EXERCISE 9-13

Alliance Atlantis Communications Inc.’s change of accounting policy to

amortize broadcast rights will probably increase its reported income. Prior

EXERCISE 9-14

(a) A company should depreciate its buildings because depreciation is

necessary in order to allocate the cost of the buildings to the periods

in which they are in use. This allows the cost of the buildings to be

matched against the revenues generated each year in accordance with

the expense recognition principle.

(b) A building can have a zero book value if it has no salvage value and it

is fully depreciated—that is, if it has been used for a period at least as

long as its expected life. Because depreciation is used to allocate cost

EXERCISE 9-14 (Continued)

Trade names and trademarks are reported on a balance sheet if there is

a cost attached to them. If the trade name or trademark is purchased,

EXERCISE 9-15

(a) Asset turnover

$35,497

= = 1.42

($25,633 + $24,244) ÷ 2

times

EXERCISE 9-16

(a)

Without new products

With new products

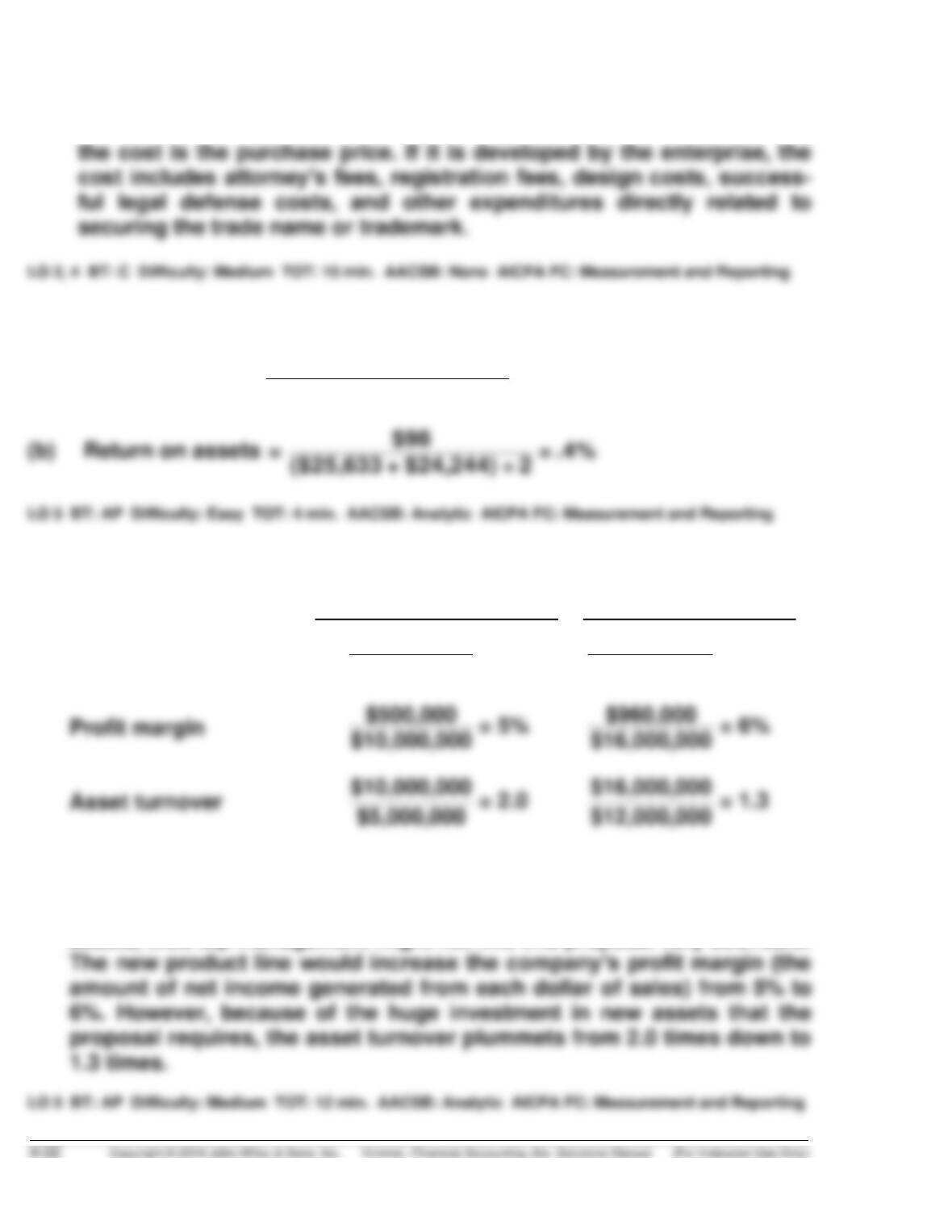

Return on assets

$500,000

= 10%

$960,000

= 8%

$5,000,000

$12,000,000

Profit margin

$16,000,000

$5,000,000

$12,000,000

(b) The return on assets declined from 10% to 8%. This means that the

company is not generating as much income from each dollar invested

in assets. It is common for companies to try to maximize their return on

assets, thus top management might not find this proposal very desirable.

