CHAPTER 22 (FIN MAN); CHAPTER 8 (MAN) Budgeting

Prob. 22–3A (FIN MAN); Prob. 8–3A (MAN)

1.

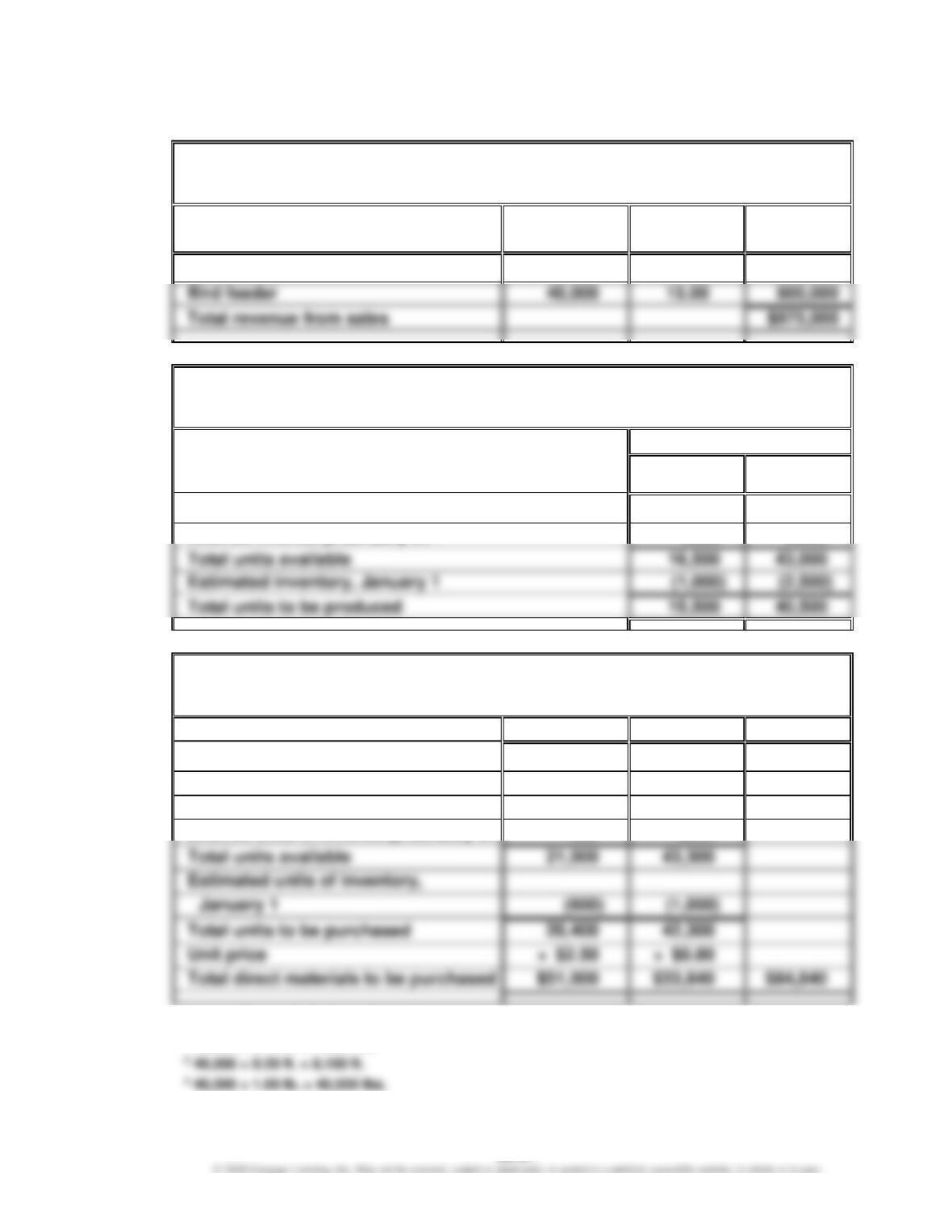

Birding Homes & Feeders Inc.

Sales Budget

For the Month Ending January 31

Unit Sales

Volume

Unit Selling

Price

Total Sales

Bird house

15,000

$25.00

$375,000

Bird feeder

Total revenue from sales

2.

Birding Homes & Feeders Inc.

Production Budget

For the Month Ending January 31

Units

Bird

House

Bird

Feeder

Expected units to be sold

15,000

40,000

Total units available

16,500

Estimated inventory, January 1

Total units to be produced

15,500

Desired inventory, January 31

1,500

3,000

3.

Birding Homes & Feeders Inc.

Direct Materials Purchases Budget

For the Month Ending January 31

Wood

Plastic

Total

Required units for production:

Bird house

12,4001

1,5502

Bird feeder

8,1003

40,5004

Total direct materials to be purchased

Desired units of inventory, January 31

500

1,250

1 15,500 × 0.80 ft. = 12,400 ft.

2 15,500 × 0.10 lb. = 1,550 lbs.

CHAPTER 22 (FIN MAN); CHAPTER 8 (MAN) Budgeting

Prob. 22–3A (FIN MAN); Prob. 8–3A (MAN) (Continued)

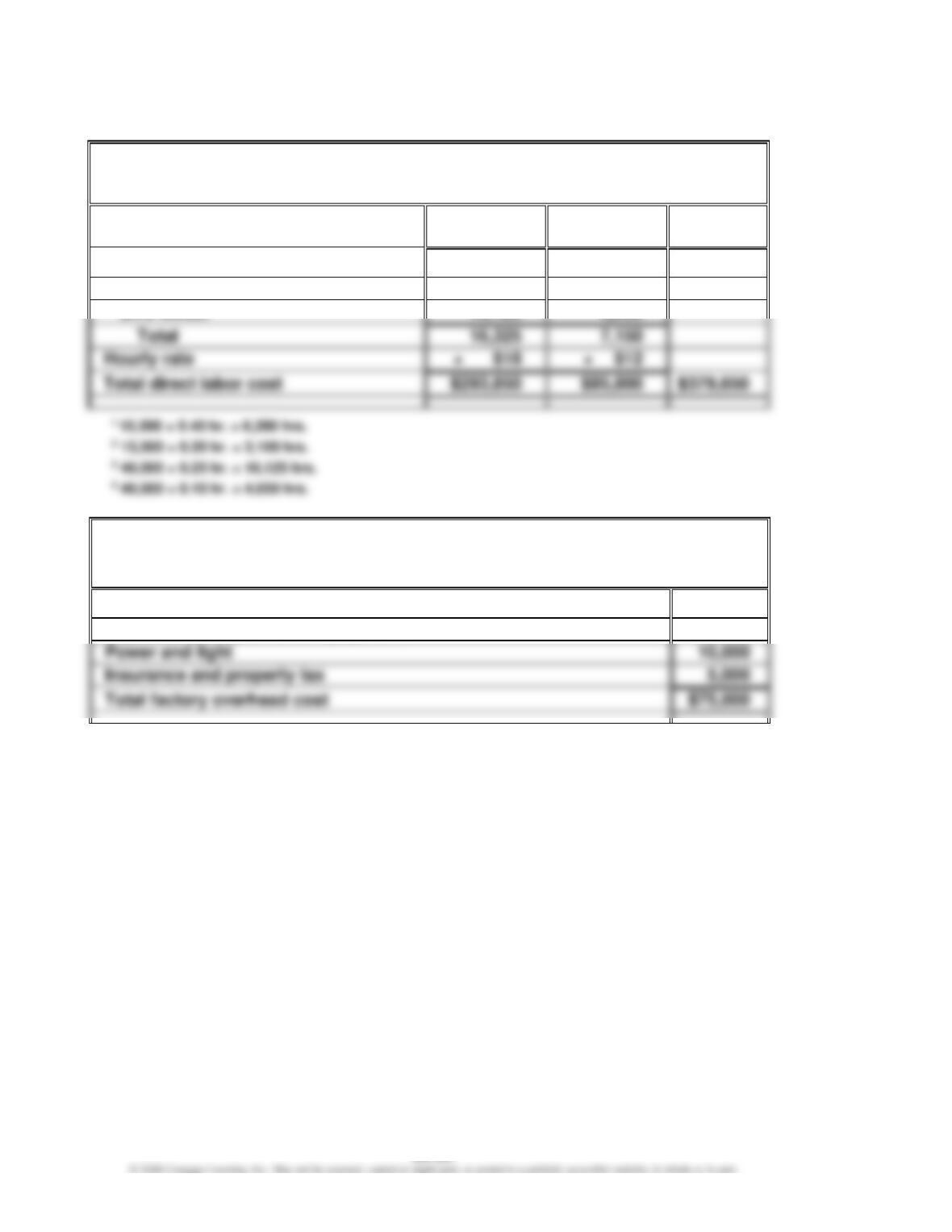

4.

Birding Homes & Feeders Inc.

Direct Labor Cost Budget

For the Month Ending January 31

Fabrication

Department

Assembly

Department

Total

Hours required for production:

Bird house

6,2001

3,1002

Bird feeder

5.

Birding Homes & Feeders Inc.

Factory Overhead Cost Budget

For the Month Ending January 31

Indirect factory wages

$40,000

Depreciation of plant and equipment

20,000

Power and light

10,000

Insurance and property tax

Total factory overhead cost

CHAPTER 22 (FIN MAN); CHAPTER 8 (MAN) Budgeting

Prob. 22–3A (FIN MAN); Prob. 8–3A (MAN) (Continued)

6.

Birding Homes & Feeders Inc.

