Chapter 9 – Long-Term Liabilities

Requirement 5

The debt to equity ratio will not be in violation (exceed 2.0) under an operating lease,

but will be in violation (exceed 2.0) under a capital lease. Therefore, Thrillville has a

strong incentive to structure the lease agreement as an operating lease.

Operating lease:

Total

Liabilities

÷

Stockholders’

Equity

=

Debt to Equity Ratio

Capital lease:

Total

Liabilities

÷

Stockholders’

Equity

=

Debt to Equity Ratio

Problem 9-3A (LO 9-5, 9-6)

Requirement 1

Face amount. The issue price is $1,300,000.

Calculator Input

Bond

Characteristics

Key

Amount

Calculator Output

(1)

Date

(2)

Cash

Paid

(3)

Interest

Expense

(4)

Increase in

Carrying

Value

(5)

Carrying

Value

Face Amount

x 3.5% Stated

Rate

Carrying Value

x 3.5% Market

Rate

(3) – (2)

Prior Carrying

Value + (4)

Chapter 9 – Long-Term Liabilities

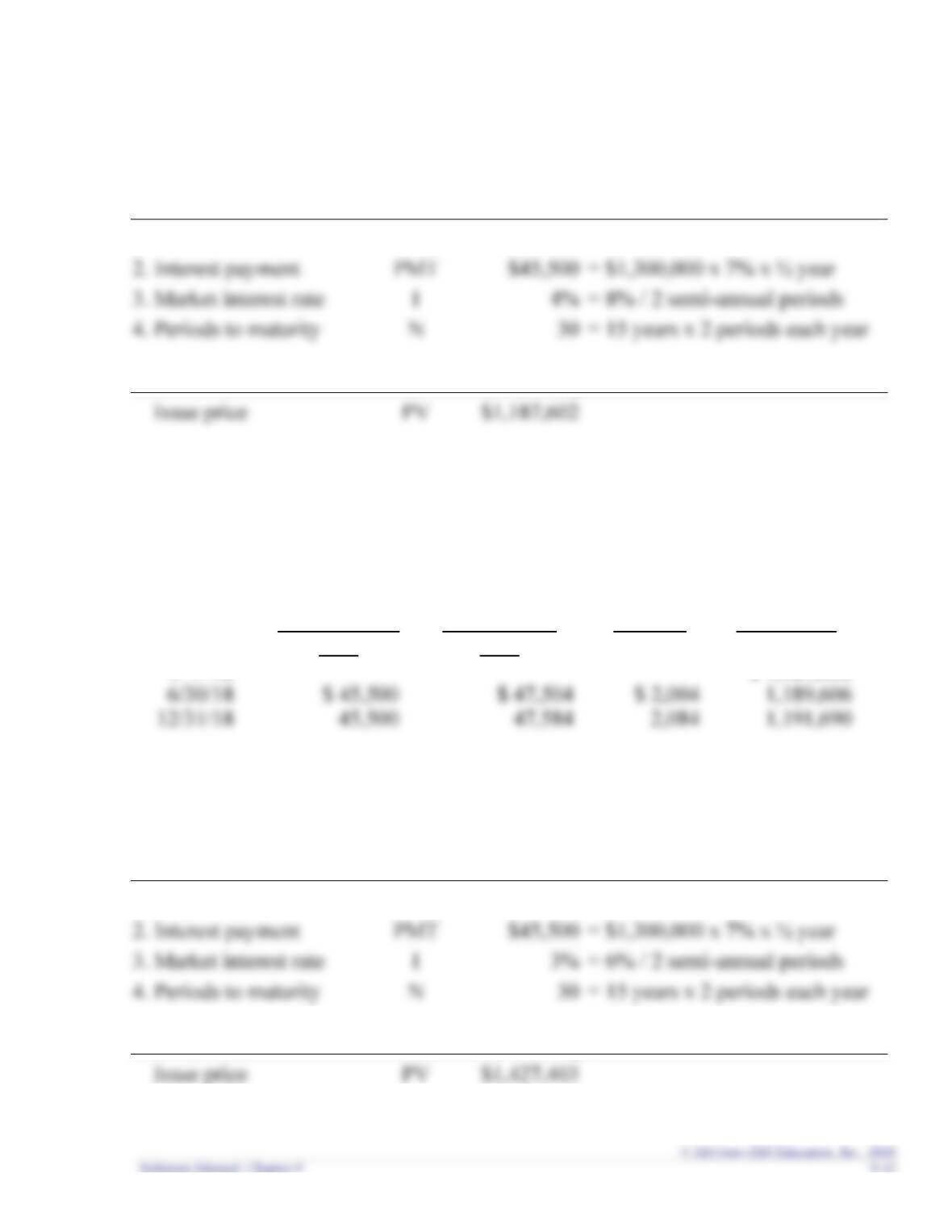

Requirement 2

Discount. The issue price is $1,187,602.

Calculator Input

Bond

Characteristics

Key

Amount

1. Face amount

FV

$1,300,000

2. Interest payment

3. Market interest rate

4. Periods to maturity

Calculator Output

PV

(1)

Date

(2)

Cash

Paid

(3)

Interest

Expense

(4)

Increase in

Carrying

Value

(5)

Carrying

Value

Face Amount

x 3.5% Stated

Rate

Carrying Value

x 4% Market

Rate

(3) – (2)

Prior Carrying

Value + (4)

1/ 1 /18

$ 1,187,602

6/30/18

Requirement 3

Premium. The issue price is $1,427,403.

Calculator Input

Bond

Characteristics

Key

Amount

1. Face amount

FV

$1,300,000

2. Interest payment

3. Market interest rate

