8

Process Costing

Solutions to Review Questions

8-1.

8-2.

Using the basic cost flow equation, rearrange the terms to solve for the unknown

8-3.

With FIFO costing, the units in the beginning inventory are transferred out first. These

beginning inventory units carry with them the costs incurred in a previous period plus the

8-4.

The five steps are:

1) Measure the physical flow of resources.

8-5.

Under FIFO costing, the equivalent units represent only the work done in the current

8-6.

8-7.

Prior department costs behave the same as direct materials, which are typically added at

the start of production. They are treated separately because they represent the

8-8.

8-9.

Solutions to Critical Analysis and Discussion Questions

8-10.

To assign costs to specific barrels of liquid cleaning products or similarly mass–produced

8-11.

This is a fairly common problem. LIFO is usually beneficial for tax purposes when prices

are rising and inventory levels are steady or rising. However, maintaining internal records

8-12.

The results will be the same using either costing system. The important point is that job

8-13.

Answers will differ. Factors to consider include: (a) the relative size of beginning work–in–

8-14.

We could treat direct labor costs and manufacturing overhead as a single resource

8-15.

It is not necessary that both departments use the same cost-flow assumption. Department

8-16.

With prior period costs, a department manager often does not control the decision to

8-17.

It is unlikely, but not impossible, for process costing to work well in a service firm. Process

Solutions to Exercises

8-18. (20 min.) Compute Equivalent Units—Weighted-Average Method: Conlon

Chemicals.

a.

Materials

b.

Conversion Costs

– 157,500 units transferred out.

8-19. (20 min.) Compute Equivalent Units—FIFO method: Conlon Chemicals.

Compute Equivalent Units—FIFO

a.

Materials

b.

Conversion Costs

To complete beginning inventory:

Materials: 50%a x 30,000 units…………………..

15,000

EU

Conversion costs: 70%b x 30,000 units ……….

EU

Started and completed during the period ………..

EU

EU

Materials: 10% x 52,500d units…………………..

EU

EU

Alternative Method:

Conversion Costs:

157,500 units

Equivalent

units of work

=

Units

transferred

+

EU

ending

–

EU

beginning

8-20. (15 min.) Compute Equivalent Units—Weighted-Average Method: Pierce &

Company.

a.

Materials

b.

Conversion

Costs

Units transferred out ………………………………………..

210,000

210,000

Equivalent units in ending inventory:

140,000

Total equivalent units for all work done to date ……

8-21. (20 min.) Compute Equivalent Units—FIFO method: Pierce & Company.

a.

Materials

b.

Conversion

Costs

To complete beginning inventory:

Materials: 0%b x 98,000a units …………………………

0

EU

Conversion costs: 60%c x 98,000 units ……………..

58,800

EU

Started and completed during the period ………………

Units still in ending inventory:

EU

63,000

EU

EU

a 98,000 units in beginning inventory

Alternative Method

Materials:

Conversion Costs:

Equivalent

units of work

=

Units

transferred

+

EU

ending

–

EU

beginning

8-22. (30 min.) Compute Equivalent Units: Magic Company.

a. Weighted-average method:

Materials

Conversion

Costs

Units transferred out ……………………………………………….

480,000

480,000

Materials

Conversion

Costs

To complete beginning inventory:

Materials: 0%a x 72,000 units ……………………

0

EU

Conversion costs: 40%b x 72,000 units ……….

28,800

EU

Started and completed during the periodc ………

EU

EU

Materials: 100% x 72,000 units ………………….

EU

EU

480,000

EU

EU

8-23. (10 min.) Equivalent Units: Weighted-Average Process Costing.

(e). None of these answers are correct.

8-24. (30 min.) Compute Equivalent Units—Ethical Issues: Aaron Company.

a. Weighted-average method:

Materials

Conversion

Costs

Units transferred out ………………………………………..

630,000

630,000

Conversion costs: 40% x 120,000 units …………..

b. First-in, First-out (FIFO) method:

a.

Materials

b.

Conversion

Costs

To complete beginning inventory:

Materials: 0%a x 150,000 units …………………..

0

EU

Started and completed during the periodc ……….

EU

EU

Materials: 0% x 120,000 units…………………….

EU

480,000

c.

8-25. (10 min.) Equivalent Units and Cost of Production.

If the percentage completion is overstated, (a) the total equivalent units for the period will

be overstated, because the work-in-process ending inventory will be assumed to have

8-26. (20 min.) Compute Cost per Equivalent Unit—Weighted-Average Method:

Moline Facility.

Physical

Units

Materials

Eq. Units

Flow of units:

Units to be accounted for:

Beginning WIP inventory …………………………..

54,000

Units started this period…………………………….

Total units to account for ……………………….

Completed and transferred out

Materials (153,000 x 100%) ……………………

Units in ending inventory:

Materials (45,000 x 100%) ……………………..

Total units accounted for …………………….

Flow of costs:

Costs to be accounted for:

Costs in beginning WIP inventory …………………………..

Current period costs ……………………………………………..

Total costs to be accounted for …………………………...

Materials ($623,700 ÷ 198,000 units) ……………………..

8-27. (20 min.) Compute Cost per Equivalent Unit—FIFO method: Moline Facility.

Physical

Units

Materials Eq.

Units

Flow of units:

Units to be accounted for:

Beginning WIP inventory ………………………………….

54,000

Units started this period ……………………………………

144,000

Total units to account for ……………………………….

198,000

Completed and transferred out

From beginning WIP inventory (54,000 x 100%)

99,000

Units in ending inventory:

Materials (45,000 x 100%) …………………………….

Total units accounted for …………………………...

198,000

Direct

Materials

Flow of costs:

Costs to be accounted for:

Total costs to be accounted for (current period costs only) ………..

$475,200

Cost per equivalent unit

Materials ($475,200 ÷ 144,000 units) ……………………………………….

8-28. (20 min.) Compute Equivalent Units—FIFO method: Campo Company.

Physical

Units

Conversion

Eq. Units

Flow of units:

Units to be accounted for:

Beginning WIP inventory ……………………………………….

90,000

Units started this period…………………………………………

Total units to account for ……………………………………

Units accounted for:

Completed and transferred out

From beginning WIP inventory [90,000 x (1 – 70%)]

90,000

Units in ending inventory:

Conversion (150,000 x 40%) ………………………………

Total units accounted for …………………………………

8-29. (20 min.) Compute Equivalent Units and Cost per Equivalent Unit—

Weighted-Average method: Campo Company.

a.

Physical

Units

Equivalent Units

Materials

Eq. units

Conversion

Costs Eq. units

Flow of units:

Units to be accounted for:

Beginning WIP inventory …………………………..

90,000

Units started this period …………………………….

1,020,000

Total units to account for ………………………..

Completed and transferred out …………………..

Units in ending inventory …………………………..

Materials (150,000 x 100%) ……………………

Conversion costs (150,000 x

40%) ………………………………………………………….

Total units accounted for ………………………..

b.

Total

Direct

Materials

Conversion

Costs

Flow of costs:

Costs to be accounted for:

$35,670

$2,076,000

$444,000

Cost per equivalent unit

units) ………………………………………………………..

8-30. (10 min.) Cost Per Equivalent Unit: Weighted-Average Method.

