Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

(a) Columbia Sports Wear VF Corporation

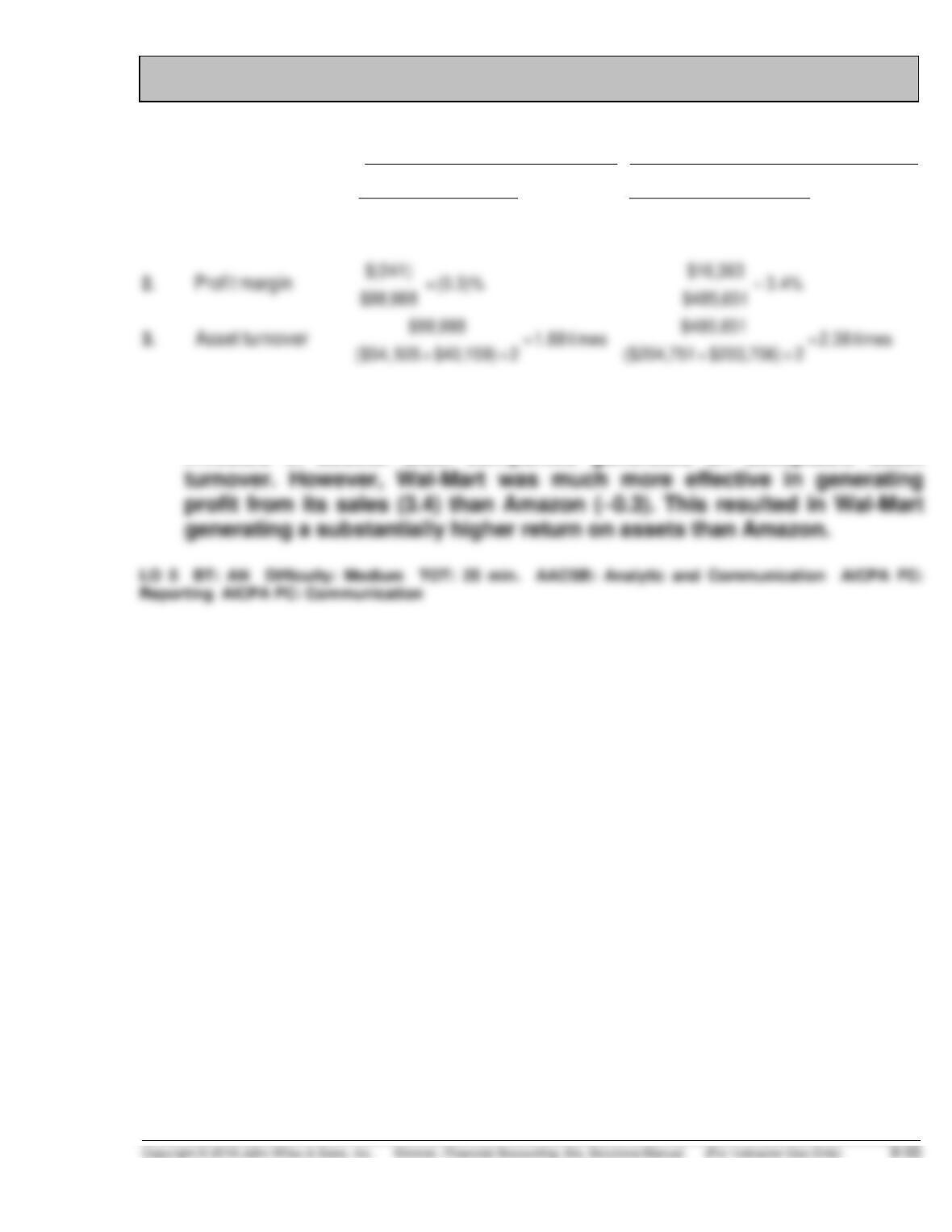

(b) The asset turnover measures how efficiently a company uses its assets

to generate sales. It shows the dollars of sales generated by each dollar

invested in assets. Both companies generated roughly the same asset

turnover. However, VF Corporation was more effective in generating

CT 9-2 COMPARATIVE ANALYSIS PROBLEM

(a) Amazon.com Wal-Mart Stores

1. $(241) $16,363

= (0.5)% = 8.0%

($54,505 + $40,159) / 2 ($204,751 $203,706) ÷2

Return on assets

+

(b) The asset turnover measures how efficiently a company uses its assets

to generate sales. It shows the dollars of sales generated by each dollar

invested in assets. Both companies generated an acceptable asset

CT 9-3 COMPARATIVE ANALYSIS PROBLEM

(a) Online retailers, such as Amazon, have large investments in

sophisticated warehouses, but they have no money tied up in massive

stores, such as those of Best Buy. This is would mean that, all else equal,

an online retailer would have lower total assets, which would increase

2017 2012

(b) Profit Margin

$1,277 = 2.5%

$50,272

$1,140 = 3.7%

$30,848

(c) Profit Margin × Asset Turnover = Return on Assets

2012 3.7% × 2.78 = 10.3

(d) It is interesting to note that the asset turnover stayed the same, at 2.78

times between 2012 and 2017. This means that the company generates

the same amount of sales per dollar invested in assets. However, the

profit margin declined from 3.7% down to 2.5%. This means that the

CT 9-4 INTERPRETING FINANCIAL STATEMENTS

