CHAPTER 8

Pricing

ASSIGNMENT CLASSIFICATION TABLE

Learning Objectives

Questions

Brief

Exercises

Do It!

Exercises

A

Problems

1. Compute a target cost when

the market determines a

product price.

1, 2

1

1

1, 2, 3

2. Compute a target selling price

using cost-plus pricing.

3, 4, 5,

6, 7, 8

2, 3,

4, 5

2

3, 4, 5,

6, 7

1A, 2A

3. Use time-and-material pricing

to determine the cost of

services provided.

9, 10

6

3

8, 9, 10

3A

4. Determine a transfer price

using the negotiated, cost-

based, and market-based

approaches.

11, 12, 13,

14, 15,

16, 17

7, 8, 9

4

11, 12, 13,

14, 15,

16, 17

4A, 5A, 6A

*5. Determine prices using

absorption-cost pricing

and variable-cost pricing.

18, 19

10, 11

18, 19, 20

7A, 8A

*6. Explain issues involved in

transferring goods between

divisions in different countries.

20

*Note: All asterisked Questions, Exercises, and Problems relate to material contained in the appendix to the

chapter.

ASSIGNMENT CHARACTERISTICS TABLE

Problem

Number

Description

Difficulty

Level

Time

Allotted (min.)

1A

Use cost-plus pricing to determine various amounts.

Simple

20–30

2A

Use cost-plus pricing to determine various amounts.

Simple

20–30

3A

Use time-and-material pricing to determine bill.

Simple

20–30

4A

Determine minimum transfer price with no excess capacity

and with excess capacity.

Moderate

20–30

5A

Determine minimum transfer price with no excess capacity.

Moderate

20–30

6A

Determine minimum transfer price under different situations.

Moderate

20–30

*7A*

Compute the target price using absorption-cost pricing and

variable-cost pricing.

Moderate

30–40

*8A*

Compute various amounts using absorption-cost pricing and

variable-cost pricing.

Complex

40–50

BLOOM’ S TAXONOMY TABLE

Correlation Chart between Bloom’s Taxonomy, Learning Objectives and End–of-Chapter Exercises and Problems

Learning Objective

Knowledge

Comprehension

Application

Analysis

Synthesis

Evaluation

*1. Compute a target cost when the

market determines a product

price.

Q8-1

Q8-2

BE8-1

DI8-1

E8-1

E8-2

E8-3

*2. Compute a target selling price

using cost-plus pricing.

Q8-3

Q8-5

Q8-6

Q8-4

Q8-7

Q8-8

BE8-2

BE8-3

BE8-4

BE8-5

DI8-2

E8-3

E8-4

E8-5

E8-6

E8-7

P8–1A

P8–2A

*3. Use time-and-material pricing

to determine the cost of

services provided.

Q8–10

Q8-9

BE8-6

DI8-3

E8-8

E8-9

E8–10

P8–3A

*4. Determine a transfer price using

the negotiated, cost-based, and

market-based approaches.

Q8–13

Q8–15

Q8–16

Q8–11

Q8–12

Q8–14

Q8–17

BE8-7 E8–16

BE8-8 E8–17

BE8-9 P8–4A

DI8-4 P8–5A

E8–11 P8–6A

E8–13

E8–14

E8–15

E8–12

*5. Determine prices using

absorption-cost pricing

and variable-cost pricing.

Q8–18

Q8–19 E8–20

BE8-10 P8–7A

BE8-11 P8–8A

E8–18

E8–19

*6. Explain issues involved in

transferring goods between

divisions in different countries.

Q8–20

Broadening Your Perspective

BYP8-4

BYP8-5

BYP8-6

BYP8-2

BYP8-3

BYP8-7

BYP8-1

ANSWERS TO QUESTIONS

1. The first type of pricing environment is where the company is a price taker; that is, the company

does not set the price, but instead the price is set by a competitive market. In the second type of

situation, the company sets the price. This happens most often when the product is specially made

for a customer or there are few or no other producers capable of manufacturing a similar item.

2. A company focuses on target cost when it cannot influence the market price. The target cost is

determined by subtracting the desired profit per unit from the market-determined selling price.

3. The basic formula to determine the target selling price in cost-plus pricing is:

Target selling price

=

Cost

+

(Markup percentage X Cost)

4. The basic formula to determine the target selling price in cost-plus pricing is:

Target selling price

=

Cost

+

(Markup percentage X Cost)

$23.40

=

$18

+

(30% X $18)

5. The basic formula to compute the markup percentage is:

Markup percentage

=

Desired ROI per unit

Total unit cost

6. Some of the factors that affect a company’s desired ROI are competitive and market conditions,

political and legal issues, and other relevant risk factors.

7. Total cost base per unit, excluding selling and administrative expenses ……………………. $60

Selling and administrative expenses per unit ………………………………………………………… 15

Total unit cost ………………………………………………………………………………………………….. $75

The markup percentage is computed as follows:

$6

=

8%

$75

8. Variable cost per unit ………………………………………………………………………………………… $16

Fixed cost per unit ……………………………………………………………………………………………. 9

Desired ROI per unit …………………………………………………………………………………………. 6

Target selling price …………………………………………………………………………………………… $31

The markup percentage is:

$6

= 24%

$25

9. Time-and-material pricing is most often used in service industries. It involves two pricing rates,

one for the labor used on a job, while the other involves the materials used. Each typically has a

profit rate factored into it.