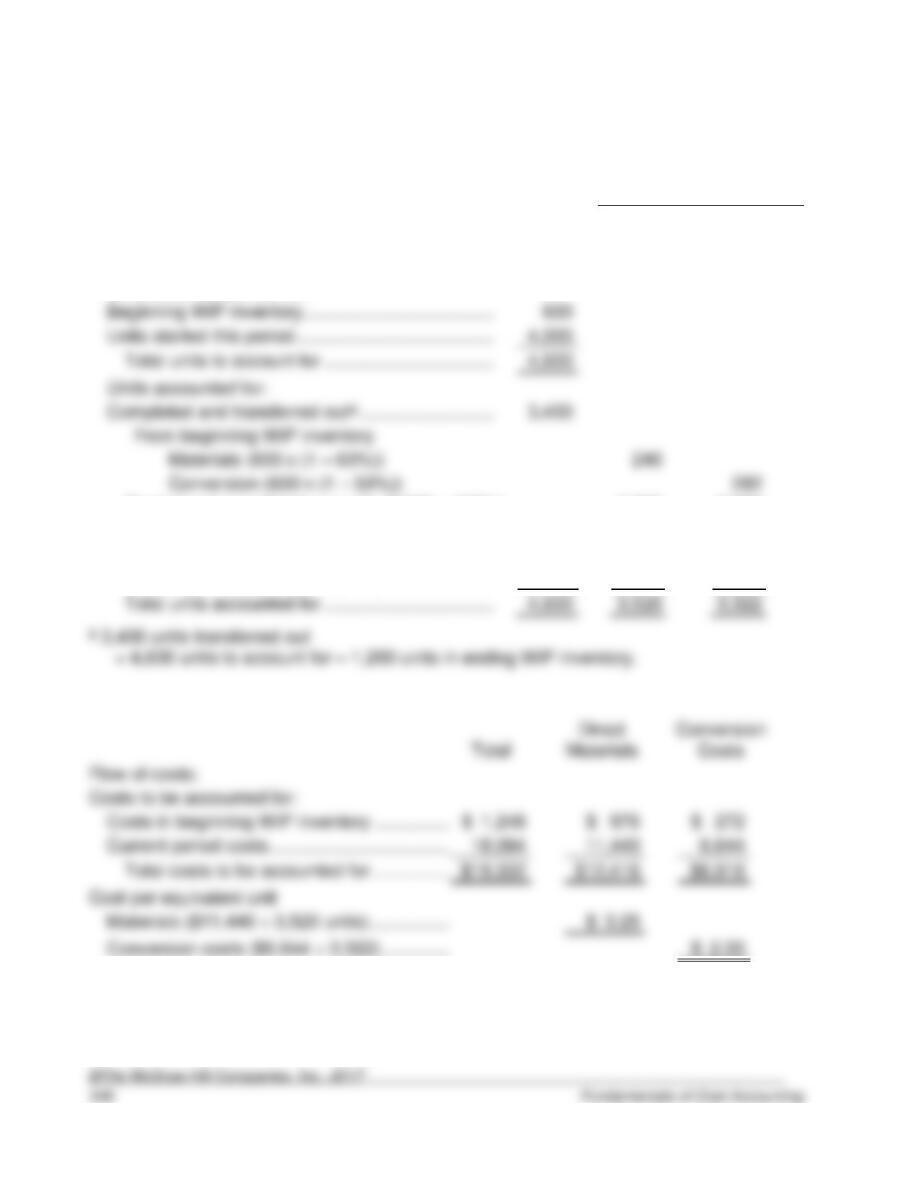

8-31. (35 min.) Compute Costs per Equivalent Unit—Weighted-Average Method:

Matsui Lubricants.

Physical

Units

Equivalent Units

Materials

Eq. units

Conversion

Costs Eq. units

Flow of units:

Units to be accounted for:

Beginning WIP inventory …………………………..

600

Units started this period…………………………….

4,000

Total units to account for ……………………….

4,600

3,400

3,400

Units in ending inventory …………………………..

1,200

Materials (1,200 x 40%) …………………………

Conversion costs (1,200 x 20%) ……………..

Total units accounted for ……………………….

4,600

3,880

a 3,400 units transferred out = 4,600 units to account for – 1,200 units in ending WIP

inventory.

Total

Direct

Materials

Conversion

Costs

Flow of costs:

Costs to be accounted for:

Costs in beginning WIP inventory ………

$ 1,248

$ 976

$ 272

$12,416

Cost per equivalent unit

8-32. (20 min.) Assign Costs to Goods Transferred Out and Ending Inventory—

Weighted-Average Method: Matsui Lubricants.

Total

Direct

Materials

Conversion

Costs

Flow of costs:

Costs to be accounted for:

Costs in beginning WIP inventory ……………….

$ 1,248

$ 976

$ 272

Current period costs …………………………………

18,084

11,440

Total costs to be accounted for ……………….

$19,332

$12,416

Cost per equivalent unit

Materials ($12,416 ÷ 3,880 units) ……………….

$ 3.20

Conversion costs ($6,916 ÷ 3,640) ……………..

$ 1.90

Costs accounted for:

$17,340

$10,880

Cost of ending WIP inventory …………………….

$19,332

$12,416

8-33. (35 min.) Compute Costs per Equivalent Unit—FIFO Method: Matsui

Lubricants.

Physical

Units

Equivalent Units

Materials

Eq. units

Conversion

Costs Eq. units

Flow of units:

Units to be accounted for:

Beginning WIP inventory ………………………………..

Units started this period………………………………….

Total units to account for …………………………….

From beginning WIP inventory

Materials (600 x (1 – 60%))

Conversion (600 x (1 – 53%))

282

Started and completed currently (2,800 x 100%)

2,800

2,800

Units in ending inventory ………………………………..

1,200

Materials (1,200 x 40%) ………………………………

480

Conversion costs (1,200 x 20%) …………………..

240

Total units accounted for …………………………….

4,600

Costs

Flow of costs:

Costs to be accounted for:

Cost per equivalent unit

8-34. (20 min.) Assign Costs to Goods Transferred Out and Ending Inventory—

FIFO Method: Matsui Lubricants.

Physical

Units

Equivalent Units

Materials

Eq. units

Conversion Costs

Eq. units

Flow of units:

Units to be accounted for:

Beginning WIP inventory …………………………..

600

Units started this period …………………………….

Total units to account for ………………………..

From beginning WIP inventory

Materials (600 x (1 – 60%))

Conversion (600 x (1 – 53%))

(2,800 x 100%) ……………………………………..

Units in ending inventory …………………………..

Materials (1,200 x 40%) …………………………

Conversion costs (1,200 x 20%) ……………..

Total units accounted for ………………………..

8-34. (continued)

Total

Direct

Materials

Conversion

Costs

Flow of costs:

Costs to be accounted for:

18,084

6,644

Total costs to be accounted for ……………….

Cost per equivalent unit

out:

Current costs added to complete

beginning WIP inventory ………………………………

1,344

Materials ($3.25 x 240) …………………..

780

Conversion costs ($2.00 x 282) ……….

564

completed:

Total costs transferred out …………………………...

Cost of ending WIP inventory ……………………….

2,040

Current costs of units started and

14,700

8-35. (35 min.) Compute Costs per Equivalent Unit—Weighted-Average Method:

Pacific Ink.

Physical

Units

Equivalent Units

Materials

Eq. units

Conversion Costs

Eq. units

Flow of units:

Units to be accounted for:

Total units to account for ………………………..

Completed and transferred out (given) ………..

Units in ending inventory …………………………..

Conversion costs (30,000 x 40%) ……………

12,000

Total units accounted for ………………………..

Total

Direct

Materials

Conversion

Costs

Flow of costs:

Costs to be accounted for:

Costs in beginning WIP inventory ……………….

$ 744,960

$ 304,920

$ 440,040

Current period costs …………………………………

2,343,600

Cost per equivalent unit

Materials ($2,648,520 ÷ 126,000 units) ……….

Conversion costs ($3,467,880 ÷ 114,000) ……

8-36. (20 min.) Assign Costs to Goods Transferred Out and Ending Inventory—

Weighted-Average Method: Pacific Ink.

Total

Direct

Materials

Conversion

Costs

Flow of costs:

Costs to be accounted for:

Costs in beginning WIP inventory ………………

$ 744,960

$ 304,920

$ 440,040

Current period costs …………………………………

5,371,440

2,343,600

3,027,840

Total costs to be accounted for ……………….

$6,116,400

$2,648,520

$3,467,880

Cost per equivalent unit

Materials ($2,648,520 ÷ 126,000 units) ……….

Conversion costs ($3,467,880 ÷ 114,000)……

Costs accounted for:

Cost of ending WIP inventory …………………….

8-37. (35 min.) Compute Costs per Equivalent Unit—FIFO Method: Pacific Ink.

Physical

Units

Equivalent Units

Materials

Eq. units

Conversion

Costs Eq.

units

Flow of units:

Units to be accounted for:

Units accounted for:

Completed and transferred out

102,000

From beginning WIP inventory

Materials (48,000 x (1 – 30%)) ……

Conversion (48,000 x (1 – 30%)) ..

Started and completed …………………….

Materials (30,000 x 80%) …………………..

Total

Direct

Materials

Conversion

Costs

Flow of costs:

Costs to be accounted for:

Costs in beginning WIP inventory ……………….

$ 744,960

$ 304,920

$ 440,040

5,371,440

2,343,600

3,027,840

Cost per equivalent unit

8-38. (20 min.) Assign Costs to Goods Transferred Out and Ending Inventory—

FIFO Method: Pacific Ink.

Physical

Units

Equivalent Units

Materials

Eq. units

Conversion

Costs Eq. units

Flow of units:

Units to be accounted for:

Beginning WIP inventory …………………………..

48,000

Total units to account for ……………………….

Completed and transferred out

To complete beginning WIP inventory

Materials (48,000 x (1 – 30%)) ………..

Conversion (48,000 x (1 – 30%)) …….

Started and completed …………………………

Units in ending inventory …………………………..

30,000

Materials (30,000 x 80%) ……………………….

Conversion costs (30,000 x 40%) ……………

Total units accounted for ……………………….

8-38. (continued)

Total

Direct

Materials

Conversion

Costs

Flow of costs:

Costs to be accounted for:

Current period costs …………………………………

Materials ($2,343,600 ÷ 111,600 units) ……….

Conversion costs ($3,027,840 ÷ 99,600) ……..

Costs accounted for:

Costs assigned to units transferred out:

Costs from beginning WIP inventory ………..

$ 744,960

$ 304,920

$ 440,040

beginning WIP inventory …………………..

Materials ($21.00 x 33,600) …………………..

completed: ……………………………………….

Materials ($21.00 x 54,000) …………………..

Total costs transferred out …………………………...