Cost of Goods Sold Budget

For the Month Ending January 31

Finished goods inventory, January 11

$ 35,000

Work in process inventory, January 1

$ 9,000

Direct materials:

Direct materials inventory, January 12

$ 2,300

Direct materials inventory, January 313

production

$ 84,890

Direct labor (from part 4)

379,650

Factory overhead (from part 5)

75,000

Total manufacturing costs

539,540

Total work in process during period

$548,540

Cost of finished goods available for sale

1

Bird house (1,000 × $15) …………………………………………………………………….

$15,000

Bird feeder (2,500 × $8) ………………………………………………………………………

20,000

Finished goods inventory, December 1 ……………………………………………….

$35,000

2

Wood (600 × $2.50) …………………………………………………………………………….

$ 1,500

Plastic (1,000 × $0.80)…………………………………………………………………………

800

Direct materials inventory, December 1 …………………………..………………….

$ 2,300

CHAPTER 22 (FIN MAN); CHAPTER 8 (MAN) Budgeting

Prob. 22–3A (FIN MAN); Prob. 8–3A (MAN) (Concluded)

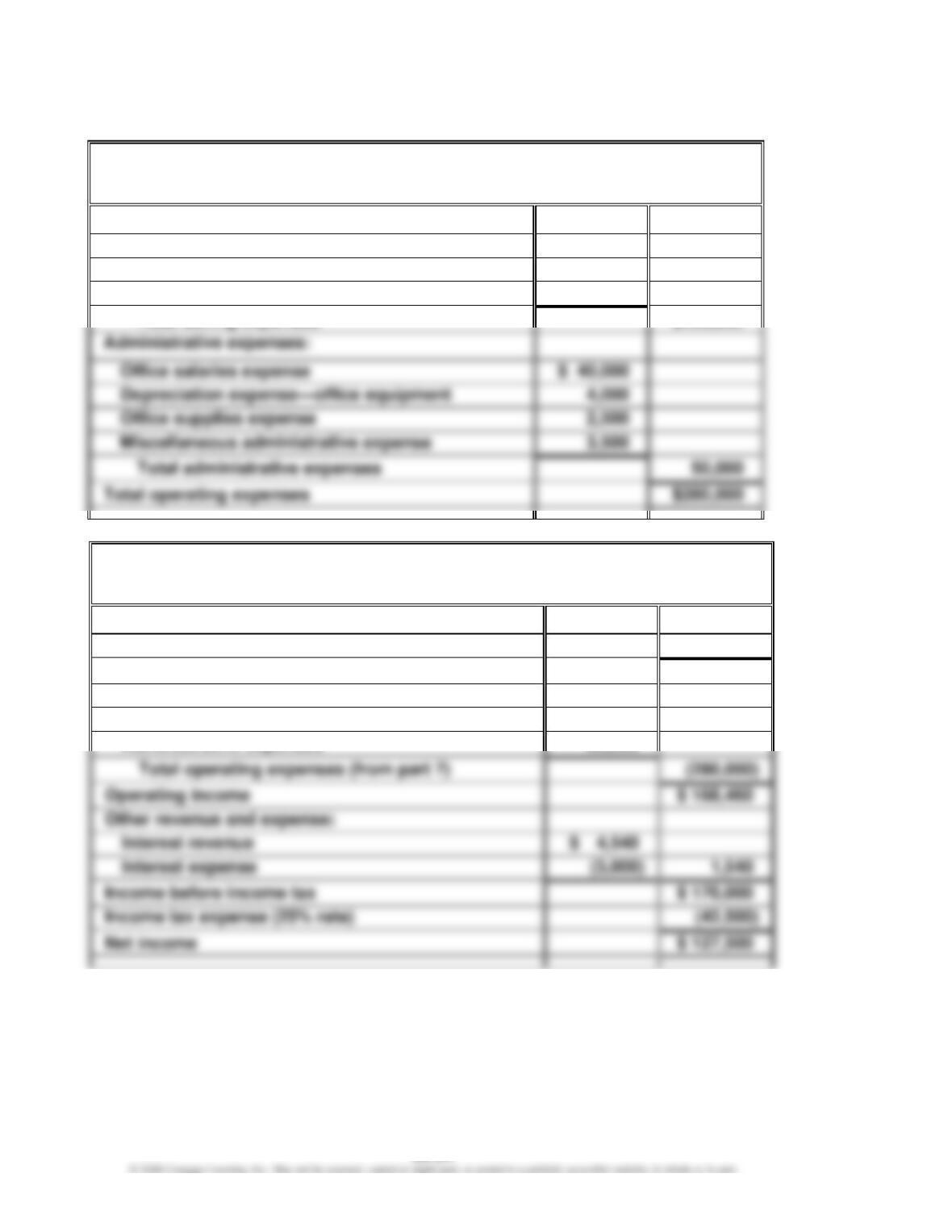

7.

Birding Homes & Feeders Inc.

Selling and Administrative Expenses Budget

For the Month Ending January 31

Selling expenses:

Sales salaries expense

$125,000

Advertising expense

80,000

Travel expense—selling

25,000

$230,000

Depreciation expense—office equipment

Office supplies expense

Miscellaneous administrative expense

50,000

8.

Birding Homes & Feeders Inc.

Budgeted Income Statement

For the Month Ending January 31

Revenue from sales (from part 1)

$ 975,000

Cost of goods sold (from part 6)

(526,540)

Gross profit

$ 448,460

Operating expenses:

Selling expenses (from part 7)

$230,000

Administrative expenses

50,000

(280,000)

Operating income

$ 168,460

Other revenue and expense:

Interest revenue

Interest expense

Income tax expense (25% rate)

CHAPTER 22 (FIN MAN); CHAPTER 8 (MAN) Budgeting

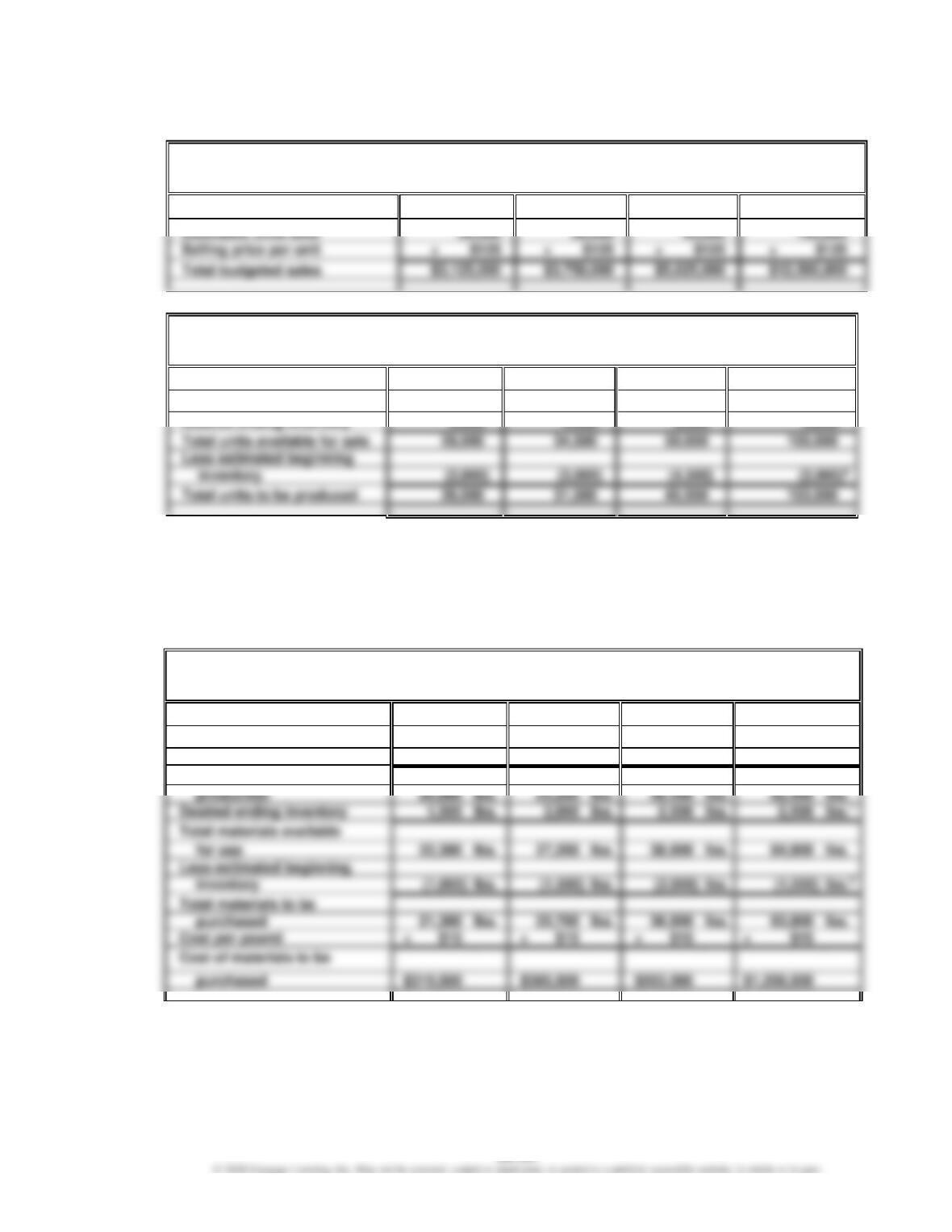

Prob. 22–4A (FIN MAN); Prob. 8–4A (MAN)

1.

Bellaire Inc.

