Chapter 9 – Long-Term Liabilities

PROBLEMS: SET A

Problem 9-1A (LO 9-2)

Requirement 1

January 1, 2021

Building

360,000

Requirement 2

(1)

Date

(2)

Cash

Paid

(3)

Interest

Expense

(4)

Decrease in

Carrying

Value

(5)

Carrying

Value

$3,483.25

Requirement 3

January 31, 2021

Interest Expense ($300,000 × 7% × 1/12)

1,750.00

Notes Payable (difference)

1,733.25

3,483.25

Requirement 4

Total payments on the loan are $417,990. Since actual payments on the loan are

9-42 Financial Accounting, 5e

Problem 9-2A (LO 9-2)

Requirement 1

January 1, 2021

Cash

2,000,000

Notes Payable

2,000,000

(Issue a note payable)

Requirement 2

Date

Cash

Paid

Interest

Expense

Decrease in

Carrying Value

Carrying

Value

2,000,000

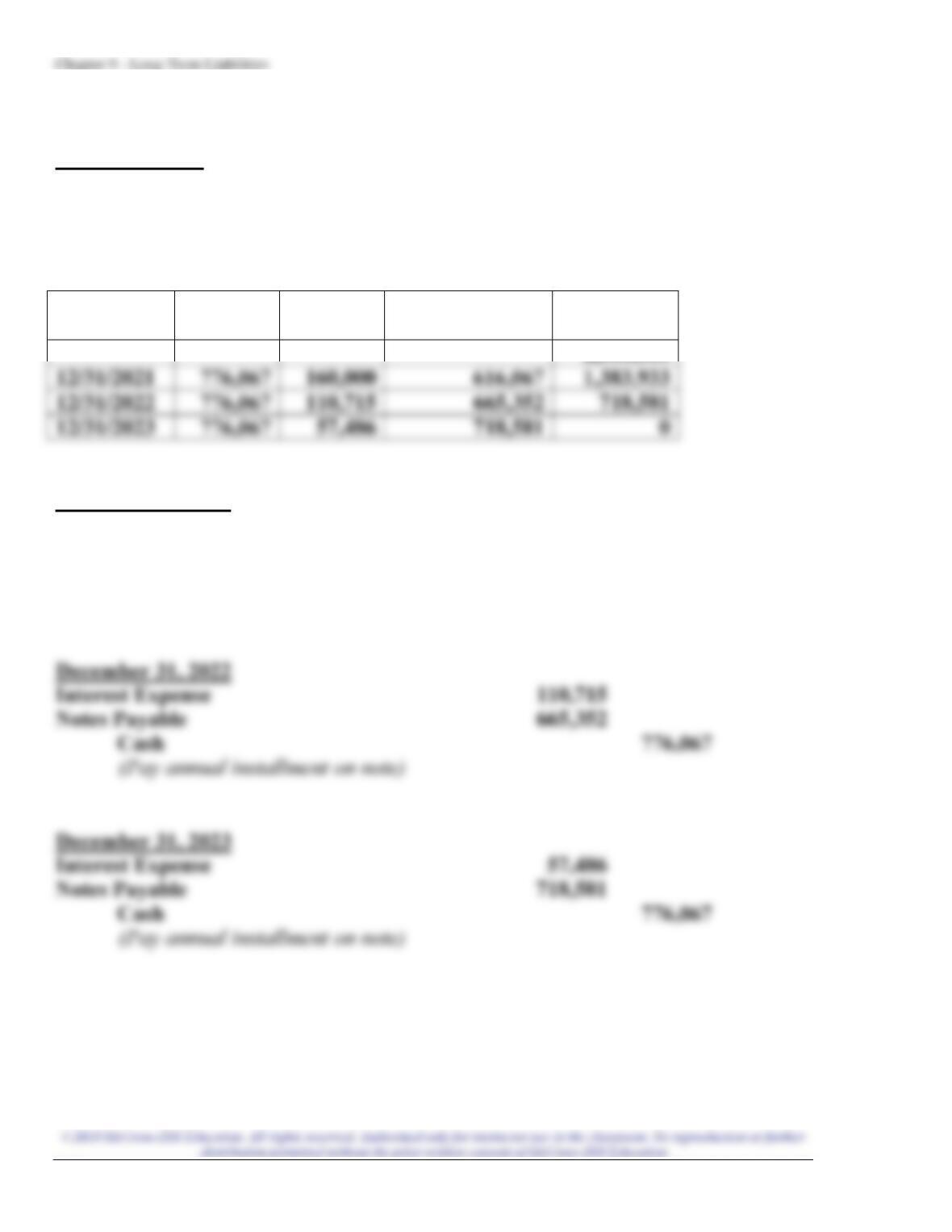

12/31/2021

12/31/2023

Requirement 3

December 31, 2021

Interest Expense

160,000

Notes Payable

616,067

Cash

776,067

(Pay annual installment on note)

