CHAPTER 9

Reporting and Analyzing Long-Lived Assets

Learning Objectives

1. Describe how the historical cost principle applies to plant assets.

2. Explain the concept of depreciation.

3. Compute periodic depreciation using the straight-line method, and contrast its

expense pattern with those of other methods.

4. Describe the procedure for revising periodic depreciation.

5. Explain how to account for the disposal of plant assets.

6. Describe methods for evaluating the use of plant assets.

7. Identify the basic issues related to reporting intangible assets.

8. Indicate how long-lived assets are reported in the financial statements.

*9. Compute periodic depreciation using the declining-balance method and the units-

of-activity method.

Summary of Questions by Learning Objectives and Bloom’s Taxonomy

Item LO BT Item LO BT Item LO BT Item LO BT Item LO BT

Questions

1. 1 C 7. 3 C 13. 8 K 18. 7 C 23. 6 C

Brief Exercises

1. 1 AP 4. 3 AN 7. 5 AP 10. 7 AP 13. 9* AP

Do It! Review Exercises

Exercises

1. 1 C 5. 3 AP 9. 1, 2,

13. 7 AN 17. 8 AN

Problems: Set A

1. 1 C 3. 5 AP 5. 7 AP 7. 3, 9* AP 8. 3, 9* AP

Problems: Set B

1. 1 C 3. 5 AP 5. 7 AP 7. 3, 9* AP 8. 3, 9* AP

*Continuing Cookie Solutions for this chapter are available online.

ASSIGNMENT CLASSIFICATION TABLE

Problem

Number

Description

Difficulty

Level

Time

Allotted (min.)

1A Determine acquisition costs of land and building. Simple 20–30

2A Journalize equipment transactions related to purchase,

sale, retirement, and depreciation.

Moderate 40–50

1B Determine acquisition costs of land and building. Simple 20–30

2B Journalize equipment transactions related to purchase,

sale, retirement, and depreciation.

Moderate 40–50

3B Journalize entries for disposal of plant assets. Simple 20–30

4B Prepare entries to record transactions related to

acquisition and amortization of intangibles; prepare the

intangible assets section and note.

Moderate 30–40

ANSWERS TO QUESTIONS

1. For plant assets, the historical cost principle states that plant assets are recorded at cost, which

consists of all expenditures necessary to acquire the asset and make it ready for its intended

use.

2. In a cash transaction, cost is equal to the cash paid.

In a noncash transaction, cost is equal to the cash equivalent price paid, which is the fair value of

the asset given up or the fair value of the asset received, whichever is more clearly determinable.

5. You should explain to the president that depreciation is a process of allocating the cost of a plant

asset to expense over its service (useful) life in a rational and systematic manner. Recognition of

depreciation is not intended to result in the accumulation of cash for replacement of the asset.

6. (a) Salvage value is the expected cash value of the asset at the end of its useful life.

(b) Salvage value is used in determining depreciable cost in the straight-line method by subtracting

it from the plant asset’s cost.

Questions Chapter 9 (Continued)

11. In a sale of plant assets, the book value of the asset is compared to the proceeds received from

the sale. If the proceeds of the sale exceed the book value of the plant asset, a gain on disposal

occurs. If the proceeds of the sale are less than the book value of the plant asset sold, a loss on

disposal occurs.

12. The plant asset and related accumulated depreciation should continue to be reported on the

balance sheet without further depreciation or adjustment until the asset is retired. Reporting

the asset and related accumulated depreciation on the balance sheet informs the reader of the

16. The intern is not correct. If an intangible asset has a limited life, the cost of the asset should be

amortized over that asset’s useful life (the period of time when operations are benefited by use of

the asset) or its legal life, whichever is shorter. The cost of intangible assets with indefinite lives

should not be amortized.

17. The favorable attributes which could result in goodwill include exceptional management, desirable

location, good customer relations, skilled employees, high quality products, fair pricing policies, and

harmonious relations with labor unions.

Questions Chapter 9 (Continued)

20. Research and development costs present several accounting problems. It is sometimes difficult

to assign the costs to specific projects, and there are uncertainties in identifying the extent and

timing of future benefits. As a result, research and development costs are usually recorded as an

expense when incurred.

