PROBLEM 9-42 (CONTINUED)

4.

Cash disbursements budget:

20×1

January

February

March

First

Quarter

Inventory purchases:

Cash payments for purchases

during the current month* ……..

$258,720

$284,592

$298,144

$ 841,456

Total cash payments for

inventory purchases …………………..

$611,520

$672,672

$725,032

$2,009,224

Cash payments for purchases

Other expenses:

Sales salaries …………………………….

$ 42,000

$ 42,000

$ 42,000

$ 126,000

Advertising and promotion …………

32,000

32,000

32,000

96,000

Administrative salaries ……………….

42,000

42,000

42,000

Interest on bonds** …………………….

30,000

30,000

Property taxes** …………………………

10,800

10,800

Total cash payments for other

$154,800

$136,480

$126,648

*40% of current month’s purchases [see requirement (3)].

**Bond interest is paid every six months, on January 31 and July 31. Property taxes also

PROBLEM 9-42 (CONTINUED)

5.

Summary cash budget:

20×1

January

February

March

First

Quarter

Cash receipts [from req. (2)] …………….

$ 826,000

$ 908,600

$ 999,460

$2,734,060

Cash disbursements

[from req. (4)] …………………………….

(766,320)

(809,152)

(851,680)

(2,427,152)

during period due to operations ….

$ 306,908

Sale of marketable securities

(1/2/x1) ………………………………………

Proceeds from bank loan

200,000

200,000

Purchase of equipment ……………………

Repayment of bank loan

(3/31/x1) …………………………………….

Interest on bank loan* ……………………..

Payment of dividends ……………………..

first quarter ………………………………..

Cash balance, 1/1/x1 ……………………….

Change in cash balance

6.

Analysis of short-term financing needs:

Projected cash balance as of December 31, 20×0 ………………………………..

$ 70,000

Less: Minimum cash balance ……………………………………………………………..

Cash available for equipment purchases …………………………………………….

$ 20,000

Projected proceeds from sale of marketable securities ……………………….

Cash available …………………………………………………………………………………..

Less: Cost of investment in equipment …………………………..…………………..

PROBLEM 9-42 (CONTINUED)

7.

GLOBAL ELECTRONICS COMPANY

BUDGETED INCOME STATEMENT

FOR THE FIRST QUARTER OF 20X1

Sales revenue ………………………………………………………………

$2,912,800

Less: Cost of goods sold ……………………………………………..

2,038,960

Gross margin ……………………………………………………….………

Selling and administrative expenses:

Sales salaries ……………………………………………………….…

Sales commissions ………………………………………………….

Advertising and promotion ………………………………………

Administrative salaries …………………………………………….

Depreciation ……………………………………………………………

Interest on bonds …………………………………………………….

Interest on short-term bank loan ………………………………

Property taxes …………………………………………………………

Total selling and administrative expenses ……………………..

Net income …………………………………………………………………..

8.

GLOBAL ELECTRONICS COMPANY

BUDGETED STATEMENT OF RETAINED EARNINGS

FOR THE FIRST QUARTER OF 20X1

Retained earnings, 12/31/x0 ………………………………………………………………

Add: Net income ……………………………………………………………………………….

Deduct: Dividends …………………………………………………………………………….

Retained earnings, 3/31/x1 …………………………..……………………………………

PROBLEM 9-42 (CONTINUED)

9.

GLOBAL ELECTRONICS COMPANY

BUDGETED BALANCE SHEET

MARCH 31, 20X1

Cash …………………………………………………………………………………………………

$ 51,908

Accounts receivable* …………………………………………………………………………

718,740

Inventory …………………………………………………………………………………………..

372,680

Buildings and equipment (net of accumulated depreciation)† ………………

Total assets ………………………………………………………………………………………

$2,495,328

Accounts payable** ……………………………………………………………………………

$ 447,216

Bond interest payable ………………………………………………………………………..

10,000

Property taxes payable ………………………………………………………………………

1,800

Bonds payable (10%; due in 20×6) ………………………………………………………

Common Stock ………………………………………………………………………………….

1,000,000

Retained earnings ……………………………………………………………………………..

Total liabilities and stockholders’ equity ……………………………………………..

$2,495,328

*Accounts receivable, 12/31/x0 …………………………………………………………..

$ 540,000

Sales on account [req. (1)] ………………………………………………………………….

2,184,600

Accounts receivable, 3/31/x1 ………………………………………………………………

$1,252,000

Cost of equipment acquired ……………………………………………………………….

250,000

Depreciation expense for first quarter …………………………………………………

Buildings and equipment (net), 3/31/x1 ……………………………………………….

$1,352,000

**Accounts payable, 12/31/x0 ……………………………………………………………..

$ 352,800

Purchases [req. (3)] ……………………………………………………………………………

2,103,640

Cash payments for purchases [req. (4)] ………………………………………………

Accounts payable, 3/31/x1 ………………………………………………………………….

