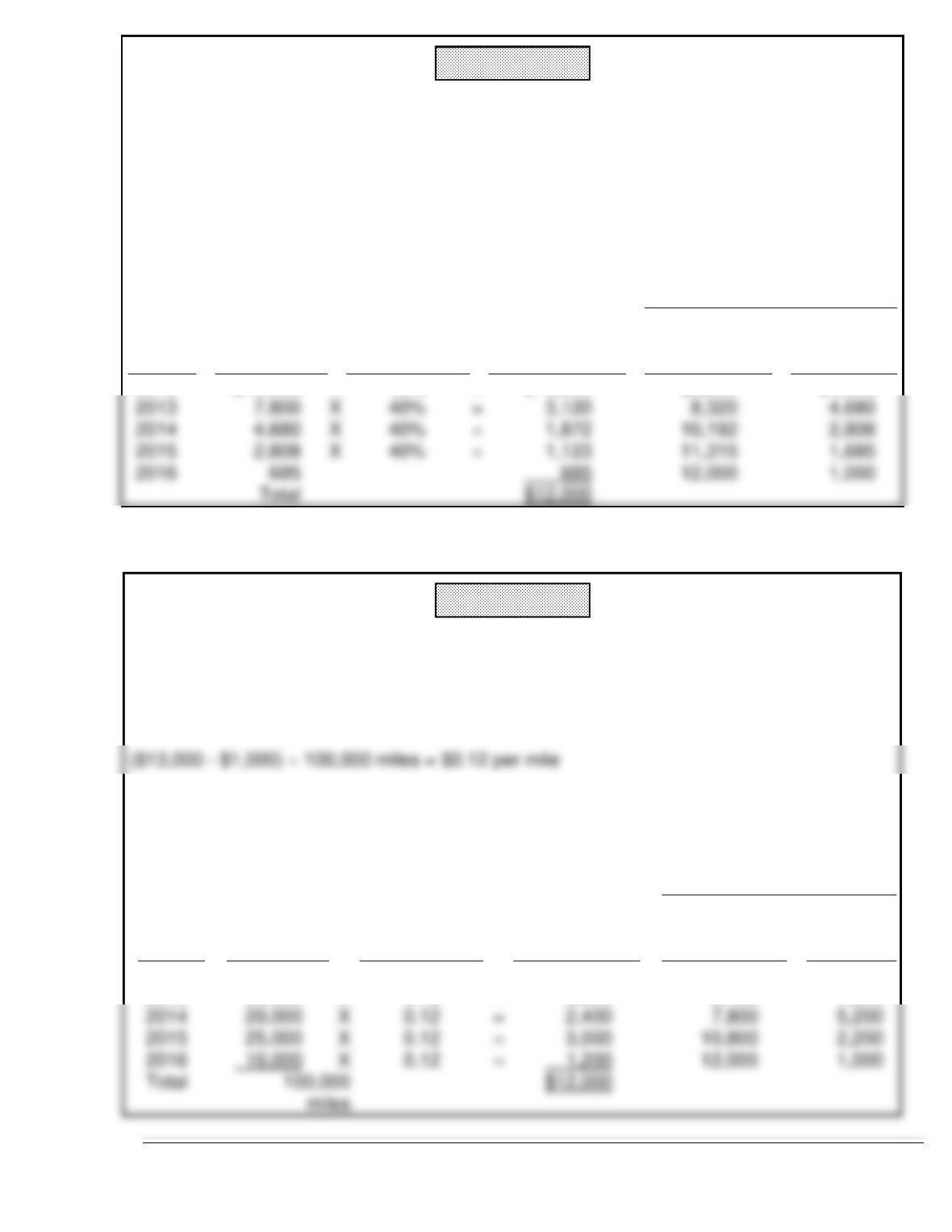

Depreciation Schedule Assuming Double-Declining-Balance Depreciation

Rate = 100% ÷ 5 years = 20%, 20% X 200% (DDB) = 40% per year

End of Year

Year

Book Value

Beginning

of Year

Depreciation

Rate

Annual

Depreciation

Expense

Accumulated

Depreciation

To Date

Book

Value

2012

$13,000

X

40%

=

$ 5,200

$5,200

$7,800

2013

X

40%

=

2014

X

40%

=

10,192

2015

X

40%

=

11,315

2016

685

12,000

TEACHING TIP

Computing depreciation under units–of-activity is the much the same as straight line. The

only difference is that the life is expressed in terms of activity rather than years. Activity may

be measured in units produced, miles driven, or hours flown, depending on the asset.

