CHAPTER 22 (FIN MAN); CHAPTER 8 (MAN) Budgeting

Prob. 22–3B (FIN MAN); Prob. 8–3B (MAN) (Continued)

4.

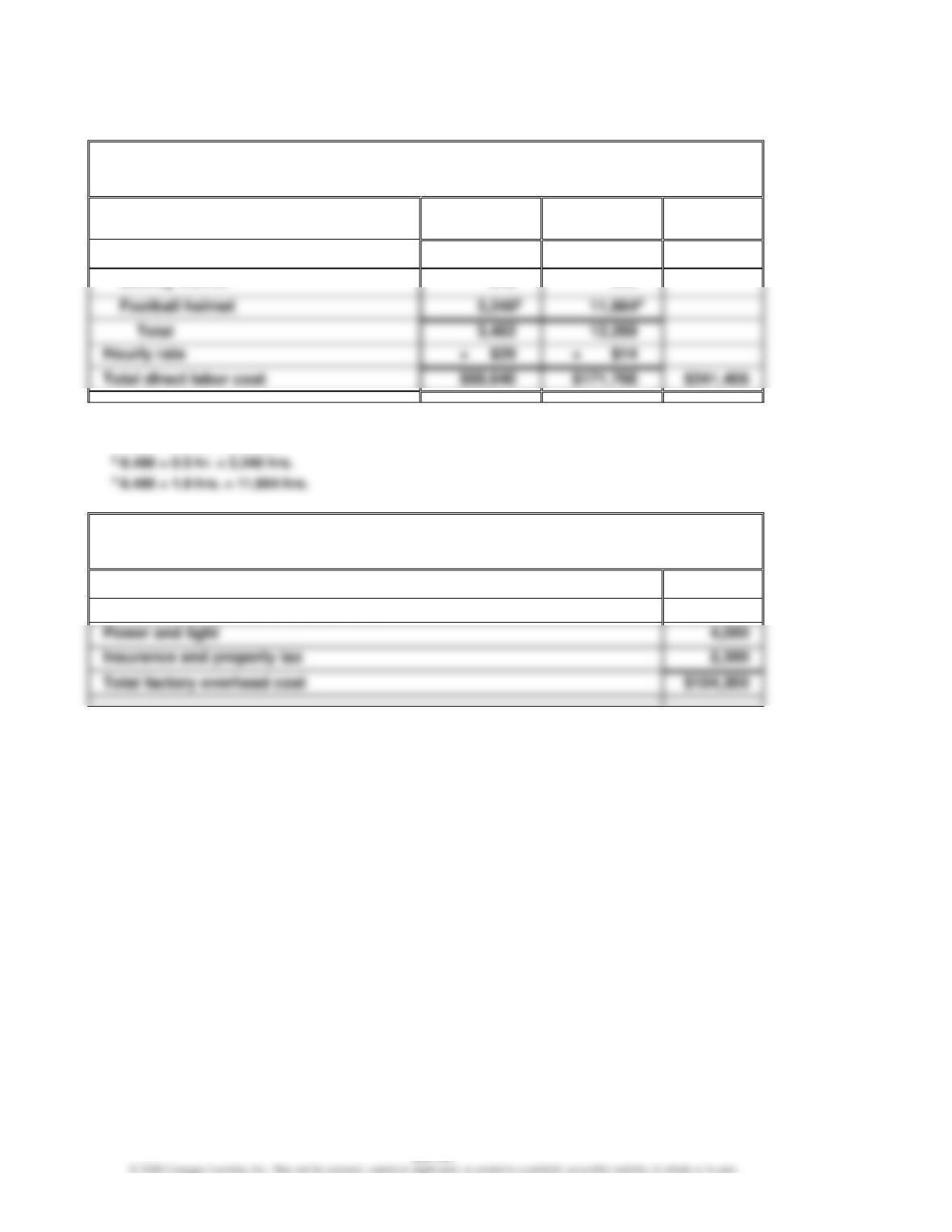

Gold Medal Athletic Co.

Direct Labor Cost Budget

For the Month Ending March 31

Molding

Department

Assembly

Department

Total

Hours required for production:

1 1,210 × 0.2 hr. = 242 hrs.

2 1,210 × 0.5 hr. = 605 hrs.

5.

Gold Medal Athletic Co.

Factory Overhead Cost Budget

For the Month Ending March 31

Indirect factory wages

$ 86,000

Depreciation of plant and equipment

12,000

Insurance and property tax

CHAPTER 22 (FIN MAN); CHAPTER 8 (MAN) Budgeting

Prob. 22–3B (FIN MAN); Prob. 8–3B (MAN) (Continued)

6.

Gold Medal Athletic Company

Cost of Goods Sold Budget

For the Month Ending March 31

Finished goods inventory, March 11

$ 19,480

Work in process inventory, March 1

$ 15,300

Direct materials:

Cost of direct materials placed in

production

$186,092

Direct labor (from part 4)

241,406

Factory overhead (from part 5)

104,300

Total manufacturing costs

531,798

Work in process, March 31

Cost of goods manufactured

Cost of finished goods available for sale

Cost of goods sold

1 Batting helmet (40 × $25.00) …………………………………………………

$ 1,000

Football helmet (240 × $77.00) …………………………..…………………

18,480

Finished goods inventory, March 1 ………………………………………

$19,480

2 Plastic (90 × $6.00) ……………………………………………………………….

$ 540

Foam lining (80 × $4.00) ……………………………………………………….

320

Direct materials inventory, March 1 ………………………………………

$ 860

CHAPTER 22 (FIN MAN); CHAPTER 8 (MAN) Budgeting

Prob. 22–3B (FIN MAN); Prob. 8–3B (MAN) (Concluded)