$ 447,216

Chapter 09 – Financial Planning and Analysis: The Master Budget

SOLUTIONS TO CASES

CASE 9-43 (35 MINUTES)

1. Some of the operational and behavioral benefits that are generally attributed to a

participatory budgeting process are as follows:

2. Four deficiencies in Jack Riley’s participatory policy for planning and performance

evaluation, along with recommendations of how the deficiencies can be corrected:

Deficiencies

Recommendations

The setting of constraints on fixed

expenditures includes uncontrollable fixed

costs, thereby mitigating the positive effects

of participatory budgeting.

Rewards should be based on meeting

budget and/or organizational goals or

objectives.

Chapter 09 – Financial Planning and Analysis: The Master Budget

CASE 9-44 (60 MINUTES)

1.

Yes, Triple-F Health Club should be better able to plan its cash receipts with the new

2.

a.

Factors that management should consider before adopting the new membership

plan and fee structure include:

• Costs associated with the plan changeover

• Public acceptance of the new proposal

3.

Because Triple-F’s cash flows should be more predictable, management should be

better able to plan for and control cash disbursements. In addition, management

should be better able to plan for short-term investments when excess cash occurs or

to arrange for short-term financing when there are cash shortages.

Chapter 09 – Financial Planning and Analysis: The Master Budget

CASE 9-45 (120 MINUTES)

1.

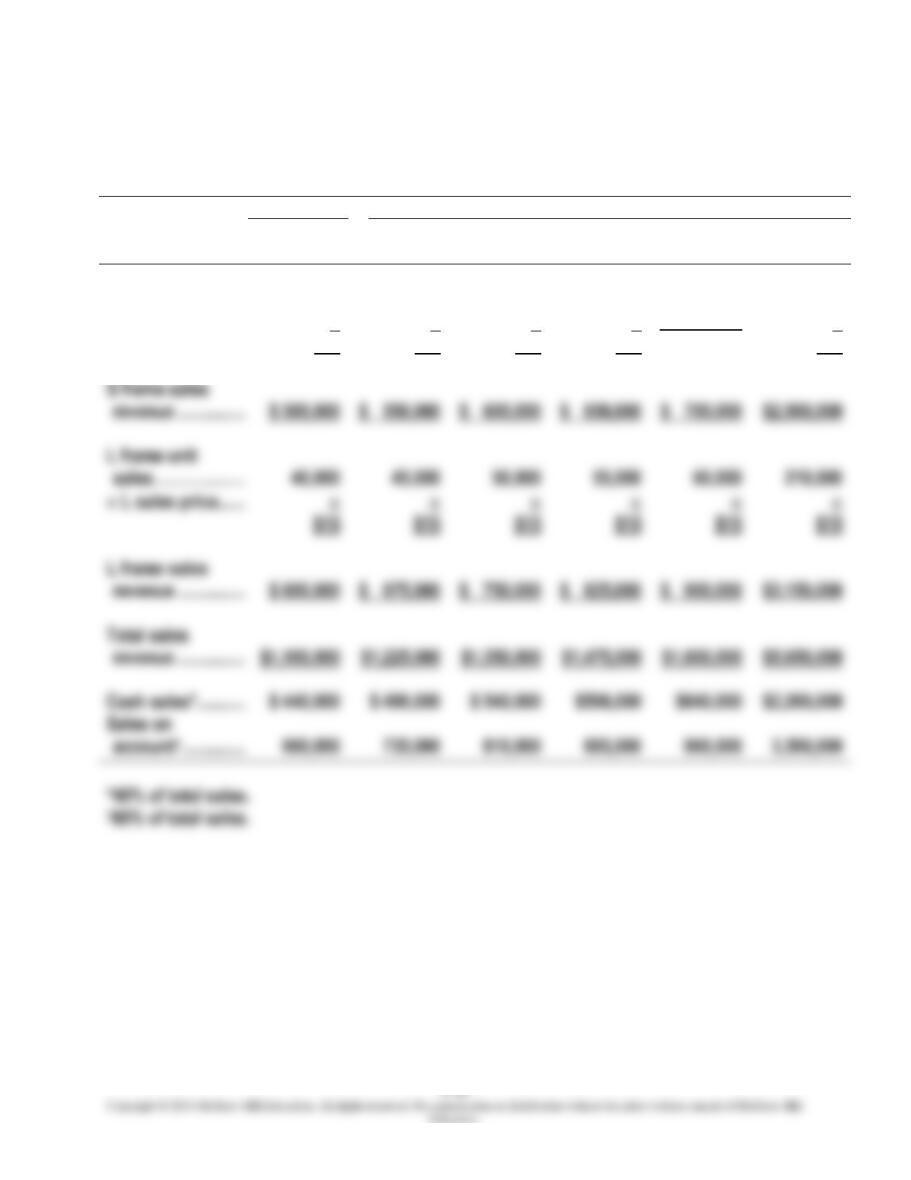

Sales budget:

20×4

20×5

4th

Quarter

1st

Quarter

2nd

Quarter

3rd

Quarter

4th

Quarter

Entire

Year

S frame unit

sales ………………..

50,000

55,000

60,000

65,000

70,000

250,000

S sales price …..