21. Campbell Soup Company’s return on assets is computed as follows:

22. The return on assets is closely monitored by management. It is the product of the profit margin

and the asset turnover. At first glance, if this new product line has a lower profit margin, then it

will reduce the company’s asset turnover. However, it is likely that it will have a higher turnover

23. (a) Grocery stores usually have a high asset turnover and a low profit margin.

24. Since Gooden uses the straight-line depreciation method, its depreciation expense will be lower

in the early years of an asset’s useful life as compared to using an accelerated method. Perron’s

depreciation expense in the early years of an asset’s useful life will be higher as compared to the

straight-line method. Gooden’s net income will be higher than Perron’s in the first few years of

the asset’s useful life.

25. Yes, the tax regulations of the IRS allow a company to use a different depreciation method on the

tax return than is used in preparing financial statements. Garcia Corporation uses an accelerated

SOLUTIONS TO BRIEF EXERCISES

BRIEF EXERCISE 9-1

BRIEF EXERCISE 9-2

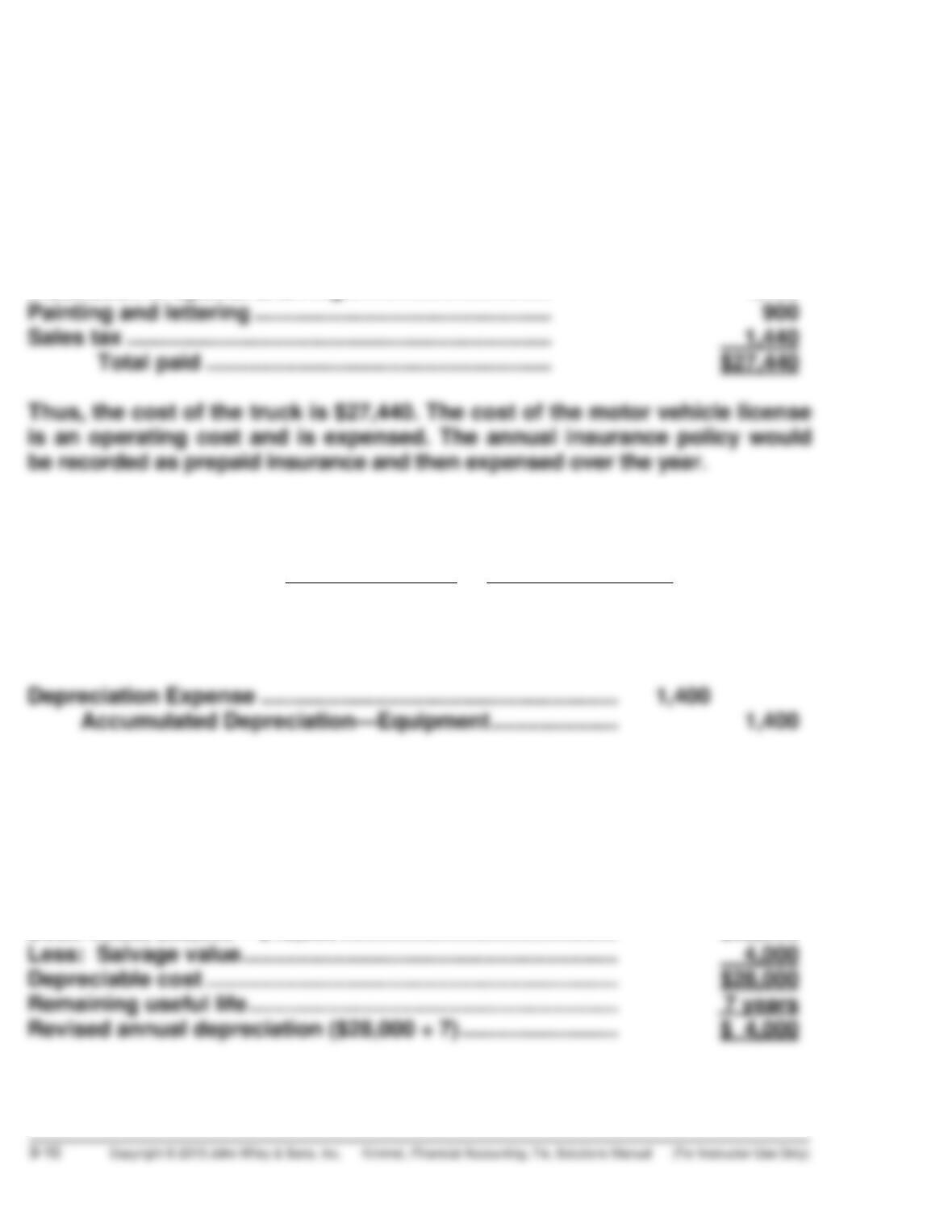

The cost of the truck is $26,780 (cash price $24,000 + sales taxes $1,080 +

BRIEF EXERCISE 9-3

The depreciable cost is $27,000 ($31,000 – $4,000). With a 4-year useful life,

BRIEF EXERCISE 9-4

It is likely that management requested this accounting treatment to boost

BRIEF EXERCISE 9-5

Book value, 1/1/14 ($36,000 – $13,600) ……………………………………. $22,400

BRIEF EXERCISE 9-6

(a) Maintenance and Repairs Expense ……………………. 38

Cash …………………………………………………………… 38

BRIEF EXERCISE 9-7

(a) Accumulated Depreciation—Equipment ……………. 41,000

Equipment …………………………………………………… 41,000

(b) Accumulated Depreciation—Equipment ……………. 37,200

Loss on Disposal of Plant Assets ……………………… 3,800

Equipment…………………………………………………… 41,000

Cost of delivery equipment $41,000

BRIEF EXERCISE 9-8

(a) 7/31/14 Depreciation Expense …………………………. 4,600