EXERCISE 9-17

(a)

($ in millions)

1. Return on assets

$264.8

= 6.2%

($4,312.6 + $4,254.3) ÷ 2

= 2.7 times

($4,312.6 + $4,254.3) ÷ 2

(b) Profit Margin X Asset Turnover = Return on Assets

(c) Asset turnover and profit margin vary considerably across industries.

Therefore, when you have a diverse group of businesses from several

industry types combined into one company, such as in Linley Com–

EXERCISE 9-18

Net Income

10-year life

15-year life

$58,000

$102,000*

EXERCISE 9-18 (Continued)

The CEO is correct regarding the impact on net income. By increasing the

expected useful life depreciation, expense would be lowered and net income

would increase. However, this move would be appropriate only if, in fact, a

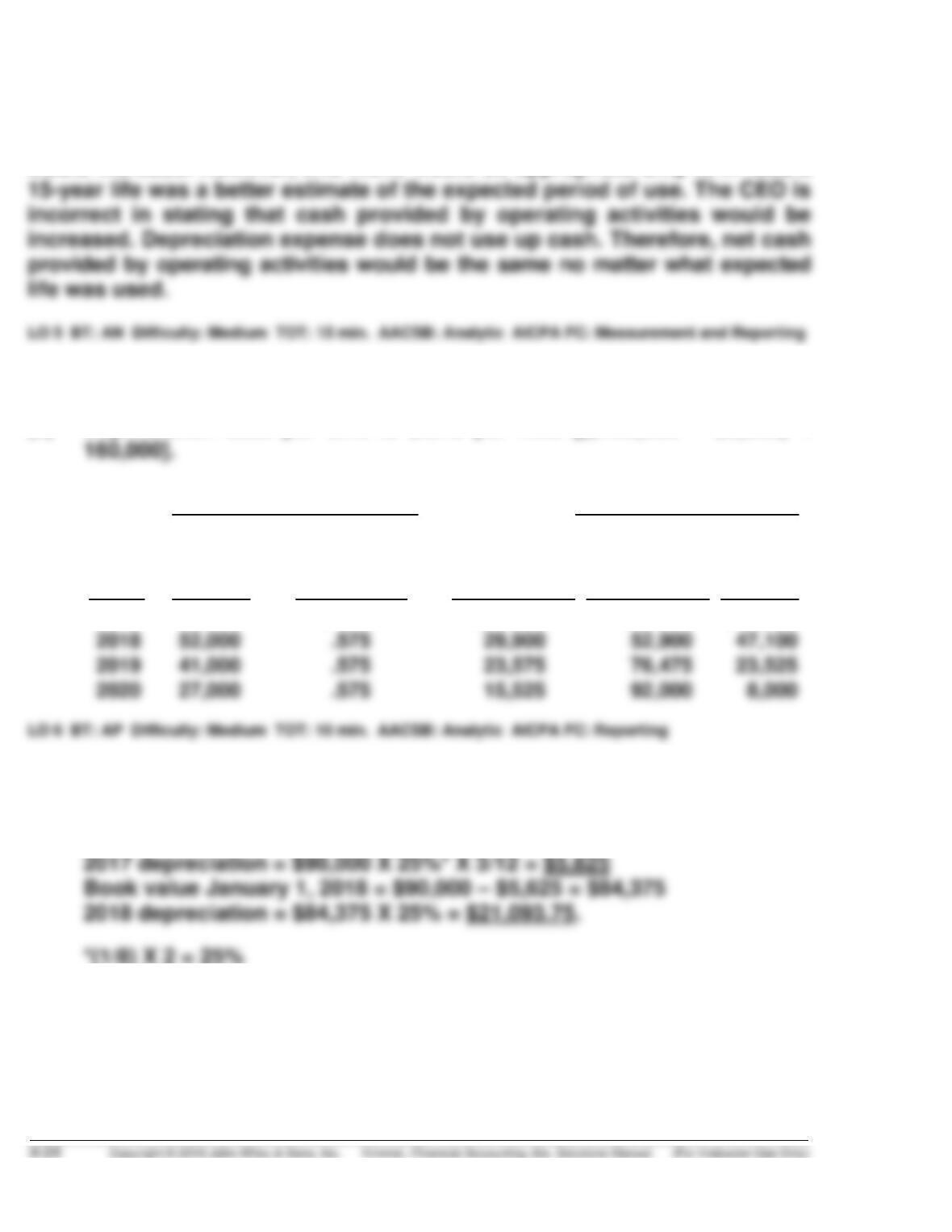

*EXERCISE 9-19

(a) Depreciation cost per unit is $.575 per mile [($100,000 – $8,000) ÷

(b) Computation End of Year

Annual

Units of Depreciation Depreciation Accumulated Book

Years Activity X Cost/Unit = Expense Depreciation Value

2017 40,000 $.575 $23,000 $23,000 $77,000

*EXERCISE 9-20

(a) Declining-balance method:

EXERCISE 9-20 (Continued)

(b) Units-of-activity method:

$90,000– $8,000 = $1.17 per hour

70,000

SOLUTIONS TO PROBLEMS

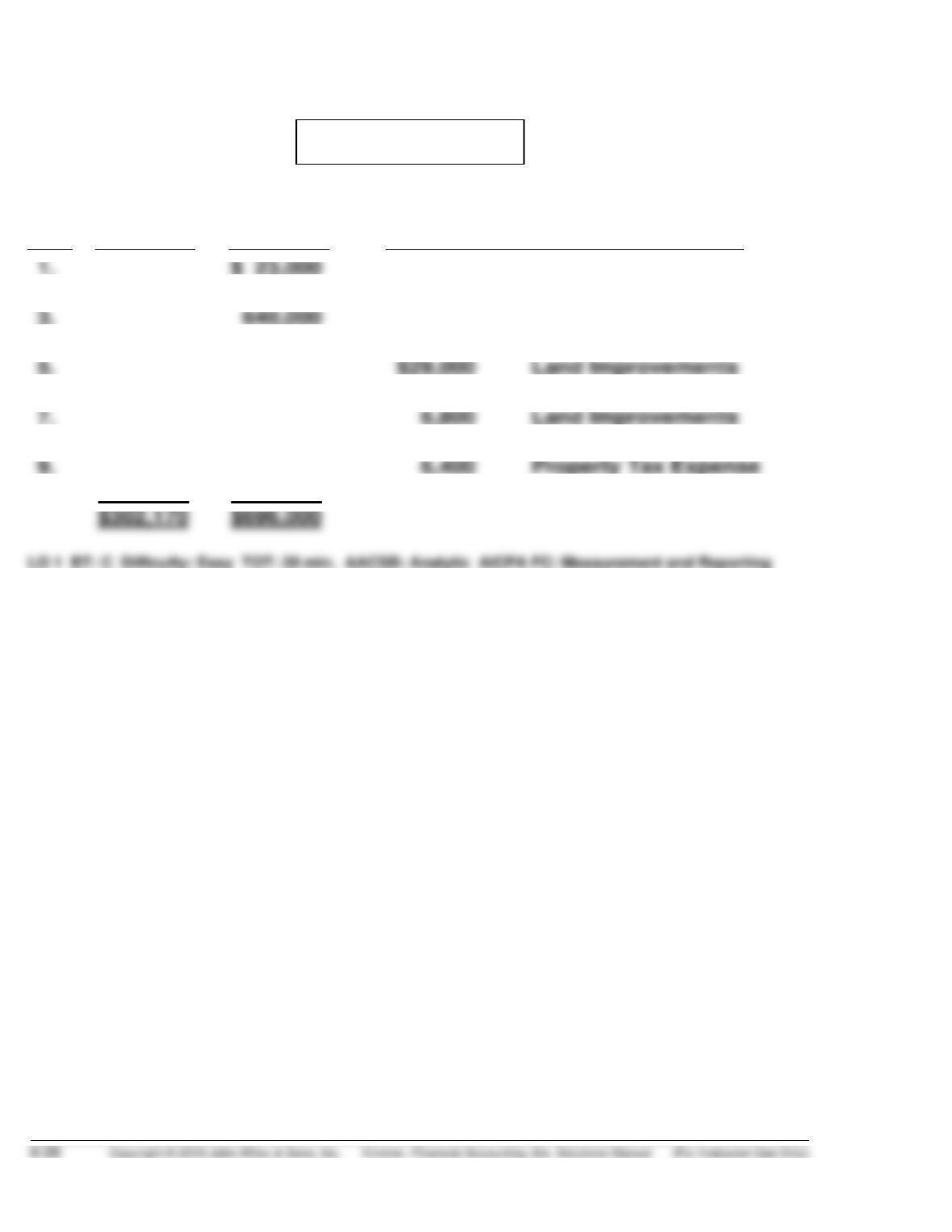

Item Land Building Other Accounts

2. 33,000

4. $280,000

6. 3,170

8. 31,000

10. (12,000)