$10

$10

$10

$10

x $10

$10

S frame sales

revenue ……………

L frame unit

sales ………………..

40,000

45,000

50,000

55,000

60,000

210,000

L frame sales

$ 600,000

Total sales

Cash sales* ………..

*40% of total sales.

Chapter 09 – Financial Planning and Analysis: The Master Budget

CASE 9-45 (CONTINUED)

2.

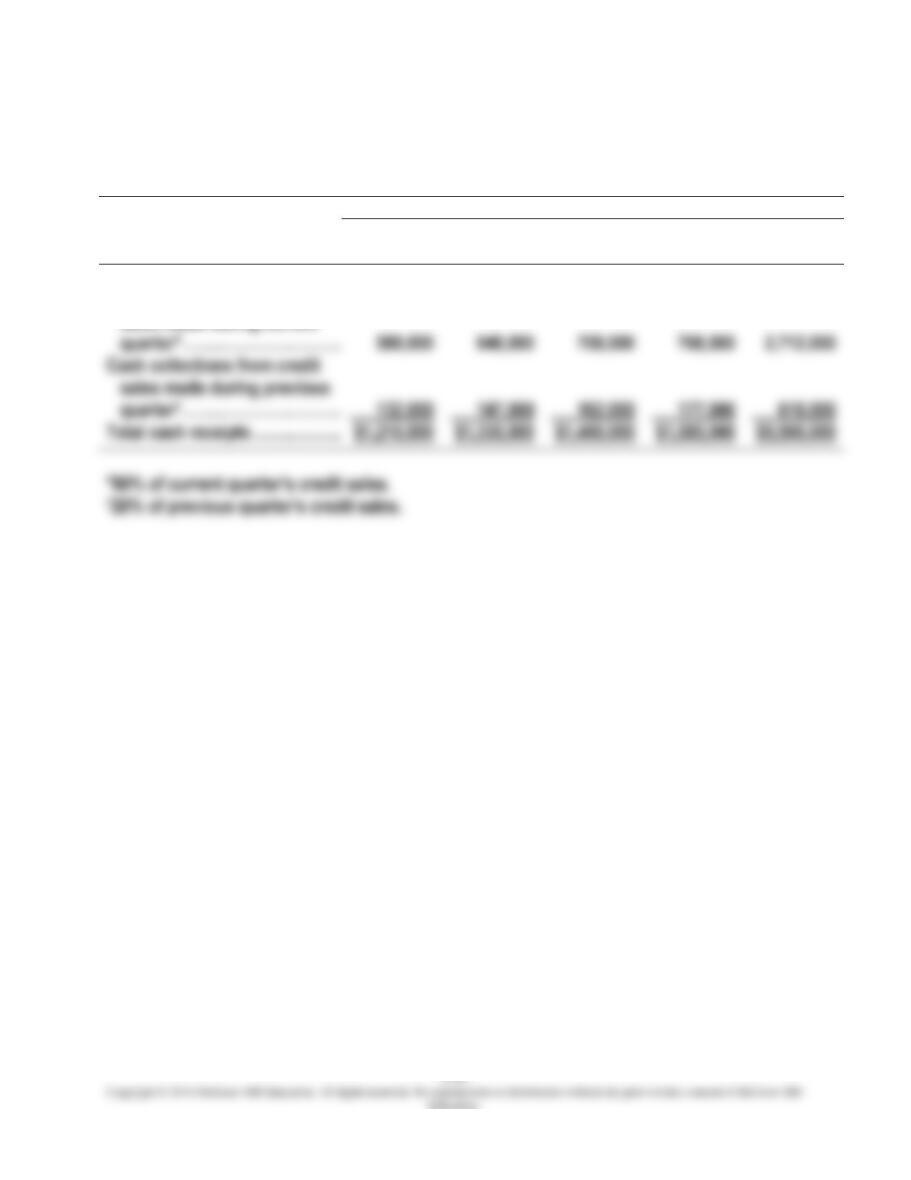

Cash receipts budget:

20×5

1st

Quarter

2nd

Quarter

3rd

Quarter

4th

Quarter

Entire

Year

Cash sales ……………………………………

$ 490,000

$ 540,000

$ 590,000

$ 640,000

$2,260,000

Cash collections from credit

*80% of current quarter’s credit sales.

