9

Activity-Based Costing

Solutions to Review Questions

9-1.

9-2.

The term “death spiral” refers to a process that begins by attempting to increase prices

9-3.

False. Department allocation is a two-stage process, so the first-stage assignment of

differ. This can affect the decisions managers make regarding individual products.

9-4.

Most companies produce multiple products and simply adding them up does not

9-5.

The costs include the systems and the software, but the most important cost is

managers’ time. Managers need to make many decisions about the activities and the

9-6.

1. Identify activities that consume resources.

2. Identify the cost driver associated with each activity.

9-7.

9-8.

9-9.

Activity-based costing will benefit most companies with high overhead costs and diverse

9-10.

A personnel department provides its services by completing a set of activities using

9-11.

9-12.

9-13.

Solutions to Critical Analysis and Discussion Questions

9-14.

9-15.

Activity-based costing does not change the process for direct costs, so the statement is

9-16.

Disagree. The services in a business school, as in any service business, require

9-17.

False. Activity-based costing is most useful when the first-stage allocation is to

9-18.

There is no rule that the price charged for a product has to exceed its cost. There may

9-19.

Activity-based costing is like any other information system; it has its benefits and its

9-20.

False. The lesson learned from activity-based costing is that costs are a function not

9-21.

False. Activity-based costing breaks down the costs into cost pools according to the

9-22.

9-23.

Without information on the use of overhead resources by products, it is difficult for

9-24.

when managers use product cost data to make decisions at the product level.

9-25.

Answers will vary based on the degrees offered and the nature of the school. Some

9-26.

Answers will vary. The function selected will determine the activities, but some

9-27.

Answers will vary. Elements of the system that suggest it is an ABC system include cost

9-28.

Although it appears that a time-driven activity-based cost system lacks a cost hierarchy,

Solutions to Exercises

9-29. (15 min.) Reported Costs and Decisions: McNulty, Inc.

Chairs

Desks

Total

a.

Sales revenue …………………………………………….

$1,150,000

$2,105,000

$3,255,000

Direct material …………………………………………….

Direct labor ………………………………………………..

b

Product cost ………………………………………………

$1,000,000

$1,684,000

$2,684,000

b. After dropping chairs, the profit margin on desks falls below 20 percent.

Desks

Total

Sales revenue …………………………………………….

$2,105,000

$2,105,000

Direct Labor ……………………………………………….

Direct materials …………………………………………..

Overhead …………………………………………………..

a

Product cost

$1,790,000

$1,790,000

Margin ……………………………………………………….

9-30. (15 min.) Reported Costs and Decisions: Kima Company.

Standard

Galaxy

Total

a.

Sales revenue …………………………………………….

$6,000,000

$2,700,000

$8,700,000

2,400,000

1,600,000

b

b. After dropping the standard model, the profit on the Galaxy model (and for the

company) becomes negative.

Total

Direct Labor ……………………………………………….

2,250,000

Product cost

$3,030,000

$3,030,000

9-31. (30 min.) Plantwide versus Department Allocation: Munoz Sporting

Equipment.

Baseball

Bats

Tennis

rackets

a.

Sales revenue …………………………………………….

$2,700,000

$1,800,000

Direct Labor ……………………………………………….

500,000

250,000

Direct Materials …………………………………………..

550,000

Overhead …………………………………………………..

a

b

b. Maria was wrong; Baseball bats were more profitable.

Baseball

Bats

Tennis

rackets

Sales revenue …………………………………………….

$2,700,000

$1,800,000

Direct Labor ……………………………………………….

Direct Materials …………………………………………..

550,000

Overhead …………………………………………………..

750,000

a

750,000

b

c. The plantwide allocation method allocates overhead at 200% of direct labor for both

9-32. (35 min.) Plantwide versus Department Allocation: Main Street Ice Cream

Company.

Strawberry

Vanilla

Chocolate

a.

Direct Labor (per 1,000 gallons) ……………………

$750

$825

$1,125

Raw Materials (per 1,000 gallons) …………………

800

500

600

c.

Strawberry

Vanilla

Chocolate

Direct Labor (per 1,000 gallons) ……………………

$750

$825

$1,125

Overhead …………………………………………………..

d. Charlene was correct in her belief that she was being allocated some of Department

9-33. (30 min.) Unitwide versus Department Allocation: Hernandez Bros.

a.

b.

Miami

New York

Employees …………………………………………………

1,900

600

Rate per employee ………………………………………

Allocated cost ……………………………………………..

Transitions …………………………………………………

Rate per transition ……………………………………….

Allocated cost …………………………………………….. $

Total allocated cost …………………………………….. $

Miami

New York

Employees …………………………………………………

1,900

600

Rate per employee ……………………………………..

$300

Allocated cost …………………………………………….

9-34. (30 min.) Unit wide versus Department Allocation: Hernandez Bros.

a. First, note that the total to be allocated is $750,000 (= $570,000 + $180,000 in the

New York

Employees …………………………………………………

600

Rate per employee ……………………………………..

Allocated cost …………………………………………….

Transitions …………………………………………………

Rate per transition ………………………………………

Allocated cost ……………………………………………. $

Total allocated cost …………………………………….. $

9-35. (30 min.) Activity-Based Costing: Joplin Industries.

a.

J25P

J40X

Direct material ……………………………………………………..

$1,500,000

$2,400,000

Direct labor

Assembly ………………………………………………………..

$ 750,000

$ 600,000

Packaging ………………………………………………………

990,000

360,000

Direct costs …………………………………………………………

$3,240,000

$3,360,000

Overhead

Assembling (@ $30/mh) ……………………………………

$ 180,000

$ 900,000

270,000

Handling material (@$3,000/run) ……………………….

120,000

Packaging building

Inspecting and Packaging (@$5/direct labor-hour) .

300,000

114,000

Shipping (@$1,320/shipment) …………………………...

132,000

264,000

Total ABC cost …………………………………………………….

$3,903,000

$5,028,000

Number of units ……………………………………………………

100,000

Unit cost ……………………………………………………………..

9-35. (continued)

b. Kris could have made the reductions he planned, but the effect on the product costs

would have been different. The $99,000 reduction in setup costs (25% of $396,000),

9-36. (30 min.) Activity-Based Costing in a Nonmanufacturing Environment:

Cathy’s Catering.

a. & b.

