8-41

8-42

8-43

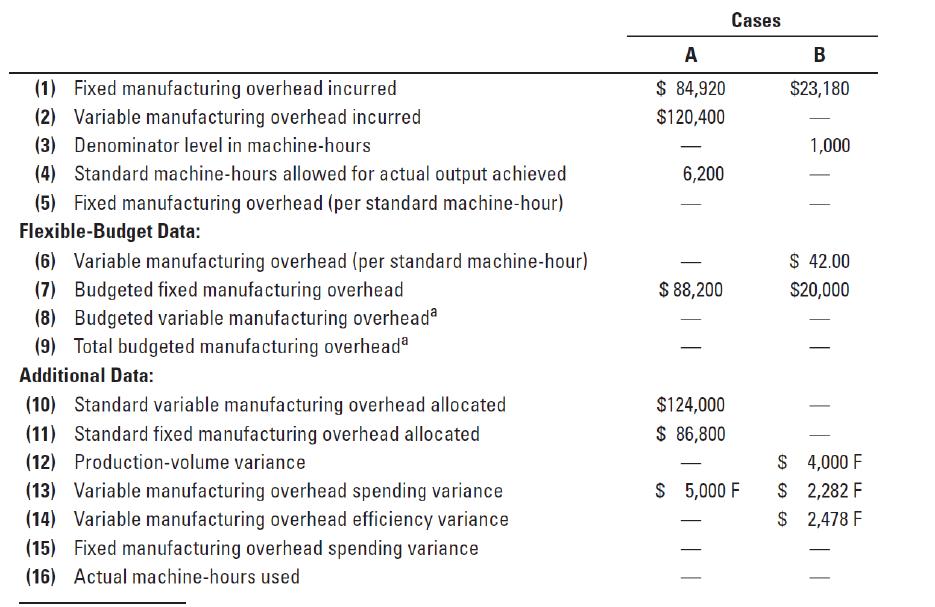

8-33 (30 min.) Overhead variance, missing information.

Consider the following two situations—cases A and B—independently. Data refer to operations

for April 2014. For each situation, assume standard costing. Also assume the use of a flexible

budget for control of variable and fixed manufacturing overhead based machine-hours.

aFor standard machine-hours allowed for actual output produced.

Required:

Fill in the blanks under each case. [Hint: Prepare a worksheet similar to that in Exhibit 8-4 (page

304). Fill in the knowns and then solve for the unknowns.]