Accumulated Depreciation—

BRIEF EXERCISE 9-9

BRIEF EXERCISE 9-10

(a) Amortization Expense ($156,000 ÷ 6) ………………… 26,000

Patent ……………………………………………………….. 26,000

BRIEF EXERCISE 9-11

NIKE, INC.

Partial Balance Sheet

As of May 31, 2014

(in millions)

Property, plant, and equipment

Land ……………………………………………….. $ 221.6

Buildings ………………………………………… $ 974.0

Machinery and equipment ……………….. 2,094.3

*Alternatively, many companies would simply show a single line for net

intangibles.

BRIEF EXERCISE 9-12

In the determination of net cash provided by operating activities, add

depreciation expense and amortization expense to net income:

*BRIEF EXERCISE 9-13

The declining-balance rate is 50% (1/4 X 2) and this rate is applied to the

book value at the beginning of the year. The computations are:

Book Value X Rate = Depreciation

*BRIEF EXERCISE 9-14

The depreciation cost per unit is 18 cents per mile computed as follows:

Depreciable cost ($27,500 – $500) ÷ 150,000 = $.18

SOLUTIONS TO DO IT! REVIEW EXERCISES

DO IT! 9-1

The following four items are expenditures necessary to acquire the truck

and get it ready for use:

Negotiated purchase price ………………………………….. $24,000

Installation of special shelving ……………………………. 1,100

DO IT! 9-2

Depreciation expense = Cost

–

Salvage =$15,000

–

$1,000 = $1,400

Useful life 10 years

The entry to record the first year’s depreciation would be:

DO IT! 9-3

Original depreciation expense = ($50,000 – $2,000) ÷ 8 years = $6,000

Accumulated depreciation after three years = 3 X $6,000 = $18,000

Book value, $50,000 – $18,000 ………………………………………. $32,000

DO IT! 9-4

(a) Sale of machine for cash at a gain:

Accumulated Depreciation—Equipment ……………….. 28,000

Cash ……………………………………………………………………. 25,000

(b) Sale of machine for cash at a loss:

Accumulated Depreciation—Equipment ……………….. 28,000

DO IT! 9-5

1. Intangible assets

SOLUTIONS TO EXERCISES

EXERCISE 9-1

(a) The following points explain the application of the historical cost

principle to plant assets.