Sales Budget

For the First Quarter Ending March 31

January

February

March

First Quarter

Estimated units sold

$3,125,000

2.

Bellaire Inc.

Production Budget

For the First Quarter Ending March 31

January

February

March

First Quarter

Estimated units sold

25,000

30,000

45,000

100,000

Less estimated beginning

inventory

1 30,000 units × 10% = 3,000 units

2 45,000 units × 10% = 4,500 units

3 50,000 units × 10% = 5,000 units

4 Ending finished goods inventory as of March 31, the end of the first quarter.

5 Beginning finished goods inventory as of January 1, the beginning of the first quarter.

3.

Bellaire Inc.

Direct Materials Purchases Budget

For the First Quarter Ending March 31

January

February

March

First Quarter

Units to be produced

26,000

31,500

45,500

103,000

Materials required per unit

× 0.8

lb.

× 0.8

lb.

× 0.8

lb.

× 0.8

lb.

Materials required for

production

Desired ending inventory

2,500

22,300

38,900

Less estimated beginning

(2,000)

Total materials to be

1 Ending materials inventory as of March 31, the end of the first quarter.

2 Beginning materials inventory as of January 1, the beginning of the first quarter.

CHAPTER 22 (FIN MAN); CHAPTER 8 (MAN) Budgeting

Prob. 22–4A (FIN MAN); Prob. 8–4A (MAN) (Continued)

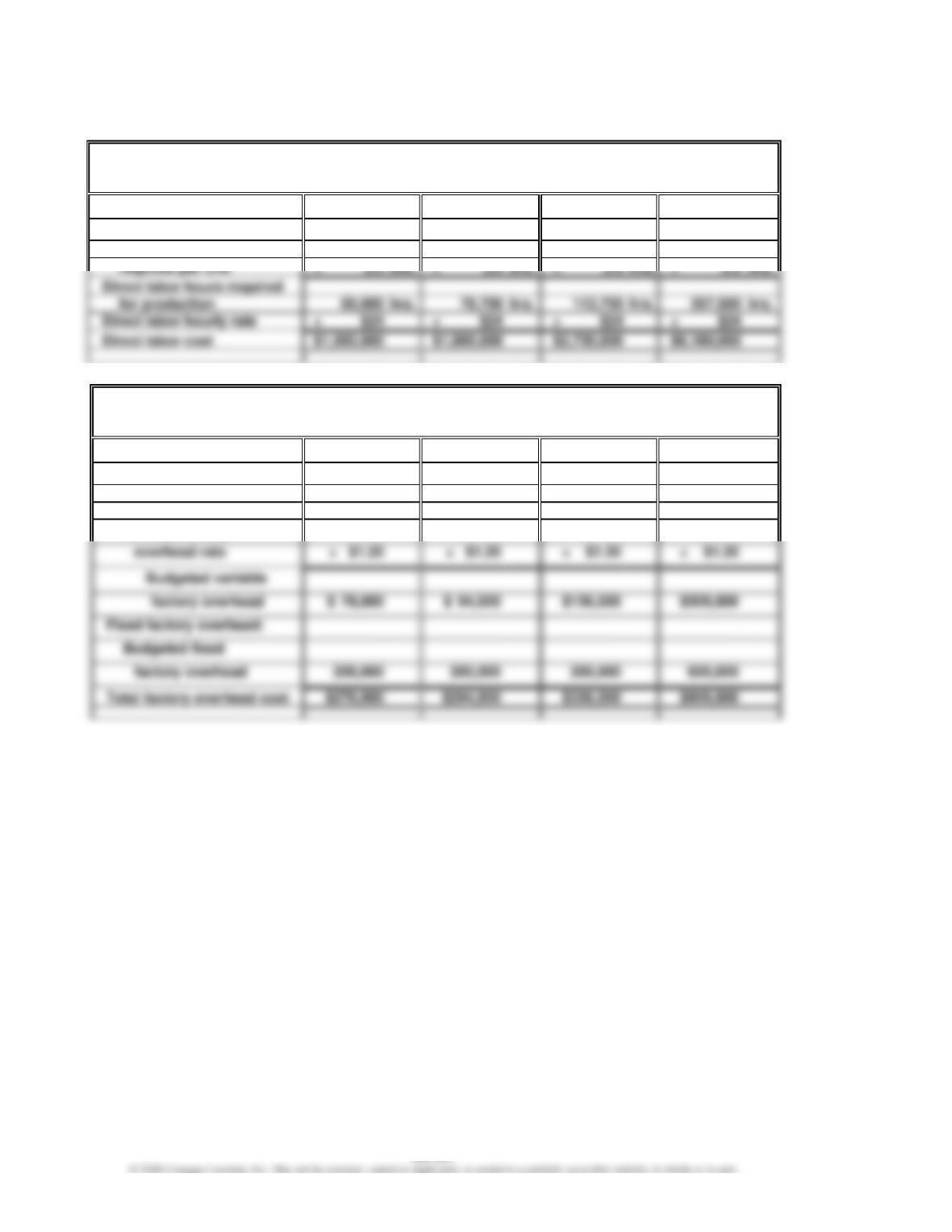

4.

Bellaire Inc.

Direct Labor Cost Budget

For the First Quarter Ending March 31

January

February

March

First Quarter

Units to be produced

26,000

31,500

45,500

103,000

Direct labor hours

required per unit

hrs.

hrs.

hrs.

hrs.

Direct labor hours required

Direct labor hourly rate

Direct labor cost

5.

Bellaire Inc.

Factory Overhead Cost Budget

For the First Quarter Ending March 31

January

February

March

First Quarter

Variable factory overhead:

Budgeted direct labor

hours

65,000

hrs.

78,750

hrs.

113,750

hrs.

257,500

hrs.

Variable factory

Total factory overhead cost

CHAPTER 22 (FIN MAN); CHAPTER 8 (MAN) Budgeting

Prob. 22–4A (FIN MAN); Prob. 8–4A (MAN) (Continued)

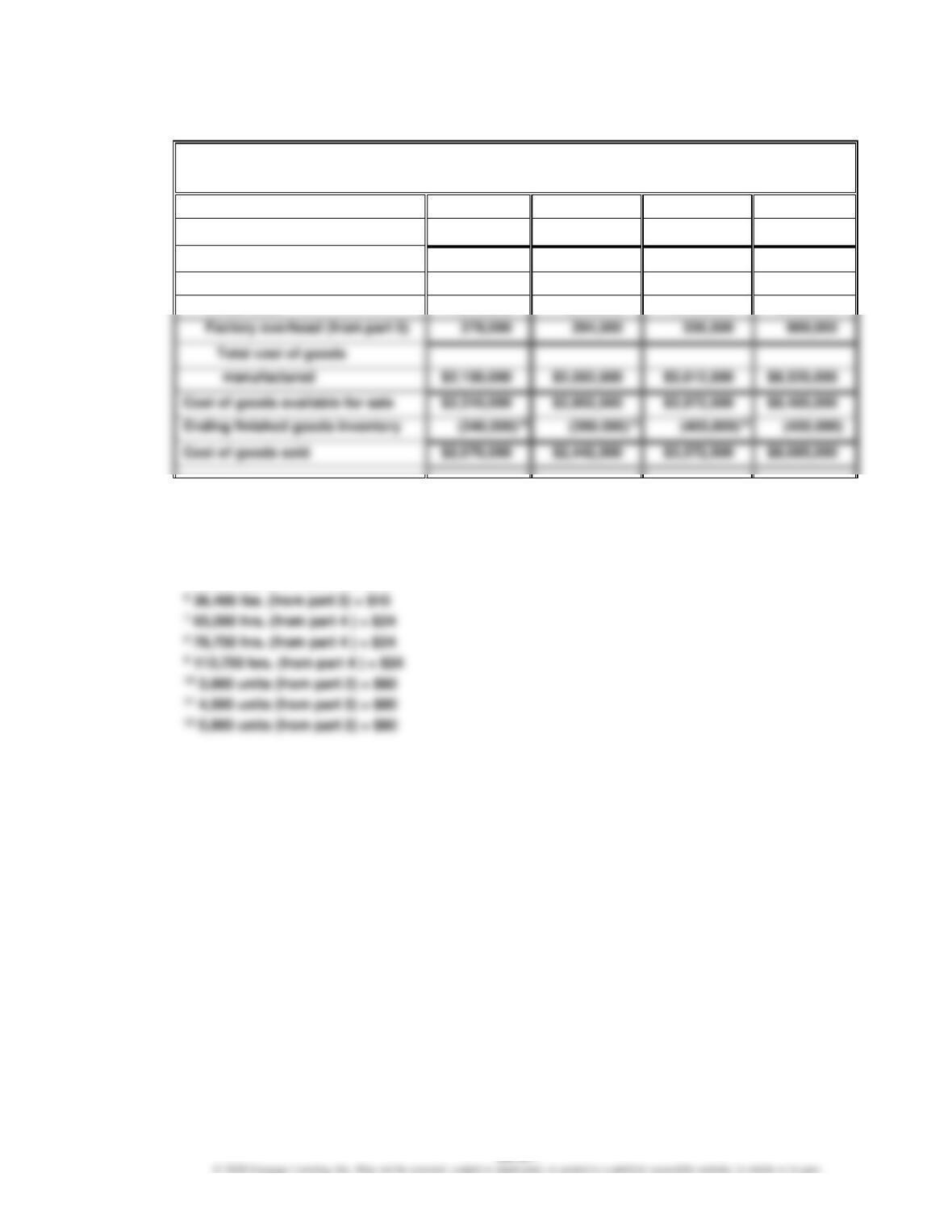

6.