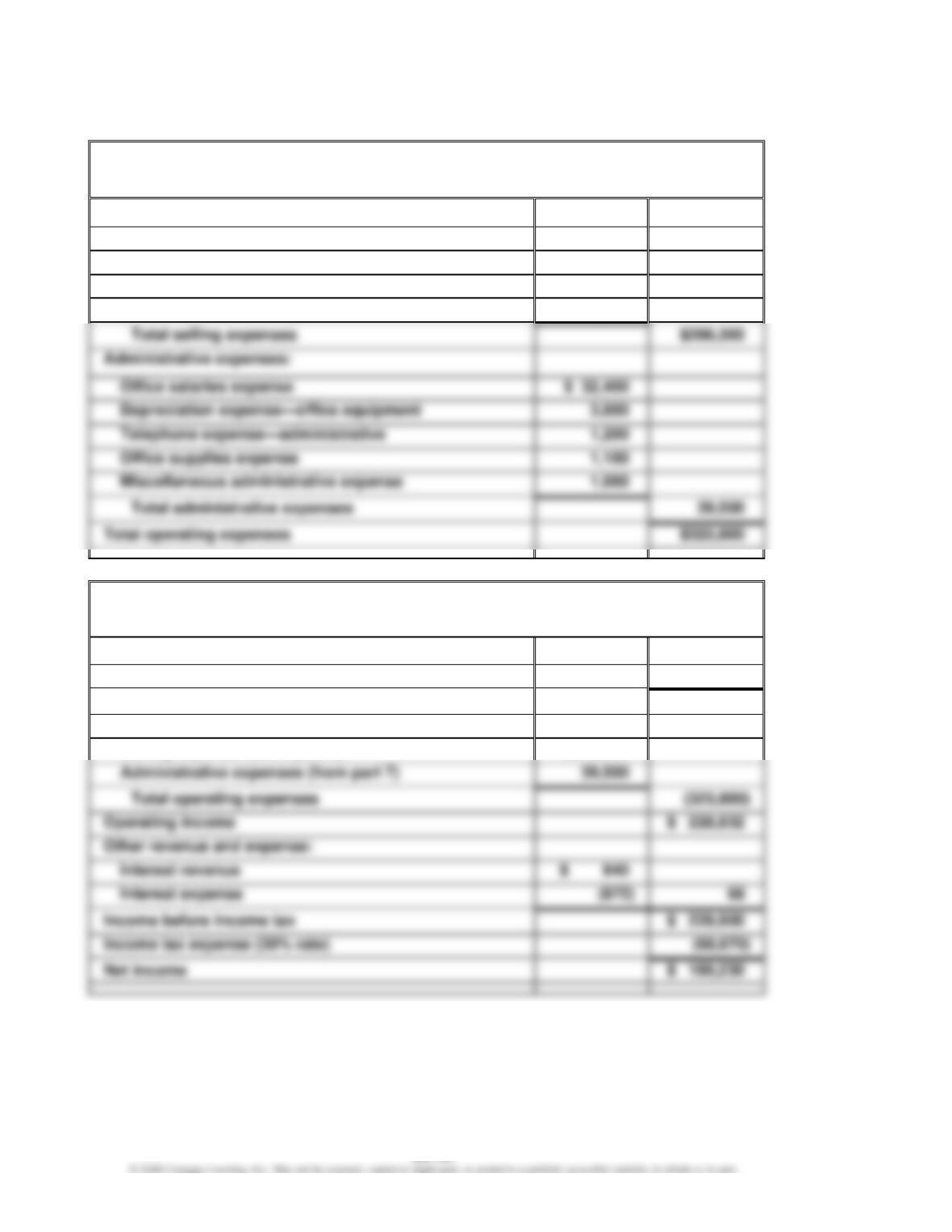

7.

Gold Medal Athletic Co.

Selling and Administrative Expenses Budget

For the Month Ending March 31

Selling expenses:

Sales salaries expense

$184,300

Advertising expense

87,200

Telephone expense—selling

5,800

Travel expense—selling

9,000

Office salaries expense

Depreciation expense—office equipment

Telephone expense—administrative

1,200

Office supplies expense

1,100

Miscellaneous administrative expense

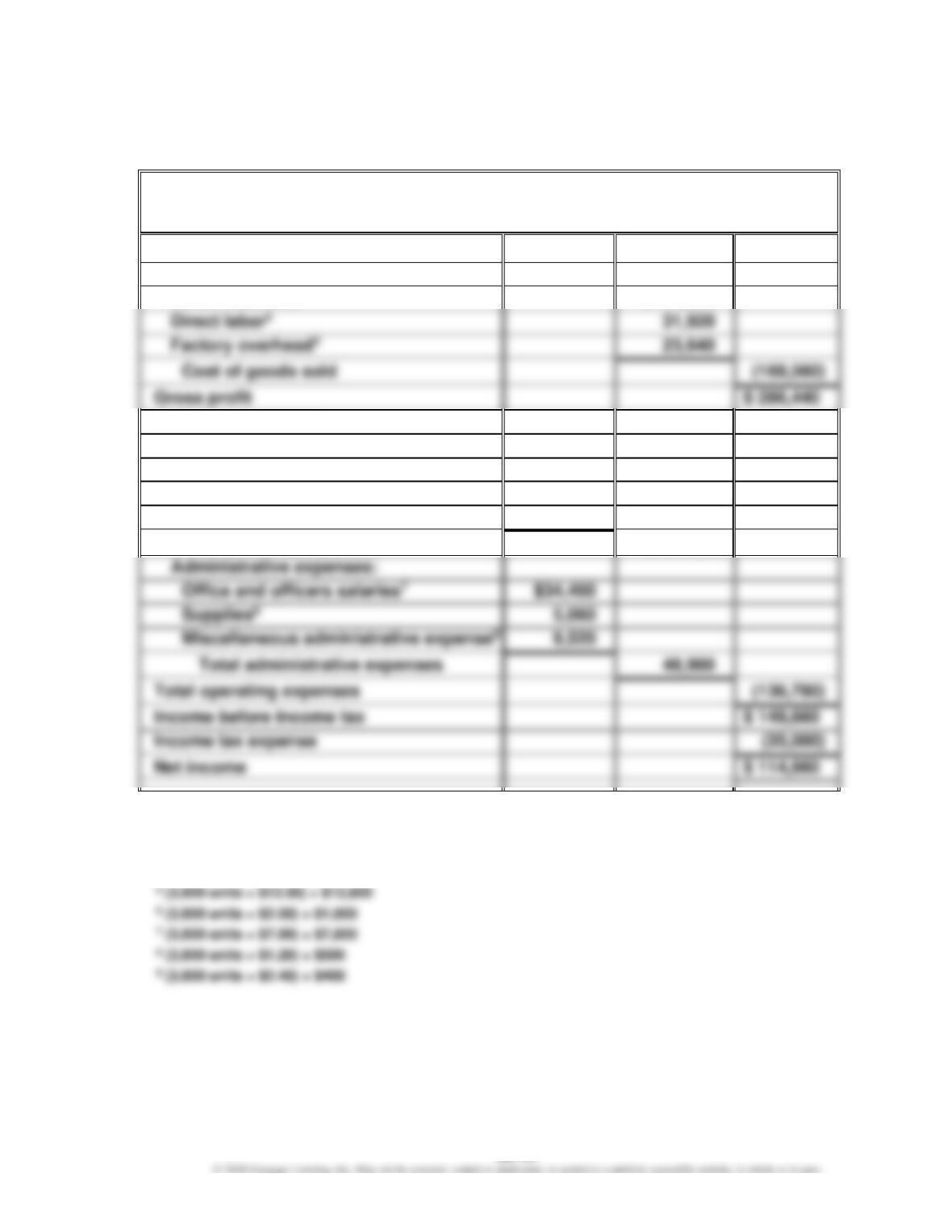

8.

Gold Medal Athletic Co.

