CHAPTER 8

The Time Value of Money

THINKING BEYOND THE QUESTION

How much will it cost to borrow money?

A shorter borrowing period means that a creditor will receive repayment

of a loan sooner than if the borrowing period is longer. Consequently, the

money that is borrowed is at risk over a shorter period. The lender has

QUESTIONS

Q8-1 Future value and present value are based on the concept of interest. Both

recognize that, when invested at a rate of interest, an amount of money

will grow to a larger amount as time passes. Future value is the amount

202 Chapter 8

Q8-2 The concept of future value assumes that money has a time value. It as-

sumes, for example, that a specific amount of money invested today will

Q8-3 The concept of present value assumes that money has a time value. It as-

Q8-4 Any interest factor found on Table 1 reveals the amount that $1 will grow

Q8-5 Each year the interest earned will be larger than the interest earned in the

Q8-6 Table 1 reveals what happens to $1 when it is invested at varying periods

and interest rates. As one moves from the upper left corner of the table to

Q8-7 The problem can be solved in two steps using Table 1 only. First, find the

Q8-8 $572,066.55 FVA = Amount × Interest Factor

Q8-9 Any interest factor found on Table 2 reveals the amount that a $1 ordinary

Q8–10 Table 3 reveals what happens to $1 when it is discounted for varying pe-

riods and rates. In general, the farther (in time) that money is away from

The Time Value of Money 203

Q8–11 The problem can be solved in two steps using Table 3 only. First, dis-

Q8–12 Table 4 reveals what happens to an ordinary annuity of $1 when it is dis-

4. This is correct. But, as the length of the annuity increases, the effect of

the higher discount rate is offset by the effect of the additional annuity

Q8–13 If part of Jeraldo’s capital was returned to him at the end of each year

Q8–14 The rows in time value of money tables (whether in textbooks or pro-

grammed into calculators or computers) represent periods rather than

Q8–15 The size of the monthly payment is fixed at $288. When a payment is

made, the interest incurred since the previous payment is deducted first

and the remainder is subtracted from the balance of the loan. Therefore,

204 Chapter 8

EXERCISES

E8-2 Owed on

March 31, 2008

$26,750

FV = $25,000 × (1.07)1 = $26,750

March 31, 2009

$28,622.50

E8-3 a. The future value $10,000 deposited for 25 years at 6% is computed as

follows:

FVA = A × IF

E8-4 a. The future value of a seven-year, 5%, $2,000 annuity is computed as

follows:

E8-5 a. $1,829,252 Future value of a four-year, 9%, $400,000 annuity:

The Time Value of Money 205

c. The future value of an annuity grows from the contribution of addi-

E8-6 a. $226,566 =FV(0.08, 30, –2,000)

b. $237,991 =FV(0.04, 60, –1,000)

E8-7 $925.93 $1,000 ÷ 1.08 = $925.93 (or $1,000 × 0.92593)

E8-8 $740.74 $800 ÷ 1.08 = $740.74 (or $800 × 0.92593)

E8-9 $952.38 $1,000 ÷ 1.05 = $952.38 (or $1,000 × 0.95238)

