227

CHAPTER 8

LIABILITIES AND STOCKHOLDERS’ EQUITY

CLASS DISCUSSION QUESTIONS

1. Accounts payable and accruals

2. Short-term notes payable may be issued to

purchase merchandise or other assets or to

satisfy an account payable which was cre-

ated earlier.

5. (1) To pay the face (maturity) amount of the

bonds at a specified date. (2) To pay peri-

odic interest at a specified percentage of

the face amount.

6. a. Less than $40,000,000

b. 1. $40,000,000

2. 8%

3. 6%

4. $40,000,000

7. a. Premium

b. Interest Expense

b. A contingent liability should be record–

ed when it is probable and can be rea-

sonably estimated. Each year, Delta Air

Lines estimates its contingent liability

based on frequent flyer miles flown and

13. a. Unissued stock has never been issued,

but treasury stock has been issued as

fully paid and has subsequently been

reacquired.

b. As a deduction from the total of other

stockholders’ equity accounts.

14. a. It has no effect on revenue or expense.

b. It reduces stockholders’ equity by

$2,250,000.

15. a. It has no effect on revenue.

b. It increases stockholders’ equity by

228

EXERCISES

E8–1

BSF Co.

a. Earnings before bond interest and income tax ……….. $ 1,000,000

Bond interest ($7,500,000 × 8%) …………………………….. (600,000)

Balance ………………………………………………………………… $ 400,000

Income tax (40%) …………………………………………………… (160,000)

b. Earnings before bond interest and income tax ……….. $ 3,000,000

Bond interest ($7,500,000 × 8%) …………………………….. (600,000)

Balance ………………………………………………………………… $ 2,400,000

Income tax (40%) …………………………………………………… (960,000)

Net income ……………………………………………………………. $ 1,440,000

c. Earnings before bond interest and income tax ……….. $ 4,500,000

Bond interest ($7,500,000 × 8%) …………………………….. (600,000)

Balance ………………………………………………………………… $ 3,900,000

Income tax (40%) …………………………………………………… (1,560,000)

Net income ……………………………………………………………. $ 2,340,000

Dividends on preferred stock ($7,500,000 × 2%) ……… (150,000)

Earnings available for dividends on common stock .. $ 2,190,000

E8–2

Factors other than earnings per share that should be considered in evaluating

financing plans include the following: Bonds represent a fixed annual interest

229

E8–3

Current liabilities:

Accounts payable …………………………………………. $ 43,000

Accrued wages payable ………………………………… 12,200

Accrued interest payable ………………………………. 1,600*

Notes payable ………………………………………………. 96,000

E8–4

a.

Balance Sheet

Assets = Liabilities + Stockholders’ Equity

Accounts Notes

b.

Balance Sheet

Statement of Assets = Liabilities + Stockholders’ Equit

y

Cash Flows Retained

Cash = Notes Pa

y

able + Earnin

g

s

(

60,750

)

(

60,000

)

(

750

)

Statement of Cash Flows Income Statement

Operatin

g

(

60,750

)

Interest expense

(

750

)

*

*$60,000 × 5% × 90/360 = $750

230

E8–5

a. Regular pay (40 hrs. × $24) …………………………………. $ 960.00

Overtime pay (3 hrs. × $36) …………………………………. 108.00

Gross pay ………………………………………………………….. $1,068.00

E8–6

Summary: (1) $720,000; (3) $840,000; (7) $15,000; (11) $290,000

Net amount paid …………………………………………….. $ 525,000

Total deductions ……………………………………………. 315,000

(3) Total earnings ……………………………………………….. $ 840,000

Less overtime ………………………………………………… (120,000)

(1) Regular earnings ……………………………………………. $ 720,000

231

E8–7

a. FICA tax (7.5% × $90,000) ……………………………………………….. $6,750

State unemployment (2.7% × $30,000) …………………………….. 810

Federal unemployment (0.8% × $30,000) …………………………. 240

$7,800

b.