December 31, 2022

Interest Expense

Notes Payable

December 31, 2023

Interest Expense

Notes Payable

Chapter 9 – Long-Term Liabilities

Problem 9-3A (LO 9-3, 9-8)

Requirement 1

Assets

=

Liabilities

+

Stockholders’

Equity

Requirement 2

Requirement 3

($ in millions)

Lease Asset

16

Requirement 4

Yes.

The revised debt to equity ratio of 2.34 is greater than the 2.0 ratio required in the

bond agreement.

Total

=

Chapter 9 – Long-Term Liabilities

9-44 Financial Accounting, 5e

Problem 9-4A (LO 9-5)

Requirement 1

January 1, 2021

Cash

600,000

Bonds Payable

600,000

(Issue bonds at face amount)

June 30, 2021

Interest Expense

(Pay semiannual interest)

December 31, 2021

Interest Expense

(Pay semiannual interest)

Requirement 2

January 1, 2021

Cash

544,795

Discount on Bonds Payable

55,205

Bonds Payable

600,000

(Issue bonds at a discount)

June 30, 2021

24,516

December 31, 2021

24,539

(Pay semiannual interest)

Chapter 9 – Long-Term Liabilities

Requirement 3

January 1, 2021

Cash

664,065

Bonds Payable

600,000

Premium on Bonds Payable

64,065

(Issue bonds at a premium)

June 30, 2021

Premium on Bonds Payable (difference)

December 31, 2021

Chapter 9 – Long-Term Liabilities

9-46 Financial Accounting, 5e

Problem 9-5A (LO 9-5)

1. Discount

2. $37,281,935

Chapter 9 – Long-Term Liabilities

Problem 9-6A (LO 9-5)

Requirement 1

(1)

Date

(2)

Cash

Paid

(3)

Interest

Expense

(4)

Increase in

Carrying

Value

(5)

Carrying

Value

Face Amount

Carrying Value

Prior Carrying

Requirement 2

January 1, 2021

Cash

841,464

Requirement 3

June 30, 2021

Interest Expense ($841,464 × 9% × ½)

37,866

December 31, 2021

Interest Expense ($843,330 × 9% × ½)

37,950

Chapter 9 – Long-Term Liabilities

9-48 Financial Accounting, 5e

Problem 9-7A (LO 9-5, 9-7)

Requirement 1

Face amount. The issue price is $1,300,000.

Calculator Input

Bond

Characteristics

Key

Amount

1. Face amount

FV

$1,300,000

2. Interest payment

3. Periods to maturity

PV

(1)

Date

(2)

Cash

Paid

(3)

Interest

Expense

(4)

Increase in

Carrying

Value

(5)

Carrying

Value

Face Amount

Carrying Value

Prior Carrying

Chapter 9 – Long-Term Liabilities

Requirement 2

Discount. The issue price is $1,187,602.

Calculator Input

Bond

Characteristics

Key

Amount

1. Face amount

FV

$1,300,000

2. Interest payment

3. Periods to maturity

4. Market interest rate

PV

(1)

Date

(2)

Cash

Paid

(3)

Interest

Expense

(4)

Increase in

Carrying

Value

(5)

Carrying

Value

Face Amount

Carrying Value

Prior Carrying

Requirement 3

Premium. The issue price is $1,427,403.