Materials ($21.00 x 24,000) …………………..

Conversion costs ($30.40 x 12,000) ……….

Total costs accounted for ………………………….

Current costs added to complete

costs are lower under FIFO.

8-39. (50 min.) Prepare a Production Cost Report—FIFO method: Lansing, Inc.

Physical Units

Equivalent Units

Prior

Department

Department

No. T

Flow of units:

Units to be accounted for:

Beginning WIP inventory …………………………..

15,000

Units started this period…………………………….

35,000

Completed and transferred out

Units in ending WIP inventory ……………………….

8-39. (continued)

Total

Prior

Department

Department

No. T

Flow of costs:

Costs to be accounted for:

Costs in beginning WIP inventory ……………….

$169,150

$116,000

$ 53,150

Current period costs …………………………………

489,050

280,000

209,050

Total costs to be accounted for ……………….

$396,000

$262,200

Cost per equivalent unit

Prior department ($280,000 ÷ 35,000 units) ..

Department. T ($209,050 ÷ 37,000 units) ……

Costs assigned to units transferred out:

$116,000

beginning WIP inventory ………………………………

Prior department ………………………………..

Department T ($5.65 x 6,000 units) ……..

completed: ………………………………………………..

Total costs transferred out …………………………...

$356,000

Cost of ending WIP inventory ………………………..

Prior department ($8.00 x 5,000) …………

40,000

Total costs accounted for ……………………….

$658,200

$396,000

$262,200

8-40. (50 min.) Prepare a Production Cost Report—Weighted-Average Method:

Lansing Inc.

a.

Physical

Units

Equivalent Units

Prior

Department

Department

No. T

Flow of units:

Units to be accounted for:

Beginning WIP inventory …………………………..

15,000

Units started this period…………………………….

35,000

Completed and transferred out …………………..

45,000

45,000

Total

Prior

Department

Department

No. T

Flow of costs:

Costs to be accounted for:

Costs in beginning WIP inventory ………………

$169,150

$116,000

$ 53,150

Current period costs …………………………………

$396,000

$262,200

Cost per equivalent unit

Prior department ($396,000 ÷ 50,000 units) …

Department No. T ($262,200 ÷ 46,000) ………

Costs accounted for:

$356,400

$256,500

Costs of ending WIP inventory …………………..

45,300

$396,000

$262,200

8-40. (continued)

c. The decision depends on the decisions that will be made using the data. If the most

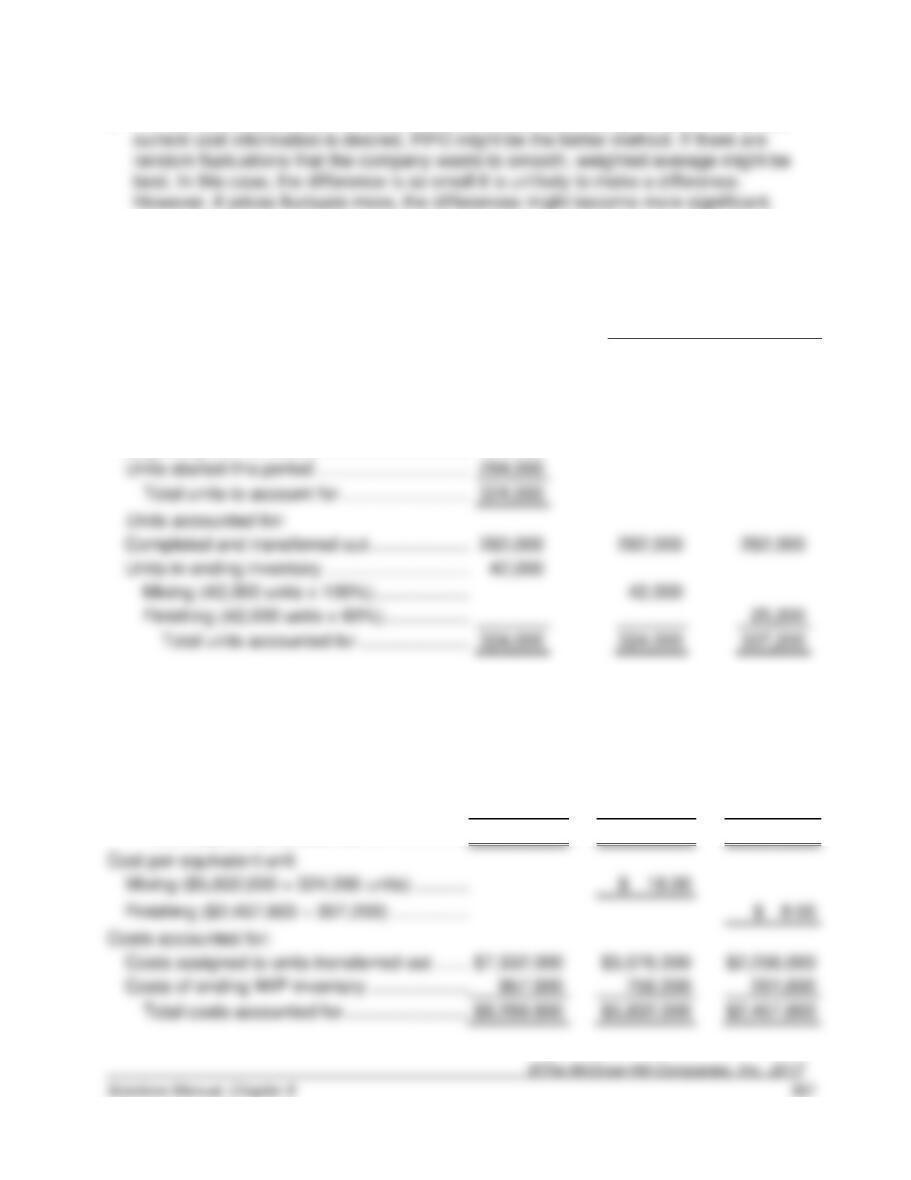

8-41. (50 min.) Prepare a Production Cost Report—Weighted-Average Method:

Yarmouth Company.

Physical

Units

Equivalent Units

Mixing

Department

Finishing

Department

Flow of units:

Units to be accounted for:

Beginning WIP inventory …………………………..

30,000

Units started this period …………………………….

Total units to account for ………………………..

Units accounted for:

Completed and transferred out …………………..

Units in ending inventory …………………………..

Mixing (42,000 units x 100%) ………………….

Total units accounted for …………………….

Total

Direct

Materials

Conversion

Costs

Flow of costs:

Costs to be accounted for:

Costs in beginning WIP inventory ……………….

$723,636

$657,600

$ 66,036

Current period costs …………………………………

7,565,964

5,174,400

2,391,564

Total costs to be accounted for ……………….

$8,289,600

$5,832,000

$2,457,600

Cost per equivalent unit

Mixing ($5,832,000 ÷ 324,000 units) …………..

Finishing ($2,457,600 ÷ 307,200) ……………….

Costs accounted for:

Costs assigned to units transferred out ……….

$2,256,000

Costs of ending WIP inventory …………………..

Total costs accounted for ……………………….

$8,289,600

$5,832,000

$2,457,600

8-42. (50 min.) Production Cost Report—FIFO method: Yarmouth Company.

a.

Physical Units

Equivalent Units

Mixing

Department

Finishing

Department

Flow of units:

Units to be accounted for:

Beginning WIP inventory …………………………..

30,000

Units started this period…………………………….

Completed and transferred out

Units in ending WIP inventory ……………………….

298,200

8-42. (continued)

Total

Mixing

Department

Finishing

Department

Flow of costs:

Costs to be accounted for:

Costs in beginning WIP inventory ……………….

$723,636

$657,600

$ 66,036

Total costs to be accounted for ……………….

Cost per equivalent unit

Costs accounted for:

Costs assigned to units transferred out:

Costs from beginning WIP inventory ………..

$723,636

$657,600

$ 66,036

WIP inventory …………………………..…………………

168,420

Mixing ………………………………………………

Current costs of units started and completed:

Mixing ($17.60 x 252,000) …………………..

4,435,200

Cost of ending WIP inventory ………………………..

Prior department ($17.60 x 42,000) ……..

Department B ($8.02 x 25,200) …………..

Total costs accounted for ……………………….

Current costs added to complete beginning

8-42. (continued)

8-43. (10 min.) Cost Per Equivalent Unit: Weighted-Average Method.

The correct answer is (b). The difference between the weighted-average and FIFO

methods of process costing is how they handle beginning WIP. When there is no

beginning WIP there is no difference between the two costing methods.

Answer (a) is incorrect because both methods assume units are homogeneous. Answer

8-44. (50 min.) Operations Costing―Ethical Issues: Brokia Electronics.

a.

Total

Basic

(40,000

units)

Photo

(30,000

units)

UrLife

(10,000

units)

Materials ………………….

$2,240,000

$480,000

$1,200,000

$560,000

Conversion

Assemblya …………..

$ 2,100,000

1,050,000

787,500

262,500

600,000

–0–

Total conversion ..

