COMPREHENSIVE PROBLEM SOLUTION

(a) Jan. 1 Notes Receivable …………………………………….

Accounts Receivable—

1,200

3 Allowance for Doubtful Accounts……………..

730

8 Inventory …………………………………………………

Accounts Payable ……………………………..

17,200

17,200

15 Cash ……………………………………………………….

Service Charge Expense ………………………….

970

30

17 Cash ……………………………………………………….

Accounts Receivable ………………………..

22,900

22,900

27 Supplies ………………………………………………….

Cash …………………………………………………

1,400

1,400

COMPREHENSIVE PROBLEM SOLUTION (Continued)

Adjusting Entries

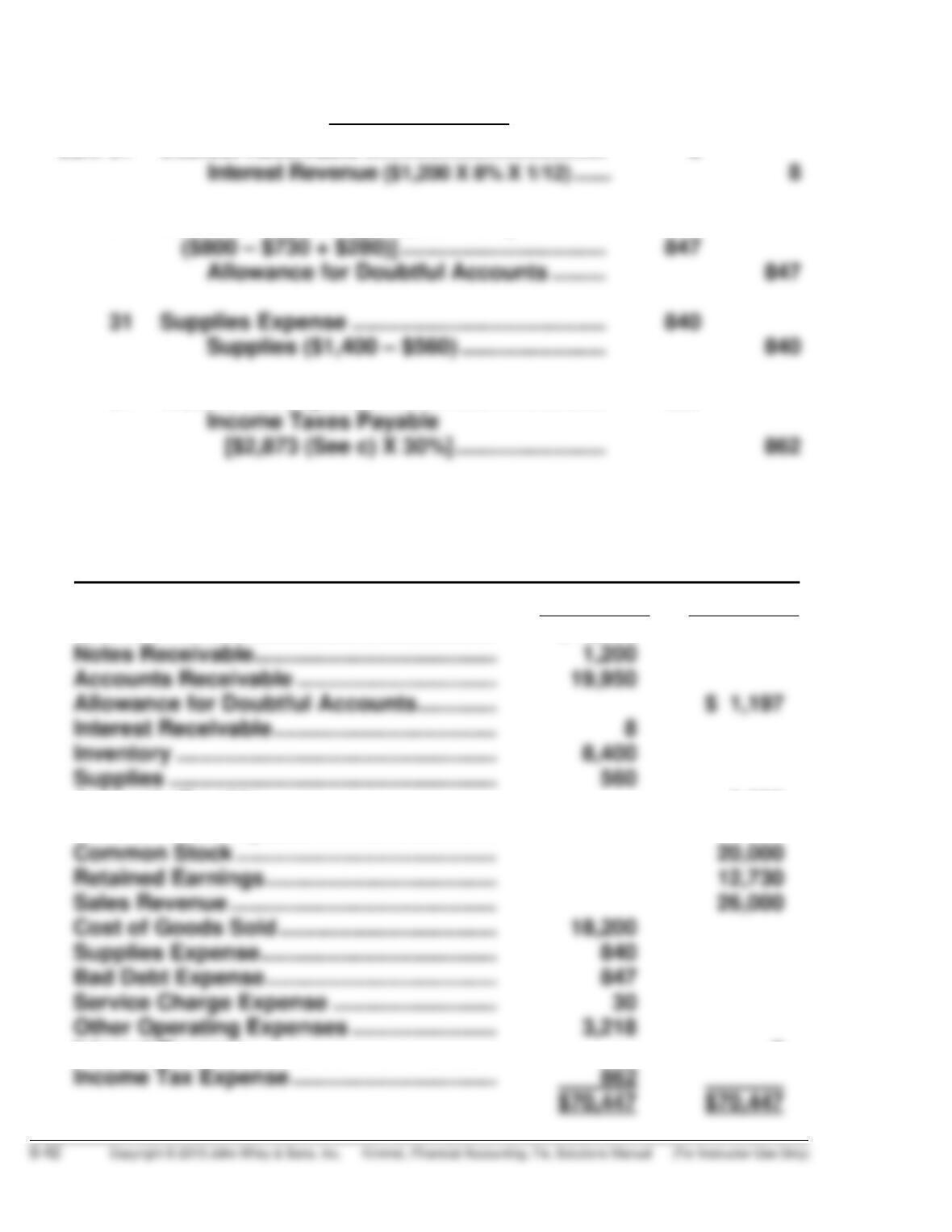

Jan. 31 Interest Receivable ………………………………….