Returning to the example of Bill’s delivery truck the units-of-activity depreciation would be

computed as follows:

Depreciation Schedule Assuming Units-of-Activity Depreciation

End of Year

Year

Units of

Activity

(Miles)

Depreciation

Rate

Annual

Depreciation

Expense

Accumulated

Depreciation

Book

Value

2012

15,000

X

$0.12

=

$ 1,800

$ 1,800

$11,200

2013

30,000

X

0.12

=

3,600

5,400

7,600

2014

20,000

X

0.12

=

2,400

7,800

5,200

2015

25,000

X

0.12

=

3,000

2,200

X

0.12

=

1,000

9-8

TEACHING TIP

Students need to have a good understanding of the effect different methods of depreciation

have on the Income Statement and the Balance Sheet.

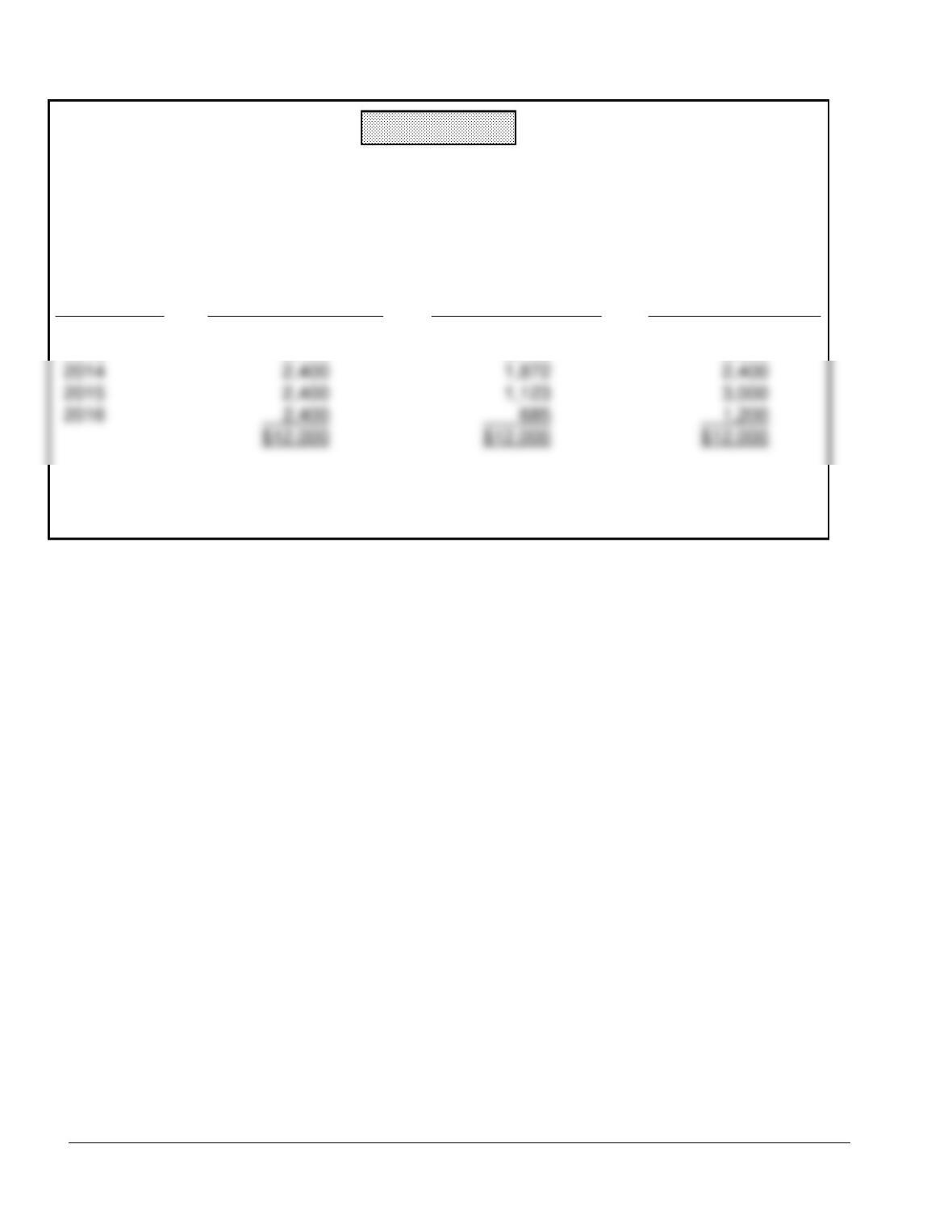

Comparison of Depreciation Expense with Three Methods of Depreciation

Year

Straight-Line

Double-Declining

Balance

Units-of-Activity

2012

$ 2,400

$ 5,200

$1,800

2013

2,400

3,120

3,600

2014

2,400

1,872

2,400

2015

2,400

1,123

3,000

2016

Note that total depreciation is the same for the five-year period. The depreciable cost has

been expensed over the useful life or the estimated activity.

9-9

Depreciation and Income Taxes—The internal Revenue Service (IRS) allows

corporate taxpayers to deduct depreciation expense when computing taxable income.

▪ The IRS does not require the taxpayer to use the same depreciation method on the

tax return that is used in preparing financial statements.

Depreciation Disclosure in the Notes—The choice of depreciation method must be

disclosed in a company’s financial statements or in related notes that accompany the

statements.

TEACHING TIP

Ask students which depreciation method they would use if they were trying to minimize

income taxes. Which method would they choose if they wanted to maximize net income?

Suppose they wanted to do both?

Learning Objective 4 – Describe the Procedure for Revising Periodic

Depreciation

Revising Periodic Depreciation—Management should periodically review annual