E8–10 $600.00 The present value of $802.93 at 6% for five years is $802.93 ×

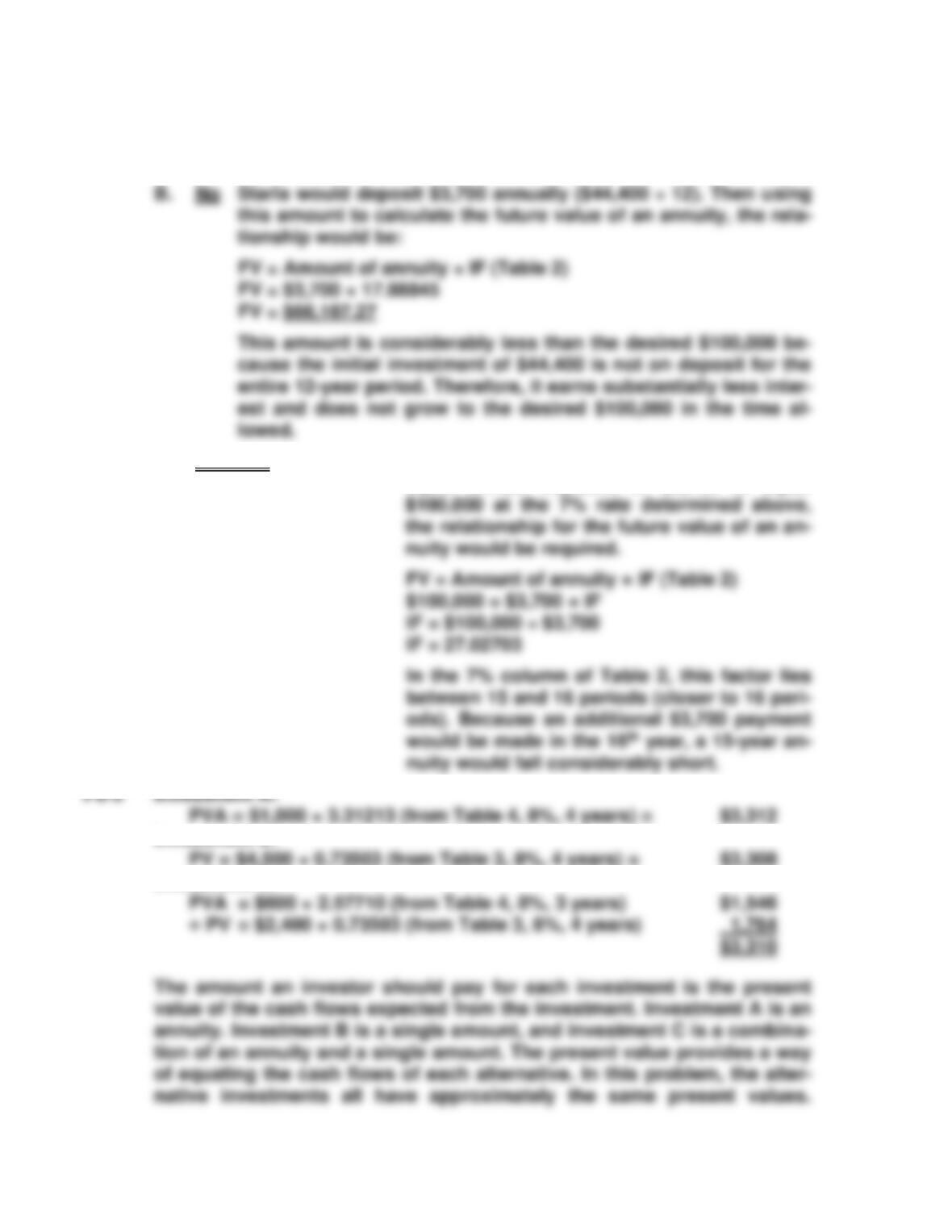

E8–12 $798.54 $200 × 3.99271 (from Table 4, 8%, 5 years) = $798.54

206 Chapter 8

E8–13 a. $408.15 $500 × 0.81630 (from Table 3, 7%, 3 years) = $408.15

E8–14

a. No. The present value of the net cash inflows to be received is less

than the present value of the investment made to obtain those cash

inflows.

Proof:

Expected additional cash inflow per year $50,500

Proof:

To earn exactly 8%, the present value of the future net cash

Current expectations

Expected new cash inflows $ 50,500.00

The Time Value of Money 207

E8–15

b. i. $2,464.51 FV = Amount of annuity × IF (Table 2)

iv. The total of column C is the amount of interest earned over the

six years.

A

B

C

D

E

Year

Value

at Beg.

of Year

Int. Earned

(Col. B ×

Int. Rate)

Amount

Invested at

End of Year

Future Value at

End of Year

(Cols. B + C + D)

0.00

1,413.44

1,878.80

5,212.90

E8–16

a. Present value of Option 1:

= $79,025.80

b. Option 2 is worth more (has a higher present value) even though he

208 Chapter 8

E8–17 a.

Compounding

Frequency

Interest Factor

(Table 1)

Future

Value

Annual

1.25440

$1,254.40

c. The same effect should take place. An annuity is merely a series of

d.

Compounding

Frequency

Interest Factor

(Table 3)

Present

Value

Annual

0.79719

e. The more frequent the compounding period, the smaller is the pre-

f. More frequent compounding reduces the interest earned each peri-

od, but the annuity payments are received more frequently. The total

effect depends on frequency and interest rates.

E8–18 $410.02 (5 years) PVA = $100 × 4.10020 (from Table 4, 5 periods,

The Time Value of Money 209

E8–19 $1,070.24 $80 × 7.02358 (from Table 4, 7%, 10 years) + $1,000 ×

0.50835 (from Table 3, 7%, 10 years) = $561.89 + $508.35 =

pay. At any price above this amount, the company will earn

less than a 12% return on its investment. If the company is

able to pay less than this amount, its rate of return will be

higher than 12%.

b. Year 1 = $90,000 $1,000,000 × 9% = $90,000

Proof:

Period

Present Value

at Beginning

of Period

Interest

Expense

at 9%

Payment

Repayment

of Principal

Value

of Debt at

End of Period

Year 1

$1,000,000

$90,000

$395,055

$305,055

$694,945

210 Chapter 8

c.

ASSETS

=

LIABILITIES

+

OWNERS’ EQUITY

Date

Accounts

Cash

Other

Assets

Contributed

Capital

Retained

Earnings

d.