PROBLEM 9-1A

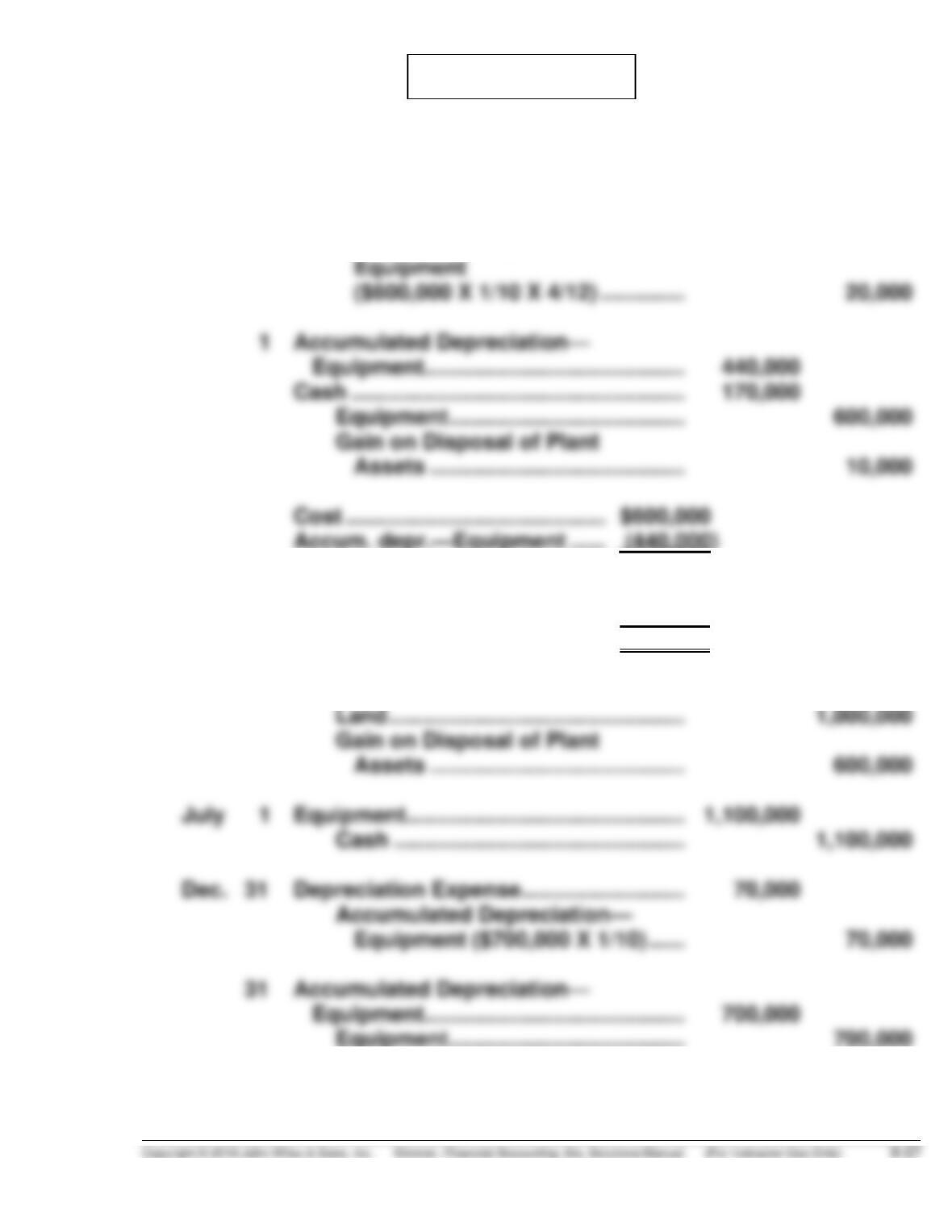

(a) April 1 Land ………………………………………………. 2,200,000

Cash ………………………………………… 2,200,000

May 1 Depreciation Expense ……………………… 20,000

Accumulated Depreciation—

[($600,000 X 1/10) X 7 + $20,000)]

