218 Chapter 8

Month

Present

Value (Beg.)

Interest

Expense

Total

Payment

Principal

Payment

Value (End)

May

$600,000.00

$6,000.00

$53,309.26

$47,309.26

$552,690.74

June

552,690.74

5,526.90

53,309.26

47,782.36

504,908.38

July

504,908.38

5,049.08

53,309.26

48,260.18

456,648.20

August

456,648.20

4,566.48

48,742.78

407,905.42

September

407,905.42

4,079.05

53,309.26

49,230.21

358,675.21

October

358,675.21

3,586.75

53,309.26

49,722.51

308,952.70

November

308,952.70

3,089.53

53,309.26

50,219.73

258,732.97

December

258,732.97

2,587.33

53,309.26

50,721.93

208,011.04

January

208,011.04

2,080.11

53,309.26

51,229.15

February

1,567.82

53,309.26

51,741.44

105,040.45

March

105,040.45

1,050.40

53,309.26

52,258.86

53,309.26

52,781.44

1Note: Students may observe slight rounding errors between their solutions

and the solutions presented here. Rounding errors typically occur because of

the number of significant digits Excel uses in its calculations.

B. Interest expense for the 2007 fiscal year would be the sum of interest

rate applies to the other years also.

The Time Value of Money 219

P8–12 A. $147,763 PVA = Payment × Interest factor

B. The amortization table follows.

Period

Amount

Interest at

5%

Payment

Payment of

Principal

Balance

at End of

Period

Year 2007

$750,000

$37,500

$147,763

$110,263

$639,737

Year 2008

Year 2009

Year 2010

Year 2011

Year 2012

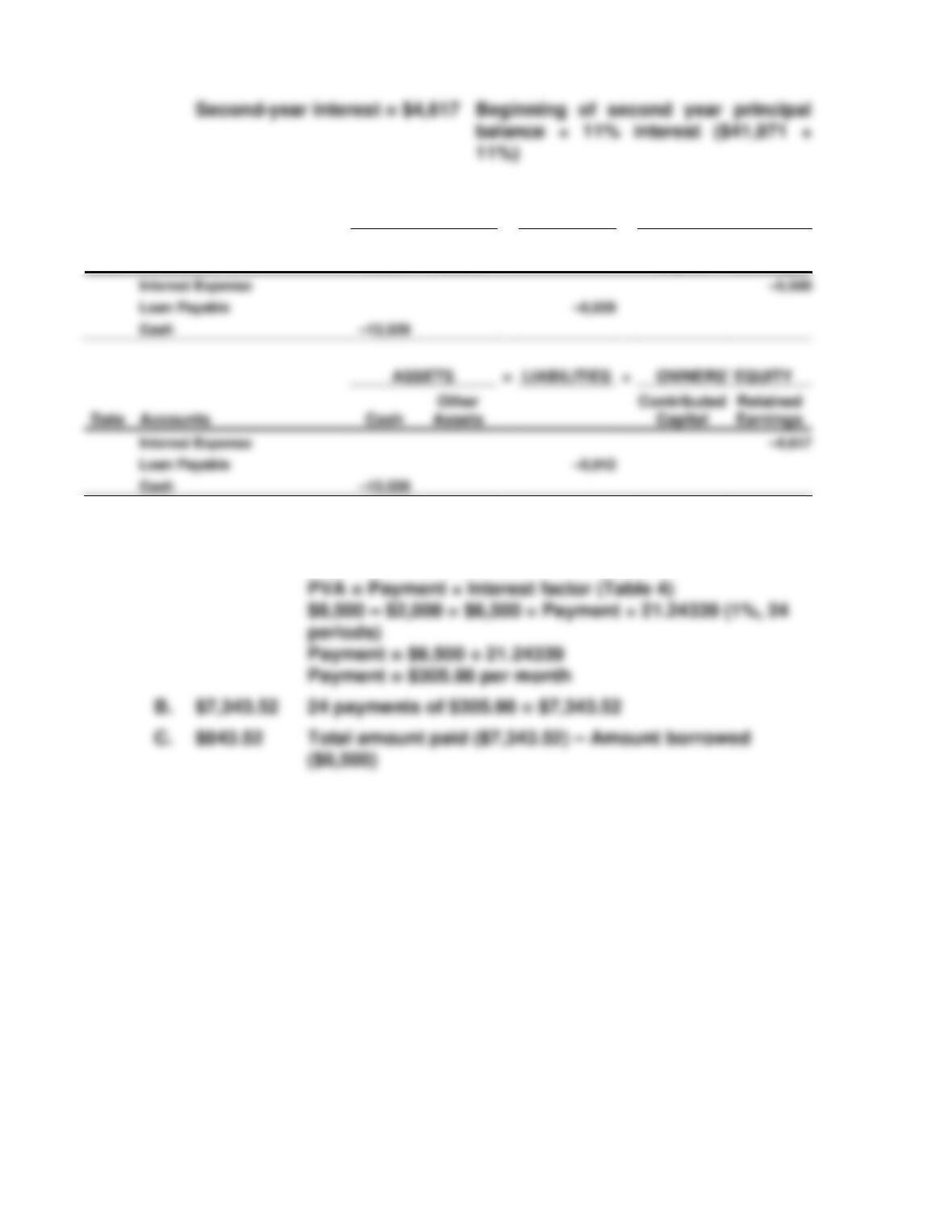

P8–13 A. $13,529 PVA = Payment × Interest factor

B. First-year interest = $5,500 $50,000 × 11% = $5,500. The differ-

220 Chapter 8

C.

ASSETS

=

LIABILITIES

+

OWNERS’ EQUITY

Date

Accounts

Cash

Other

Assets

Contributed

Capital

Retained

Earnings

Other

Assets

Contributed

Capital

Retained

Earnings

P8–14 A. $305.98 The amount of monthly payments can be determined

from the present value of an annuity equation:

The Time Value of Money 221

Period

Amount

Owed at

Beginning

1% Interest

Expense

Payment

Amount of

Principal

Paid

Amount

Owed at End

1

$6,500.00

$65.00

$305.98

$240.98

$6,259.02

2

6,259.02

