Chapter 8 – Variable Costing and the Costs of Quality and Sustainability

8-1

CHAPTER 8

VARIABLE COSTING AND THE COSTS OF QUALITY

AND SUSTAINABILITY

Learning Objectives

1. Explain the accounting treatment of fixed manufacturing overhead under

absorption and variable costing.

2. Prepare an income statement under absorption costing.

4. Reconcile reported income under absorption and variable costing.

5. Explain the implications of absorption and variable costing for cost-volume-

profit analysis.

6. Evaluate absorption and variable costing.

8. Discuss two contrasting views of the optimal level of product quality.

Chapter 8 – Variable Costing and the Costs of Quality and Sustainability

8-2

Chapter Overview

I. Absorption and Variable Costing

A Fixed manufacturing overhead

B. Illustration of absorption and variable costing

C. Absorption-costing income statements

D. Variable-costing income statements

E. Reconciling income under absorption and variable costing

F. CVP analysis

G. Evaluation of absorption and variable costing

II. Costs of Assuring Quality

A. Measuring and reporting quality costs

B. Changing views of optimal product quality

C. ISO 9000 standards

III. Costs of Environmental Sustainability

A. Classifying environmental costs

Chapter 8 – Variable Costing and the Costs of Quality and Sustainability

8-3

Key Lecture Concepts

I. Absorption and Variable Costing

• Product, or manufacturing, costs are comprised of direct materials, direct

labor, variable manufacturing overhead, and fixed manufacturing

overhead. The basic difference between absorption and variable costing is

the treatment of fixed manufacturing overhead.

➢ With absorption (full) costing, all costs related to the manufacture

of a good are product costs. Therefore, fixed manufacturing

overhead attaches to the units being made and is carried in

inventory until the product is sold.

➢ Under variable costing, product cost is comprised solely of

variable manufacturing costs. Fixed manufacturing overhead is

viewed as a cost of being ready to produce, not an actual production

cost (i.e., the cost will remain constant no matter how many units

are manufactured).

▪ Fixed manufacturing overhead is treated as a period cost

and expensed immediately.

• Reconciliation of absorption and variable-costing income.

➢ The difference between the two approaches is the timing of when

fixed manufacturing overhead is shown on the income statement:

when the product is sold under absorption costing and when

incurred under variable costing.

Chapter 8 – Variable Costing and the Costs of Quality and Sustainability

8-4

➢ The two methods will usually produce different income figures.

▪ No change in inventory: production = sales

o Under variable costing, all fixed manufacturing

▪ Increase in inventory: production > sales

o Under variable costing, all fixed manufacturing

overhead is expensed. With absorption costing, a

portion of the period’s fixed overhead flows through

▪ Decrease in inventory: sales > production

o Under variable costing, all fixed manufacturing

overhead is expensed. With absorption costing, as

units manufactured in a prior period are sold, an

amount greater than the current period’s fixed

overhead flows through to cost of goods sold.

o Absorption-costing net income is less than variable-

costing net income.

▪ The difference between absorption- and variable-costing

income figures can be reconciled as follows:

o Income difference = Inventory change in units x Fixed

Chapter 8 – Variable Costing and the Costs of Quality and Sustainability

8-5

• CVP analysis

• Evaluation of absorption and variable costing

➢ Absorption-cost proponents argue that fixed manufacturing

overhead is a necessary production cost. Excluding this element

from the inventoried cost of a product will understate the good’s

cost, which is troublesome for companies that use cost-based

pricing techniques.

➢ Variable-cost proponents argue that variable cost is better for

pricing decisions. Any price above a good’s variable cost results in

a positive contribution margin for the company.

➢ Many firms use variable costing for internal-reporting purposes.

Given that absorption costing must be employed for external

financial reporting, companies can use both methods by making

several simple end-of-period adjustments.

➢ If a company operates in a just-in-time environment, inventories

are kept very low and there will be little change in inventory from

period to period. Thus, the income differences between absorption

and variable costing will normally be insignificant.

II. Costs of Assuring Quality

• Don’t confuse a product’s grade with its quality. Grade refers to the extent

of its capabilities in performing an intended purpose, in relation to other

products with the same functional use. Quality of design refers to how

well it is conceived or designed for its intended use. Quality of

conformance refers to the extent to which a product meets the

specification of its design.

• There are four types of quality costs.

➢ Prevention costs are the costs of preventing defects.

Chapter 8 – Variable Costing and the Costs of Quality and Sustainability

8-6

to product delivery.

➢ External failure costs are those costs incurred after product

delivery.

• The optimal level of product quality is a balancing act between the costs of

prevention and appraisal and the costs of failure (internal and external).

• Total quality management (TQM) programs monitor product quality

with measuring and reporting quality costs.

• ISO 9000 standards require that a company have a well-defined quality

control system in place and that the target level of product quality is

consistently maintained.

III. Costs of Environmental Sustainability

• Sustainable development includes business activity that produces the

goods and services needed in the present without limiting the ability of

future generations to meet their needs.

• Environmental costs are the costs of dealing with environmental issues,

• Environmental costs may be categorized in several ways.

➢ Private environmental costs are those borne by a company or

individual. Social environmental costs are those borne by the public

at large.

Chapter 8 – Variable Costing and the Costs of Quality and Sustainability

8-7

➢ Visible environmental costs are those that are known and clearly

identified as tied to environmental issues. Hidden social

environmental costs cannot be clearly tied to environmental issues.

