Exercise 8-13

Requirement 1

Requirement 2

December 31

Requirement 3

January 31

Requirement 4

Warranty Liability

Exercise 8-14

Requirement 1

Yes, a contingent liability is an existing, uncertain situation that might result in a loss.

Requirement 2

Requirement 3

Exercise 8-15

Requirement 1

Current Assets

÷

Current Liabilities

=

Current Ratio

Quick Assets

÷

Current Liabilities

=

Acid-Test Ratio

Requirement 2

Queen’s Line has a lower current ratio and a lower acid-test ratio than either United

Exercise 8-16

Requirement 1 Transactions during January, 2018

January 2

Debit

Credit

Cash

8,000

Deferred Revenue

8,000

(Sell gift cards for cash)

January 6

Debit

Credit

Inventory

147,000

Accounts Payable

147,000

January 15

Debit

Credit

Sales Revenue

135,000

(Sell inventory on account)

Cost of Goods Sold

73,800

Inventory

(Record cost of inventory sold)

January 23

Debit

Credit

Cash

125,400

Accounts Receivable

125,400

(Receive cash on account)

January 25

Debit

Credit

Accounts Payable

90,000

(Pay cash on account)

January 28

Debit

Credit

Allowance for Uncollectible Accounts

Accounts Receivable

4,800

(Write off uncollectible accounts)

January 30

Debit

Credit

Cash

11,000

Accounts Receivable

132,000

Sales Revenue

143,000

(Sell inventory for cash and on account)

Inventory

January 31

Debit

Credit

Salaries Expense

52,000

Cash

(Pay monthly salaries)

Exercise 8-16 (continued)