4. Periods to maturity

Calculator Output

PV

(1)

Date

(2)

Cash

Paid

(3)

Interest

Expense

(4)

Decrease in

Carrying

Value

(5)

Carrying

Value

Face Amount

x 3.5% Stated

Rate

Carrying Value

x 3% Market

Rate

(2) – (3)

Prior Carrying

Value – (4)

Problem 9-4A (LO 9-6)

Requirement 1

January 1, 2018

Cash

600,000

Bonds Payable

600,000

June 30, 2018

Interest Expense

December 31, 2018

Interest Expense

January 1, 2018

Discount on Bonds Payable

Bonds Payable

June 30, 2018

Chapter 9 – Long-Term Liabilities

Discount on Bonds Payable (difference)

516

Cash ($600,000 x 8% x ½)

December 31, 2018

Interest Expense ([$544,795+$516] x 9% x ½)

24,539

Discount on Bonds Payable (difference)

539

Cash ($600,000 x 8% x ½)

Requirement 3

January 1, 2018

Cash

664,065

June 30, 2018

Interest Expense (664,065 x 7% x ½)

23,242

Cash ($600,000 x 8% x ½)

December 31, 2018

Interest Expense ([$664,065 – $758] x 7% x ½)

23,216

Premium on Bonds Payable (difference)

Cash ($600,000 x 8% x ½)

Problem 9-5A (LO 9-6)

1. Discount

Problem 9-6A (LO 9-6)

Requirement 1

(1)

Date

(2)

Cash

Paid

(3)

Interest

Expense

(4)

Increase in

Carrying

Value

(5)

Carrying

Value

Face Amount

x 4% Stated

Rate

Carrying Value

x 4.5% Market

Rate

(3) – (2)

Prior Carrying

Value + (4)

1/ 1 /18

$ 841,464

845,280

Requirement 2

January 1, 2018

Cash

841,464

Requirement 3

June 30, 2018

Interest Expense ($841,464 x 9% x ½)

37,866

December 31, 2018

Interest Expense ($843,330 x 9% x ½)

37,950

Problem 9-7A (LO 9-8)

Requirement 1

($ in millions)

Total

Liabilities

÷

Stockholders’