Total Product Cost

Number of Units

10,000

Cost per unit

$142.25

(1)

Total

Basic

(40,000

units)

Photo

(30,000

units)

UrLife

(10,000

units)

Materials

$2,240,000

$480,000

$1,200,000

$560,000

Conversion

Assemblya

$ 2,100,000

450,000

1,125,000

525,000

–0–

Total Product Cost

Number of Units

40,000

Cost per unit

$23.25

$168.50

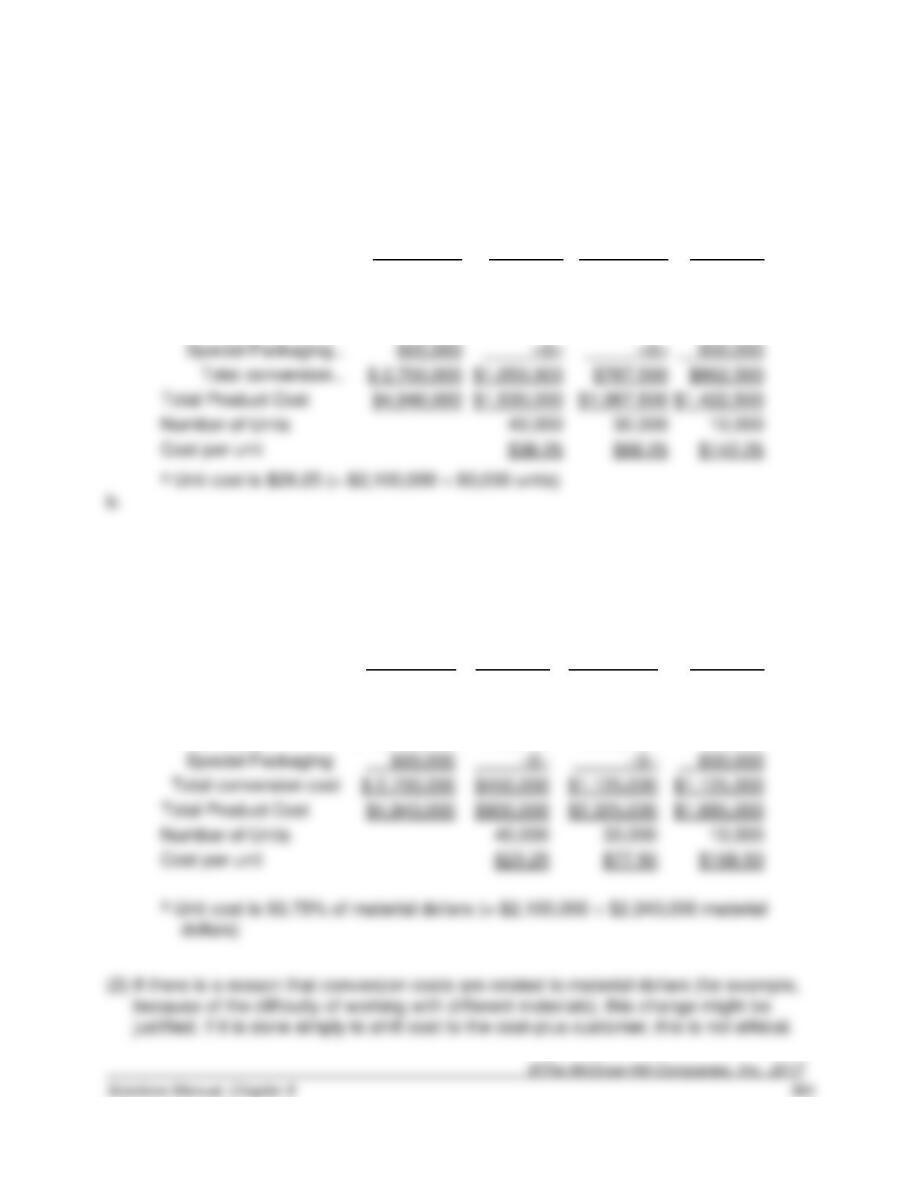

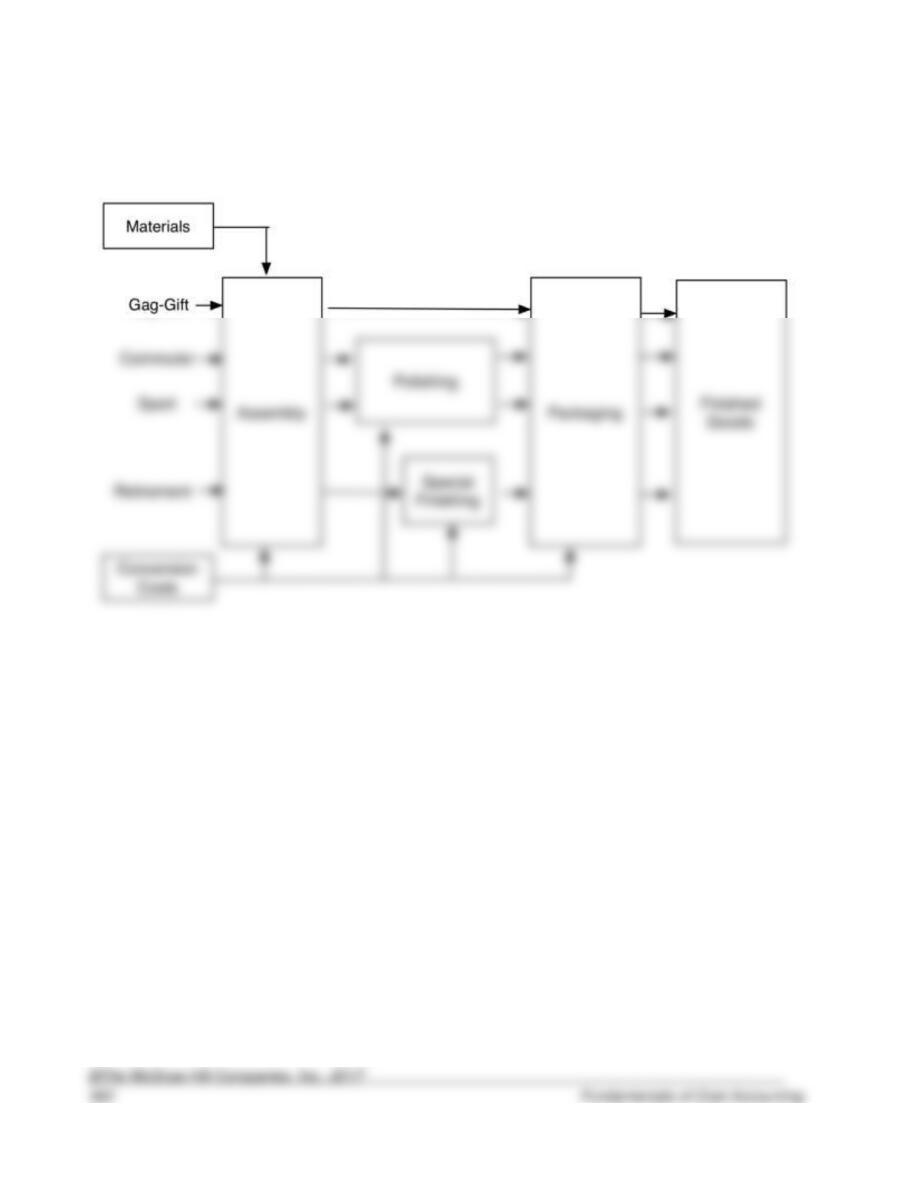

8-45. (50 min.) Operation Costing: Ferdon Watches.

a.

8-45. (continued)

b.

Total

Gag-Gift

(5,000

units)

Commuter

(10,000

units)

Sport

(13,000

units)

Retirement

(2,000

units)

Materials …………………

Conversion

Assemblya …………..

$120,000

$20,000

$40,000

$52,000

$ 8,000

Polishingb ……………

69,000

–0–

30,000

39,000

–0–

Special Finishingc ….

20,000

–0–

20,000

$299,000

$35,000

Total Product Cost ……

$620,000

Number of Units ………

10,000

13,000

Cost per unit ……………

Solutions to Problems

8-46. (45 min.) Compute Equivalent Units: Multiple Choice.

a. The answer is (4).

Materials

Conversion

Costs

Units transferred out …………………………..……….

790,000

a

790,000

a

EU in ending inventory:

Conversion costs 30% x 80,000

units ………………………………………………………….

EU

EU produced this period ………………………………

870,000

814,000

=

units started + beg. inventory – ending inventory

=

b. The answer is (3).

Prior

Department

Costs

Materials

Conversion

Costs

Units transferred out …………………………..……….

330,000

a

330,000

a

330,000

a

Prior department costs ……………………………..

Conversion costs 65% x 40,000

units ………………………………………………………….

EU

c. The answer is (4).

units …………………………………………………………..

EU done this period ……………………………………..

EU to complete beginning inventory 70%a x 20,000

14,000

EU

8-46. (continued)

d. The answer is (1).