Balance Sheet

Assets = Liabilities + Stockholders’ Equit

y

FICA SUTA FUTA Retained

y

y

g

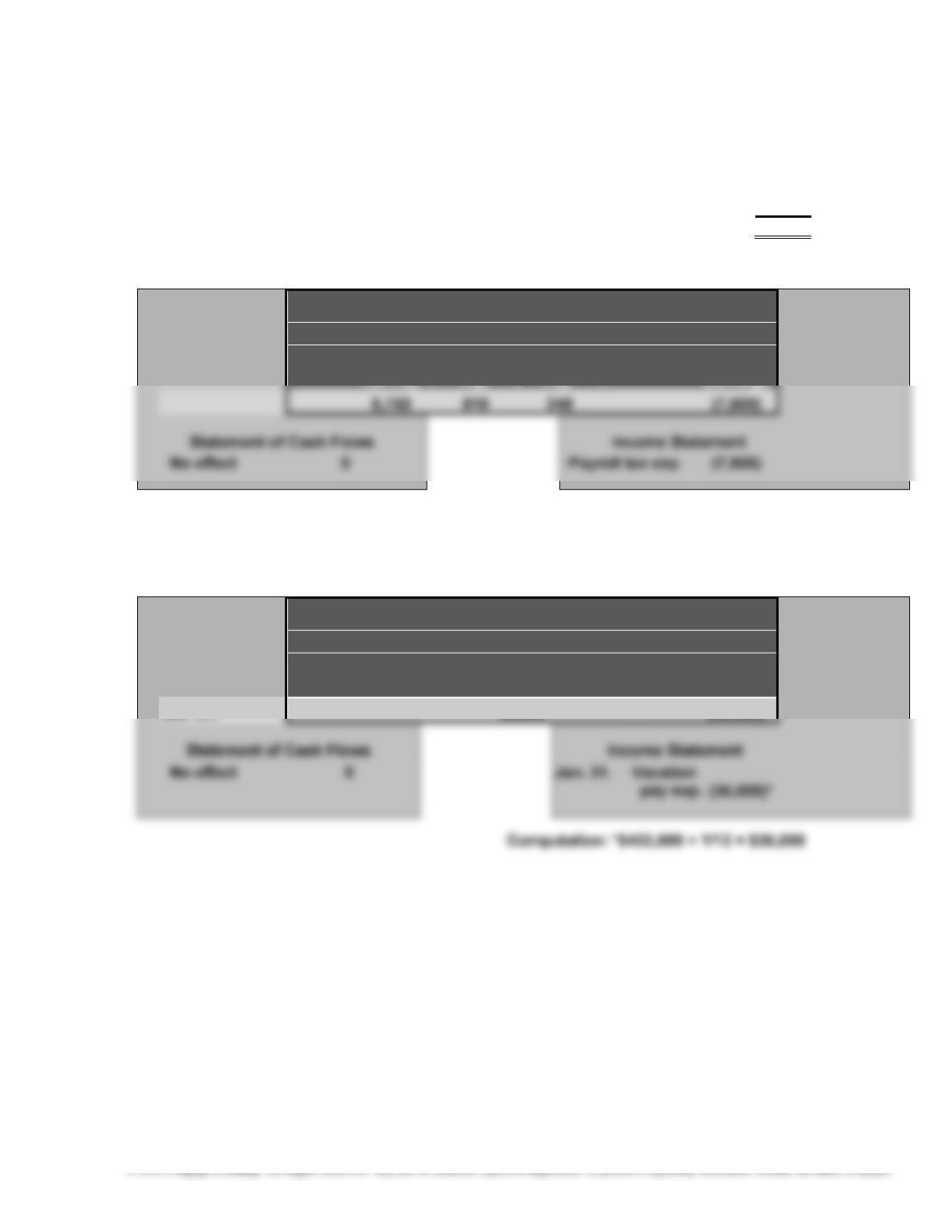

E8–8

Balance Sheet

Assets = Liabilities + Stockholders’ Equit

y

Vacation Pay Retained

Pa

y

able + Earnin

g

s

232

E8–9

The bonds sold at a premium. This is indicated by the selling price of 113.04,