Equity

=

Debt to Equity

Ratio

Bahama Bay

$5,724

÷

$3,137

=

1.82

Caribbean Key

÷

=

Requirement 2

($ in millions)

Net

Income

÷

Average

Total Assets

=

Return on

Assets Ratio

Bahama Bay

$562

÷

$9,210.5*

=

6.1%

Caribbean Key

÷

=

Requirement 3

($ in millions)

Net Income +

Interest + Taxes

÷

Interest

=

Times Interest

Earned Ratio

Bahama Bay

$880

÷

$170

=

5.2

Caribbean Key

$166

÷

=

2.4

Chapter 9 – Long-Term Liabilities

PROBLEMS: SET B

Problem 9-1B (LO 9-2)

Requirement 1

January 1, 2018

Building

610,000

Cash

110,000

500,000

Requirement 2

(1)

Date

(2)

Cash

Paid

(3)

Interest

Expense

(4)

Decrease in

Carrying

Value

(5)

Carrying

Value

Monthly

Payment

Carrying Value

x 0.09 x 1/12

(2) – (3)

Prior Carrying

Value – (4)

Requirement 3

January 31, 2018

Interest Expense ($500,000 x 9% x 1/12)

3,750.00

Notes Payable (difference)

1,321.33

Requirement 4

Over the 15 year mortgage, $412,839 is interest expense and $500,000 goes to

Problem 9-2B (LO 9-3, 9-8)

Requirement 1

Assets

=

Liabilities

+

Stockholders’

Equity

$201 million

$91 + $61 = $152 million

?

Requirement 2

Total

Liabilities

÷

Stockholders’

Equity

=

Debt to Equity Ratio

Requirement 3

An operating lease is like a rental. Over the lease term, the company making the lease

payments records rent expense and the company receiving the rent payments records

Requirement 4

Yes. The debt to equity ratio will not be affected under an operating lease. However,

Chapter 9 – Long-Term Liabilities

Requirement 5

The debt to equity ratio will not be in violation under an operating lease, but will be in

violation under a capital lease. Therefore, Chunky Cheese Pizza has a strong incentive

to structure the lease agreement as an operating lease.

Operating lease:

Total

Liabilities

÷

Stockholders’

Equity

=

Debt to Equity Ratio

Capital lease:

Problem 9-3B (LO 9-5, 9-6)

Requirement 1

Face amount. The issue price is $850,000.

Calculator Input

Bond

Characteristics

Key

Amount

$25,500

Calculator Output

(1)

Date

(2)

Cash

Paid

(3)

Interest

Expense

(4)

Increase in

Carrying

Value

(5)

Carrying

Value

Face Amount

x 3% Stated

Rate

Carrying Value

x 3% Market

Rate

(3) – (2)

Prior Carrying

Value + (4)

1/ 1 /18

$ 850,000

850,000

850,000

Chapter 9 – Long-Term Liabilities

Requirement 2

Discount. The issue price is $789,597.

Calculator Input

Bond

Characteristics

Key

Amount

1. Face amount

FV

$850,000

2. Interest payment

3. Market interest rate

4. Periods to maturity

Calculator Output

PV

(1)

Date

(2)

Cash

Paid

(3)

Interest

Expense

(4)

Increase in

Carrying

Value

(5)

Carrying

Value

Face Amount

x 3% Stated

Rate

Carrying Value

x 3.5% Market

Rate

(3) – (2)

Prior Carrying

Value + (4)