10. The material loading charge is a fee added to each bill to cover the costs of purchasing, receiving,

handling, and storing materials, plus any desired profit margin on the materials themselves. The

material loading charge is expressed as a percentage of the total estimated costs of parts and

materials for the year.

Questions Chapter 8 (Continued)

*11. A transfer price is the price used to record the transfer of goods or services between two divisions

in the same company. Setting a fair transfer price is important because an improper price will

benefit one division while hurting the other.

*12. The objective of an appropriate transfer price is to maximize the return to the whole company

and not cause divisional performance to decline.

*13. The three approaches for determining transfer prices are:

(1) Negotiated transfer prices

(2) Cost-based transfer prices

(3) Market-based transfer prices

*14. When a cost-based transfer price is used, the exchange of goods between divisions is recorded

by using the costs incurred by the selling division. This may either be the variable costs or

the variable costs with an additional markup to cover fixed costs. The primary advantage of this

approach is that it is relatively simple to use. The disadvantage is that it understates the selling

division’s contribution to the company’s total contribution margin. Finally, it reduces the selling

division’s incentive to control cost.

*15. The general formula for determining the minimum transfer price that the selling division should

be willing to accept is:

Minimum transfer price

=

Variable cost

+

Opportunity cost

*16. When determining the minimum transfer price, the opportunity cost is the contribution margin

that would be received if the goods were sold externally.

*17. A company is likely to use a negotiated transfer price rather than a market-based price when the

selling division has excess capacity, and is therefore eager to expand production, or when a

market price does not exist (e.g., for a special order).

*18. The absorption-cost approach defines the cost base as manufacturing cost. Therefore, it excludes

variable and fixed selling and administrative costs.

*19. The markup percentage using variable-cost pricing would be:

$3 + $9

= 75%

$16

*20. A company with divisions in different countries will set the transfer price so that more profit is

allocated to the division located in the country with the lower tax rate. This is improper. The

proper (and legal) treatment is to base the transfer price on the market value of the goods

transferred.

SOLUTIONS TO BRIEF EXERCISES

BRIEF EXERCISE 8-1

In order to obtain a profit of $10 per drive, Ortega must set its target cost at

BRIEF EXERCISE 8-2

Direct materials …………………………………………………………………………… $12

Direct labor …………………………………………………………………………………. 8

Variable manufacturing overhead …………………………………………………. 6

BRIEF EXERCISE 8-3

ROI per unit

=

(Total investment X Desired ROI percentage)

Number of units

=

=

BRIEF EXERCISE 8-4

The markup percentage would be:

BRIEF EXERCISE 8-5

The markup percentage is equal to Desired ROI per unit divided by total

unit cost. The desired ROI per unit is computed as follows:

The total unit cost is computed as follows:

BRIEF EXERCISE 8-6

Rooney’s total bill would equal:

BRIEF EXERCISE 8-7

The minimum transfer price is equal to the division’s variable cost plus its

opportunity cost. The opportunity cost is equal to its contribution margin

on goods sold to external parties. Thus, the minimum transfer price in this

case is:

BRIEF EXERCISE 8-8

If the division has excess capacity, then its opportunity cost is zero. In this

case, the minimum transfer price is:

The minimum transfer price is equal to the division’s variable cost plus its

opportunity cost. In this case the minimum transfer price is:

*BRIEF EXERCISE 8-10

The markup percentage using the absorption-cost approach is calculated

by including only manufacturing costs in the cost base. Therefore, all costs

related to selling and administration are excluded from the cost base and

added back in the numerator.

*BRIEF EXERCISE 8-11

The markup percentage using variable-cost pricing is calculated by including

only variable costs in the cost base. Therefore, all fixed costs are excluded

from the cost base and added back in the numerator.

SOLUTIONS TO DO IT! EXERCISES

DO IT! 8-1

The desired profit for this new product line is $320,000 ($2,000,000 X 16%)

Each filter must result in $.32 of profit ($320,000/1,000,000 units)

DO IT! 8-2

Direct materials ………………………………………………………

$18

Direct labor …………………………………………………………….

9

Variable manufacturing overhead …………………………...

5

Fixed manufacturing overhead ………………………………..

6

Variable selling and administrative expenses …………..

3

Fixed selling and administrative expenses ……………….

$48

Total unit cost + (Total unit cost X Markup percentage) = Target selling price

DO IT! 8-3

Total Cost /

Total Hours =

Per Hour

Charge

Repair-technicians’ wages

$110,000

5,000

$22

Fringe benefits

40,000

5,000

8

5,000

$200,000

5,000

$40

Profit margin

$60

Materials cost ………………………………………. $ 70

Materials loading charge ($70 X 60%) …….. 42

DO IT! 8-4

(a) Minimum transfer price = Variable cost + Opportunity cost

(b) Minimum transfer price = Variable cost + Opportunity cost

SOLUTIONS TO EXERCISES

EXERCISE 8-1

(a) The target cost formula is: Target cost = Market price – Desired profit.

(b) Target costing is particularly helpful when a company faces a competi–

EXERCISE 8-2

The following formula may be used to determine return on investment

Return on investment per unit is then $16 ($1,600,000 ÷ 100,000)

The target cost is therefore $74 computed as follows:

EXERCISE 8-3

(a) (1) In this case the selling price would be $125 ($100 + [$100 X 25%]).

The problem with the $125 is that it is unlikely that Leno will be able to

sell any All-Body suits at that price. Market research seems to

(b) In this case, the amount would be the selling price of $100.