ASSETS

=

LIABILITIES

+

OWNERS’ EQUITY

Date

Accounts

Cash

Other

Assets

Contributed

Capital

Retained

Earnings

E8–23 a. The size of the payment is solved by the following equation:

b. The loan would be entered into the accounting system as follows:

ASSETS

=

LIABILITIES

+

OWNERS’ EQUITY

The three payments would be entered into the accounting system as

follows:

ASSETS

=

LIABILITIES

+

OWNERS’ EQUITY

Date

Accounts

Cash

Other

Assets

Contributed

Capital

Retained

Earnings

Date

Accounts

Other

Assets

Contributed

Capital

Retained

Earnings

The Time Value of Money 211

ASSETS

=

LIABILITIES

+

OWNERS’ EQUITY

Other

Contributed

Retained

Cash

–18,173

Presentation of an amortization table was not part of the require-

ments. The following table, however, explains the entries to the ac-

counting system above.

Year

Beginning of

Year Balance

Interest

Expense

Cash

Payment

Reduction in

Loan Balance

End of Year

Balance

E8–24

a. PV = Amount × IF

i. $251.89 $300 × 0.83962 (Table 3)

Total $999.48

b. Implications: 1. The present value of an investment decreases as

the time until the investment is received increases.

E8–25

a. $3,851 PV(.11,18,500)

Interest Expense

Loan Payable

212 Chapter 8

PROBLEMS

P8-1

The difference relates to the length of time the money is invested.

Time is a powerful component of the value of money. Even though

an investor may be able to save only small amounts, it is important

to begin investing early rather than wait until later and have to invest

larger amounts or look for higher paying, but riskier investments.

P8-2 Future value of plan #1:

Employee contribution per year $3,000

Future value of plan #2:

Employee contribution per year $2,500

The Time Value of Money 213

Choosing between plan #1 and plan #2:

Effective arguments can be made in favor of either alternative. Plan #1

P8-3

A. Prudence = $16,000 $2,000 on each of 8 birthdays starting

C. $518,113.04 FV annuity = Amount × IF

= $2,000 × IF (40 periods @ 8%)

= $2,000 × 259.05652

= $518,113.04

E. Compound interest is a powerful financial tool when savings are

started early and continue over a long period of time. Here we see

two examples. First, Prudence invested only $16,000 yet ended up

214 Chapter 8

P8–4

A. FV = PV × IF = 44,400 × 2.25219 = 99,997. Almost. She will fall just

short of her goal.

C. 16 years To determine the approximate number of

equal annual deposits of $3,700 to equal

Investment B:

PV = $4,500 × 0.73503 (from Table 3, 8%, 4 years) = $3,308

Investment C:

The Time Value of Money 215

P8-6

Use the future value of the annuity formula in this problem. The

payments can be treated as 10 separate calculations of the future

value of a single amount. The relationship used is: FV = PV × IF (Ta-

ble 1)

Year

PV

Amount

Deposited

Years on

Deposit

IF

Interest

Factor

FV

Future Val-

ue

1

$ 3,000

10

2.36736

$ 7,102.08

2

3,000

9

2.17189

6,515.67

3

3,000

8

1.99256

5,977.68

4

3,000

7

1.82804

5,484.12

5

3,000

6

1.67710

5,031.30

6

3,000

5

1.53862

4,615.86

7

3,000

4

1.41158

4,234.74

8

3,000

3

1.29503

3,885.09

9

3,000

2

1.18810

3,564.30

1

1.09000

$49,680.84

C. The amounts are larger in part B because the amount of interest

earned is greater. The reason for the greater amount of interest is

that each $3,000 IRA contribution was on deposit one extra period.

216 Chapter 8

P8-7

(a)

(b)

(c)

Group

Number

of

employees

Annual

pension

benefit

Years

to be

paid

Cash

required

5

10,000

5

10,000

5

dates. The present value of each group’s benefits, if

payments started at year-end 2007, is obtained by

multiplying column (a) by column (b) by column (c).

do start.

(a)

(b)

(c)

(d)

(e)

(f)

benefit

Annual

pension

PV factor for

5 period

PV @

year-end

PV factor

for 4, 9 or

Year-end

2007 pension

C.

ASSETS

=

LIABILITIES

+

OWNERS’ EQUITY

Date

Accounts

Cash

Other

Assets

Contributed

Capital

Retained

Earnings

P8-8 A. and B.

Monthly rate

(annual ÷ 12)

Number

of periods

Amount

borrowed

Monthly

payment

The Time Value of Money 217

C. Responses will vary. Many students will automatically select the op-

D. Dealer financing (72 payments of $721.21) $51,927.12

E.

Total payments

Amount

borrowed

Interest

Dealer financing

$51,927.12

$35,000

$16,927.12

Bank financing

Credit union financing

P8-9

D. If the Taylors can afford the additional $305.31 per month, they will