Bellaire Inc.

Cost of Goods Sold Budget

For the First Quarter Ending March 31

January

February

March

First Quarter

Beginning finished goods inventory

$ 160,0001

$ 240,0002

$ 360,0003

$ 160,000

Cost of goods manufactured:

Direct materials

$ 312,0004

$ 378,0005

$ 546,0006

$1,236,000

Factory overhead (from part 5)

$2,310,000

$8,485,000

Cost of goods sold

Direct labor

1,560,0007

1,890,0008

2,730,0009

6,180,000

1 2,000 units (from part 2) × $80

2 3,000 units (from part 2) × $80

3 4,500 units (from part 2) × $80

4 20,800 lbs. (from part 3) × $15

5 25,200 lbs. (from part 3) × $15

CHAPTER 22 (FIN MAN); CHAPTER 8 (MAN) Budgeting

Prob. 22–4A (FIN MAN); Prob. 8–4A (MAN) (Concluded)

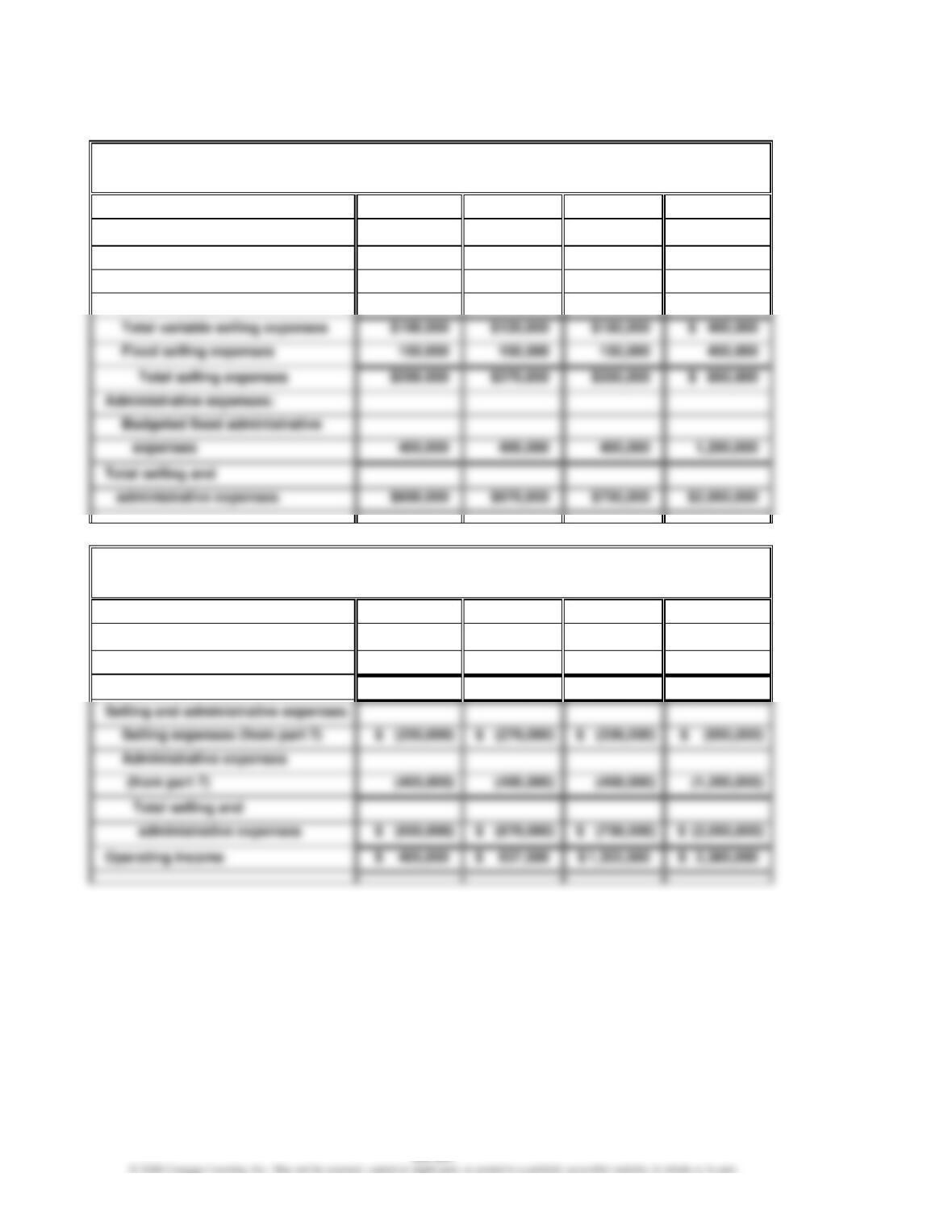

7.

Bellaire Inc.

Selling and Administrative Expenses Budget

For the First Quarter Ending March 31

January

February

March

First Quarter

Selling expenses:

Budgeted sales units

25,000

30,000

45,000

100,000

Variable selling expenses

Total variable selling expenses

Fixed selling expenses

450,000

Administrative expenses:

Budgeted fixed administrative

Total selling and

per unit sold

× $4.00

× $4.00

× $4.00

× $4.00

8.

Bellaire Inc.

Budgeted Income Statement

For the First Quarter Ending March 31

January

February

March

First Quarter

Sales (from part 1)

$ 3,125,000

$ 3,750,000

$ 5,625,000

$12,500,000

Cost of goods sold (from part 6)

(2,070,000)

(2,442,500)

(3,572,500)

(8,085,000)

Gross profit

$ 1,055,000

$ 1,307,500

$ 2,052,500

$ 4,415,000

Selling and administrative expenses:

Selling expenses (from part 7)

Administrative expenses

Operating income

CHAPTER 22 (FIN MAN); CHAPTER 8 (MAN) Budgeting

Prob. 22–5A (FIN MAN); Prob. 8–5A (MAN)

1.

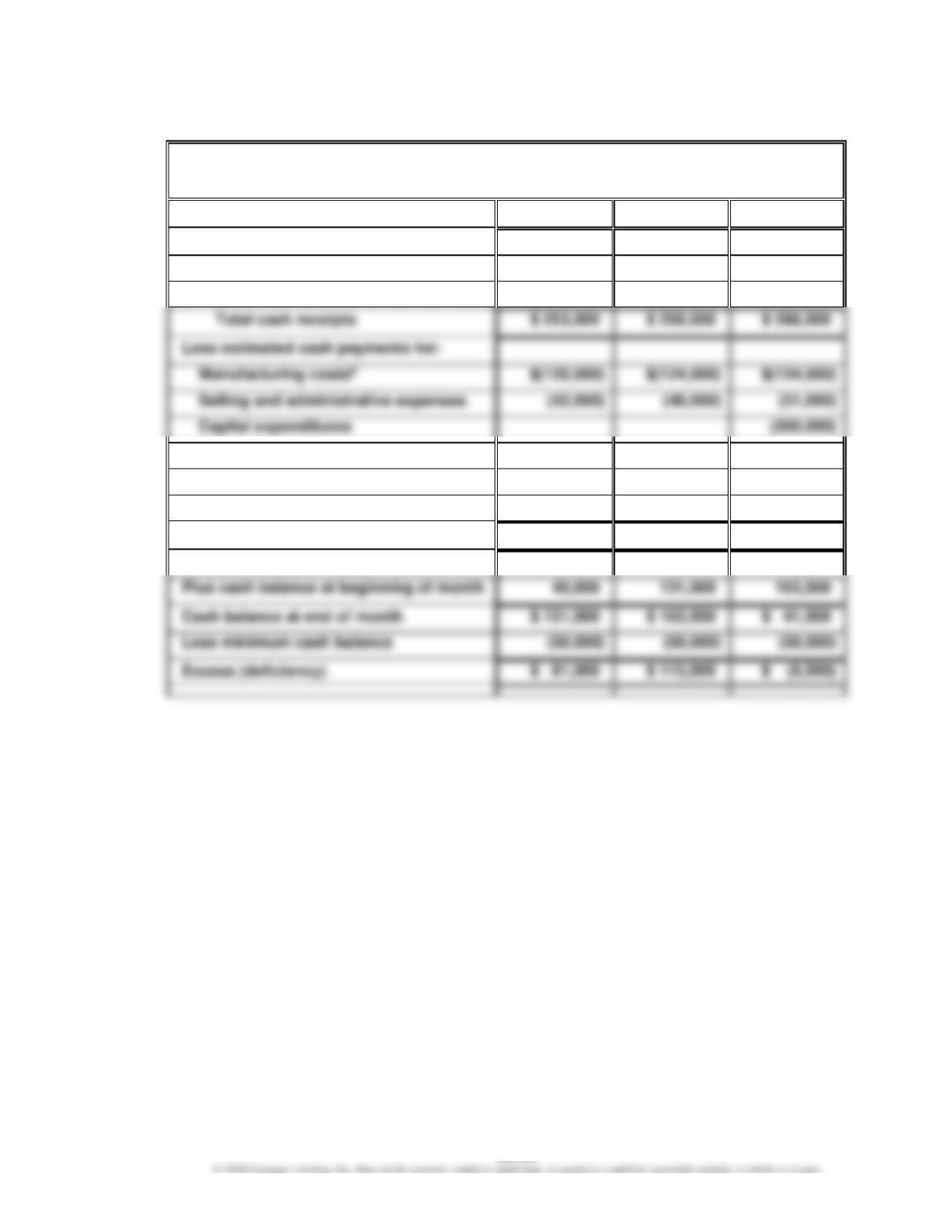

Bridgeport Housewares Inc.