Cash collections from credit

sales made during current

Chapter 09 – Financial Planning and Analysis: The Master Budget

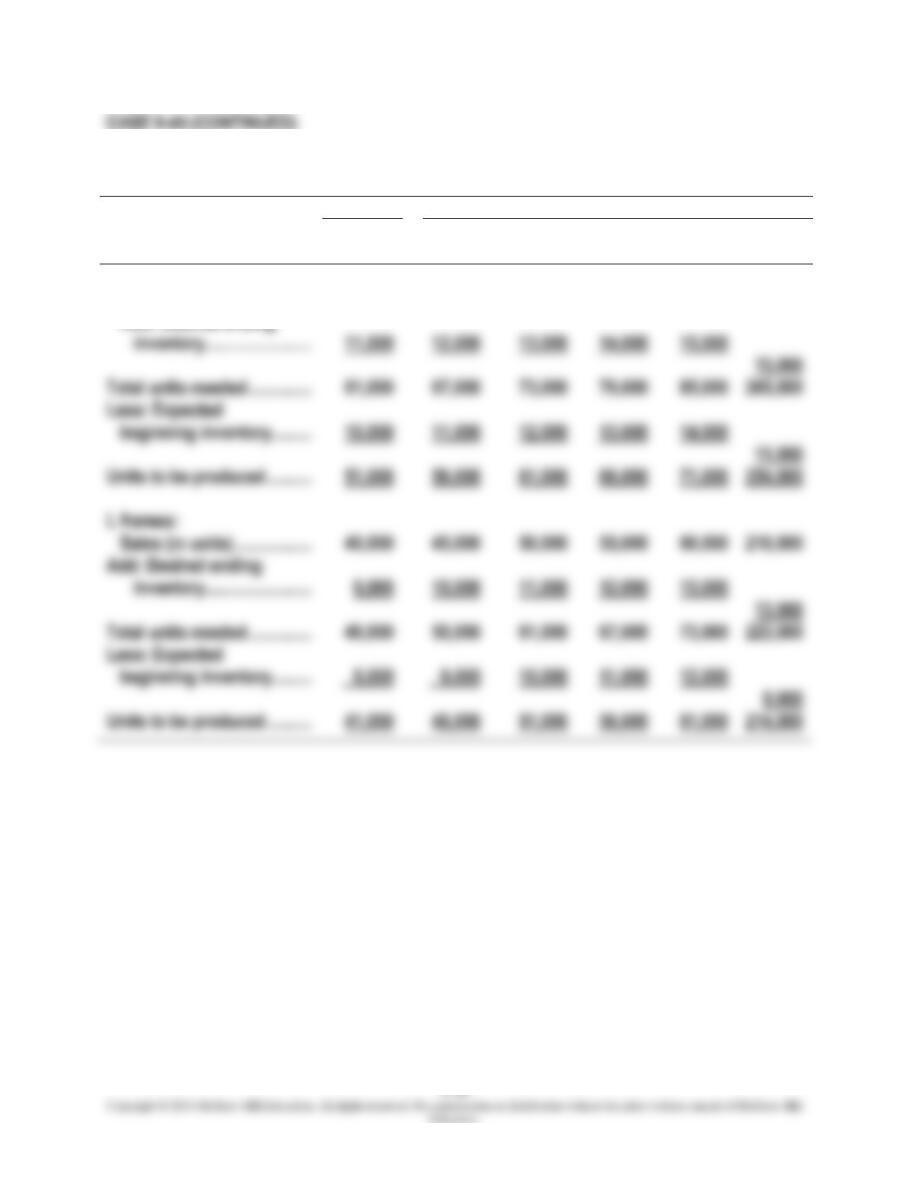

3.

Production budget:

20×4

20×5

4th

Quarter

1st

Quarter

2nd

Quarter

3rd

Quarter

4th

Quarter

Entire

Year

S frames:

Sales (in units) ……………..

50,000

55,000

60,000

65,000

70,000

250,000

Total units needed …………..

61,000

67,000

73,000

79,000

85,000

265,000

Units to be produced ……….

51,000

56,000

61,000

66,000

71,000

254,000

L frames:

Sales (in units) ……………..

40,000

45,000

50,000

55,000

60,000

210,000

Total units needed …………..

49,000

55,000

61,000

67,000

223,000

Add: Desired ending

Chapter 09 – Financial Planning and Analysis: The Master Budget

CASE 9-45 (CONTINUED)

4.