1. Under the historical cost principle, the acquisition cost for a plant

asset includes all expenditures necessary to acquire the asset

(b) 1. Land 5. Equipment

EXERCISE 9-2

1. Equipment

2. Equipment

EXERCISE 9-3

(a) Cost of land

Cash paid …………………………………………………………. $80,000

Net cost of removing warehouse ($8,200 – $1,700) … 6,500

(b) The architect’s fee ($9,100) should be debited to the building account.

The cost of the driveways and parking lot ($14,000) should be debited to

Land Improvements.

EXERCISE 9-4

1. False. Depreciation is a process of cost allocation, not asset valuation.

EXERCISE 9-5

Straight-line method:

$90,000 – $8,000

8

⎛

⎝

⎜

⎞

⎠

⎟=$10,250 per year.

EXERCISE 9-6

(a) Type of Asset

Building Warehouse

Cost ………………………………………………… $700,000 $120,000

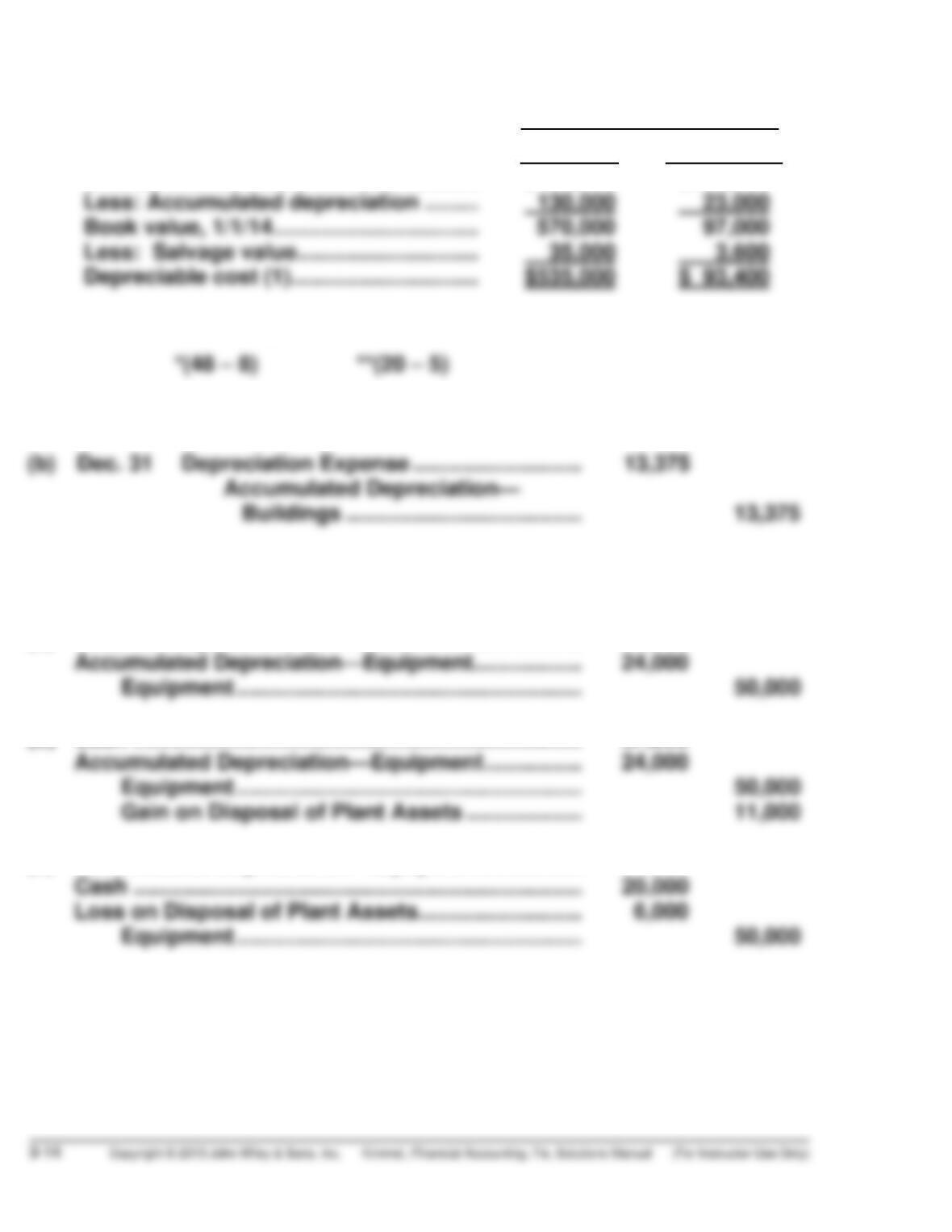

Revised remaining useful life in years (2) 40* 15**

Revised annual depreciation (1) ÷ (2) $13,375 $6,227

EXERCISE 9-7

(a) Loss on Disposal of Plant Assets ……………………… 26,000

(b) Cash ……………………………………………………………….. 37,000

(c) Accumulated Depreciation—Equipment ……………. 24,000

EXERCISE 9-8

Jan. 1 Accumulated Depreciation—Equipment ……….. 62,000

Equipment ……………………………………………… 62,000

June 30 Depreciation Expense ………………………………….. 6,000

Accumulated Depreciation—Equipment

Dec. 31 Depreciation Expense ………………………………….. 4,200

Accumulated Depreciation—Equipment

[($25,000 – $4,000) X 1/5] ……………………… 4,200

31 Accumulated Depreciation—Equipment

EXERCISE 9-9

1. Depreciation is the process of allocating the cost of a long-lived asset

to expense over the asset’s useful life. Because the value of land generally

2. Goodwill is an intangible asset with an indefinite life. According to

generally accepted accounting principles, goodwill is not amortized but

EXERCISE 9-9 (Continued)

3. This is a violation of the historical cost principle. Because current

market values are subjective and not reliable, they are not used to

increase the recorded value of an asset after acquisition. The

appropriate accounting treatment is to leave the building on the books

at its zero book value.