62.59

305.98

243.39

6,015.63

3

6,015.63

60.16

305.98

5,769.81

4

5,769.81

57.70

305.98

248.28

5,521.53

5

5,521.53

55.22

305.98

250.76

5,270.77

6

5,270.77

52.71

305.98

253.27

7

50.17

305.98

255.81

4,761.69

8

4,761.69

47.62

305.98

258.36

4,503.33

9

4,503.33

45.03

305.98

260.95

10

4,242.38

42.42

305.98

263.56

3,978.82

11

3,978.82

39.79

305.98

266.19

3,712.63

12

3,712.63

37.13

305.98

268.85

3,443.78

Therefore, the amount owed at the end of the first year would be

$3,443.78.

Alternatively, it could be pointed out that the amount owed at any point in

the life of the loan is equal to the present value of the remaining pay-

P8-15 A. Column (i) refers to the year. This is customary. Column (iv) has to

be the annual cash payment because that is the only item that is

constant over time. If column (iv) is the annual cash payment, there

222 Chapter 8

The complete amortization table is as follows:

(i)

Year

(ii)

Beginning

of Year

Balance

(iii)

Interest

at 8%

(iv)

Annual

Cash

Payment

(v)

Reduction

of Principal

(vi)

End of Year

Balance

D. Cannot tell This table fits either side of the transaction. A note

amortizes exactly the same way for the borrower (Note

G. $50,444 Cash outflows totaling $50,444 will be reported by the

The Time Value of Money 223

This problem must be split into pieces. One approach is to assume

two different annuities. The first annuity is $4,000 for 12 years. A

Alternatively, one could treat the two annuities completely separate-

ly. The first annuity grows for eight years (to $39,589.88) and then

continues to grow as a single sum for four additional years (to a total

P8–17 A. $8,856.77 The four equal annual withdrawals constitute an annui-

ty. The $30,000 gift is the present value of that annuity.

C. $7,659.13 Balance after 1 year, just before

224 Chapter 8

P8–18 A. $13,490.05 To determine the maximum purchase price for the in-

PVA = Amount of annuity × IF (Table 4)

PVA = $1,050 × 5.78637

PVA = $6,075.69

C. The investment in part B has the higher cost. The cash flows to be

more for the investment.