depreciation expense. If wear and tear or obsolescence indicates that annual

depreciation is either inadequate or excessive, the company should change the

depreciation expense amount.

▪ When a change in an estimate is required, the change is made in current and

future years but not to prior periods. Thus, when a change is made (1) there is

no correction of previously recorded depreciation expense, and (2) depreciation

Expenditures During Useful Life—During the useful life of a plant asset, a

company may incur costs for ordinary repairs, additions, and improvements.

▪ Ordinary repairs are expenditures to maintain the operating efficiency and

expected productive life of the asset.

o Ordinary repairs are usually fairly small amounts that occur frequently

throughout the service life.

9-10

o They are usually material in amount.

o Occur infrequently during the period of ownership.

• Additions and improvements are debited to the plant asset affected and

generally increase the company’s investment in productive facilities.

• Additions and improvements are capital expenditures.

TEACHING TIP

Provide students with examples of additions and improvements. The installation of air

conditioning in a delivery van that did not have air conditioning previously is a good example

Impairment—is a permanent decline in the fair value of an asset.

▪ In order that the asset is not overstated on the books, it is written down to its new

fair value during the year in which the decline in value occurs.

▪ In the past some companies delayed recording losses on impairments until a year

Learning Objective 5 – Explain How to Account for the Disposal of Plant Assets

Plant Asset Disposals—Companies dispose of plant assets that are no longer

useful to them. There are three ways in which companies make plant asset

disposals:

1. Sale

2. Retirement

3. Exchange.

▪ Whether a plant asset is sold, retired or exchanged, the company must

determine the book value of the plant asset at the time of disposal to

determine the gain or loss.