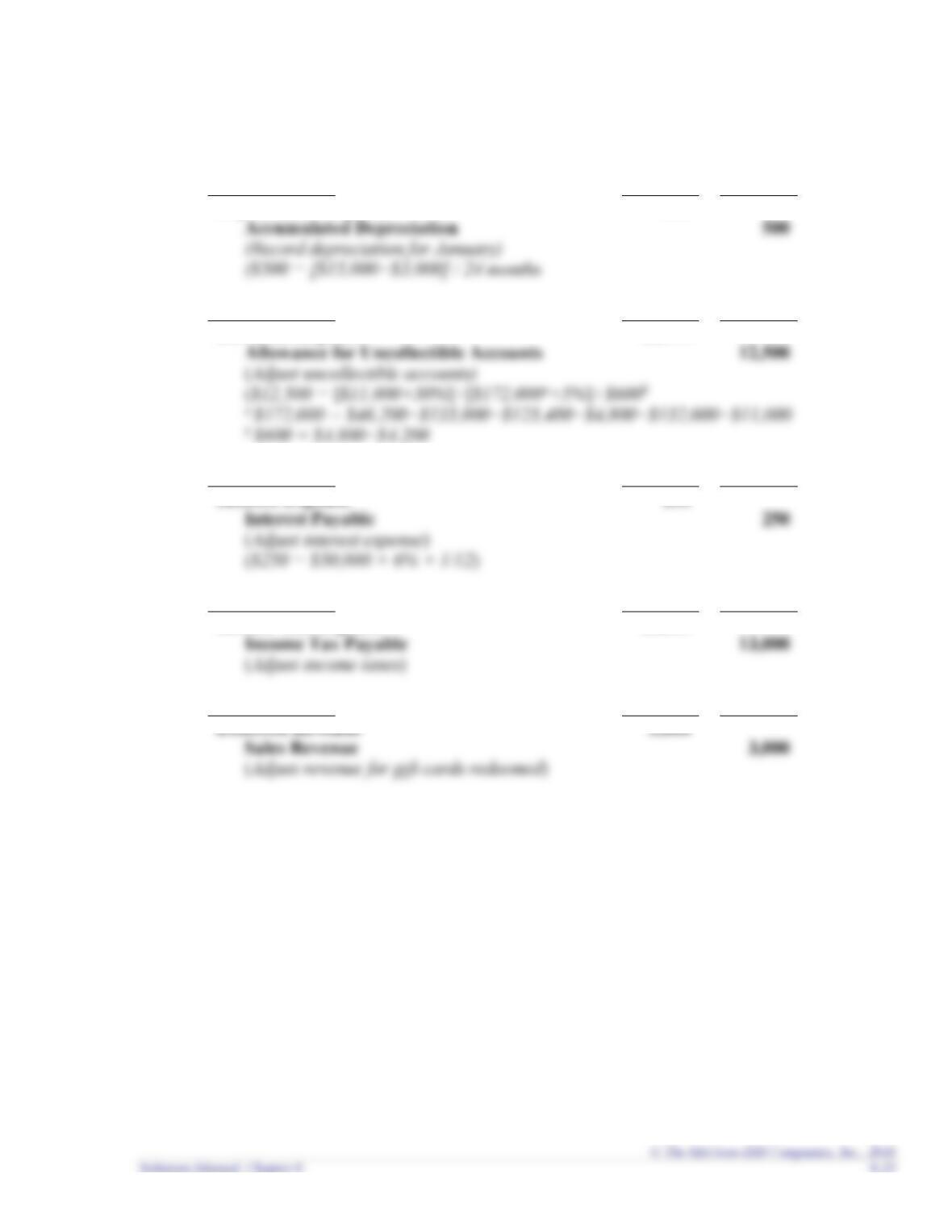

Requirement 2 Adjusting entries at end of January, 2018

(a) January 31

Debit

Credit

Depreciation Expense

500

500

(b) January 31

Debit

Credit

Bad Debt Expense

12,500

12,500

(c) January 31

Debit

Credit

Interest Expense

250

250

(d) January 31

Debit

Credit

Income Tax Expense

13,000

(e) January 31

Debit

Credit

Deferred Revenue

Exercise 8-16 (continued)