➢ Visible and hidden environmental costs may be further classified

into one of three types.

▪ Monitoring costs include the costs of monitoring the

regulatory environment as well as monitoring the

production process to determine if pollution is being

generated.

• The International Organization for Standardization (ISO) created

standards for environmental sustainability and management known as

ISO 14000 standards.

➢ ISO 14000 is not as widely implemented as ISO 9000 standards.

Chapter 8 – Variable Costing and the Costs of Quality and Sustainability

8-8

Teaching Overview

Students sometimes have difficulty recognizing that the only difference between

absorption costing and variable costing is the treatment of fixed manufacturing

overhead. After they grasp the mechanics, students should be urged to think about the

underlying theoretical and practical differences between the two approaches.

Chapter 8 – Variable Costing and the Costs of Quality and Sustainability

8-9

Links to the Text

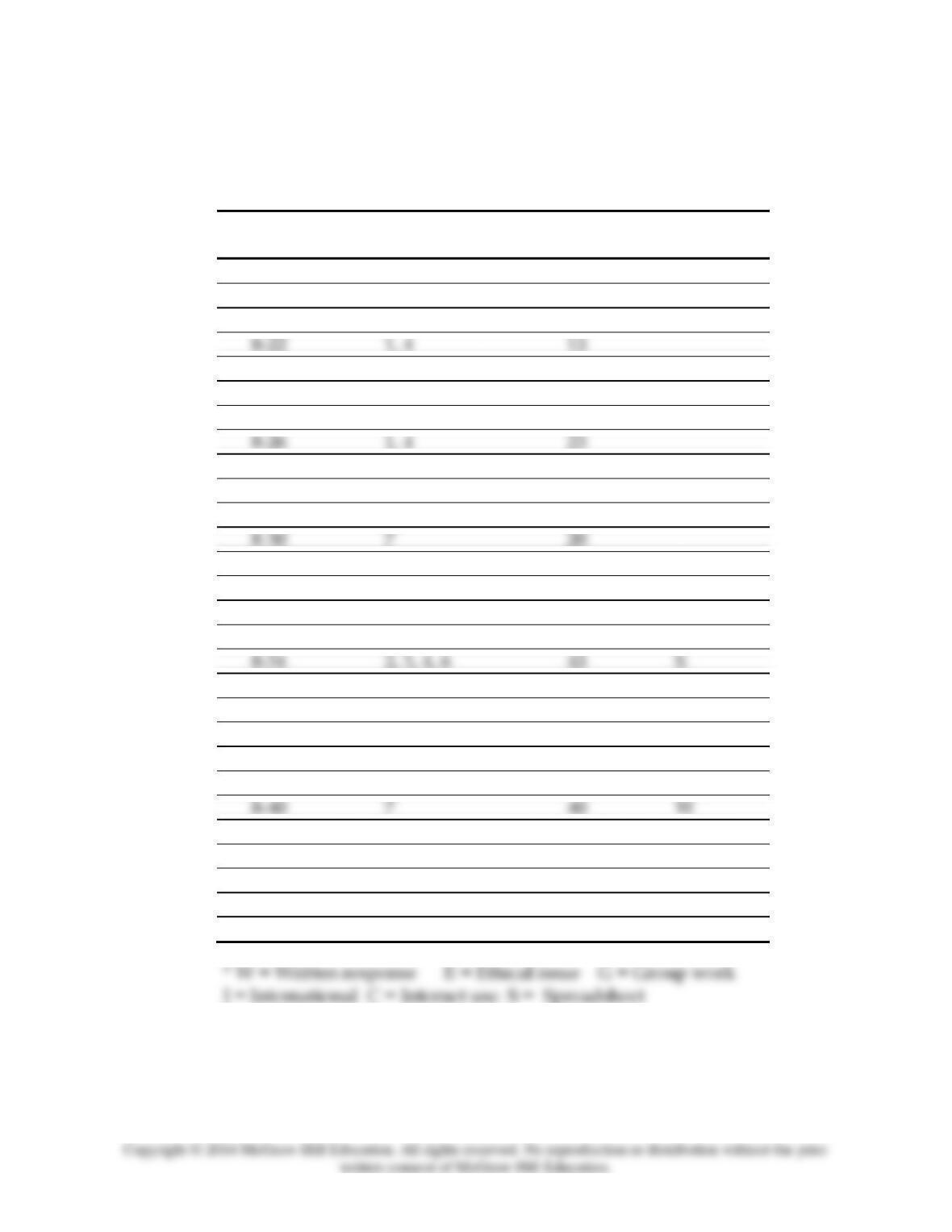

Homework Grid – CHAPTER 8

Item No.

Learning

Objectives

Completion

Time (min.)

Special

Features*

Exercises:

8-20

1, 4

15

8-21

5

20

W

8-22

1, 4

15

8-23

1, 4

15

8-24

1

10

8-25

1

30

C

8-26

1, 4

25

8-27

1

10

8-28

7

10

8-29

7

5

I

8-30

7

20

8-31

9

45

C

Problems:

8-32

2, 3, 4

45

8-33

4, 5, 6

45

8-34

2, 3, 4, 6

45

S

8-35

1, 4

25

I

8-36

1, 2, 3

35

8-37

4

45

8-38

2, 3, 4, 6

40

8-39

7

35

8-40

7

40

W

8-41

9

60-180

G, W

Cases:

8-42

2, 3, 4

45

S

8-43

1, 4

30

8-44

1, 4

40