▪ Recall that book value is the difference between the cost of the plant asset and

Sale of Plant Assets—In the sale of an asset, the book value of the asset is

compared with the proceeds received from the sale. If the proceeds exceed the book

value a gain on disposal occurs. Conversely, if proceeds from the sale are less than

the book value a loss on disposal occurs.

9-11

Gain On Sale—To illustrate a gain on sale of plant assets, assume that on July 1,

2010, Wright Company sells office furniture for $16,000 cash. The office furniture

originally cost $60,000 and as of January 1, 2012, had accumulated depreciation of

$41,000. Depreciation for the first six months of 2012 is $8,000. Then entries to

record depreciation expense and update accumulated depreciation to July 1 and to

record the sale and the gain on sale is are as follows:

July 1 Depreciation Expense ……………………………………… 8,000

Accumulated Depreciation—Equipment ……. 8,000

Loss on Sale—Assume that the office furniture was sold for $9,000. There will be a

loss of $2,000. To record the loss on the sale is as follows:

July 1 Cash …………………………………………………………….. 9,000

Accumulated Depreciation—Equipment …………….. 49,000

Loss on Disposal ……………………………………………. 2,000

9-12

Learning Objective 6 – Describe Methods for Evaluating the Use of Plant

Assets

Analyzing Plant Assets—The presentation of financial information about plant assets

enables decision makers to analyze the company’s use of its plant assets. Two

measures to analyze plant assets are:

▪ Return on assets ratio – an overall measure of profitability. This ratio is computed

▪ Asset turnover ratio – indicates how efficiently a company uses its assets to

generate sales—that is, how many dollars of sales are generated by each dollar

▪ Profit Margin Revisited – As was discussed in Chapter 5 the profit margin ratio is

calculated by dividing net income by net sales.

o It tells how effective a company is in turning its sales into income—that

Profit Margin x Asset Turnover = Return on Assets

Where:

o Profit Margin = Net Income Net Sales

This relationship has important strategic implications for management.

If a company wants to increase its return on assets, it can do so in two ways:

TEACHING TIP

With most businesses there is a trade-off between margin and turnover. If a business has a

high margin, turnover will be low, and vice-versa. Give examples of businesses in your area

one of which has a high margin and low turnover, and another with a high turnover and low

margin.

Learning Objective 7 – Identify the Basic Issues Related to Reporting

Intangible Assets

9-13

Intangible Assets—are rights, privileges, and competitive advantages that result from

ownership of long-lived assets that do not possess physical substance. Well known

intangibles are the patents of Microsoft, the franchises of McDonald’s, the trade name

iPod and Nike’s trademark “swoosh.”

▪ Intangibles may be evidenced by contracts, licenses, and other documents.

▪ Intangibles may arise from the following sources:

o Government grants.

Accounting For Intangible Assets—Intangible assets are recorded at cost.

Intangibles are categorized as having either a limited life or an indefinite life.

▪ The cost of intangible assets with indefinite lives should not be amortized.

▪ If an intangible has a limited life, its cost should be allocated over its useful life

using a process similar to depreciation.

▪ The process of allocating to expense the cost of intangibles is referred to as

amortization.

o To record amortization of an intangible asset, Amortization Expense is

increased (debited), and the specific intangible asset is decreased

Types of intangible assets:

▪ Patent – an exclusive right issued by the U.S. Patent Office that enables the

recipient to manufacture, sell, or otherwise control an invention for a period

of 20 years from the date of the grant.

o The initial cost of a patent is the cash or cash equivalent price paid

▪ Research and development costs are expenditures that may lead to

9-14

TEACHING TIP

Discuss the fact that some accountants argue that expensing R & D costs leads to

understated assets and net income. On the other side, some accountants argue that

capitalizing these costs would lead to highly speculative assets on the balance sheet.

▪ Copyrights are granted by the federal government and give the owner the

exclusive right to reproduce and sell an artistic or published work.

TEACHING TIP

Sometimes the acquisition of a copyright can be very expensive. Michael Jackson paid

millions of dollars for the copyrights to the Beatles music. However, the cost of a copyright

for a created work may be only the $10 fee paid to the U.S. Copyright Office.