Budgeted Income Statement

For the Month Ending March 31

Revenue from sales (from part 1)

$1,088,000

Cost of goods sold (from part 6)

(533,368)

Gross profit

$ 554,632

Operating expenses:

Administrative expenses (from part 7)

Operating income

$ 228,832

Interest revenue

Income before income tax

$ 228,900

Income tax expense (30% rate)

Net income

Selling expenses (from part 7)

$286,300

CHAPTER 22 (FIN MAN); CHAPTER 8 (MAN) Budgeting

Prob. 22–4B (FIN MAN); Prob. 8–4B (MAN)

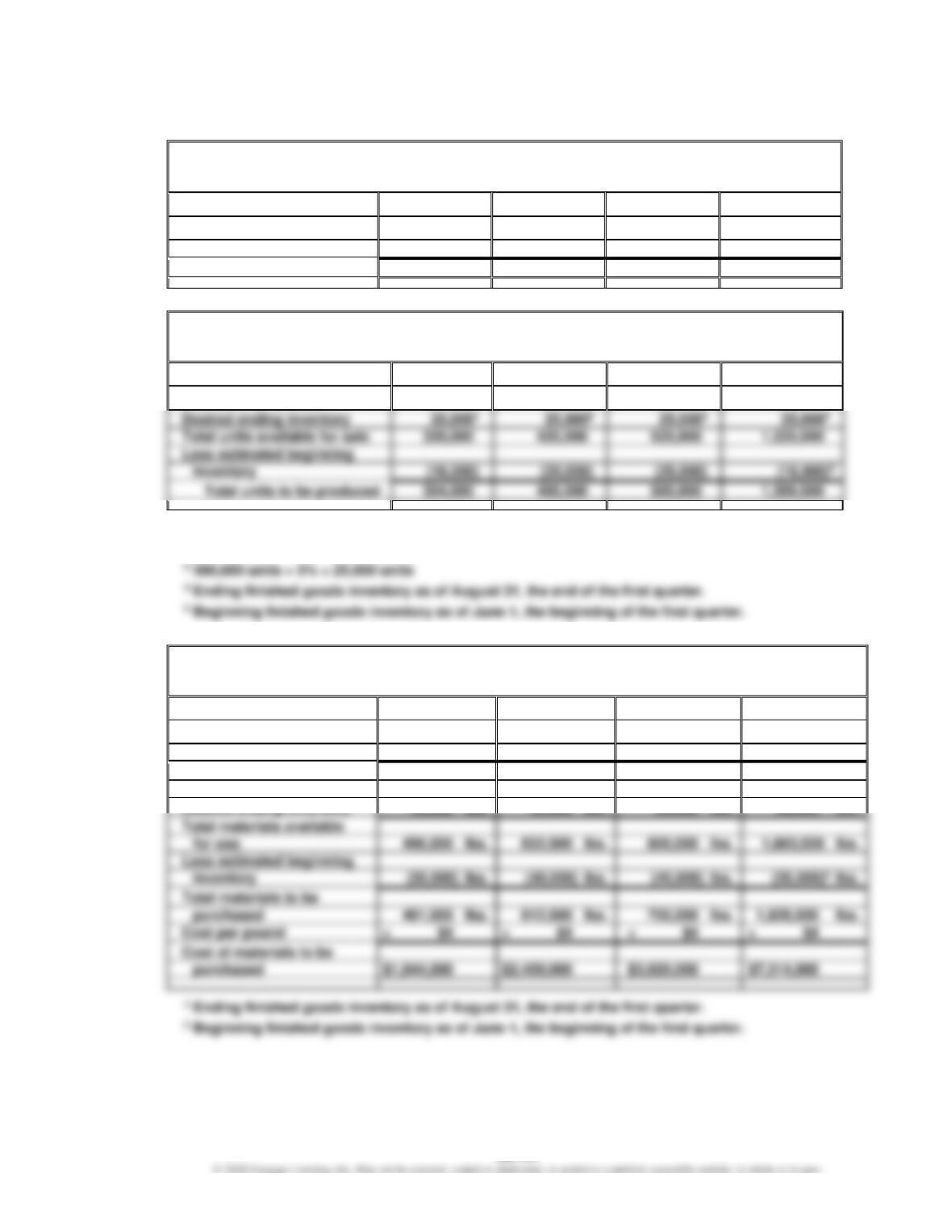

1.

Newport Inc.

Sales Budget

For the First Quarter Ending August 31

June

July

August

First Quarter

Estimated units sold

300,000

400,000

500,000

1,200,000

Selling price per unit

× $36

× $36

× $36

× $36

Total budgeted sales

$10,800,000

$14,400,000

$18,000,000

$43,200,000

2.

Newport Inc.

Production Budget

For the First Quarter Ending August 31

June

July

August

First Quarter

Estimated units sold

300,000

400,000

500,000

1,200,000

Total units available for sale

Less estimated beginning

1 400,000 units × 5% = 20,000 units

2 500,000 units × 5% = 25,000 units

3.

Newport Inc.

Direct Materials Purchases Budget

For the First Quarter Ending August 31

June

July

August

First Quarter

Units to be produced

304,000

405,000

500,000

1,209,000

Materials required per unit

× 1.5

lbs.

× 1.5

lbs.

× 1.5

lbs.

× 1.5

lbs.

Materials required for

production

456,000

lbs.

607,500

lbs.

750,000

lbs.

1,813,500

lbs.

Desired ending inventory

lbs.

lbs.

50,000

lbs.

lbs.

Total materials available

496,000

lbs.

652,500

lbs.

800,000

lbs.

lbs.

Less estimated beginning

inventory

lbs.

lbs.

lbs.

lbs.

purchased

461,000

lbs.

612,500

lbs.

lbs.

1,828,500

lbs.

Cost per pound

× $4

× $4

× $4

Cost of materials to be

CHAPTER 22 (FIN MAN); CHAPTER 8 (MAN) Budgeting

Prob. 22–4B (FIN MAN); Prob. 8–4B (MAN) (Continued)

4.

Newport Inc.

Direct Labor Cost Budget

For the First Quarter Ending August 31

June

July

August

First Quarter

Units to be produced

304,000

405,000

500,000

1,209,000

Direct labor required per unit

× 0.4

hr.

× 0.4

hr.

× 0.4

hr.

× 0.4

hr.

162,000

Direct labor hourly rate

× $25

× $25

× $25

Direct labor cost

5.

Newport Inc.