EXERCISE 8-3 (Continued)

(c) The highest acceptable cost would be the target cost. The target cost

is $75 as shown below:

EXERCISE 8-4

(a) Total cost per unit:

Per Unit

Direct materials ……………………………………………………….……….

Direct labor ………………………………………………………………………

Variable manufacturing overhead ……………………………………..

$17

8

11

EXERCISE 8-5

(a) Total cost per unit:

Per Unit

Direct materials ……………………………………………………….……….

Direct labor ………………………………………………………………………

Variable manufacturing overhead ……………………………………..

$ 7

11

15

EXERCISE 8-5 (Continued)

(c) Markup percentage using total cost per unit:

EXERCISE 8-6

(a)

Total cost per session:

Per Session

Direct materials ………………………………………….

$ 20

Direct labor ………………………………………………..

400

Variable overhead ……………………………………….

Fixed overhead ($950,000 ÷ 1,000) ……………….

Variable selling & administrative expenses…..

Fixed selling & administrative expenses

($500,000 ÷ 1,000) ……………………………………

500

Total cost per session ………………………….

(b) Desired ROI per session = (20% X $2,352,000) ÷ 1,000 = $470.40

EXERCISE 8-7

(a)

Fixed manufacturing overhead per unit

=

$1,500,000

=

$500 per unit

3,000

(b)

Desired ROI per unit

=

20% X $54,000,000

=

=

EXERCISE 8-7 (Continued)

(c)

Per Unit

Direct materials ……………………………………………………….……….

Direct labor ………………………………………………………………………

Variable manufacturing overhead ……………………………………..

$ 380

290

72

EXERCISE 8-8

(a)

Total

Cost

÷

Total

Hours

=

Per Hour

Charge

Hourly labor rate for repairs

Technician’s wages and benefits

Overhead costs

$228,000

÷

7,600

=

$30

(b)

Material

Loading

Charges

÷

Total

Invoice Cost,

Parts and

Materials

=

Material

Loading

Percentage

Overhead costs

Parts manager’s salary and

benefits

$42,500

EXERCISE 8-8 (Continued)

(c) Job: Pace Corporation—Rebuild spot welder

Labor charges

EXERCISE 8-9

(a)

Total

Cost

÷

Total

Hours

=

Per Hour

Charge

$195,000

Hourly labor rate for repairs

(b)

Material

Loading

Charges

÷

Total

Invoice Cost,

Parts and

Materials

=

Material

Loading

Percentage

Overhead costs

Parts manager’s salary and

benefits

$34,000

EXERCISE 8-9 (Continued)

(c) Job: Buil Builders

Labor charges

80 hours @ $69.20 ………………………….. $ 5,536

EXERCISE 8-10

(a)

Total

Cost

÷

Total Hours

=

Hourly

Charge

Hourly labor rate:

Restorers’ wages and

fringes

$270,000

÷

12,000

=

$22.50

Overhead costs:

fringes

Other overhead costs

2.00

Total hourly cost

÷

=

Profit margin = Hourly rate – total hourly cost

EXERCISE 8-10 (Continued)

(b)

Material

Loading

Charges

÷

Total Invoice

Cost, Parts &

Materials

=

Material

Loading

Percentage

Overhead costs:

Purchasing agent’s

(c)

Labor charges:

150 hours @ $70

$ 10,500

Material charges:

Cost of parts & materials

Material loading charge

($60,000 X 83.25%)

Total price of labor and materials

EXERCISE 8-11

(a) The minimum transfer price is:

Minimum transfer price = Variable cost + opportunity cost

(b) Given no excess capacity, the minimum transfer price is $35, which is

its variable cost plus the lost contribution margin.

salary and fringes

salaries and

fringes

÷

=

Other overhead costs

÷

=

Total

÷

=

EXERCISE 8-11 (Continued)

(c) The level of capacity plays a significant role in determining the appro-

priate transfer price. If a division has no excess capacity, why should

EXERCISE 8-12

(a) As indicated, FrameBody has excess capacity and therefore should be

willing to accept any price that equals or exceeds its variable cost.

1. The effect on Cycle Division is as follows:

Present Situation

Purchase from

FrameBody

Selling price

$2,200

$2,200

2. The effect on FrameBody is that it makes $10 on each frame sold

as shown below:

Selling price to Cycle Division $280

3. As a result, the overall income for Ayala increases $30,000 ($20,000

from Cycle Division and $10,000 from FrameBody).

EXERCISE 8-12 (Continued)

(b) 1. The answer would not change from (a)(1). Cycle Division would

gain $20,000 if it purchased the frames from FrameBody.

2. However, FrameBody would incur a loss of $70,000 as computed

below:

Selling price to outside buyer $ 350

Selling price to Cycle Division 280

3. The effect on the overall income to Ayala is a net loss of $50,000 as

shown below:

EXERCISE 8-13

(a) The minimum transfer price that Benson should accept is:

(b) The lost contribution margin per unit to the company is:

Contribution margin lost by Benson

[($86 – $37) – ($35 – $34)] ……………………………………………. $48

(c) If management insists that it wants Benson to provide the stereo units,

and Benson is operating at full capacity, then it must be willing to pay

EXERCISE 8-14

The minimum transfer price on this special order would be:

EXERCISE 8-15

(a) Minimum transfer price = ($130 – $8) + $0 = $122

EXERCISE 8-16

(a) The minimum transfer price for Division B would be variable costs,

which are $6 per unit ($7, variable cost – $1, variable selling expense).