Activities

a.

Afternoon

Picnic

b.

Formal

Dinner

Advertising (parties) ………………………….

$ 100

$ 100

Planning (parties) ……………………………..

75

125

9-37. (35 min.) Activity-Based versus Traditional Costing: Maglie Company.

a.

Rate

Handheld

Home

Total

Direct labora ……………………………………………….

$1,160,400

$ 439,600

$1,600,000

Direct materialsb …………………………………………

$750,000

$ 684,000

$1,434,000

Overhead costs

$ 132,000

$ 660,000

$ 550,400

$1,440,000

Total costs ………………………………………………….

Total unit cost ……………………………………………..

9-37. (continued)

b.

Rate

Handheld

Home

Total

Direct labora ……………………………………………….

$1,160,400

$ 439,600

$1,600,000

Direct materialsb …………………………………………

750,000

684,000

1,434,000

Total costs ………………………………………………….

$2,954,760

$4,474,000

9-38. (35 min.) Activity-Based versus Traditional Costing: Doaktown Products.

a.

Rate

M-008

M-123

Total

Direct materialsa …………………………………………

$100,000

$ 80,000

$180,000

$ 15

$ 75,000

$ 45,000

$140,000

$140,000

$280,000

9-38. (continued)

b.

Rate

M-008

M-123

Total

Direct materialsa …………………………………………

$100,000

$ 80,000

$180,000

Direct laborb ……………………………………………….

Total costs ………………………………………………….

$400,000

9-39. (30 min.) Activity-Based Costing in a Service Environment: EL&P.

Note: Answers may vary slightly due to rounding.

a.

Commercial

Residential

Total

Revenuea …………………………………………………..

$315,000

$780,000

$1,095,000

Direct Laborb ……………………………………………..

175,000

325,000

500,000

b.

Rate

Commercial

Residential

Total

Revenue ……………………………………………………

$315,000

$780,000

$1,095,000

Direct Labor ……………………………………………….

175,000

325,000

500,000

Overhead

a

b

$ 19,000

c

$ 25,000

d

35,500

e

24,500

f

1.20

g

h

i

Total Overhead …………………………..………………

$ 119,500

$ 85,500

9-39. (continued)

c. The recommendation to EL&P is that they should reconsider dropping residential

9-40. (35 min.) Activity-Based versus Traditional Costing: Isadore’s

Implements, Inc.

a.

Cost Driver

Rate

Pencils

Pens

Setting up…………………………………………………..

$1,440

a

$28,800

d

$ 43,200

b.

Pencils

Pens

Total

Direct Labor Hours ………………………………………

4,500

a

15,000

19,500

Overhead …………………………………………………..

b

9-41. (35 min.) Activity-Based versus Traditional Costing—Ethical Issues:

Windy City Coaching.

a.

Account

Rate

Teen

Counseling

Executive

Coaching

Total

Revenue ……………………………………………………

$66,000

$135,000

$201,000

Expenses:

Administrative support ………………………………

$4,000

a

24,000

d

16,000

40,000

Transportation …………………………………………

b

14,400

e

21,600

36,000

b.

Account

Rate

Teen

Counseling

Executive

Coaching

Total

Revenue …………………………………………………….

$66,000

$135,000

$201,000

Expenses …………………………………………………..

a

b

9-41. (continued)

e. Activity-based costing assigns higher costs to teen counseling than the traditional

method does, so using this would increase the chances of receiving the grant. If teen

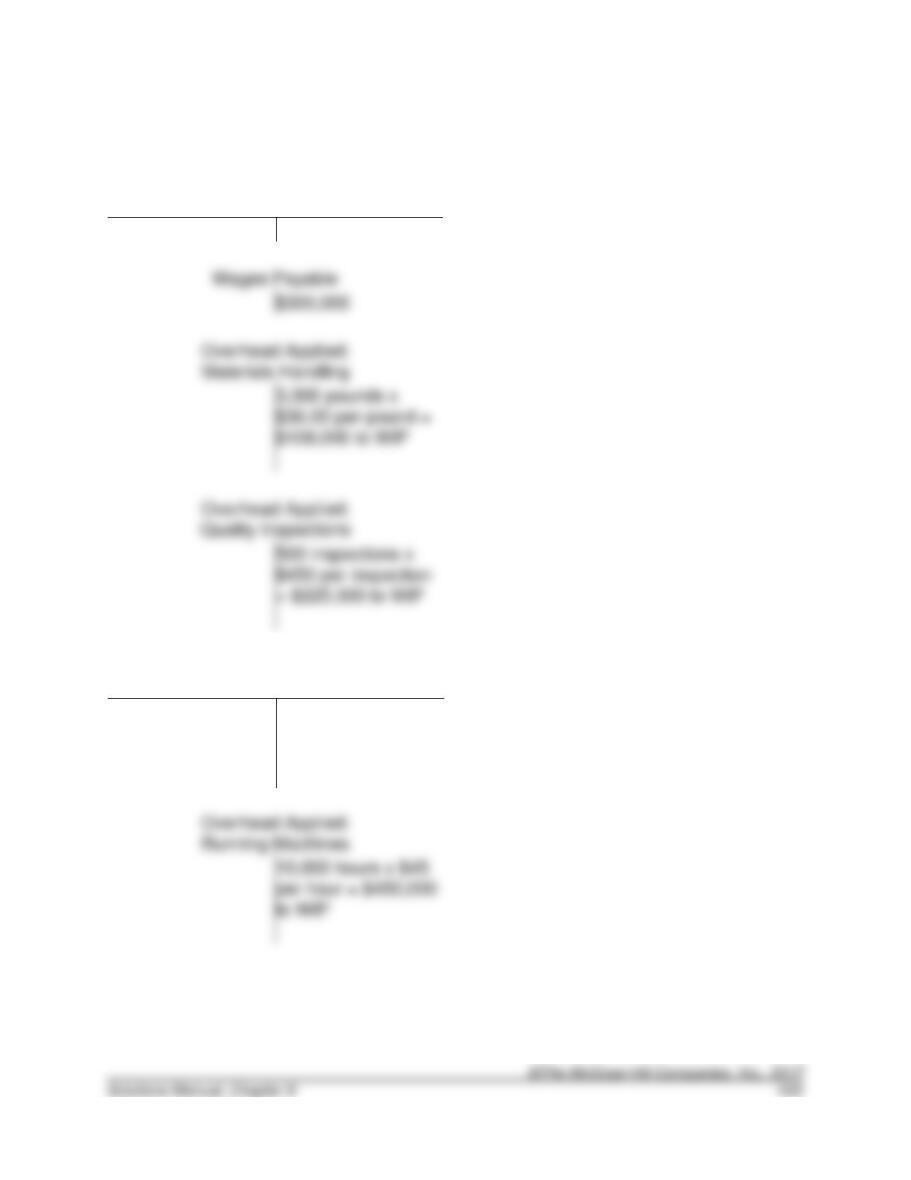

9-42. (30 min.) Activity-Based Costing—Cost Flows Through T-accounts:

Southwest Components.