Factory Overhead Cost Budget

For the First Quarter Ending August 31

June

July

August

First Quarter

Variable factory overhead:

Budgeted direct labor

hours

121,600

162,000

200,000

483,600

Variable factory

Fixed factory overhead:

Budgeted fixed factory

overhead

Total factory overhead cost

CHAPTER 22 (FIN MAN); CHAPTER 8 (MAN) Budgeting

Prob. 22–4B (FIN MAN); Prob. 8–4B (MAN) (Continued)

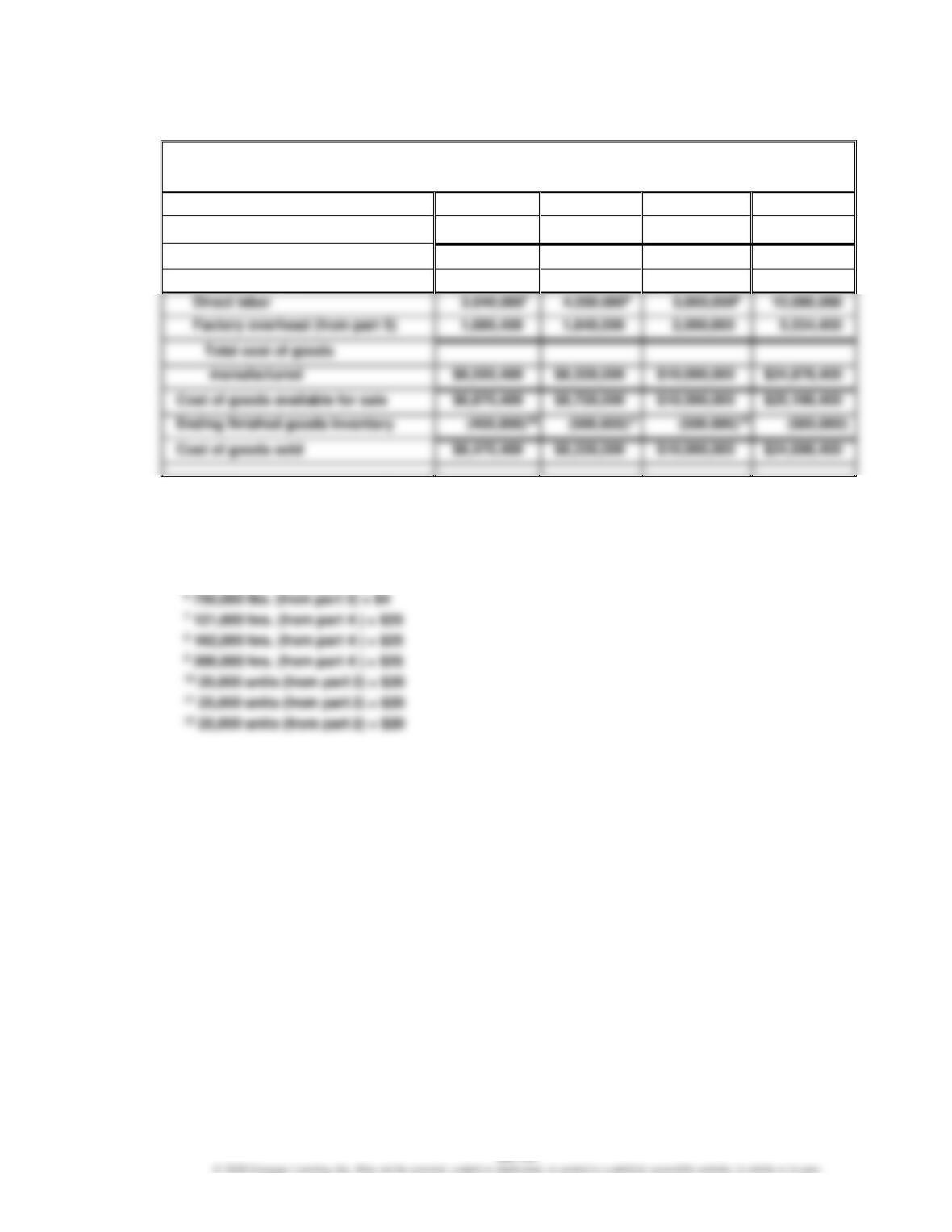

6.

Newport Inc.

Cost of Goods Sold Budget

For the First Quarter Ending August 31

June

July

August

First Quarter

Beginning finished goods inventory

$ 320,0001

$ 400,0002

$ 500,0003

$ 320,000

Cost of goods manufactured:

Direct materials

$1,824,0004

$2,430,0005

$ 3,000,0006

$ 7,254,000

Factory overhead (from part 5)

Cost of goods available for sale

$8,728,000

Ending finished goods inventory

Cost of goods sold

1 16,000 units (from part 2) × $20

2 20,000 units (from part 2) × $20

3 25,000 units (from part 2) × $20

4 456,000 lbs. (from part 3) × $4

5 607,500 lbs. (from part 3) × $4

CHAPTER 22 (FIN MAN); CHAPTER 8 (MAN) Budgeting

Prob. 22–4B (FIN MAN); Prob. 8–4B (MAN) (Concluded)