(b) Minimum transfer price = variable costs + opportunity cost

Variable costs = $6 (as in (a))

EXERCISE 8-16 (Continued)

(c) Minimum transfer price = variable costs + opportunity cost

Variable costs = $6.00 (as in (a))

EXERCISE 8-17

(a) Division Division Total

A B Company

Sales $1,500 $2,400 $3,900

Less: Costs

(b) The opportunity cost is the market price. Transfers should be made at

market prices less any avoidable costs. In the current situation, it

would appear that no transfers would be made.

(c) (i) Maintain price, no transfers

(500 X $1,500) – (500 X $1,100) = $200,000

The firm is better off by maintaining the current market price for

Division A’s product and transferring 500 units to Division B. A

transfer price within the range of $1,100 to $1,200 would be needed to

*EXERCISE 8-18

(a) Cost per unit:

Per Unit

Direct materials ……………………………………………………….……….

$ 7

(b) Desired ROI per unit = (25% X $28,000,000)/500,000 = $14

*EXERCISE 8-19

(a) The cost base of absorption-cost pricing includes only manufacturing

costs. All selling and administrative costs are excluded from the cost

base and are added back in the numerator of the markup percentage.

(b) The cost base of variable-cost pricing includes only variable costs. All

fixed costs are excluded from the cost base and are added back in the

numerator of the markup percentage.

*EXERCISE 8-20

(a)

Fixed manufacturing

overhead per unit

=

$1,500,000

=

$500 per unit

3,000

(b)

Desired ROI per unit

=

20% X $54,000,000

=

$3,600 per unit

3,000

$380 + $290 + $72 + $500

Target selling price = $1,242 + ($1,242 X 302.979%) = $5,005

expenses per unit

=

$324,000

=

$108 per unit

SOLUTIONS TO PROBLEMS

PROBLEM 8-1A

(a) Direct materials ……………………………………………………………….. $25

Total

Costs

÷

Budgeted

Volume

=

Cost

Per Unit

expenses

960,000

÷

=

Fixed manufacturing overhead

$1,440,000

÷

80,000

=

$18

(c) Total cost per unit ……………………………………………………………. $110

(d) Variable cost per unit ……… $ 80 (same as above)

PROBLEM 8-2A

(a) Direct materials ………………………………………………………………. $ 50

Direct labor …………………………..………………………………………… 26

Total

Costs

÷

Budgeted

Volume

=

Cost

Per Unit

expenses

÷

=

=

Fixed manufacturing overhead

$ 600,000

÷

50,000

=

$12

Variable cost per unit ……………………………………………………… $115

Fixed cost per unit ………………………………………………………….. 20

Total cost per unit …………………………………………………………… $135

Total cost per unit …………………………………………………………… $135

(b) Variable cost per unit ……………………………………… $115 (same as (a))

Total

Costs

÷

Budgeted

Volume

=

Cost

Per Unit

expenses

400,000

÷

=

PROBLEM 8-2A (Continued)