Materials Inventory

$600,000

$300,000

$108,000 to WIP

Overhead Applied:

500 inspections x

$450 per inspection

= $225,000 to WIP

Overhead Applied:

Machine Setups

25 setups x $5,400

per setup =

$135,000 to WIP

Overhead Applied:

per hour = $450,000

to WIP

9-42. (continued)

Work in Process (WIP) Inventory

Fabrication Department

Direct Materials

600,000

Material Handling OH

Quality Inspect. OH

225,000

Running Machines OH

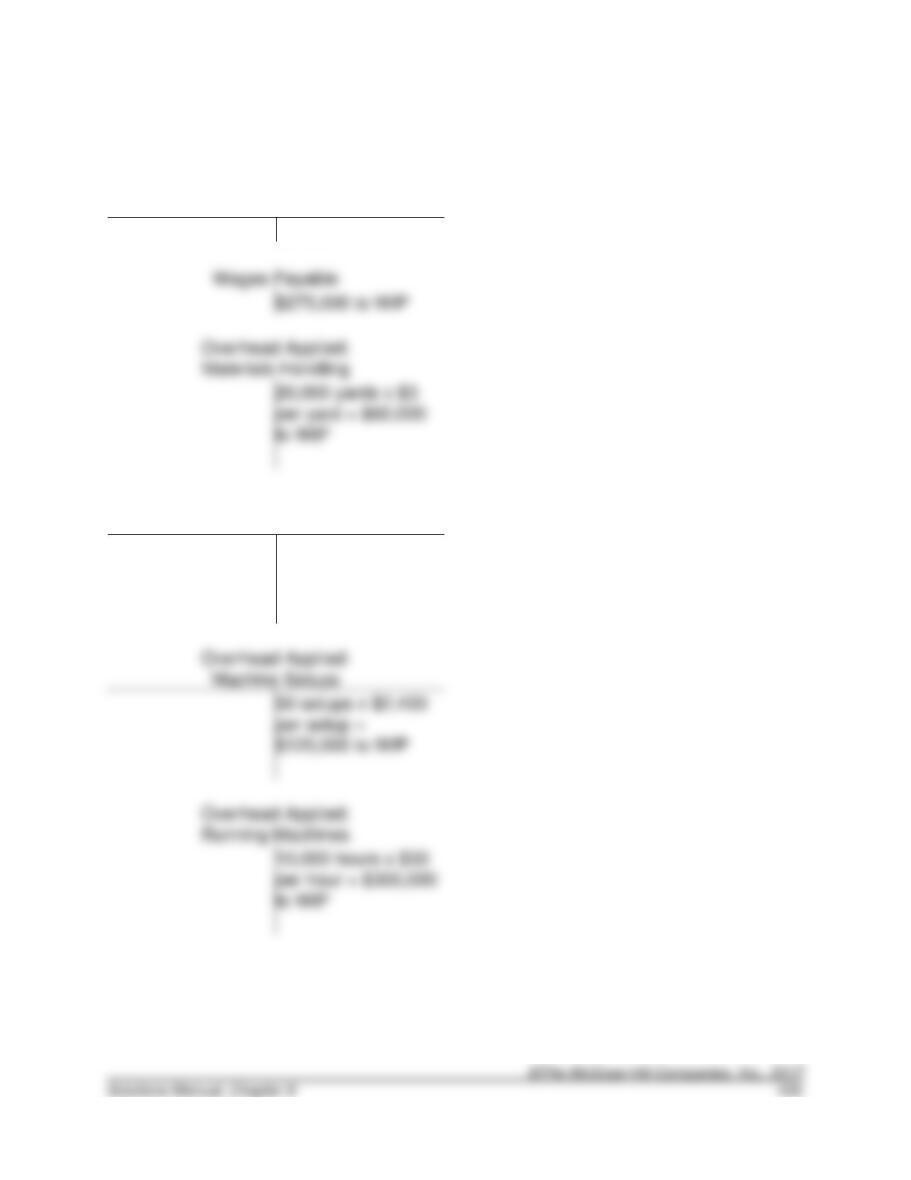

9-43. (30 min.) Activity-Based Costing—Cost Flows Through T-accounts:

Catalina Sails.

Materials Inventory

$550,000 to WIP

$275,000 to WIP

to WIP

Overhead Applied:

Quality Inspections

400 inspections x

$300 per inspection

= $120,000 to WIP

Overhead Applied:

$120,000 to WIP

Overhead Applied:

to WIP

9-43. (continued)

Work in Process (WIP) Inventory

Department Y

Direct Materials

550,000

Direct Labor

275,000

Material Handling

Quality Inspect.

120,000

Machine Setup

120,000

Running Machines

9-44. (20 min.) Activity-Based Costing for an Administrative Service: LastCall

Enterprises.

a.

Rate

LaidBack

StressedOut

Total

Allocated costsa …………………………..……………..

$1,100

$220,000

b

$55,000

c

$275,000

b.

Rate

LaidBack

StressOut

Total

Employee maintenancea ………………………………

$6,000

$60,000

b

$180,000

c

$240,000

Payrolld ……………………………………………………..

$140

28,000

e

7,000

f

35,000

9-45. (20 min.) Activity-Based Costing for an Administrative Service: John’s

Custom Computer Shop.

a.

Rate

Personal

Business

Total

b.

Rate

Personal

Business

Total

Billinga ……………………………………………………….