EXERCISE 9-10

EXERCISE 9-11

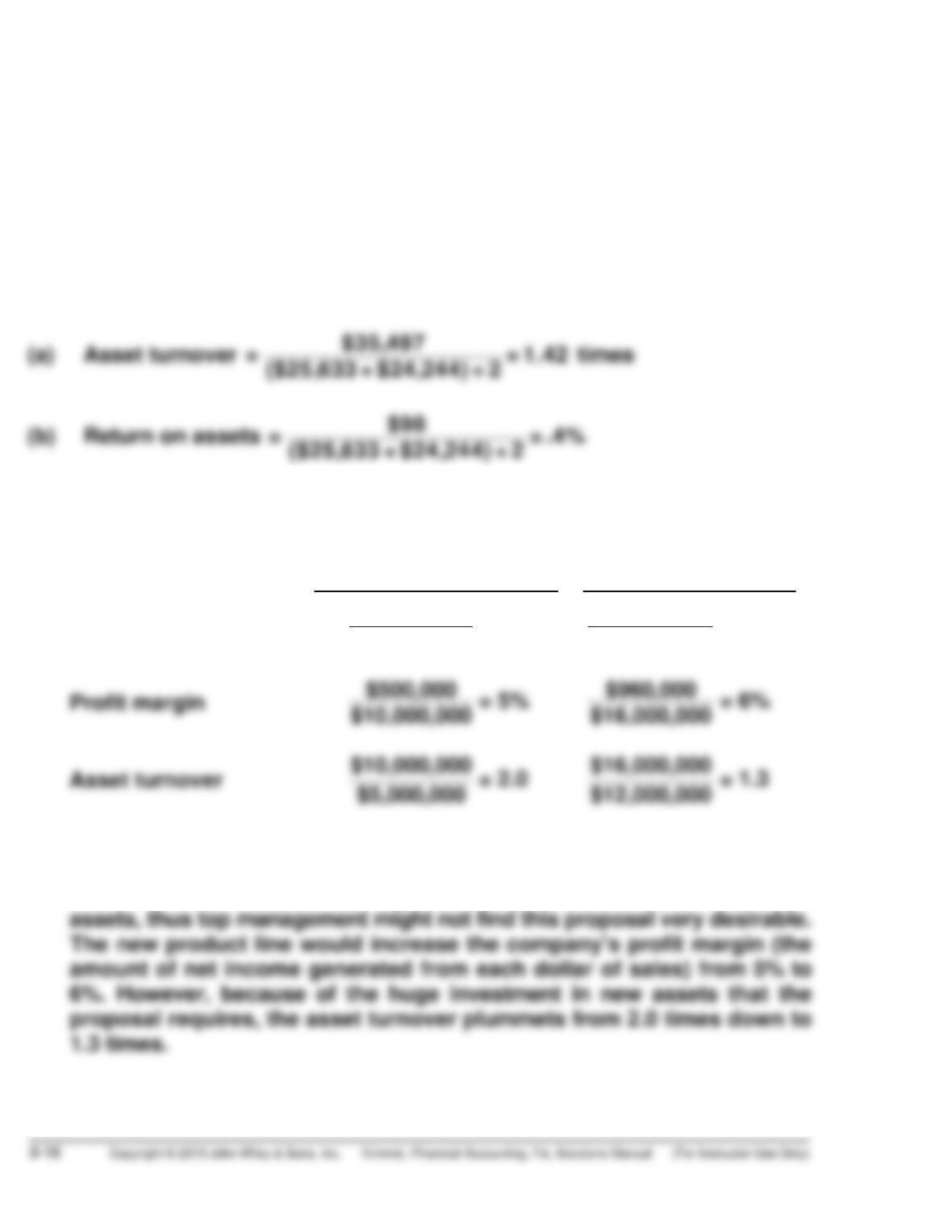

(a) Without new products With new products

Return on assets $500,000 = 10% $960,000 = 8%

$5,000,000 $12,000,000

(b) The return on assets declined from 10% to 8%. This means that the

company is not generating as much income from each dollar invested

in assets. It is common for companies to try to maximize their return on

EXERCISE 9-12

(a) ($ in millions)

(c) Asset turnover and profit margin vary considerably across industries.

Therefore, when you have a diverse group of businesses from several

EXERCISE 9-13

Dec. 31 Amortization Expense ……………………………….. 20,000

Copyright ($120,000 X 1/6) …………………… 20,000

EXERCISE 9-14

(a) 1/2/14 Patent ………………………………………………… 280,000

Cash ……………………………………………. 280,000

7/1/14 Franchise …………………………………………… 540,000

Cash ……………………………………………. 540,000

(c) Ending balances, 12/31/14:

EXERCISE 9-15

Alliance Atlantis Communications Inc.’s change of accounting policy to

amortize broadcast rights will probably increase its reported income. Prior

to the change, Alliance Atlantis had amortized broadcast rights over a maxi-

EXERCISE 9-16

(a) A company should depreciate its buildings because depreciation is

necessary in order to allocate the cost of the buildings to the periods

(b) A building can have a zero book value if it has no salvage value and it

is fully depreciated—that is, if it has been used for a period at least as

(c) Examples of intangibles that might be found on a college campus are

(d) Typical company or product trade names are:

Clothes—Gap, Gitano, Dockers, Calvin Klein, Chaus, Guess.

Trade names and trademarks are reported on a balance sheet if there is

a cost attached to them. If the trade name or trademark is purchased,

EXERCISE 9-17

Calculation of net cash provided by operating activities:

10-year 15-year

Net income $ 58,000 $102,000

The CEO is correct regarding the impact on net income. By increasing the

expected useful life depreciation, expense would be lowered and net income

would increase. However, this move would be appropriate only if, in fact, a

*EXERCISE 9-18

(a) Depreciation cost per unit is $.575 per mile [($100,000 – $8,000) ÷

160,000].

(b) Computation End of Year

Annual

Units of Depreciation Depreciation Accumulated Book

Years Activity X Cost/Unit = Expense Depreciation Value

2014 40,000 $.575 $23,000 $23,000 $77,000