Materials

Conversion

Costs

To complete beginning inventory:

Materials: 0%a x 40,000 units ……………………

0

Conversion costs: 30%b x 40,000 units ……….

12,000

EU

Started and completed during the period ………..

EU

EU

Materials: 100% x 32,000 units ………………….

EU

Conversion costs: 50% x 32,000 units ………..

16,000

EU

8-47. (30 min) FIFO Method: Glasgow Corporation.

a.

Physical

Units

Equivalent Units

Conversion

Costs

Flow of units

Units to be accounted for:

Beginning WIP inventory …………………………..

20,000

Conversion Costs

Flow of costs:

Costs to be accounted for:

Costs in beginning WIP inventory ……………………….

$ 232,200

Current period costs ………………………………………….

Total costs to be accounted for ………………………..

Cost per equivalent unit ($1,306,800 ÷ 88,000) ……….

$ 14.85

Costs accounted for:

Costs assigned to units transferred out:

Costs from beginning WIP inventory ………………..

beginning WIP inventory:

Conversion costs ($14.85 x 4,000) ………………

Current costs of units started and completed:

Conversion costs ($14.85 x 60,000) ………………..

Total costs transferred out………………………………….

Cost of ending WIP inventory:

Conversion costs ($14.85 x 24,000) …………….

(Answer)

8-47. (continued)

b.

8-48.

(50 min.) Prepare a Production Cost Report—Weighted Average Method: Kansas Supplies.

a.

Kansas Supplies

Assembling Department

Production Cost Report—Weighted-Average

Flow of Production Units

(Section 1)

units

Beginning WIP inventory …………………………..

Units started this period …………………………….

Total units to be accounted for ………………………

COMPUTE EQUIVALENT UNITS

department

costs

Materials

Labor

overhead

Units accounted for:

Total units accounted for ………………………………

Physical

8-48. (continued)

Total costs

Prior

department

costs

Materials

Labor

Manufacturing

overhead

Costs to be accounted for: (Section 3)

Costs in beginning WIP inventory ……………….

$ 382,800

$192,000

$120,000

$ 43,200

$27,600

Current period costs …………………………………

960,000

Prior department costs ($1,152,000 450,000)

Materials ($696,000 435,000) ………………….

$1.60

Labor ($259,200 405,000) ………………………

$0.64

Manufacturing overhead ($141,000 352,500)

Costs accounted for: (Section 5)

Costs assigned to units transferred out:

480,000

120,000

Total costs of units transferred out ………………

384,000

216,000

Total ending WIP inventory ………………………..

8-48. (continued)

b. The report to management should include the following items:

8-49.

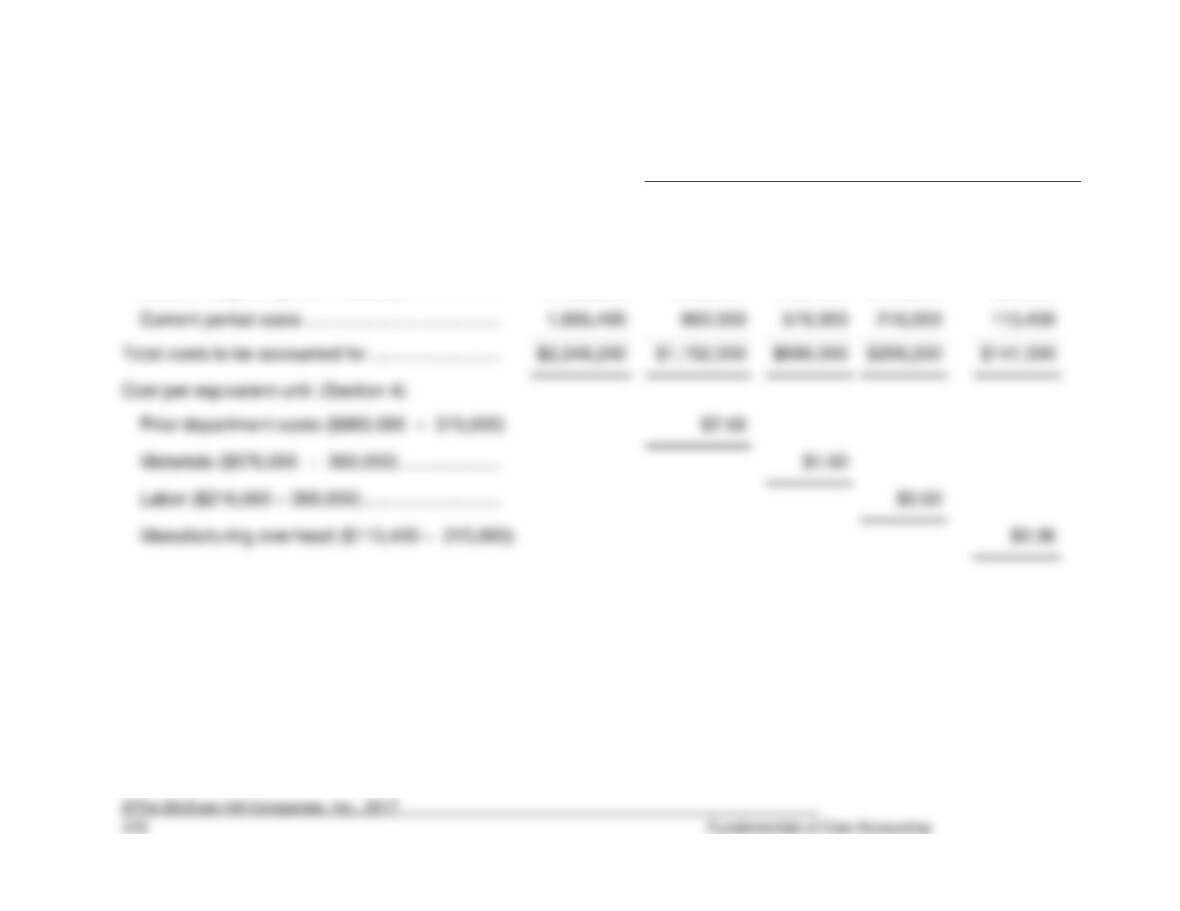

(50 min.) Prepare a Production Cost Report—FIFO Method: Kansas Supplies.

a.

Kansas Supplies

Assembling Department

Production Cost Report—FIFO

Flow of Production Units

(Section 1)

(Section 2)

COMPUTE EQUIVALENT UNITS

Physical

units

Prior

department

costs

Materials

Labor

Manufacturing

overhead

Units to be accounted for:

Beginning WIP inventory …………………………..

75,000

Total units to be accounted for ………………………

Units accounted for:

225,000

(90%)

Total units accounted for ………………………………

8-49. (continued)

Costs

DETAILS

Total Costs

Prior

department

costs

Materials

Labor

Manufacturing

overhead

Costs to be accounted for: (Section 3)

Costs in beginning WIP inventory ……………….

$ 382,800

$192,000

$120,000

$ 43,200

$27,600

Current period costs …………………………………

Total costs to be accounted for ……………………..

Cost per equivalent unit: (Section 4)

Prior department costs ($960,000 375,000)

Materials ($576,000 360,000) ………………..

Labor ($216,000 360,000) ………………………

Manufacturing overhead ($113,400 315,000)