$48

$28,800

b

$19,200

c

$48,000

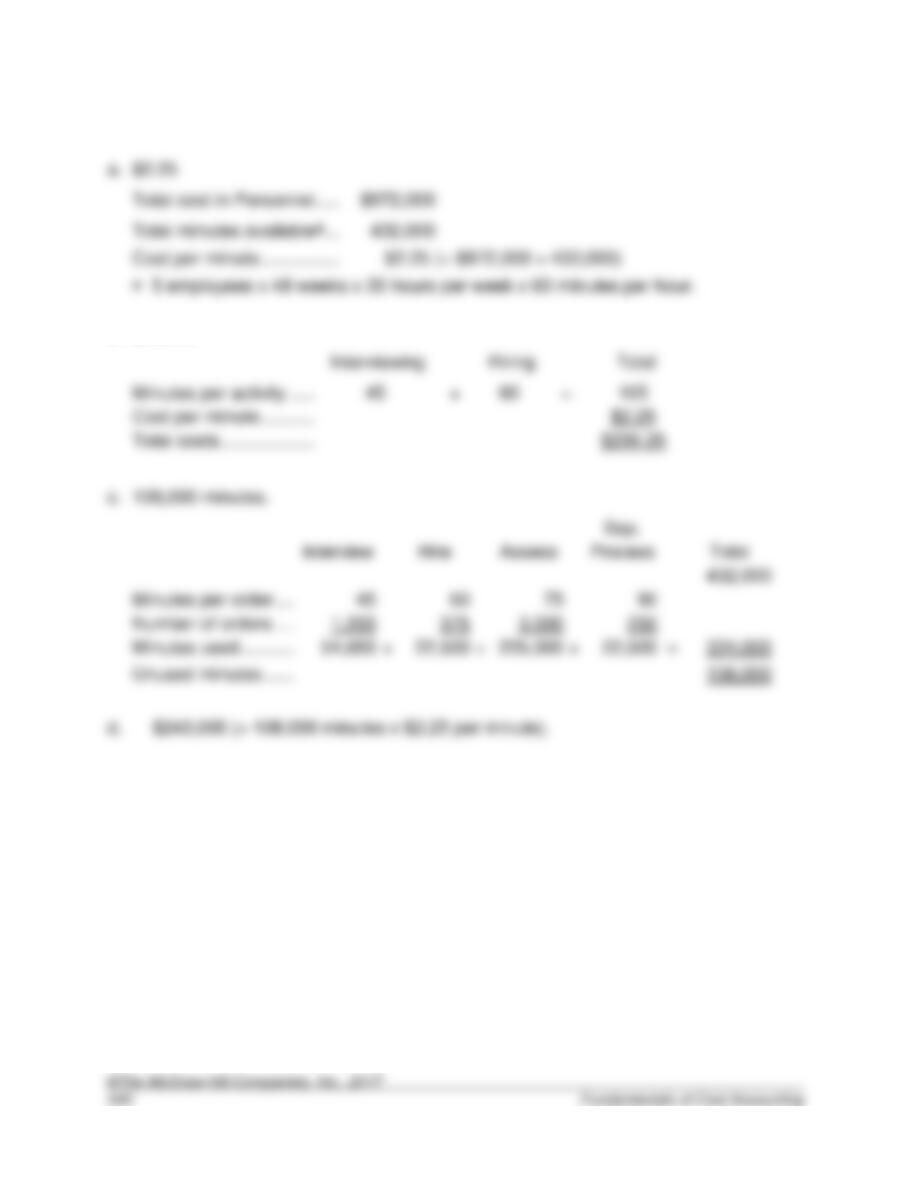

9-46. (20 min.) Time-Driven Activity-Based Costing: Kim Distribution Services.

Total cost in Distribution ……………………………….

9-47. (20 min.) Time-Driven Activity-Based Costing: City Enterprises.

Total cost in Personnel …………………………………

b.

$236.25

c.

108,000 minutes.

Solutions to Problems

9-48. (40 min.) Comparative Income Statements and Management Analysis: EZ–

Seat, Inc.

a. EZ-Seat, Inc. Income Statement

Account

Rate

Ergo

Standard

Total

Sales revenue …………………………………………….

$2,925,000

$2,760,000

$5,685,000

Direct materials …………………………………………..

$ 550,000

$ 500,000

Direct labor ………………………………………………..

Overhead costs:

a

e

b

f

1,080,000

c

g

d

h

Total overhead costs …………………………………..

3,708,000

b. Activity-based costing highlights the activities that cause costs, and provides insight

9-48. (continued)

c. EZ-Seat, Inc. Income Statement

Account

Rate

Ergo

Standard

Total

Sales revenue …………………………………………….

$2,925,000

$2,760,000

$5,685,000

Direct Materials …………………………………………..

Overhead Costs ………………………………………….

a

b

Operating Profit …………………………………………..

)

d. Dear Members of the Management Board:

9-49. (40 min.) Comparative Income Statements and Management Analysis:

Pepper’s Products.

a. Pepper’s Products: Income Statement

Account

Rate

Squeaky

Silent

Total

Sales revenue …………………………………………….

$43,200

$48,000

$91,200

Direct labor ………………………………………………..

Overhead costs:

b

f

c

g

Total overhead costs …………………………………..

a 25% = $6,000 administrative costs ÷ $24,000 direct labor costs.

b. Activity-based costing highlights the activities that cause costs, and provides insight

9-49. (continued)

c.

Pepper’s Products

Income Statement

Account

Rate

Squeaky

Silent

Total

Sales revenue …………………………………………….

$43,200

$48,000

$91,200

Direct Labor ……………………………………………….

Overhead Costs ………………………………………….

a

b

d. Dear Members of the Management Board:

The purpose of this report is to explain the differences between the profits in our

9-50. (15 min.) Ethics and Choice of Accounting Methods: Pepper’s Products.

Yes, you should show the results to management. You have an ethical responsibility

9-51. (50 min.) Activity-Based Costing and Predetermined Overhead Allocation

Rates: Kitchen Supply, Inc.

a. Computing overhead allocation rates

Activity

Cost

Driver

Est.

Costs

Driver

Units

Rate

Processing orders ………

No. of orders

$ 54,000

÷

200

=

$ 270

2,160

Using machines …………

Machine-hrs.