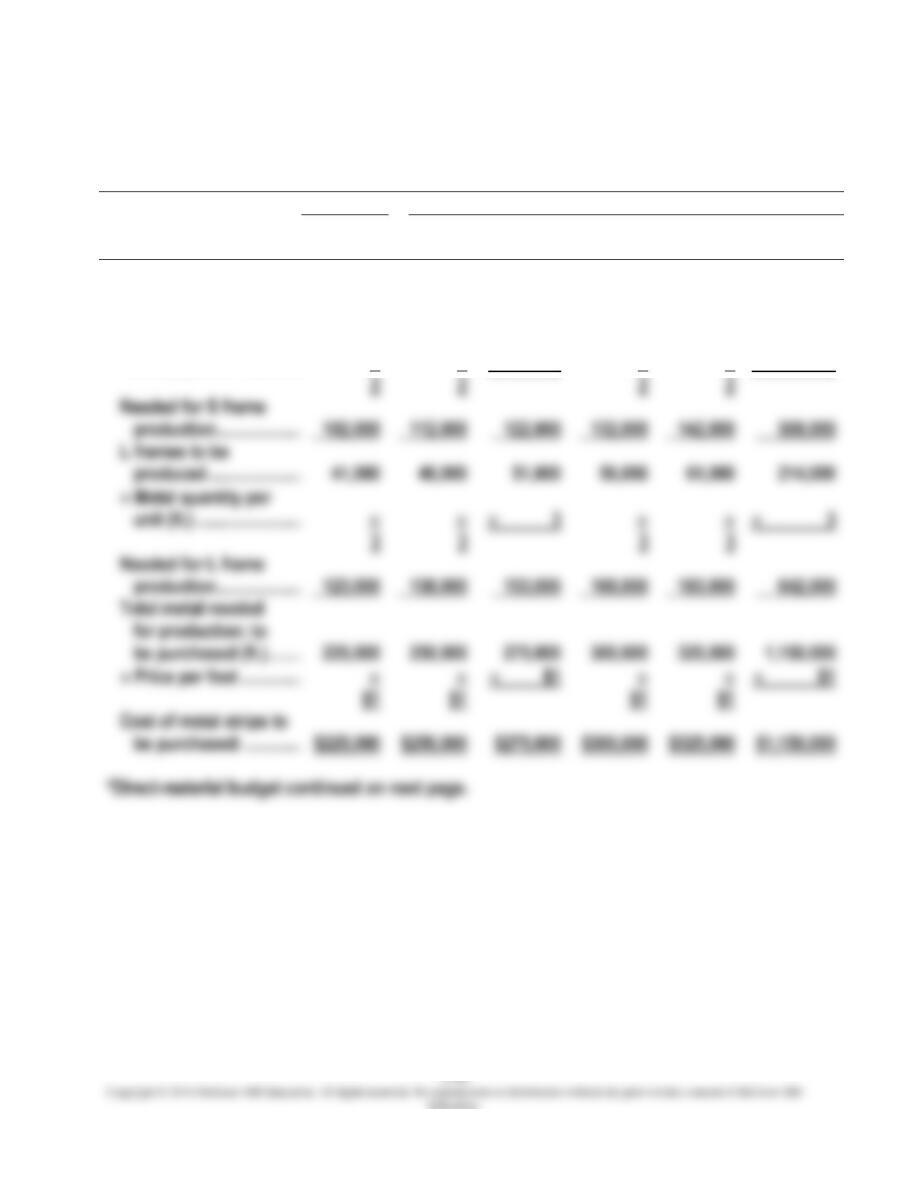

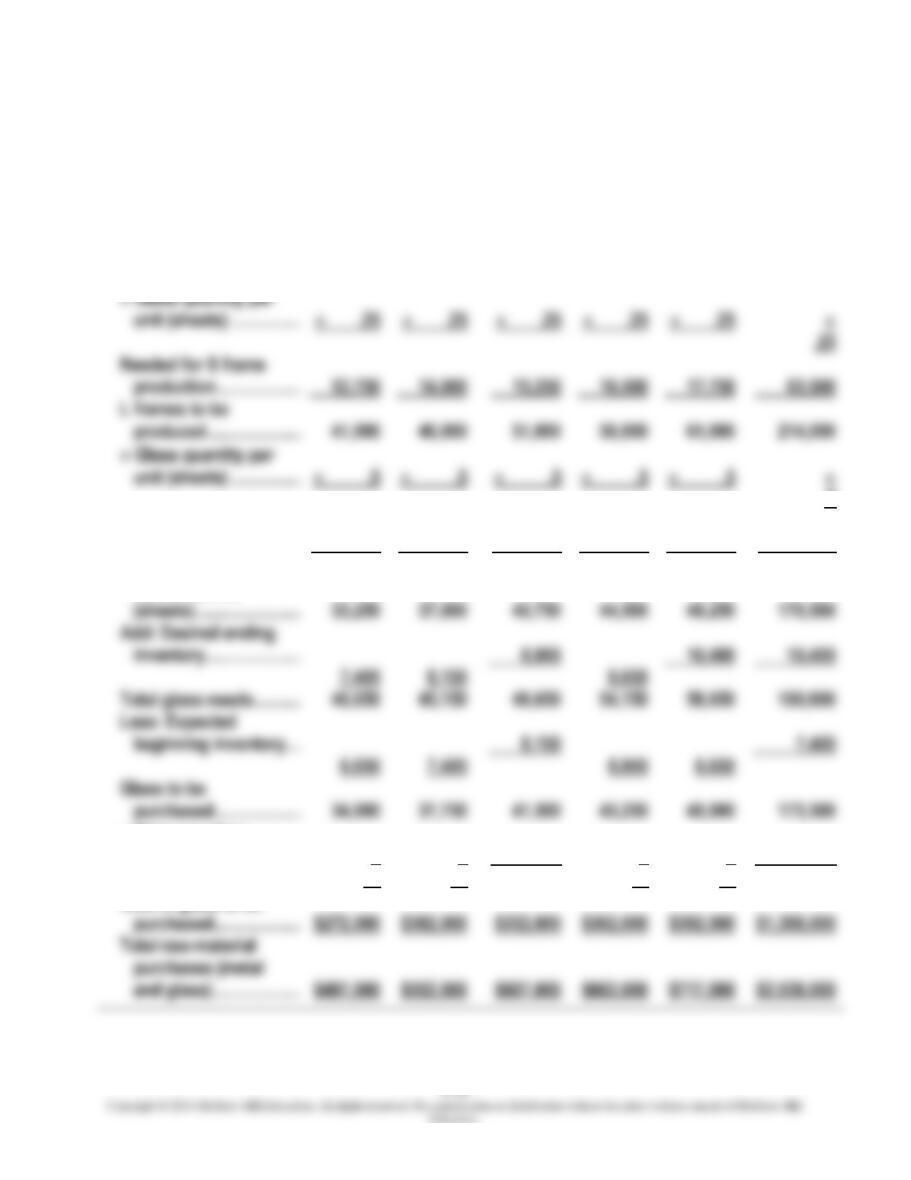

Direct-material budget:*

20×4

20×5

4th

Quarter

1st

Quarter

2nd

Quarter

3rd

Quarter

4th

Quarter

Entire

Year

Metal strips:

S frames to be

produced …………………..

51,000

56,000

61,000

66,000

71,000

254,000

Metal quantity per

unit (ft.) ……………………..

Needed for S frame

L frames to be

Metal quantity per

unit (ft.) ……………………..

3

3

Needed for L frame

be purchased (ft.) ……….

Cost of metal strips to

be purchased: ……………

*Direct-material budget continued on next page.

2

2

Chapter 09 – Financial Planning and Analysis: The Master Budget

CASE 9-45 (CONTINUED)

20×4

20×5

4th

Quarter

1st

Quarter

2nd

Quarter

3rd

Quarter

4th

Quarter

Entire

Year

Glass sheets:

S frames to be

produced …………………..

51,000

56,000

61,000

66,000

71,000

254,000

Glass quantity per

unit (sheets) ………………

Needed for S frame

production …………………

12,750

14,000

15,250

16,500

17,750

L frames to be

Glass quantity per

unit (sheets) ………………

.5

Needed for L frame

production …………………

20,500

23,000

25,500

28,000

30,500

107,000

Add: Desired ending

inventory……………………

Total glass needs ………….

Glass to be

purchased ………………….

34,000

37,750

41,500

45,250

49,000

173,500

Total glass needed

for production

Price per glass

sheet …………………………

$8

$8

$8

$8

$8

$8

purchased ………………….

Cost of glass to be

CASE 9-45 (CONTINUED)