Book value ………………………….. 160,000

Cash proceeds ……………………. 170,000

Gain on disposal …………………. $ 10,000

June 1 Cash ………………………………………………. 1,600,000

PROBLEM 9-2A

PROBLEM 9-2A (Continued)

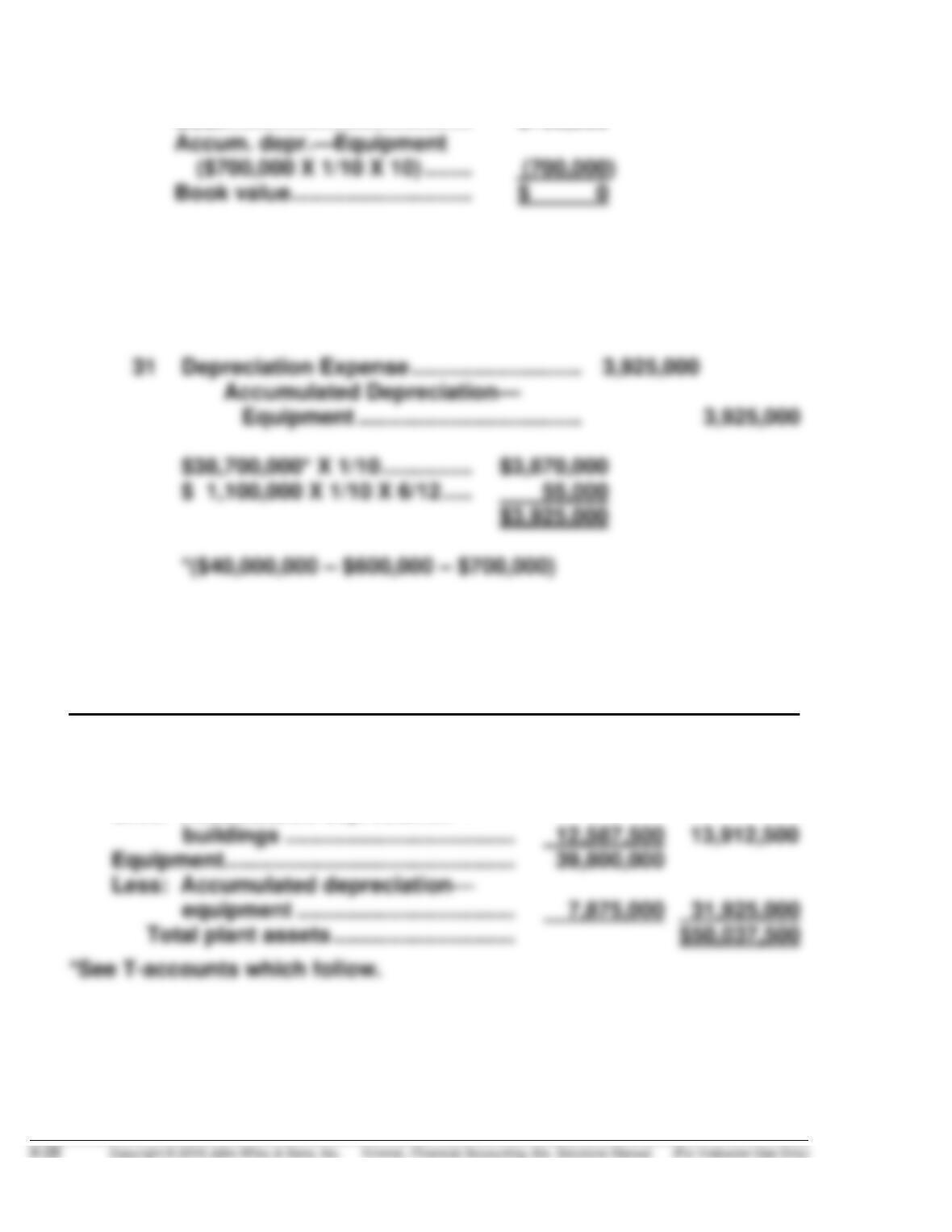

Cost ………………………………….. $700,000

(b) Dec. 31 Depreciation Expense ………………………. 662,500

Accumulated Depreciation—

Buildings ($26,500,000 X 1/40)….. 662,500

(c) ARNOLD CORPORATION

Partial Balance Sheet

December 31, 2018

Plant Assets*

Land ………………………………………………… $ 4,200,000

Buildings ………………………………………….. $26,500,000

Less: Accumulated depreciation—

PROBLEM 9-2A (Continued)