÷

12,000

=

1,600

b. Production Costs using Direct Labor-Hours

Account

Institutional

Standard

Silver

Total

Direct materials …………………………………………..

$ 39,000

$24,000

$15,000

$ 78,000

6,750

9-51. (continued)

c. Production Costs using ABC

Account

Institutional

Standard

Silver

Total

Direct materials …………………………………………..

$39,000

$ 24,000

$15,000

$78,000

Direct labor ………………………………………………..

6,750

6,750

9,000

22,500

Indirect costs

6,480

6,480

25,920

9,000

27,900

Total cost …………………………..………………………

$137,190

d. Internal Memorandum

The discrepancy between our product costs using direct-labor hours as the

allocation base versus activity-based costing is found in the way overhead costs are

9-52. (50 min.) Activity-Based Costing and Predetermined Overhead Rates:

College Supply Company.

a.

Activity

Recommended Base

Allocation Rate

Setting up production …

No. of runs

$360 per run ($36,000 ÷ 100 runs)

Processing orders ……..

No. of orders

$300 per order ($60,000 ÷ 200 orders)

Handling materials …….

$3.00 per lb. ($24,000 ÷ 8,000 lbs.)

Using machines …………

$7.20 per hour ($72,000 ÷ 10,000 hrs.)

management …………….

$1,500 per insp. ($60,000 ÷ 40 insp.)

Packing & shipping …….

$2.40 per unit ($48,000 ÷ 20,000 units)

Direct labor hour rate …

$150 per hour ($300,000 ÷ 2,000 hrs.)

b.

Short

Medium

Tall

Direct materials …………………………………………..

$ 6,000

$ 3,750

$ 3,000

9-52 (continued)

c.

Short

Medium

Tall

Direct materials …………………………………………..

$ 6,000

$ 3,750

$ 3,000

Direct labor ………………………………………………..

3,000

3,600

3,300

Setting up production …………………………………..

a

1,440

2,880

Processing orders ……………………………………….

b

Handling materials ………………………………………

1,200

c

2,400

Using machines ………………………………………….

3,600

d

2,160

2,160

Performing quality management ……………………

e

Shipping …………………………..………………………..

2,400

f

1,200

Total cost …………………………..………………………

d. Internal Memorandum

Re: Product Cost Discrepancy

9-53. (40 min.) Choosing an Activity-Based Costing System: Pickle

Motorcycles, Inc.

a.

Pickle Motorcycles

Income Statement

Route 66

Main Street

Alley Cat

Total

Sales revenue …………………………………………….

$7,600,000

$11,200,000

$9,500,000

$28,300,000

Direct costs:

Fixed OH:

9-53. (continued)

b.

Pickle Motorcycles

Income Statement

Route 66

Main Street

Alley Cat

Total

Sales revenue …………………………………………….

$7,600,000

$11,200,000

$9,500,000

$28,300,000

Direct costs:

Direct material …………………………………………

3,000,000

4,800,000

4,000,000

11,800,000

Var. OH:

Mach. setup …………………………………………….

Energy ……………………………………………………

Cont. margin ………………………………………………

$ 9,954,000

Fixed OH:

9-54. (40 min.) Activity-Based Costing, Cost Flow Diagram, and Predetermined

Overhead Rates: Churchill Products.

a.

Burden rate = (Total overhead costs ÷ Budgeted total direct labor-hours)

9-54. (continued)

b.

9-54. (continued)

d.

Unit Costs:

Oval

Round

Square

Direct Costs ……………………………………..

$240,000

$240,000

$240,000

Overhead:

Utilities ………………………………………..

675,000a

225,000

450,000

Material handling ………………………….

Total costs …………………………..…………..

Number of units ………………………………..

Unit cost ………………………………………….

$605.00

$331.67

e. If management implemented an activity-based costing system it should be provided

with a more thorough understanding of product costs. By breaking down costs into

9-55. (40 min.) Activity-Based Costing, Cost Flow Diagram, and Predetermined

Overhead Rates: Utica Manufacturing.

a.

Burden rate = (Total overhead costs ÷ Budgeted total machine-hours)

Budgeted total machine-hours = 60,000 + 90,000 = 150,000 hours

9-55. (continued)

b.

Inspection ……………………..

=

Production …………………….

=

Machine setup ……………….

=

$5,000 per setup.

Shipping ……………………….

=

c.

Unit Costs:

308

510

Direct Costs ……………………………………..

$216,000

$216,000

Overhead:

Total costs …………………………..…………..

Number of units ………………………………..

Unit cost ………………………………………….

d. If management implemented an activity-based costing system it should be provided

with a more thorough understanding of product costs. By breaking down costs into

9-56. (40 min.) Activity-Based Costing and Predetermined Overhead Rates:

Cain Components.

a.

Burden rate = (Total overhead costs ÷ Budgeted total machine-hours)

Budgeted total machine-hours = 150,000 + 100,000 = 250,000 hours

9-56. (continued)

b.

Receiving ……………………..

$600,000 ÷ $400,000 material dollars

=

150% of material dollars.

Production …………………….

=

Machine setup ……………….

=

$4,500 per setup.

Shipping ……………………….

=

Unit Costs:

Standard

Deluxe

Direct Costs ……………………………………..

$895,000

$405,000

Overhead:

Total costs …………………………..…………..

Number of units ………………………………..

Unit cost ………………………………………….

c. If these results are typical, it will probably not be worth adopting the ABC system.

The difference in the reported product costs are not significant, meaning they would

9-57. (40 min.) Activity-Based Costing and Predetermined Overhead Rates:

Cain Components.

a.

Receiving ……………………..

$600,000 ÷ $400,000 material dollars

=

150% of material dollars.

Manufacturing ……………….

=

$13.20 per machine-hour

Machine setup ……………….

=

$4,500 per setup.

Shipping ……………………….

=

$40.00 per unit.

Unit Costs:

Standard

Deluxe

Direct Costs ……………………………………..

$895,000

$405,000

Overhead:

Receiving …………………………………….

367,500a

232,500

Machine setup ……………………………..

337,500d

562,500

200,000

Total costs …………………………..…………..

9-58. (15 min.) Benefits of Activity-Based Costing: Cawker Products.

Activity-based costing would help to clear his confusion by identifying the activities that

drive overhead costs.