Answers will vary depending on the company chosen by student.

CT 9-5 REAL-WORLD FOCUS

(a) All of the companies have market values (that is, the total market price of

all of their shares) that is less than the shareholders’ equity on their

(b) In most instances, when a company’s market value is less than its book

(c) In order for goodwill to be present on a company’s balance sheet, that

company must have purchased another business. If the amount paid for

(d) The write-down of goodwill as part of an impairment adjustment (or the

write-down of any asset) does not affect cash.

CT 9-6 RESEARCH CASE

(a)

(in thousands)

Current results

Proposed results

without cannibalization

Proposed results

with cannibalization

Return on assets

$12,000

= .12

$13,500

= .135

$12,000

= .12

$100,000

$100,000

$100,000

(b) If there is no cannibalization, return on assets increases from 12% to

13.5%. This occurs even though the profit margin decreases from 27%

to 22.5% because the asset turnover increases significantly, from .45

times to .60 times. However, if there is cannibalization, the return on

(c) Yes, there are other alternatives. Here are some examples.

1. Increase spending on marketing in an effort to increase sales of

2. Consider marketing the new line under a different name, so as to

minimize the cannibalization. This might substantially increase

3. If neither of 1. or 2. seem feasible, they should consider closing a

plant. This would increase the asset turnover and return on

CT 9-7 DECISION MAKING ACROSS THE ORGANIZATION

Answers will depend on the position selected by the student. Some points

that should be considered include:

1. Some relatively small companies may spend less on R&D because they

must expense these costs. However, the vast majority of companies

realize that for continued growth and stability, R&D expenditures are

2. The tangible future benefits of R&D costs may not be realized for

several years, if ever. Conversely, the purchase of a long-lived asset

(i.e., equipment, building) will provide benefits immediately as well as in

CT 9-8 COMMUNICATION ACTIVITY

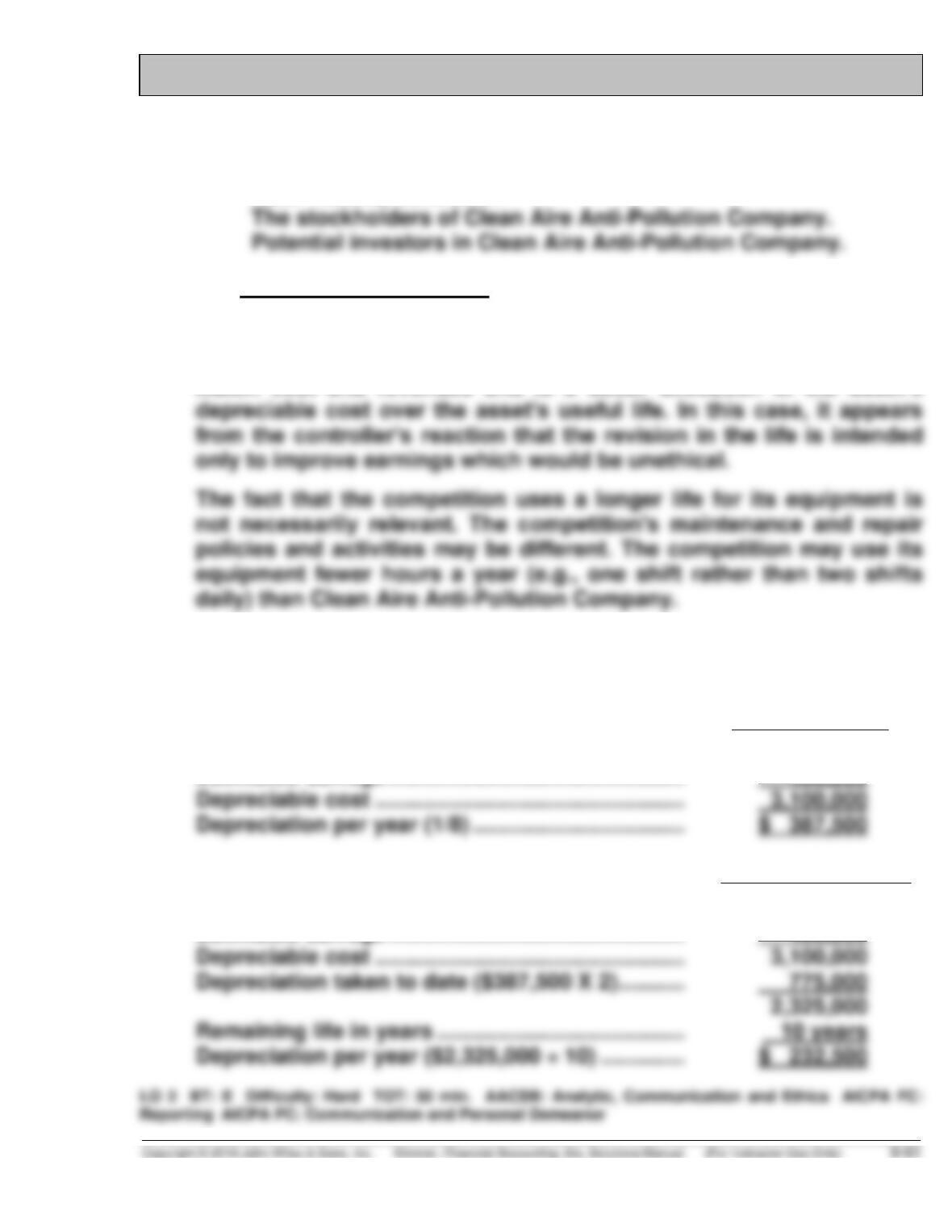

(a) The stakeholders in this situation are:

Wade Truman, president of Clean Aire Anti-Pollution Company.

Kate Rollins, controller.

(b) The intentional misstatement of the life of an asset or the amount of the

salvage value is unethical for whatever the reason. There is nothing

unethical per se about changing the estimates used for the life of an

asset or of an asset’s salvage value if the change is an attempt to better

match cost and revenues and is a better allocation of the asset’s

(c) Income before income taxes in the year of change is increased $155,000

($387,500 – $232,500) by implementing the president’s proposed changes.

Old Estimates

Asset cost .............................................................. $3,500,000

Estimated salvage ................................................. 400,000

Revised Estimates

Asset cost .............................................................. $3,500,000

Estimated salvage ................................................. 400,000

CT 9-9 ETHICS CASE

CT 9-10 ALL ABOUT YOU

(b) For the most part, the value of a brand is not reported on a company’s

balance sheet. Most companies are required to expense all costs related

to the maintenance of a brand name. Also any research and development

that went into the development of the related product is generally

CT 9-11 FASB CODIFICATION ACTIVITY

(a) Capitalize is a term used to indicate that the cost would be recorded as

the cost of an asset. That procedure is often referred to as deferring a

cost, and the resulting asset is sometimes described as a deferred cost.

CT 9-12 CONSIDERING PEOPLE, PLANET AND PROFIT

(a) Airbus developed a wing attachment called a Sharklet that is designed to

reduce fuel consumption. It is quite similar to a device that is sold by

Aviation Partners called a Winglet. Aviation Partners has a patent on the

device. Airbus filed a lawsuit against Aviation Partners claiming that the

IFRS CONCEPTS AND APPLICATION

IFRS9-1

Component depreciation is a method of allocating the cost of a plant asset

IFRS9-2

Revaluation is an accounting procedure that adjusts plant assets to fair value

IFRS9-3

Both types of development expenditures relate to the creation of new products

but one is expensed and the other is capitalized. Development costs incurred

before a new product achieves technological feasibility are recorded as

IFRS9-4 INTERNATIONAL FINANCIAL STATEMENT ANALYSIS

(a) Note 1.13 indicates that “Property, Plant and equipment is

depreciated on a straight-line basis over its estimated useful life; the

estimated useful lives are as follows:

Buildings including investment property

20 to 50 years

(b) Note 5 indicates that “Brands, trade names and other intangible

(c) (1) Per Note 3.1, the balance of Accumulated amortization and

impairment as of December 31, 2014 was 3,506 (EUR millions). (2) Per