Cash Budget

For the Three Months Ending November 30

September

October

November

Estimated cash receipts from:

Cash sales

$ 25,000

$ 30,000

$ 31,500

Collection of accounts receivablea

228,000

229,500

256,500

Total cash receipts

Selling and administrative expenses

(51,000)

Other purposes:

Income tax

(55,000)

Dividends

(25,000)

Total cash payments

$(162,000)

$(227,000)

$(410,000)

Cash increase (decrease)

$ 91,000

$ 32,500

$(122,000)

Cash balance at end of month

$ 41,500

CHAPTER 22 (FIN MAN); CHAPTER 8 (MAN) Budgeting

Prob. 22–5A (FIN MAN); Prob. 8–5A (MAN) (Concluded)

Computations:

a Collections of accounts receivable:

September

October

November

July sales …………………………………………………..

$ 60,0001

September sales …………………………………………

October sales …………………………………………….

1 $200,000 × 30% = $60,000

2 $240,000 × 70% = $168,000

b Payments for manufacturing costs:

September

October

November

Payment of accounts payable, beginning

of month balancec ……………………………………

$ 40,000

$ 20,000

$ 26,000

Payment of current month’s costd ……………….

80,000

104,000

108,000

Total ………………………………………………………..

$120,000

$124,000

$134,000

c Accounts payable, September 1 balance = $40,000

($150,000 – $50,000) × 20% = $20,000

($180,000 – $50,000) × 20% = $26,000

2. The budget indicates that the minimum cash balance will not be maintained in

November. This is due to the capital expenditures requiring significant cash

CHAPTER 22 (FIN MAN); CHAPTER 8 (MAN) Budgeting

Prob. 22–6A (FIN MAN); Prob. 8–6A (MAN)

1.

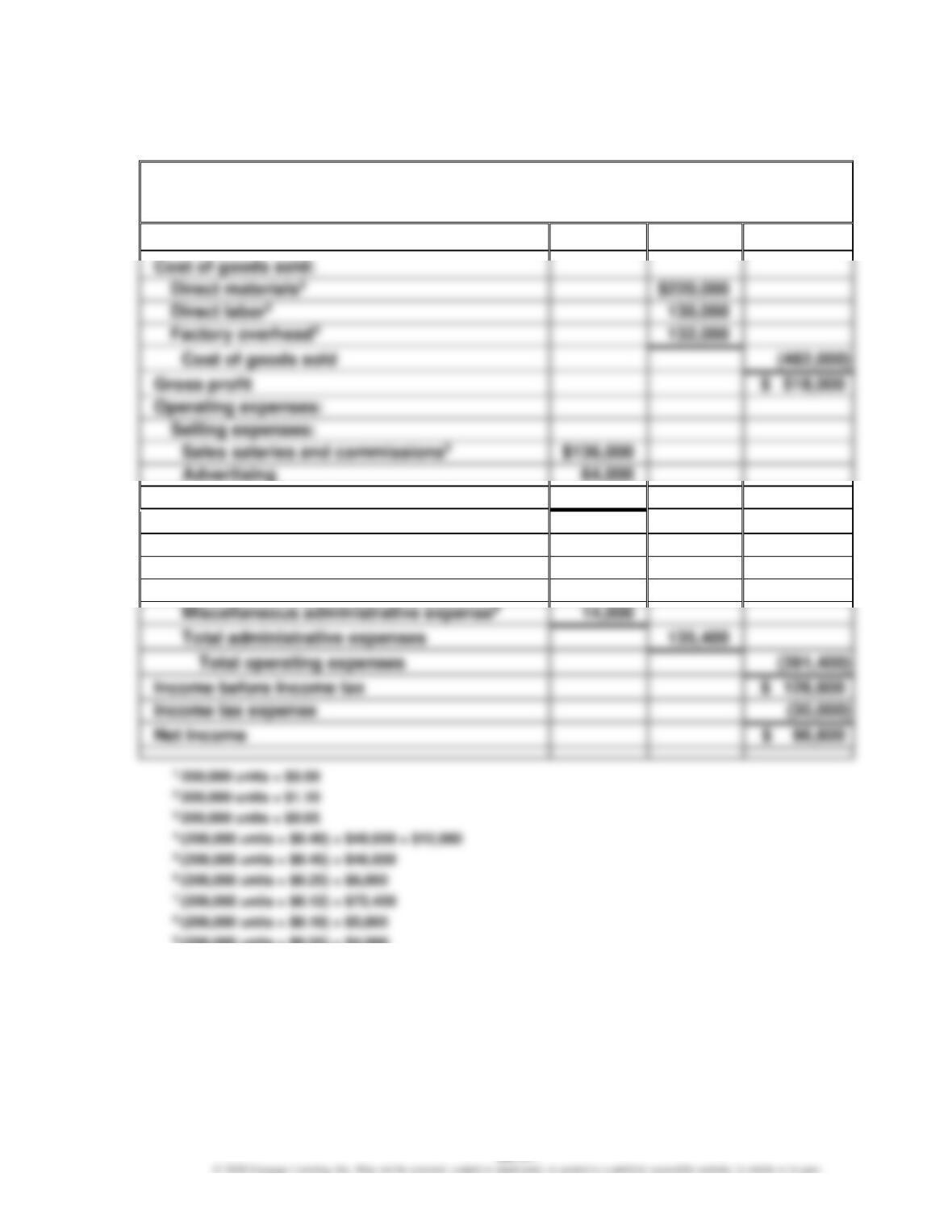

Regina Soap Co.

Budgeted Income Statement

For the Year Ending December 31, 20Y9

Sales1

$1,000,000

$220,000

Selling expenses:

Sales salaries and commissions5

64,000

Miscellaneous selling expenses6

56,000

Total selling expenses

$256,000

Administrative expenses:

Office and officers salaries7

$ 96,400

Supplies8

25,000

Miscellaneous administrative expense9

14,000

Total operating expenses

CHAPTER 22 (FIN MAN); CHAPTER 8 (MAN) Budgeting

Prob. 22–6A (FIN MAN); Prob. 8–6A (MAN) (Concluded)

2.

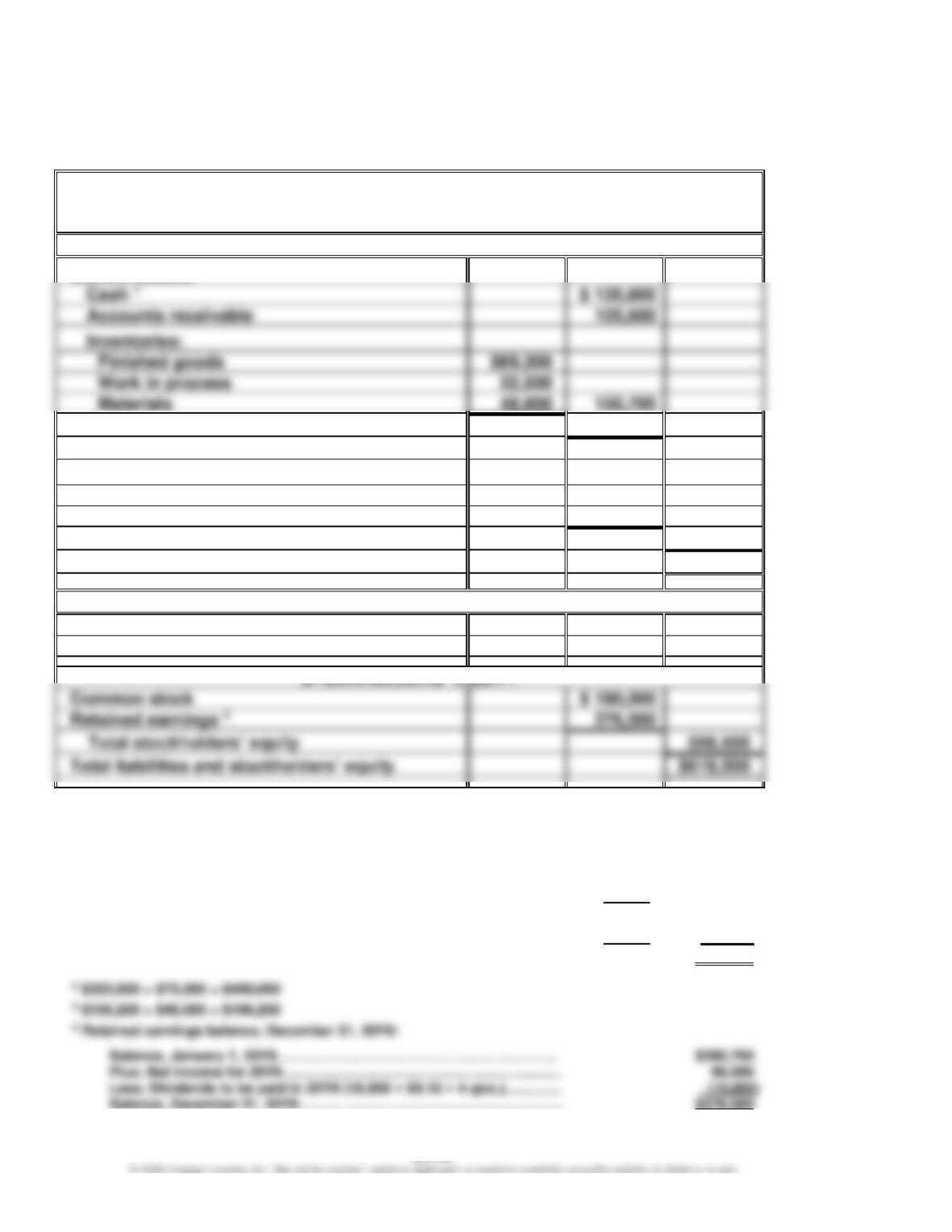

Regina Soap Co.