8-44

SOLUTION

8-45

8-46

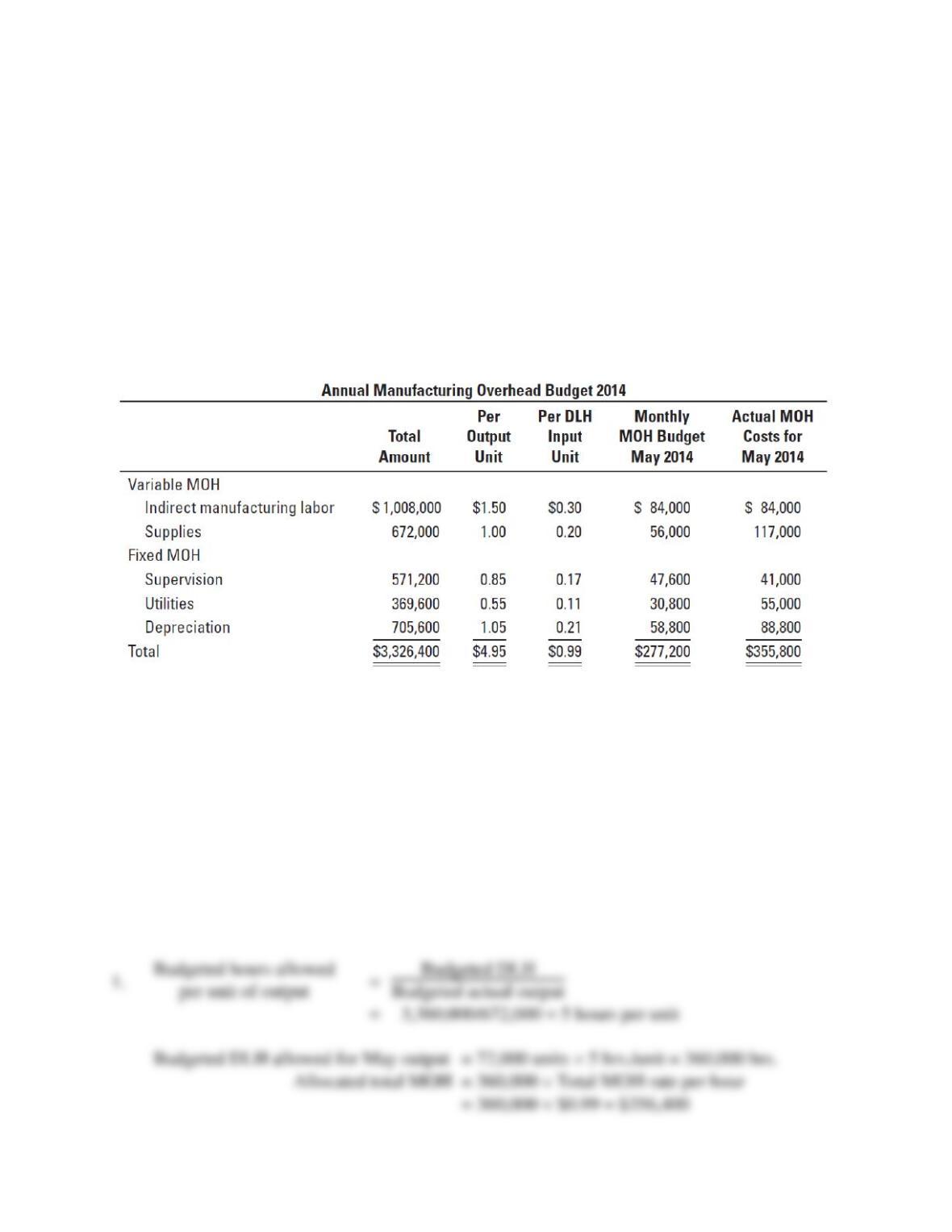

8-34 (15−25 min.) Flexible budgets, 4-variance analysis.

(CMA, adapted) Wilson Products uses standard costing. It allocates manufacturing overhead

(both variable and fixed) to products on the basis of standard direct manufacturing labor-hours

(DLH). Wilson Products develops its manufacturing overhead rate from the current annual

budget. The manufacturing overhead budget for 2014 is based on budgeted output of 672,000

units, requiring 3,360,000 DLH. The company is able to schedule production uniformly

throughout the year.

A total of 72,000 output units requiring 321,000 DLH was produced during May 2014.

Manufacturing overhead (MOH) costs incurred for May amounted to $355,800. The actual costs,

compared with the annual budget and 1/12 of the annual budget, are as follows:

Calculate the following amounts for Wilson Products for May 2014:

Required:

1. Total manufacturing overhead costs allocated

2. Variable manufacturing overhead spending variance

3. Fixed manufacturing overhead spending variance

4. Variable manufacturing overhead efficiency variance

5. Production-volume variance

Be sure to identify each variance as favorable (F) or unfavorable (U).