9-59. (40 min.) Choosing an Activity-Based Costing System: MTI.

a. Total overhead to allocate is $8,700,000 (= $2,400,000 + $1,800,000 + $2,400,000 +

$1,200,000 + $900,000).

The overhead rate is $348 per machine-hour (= $8,700,000 ÷ 25,000 machine-hours).

MTI

Income Statement

M3100

M4100

M6100

Total

Sales revenue …………………………………………….

$9,000,000

$15,000,000

$13,500,000

$37,500,000

Direct costs:

4,500,000

3,300,000

Var. overhead …………………………………………….

a

Contribution margin …………………………………….

$3,312,000

$4,920,000

$14,700,000

6,000,000

b. Cost driver rates:

Activity

Cost

Activity Volume

Unit Rate

Setting up machines ….

$2,400,000

÷

50 runs

=

$48,000 per run

Processing sales orders ………………………………

$1,800,000

÷

=

2,250 per order

÷

6,000 per unit

Operating machines …..

$1,200,000

÷

=

48 per machine-hr.

Shipping …………………..

÷

37,500 units shipped

=

24 per unit shipped

9-59. (continued)

Income Statement

M3100

M4100

M6100

Total

Sales revenue …………………………………………….

$9,000,000

$15,000,000

$13,500,000

$37,500,000

Direct costs:

Direct material. ………………………………………..

3,000,000

4,500,000

3,300,000

10,800,000

Direct labor ……………………………………………..

600,000

900,000

1,800,000

3,300,000

Var. overhead …………………………………………….

Setting up machines ……………………………………

a

Processing orders ………………………………………

405,000

b

900,000

495,000

1,800,000

Warehousing ………………………………………………

600,000

c

600,000

2,400,000

Operating machines …………………………………….

d

Shipping …………………………..………………………..

e

Cont. margin ………………………………………………

$3,387,000

$ 5,625,000

$14,700,000

Plant admin. ……………………………………………

c. Although both methods yield similar product costs, the activity-based costing method

provides a more detailed breakdown of the costs. This additional information should

9-60. (15 min.) Time-Based ABC – Time Equations: Kim Distribution Systems.

a.

Taking order = 10 minutes + 30 minutes (if retailer is new).

b.

c.

From the solution to Exercise 9-46 (a):

9-61. (15 min.) Time-Based ABC – Time Equations: City Enterprises.

a.

b.

c.

From the solution to Exercise 9-47 (a):

d.

Solutions to Integrative Cases

9-62. (50 Min) Cost Allocation and Environmental Processes—Ethical Issues:

California Circuits Company.

a.

Raw material …………………………….

Direct labor – Production …………….

$2.00

$2.00

Direct labor – Assembly ……………..

= 120% of direct labor costs

b.

XL-D

XL-C

Raw material ……………………………..

$12.00

$14.00

Direct labor – Production ……………..

$2.00

Direct labor – Assembly ………………

$8.00

a Overhead rate—Production Department = Production overhead ÷ Total machine–

hours

9-62. (continued)

d.

XL-D

XL-C

Raw material …………………………………..

$12.00

$14.00

Direct labor – Production …………………..

$2.00

$2.00

Direct labor – Assembly ……………………

$0.80

$0.80

Total production overhead …………………

8.47

6.12

a Production Department Overhead Calculations (Rate = Activity cost ÷ Driver volume):

Activity

Activity

Cost

Driver

Driver Volume

Rate

Supervision ………………………………………………..

$100,000

Direct

labor-hrs

100,000 .1 + 25,000 .1

= 12,500 hours

$8.00

Testing ………………………………………………………

Test

hours

100,000 3 + 25,000 3

= 375,000 hours

$0.40

= 200,000 machine-hours

Shipping …………………………………………………….

Weight

100,000 1.0 + 25,000 1.6

= 140,000 pounds

$0.05

= $10 per direct labor-hour

9-62. (continued)

e. This question raises the issue of costs that are missing in the typical accounting

records of the firm. In this case, the ABC system suggests that XL-C, the model that

9-63. (60 min.) Distortions Caused By Inappropriate Overhead Allocation Base:

Chocolate Bars, Inc.

a.

Almond

Dream

Krispy

Krackle

Creamy

Crunch

Product costs:

Labor-hours per case ……………………………….

7

3

1

Total cases produced ……………………………….

1,000

1,000

1,000

Material cost per case ………………………………

$8.00

$2.00

$9.00

Direct labor cost per case………………………….

Labor-hours per product …………………………...

7,000

3,000

1,000

Costs of products:

Material cost per case ………………………………

$ 8.00

$ 2.00

$ 9.00

Direct labor cost per case………………………….

Allocated overhead per case ……………………..

44.24

18.96

Product cost ……………………………………………

Selling price ……………………………………………….

Gross profit margin ……………………………………..

(10.87

29.16

%

39.09

%

Drop product? …………………………………………….

Yes

9-63. (continued)

c.

Krispy

Krackle

Creamy

Crunch

Direct labor cost per hour …………………………….

$6.00

$6.00

Direct labor-hours per case…………………………..

Total cases produced ………………………………….

2,000

Labor-hours per product ………………………………

3,000

2,000

Total labor-hours: 5,000

Allocation rate per labor-hour

=

Total overhead ÷ Total labor-hours

=

$69,500/5,000

=

per labor-hour

Allocated production costs:

Krispy

Krackle

Creamy

Crunch

Material cost per case ………………………………….

$ 2.00

$ 9.00

Direct labor cost per case …………………………....

18.00

6.00

Allocated overhead per case

Product cost ……………………………………………….

Selling price ……………………………………………….

Product cost—direct labor allocation base ………

)

)

)

Profit margin percentage ……………………………..

$(6.70) ÷ $55.00

$6.10 ÷ $35.00

(12.2)

%

17.4%

9-63. (continued)

d.

Creamy

Crunch

Direct labor cost per hour …………………………….

$6.00

Direct labor hours per case …………………………..

Total cases produced ………………………………….

3,000

Labor hours per product ………………………………

3,000

Total labor hours: 3,000

Allocation rate per labor hour

=

Total overhead/Total labor hours

=

$69,500/3,000

=

Allocated Production Costs:

Creamy

Crunch

Material cost per case ………………………………….

$ 9.00

Direct labor cost per case …………………………....