8

31 Bad Debt Expense [($19,950 X 6%)

–

31 Income Tax Expense ………………………………..

862

(b) MADSON CORPORATION

Adjusted Trial Balance

January 31, 2014

Debit Credit

Cash ……………………………………………………. $16,332

Accounts Payable ……………………………….. 9,650

Income Taxes Payable …………………………. 862

Interest Revenue …………………………………. 8

COMPREHENSIVE PROBLEM SOLUTION (Continued)

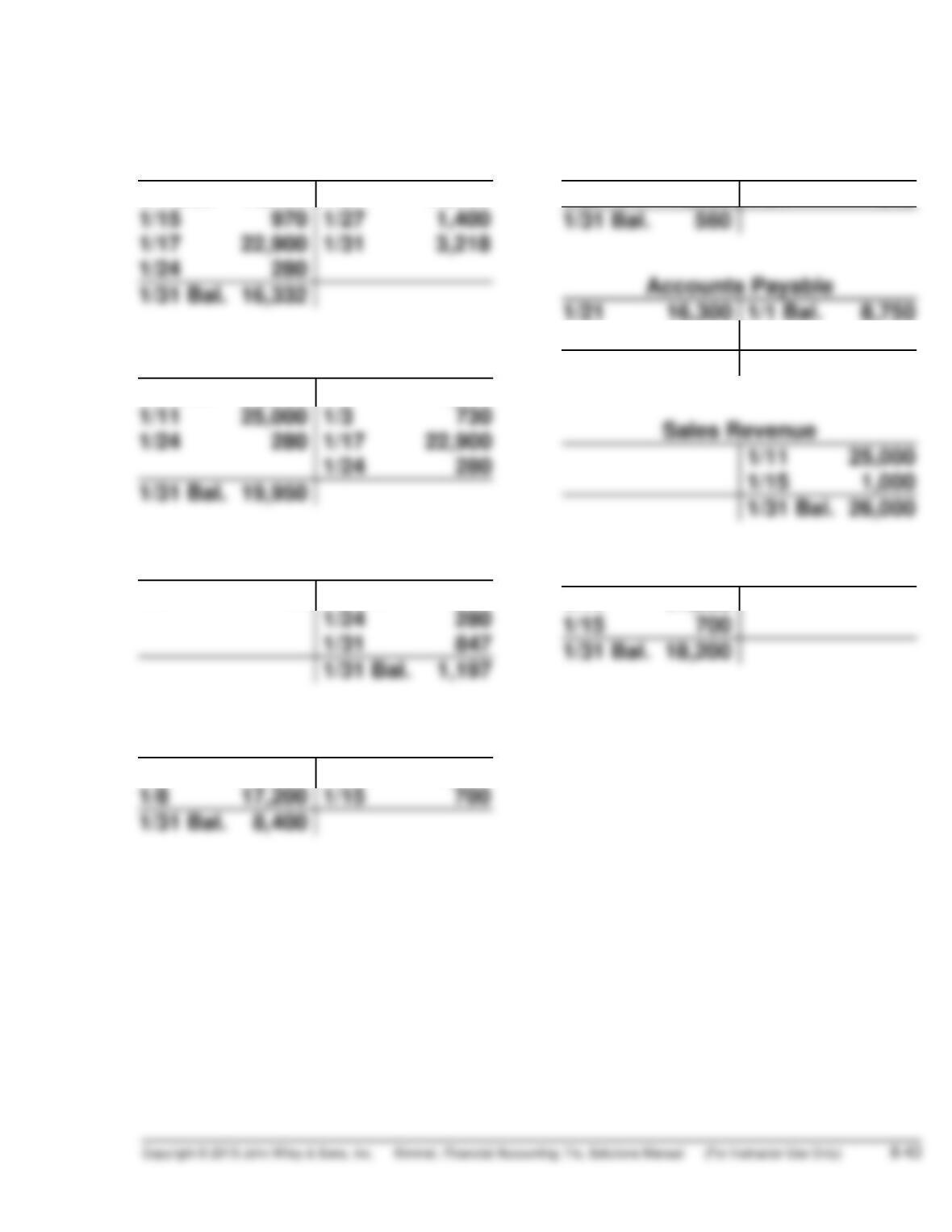

(b) Optional T accounts for accounts with multiple transactions

Cash

1/1 Bal. 13,100

1/21 16,300

Accounts Receivable

1/1 Bal. 19,780

1/1 1,200

Allowance for Doubtful Accounts

1/3 730 1/1 Bal. 800

Inventory

1/1 Bal. 9,400

1/11 17,500

Supplies

1/27 1,400 1/31 840

1/8 17,200

1/31 Bal. 9,650

Cost of Goods Sold

1/11 17,500

COMPREHENSIVE PROBLEM SOLUTION (Continued)

(c) MADSON CORPORATION

Income Statement

For the Month Ending January 31, 2014

Sales revenue ………………………………………….

.

$26,000

Cost of goods sold …………………………………..

.

18,200

Supplies expense ………………………………

.

840

Service charge expense …………………….

.

30

Total operating expenses …………………………

.

4,935

COMPREHENSIVE PROBLEM SOLUTION (Continued)

MADSON CORPORATION

Retained Earnings Statement

For the Month Ending January 31, 2014

Retained earnings, January 1 ……………………………………

.

$12,730

Add: Net income ………………………………………………………

.

2,011

Retained earnings, January 31 ………………………………….

.