SOLUTION

8-47

8-48

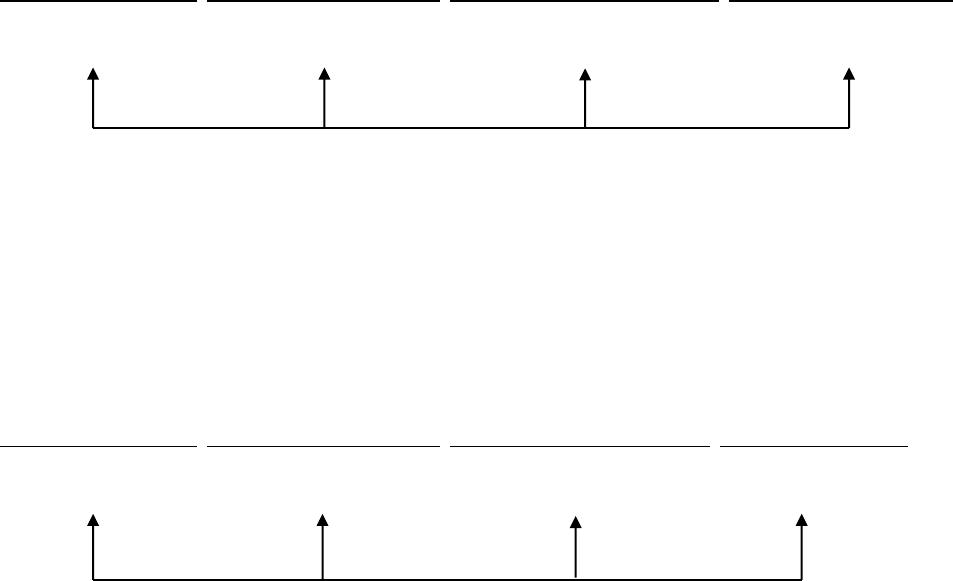

SOLUTION EXHIBIT 8-34

Variable Manufacturing Overhead

Actual Costs

Incurred

(1)

Actual Input Qty.

× Budgeted Rate

(2)

Flexible Budget:

Budgeted Input Qty.

Allowed for

Actual Output

× Budgeted Rate

(3)

Allocated:

Budgeted Input Qty.

Allowed for

Actual Output

× Budgeted Rate

(4)

$201,000

(321,000 $0.50)

$160,500

(360,000 $0.50)

$180,000

(360,000 $0.50)

$180,000

Fixed Manufacturing Overhead

Actual Costs

Incurred

(1)

Same Budgeted

Lump Sum

(as in Static Budget)

Regardless of

Output Level

(2)

Flexible Budget:

Same Budgeted

Lump Sum

(as in Static Budget)

Regardless of

Output Level

(3)

Allocated:

Budgeted Input

Allowed for

Actual Output

× Budgeted Rate

(4)

$154,800

$137,200

$137,200

(360,000 $0.49)