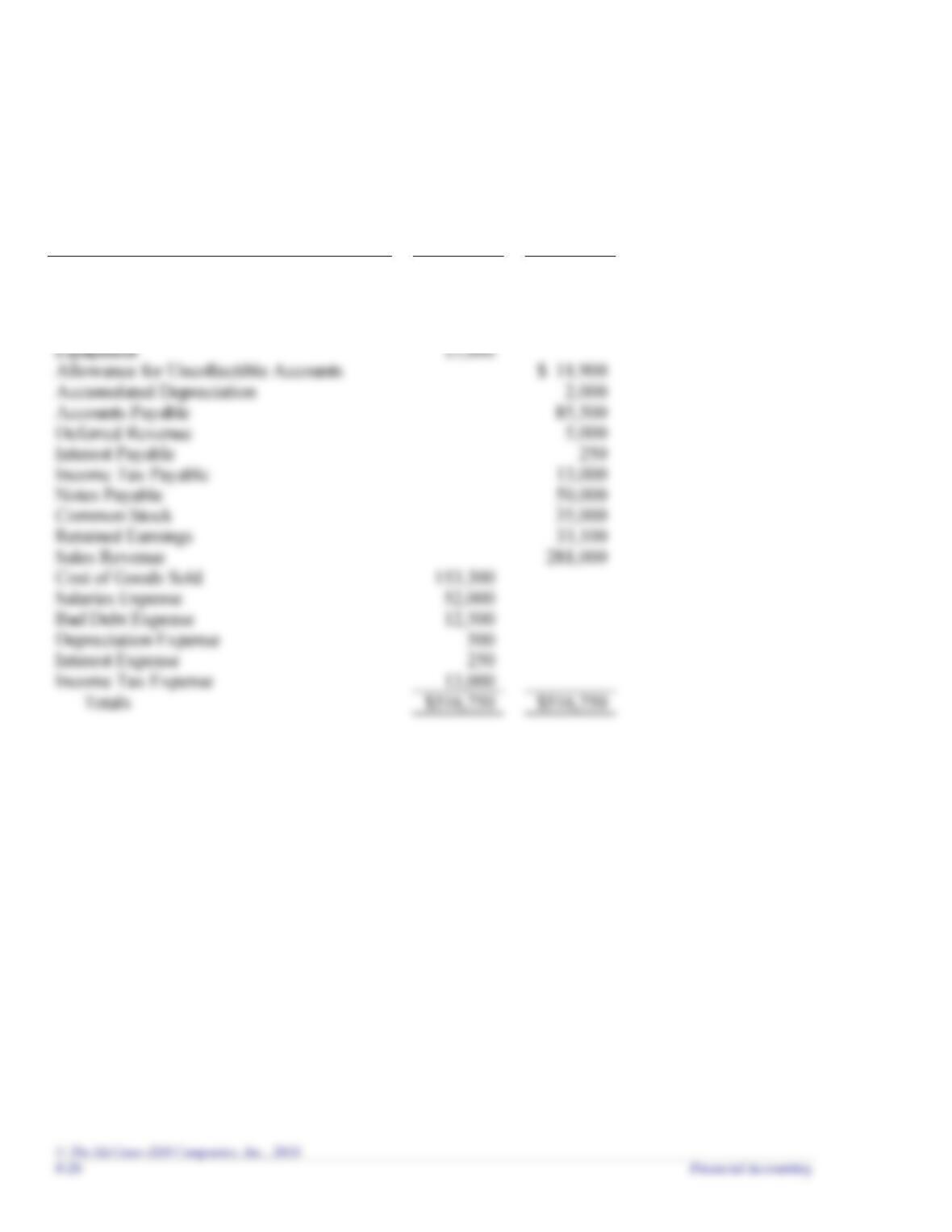

Requirement 3

ACME Fireworks

Adjusted Trial Balance

January 31, 2018

Accounts

Debit

Credit

Cash

$ 27,500

Accounts Receivable

183,000

Inventory

13,700

Land

46,000

Equipment

15,000

Allowance for Uncollectible Accounts

$ 11,900

Accumulated Depreciation

Accounts Payable

85,500

Deferred Revenue

Interest Payable

Income Tax Payable

13,000

Notes Payable

50,000

Common Stock

35,000

Retained Earnings

33,100

Sales Revenue

281,000

Cost of Goods Sold

153,300

Salaries Expense

52,000

Bad Debt Expense

12,500

Depreciation Expense

Interest Expense

Income Tax Expense

13,000

Totals

$516,750

$516,750

Exercise 8-16 (continued)

Requirement 3 (concluded)

Accounts

Ending

Balance

Beginning balance in bold, entries during January in blue,

and adjusting entries in red.

Cash

$ 27,500

=

25,100+8,000+125,400−90,000+11,000−52,000

Accounts Receivable

183,000

=

46,200+135,000−125,400−4,800+132,000

Inventory

=

20,000+147,000−73,800−79,500

Land

=

46,000

Equipment

=

Allow for Unc. Accounts

=

4,200−4,800+12,500

Accumulated Depreciation

=

1,500+500

Accounts Payable

=

28,500+147,000−90,000

Deferred Revenue

=

Interest Payable

=

Income Tax Payable

=

Notes Payable

=

50,000

Common Stock

=

Retained Earnings

=

Sales Revenue

281,000

=

Cost of Goods Sold

153,300

=

Salaries Expense

=

Bad Debt Expense

=

Depreciation Expense

=

Interest Expense

=

Income Tax Expense

=

Exercise 8-16 (continued)