which is stated as a percentage of face amount and is more than par (100%). The

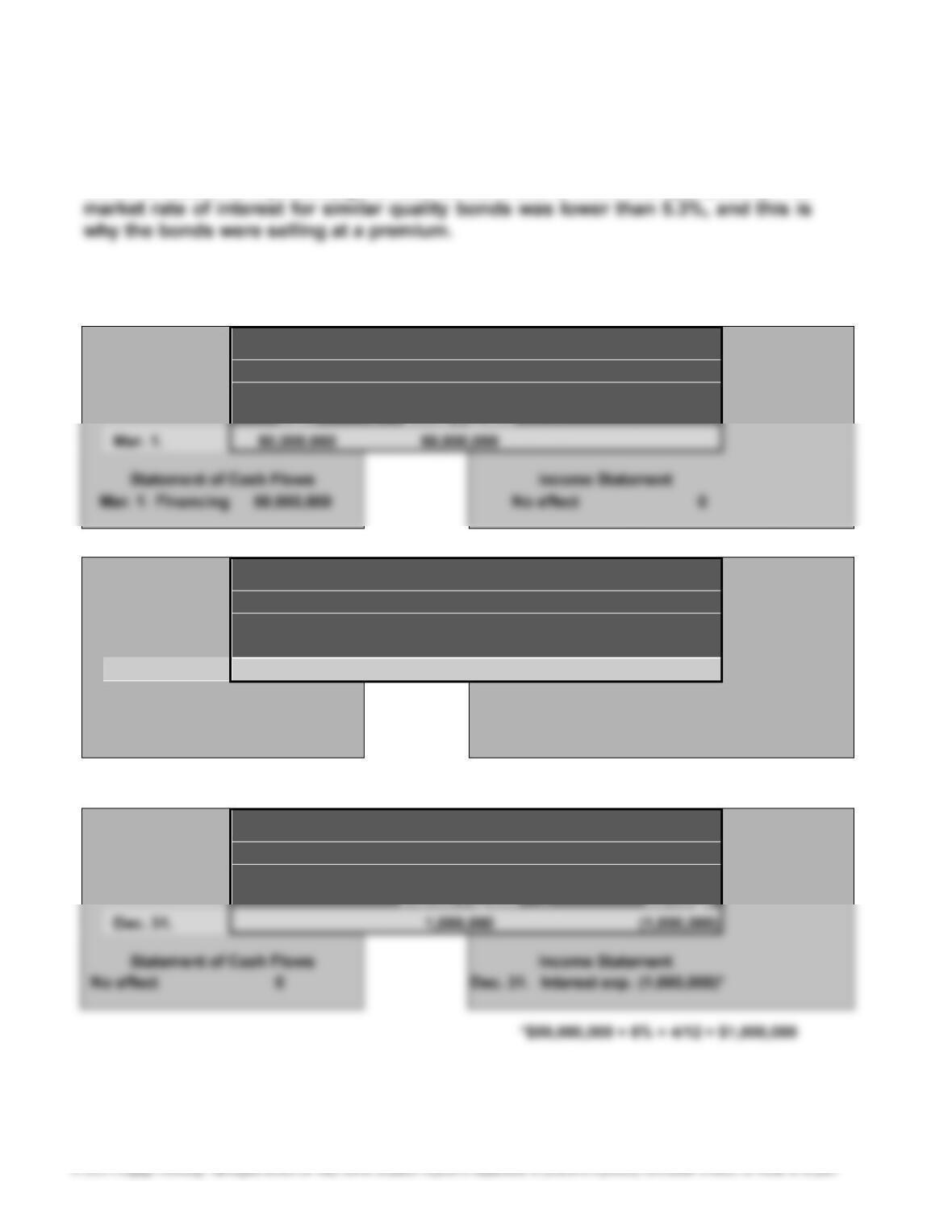

E8–10

Balance Sheet

Assets = Liabilities + Stockholders’ Equit

y

g

Balance Sheet

Assets = Liabilities + Stockholders’ Equity

Retained

Cash = Earnings

Sept. 1. (1,500,000) (1,500,000)

Statement of Cash Flows Income Statement

Sept.1. Operatin

g

(

1,500,000

)

Sept. 1. Interest exp.