$176,400

$40,500 U

Spending variance

$19,500 F

Efficiency variance

Never a variance

$17,600 U

Spending variance

Never a variance

$39,200 F

Production-volume variance

8-49

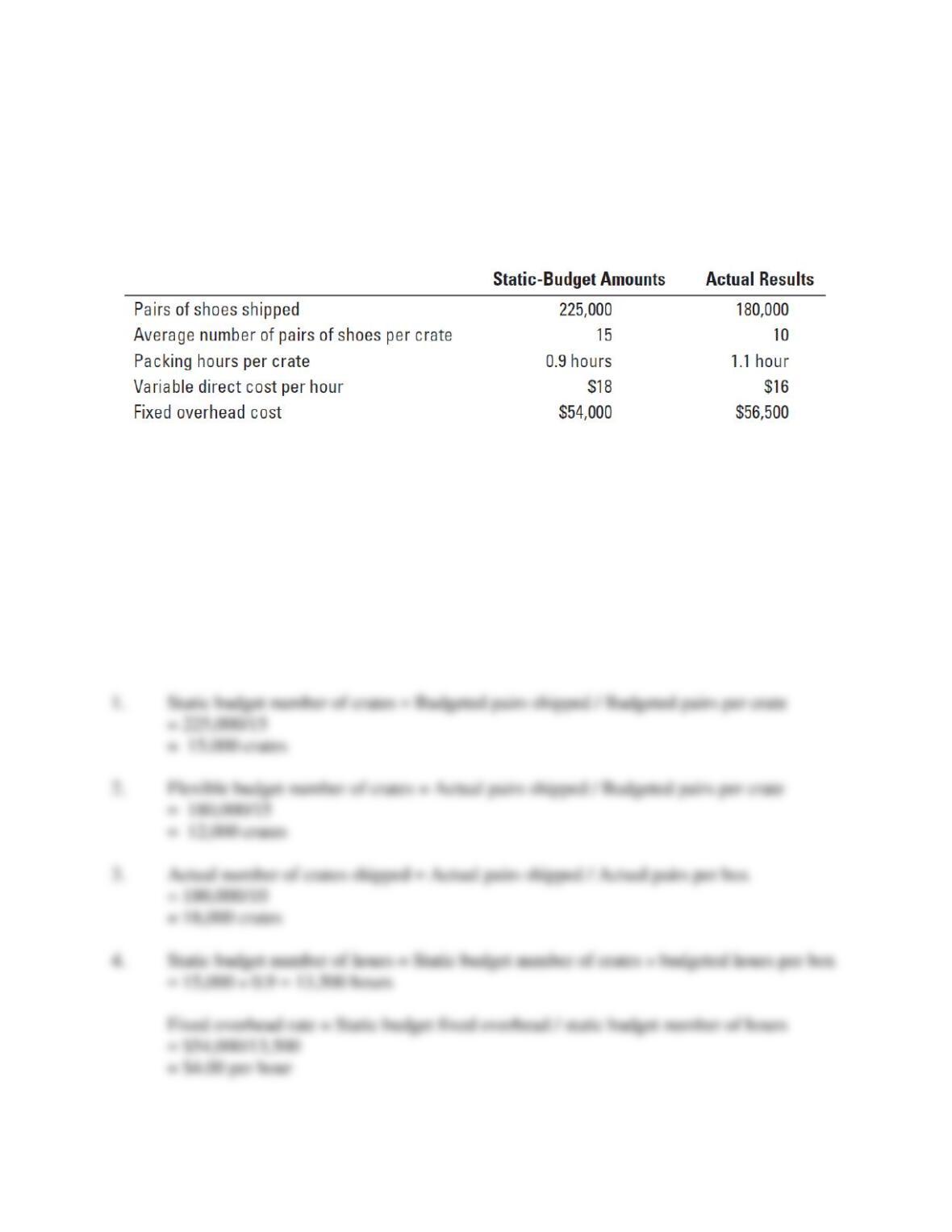

8-35 (20 min.) Activity-based costing, batch-level variance analysis

Audrina’s Fleet Feet, Inc., produces dance shoes for stores all over the world. While the pairs of

shoes are boxed individually, they are crated and shipped in batches. The shipping department

records both variable direct batch-level costs and fixed batch-level overhead costs. The following

information pertains to shipping department costs for 2014.

Required:

1. What is the static budget number of crates for 2014?

2. What is the flexible budget number of crates for 2014?

3. What is the actual number of crates shipped in 2014?

4. Assuming fixed overhead is allocated using crate-packing hours, what is the predetermined

fixed overhead allocation rate?

5. For variable direct batch-level costs, compute the price and efficiency variances.

6. For fixed overhead costs, compute the spending and the production-volume variances.

SOLUTION

8-50

8-51

8-36 (30 – 40 minutes) Overhead variances and sales volume variance

Birken Company manufactures shopping bags made of recycled plastic that it plans to sell for $5

each. Birken budgets production and sales of 800,000 bags for 2014, with a standard of 400,000

machine-hours for the whole year. Budgeted fixed overhead costs are $500,000, and variable

overhead cost is $1.60 per machine-hour.

Because of increased demand, Birken actually produced and sold 900,000 bags in 2014, using

a total of 440,000 machine-hours. Actual variable overhead costs are $699,600 and actual fixed

overhead is $501,900. Actual selling price is $6 per bag.

Direct materials and direct labor actual costs were the same as standard costs, which were

$1.20 per unit and $1.80 per unit, respectively.

Required:

1. Calculate the variable overhead and fixed overhead variances (spending, efficiency,

spending, and volume).

2. Create a chart like that in Exhibit 7-2 showing Flexible Budget Variances and Sales Volume

Variances for revenues, costs, contribution margin, and operating income.