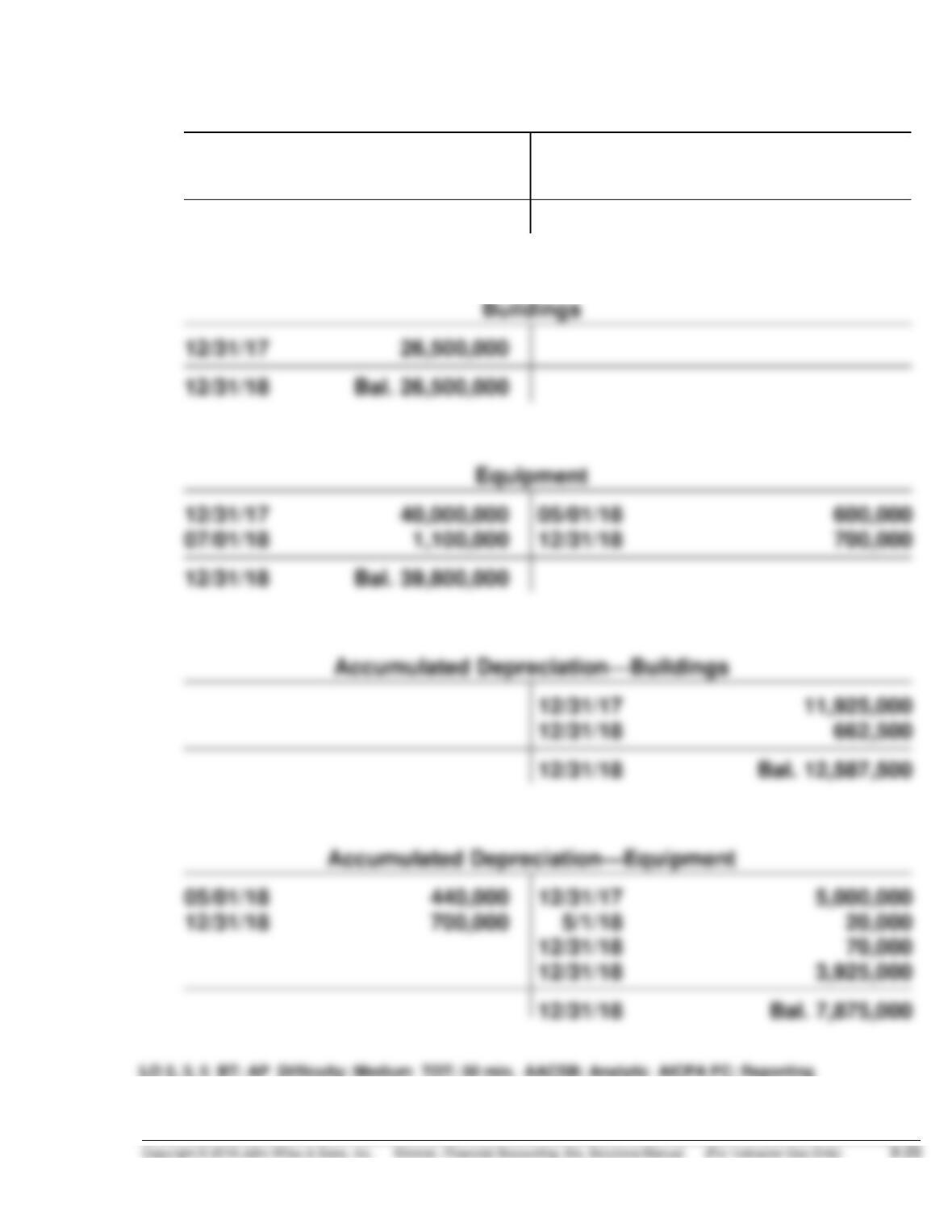

Land

12/31/17 3,000,000 6/1/17 1,000,000

04/01/18 2,200,000

12/31/18 Bal. 4,200,000

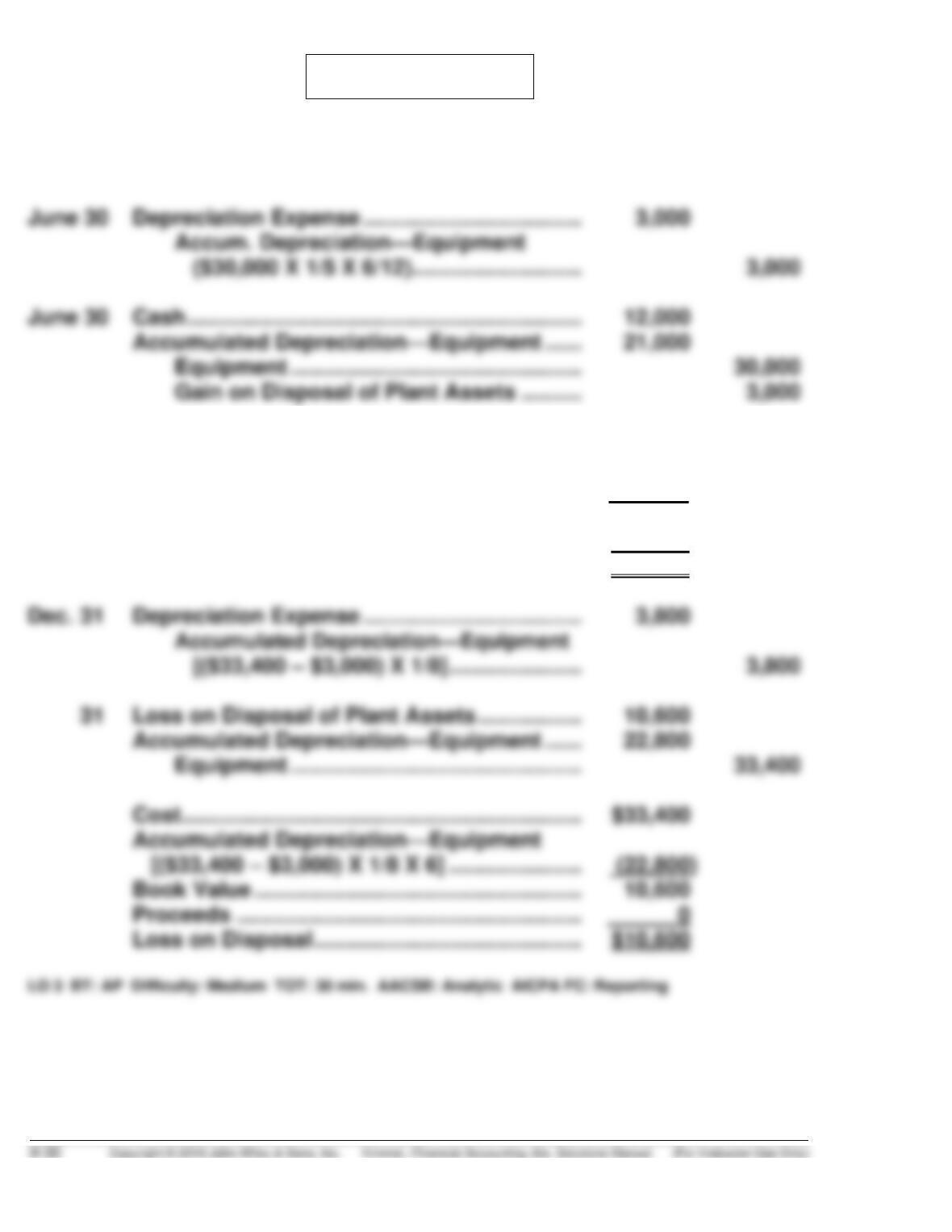

Jan. 1 Accumulated Depreciation—Equipment …… 71,000

Equipment ………………………………………… 71,000

Cost ………………………………………………………… $30,000

Accumulated Depreciation—Equipment

[($30,000 X 1/5) X 3 + $3,000] …………………. (21,000)

Book Value ……………………………………………… 9,000

Cash Proceeds ………………………………………… 12,000

Gain on Disposal …………………………………….. $ 3,000

PROBLEM 9-3A

(a) April 1 Land ……………………………………………………… 4,400,000

Cash ……………………………………………… 1,100,000

Mortgage Payable …………………………... 3,300,000

1 Cash ……………………………………………………… 300,000

Accumulated Depreciation—Equipment …. 2,333,333

Loss on Disposal …………………………………… 166,667

Equipment ……………………………………… 2,800,000

PROBLEM 9-4A

PROBLEM 9-4A (Continued)

(b) Dec. 31 Depreciation Expense ……………………………… 2,435,000

Accumulated Depreciation—Buildings . 2,435,000

($97,400,000 ÷ 40 = $2,435,000)