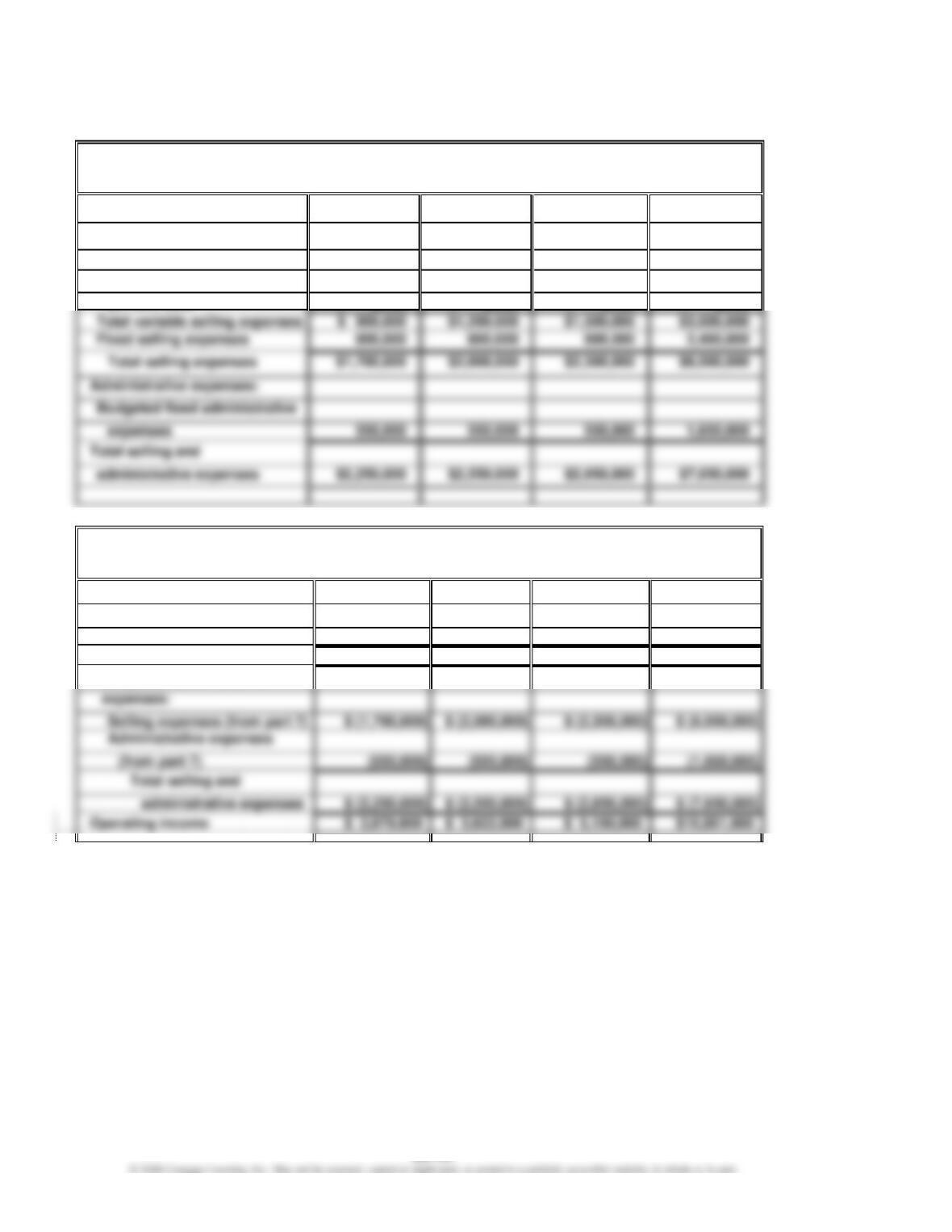

7.

Newport Inc.

Selling and Administrative Expenses Budget

For the First Quarter Ending August 31

June

July

August

First Quarter

Selling expenses:

Budgeted sales units

300,000

400,000

500,000

1,200,000

Variable selling expenses

per unit sold

× $3.00

× $3.00

× $3.00

× $3.00

Fixed selling expenses

800,000

800,000

2,400,000

Administrative expenses:

Budgeted fixed administrative

Total selling and

8.

Newport Inc.

Budgeted Income Statement

For the First Quarter Ending August 31

June

July

August

First Quarter

Sales (from part 1)

$10,800,000

$14,400,000

$18,000,000

$43,200,000

Cost of goods sold (from part 6)

(6,470,400)

(8,228,000)

(10,000,000)

(24,698,400)

Gross profit

$ 4,329,600

$ 6,172,000

$ 8,000,000

$18,501,600

Selling and administrative

Selling expenses (from part 7)

$ (2,550,000)

CHAPTER 22 (FIN MAN); CHAPTER 8 (MAN) Budgeting

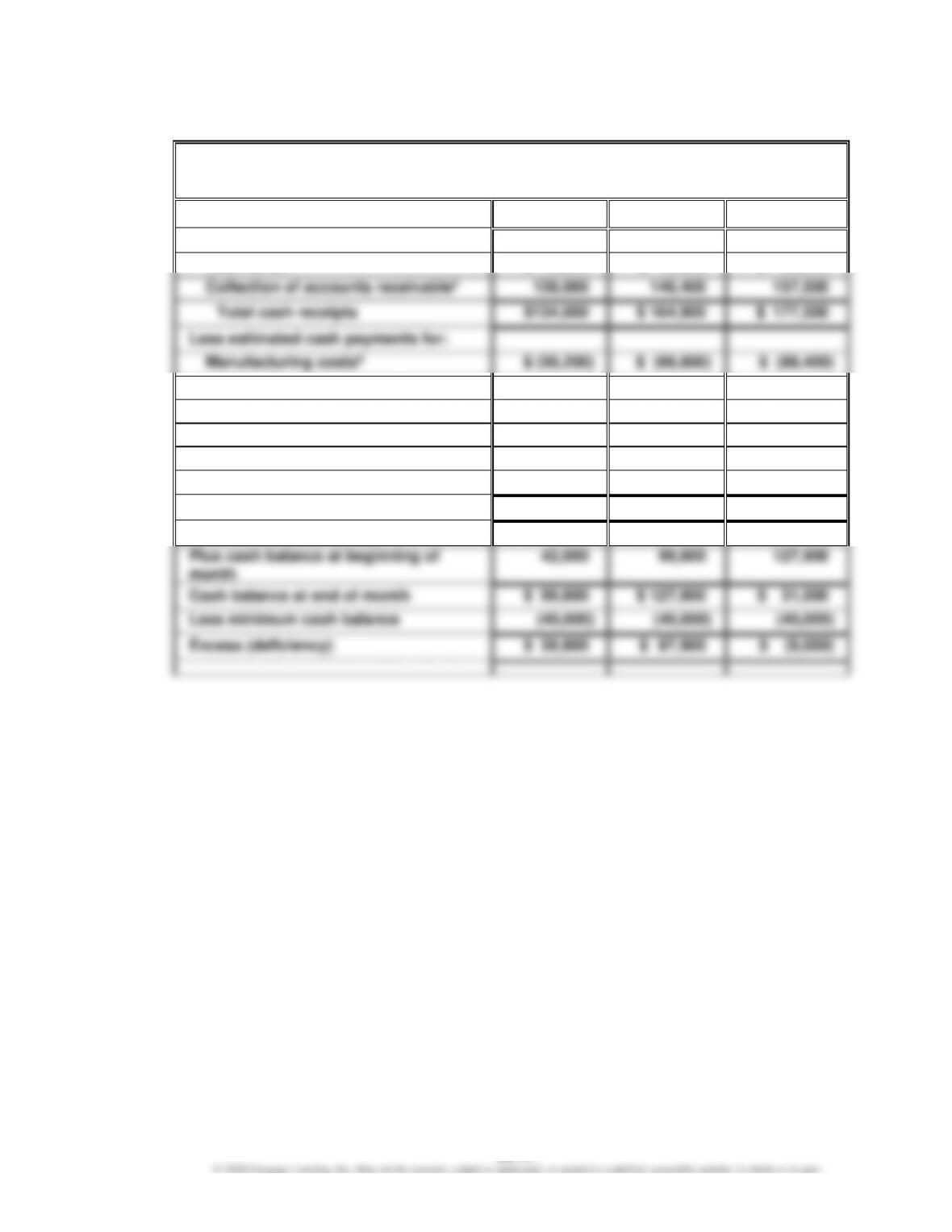

Prob. 22–5B (FIN MAN); Prob. 8–5B (MAN)

1.

Mercury Shoes Inc.