Variable cost per unit ………………………………………………………. $115

Fixed cost per unit …………………………………………………………… 25

Total cost per unit ……………………………………………………………. $140

PROBLEM 8-3A

(a) Computation of time charge rate

Total

Cost

÷

Total

Hours

=

Per Hour

Charge

Hourly labor rate for repairs

Shop employees’ wages and benefits

$108,000

÷

5,000

=

$21.60

(b) Computation of material loading charge

Material

Loading

Charges

÷

Total Invoice Cost,

Parts and Materials

=

Material

Loading

Percentage

Total

Overhead costs

Parts manager’s salary

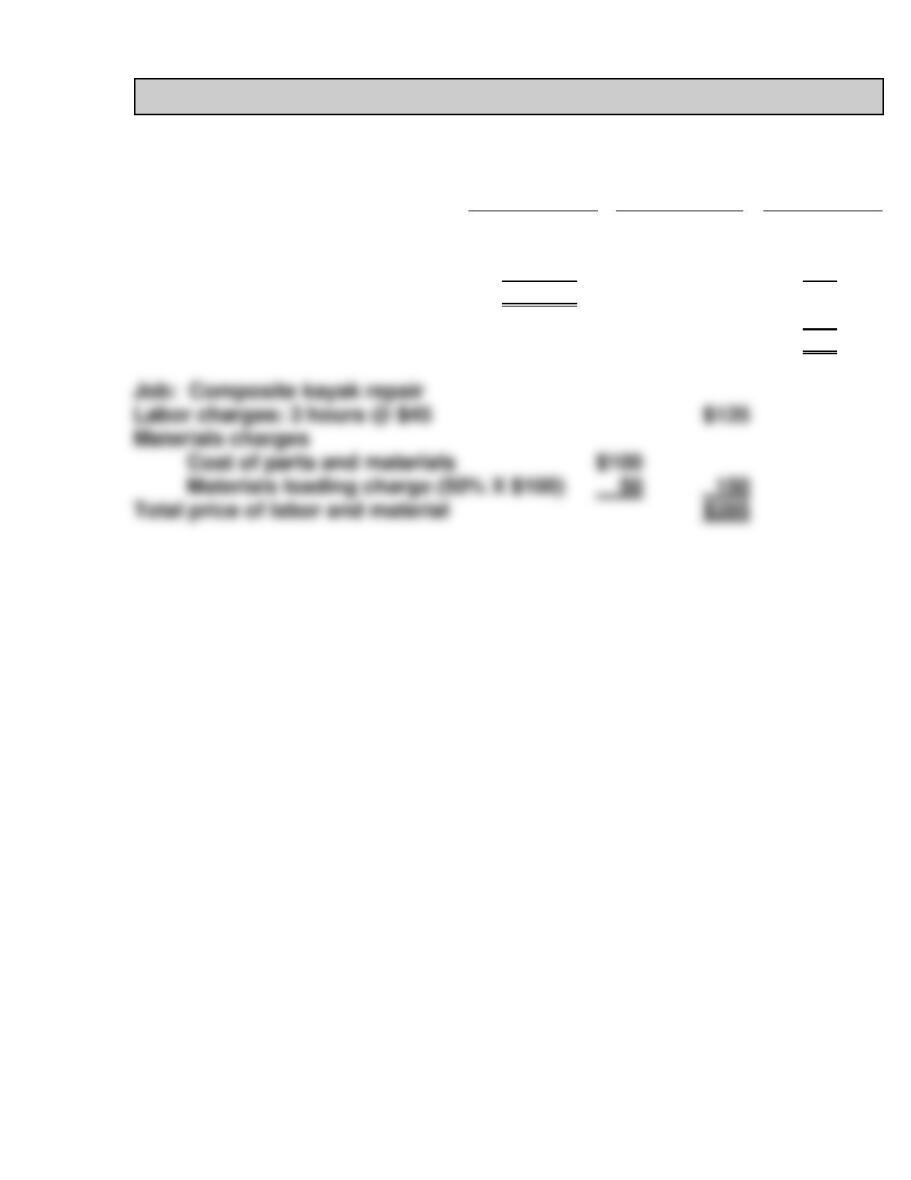

PROBLEM 8-3A (Continued)

(c) Price quotation for time and material

SUTTON’S ELECTRONIC REPAIR SHOP

Time and Material Price Quotation

January 5, 2017

Job: Fix big screen TV set

Labor charges: 4 hours @ $41.50 ……………….. $166

PROBLEM 8-4A

(a) Assuming no available capacity, the printing operation’s variable cost

is $0.004 per page and its opportunity cost is $0.006 ($0.01 – $0.004)

(b) Assuming that the printing operation has available capacity, the print–

ing operation’s variable cost is $0.004 and its opportunity cost is $0.

The minimum transfer price would be $0.004 ($0.004 + $0). Therefore,

(c) The advantages of having all of the company’s printing done intern–

ally include: (1) ensuring that the company’s quality expectations are

met, (2) ensuring that all projects are completed on a timely basis, and

(d) The printing operation would lose:

PROBLEM 8-5A

(a) The minimum transfer price is based on the variable cost of units

transferred internally, plus the opportunity cost of units sold externally.

The variable cost of internal sales would be $10 ($14.50 – $4.50). The

(b) If the Chip Division rejects the offer, each division will suffer a loss of

contribution margin, as well as the company as a whole. The amount

of this loss is calculated as:

Lost contribution margin by Board Division:

Cost of buying externally, per chip $22

Lost contribution margin by Chip Division:

Unit contribution margin on internal sales

($21 – $10) $11

Unit contribution margin on external sales

PROBLEM 8-6A

(a) Assuming no available capacity, and that the number of new units

produced would be equal to the number of standard units forgone,

variable cost of the special pager would be $80 ($50 + $30) and the

(b) Assuming no available capacity, and that in order to produce the

12,000 special pagers, 16,000 standard pagers would be forgone, the

(c) Assuming that the CD Division has available capacity, variable cost

would be $80 ($50 + $30) and the opportunity cost would be zero.

*PROBLEM 8-7A

(a) Absorption-cost pricing:

Computation of unit manufacturing cost and target selling price

Direct materials ………………………………………………………………. $ 20

Direct labor …………………………………………………………………….. 40

Variable manufacturing overhead ……………………………………. 10

(b) Variable-cost pricing:

Computation of total variable cost and target selling price

Direct materials ………………………………………………………………. $ 20

Direct labor …………………………………………………………………….. 40

Variable manufacturing overhead ……………………………………. 10

*PROBLEM 8-8A

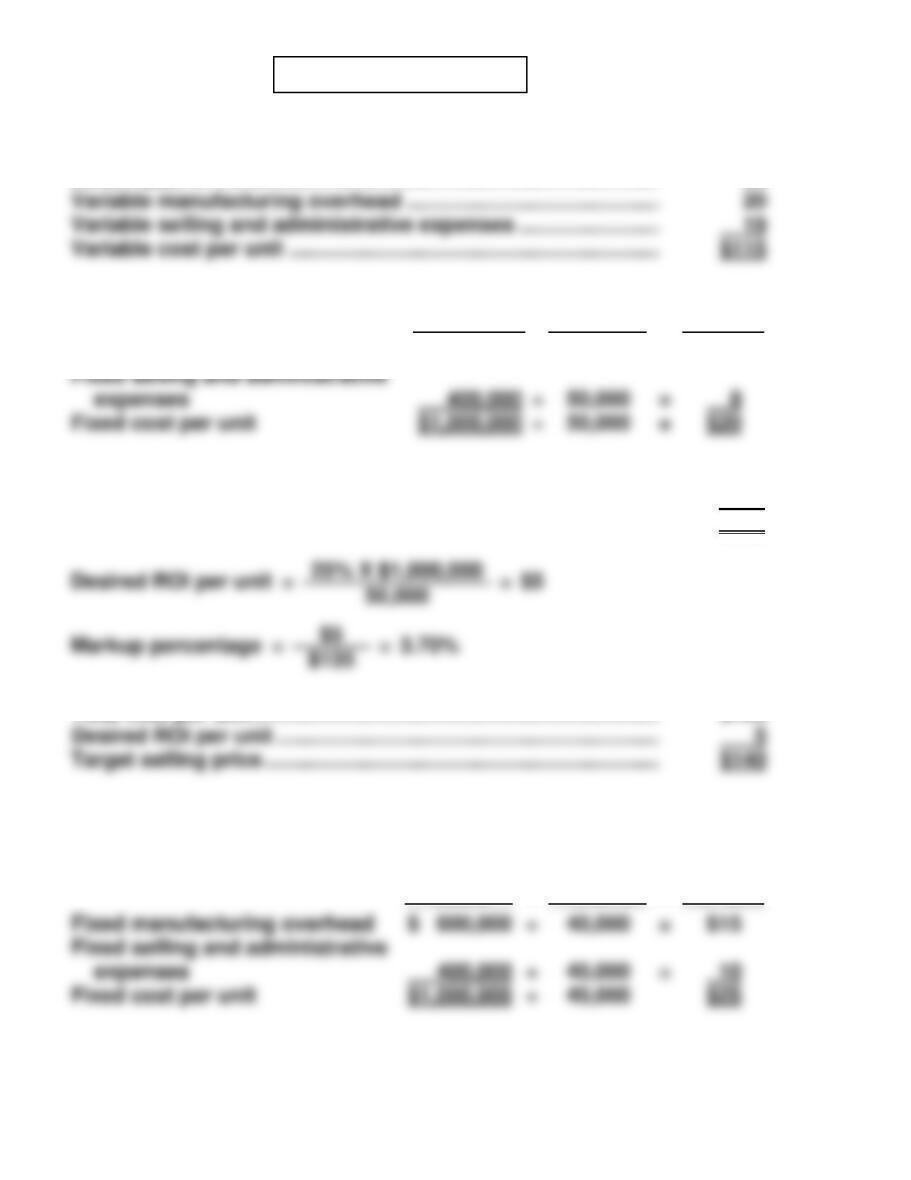

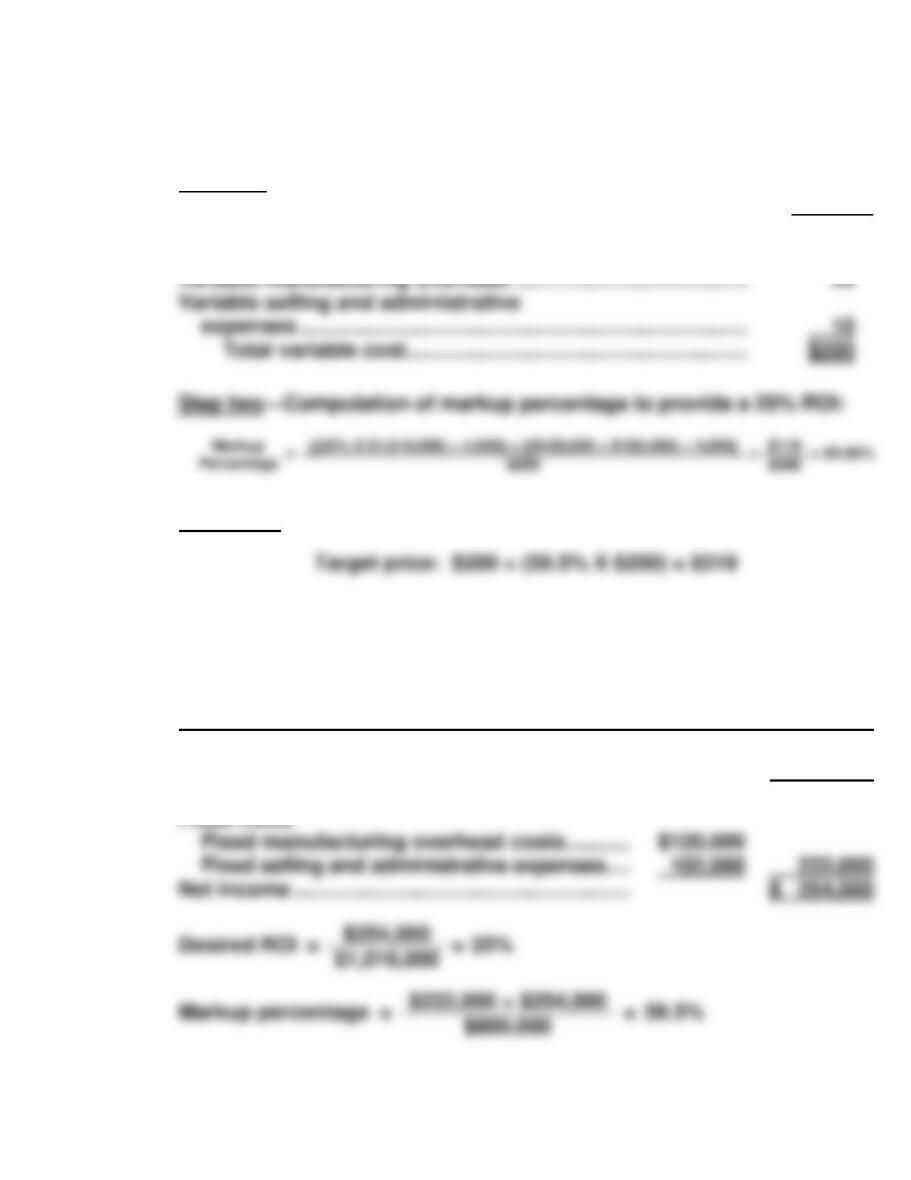

Absorption-cost pricing

(a) Step one—Computation of unit manufacturing cost:

Per Unit

Direct materials ………………………………………………………………

$100

(b) Step three—Computation of target price:

Proof of 25% ROI under absorption-cost pricing:

ANDERSON WINDOWS INC.