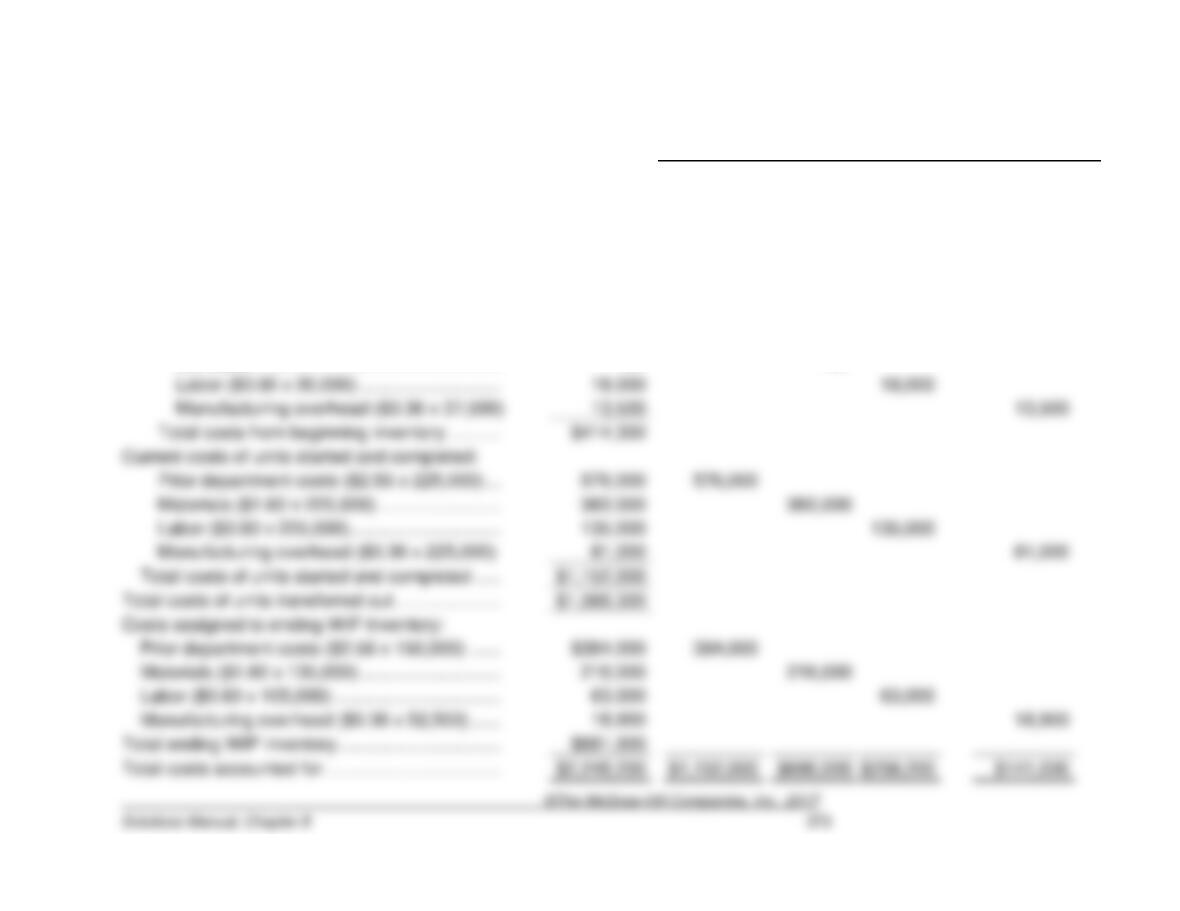

8-49. (continued)

Details

Total Costs

Prior

department

costs

Materials

Labor

Manufacturing

overhead

Costs accounted for: (Section 5)

Costs assigned to units transferred out:

Costs from beginning WIP inventory ………..

$ 382,800

$192,000

$120,000

$ 43,200

$27,600

Current costs added to complete beginning WIP inventory:

Prior department costs ……………………….

–0–

–0–

Materials …………………………………………..

–0–

–0–

Labor ($0.60 x 30,000) ……………………….

Manufacturing overhead ($0.36 x 37,500)

Total costs from beginning inventory ……….

Current costs of units started and completed:

Prior department costs ($2.56 x 225,000) …

Materials ($1.60 x 225,000) ……………………

Labor ($0.60 x 225,000) …………………………

Manufacturing overhead ($0.36 x 225,000)

Total costs of units started and completed …..

Total costs of units transferred out …………………

Costs assigned to ending WIP inventory:

Prior department costs ($2.56 x 150,000) ……

Materials ($1.60 x 135,000) ……………………….

Manufacturing overhead ($0.36 x 52,500) ……

Total ending WIP inventory …………………………..

Total costs accounted for ……………………………..

8-49. (continued)

b. The report to management should include the following items:

8-50. (60 min.) Prepare a Production Cost Report and Adjust Inventory Balances—Weighted-Average Method:

Fremont Corporation.

a.

Fremont Corporation

Production Cost Report—Weighted-Average

Flow of Production Units

(Section 1)

Physical units

Units to be accounted for:

Beginning WIP inventory …………………………..

Total units to be accounted for ………………………

(Section 2)

COMPUTE EQUIVALENT UNITS

Materials

Labor

Overhead

Units accounted for:

Units completed and transferred out:

From beginning inventory……………………….

80,000

Started and completed currently ……………..

Total units accounted for ………………………………

8-50. (continued)

Costs

Details

Total costs

Materials

Labor

Overhead

Costs to be accounted for: (Section 3)

Costs in beginning WIP inventory ……………….

$ 1,222,800

$ 240,000

$ 546,000

$ 436,800

Current period costs …………………………………

5,534,400

1,560,000

2,208,000

1,766,400

Total costs to be accounted for ……………………..

Cost per equivalent unit: (Section 4)

Materials ($1,800,000 480,000) ……………..

Labor ($2,754,000 408,000) ………………….

Overhead ($2,203,200 408,000) …………….

Costs accounted for: (Section 5)

Costs assigned to units transferred out:

Total costs of units transferred out ……………..

Costs assigned to ending WIP inventory:

Total ending WIP inventory………………………..

Total costs accounted for ……………………………..

8-50. (continued)

b. Adjustment required:

Work in

Process

Finished

Goods

c. Income would have been understated.

8-51. (40 min.) Prepare a Production Cost Report and Show Cost Flows Through

Accounts—FIFO Method: Recyclers, Inc.

Recyclers, Inc.

Production Cost Report—FIFO

a.

Flow of Production Units

(Section 2)

Compute Equivalent

Units

(Section 1)

Physical units

Conversion

costs

Units to be accounted for:

Beginning WIP inventory …………………………..

300

Total units to be accounted for ……………………..

Units accounted for:

Units completed and transferred out:

Units in ending WIP inventory ……………………

150

Total units accounted for ……………………………..

8-51. (continued)

Costs

Total costs

Conversion

costs

Costs to be accounted for: (Section 3)

Costs in beginning WIP inventory ………………….

$ 576

$ 576

Current period costs ……………………………………

10,800

10,800

Total costs to be accounted for ………………………..

Cost per equivalent unit: (Section 4)

Conversion costs ($10,800 2,700) ………………

Costs accounted for: (Section 5)

Costs assigned to units transferred out:

Costs from beginning inventory ………………….

$ 576

$ 576

WIP inventory:

Conversion costs ($4.00 x 120) ………………

Total costs from beginning inventory ……………..

$1,056

Current costs of units started and completed:

Conversion costs ($4.00 x 2,550) ………………

Total costs of units started and completed ……..

Total costs of units transferred out ………………..

Costs assigned to ending WIP inventory:

Conversion costs ($4.00 x 30) …………………..

Total ending WIP inventory ………………………….

$ 120

Total costs accounted for ………………………………..

b.

Work in Process

Beginning inventory:

Conversion costs

576

This period’s costs:

Conversion costs

To Finished Goods Inventory

Ending inventory

10,800

8-52. (40 min.) Prepare a Production Cost Report and Show Cost Flows Through

Accounts—Weighted-Average Method: Recyclers, Inc.

Recyclers, Inc.

Production Cost Report—Weighted Average

a.

Flow of Production Units

(Section 2)

Compute Equivalent

Units

(Section 1)

Physical units

Conversion

costs

Units to be accounted for:

Total units to be accounted for ……………………..

Units accounted for:

8-52. (continued)

Costs

Total costs

Conversion

costs

Costs to be accounted for: (Section 3)

Costs in beginning WIP inventory ………………….

$ 576

$ 576

Current period costs ……………………………………

10,800

10,800

Total costs to be accounted for ………………………..

$11,376

Cost per equivalent unit: (Section 4)

Conversion costs ($11,376 2,880) ………………

Costs accounted for: (Section 5)

Costs assigned to units transferred out:

Conversion costs ($3.95 x 2,850) ………………

Costs assigned to ending WIP inventory:

Conversion costs ($3.95 x 30) …………………..

Total costs accounted for ………………………………..

b.

Work in Process

Beginning inventory:

Conversion costs

576.00

Conversion costs

11,257.50

To Finished Goods Inventory

Ending inventory

10,800

11,257.50

8-53. (60 min.) FIFO Process Costing: Pantanal, Inc.

Pantanal, Inc.

Assembling Department

Production Cost Report—FIFO

Flow of Production Units

(Section 1)

(Section 2)

COMPUTE EQUIVALENT UNITS

Physical units

Prior

department

costs

Materials

Conversion

Units to be accounted for:

Beginning WIP inventory …………………………..

12,500

Units started this period …………………………….

Units completed and transferred out:

Started and completed currently ……………..

Units in ending WIP inventory …………………….

20,000

Total units accounted for ………………………………

130,500

8-53. (continued)

Costs

DETAILS

Total Costs

Prior

department

costs

Materials

Conversion

Costs to be accounted for: (Section 3)

Costs in beginning WIP inventory ……………….

$323,400

$ 98,000

$ 164,400

$ 61,000

Total costs to be accounted for ……………………..

Cost per equivalent unit: (Section 4)

Prior department costs ($2,142,000 127,500)

Materials ($939,600 130,500) ………………….

8-53. (continued)

Details

Total Costs

Prior

department

costs

Materials

Conversion

Costs accounted for: (Section 5)

Costs assigned to units transferred out:

Costs from beginning WIP inventory …………………………….

$ 323,400

$ 98,000

$ 164,400

$ 61,000

Current costs added to complete beginning WIP inventory:

Prior department costs ……………………………………………

Materials ($7.20 x 5,000) ………………………………………..

Conversion ($1.80 x 7,500) …………………………………….

Total costs from beginning inventory …………………………….

$ 372,900

Current costs of units started and completed:

Prior department costs ($16.80 x 107,500) ……………………

1,806,000

Materials ($7.20 x 107,500) ………………………………………..

Conversion ($1.80 x 107,500) ……………………………………..