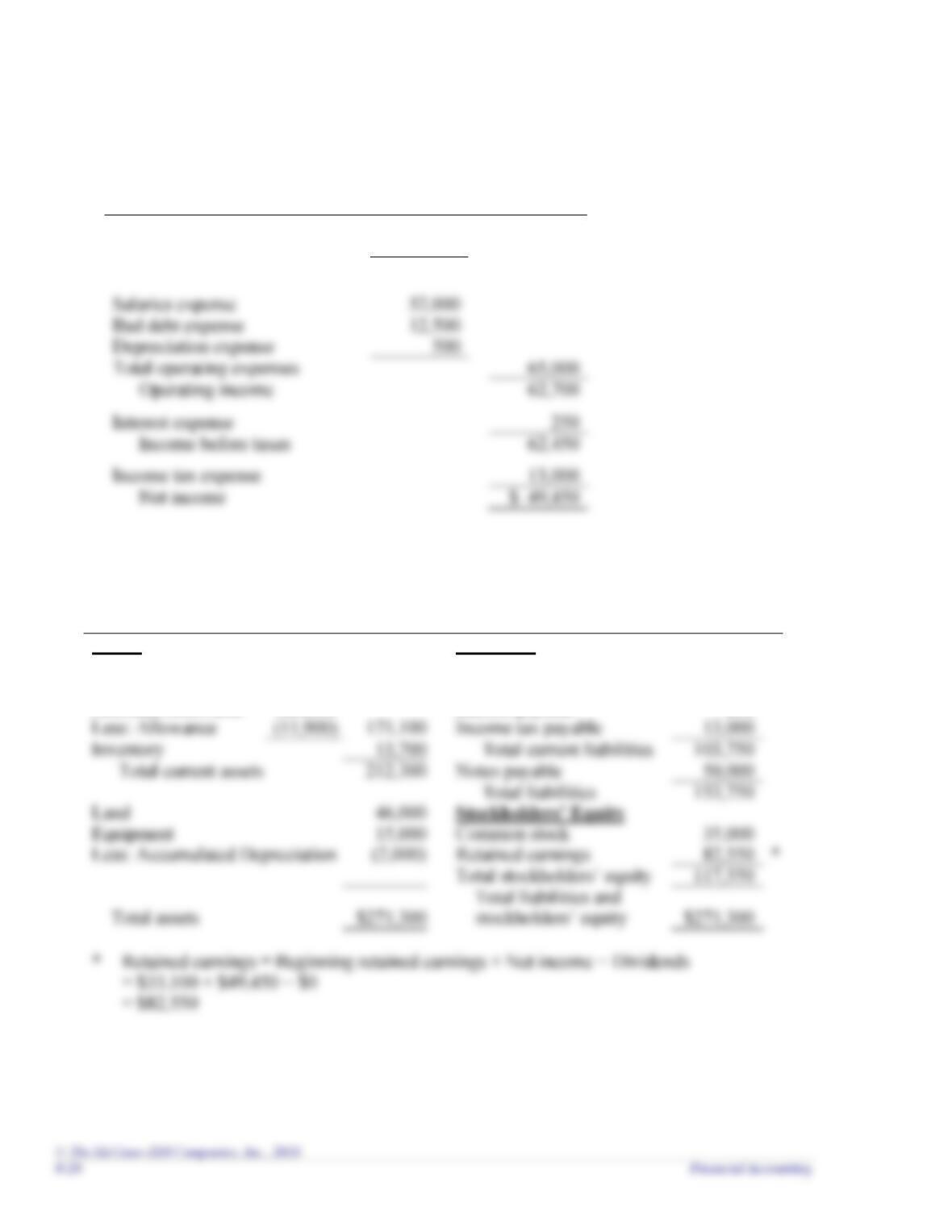

Requirement 4

ACME Fireworks

Multiple-Step Income Statement

For the year ended January 31, 2018

Sales revenue

$281,000

Cost of goods sold

153,300

Gross profit

$127,700

Bad debt expense

Depreciation expense

Total operating expenses

Interest expense

Income tax expense

$ 49,450

Requirement 5

ACME Fireworks

Classified Balance Sheet

January 31, 2018

Assets

Liabilities

Accounts payable

$ 85,500

Cash

$ 27,500

Deferred revenue

5,000

Accounts receivable

183,000

Interest payable

250

Less: Allowance

(11,900)