Budgeted Balance Sheet

December 31, 20Y9

ASSETS

Current assets:

Cash 1

$ 135,800

Accounts receivable

Work in process

Prepaid expenses

2,600

Total current assets

$414,700

Property, plant, and equipment:

Plant and equipment 2

$ 400,000

Accumulated depreciation 3

(196,200)

Total property, plant, and equipment

203,800

Total assets

$618,500

LIABILITIES

Current liabilities:

Accounts payable

$ 62,000

Common stock

$ 180,000

$618,500

1 Cash balance, December 31, 20Y9:

Balance, January 1, 20Y9 ………………………………………………………………….

$ 85,000

Add cash from operations:

Net income ………………………………………………………………………….

$96,600

Depreciation of plant and equipment …………………………………….

40,000

136,600

Less: Dividends to be paid in 20Y9 (18,000 × $0.15 × 4 qtrs.) ……………

$10,800

Plant and equipment to be acquired in 20Y9 ………………………….

75,000

(85,800)

Cash balance, December 31, 20Y9 …………………………………………………….

$135,800

CHAPTER 22 (FIN MAN); CHAPTER 8 (MAN) Budgeting

Prob. 22–1B (FIN MAN); Prob. 8–1B (MAN)

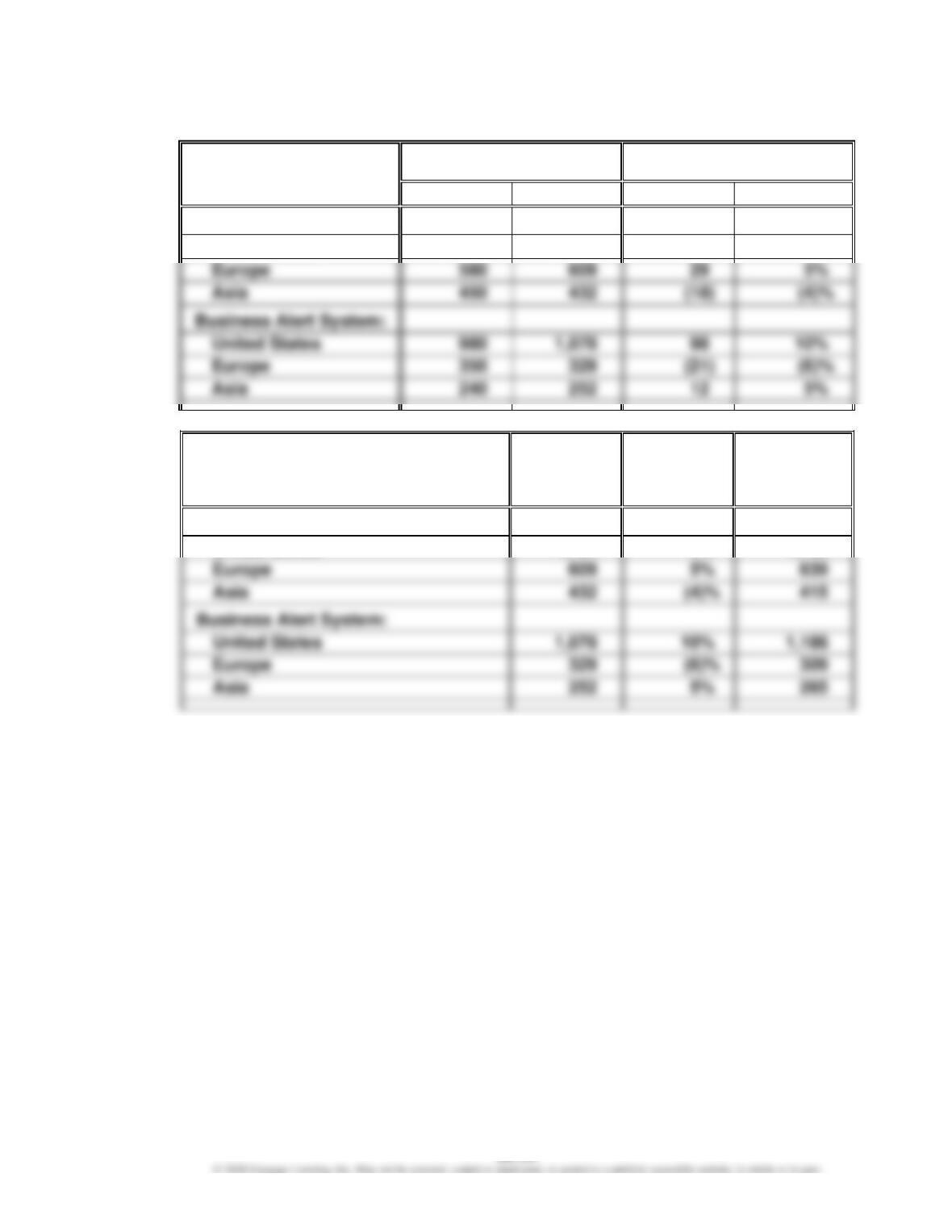

1.

Unit Sales, Year Ended 20Y8

Increase (Decrease)

Actual Over Budget

Budget

Actual Sales

Amount

Percent

Home Alert System:

United States

1,700

1,734

34

2%

29

Business Alert System:

United States

1,078

98

12

2.

20Y8

Actual

Units

Percentage

Increase

(Decrease)

20Y9

Budgeted

Units

(rounded)

Home Alert System:

5%

Business Alert System:

United States

1,078

1,186

5%

United States

1,734

2%

1,769

CHAPTER 22 (FIN MAN); CHAPTER 8 (MAN) Budgeting

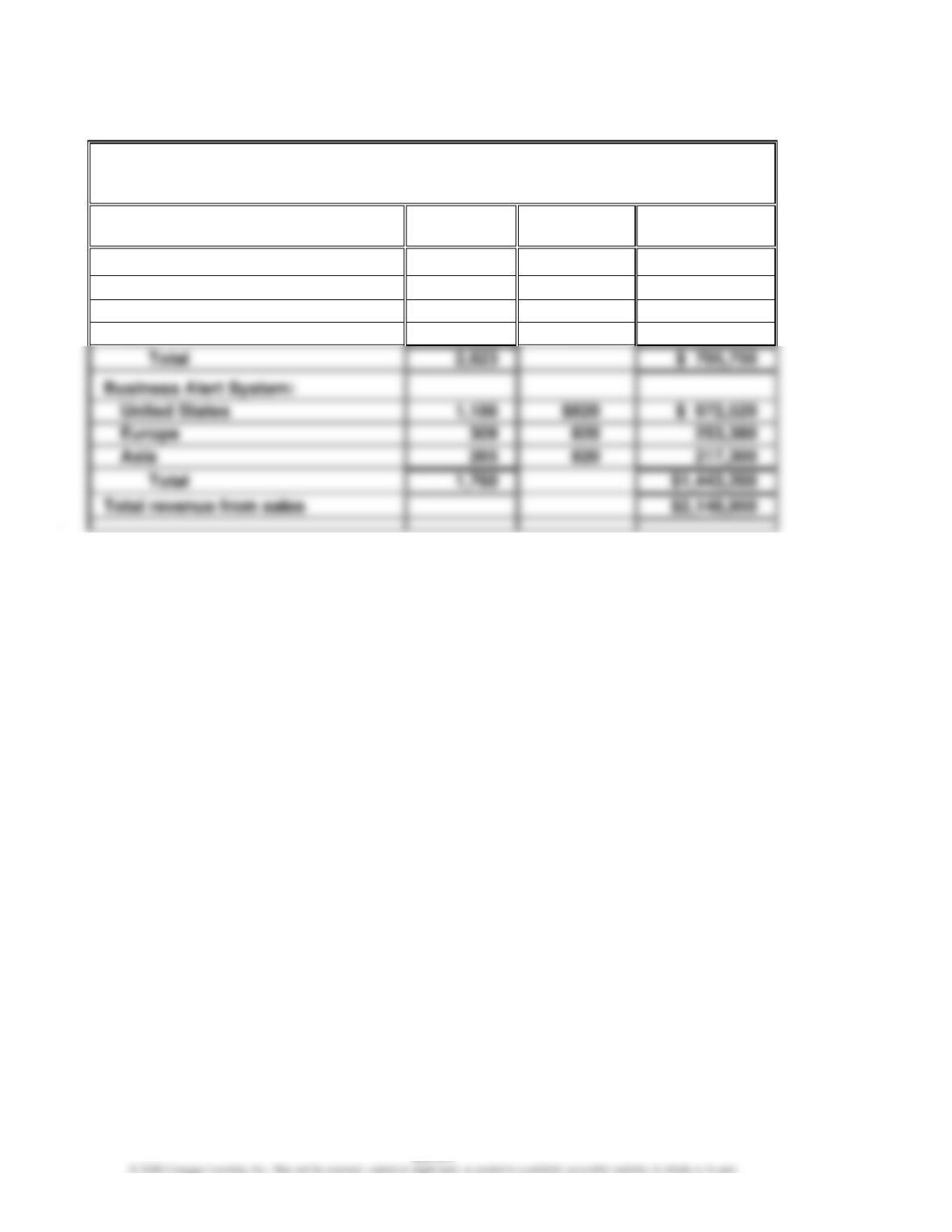

Prob. 22–1B (FIN MAN); Prob. 8–1B (MAN) (Concluded)

3.