Total costs of units started and completed ……………………….

Costs assigned to ending WIP inventory:

Prior department costs ($16.80 x 20,000) …………………………

$ 336,000

Materials ($7.20 x 18,000) ……………………………………………..

Conversion ($1.80 x 10,000) ………………………………………….

$ 483,600

Total costs accounted for ………………………………………………….

$286,000

8-54. (50 min.) Prepare a Production Cost Report—Weighted-Average Method:

Saline Solutions.

a. 60 percent complete. The key to this problem is to set up the production cost report to

the extent you can and then fill in the missing information.

Physical

Units

Equivalent Units

Materials

Conversion

Flow of units:

Units to be accounted for:

Beginning WIP inventory …………………………..

50,000

Total units to account for ………………………..

Units accounted for:

Completed and transferred out …………………..

Units in ending inventory …………………………..

70,000

Mixing (70,000 units x 100%) ………………….

Finishing (70,000 units x ??% [i]) …………….

h

Total units accounted for …………………….

b

Flow of costs:

Costs to be accounted for:

Costs in beginning WIP inventory ……………….

$482,424

$438,400

d

$ 44,024

e

Current period costs …………………………………

5,043,976

3,449,600

1,594,376

Total costs to be accounted for ……………….

c

$1,638,400

f

Cost per equivalent unit

Materials ($3,888,000 ÷ 540,000 units) ……….

a

Conversion ($1,638,400 ÷ 512,000 [g]) ……….

a

Costs accounted for:

Costs assigned to units transferred out ……….

$1,504,000

Costs of ending WIP inventory …………………..

Total costs accounted for ……………………….

$3,888,000

8-54. (continued)

Notes:

a. Given.

b. Because the units are fully complete with respect to materials, the equivalent

units are equal to the physical units.

8-55. (30 min.) Determine Degree of Completion—FIFO method: Saline Solutions.

a. The ending work in process is at least 60% complete with respect to conversion costs.

This is a problem that requires relatively few computations, but a thorough understanding

of process costing. There are various ways to work through to an answer; the following is

one.

8-56. (40 min.) Solving For Unknowns—FIFO Method.

a.

Units started and completed equals the units transferred out (units completed this

period) less the units started in a previous period (beginning inventory):

8-56. (continued)

c.

Equivalent units

=

Beginning inventory

x (1 – percentage of completion of beginning inventory)

+ 100% of units started and completed

+ ending inventory times its percentage of completion

=

5,600

equivalent units

5,600

=

1,000 (1 – X) + 4,500 + (3,000 x 30%)

5,600

=

1,000 – 1,000X + 5,400

=

=

1,000X

=

TO + EB – TI

=

(4,500 + 1,000) + 900 – 5,600

=

800 units

1,000X

=

$87,000 ÷ 10,000

d. The cost per equivalent unit is obtained by dividing the ending inventory costs by the

equivalent units in ending inventory:

which, for the problem are:

42,000 + 60,000 + 10,000

=

Equivalent units worked this period are the sum of the equivalent units to:

8-57. (50 min.) Solving For Unknowns—Weighted-Average Method.

a. Units transferred out equals beginning inventory plus current work minus ending

inventory. In equation form:

b. The inventory equation yields:

8-57. (continued)

c. First, we compute the cost of ending inventory:

BB + TI (current work)

=

TO + EB

=

$115,200 + EB

=

$120,000 – $115,200

=

$4,800

d. The materials cost per equivalent unit is:

$26,880 ÷ 12,800 units transferred out

=

$2.10 per EU

units in EB

2,400 ÷ .25

9,600

÷

÷

÷

8-58. (50 min.) Operation Costing—Work-in-Process Inventory: Washington, Inc.

a.

The material costs per unit are:

The conversion costs per equivalent unit are:

Department A:

Physical

Units

Conversion Costs

Equivalent Units

Flow of units:

Units to be accounted for:

Beginning WIP inventory …………………………..

1,000

Total units to account for ……………………….

1,000

Units accounted for:

Conversion costs (160 x 25%) ………………..

Total units accounted for ……………………….

1,000

8-58. (continued)

Total

Conversion

Costs

Flow of costs:

Costs to be accounted for:

Costs in beginning WIP inventory ……………….

$ –0–

Current period costs …………………………………

Total costs to be accounted for ……………….

$ 264,000

Cost per equivalent unit

Conversion costs ($264,000 ÷ 880) …………….

Department B:

Physical

Units

Conversion Costs

Equivalent Units

Flow of units:

Units to be accounted for:

Beginning WIP inventory …………………………..

–0–

Total units to account for ………………………..

Conversion costs (50 x 60%) ………………….

Total units accounted for ………………………..

Total

Conversion

Costs

Flow of costs:

Costs to be accounted for:

Costs in beginning WIP inventory ……………….

$ –0–

$ –0–

Current period costs …………………………………

42,000

42,000

Total costs to be accounted for ……………….

Cost per equivalent unit

Conversion costs ($42,000 ÷ 420) ………………

8-58. (continued)

Cost of units transferred to finished goods:

Product

Unit

Material

Cost

Unit

Department

A Cost

Unit

Department

B Cost

Unit Cost

b.

Work-in-Process Ending Inventory Balances are (note the number of units is equal to the

difference between the units started and units completed):

Department A:

Material cost

Number

of Units

Unit

Cost

Total Cost

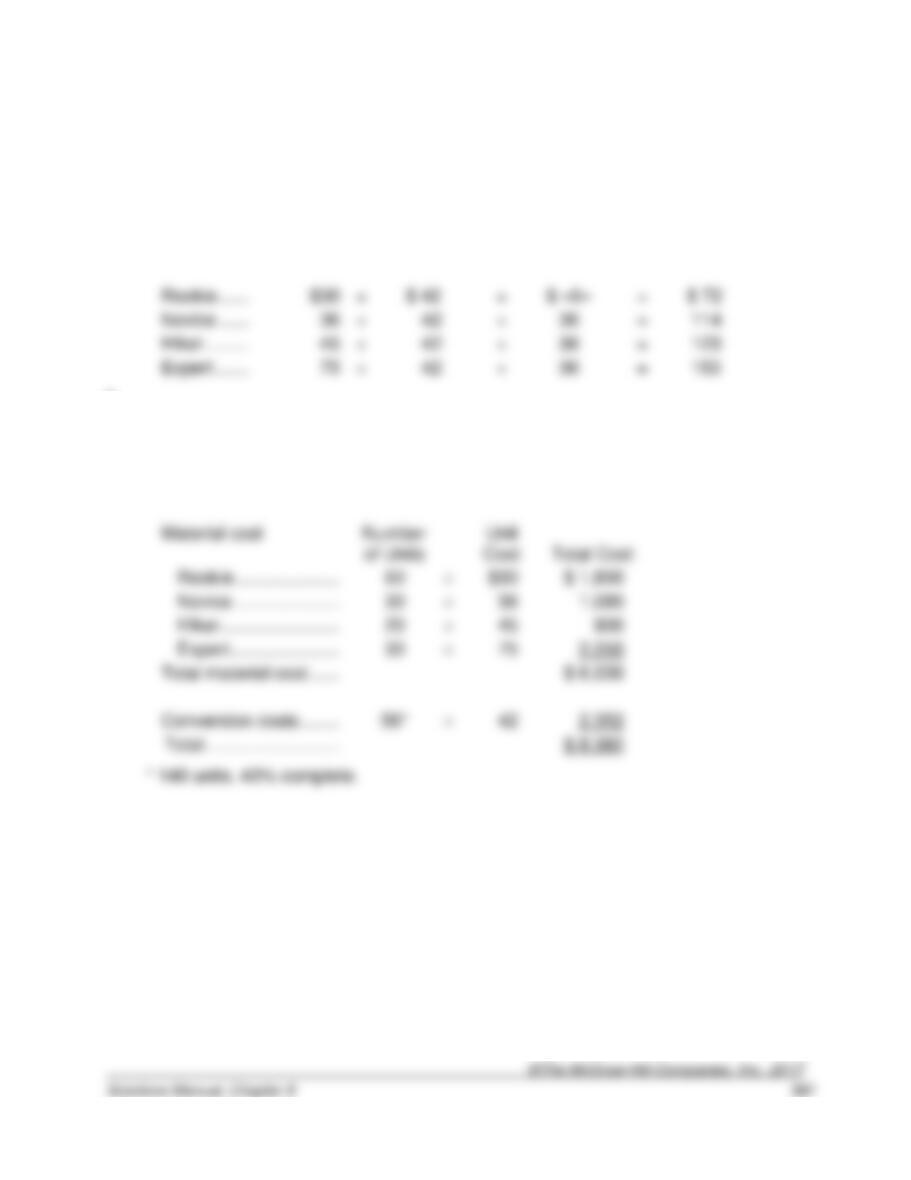

X-10 ……………………

100

$150

$ 15,000

Material cost

Number

of Units

Cost

Total Cost

300

Rookie ……

÷

17,280

÷

Hiker ………

13,050

÷

Expert …….