Income tax payable

Inventory

Notes payable

Land

Equipment

Common stock

Less: Accumulated Depreciation

(2,000)

Retained earnings

*

Total assets

$271,300

$271,300

Exercise 8-16 (concluded)

Requirement 6

January 31, 2018

Debit

Credit

Sales Revenue

281,000

Retained Earnings

281,000

(Close revenue accounts)

Retained Earnings

231,550

Cost of Goods Sold

153,300

Salaries Expense

Bad Debt Expense

Depreciation Expense

Interest Expense

Income Tax Expense

(Close expense accounts)

Requirement 7

(a) The current ratio is:

Current Liabilities

$103,750

Current Assets

$212,300

(b) The acid-test ratio is:

Acid-Test Ratio

=

Quick Assets*

=

$27,500 + $0 + $171,100

=

1.91

Current Liabilities

$103,750

=

Current Assets

$212,300

=

1.38

Current Liabilities

$153,750

PROBLEMS: SET A

Problem 8-1A

List A

List B

_i__

1. A promise to repay the amount borrowed plus

interest.

a. Recording of a

contingent liability

_d__

_a__

4. Payment amount is probable and is reasonably

d. Disclosure of a

_b__

5. A liability that requires the sacrifice of

e. Interest on debt

_j__

6. Long-term debt maturing within one year.

f. Payroll taxes

_f__

7. FICA and FUTA.

g. Line of credit

_g__

8. Informal agreement that permits a company to

borrow up to a prearranged limit

h. Capital structure

_c__

9. Classifying liabilities as either current or long-

i. Notes payable

_e__

10. Amount of note payable x annual interest rate

x fraction of the year.