P8–19 A. 0.007 8.4% ÷ 12 = 0.007 interest rate per month

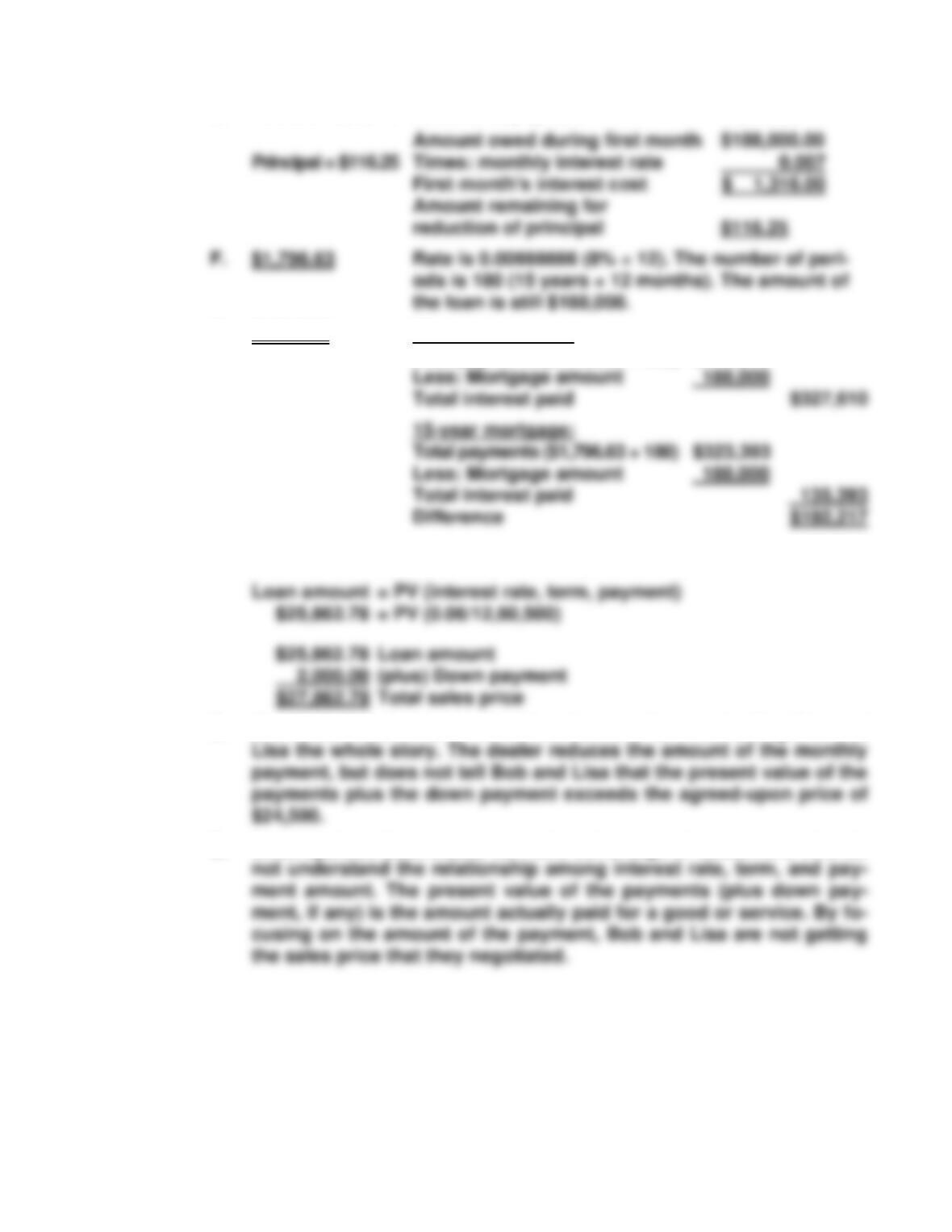

The Time Value of Money 225

E. Interest = $1,316 Amount of payment $1,432.25

G. $192,217 30-year mortgage:

Total payments ($1,432.25 × 360) $515,610

P8–20 A. Bob and Lisa can calculate the sales price of the vehicle as follows:

B. The dealer’s behavior is not ethical because he is not telling Bob and

C. Unscrupulous businesses can take advantage of customers who do

226 Chapter 8

P8-21 A. If the loan is paid off over 30 years at 8%, the monthly payment

would be $1,174.02.

B. The amount owed on 12/31/08 after the monthly payment is

Month

Present Value

at Beginning of

Month

Interest

Incurred

Amount

Paid

Principal

Paid

Value at

End of

Month

1

160,000.00

1,066.67

1,174.02

107.35

159,892.65

2

159,892.65

1,065.95

1,174.02

108.07

159,784.58

3

159,784.58

1,065.23

1,174.02

108.79

159,675.79

4

159,675.79

1,064.51

1,174.02

109.51

159,566.28

5

159,566.28

1,063.78

1,174.02

110.24

159,456.04

6

159,456.04

1,063.04

1,174.02

110.98

159,345.06

7

159,345.06

1,062.30

1,174.02

111.72

159,233.34

8

159,233.34

1,061.56

1,174.02

112.46

159,120.88

9

159,120.88

1,060.81

1,174.02

113.21

159,007.67

159,007.67

1,060.05

1,174.02

113.97

1,059.29

1,174.02

114.73

158,778.97

158,778.97

1,058.53

158,663.48

12,751.72

C. If the loan is paid off over 15 years at 8%, the monthly payment

would be $1,529.04.