Calculator Input

Bond

Characteristics

Key

Amount

1. Face amount

FV

$1,300,000

2. Interest payment

3. Periods to maturity

4. Market interest rate

PV

Chapter 9 – Long-Term Liabilities

(1)

Date

(2)

Cash

Paid

(3)

Interest

Expense

(4)

Decrease in

Carrying

Value

(5)

Carrying

Value

Face Amount

Carrying Value

Prior Carrying

Chapter 9 – Long-Term Liabilities

Problem 9-8A (LO 9-8)

Requirement 1

($ in millions)

Total

Liabilities

÷

Stockholders’

Equity

=

Debt to Equity

Ratio

Bahama Bay

$5,724

÷

$3,137

=

1.82

Caribbean Key

÷

=

Requirement 2

($ in millions)

Net

Income

÷

Average

Total Assets

=

Return on

Assets Ratio

Bahama Bay

$562

÷

$9,210.5*

=

6.1%

Caribbean Key

÷

=

Requirement 3

($ in millions)

Net Income +

Interest + Taxes

÷

Interest

=

Times Interest

Earned Ratio

Bahama Bay

÷

=

Caribbean Key

÷

=

Chapter 9 – Long-Term Liabilities

9-52 Financial Accounting, 5e

PROBLEMS: SET B

Problem 9-1B (LO 9-2)

Requirement 1

January 1, 2021

Building

610,000

500,000

Requirement 2

(1)

Date

(2)

Cash

Paid

(3)

Interest

Expense

(4)

Decrease in

Carrying

Value

(5)

Carrying

Value

Monthly

Payment

Carrying

Value

(2) – (3)

Prior Carrying

Value – (4)

Requirement 3

January 31, 2021

Interest Expense ($500,000 × 9% × 1/12)

3,750.00

Notes Payable (difference)

1,321.33

Requirement 4

Over the 15 year mortgage, $412,839 is interest expense and $500,000 goes to

Chapter 9 – Long-Term Liabilities

Problem 9-2B (LO 9-2)