Cash Budget

For the Three Months Ending August 31

June

July

August

Estimated cash receipts from:

Less estimated cash payments for:

Cash sales

$ 16,000

$ 18,500

$ 20,000

Selling and administrative expenses

(40,000)

(46,000)

(51,000)

Capital expenditures

(120,000)

Other purposes:

Income tax

(24,000)

Dividends

(15,000)

Total cash payments

$ (96,200)

$(136,800)

$(274,400)

Cash increase (decrease)

$ 57,800

$ 28,100

$ (96,900)

$ 99,800

$ 31,000

Less minimum cash balance

(40,000)

(40,000)

(40,000)

CHAPTER 22 (FIN MAN); CHAPTER 8 (MAN) Budgeting

Prob. 22–5B (FIN MAN); Prob. 8–5B (MAN) (Concluded)

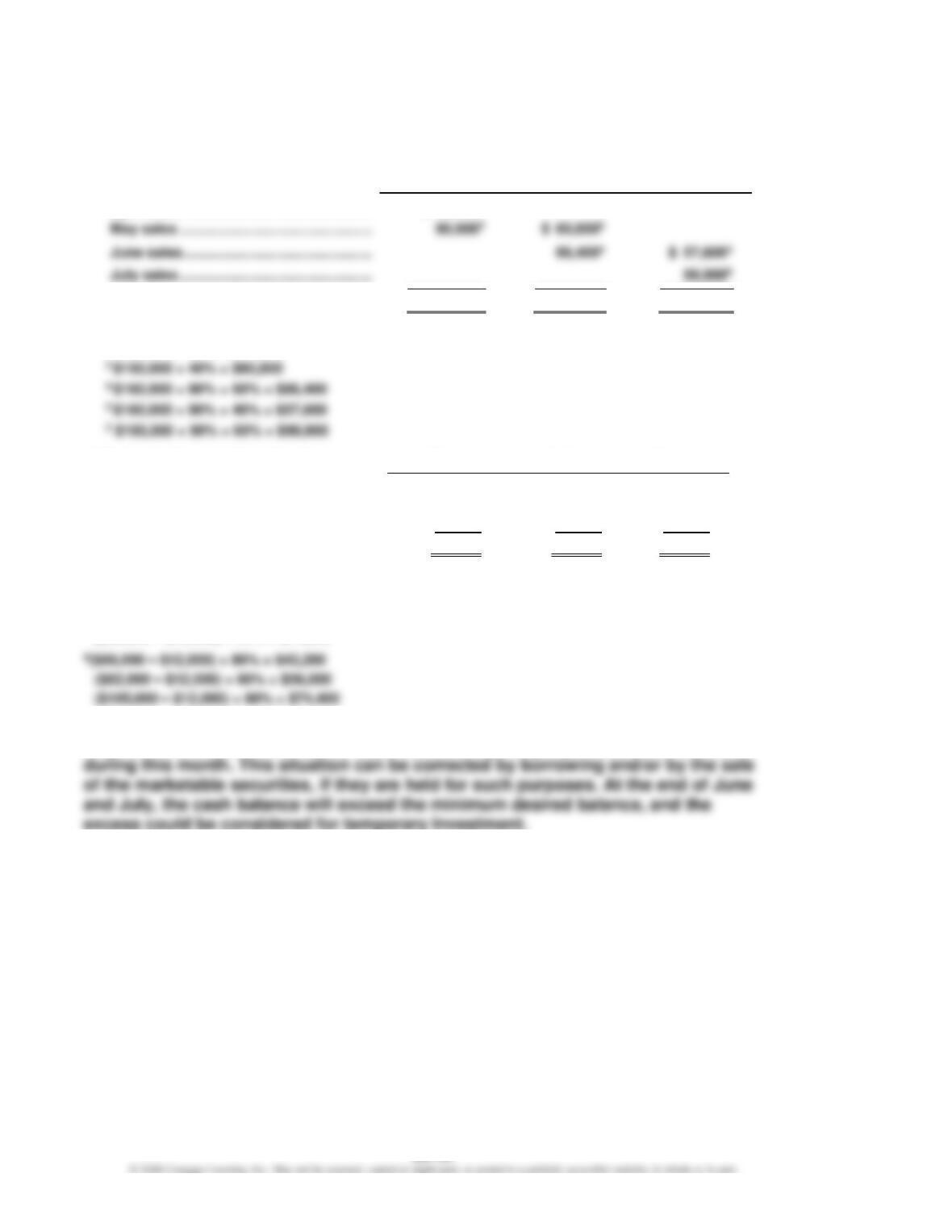

Computations:

a Collections of accounts receivable:

June

July

August

April sales …………………………………………

$ 48,0001

Total ……………………………………………….

$138,000

$146,400

$157,500

1 $120,000 × 40% = $48,000

2 $150,000 × 60% = $90,000

b Payments for manufacturing costs:

June

July

August

Payment of accounts payable,

beginning of month balancec …………..

$13,000

$10,800

$14,000

Payment of current month’s costd ………

43,200

56,000

74,400

Total ……………………………………………….

$56,200

$66,800

$88,400

c Accounts payable, June 1 balance = $13,000

($66,000 – $12,000) × 20% = $10,800

($82,000 – $12,000) × 20% = $14,000

2. The budget indicates that the minimum cash balance will not be maintained in

August. This is due to the capital expenditures requiring significant cash outflows

CHAPTER 22 (FIN MAN); CHAPTER 8 (MAN) Budgeting

Prob. 22–6B (FIN MAN); Prob. 8–6B (MAN)

1.

Mesa Publishing Co.

Budgeted Income Statement

For the Year Ending December 31, 20Y9

Sales1

$ 456,000

Cost of goods sold:

Direct materials2

$114,000

Gross profit

Operating expenses:

Selling expenses:

Sales salaries and commissions5

$64,100

Advertising

13,200

Miscellaneous selling expenses6

10,500

Total selling expenses

$ 87,800

Administrative expenses:

Office and officers salaries7

$34,400

Total operating expenses

Income tax expense

1 3,800 units × $120

2 3,800 units × $30

3 3,800 units × $8.40

4 (3,800 units × $4.80) + $4,000 + $1,400

CHAPTER 22 (FIN MAN); CHAPTER 8 (MAN) Budgeting

Prob. 22–6B (FIN MAN); Prob. 8–6B (MAN) (Concluded)