▪ A trademark or trade name is a word, phrase, jingle, or symbol that distinguishes

or identifies a particular enterprise or product. Trade names like Wheaties,

Monopoly, Sunkist, Kleenex, Coca-Cola, Big Mac, and Jeep create immediate

product identification and generally enhance the sale of the product.

o The creator or original user may obtain exclusive legal right to the

trademark or trade name by registering it with the U.S. Patent Office. The

▪ Franchises and Licenses – A franchise is a contractual agreement under which

the franchiser grants the franchisee the right to sell certain products, to provide

specific services, or to use certain trademarks or trade names, usually within a

designated geographic area. Another type of franchise, granted by a government

9-15

TEACHING TIP

Ask students to identify well-known franchises. If starting a new business would you consider

a franchise arrangement? What are the advantages and disadvantages of franchises?

▪ Goodwill represents the value of all favorable attributes that relate to a company,

including exceptional management, desirable location, good customer relations, skilled

employees, etc. Goodwill is unique: Unlike other assets such as investments, plant

assets and even other intangibles, which can be sold individually in the marketplace,

goodwill can be identified only with the business as a whole.Goodwill is recorded only

TEACHING TIP

Think of businesses in your area that have goodwill. Do you patronize a dry cleaner or drugs

store that you particularly like and would not think of leaving? What is it about this business

that makes it special?

Learning Objective 8 – Indicate how Long-lived Assets are Reported in the

Financial Statements

Financial Statement Presentation of Long-Lived Assets—Plant assets are shown

in the financial statements under “Property, plant, and equipment” and intangibles are

shown separately under “Intangible assets.”

▪ Intangibles do not usually use a contra asset account like the contra asset account

Accumulated Depreciation used for plant assets. Instead, amortization of these

Keeping An Eye On Cash—It is also interesting to examine the statement of cash

flows to determine the amount of property, plant, and equipment purchased and the

9-16

TEACHING TIP

Students may not understand why a fully depreciated asset remains on the balance sheet.

Assume a company is using equipment that is fully depreciated. If the equipment were not

listed on the balance sheet, the financial statement user would not fully understand the

Learning Objective 9 – Appendix – Compute Periodic Depreciation Using the

Declining-Balance Method and the Units-of-Activity

Method

Calculation of Depreciation Using Other Methods—In this appendix the

calculations for the depreciation expense amounts that were used in the chapter are

discussed.

▪ Declining-Balance—The declining-balance method produces a decreasing

annual depreciation expense over the useful life of the asset.

o The method is so named because the computation of periodic depreciation is

based on a declining book value (cost less accumulated depreciation) of the

asset.

9-17

TEACHING TIP

Expand the example in the book of the delivery truck purchased by Bill’s Pizzas using the

double-declining-balance method.

Depreciation Schedule Assuming Double-Declining-Balance Depreciation

Rate = 100% ÷ 5 years = 20% X 200% DDB = 40% period rate

End of Year

Year

Book

Value

Beginning

of Year

X

Depreciation

Rate

=

Annual

Depreciation

Expense

Accumulated

Depreciation

Book

Value

2012

$13,000

40%

$5,200

$5,200

$7,800*

2013

40%

2014

40%

10,192

2015

40%

11,315

2016

40%

12,000

**Computation of $674 ($1,685 x 40%) is adjusted to $685 in order for book value to equal

salvage value.

o The declining-balance method is compatible with the expense recognition

principle. The higher depreciation expense in earlier years is matched with the

higher benefits received in these years. Conversely, lower depreciation

▪ Units-Of-Activity—Under the units-of-activity method, useful life is expressed in

terms of the total units of production or use expected from the asset.

o To use this method, the total units of activity for the entire useful life are

estimated and that amount is divided into the depreciable cost to determine

TEACHING TIP

Remind students of the example earlier in the chapter. The units of activity for the delivery

truck purchased by Bill’s Pizzas were miles driven. The depreciable cost of $12,000 ($13,000