(

1,500,000

)

*

*$50,000,000 × 6% × 1/2 = $1,500,000

Balance Sheet

Assets = Liabilities + Stockholders’ Equit

y

Retained

(

)

(

)

233

E8–11

a. $6,250 = $625,000 × 1%

E8–12

a.

Balance Sheet

Assets = Liabilities + Stockholders’ Equit

y

Product Warranty Retained

Pa

y

able + Earnin

g

s

3,956

(

3,956

)

Statement of Cash Flows Income Statement

No effect 0 Product

warranty

exp.

(

3,956

)

234

E8–13

a.

Balance Sheet

Assets = Liabilities + Stockholders’ Equit

y

EPA Fines Litigation Retained

Note to Instructors: The “damage awards and fines” would be disclosed on

the income statement under “other expenses.”

b. The company experienced a hazardous materials spill at one of its plants

during the previous period. This spill has resulted in a number of lawsuits to

which the company is a party. The Environmental Protection Agency (EPA)

235

E8–14

a. The adjustment to accrue litigation contingency:

Balance Sheet

Assets = Liabilities + Stockholders’ Equit

y

Contingent Product Retained

& Tort Claims Pa

y

. + Earnin

g

s

316,000,000

(

316,000,000

)

Statement of Cash Flows Income Statement

No effect 0 Litigation

exp. and

losses

(

316,000,000

)

Note to Instructors: The actual titles in the accounts may vary from those

illustrated in this answer and, in practice, will vary according to the nature of

the contingency.

236

E8–15

a.

Balance Sheet

Assets = Liabilities + Stockholders’ Equit

y

Paid-In Capital in

Common

Excess of Par—

Balance Sheet

Assets = Liabilities + Stockholders’ Equit

y

Paid-In Capital in

Preferred

Excess of Par—

237

E8–16

Balance Sheet

Assets = Liabilities + Stockholders’ Equit

y

Common Paid-In Capital in

Stock + Excess of Par—

E8–17

a. $2,100,000 (35,000 shares × $60)

E8–18

a. $1,036,000 ($37 × 28,000 shares)

b. The balance in the treasury stock account is reported as a deduction in the

Stockholders’ Equity section of the balance sheet.