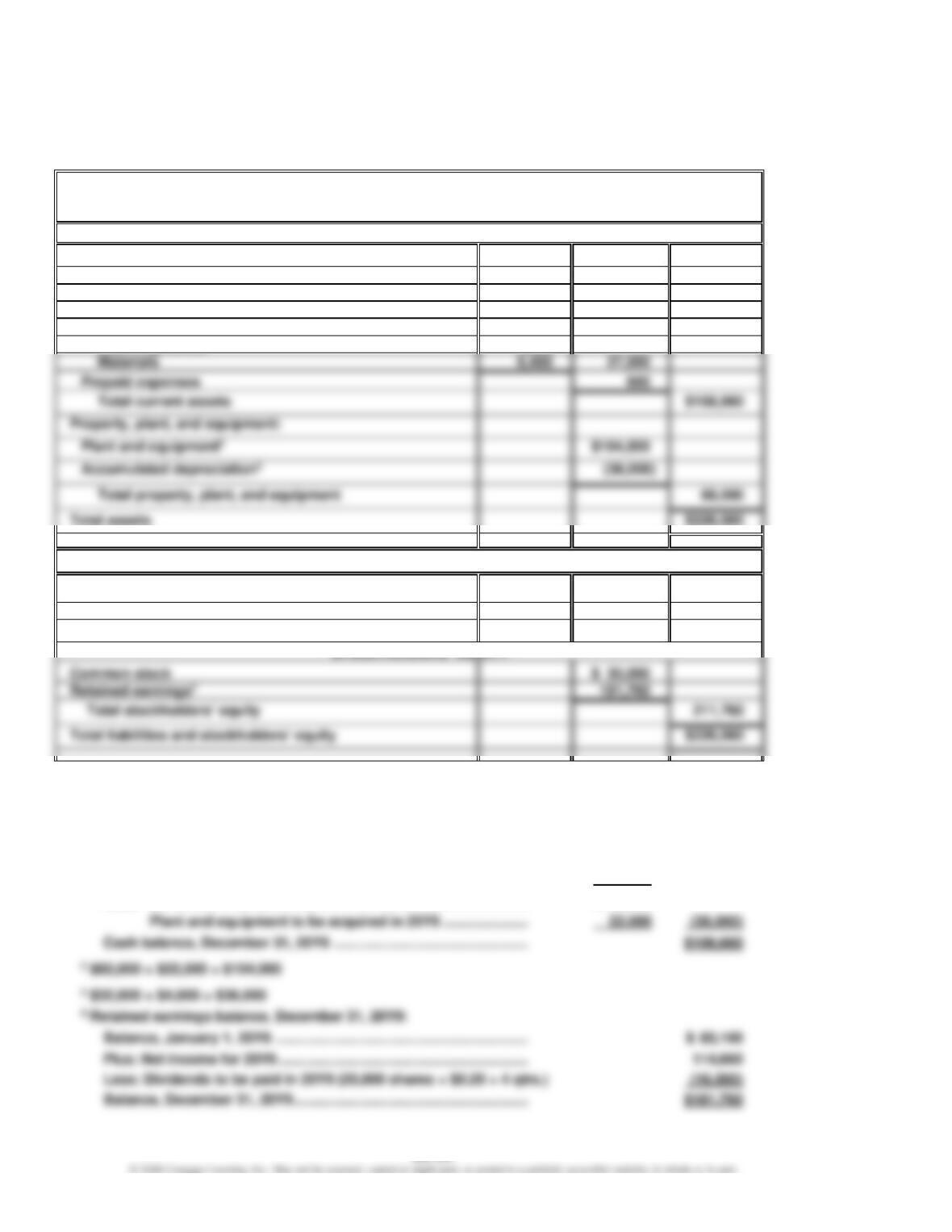

2.

Mesa Publishing Co.

Budgeted Balance Sheet

December 31, 20Y9

ASSETS

Current assets:

Cash 1

$106,660

Accounts receivable

23,800

Inventories:

Finished goods

$16,900

Work in process

4,200

6,400

27,500

Prepaid expenses

Property, plant, and equipment:

Total assets

LIABILITIES

Current liabilities:

Accounts payable

$ 14,800

Total liabilities and stockholders’ equity

1 Cash balance, December 31, 20Y9:

Balance, January 1, 20Y9 …………………………..…………………………...

$ 26,000

Add:

Cash from operations

Net income …………………………………………………………………..

$114,660

Depreciation of plant and equipment …………………………….

4,000

118,660

Less:

Dividends to be paid in 20Y9 …………………………………………

$ 16,000

Plant and equipment to be acquired in 20Y9 ………………….

CHAPTER 22 (FIN MAN); CHAPTER 8 (MAN) Budgeting

MAKE A DECISION

MAD 22–1 (FIN MAN); MAD 8–1 (MAN)

a.

Average daily revenue

$96,000

Revenue per clerk

÷12,000

Number of additional sales clerks

8

Hours per day per clerk

Number of shopping days

Rate per hour

b.

Johnson Stores should add the staff because it will be profitable.

Increase in daily revenue

$ 96,000

Gross profit percentage

× 40%

Increase in daily gross profit

$ 38,400

Staff budget increase [from (a)]

CHAPTER 22 (FIN MAN); CHAPTER 8 (MAN) Budgeting

MAD 22–2 (FIN MAN); MAD 8–2 (MAN)

a. There are 680 expected RVUs per day for the coming week.

Number of Patients

RVUs per Day

Total Daily

RVUs

5

20

100

8

25

200

b. Total daily RVUs ……………………………………….

680

Daily RVUs per nurse ………………………………..

÷ 40

MAD 22–3 (FIN MAN); MAD 8–3 (MAN)

a.

School Days

Nonschool

Days

Total

Number of vehicles per day

3,000

8,000

Vehicles per staff member

÷ 200

÷ 200

Number of staff

Daily staff expense

b.

School Days

Nonschool

Days

Total

Number of vehicles per day

3,000

8,000

c.

Total budgeted revenues [from (b)] ………………………………………………..

$20,950,000

Parking lot staff expenses [from (a)] ………………………………………………

Other expenses …………………………………………………………………………….

Budgeted parking lot profit ……………………………………………………………

$17,797,750

CHAPTER 22 (FIN MAN); CHAPTER 8 (MAN) Budgeting

MAD 22–4 (FIN MAN); MAD 8–4 (MAN)

a.

Weekday

Weekend Day

Room occupancy

Room capacity

300

300

Occupancy

×80%

×40%

Rooms occupied (1)

240

120

Number of minutes to clean a room (2)

Total minutes [(a) × (b)]

Labor rate per hour

c.

Restaurant staff

Base restaurant staff

6

6

Incremental staff for room blocks [(1) ÷

60 room blocks]

+4

+2

Total staff

10

8

CHAPTER 22 (FIN MAN); CHAPTER 8 (MAN) Budgeting

TAKE IT FURTHER

TIF 22–1 (FIN MAN); TIF 8–1 (MAN)

Cam should reject Megan’s request to charge the convention-related costs against July’s

budget. This is just one example of many attempts to slide expenses into different budget

periods than when actually incurred. This is a common issue that controllers face. Often,

TIF 22–2 (FIN MAN); TIF 8–2 (MAN)