Requirement 1

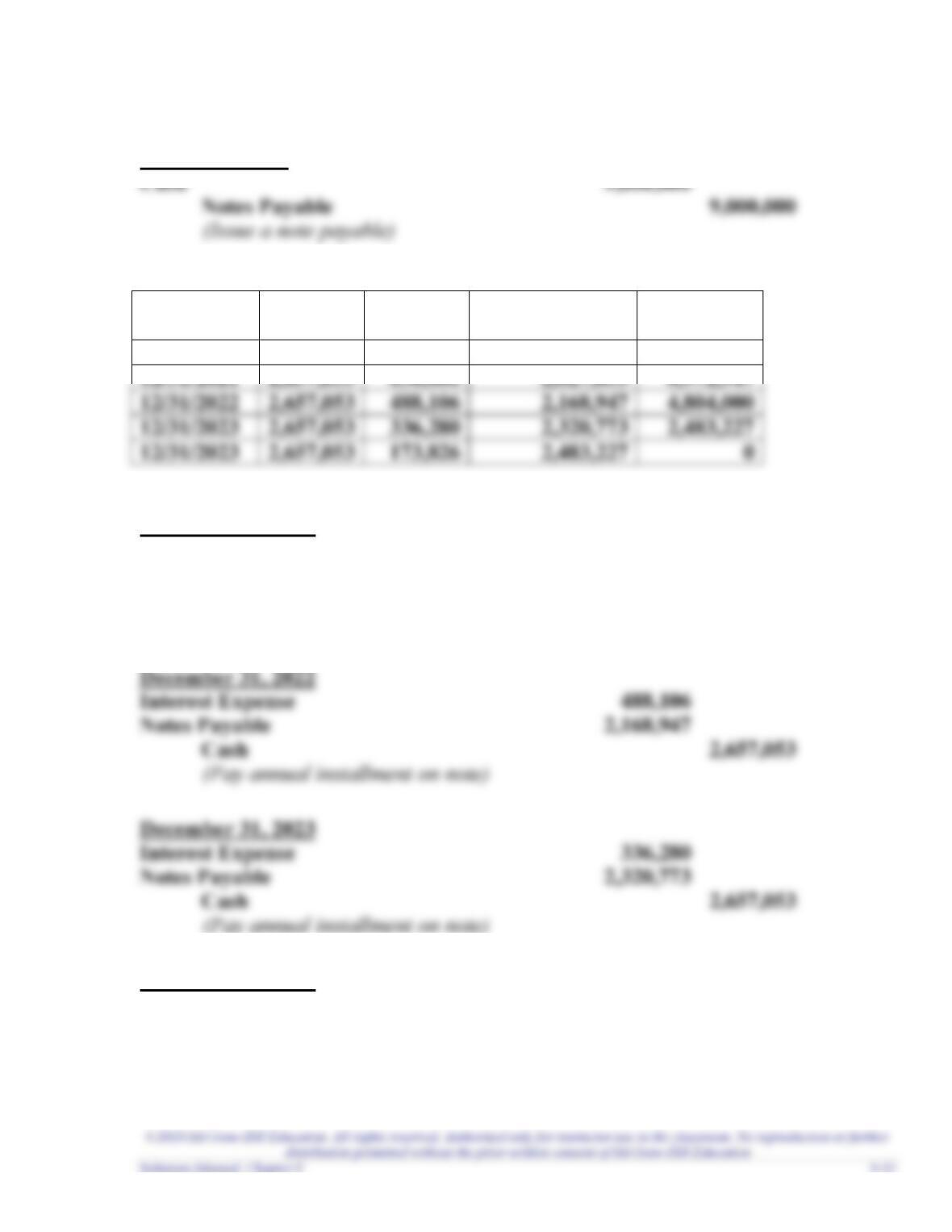

January 1, 2021

Cash

9,000,000

Notes Payable

Requirement 2

Date

Cash

Paid

Interest

Expense

Decrease in

Carrying Value

Carrying

Value

9,000,000

12/31/2021

2,657,053

6,972,947

12/31/2023

2,657,053

2,483,227

12/31/2023

2,657,053

Requirement 3

December 31, 2021

Interest Expense

630,000

Notes Payable

2,027,053

Cash

2,657,053

(Pay annual installment on note)

December 31, 2022

Interest Expense

488,106

Notes Payable

2,168,947

Cash

2,657,053

(Pay annual installment on note)

December 31, 2023

Interest Expense

336,280

Notes Payable

2,320,773

(Pay annual installment on note)

December 31, 2024

Interest Expense

173,826

Notes Payable

2,483,227

Cash

2,657,053

(Pay annual installment on note)

Problem 9-3B (LO 9-3, 9-8)

Requirement 1

Assets

=

Liabilities

+

Stockholders’

Equity

Requirement 2

Total

Liabilities

÷

Stockholders’

Equity

=

Debt to Equity Ratio

$152 million

÷

$49 million

=

3.10

Requirement 3

Requirement 4

Yes.

The revised debt to equity ratio of 3.63 is greater than the 3.25 ratio required in the

bond agreement.

Total

Chapter 9 – Long-Term Liabilities

Problem 9-4B (LO 9-5)

Requirement 1

January 1, 2021

Cash

3,000,000

Bonds Payable

3,000,000

(Issue bonds at face amount)