The Time Value of Money 227

Month

Present Value

at Beginning

of Month

Interest

Incurred

Amount

Paid

Principal

Paid

Value at End

of Month

1

160,000.00

1,066.67

1,529.04

462.37

159,537.63

2

159,537.63

1,063.58

1,529.04

465.46

159,072.17

D. If the loan is paid off over 30 years at 9%, the monthly payment

would be $1,287.40.

The total interest incurred in the first year would be $14,355.63.

Principal 160,000

Month

Present Value

at Beginning

of Month

Interest

Incurred

Amount

Paid

Principal

Paid

Value at End

of Month

1

160,000.00

1,200.00

1,287.40

87.40

159,912.60

2

159,912.60

1,199.34

1,287.40

88.06

159,824.54

3

159,824.54

1,198.68

1,287.40

88.72

159,735.82

4

159,735.82

1,198.02

1,287.40

89.38

159,646.44

5

159,646.44

1,197.35

1,287.40

90.05

6

1,196.67

1,287.40

90.73

159,465.66

7

159,465.66

1,195.99

1,287.40

91.41

159,374.25

8

159,374.25

1,195.31

1,287.40

92.09

9

1,194.62

1,287.40

92.78

1,193.92

1,287.40

93.48

159,095.90

159,095.90

1,193.22

1,287.40

94.18

159,001.72

159,001.72

94.89

158,906.83

3

159,072.17

1,060.48

1,529.04

468.56

158,603.61

4

158,603.61

1,057.36

1,529.04

471.68

158,131.93

5

158,131.93

1,054.21

1,529.04

474.83

6

1,051.05

1,529.04

7

1,047.86

1,529.04

156,697.93

8

156,697.93

1,044.65

1,529.04

484.39

156,213.54

9

156,213.54

1,041.42

1,529.04

487.62

155,725.92

155,725.92

1,038.17

1,529.04

490.87

155,235.05

155,235.05

1,034.90

1,529.04

494.14

497.43

154,243.48

228 Chapter 8

P8-22

CASES

C8-1 The essential facts of the two alternatives can be summarized as follows:

Dealer

1

2

Cost of car

$20,500

$20,000

Rebate

Net price

C8-2 M E M O R A N D U M

DATE: (today’s date)

TO: Harold

FROM: (student’s name)

SUBJECT: Evaluation of loan options

Your two financing options will result in different payments.

As a result of these payments differences, the total payments over the life

of the loans and the total interest associated with them will be quite dif-

ferent:

The Time Value of Money 229

C8-3 To analyze the various contract proposals, we use present value con-

cepts. We used Excel for our analysis; however, present value tables also

can be used. The following analysis assumes a 4% discount rate.

Proposal 1. The present value of Proposal 1 is $2,823,769. The contract

Proposal 2. The present value of Proposal 2 is $3,629,895. The contract

guarantees $1 million per year in each of four years. Using Excel, the pre-

Proposal 3. The present value of Proposal 3 is $2,739,734. The contract

guarantees a signing bonus of $900,000. Since the bonus is paid upon

230 Chapter 8

Proposal 4. The present value of Proposal 4 is $10,487,956. The contract

guarantees three annual payments of $400,000 plus a lump sum payment

Proposal 5. The present value of Proposal 5 is $2,500,000. No discount-

Proposal 6. The present value of Proposal 6 is $7,966,270. The contract

is not guaranteed. If Fleet continues to play, the contract will pay

Cash Flow

Each Period

Present

Value

Proposal 1

3-year contract at $1 million

Payable quarterly

Quarterly payment

Proposal 2

4-year contract at $1 million

Payable at the end of the year

Proposal 3

4-year contract

900,000 signing bonus

$ 900,000

125,000 end-of-quarter payments

The Time Value of Money 231

Cash Flow

Each Period

Present

Value

Proposal 4

Proposal 6

6-year contract at $1,500,000

Cancelable if injured or cut

Key points:

• The proposals with the highest present value (4 and 6) also have the

greatest risk.

3-year contract of $400,000 at each year-end

$25 million to be paid 25 years after signing

Proposal 5

3-year contract

$2.5 million signing bonus, no payments