11,250

÷

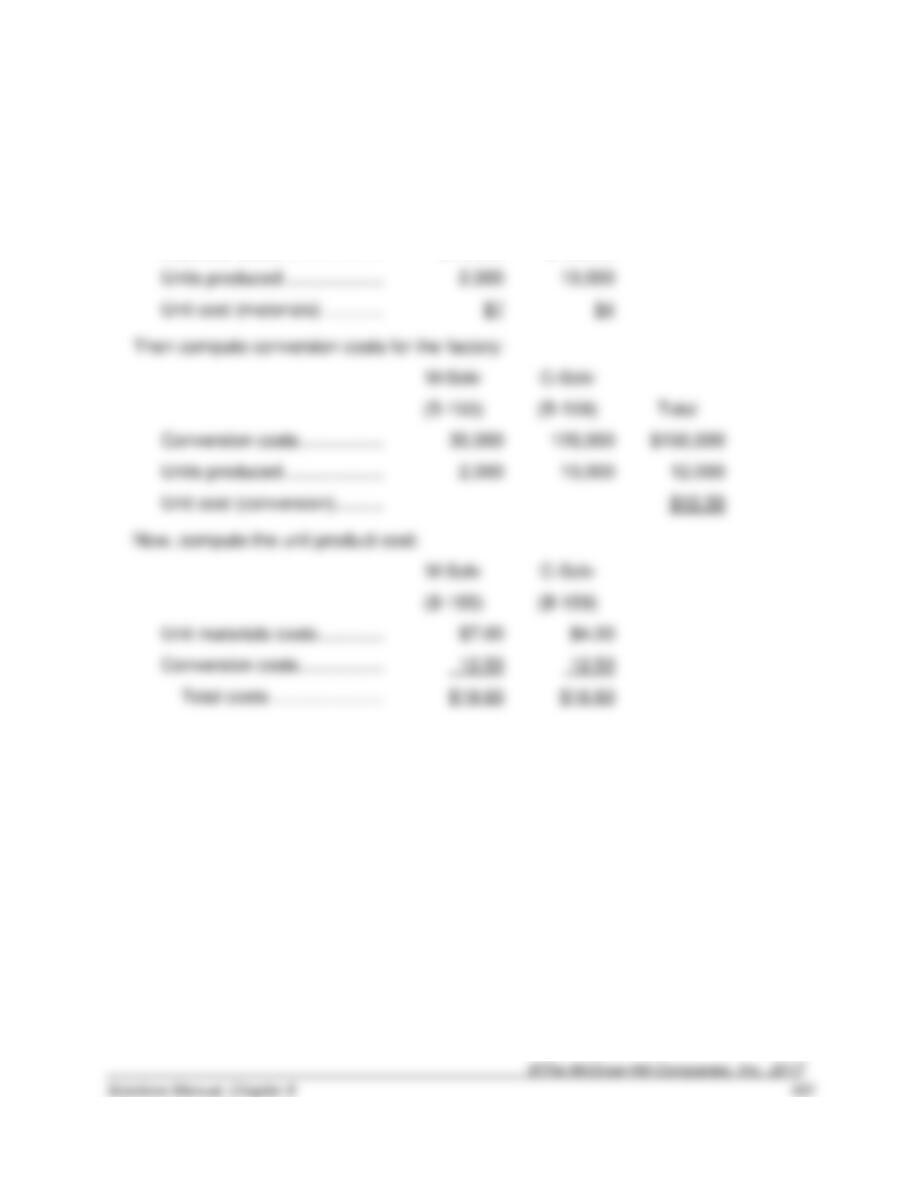

8-59. (50 min.) Operation Costing—Work-in-Process Inventory: Miller Outdoor

Equipment.

The solution to this problem is to apply process costing methods for the conversion

costs and then add the cost of materials for each product. Because there is no

beginning work-in-process inventory, FIFO and weighted-average process costing

gives the same results.

a.

The material costs per unit are:

Physical

Units

Conversion Costs

Equivalent Units

Flow of units:

Units to be accounted for:

Beginning WIP inventory …………………………..

–0–

Units started this perioda

1,520

Total units to account for ………………………..

Completed and transferred outb

1,380

Units in ending inventoryc

Conversion costs (140 x 40%) ………………..

Total units accounted for ………………………..

1,520

8-59. (continued)

Total

Conversion

Costs

Flow of costs:

Costs to be accounted for:

60,312

Cost per equivalent unit

Customizing Department:

Physical

Units

Conversion Costs

Equivalent Units

Flow of units:

Units to be accounted for:

Beginning WIP inventory …………………………..

–0–

Units started this perioda

840

Total units to account for ……………………….

840

Completed and transferred outb

790

Conversion costs (50 x 20%) ………………….

Total units accounted for ……………………….

Total

Conversion

Costs

Flow of costs:

Costs to be accounted for:

$ –0–

Cost per equivalent unit

8-59. (continued)

Cost of units transferred to finished goods:

Product

Unit

Material

Cost

Stitching

Department

Unit Cost

Customizing

Department

Unit Cost

Unit Cost

Material cost

Number

Cost

$ 1,800

b.

Work-in-Process Ending Inventory Balances are (note the number of units is equal to the

difference between the units started and units completed):

Stitching Department:

8-59. (continued)

Customizing Department:

Material cost

Number

of Units

Unit

Cost

Total Cost

Novice …………………………..

10

$36

360

Hiker …………………………….

20

45

900

Expert …………………………..

20

50

36

8-60. (50 min.) Process Costing and Ethics – Increasing Production to Boost

Profits: Pacific Siding, Inc.

8-60. (continued)

b. See the revised data entry section and production cost report below:

Data Entry Section

Unit Information

Percent Complete

Units

(board

Direct

Direct

feet)

materials

labor

Overhead

Units in beginning WIP inventory (all completed this period)

250,000

n/a

n/a

n/a

Units started and completed during the period

140,000

Units started and partially completed during the period

225,000

Direct

Direct

Cost Information

materials

labor

Overhead

Costs in beginning WIP inventory

Costs incurred during the period

$102,000

8-60. (continued)

Revised Production Cost Report

Month Ending March 31

Step 1: Summary of Physical Units and Equivalent Unit Calculations

Physical

Units to be accounted for

Units

Units in beginning WIP inventory

250,000

Units started during the period

365,000

Total units to be accounted for

615,000

Direct

Direct

Units accounted for

materials

labor

Overhead

Units completed and transferred out

390,000

Total units accounted for

615,000

Step 2: Summary of Costs to be Accounted for

Direct

Direct

Costs to be accounted for

materials

labor

Overhead

Total

Costs in beginning WIP inventory

$76,000

$90,000

$150,000

$316,000

Costs incurred during the period

102,000

150,000

347,000

Total costs to be accounted for

$192,000

$300,000

$663,000

Step 3: Calculation of Cost per Equivalent Unit

8-60. (continued)

Direct

Direct

materials

labor

Overhead

Total

$192,000

Cost per equivalent unit (a) / (b)

Step 4: Assign Costs to Units Transferred Out and Units in Ending WIP Inventory

Direct

Direct

materials

labor

Overhead

Total

$128,826

$443,294

Total costs accounted for

$192,000

$663,000

8-60. (continued)

Solutions to Integrative Cases

8-61. (70 min.) Show Cost Flows—FIFO Method: Vermont Co.

Work in Process

Beginning Balance

716,000

Transferred out:

materials (given)

300,400

From current work

conversion (given)

materials

conversion costs

Ending Balance

513,104

Additional computations:

a $240,320 = 40,000 EU transferred x ($300,400 ÷ 50,000 EU for materials)

Finished Goods

a

1,432,237

To Cost of Goods Sold

Cost of Goods Sold

(See explanation below)

$572,000

$715,000

8-61. (continued)

The journal entry to assign the overapplied overhead to cost of goods sold is:

8-62. (45 min.) Job Costing, Process Costing, Choosing a Costing Method:

Bouwens Corporation.

This problem is computationally straight-forward, but requires the student to think

about the use of the costs from the costing system and how to best reflect the

production costs for a single product for two customer types.

a. The “job” costs for each product are the unit costs in each building:

M-Solv

(B–155)

C-Solv

(B–159)

Materials costs ………………..

$14,000

$ 40,000

Conversion costs …………….

120,000

$44,000

Units produced ………………..

b. The “process” costs for each product are the unit costs for both buildings divided by

total production:

M-Solv

(B–155)

C-Solv

(B–159)

Total

Materials costs ………………..

$14,000

$ 40,000

$ 54,000

Conversion costs …………….

120,000

$44,000

Units produced ………………..

8-62. (continued)

d. Compute the unit costs for materials and conversion costs separately.

M-Solv

(B–155)

C-Solv

(B–159)

Materials costs ………………..

$14,000

$ 40,000

Units produced ………………..

M-Solv

(B–155)

C-Solv

(B–159)

Conversion costs ……………..

120,000

Units produced ………………..

M-Solv

(B–155)

C-Solv

(B–159)

Unit materials costs ………….

Conversion costs ……………..