Budgeted Absorption-Cost Income Statement

(Tinted Window)

Revenues (4,000 units X $319) …………………………………. $1,276,000

Cost of goods sold (4,000 units X $220) ……………………. 880,000

*PROBLEM 8-8A (Continued)

Variable-cost pricing

(c) Step one—Computation of unit variable cost:

Per Unit

Direct materials ……………………………………………………….……

Direct labor …………………………………………………………………..

$100

70

(d) Step three—Computation of target price:

Proof of 25% ROI under variable-cost pricing:

ANDERSON WINDOWS INC.

Budgeted Variable-Cost Income Statement

(Tinted Window)

Revenue (4,000 units X $319) ………………………. $1,276,000

Variable costs (4,000 units X $200) ……………… 800,000

Contribution margin …………………………………… 476,000

*PROBLEM 8-8A (Continued)

(e) Both absorption-cost pricing and variable-cost pricing are used because

they have differing merits.

Absorption-cost pricing, especially when it includes full or all costs, is

preferred by some because in the long-run all costs plus a normal profit

margin must be covered. Using only variable costs, as the variable-cost

pricing does, is thought to encourage decision makers to set too low a

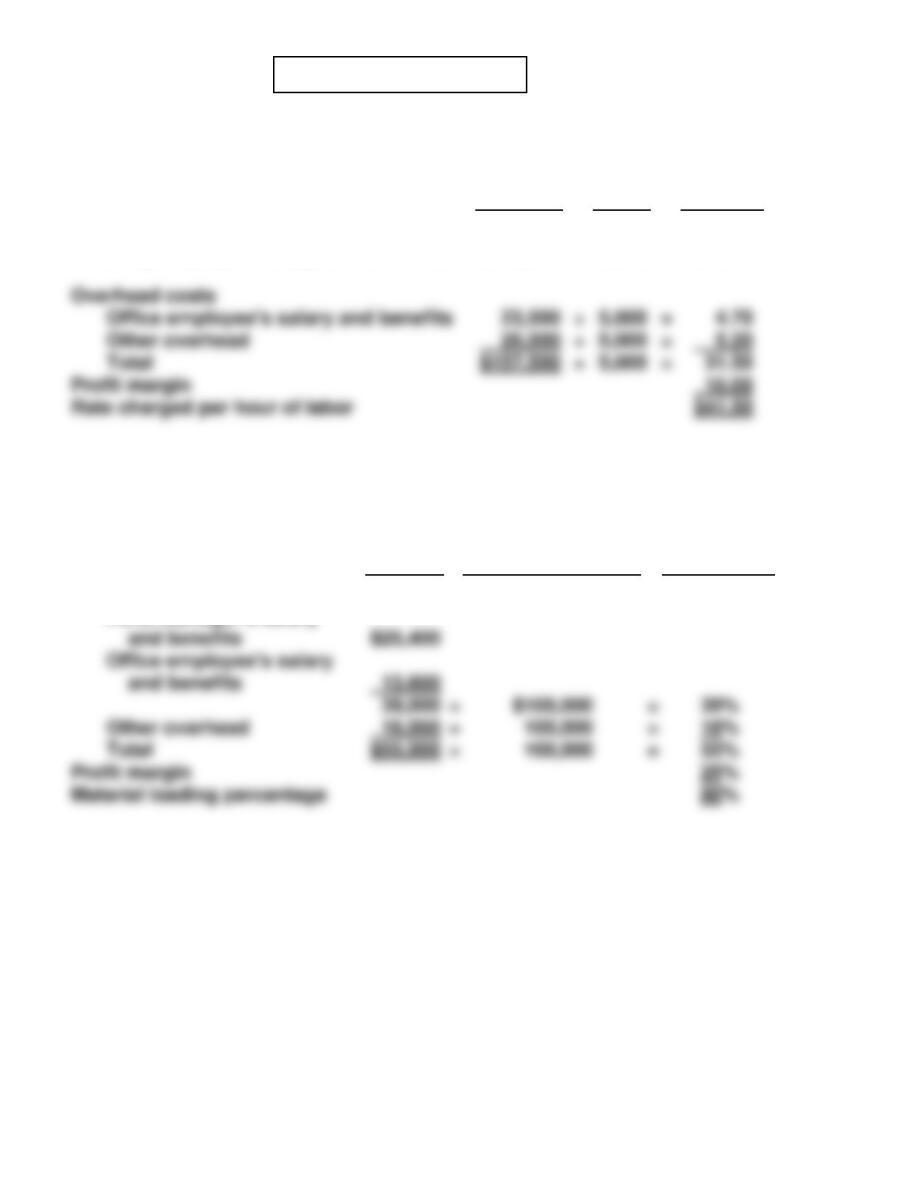

CD8 CURRENT DESIGNS

Total Cost

Total Hours

Per Hour

Charge

Repair-technician’s wages

$30,000

2,000

$15

Fringe benefits

10,000

2,000

5

Overhead

10,000

2,000

5

$50,000

2,000

25

Profit margin

20

Rate charged per hour of labor

$45

BYP 8-1 DECISION-MAKING ACROSS THE ORGANIZATION

(a) Purchasing goods from within the company offers a number of

advantages. (1) It cuts out the “middle man,” thus keeping all profits in

the company. (2) It allows the company to have more control over the

(b) Frequently the buying division will be required to buy from within the

company as long as the selling division can provide goods of compara–

ble quality and price. A selling division should not normally be forced

(c) The Wheel division would find this desirable. It would be able to get

higher quality bearings at a cost savings of $3 per set. The Bearing

division would find this very undesirable. Instead of making a profit of

(d) One possible solution is to continue on with the current situation. As

pointed out in (c), the current situation is clearly better than forcing the

Bearing division to sell its high quality bearings to a division that

BYP 8-2 MANAGERIAL ANALYSIS

(a) Dave must consider a number of issues in arriving at a price. First, he

should gather information regarding what price people would be willing

to pay for his type of service. This information could be gathered by a

marketing agency. He must consider the strengths and weaknesses of

his product. First, he is closer to housing, thus more convenient. Two,

his service is easier, especially when compared to the “self–spray”

(b) Variable cost per unit

Basic

Wash

Deluxe

Wash

Premium

Wash

expenses

0.10

Direct materials

$0.30

$0.80

$1.10

Fixed cost per unit

Total

Costs

÷

Budgeted

Volume

=

Cost

Per Unit

Fixed cost per unit

$5.50

Fixed overhead

$117,000

45,000

$2.60

BYP 8-2 (Continued)

Computation of selling price (45,000 units)

Basic

Deluxe

Premium

Variable cost per unit

$0.50

$1.50

$ 3.80

(c)

Revenues

Basic

Deluxe

Premium

Total revenues

3,000

31,000

9,000

X

X

X

$ 7.75

$ 8.75

$11.05

=

=

=

$ 23,250

271,250

99,450

$393,950

(d) Clearly, the basic wash does not use much of the more complex

capabilities of the equipment. The equipment is expensive and the

overhead related to depreciation would be a big component of the

BYP 8-3 REAL-WORLD FOCUS

(a) Pricing in the pharmaceutical industry is complicated by a number of

factors:

1. When a new drug is developed, it is patented. This protects the