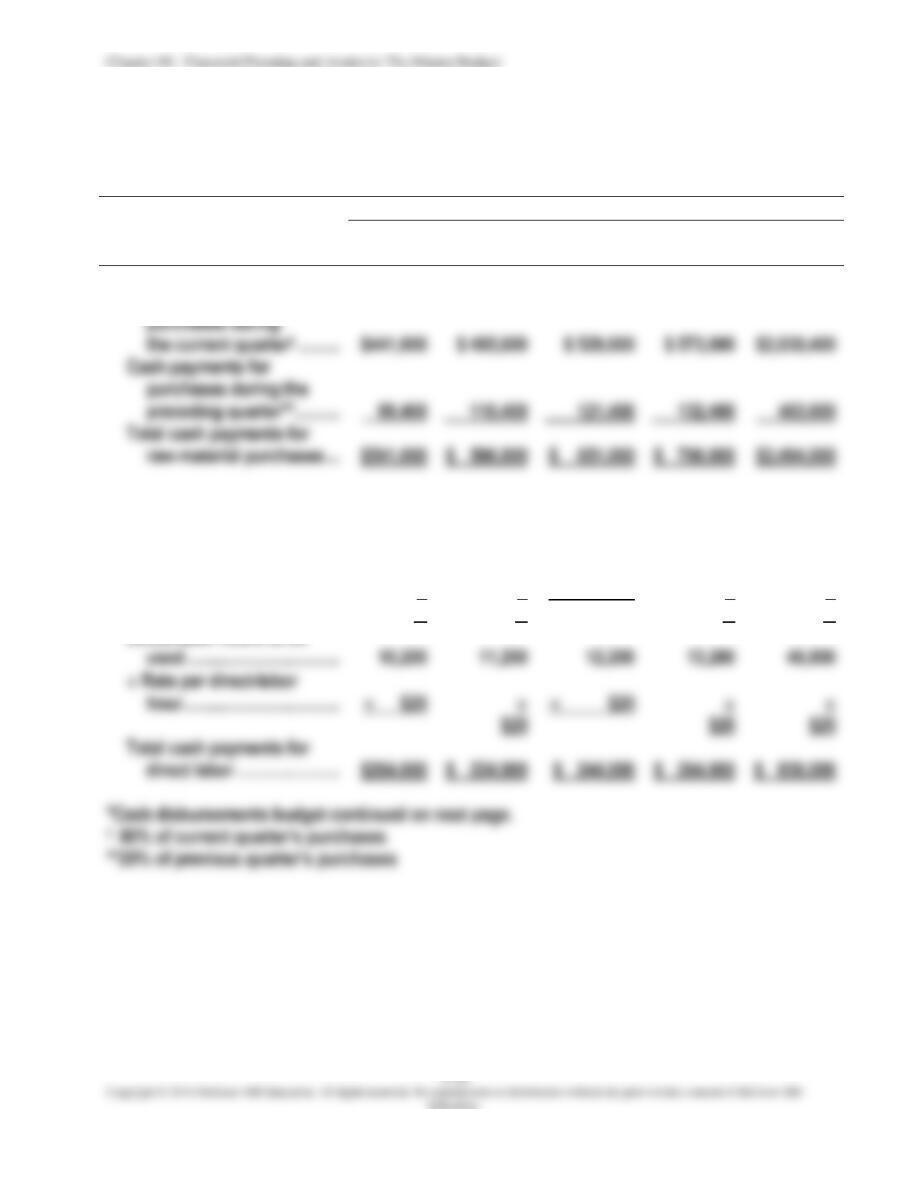

5. Cash disbursements budget:*

205

1st

Quarter

2nd

Quarter

3rd

Quarter

4th

Quarter

Entire

Year

Raw-material purchases:

Cash payments for

Total cash payments for

raw-material purchases …

Cash payments for

Direct labor:

Frames produced

(S and L) ………………………

102,000

112,000

122,000

132,000

468,000

Direct-labor hours per

frame …………………………...

.1

.1

.1

.1

.1

hour ……………………………..

Total cash payments for

*Cash disbursements budget continued on next page.

Direct-labor hours to be

CASE 9-45 (CONTINUED)

1st

Quarter

2nd

Quarter

3rd

Quarter

4th

Quarter

Entire

Year

Production overhead:

Indirect material ………………..

Indirect labor ……………………

Other ………………………………..

Total cash payments for

Chapter 09 – Financial Planning and Analysis: The Master Budget

CASE 9-45 (CONTINUED)

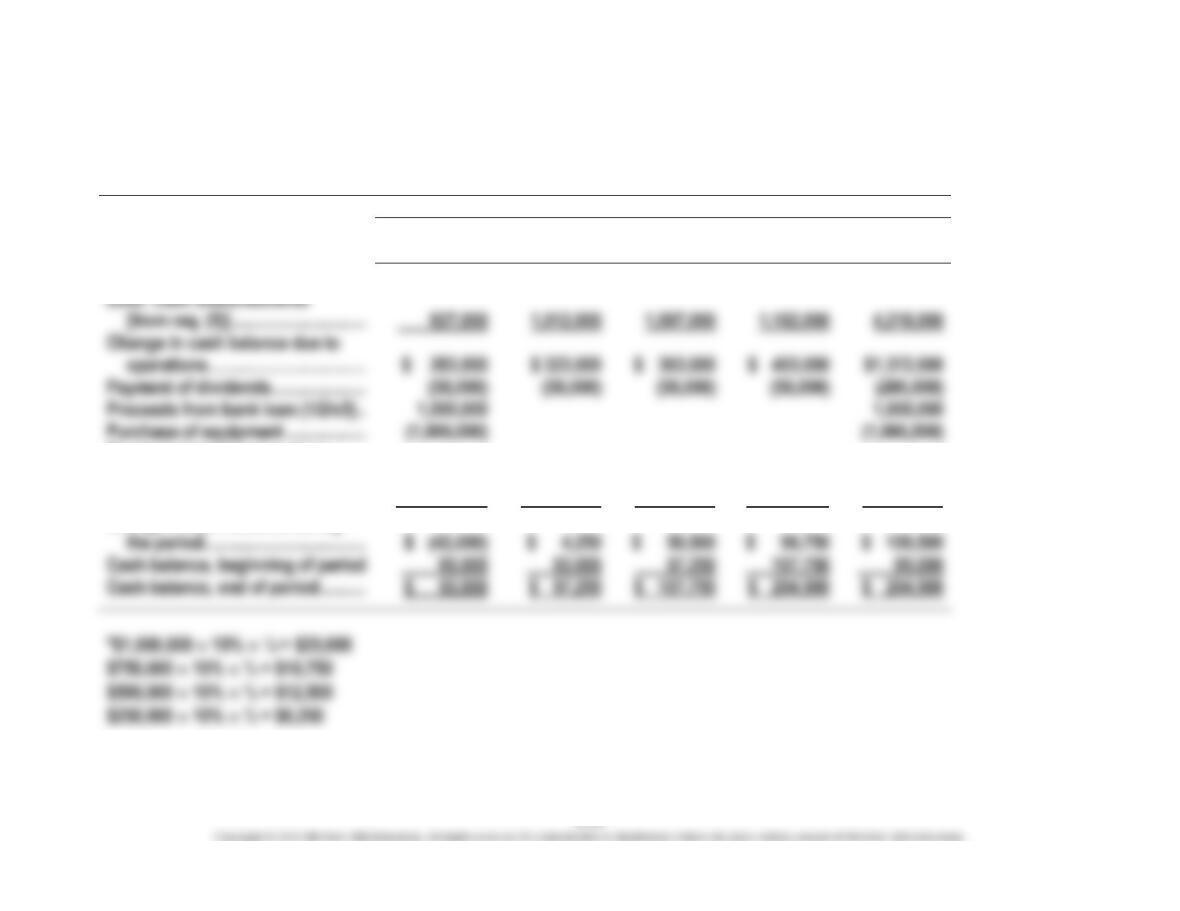

6.