Chapter 9 – Long-Term Liabilities

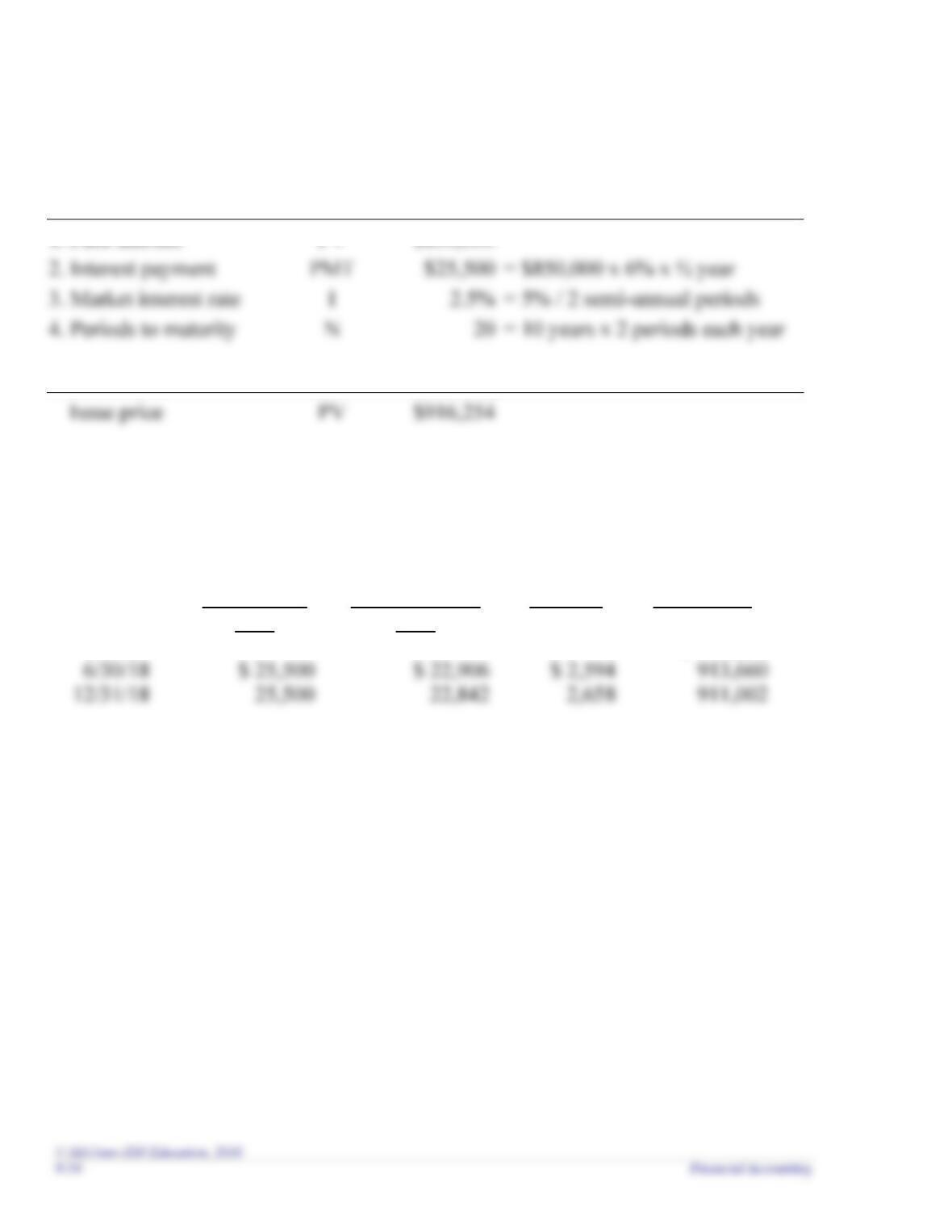

Requirement 3

Premium. The issue price is $916,254.

Calculator Input

Bond

Characteristics

Key

Amount

1. Face amount

FV

$850,000

2. Interest payment

$25,500

3. Market interest rate

4. Periods to maturity

Calculator Output

PV

(1)

Date

(2)

Cash

Paid

(3)

Interest

Expense

(4)

Decrease in

Carrying

Value

(5)

Carrying

Value

Face Amount

x 3% Stated

Rate

Carrying Value

x 2.5% Market

Rate

(2) – (3)

Prior Carrying

Value – (4)

1/ 1 /18

$ 916,254

913,660

911,002