31 Depreciation Expense ……………………………… 14,730,000

Accumulated Depreciation—Equipment 14,730,000

(c)

YOUNGSTOWN Company

Statement of Financial Position (Partial)

December 31, 2017

Property, plant, and equipment1

Land ………………………………………………………… $ 23,000,000

Buildings …………………………………………………. $97,400,000

Less: Accumulated depreciation ………………. 64,635,000 32,765,000

PROBLEM 9-4A (Continued)

(c) (Continued)

Land

Jan. 1, 2017 20,000,000 June 1, 2017 1,400,000

Buildings

Jan. 1, 2017 97,400,000

Dec. 31, 2017 Bal. 97,400,000

Equipment

Jan. 1, 2017 150,000,000 May 1, 2017 2,800,000

Accumulated Depreciation—Buildings

Jan. 1, 2017 62,200,000

Dec. 31, 2017 2,435,000

Dec. 31, 2017 Bal. 64,635,000

Accumulated Depreciation—Equipment

(a) Jan. 2 Patents …………………………………………………. 46,800

Cash ……………………………………………….. 46,800

Jan.– Research and Development Expense …….. 230,000

June Cash ……………………………………………….. 230,000

(b) Dec. 31 Amortization Expense …………………………... 11,700

Patents ……………………………………………. 11,700

[($60,000 X 1/10) + ($46,800 X 1/9) +

($20,000 X 1/20 X 6/12)]

(c) Intangible Assets

Patents ($126,800 cost less $17,700 amortization) (1) ……… $109,100

Copyrights ($236,000 cost less $29,800 amortization) (2) …. 206,200

(d) The intangible assets of Amato Corporation consist of two patents

and two copyrights. One patent with a cost of $60,000 is being amor-

PROBLEM 9-5A

1. Research and Development Expense …………………… 160,000

Patents ……………………………………………………….. 160,000

2. Goodwill …………………………………………………………….. 2,000

(a) Blythe Jacke

1.

$240,000 $300,000

Return on assets = 7.5% = 10.0%

2.

Profit margin = 20.9% = 25.0%

3.

Asset turnover = .36 times = .40 times

$3,200,000 $3,000,000

(b) Based on the asset turnover, Jacke Corp. is more effective in using

assets to generate sales. Its asset turnover is 11% higher than

Blythe’s ratio.

A factor that inhibits comparing the two companies is the differing

PROBLEM 9-7A

(a) Accumulated

Depreciation

Year Computation 12/31

MACHINE 1

2015 $84,000* X 1/8 = $10,500 $10,500

MACHINE 2

2016 $85,000 X 40%* X 6/12 = $17,000 $17,000

MACHINE 3

2016 800 X $2.00a = $ 1,600 $ 1,600

(b) Year Depreciation Expense

MACHINE 2

2016 $85,000 X 40% X 9/12 = $25,500

PROBLEM 9-8A

(a) STRAIGHT-LINE DEPRECIATION

Computation End of Year

Annual

Depreciable Depreciation Depreciation Accumulated Book

Years Cost X Rate = Expense Depreciation Value

2017 $220,000* 25%** $ 55,000 $ 55,000 $195,000

DOUBLE-DECLINING-BALANCE DEPRECIATION

Computation End of Year

Book Value Annual

Beginning Depreciation Depreciation Accumulated Book

Years of Year X Rate = Expense Depreciation Value

2017 $250,000 50%* $125,000 $125,000 $125,000

(b) Straight-line depreciation provides the lower amount for 2017 deprecia-

tion expense ($55,000) and, therefore, the higher 2017 income. Over the

(c) Double-declining-balance depreciation provides the higher amount

*PROBLEM 9-9A

ACR9-1 ACCOUNTING CYCLE REVIEW

(a) Dec. 2 Equipment ……………………………………………. 16,800

Cash ………………………………………………… 16,800

2 Depreciation Expense …………………………... 825

Accumulated Depreciation—

15 Accounts Receivable …………………………….. 5,000

Sales Revenue …………………………………. 5,000

Cost of Goods Sold ………………………………. 3,500

Inventory …………………………………………. 3,500

23 Salaries and Wages Expense ………………… 6,600

Cash ………………………………………………… 6,600

31 Bad Debt Expense ($4,000 – $500) …………. 3,500

Allowance for Doubtful Accounts ……… 3,500

Interest Receivable

ACR 9-1 (Continued)

Depreciation Expense ……………………………… 250

Accumulated Depreciation—Equipment

[($16,800 – $1,800) ÷ 5] X 1/12 …………… 250