238

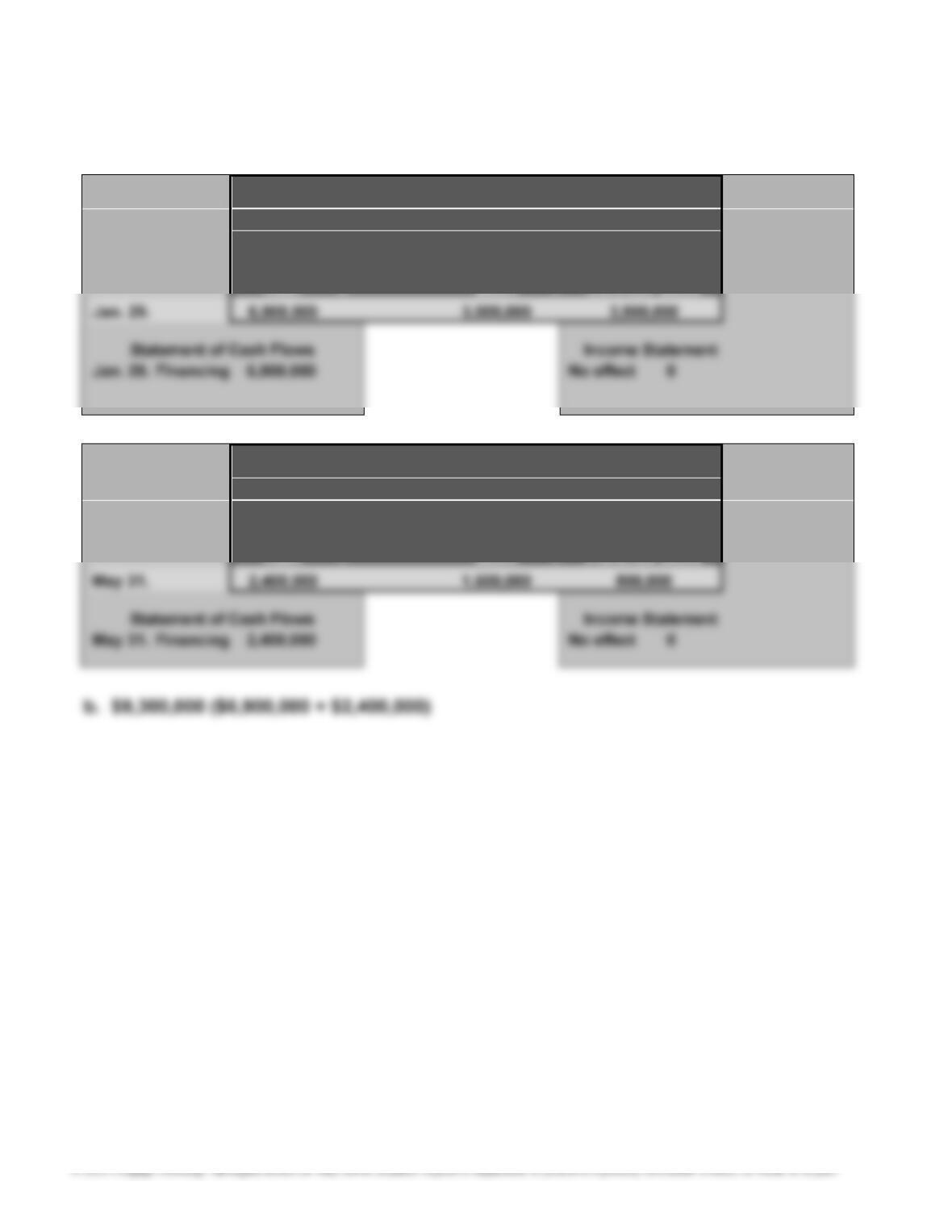

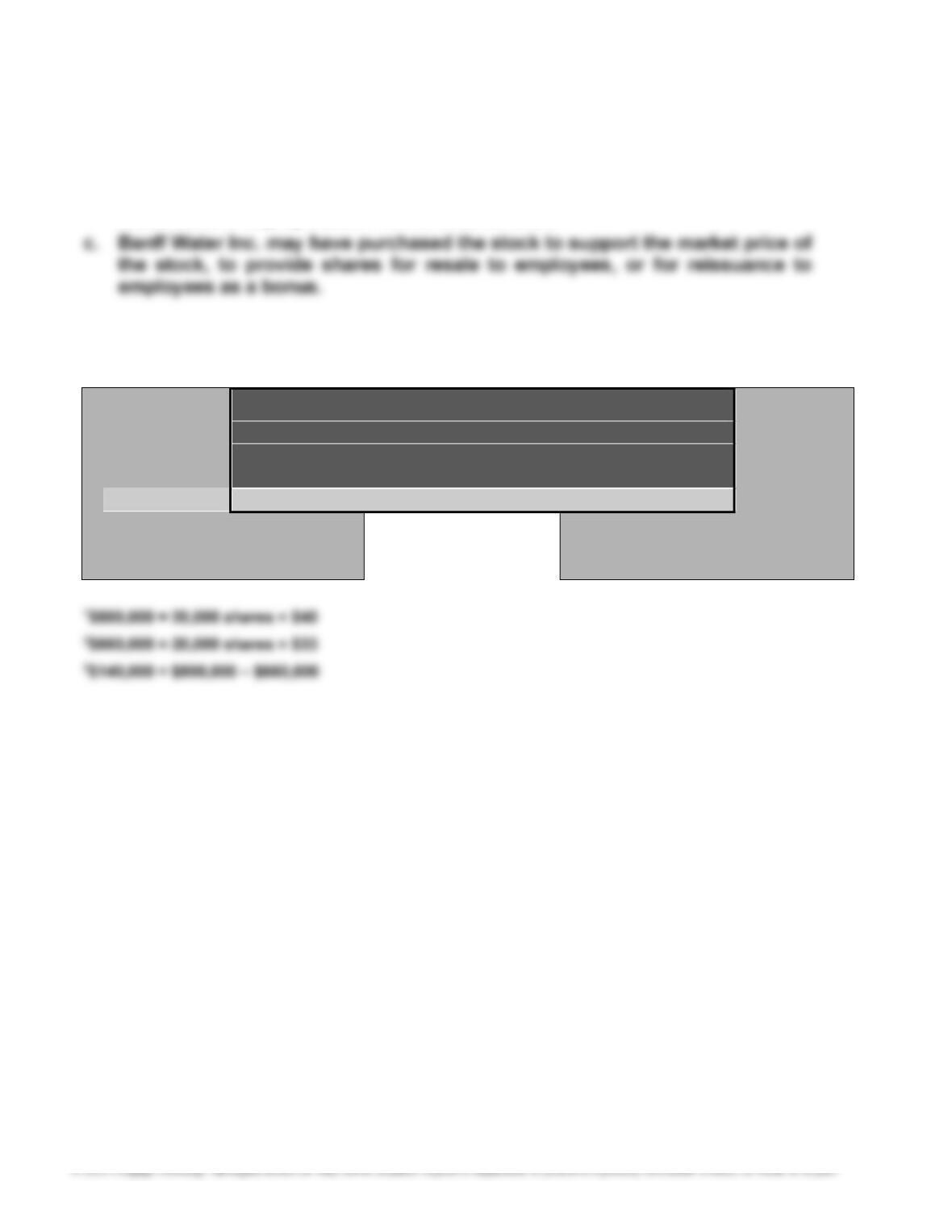

E8–19

a. $990,000 ($33 × 30,000 shares)

b. The balance in the treasury stock account is reported as a deduction in the

Stockholders’ Equity section of the balance sheet.