Sentinel Systems Inc.

Sales Budget

For the Year Ending December 31, 20Y9

Product and Area

Unit Sales

Volume

Unit Selling

Price

Total Sales

Home Alert System:

United States

1,769

$250

$ 442,250

Europe

639

250

159,750

Asia

415

250

103,750

Business Alert System:

Europe

309

820

253,380

Asia

265

820

217,300

Total revenue from sales

CHAPTER 22 (FIN MAN); CHAPTER 8 (MAN) Budgeting

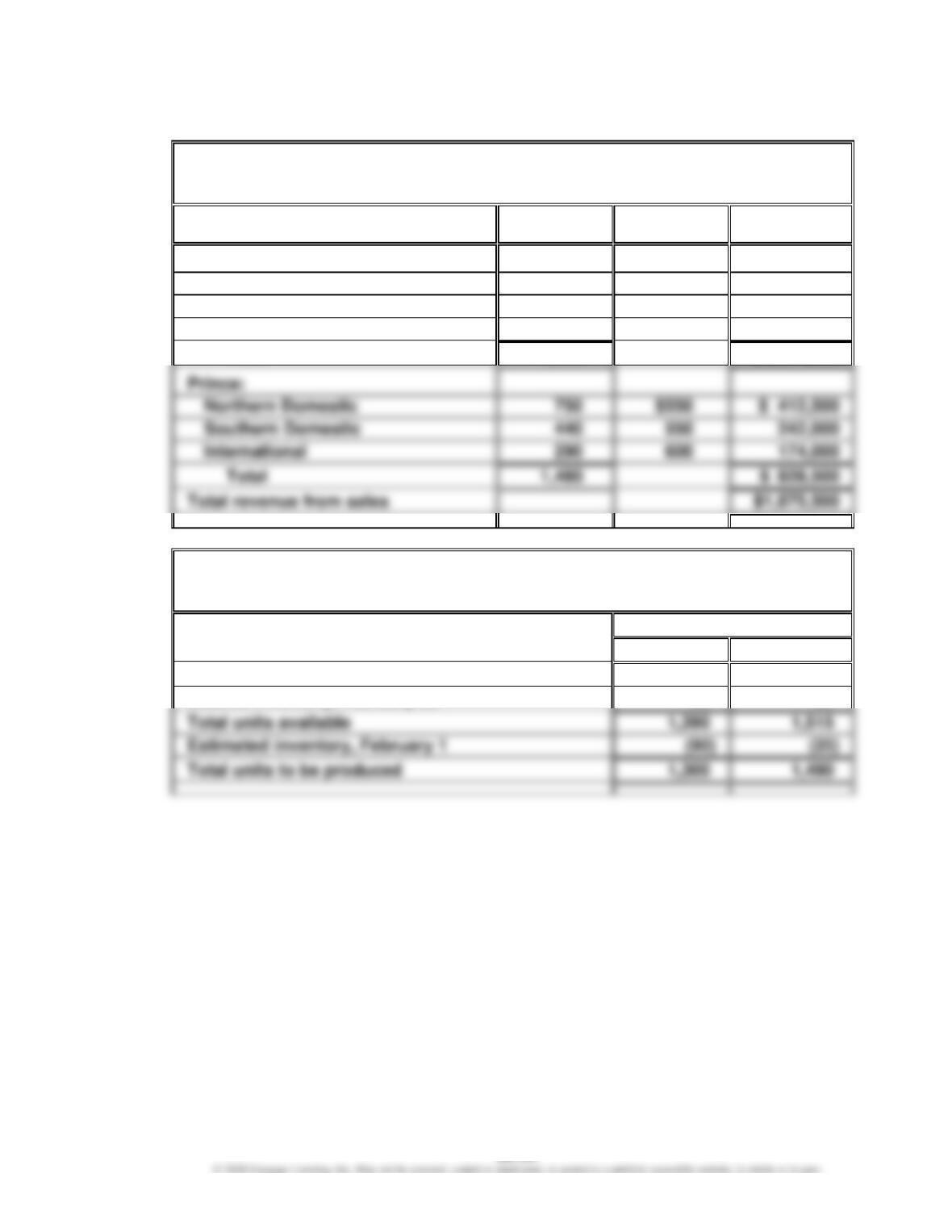

Prob. 22–2B (FIN MAN); Prob. 8–2B (MAN)

1.

Royal Furniture Company

Sales Budget

For the Month Ending February 28

Product and Area

Unit Sales

Volume

Unit Selling

Price

Total Sales

King:

Northern Domestic

610

$780

$ 475,800

Southern Domestic

340

780

265,200

International

360

850

306,000

Total

1,310

$1,047,000

Prince:

Northern Domestic

750

$550

$ 412,500

Southern Domestic

440

550

242,000

International

290

600

174,000

Total

1,480

Total revenue from sales

$1,875,500

2.

Royal Furniture Company

Production Budget

For the Month Ending February 28

Units

King

Prince

Expected units to be sold

1,310

1,480

Total units available

1,390

1,515

Total units to be produced

1,300

1,490

Desired inventory, February 28

80

35

CHAPTER 22 (FIN MAN); CHAPTER 8 (MAN) Budgeting

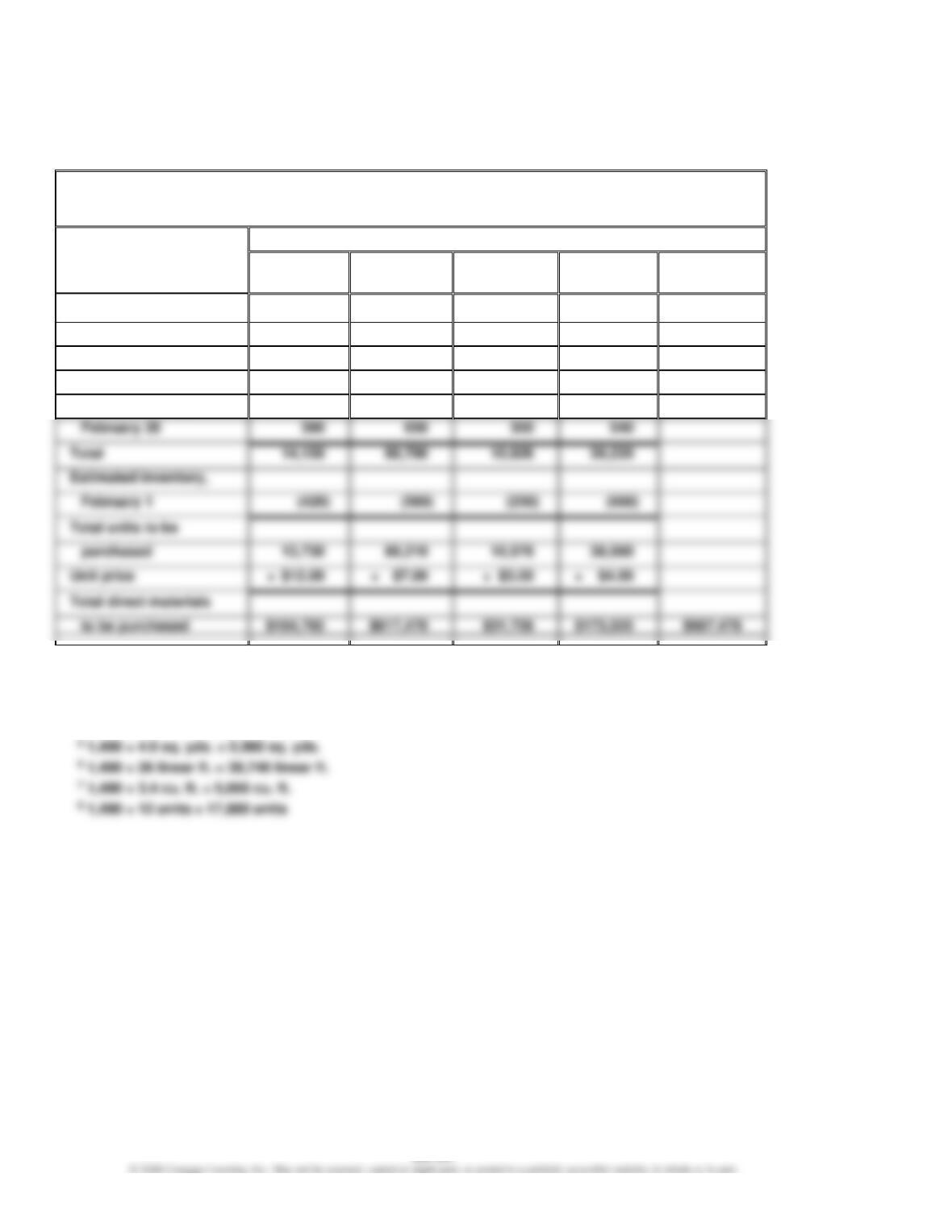

Prob. 22–2B (FIN MAN); Prob. 8–2B (MAN) (Continued)

3.

Royal Furniture Company

Direct Materials Purchases Budget

For the Month Ending February 28

Direct Materials

Fabric

(sq. yds.)

Wood

(linear ft.)

Filler

(cu. ft.)

Springs

(units)

Total

Required units for

production:

King

7,8001

49,4002

5,4603

20,8004

Prince

5,9605

38,7406

5,0667

17,8808

Desired inventory,

Estimated inventory,

Total units to be

Total direct materials

1 1,300 × 6.0 sq. yds. = 7,800 sq. yds.