Allocated overhead per case ………………………..

Product cost ……………………………………………….

Gross profit margins:

Selling price ……………………………………………….

Product cost—direct labor allocation base ………

)

)

Profit margin percentage ……………………………..

$(3.17) ÷ $35.00

(9.1)%

The recommendation to management is to drop Creamy Crunch and sell out!

e. The policies and allocation method employed by CBI encourage poor decision

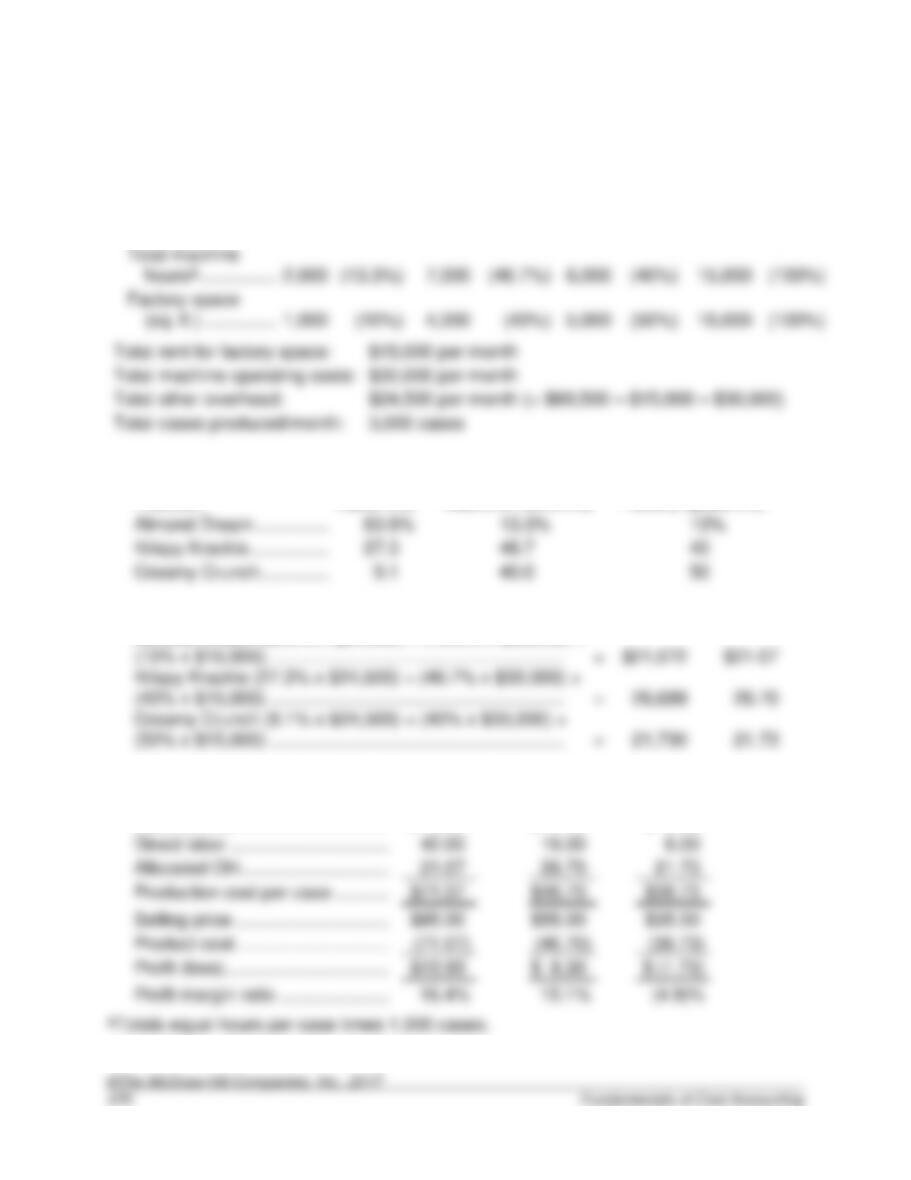

9-64. (90 min.) Multiple Allocation Bases: Chocolate Bars, Inc.

a.

Almond

Dream

Krispy

Krackle

Creamy

Crunch

Total

Total direct

labor hoursa …………………………………………….

7,000

(63.6%)

3,000

(27.3%)

1,000

(9.1%)

11,000

(100%)

Total machine

hoursa …………………………………………………….

2,000

(13.3%)

7,000

(46.7%)

6,000

(40%)

15,000

(100%)

Factory space

(sq. ft.) ……………………………………………………

1,000

(10%)

4,000

(40%)

5,000

(50%)

10,000

(100%)

Total rent for factory space:

$15,000 per month

Total machine operating costs:

$30,000 per month

Total cases produced/month:

3,000 cases

Product allocation base:

Fraction:

Labor (%)

Machine hours (%)

Factory space (%)

Krispy Krackle …………………………………………….

Creamy Crunch …………………………………………..

Allocated Costs:

Total

Per Case

(10% x $15,000) …………………………………………………..

=

Krispy Krackle (27.3% x $24,500) + (46.7% x $30,000) +

(40% x $15,000) …………………………………………………..

=

(50% x $15,000) …………………………………………………..

=

Almond Dream (63.6% x $24,500) + (13.3% x $30,000) +

Allocated production costs:

Almond

Dream

Krispy

Krackle

Creamy

Crunch

Material cost ………………………………………………

$ 8.00

$ 2.00

$ 9.00

Allocated OH ………………………………………………

Product cost ……………………………………………….

(46.70)

Profit (loss)…………………………………………………

$ 8.30

$ (1.73)

Profit margin ratio ……………………………………….

16.4%

9–64. (continued)

b. Based upon the table above and the gross profit margin rule, management would

recommend dropping Creamy Crunch. Two characteristics of Creamy Crunch

c.

Almond

Dream

Krispy

Krackle

Direct labor hours per case …………………………..

7

3

Machine hours per case ………………………………

2

7

Case of output per month …………………………….

Labor hours required …………………………………..

(82.4%)

(17.6%)

Total rent for factory space:

$15,000 per month

Total other overhead:

$24,500 per month

Total labor hours/month:

17,000

Fraction:

Almond Dream ……………………………………………

36.4%

9-64. (continued)

Allocated Cost:

Total

Per Case

Almond Dream (82.4% x $24,500) +

(36.4% x $30,000) + (33.3% x $15,000) ……………

=

$36,108

$18.05

(63.6% x $30,000) + (66.7% x $15,000) ……………

=

Allocated production costs:

Krackle

Material cost ………………………………………………

Direct labor ………………………………………………..