3. Calculate the operating income based on budgeted profit per shopping bag.

4. Reconcile the budgeted operating income from requirement 3 to the actual operating income

from your chart in requirement 2.

5. Calculate the operating income volume variance and show how the sales volume variance is

composed of the production volume variance and the operating income volume variance.

SOLUTION

8-52

8-53

8-37 (30 min.) Activity-based costing, batch-level variance analysis

Rae Steven Publishing Company specializes in printing specialty textbooks for a small but

profitable college market. Due to the high setup costs for each batch printed, Rae Steven holds

the book requests until demand for a book is approximately 520. At that point Rae Steven will

schedule the setup and production of the book. For rush orders, Rae Steven will produce smaller

batches for an additional charge of $987 per setup.

Budgeted and actual costs for the printing process for 2014 were as follows:

Required:

1. What is the static budget number of setups for 2014?

2. What is the flexible budget number of setups for 2014?

3. What is the actual number of setups in 2014?

4. Assuming fixed setup overhead costs are allocated using setup-hours, what is the

predetermined fixed setup overhead allocation rate?

5. Does Rae Steven’s charge of $987 cover the budgeted direct variable cost of an order? The

budgeted total cost?

6. For direct variable setup costs, compute the price and efficiency variances.

7. For fixed setup overhead costs, compute the spending and the production-volume variances.

8. What qualitative factors should Rae Steven consider before accepting or rejecting a special

order?

8-54

SOLUTION

8-55

8-56

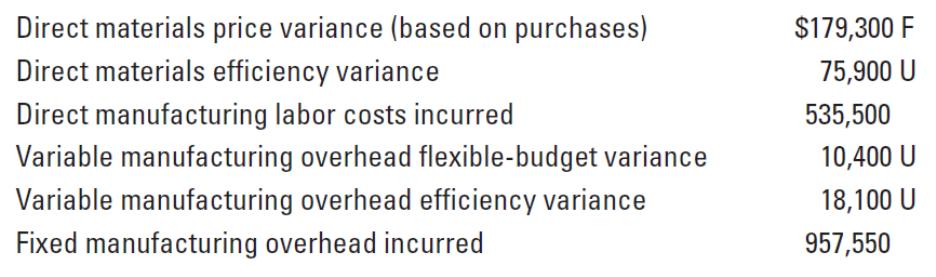

8-38 (30−40 min.) Comprehensive review of Chapters 7 and 8, working backward from

given variances.

The Gallo Company uses a flexible budget and standard costs to aid planning and control of its

machining manufacturing operations. Its costing system for manufacturing has two direct-cost

categories (direct materials and direct manufacturing labor—both variable) and two overhead–

cost categories (variable manufacturing overhead and fixed manufacturing overhead, both

allocated using direct manufacturing labor-hours).

At the 50,000 budgeted direct manufacturing labor-hour level for August, budgeted direct

manufacturing labor is $1,250,000, budgeted variable manufacturing overhead is $500,000, and

budgeted fixed manufacturing overhead is $1,000,000.

The following actual results are for August:

The standard cost per pound of direct materials is $11.50. The standard allowance is 6 pounds of

direct materials for each unit of product. During August, 20,000 units of product were produced.

There was no beginning inventory of direct materials. There was no beginning or ending work in

process. In August, the direct materials price variance was $1.10 per pound.

In July, labor unrest caused a major slowdown in the pace of production, resulting in an

unfavorable direct manufacturing labor efficiency variance of $40,000. There was no direct

manufacturing labor price variance. Labor unrest persisted into August. Some workers quit.

Their replacements had to be hired at higher wage rates, which had to be extended to all workers.

The actual average wage rate in August exceeded the standard average wage rate by $0.50 per

hour.

Required:

1. Compute the following for August:

a. Total pounds of direct materials purchased

b. Total number of pounds of excess direct materials used

c. Variable manufacturing overhead spending variance

d. Total number of actual direct manufacturing labor-hours used

e. Total number of standard direct manufacturing labor-hours allowed for the units

produced

f. Production-volume variance