2 1,300 × 38 linear ft. = 49,400 linear ft.

3 1,300 × 4.2 cu. ft. = 5,460 cu. ft.

4 1,300 × 16 units = 20,800 units

CHAPTER 22 (FIN MAN); CHAPTER 8 (MAN) Budgeting

Prob. 22–2B (FIN MAN); Prob. 8–2B (MAN) (Concluded)

4.

Royal Furniture Company

Direct Labor Cost Budget

For the Month Ending February 28

Framing

Department

Cutting

Department

Upholstery

Department

Total

Hours required for production:

King1

1,560

650

1,040

Prince2

1,490

596

3,050

1,934

2 This line is calculated as 1,490 Prince chairs from the production budget multiplied by

the hours per unit in each department estimated for the Prince chairs.

1,490 = 1,490 × 1.0; 596 = 1,490 × 0.4; 894 = 1,490 × 0.6

CHAPTER 22 (FIN MAN); CHAPTER 8 (MAN) Budgeting

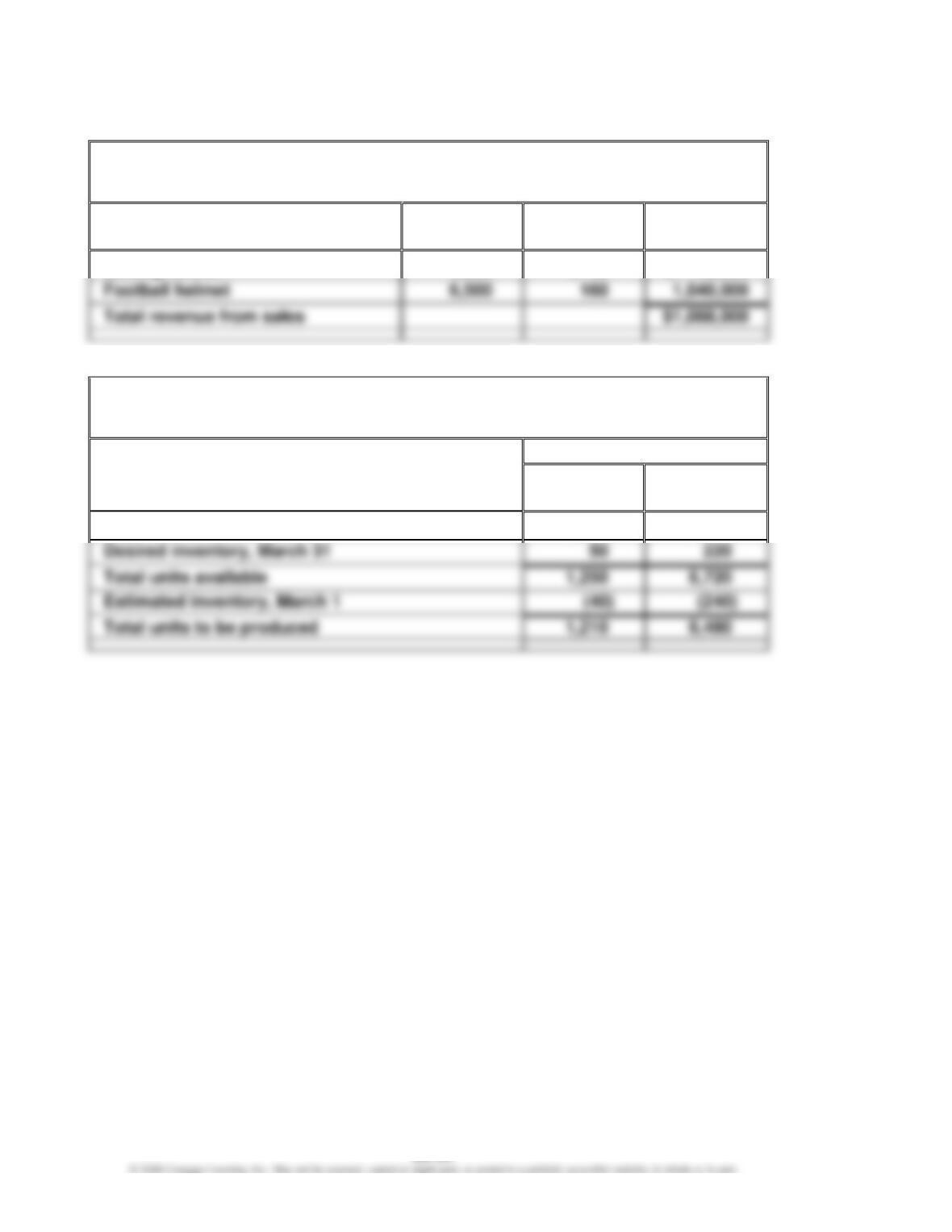

Prob. 22–3B (FIN MAN); Prob. 8–3B (MAN)

1.

Gold Medal Athletic Co.

Sales Budget

For the Month Ending March 31

Unit Sales

Volume

Unit Selling

Price

Total Sales

Batting helmet

1,200

$ 40

$ 48,000

2.

Gold Medal Athletic Co.

Production Budget

For the Month Ending March 31

Units

Batting

Helmet

Football

Helmet

Expected units to be sold

1,200

6,500

CHAPTER 22 (FIN MAN); CHAPTER 8 (MAN) Budgeting

Prob. 22–3B (FIN MAN); Prob. 8–3B (MAN) (Continued)

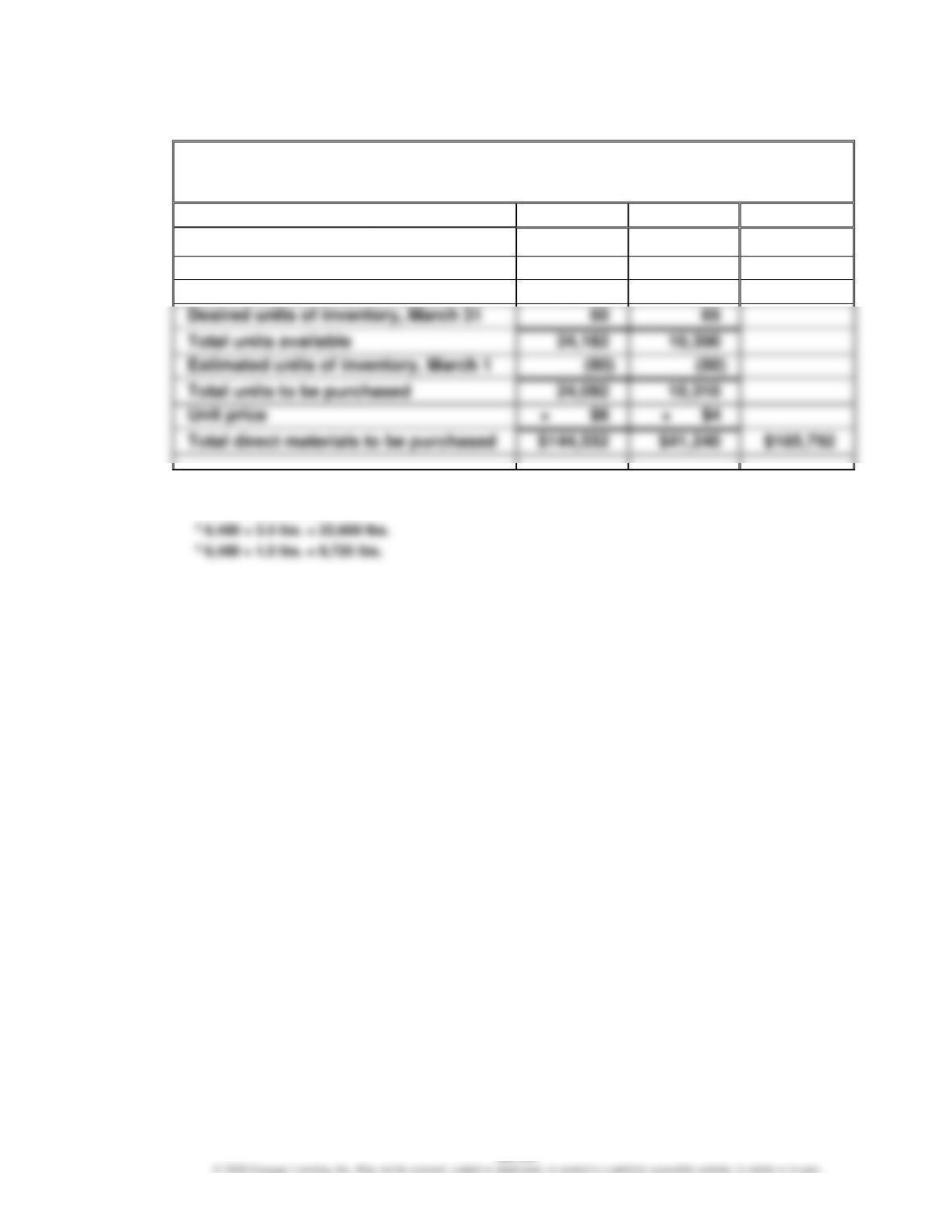

3.

Gold Medal Athletic Co.

Direct Materials Purchases Budget

For the Month Ending March 31

Plastic

Foam Lining

Total

Units required for production:

Batting helmet

1,4521

6052

Football helmet

22,6803

9,7204

1 1,210 × 1.2 lbs. = 1,452 lbs.

2 1,210 × 0.5 lb. = 605 lbs.