Allocated OH ………………………………………………

Production cost per case ……………………………..

Selling price ……………………………………………….

Product cost ……………………………………………….

Profit margin ratio:

Ratio = Gross Margin/Price …………………………..

Krispy Krackle (17.6% x $24,500) +

Allocated production costs:

Almond

Dream

Material cost ………………………………………………

Direct labor ………………………………………………..

Allocated OH ………………………………………………

Production cost per case ……………………………..

$73.17

Selling price ……………………………………………….

$85.00

Product cost ……………………………………………….

$11.83

Profit margin ratio:

Ratio = Gross Margin/Price …………………………..

9-64. (continued)

If we compute the gross margin for the three products at maximum production, we

find Almond Dream and Krispy Krackle to be equally profitable, computed as follows:

Almond

Dream

or

Krispy

Krackle

or

Creamy

Crunch

Cases ………………………………………………………..

3,000

3,000

3,000

Costs

$219,500

Revenue …………………………………………………….

$165,000

Gross margin………………………………………………

9-65. (90 min.) Activity-Based Costing – The Grape Cola Caper.

a. Percentage utilization of resource by activities:

Activity

Setups

Production

Runs

Products

Machine

Time

Indirect labor (including fringe benefits)

50%

40%

10%

0%

Information technology (IT)

Machinery depreciation

100

Machinery maintenance

100

Energy

100

Costs assigned to activiities:

Activity

Cost

Setups

Production

Runs

Products

Machine

Time

Indirect labor

$28,000

$14,000

$11,200

$2,800

$ 0

10,000

2,000

Machinery depreciation

Machinery maintenance

Energy

0

$52,000

$14,000

$19,200

$4,800

÷ Activity

110 runs

4 products

10,000 hrs

Cost driver rates

$174.55

$1,200

$1.40

9-65. (continued)

b.

Unit Costs on Cola Bottling Line

Diet

Regular

Cherry

Grape

Total

Materials

$ 25,000

$ 20,000

$ 4,680

$ 550

$ 50,230

Direct labor

10,000

8,000

1,800

200

20,000

Fringe benefits on direct labor

3,200

8,000

Setup costs

Production run costs

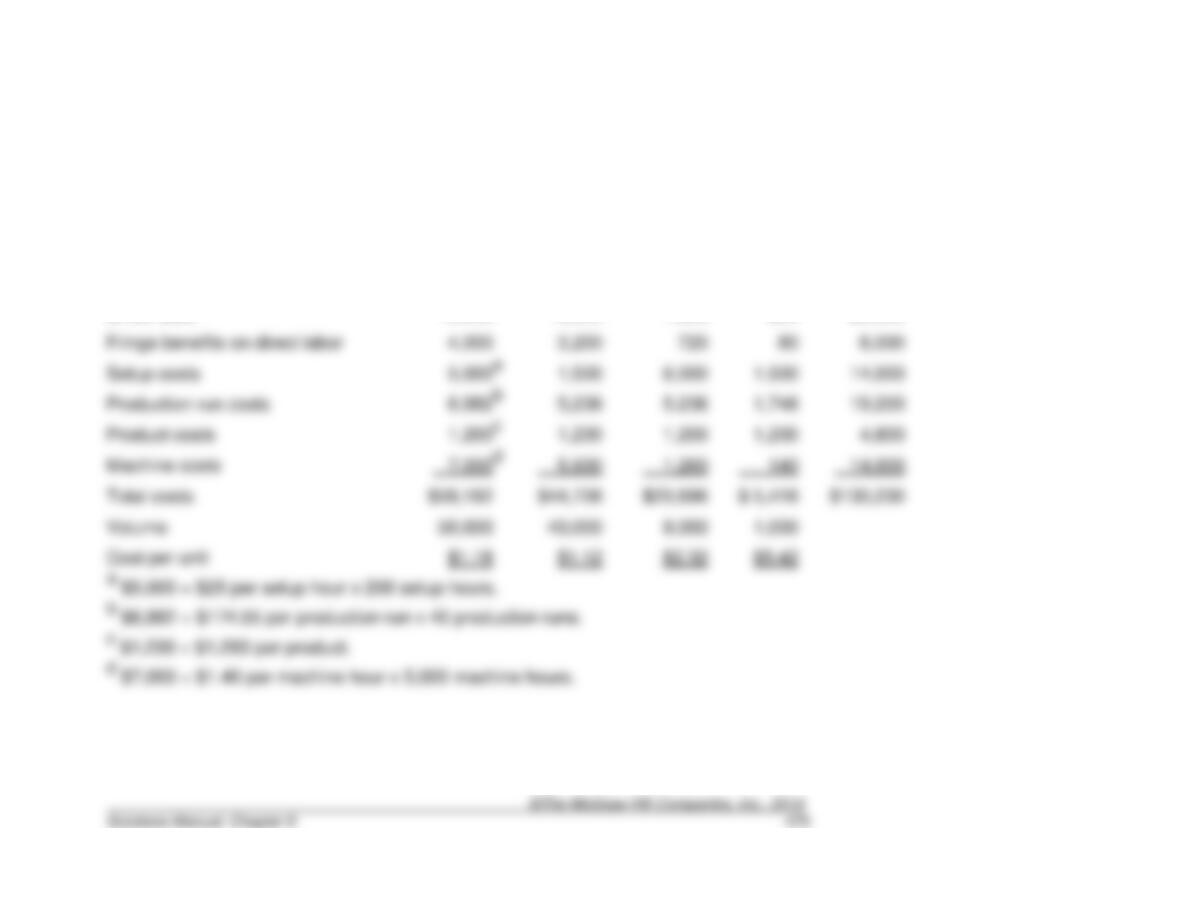

Product costs

Machine costs

Total costs

Volume

Cost per unit

9-65. (continued)

c.

Monthly Report on Cola Bottling Line

Diet

Regular

Cherry

Grape

Total

Sales revenue

$75,000

$60,000

$13,950

$1,650

$150,600

Costs

Gross margin