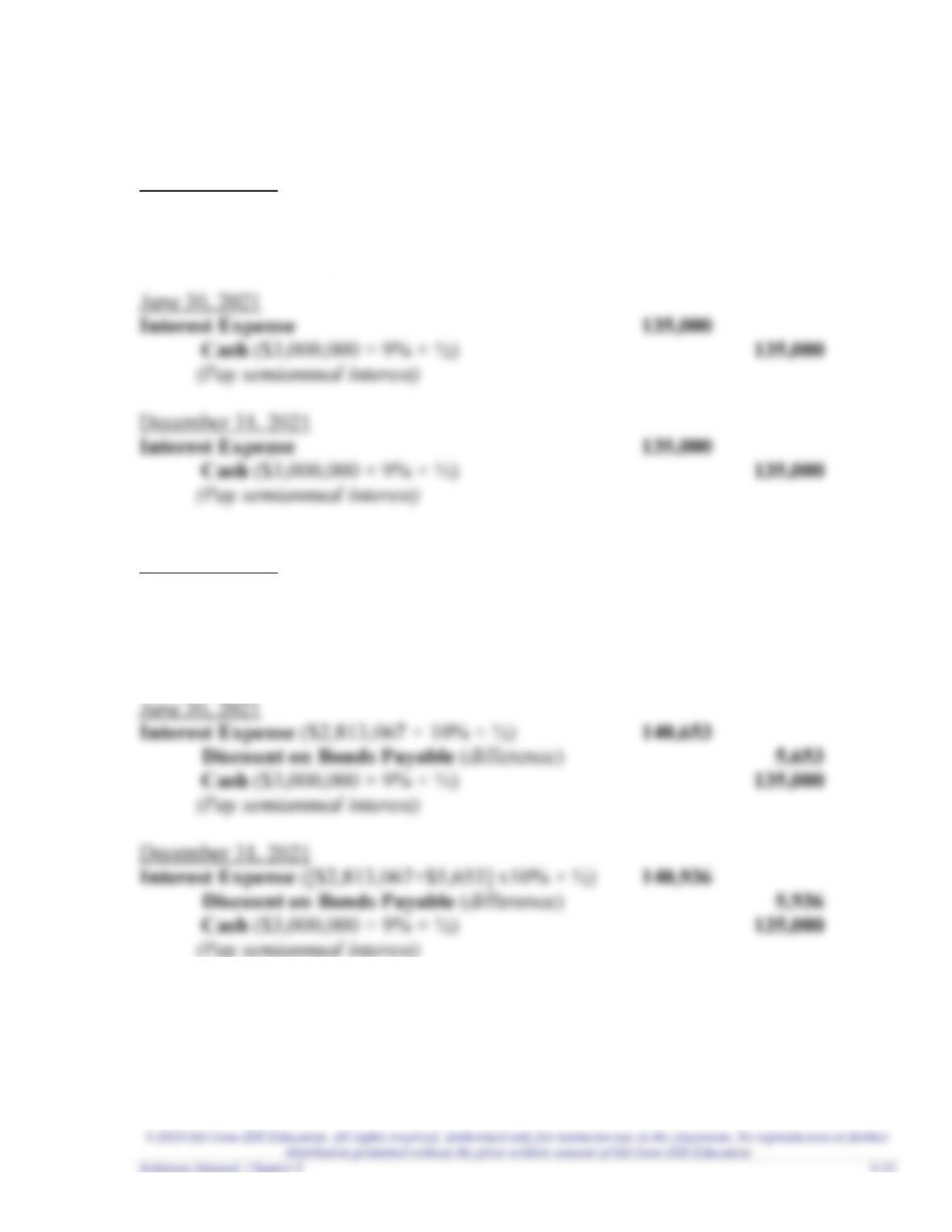

June 30, 2021

Interest Expense

135,000

135,000

(Pay semiannual interest)

December 31, 2021

Interest Expense

135,000

(Pay semiannual interest)

Requirement 2

January 1, 2021

Cash

2,813,067

Discount on Bonds Payable

186,933

Bonds Payable

3,000,000

(Issue bonds at a discount)

June 30, 2021

140,653

135,000

December 31, 2021

140,936

(Pay semiannual interest)

Chapter 9 – Long-Term Liabilities

Requirement 3

January 1, 2021

Cash

3,203,855

Bonds Payable

3,000,000

Premium on Bonds Payable

203,855

(Issue bonds at a premium)

June 30, 2021

128,154

December 31, 2021

127,880

135,000

Problem 9-5B (LO 9-5)

1. Premium

Chapter 9 – Long-Term Liabilities

Problem 9-6B (LO 9-5)

Requirement 1

(1)

Date

(2)

Cash

Paid

(3)

Interest

Expense

(4)

Decrease in

Carrying

Value

(5)

Carrying

Value

Face Amount

Carrying Value

Prior Carrying

Requirement 2

January 1, 2021

Cash

1,098,002

Bonds Payable

1,000,000

Premium on Bonds Payable

Requirement 3

June 30, 2021

Interest Expense ($1,098,002 × 6% × ½)

32,940

Premium on Bonds Payable (difference)

2,060

Interest Expense ($1,095,942 × 6% × ½)

Premium on Bonds Payable (difference)

2,122

Chapter 9 – Long-Term Liabilities

9-58 Financial Accounting, 5e

Problem 9-7B (LO 9-5, 9-7)

Requirement 1

Face amount. The issue price is $850,000.

Calculator Input

Bond

Characteristics

Key

Amount

1. Face amount

FV

$850,000

2. Interest payment

3. Periods to maturity

PV

(1)

Date

(2)

Cash

Paid

(3)

Interest

Expense

(4)

Increase in

Carrying

Value

(5)

Carrying

Value

Face Amount

Carrying Value

Prior Carrying

Chapter 9 – Long-Term Liabilities

Requirement 2

Discount. The issue price is $789,597.

Calculator Input

Bond

Characteristics

Key

Amount

1. Face amount

FV

$850,000

2. Interest payment

3. Periods to maturity

4. Market interest rate

PV

(1)

Date

(2)

Cash

Paid

(3)

Interest

Expense

(4)

Increase in

Carrying

Value

(5)

Carrying

Value

Face Amount

Carrying Value

Prior Carrying