company from competition for a period of time and allows the

company to charge a higher price.

4. Many prescription drugs are paid for by health insurance policies.

This complicates matters since it makes the user of the drug

insensitive to price, but makes the ultimate payer (the insurance

(b) Normally, if a difference exists in the price of a product across markets,

that difference will be eliminated as people take advantage of the

difference by shipping the goods. Eventually, the difference should be

equal to the cost of transporting and selling from one market to

another. However, in the pharmaceutical industry, barriers exist which

BYP 8-3 (Continued)

(c) In arriving at a price for a drug, the company would need to take into

account market factors as well as its costs. Ultimately, the price will be

arrived at through a combination of cost-plus pricing, market considera–

tions, and consideration of the other factors discussed in (a). When

BYP 8-4 REAL-WORLD FOCUS

(a) Answers will vary.

(b) One concern is the security of providing credit card information over

the Internet. While most security issues related to payment have been

(c) In the same way that sometimes consumers will choose a brick-and-

mortar retailer even though its prices are higher, the same is true of

the Web. For brick-and-mortar stores, the reasons for this often have

to do with location. It would appear that this would not be an issue

(d) These shopping “robot” sites have tremendous implications for retailers.

These sites make it incredibly easy for a customer to price shop. No

BYP 8-5 COMMUNICATION ACTIVITY

To: Jane Fleming

From: Student

Re: Proposal to start business with links to businesses of relatives

The student’s memo should address the following points:

1. In a traditional transfer pricing problem, the transactions are between

divisions within the same company. In the case of related divisions, the

challenge is to find a transfer price that is fair to all parties and results

BYP 8-6 ETHICS CASE

(a) The stakeholders in this case are:

• The two airlines

• The flying public in the affected cities

• Federal transportation regulators

(b) Most small airlines can keep their costs down (and therefore have a

lower break-even point) because they fly used aircraft, they pay their

(c) Jumbo services many different locations. If it loses money for a while

on one location, it can make it up on other locations. Econo doesn’t

have this luxury. This same phenomenon has been observed with

large discount stores that move into a community and initially offer

low prices until the local competition goes out of business.

(d) If it feels that Jumbo’s actions are anti-competitive, it can take Jumbo

to court. The problem is that anti-competitive behavior is difficult to

BYP 8-7 CONSIDERING YOUR COSTS AND BENEFITS

(a) A low-priced product is a product with a low initial purchase price. The

authors contrast this to a low-cost product by explaining that the initial

(b) Clarus Technologies often charges significantly higher prices for its

equipment when compared to competitive products. In order for the

company to compete, one option would be for the company to lower

(c) The five categories of costs used by the authors to evaluate the

Tornado and examples of each type of cost are:

a. Usual costs: Personnel and fuel savings.

b. Hidden costs: Insurance rates, regulatory costs, hazardous waste

disposal fees.

(d) Full-cost accounting, as developed by the EPA, looks at all costs incurred

using a product over its life-cycle. It focuses on including environmental

costs and benefits, as well as other “social costs of doing business” that