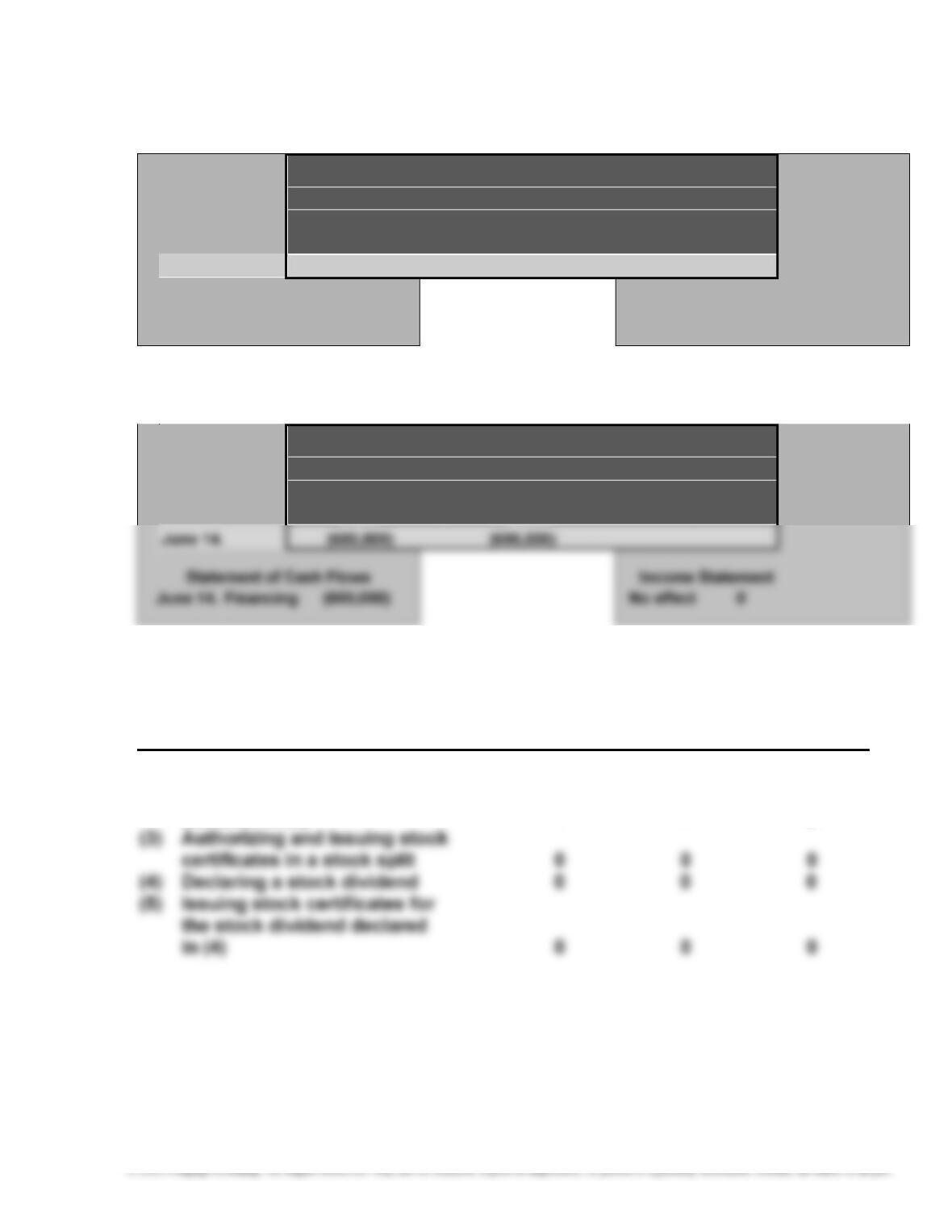

d.

Balance Sheet

Assets = Liabilities + Stockholders’ Equit

y

Treasur

y

Paid-In Capital

Cash = Stock + from Treasur

y

Stock

Jan. 25. 800,0001 660,0002 140,0003

Statement of Cash Flows Income Statement

Jan. 25. Financing 800,000 No effect 0

239

E8–20

Balance Sheet

Assets = Liabilities + Stockholders’ Equit

y

Cash Dividends Retained

Pa

y

able + Earnin

g

s

Januar

y

1. 600,000

(

600,000

)

Statement of Cash Flows Income Statement

No effect 0 No effect 0

March 15. No entry required.

Balance Sheet

Assets = Liabilities + Stockholders’ Equity

Cash Dividends

Cash = Payable

(

E8–21

Stockholders’

Assets Liabilities Equity

(1) Declaring a cash dividend 0 + –

(2) Paying the cash dividend

declared in (1) – – 0

E8–22

a. 300,000 shares (50,000 shares × 6)

b. $90 per share ($540 ÷ 6)

240

E8–23

Stockholders’ Equity

Paid-in capital:

Common stock, $40 par

(100,000 shares authorized,

75,000 shares issued*) …………….. $3,000,000

Additional paid-in capital in

excess of par …………………………….. 450,000 $ 3,450,000

Paid-in capital from treasury stock… 125,000

E8–24

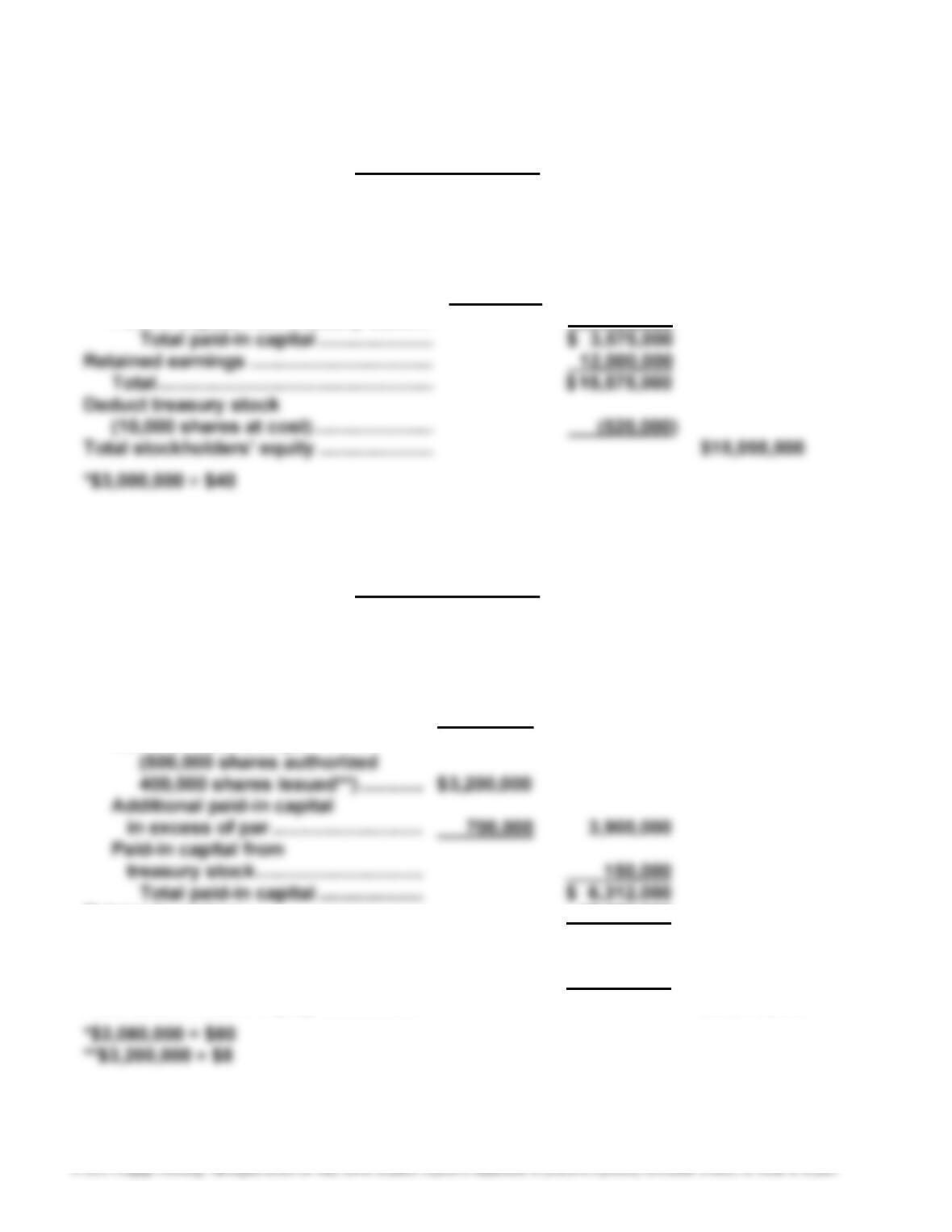

Stockholders’ Equity

Paid-in capital:

Preferred 2% stock, $80 par

(40,000 shares authorized,

26,000 shares issued*) …………… $ 2,080,000

Additional paid-in capital

in excess of par ……………………….. 182,000 $ 2,262,000

Common stock, $8 par

Retained earnings …………………………… 17,250,000

Total …………………………………………… $ 23,562,000

Deduct treasury common stock

(62,000 shares at cost) ………………… (744,000)

Total stockholders’ equity ………………. $ 22,818,000