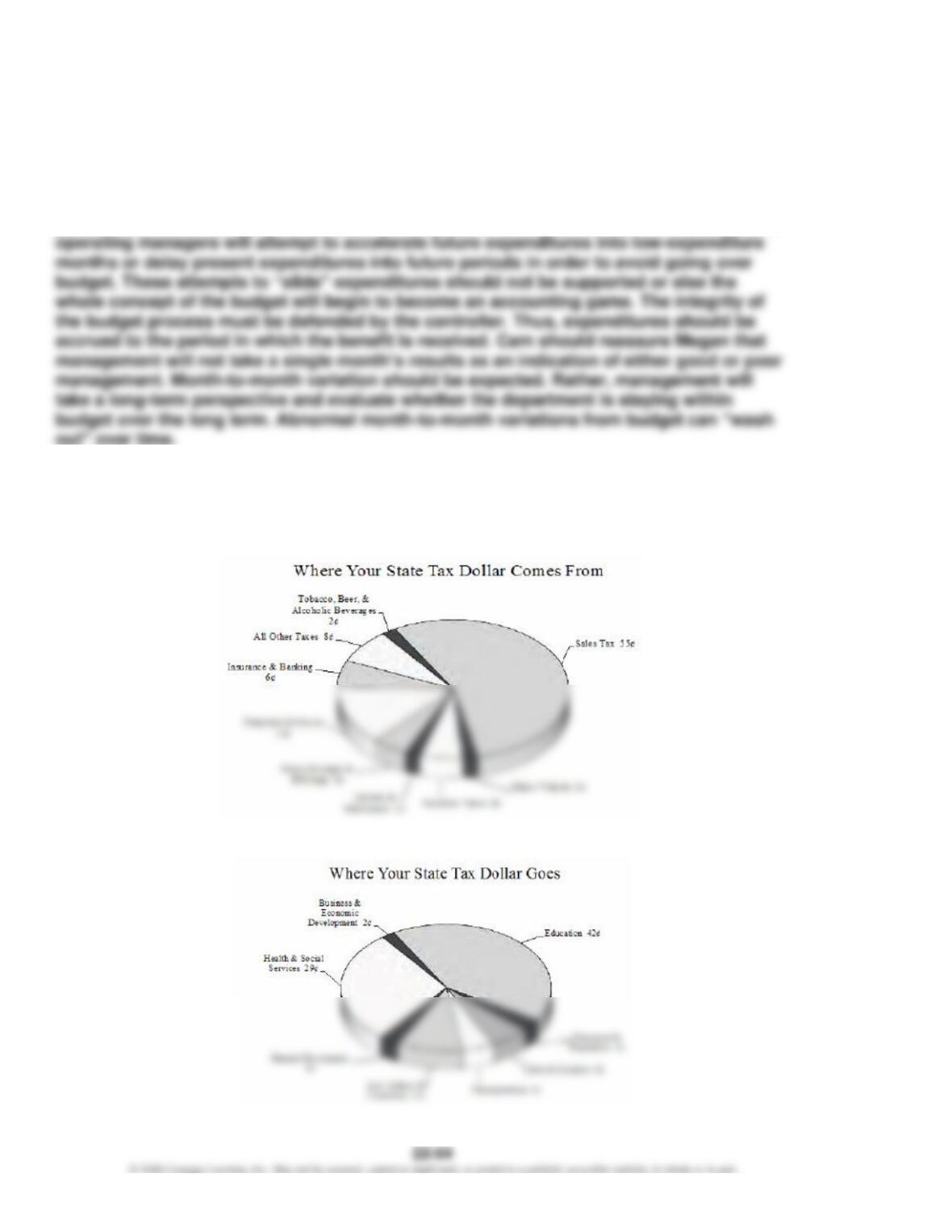

Answers will vary per state selected. Examples from the state of Tennessee are shown here.

a.

b.

CHAPTER 22 (FIN MAN); CHAPTER 8 (MAN) Budgeting

TIF 22–3 (FIN MAN); TIF 8–3 (MAN)

Memo

To: Stacy Poindexter

From: Ima Student

Re: Evaluating City of Milton Budget

After reviewing the city of Milton’s budget data, it appears that considerable goal conflict

exists within departments, resulting in department managers making poor budgeting and

spending decisions. The amount of actual expenditures was less than budgeted for the

first 10 months of the budget year. As the budget year-end approached, department

managers appear to have spent the remaining excess budget, going over budget in May

There are a number of techniques that the city could undertake to more effectively

budget and align departmental behavior with the city’s goals. First, departments could

adopt flexible budgets, which allow for monthly budgets to change with underlying

activity. For example, if the number of prisoners in the jail increased, then the budget

would increase proportionately. Department managers with a flexible budget would be

less likely to “reserve” a large portion of the budget during the year because an activity

change would automatically be reflected in the monthly budget. This reduces the

CHAPTER 22 (FIN MAN); CHAPTER 8 (MAN) Budgeting

TIF 22–4 (FIN MAN); TIF 8–4 (MAN)

a. The hospital’s new budget method is clearly an example of a flexible budget. The

budget changes with changes in underlying activity, such as patient days.

The budget helps the managers plan month-by-month expenditures.

b. The advantage of a flexible budget is to accurately plan variable costs of the

hospital with changes in the underlying activity base. Using a static budget

would create actual deviations from budget that would be difficult to

TIF 22–5 (FIN MAN); TIF 8–5 (MAN)

a. The budget information indicates that the actual expenditures by the Operations

b. The bank manager does not know if the actual resources consumed by the

Operations Department are the right amount of resources for doing the right things.

In other words, this budget doesn’t say anything about the actual work of the

CHAPTER 22 (FIN MAN); CHAPTER 8 (MAN) Budgeting

TIF 22–5 (FIN MAN); TIF 8–5 (MAN) (Concluded)

The budget doesn’t indicate why there was more travel and training than

expected. Maybe the department introduced a new computer system, and all

TIF 22–6 (FIN MAN); TIF 8–6 (MAN)

Domino’s could use a master budget to plan operations consistent with the sales

forecast. The sales forecast could be used to develop the production budget for

pizzas. The sales and production budgets would be identical because there would

be no finished goods inventory for cooked pizzas. The sales (production) budget

would be used to develop a direct materials purchases budget. For example, the

The budget process could be used to direct and coordinate all the various

restaurants. In this way, all the managers would be operating under the same set of

assumptions. The actual performance of the company and the individual stores

could be compared with the budget in order to provide all levels of the organization

appropriate feedback and control. This feedback can be used to adjust operations

CHAPTER 22 (FIN MAN); CHAPTER 8 (MAN) Budgeting

CERTIFIED MANAGEMENT ACCOUNTANT (CMA®)

EXAMINATION QUESTIONS (ADAPTED)

1. d. Flexible budgets are based on the output actually achieved and therefore

provide a realistic comparison of budgeted and actual revenue and costs.

2. b. Hannon’s budget for the purchase of inventory should be $540,000, computed as

follows:

75% of the cost of inventory to be sold in August

3. c. Ming should plan to produce 7,133 units in July, computed as follows:

4. c. The cost of one laminated putter head is $52, computed as follows:

Laminated putter head cost per unit:

Steel

$ 5.00

Copper

15.00

Direct labor

22.00

Variable OH

6.25*

Fixed OH

3.75**

Total cost

$52.00

Direct labor hours required for production:

Forged units:

8,200 – 300 + 100 = 8,000 units;

8,000 units × 0.25 hr. per unit =

2,000 hours

Laminated units:

2,000 units × 1.0 hr. per unit = 2,000 hours

2,000 hours