j. Current portion of

long-term debt

2. Payment amount is reasonably possible and is

b. Deferred revenue

Problem 8-2A

Requirement 1

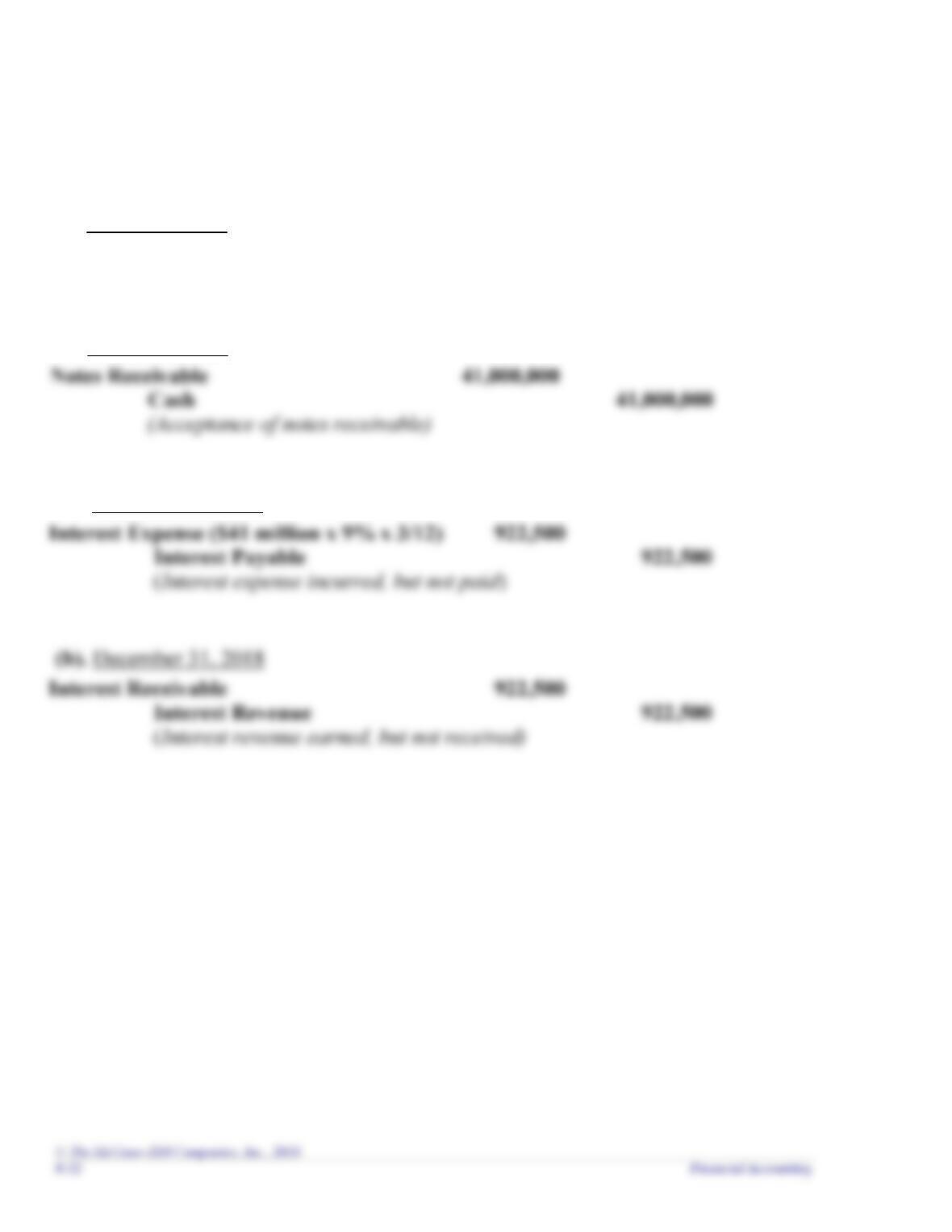

(a). October 1, 2018

Cash

41,000,000

Notes Payable

41,000,000

(Issuance of notes payable)

(b). October 1, 2018

Notes Receivable

41,000,000

Cash

41,000,000

(Acceptance of notes receivable)

Requirement 2

(a). December 31, 2018

Interest Payable

(b). December 31, 2018

Requirement 3

(a) September 30, 2019

Notes Payable

41,000,000

Interest Expense ($41 million x 9% x 9/12)

(b). September 30, 2019

Cash

44,690,000

Problem 8-3A

Requirement 1

January 31

Salaries Expense

600,000

Income Tax Payable

60,000

FICA Tax Payable

Requirement 2

January 31

January 31

FICA Tax Payable

Unemployment Tax Payable

Problem 8-4A

Requirement 1

February 14

Salaries Expense

1,500,000

Income Tax Payable

375,000

FICA Tax Payable

114,750

947,250

Requirement 2

February 14

Requirement 3

February 14

Unemployment Tax Payable

Problem 8-5A

Requirement 1

$102,600,000

=

$900 per season ticket

114,000

Requirement 2

Cash

102,600,000

Deferred Revenue

Requirement 3

Deferred Revenue

Problem 8-6A

Requirement 2

Problem 8-7A

Requirement 1

Requirement 2

Environmental Printing has a contingent gain that is probable, and is reasonably

Requirement 3

Environmental Printing should record a loss and a liability for the minimum amount

($500,000) and disclose the range between $500,000 and $900,000 in the notes to the

financial statements. The entry is as follows:

Problem 8-8A

Requirement 1

The reporting for this situation depends on the likelihood of loss occurring. If the

likelihood of loss is reasonably possible rather than probable, no journal entry is

recorded. However, if the likelihood of loss is probable, the following entry would be

recorded:

Requirement 2

The contingent loss is probable and reasonably estimable, so it would be recorded as

follows:

Requirement 3

Dinoco has a contingent gain that is probable, and is reasonably estimable at $150

Problem 8-9A

Requirement 1

($ in millions)

Total

Current

Assets

÷

Total

Current

Liabilities

=

Current

Ratio

Requirement 2

($ in millions)

Quick

Assets

÷

Total

Current

Liabilities

=

Acid-Test

Ratio

Requirement 3

The purchase of additional inventory on credit would increase current assets

(inventory) and current liabilities (accounts payable) by the same amount. This