Summary cash budget:

20×5

1st

Quarter

2nd

Quarter

3nd

Quarter

4th

Quarter

Entire

Year

Cash receipts [from req. (2)] ……….

$1,210,000

$1,335,000

$1,460,000

$1,585,000

$5,590,000

Less: Cash disbursements

[from req. (5)] …………………………

Change in cash balance due to

operations ……………………………..

Payment of dividends …………………

Purchase of equipment ………………

Quarterly installment on loan

principal ………………………………..

(250,000)

(250,000)

(250,000)

(250,000)

(1,000,000)

Quarterly interest payment* ………..

(25,000)

(18,750)

(12,500)

(6,250)

(62,500)

the period ………………………………

Cash balance, beginning of period

57,250

95,000

Change in cash balance during

Chapter 09 – Financial Planning and Analysis: The Master Budget

CASE 9-45 (CONTINUED)

7.

PHOTO ARTISTRY COMPANY

BUDGETED SCHEDULE OF COST OF GOODS MANUFACTURED AND SOLD

FOR THE YEAR ENDED DECEMBER 31, 20X5

Direct material:

Raw-material inventory, 1/1/x5 ………………………………………….

$ 59,200

Add: Purchases of raw material [req. (4)] ………………………….

Raw material available for use ………………………………………….

$2,597,200

Raw material used

$2,514,000

Direct labor [req. (5)] ……………………………………………………………..

Production overhead:

Indirect material ………………………………………………………………

Indirect labor …………………………………………………………………..

187,200

Other overhead ……………………………………………………….………

154,000

Depreciation ……………………………………………………….…………..

Total production overhead ……………………………………………….

__ 468,000

*

Cost of goods manufactured …………………………………………………

$3,918,000

†

Add: Finished-goods inventory, 1/1/x5 …………………………………..

Cost of goods available for sale …………………………………………….

$4,085,000

Deduct: Finished-goods inventory, 12/31/x5 …………………………..

Cost of goods sold ……………………………………………………………….

*In the budget, budgeted and applied production overhead are equal. The applied

production overhead may be verified independently as follows:

Total number of frames produced …………………………………….

468,000

Total direct-labor hours ……………………………………………………

Total production overhead applied …………………………………..

**See next page.

Chapter 09 – Financial Planning and Analysis: The Master Budget

CASE 9-45 (CONTINUED)

†The cost of goods manufactured may be verified independently as follows:

S Frames

L Frames

Frames produced …………………………………………………………

254,000

214,000

Total production cost ……………………………………………………

$1,778,000

$2,140,000

**The finished-goods inventory on 12/31/x5 may be verified independently as follows:

S Frames

L Frames

Projected inventory on 12/31/x5 …………………………………….

15,000

13,000

Cost of ending inventory ………………………………………………

††The cost of goods sold may be verified independently as follows:

S Frames

L Frames

Frames sold …………………………………………………………………

250,000

210,000

Cost of goods sold ……………………………………………………….

$1,750,000

$2,100,000

8.

PHOTO ARTISTRY COMPANY

BUDGETED INCOME STATEMENT

FOR THE YEAR ENDED DECEMBER 31, 20X5

Sales revenue ……………………………………………………………..

$5,650,000

Less: Cost of goods sold …………………………………………….

Gross margin ……………………………………………………….……..

$1,800,000

Selling and administrative expenses …………………………....

Interest expense ………………………………………………………….

Net income ………………………………………………………………….

$1,337,500

CASE 9-45 (CONTINUED)

9.

PHOTO ARTISTRY COMPANY

BUDGETED STATEMENT OF RETAINED EARNINGS

FOR THE YEAR ENDED DECEMBER 31, 20X5

Retained earnings, 12/31/x4 ………………………………………………………………

Add: Net income ……………………………………………………………………………….

Deduct: Dividends …………………………………………………………………………….

Retained earnings, 12/31/x5 ………………………………………………………………

10.

PHOTO ARTISTRY COMPANY

BUDGETED BALANCE SHEET

DECEMBER 31, 20X5

Cash ………………………………………………………………………………………………..

$ 204,500

Accounts receivable* ………………………………………………………………………..

192,000

Inventory:

Raw material† ……………………………………………………………………………..

Finished goods …………………………………………………………………………..

235,000

Plant and equipment (net of accumulated depreciation)** …………………..

Total assets ……………………………………………………………………………………..

Accounts payable†† …………………………………………………………………………..

$ 143,400

Common stock ……………………………………………………….………………………..

Retained earnings …………………………………………………………………………….

Total liabilities and stockholders’ equity …………………………………………….

**$8,000,000 + $1,000,000 – $80,000

Chapter 09 – Financial Planning and Analysis: The Master Budget

FOCUS ON ETHICS (See page 382 in the text.)

Is padding the budget unethical? Some accountants argue that budget padding is a

vicious cycle: budgets are padded by lower-level managers because they believe top

management will cut the budget, and budgets are cut by top management because they

believe the submitted budget has been padded by lower-level managers. This situation