$14,741

MADSON CORPORATION

Balance Sheet

January 31, 2014

Assets

Current assets

Cash …………………………………………………. $16,332

Notes receivable……………………………….. 1,200

Accounts receivable………………………….. $19,950

Less: Allowance for doubtful

accounts ………………………………… 1,197 18,753

Interest receivable…………………………….. 8

Inventory ………………………………………….. 8,400

Supplies …………………………………………… 560

Total assets …………………………………………….. $45,253

Liabilities and Stockholders’ Equity

Current liabilities

Accounts payable……………………………… $ 9,650

Income taxes payable ……………………….. 862

Total liabilities …………………………………………. $10,512

Stockholders’ equity

Common stock …………………………………. $20,000

Retained earnings …………………………….. 14,741

Total stockholders’ equity…………………. 34,741

Total liabilities and stockholders’ equity…… $45,253

BYP 8-1 FINANCIAL REPORTING PROBLEM

2011

(a) Accounts receivable

turnover =

$528,369

($41,895 + $37,394) 2÷

= $528,369 = 13.3

$39,644.5 times

Average collection period = 365 = 27.4 days

13.3

(b) Note 1 states that revenue from a major customer exceeded 20% of net

product sales in recent years. Note 9 reports significant foreign sales,

primarily Mexico and Canada. Material sales to a single customer could

create potential credit risk problems.

(c) At 27.4 days, Tootsie Roll’s average collection period appears

reasonable. It should be compared to its credit terms (normally 30 days)

and to previous years to determine whether it is of concern.

BYP 8-2 COMPARATIVE ANALYSIS PROBLEM

(a) (1) Accounts receivable turnover ratio

Tootsie Roll Hershey Company

$528,369

($41,895 + $37,394) 2÷

$6,080,788

($399,499 + $390,061) 2÷

$528,369 = 13.3 times

$39,644.5 $6,080,788 = 15.4 times

$394,780

(2) Average collection period

365 = 27.4 days

13.3 365 = 23.7 days

15.4

(b) The general rule for the average collection period is that it should not

greatly exceed the credit term period. Tootsie Roll’s average collection

period (approximately 27 days) is shorter than the normal credit term

period of 30 days but is worse than Hershey Company’s 24 day average

collection period.

BYP 8-3 RESEARCH CASE

(a) InBev told its suppliers that it would take up to 120 days to pay. This is

compared to 30 days previously.

(b) To free up cash, General Electric shortened collection times, collected on

past-due accounts, and stretched out its payments to suppliers. By doing

this the company says that it freed up $3.8 billion.

(c) Companies with sales of more than $5 billion took an average of

55.8 days to pay suppliers and they took an average of 41 days to

collect from customers. Companies with sales of less than $500 million

took an average of 40.1 days to pay suppliers and they took an average

of 58.9 days to collect from customers.

(d) If a company negotiates payment terms that are too severe for its

suppliers, the suppliers may be forced out of business. This can then

disrupt the company’s operations as it searches for substitute suppliers.

BYP 8-4 INTERPRETING FINANCIAL STATEMENTS

(a) Accounts receivable

turnover = $2,981.8

($259.8* +$248.3**)/2 =11.7 times

*$270.4

–

$10.6

**$259.7

–

$11.4

Average collection period= 365 days

11.7 = 31.2 days

(b) Accounts receivable represent 24.9% [($270.4 – $10.6)/$1,044.9] of the

company’s current assets. This is a material amount of the current

assets.

(c) The ratios would probably vary throughout the year as receivables

increase during the busy season and decrease in the “off” season. To

improve the accuracy of the ratio, average receivables should be calcu-

lated using monthly or quarterly data, rather than just the beginning

and ending balance.

(d) It is difficult to evaluate Scotts’ credit risk with only a single year’s data

and no industry norms. An average collection period of 31.2 days may be

reasonable for the type of customers that make up Scotts’ receivables.

Scotts explained that a majority of its receivables were from its North

American Consumer segment. Within this segment, there were several

subgroups (i.e., home centers, mass merchandisers, hardware stores).

The note explains that its top 3 customers accounted for 48% of its total

receivables from the North American consumer business. In addition its

two largest customers accounted for more than 34% of its net sales.

These facts indicate a higher degree of credit risk than having numerous

smaller customers.

BYP 8-4 (Continued)

(e) Note 19 addressed the issues that surround credit risk. It provided the

reader with at least a moderate degree of “comfort” that Scotts’

accounts receivable and allowance policies were acceptable. The note

also appears to comply with the full disclosure principle required

under GAAP. It does not, however, disclose what the company’s

credit exposure is to any individual customers. This would be of

interest, since some of its customers are probably very large. As noted in

part (d), having the receivables balance spread across multiple

customers is usually less risky than having a few large customers.

BYP 8-5 REAL-WORLD FOCUS

(a) Factoring invoices enhances cash flow and allows a company to meet

business expenses and take on new opportunities. The benefits of

factoring include:

• Predictable cash flow and elimination of slow payments

• Flexible financing, as factoring line is tied to sales. It’s the ideal

tool for growth

• Factoring is easy to obtain. Works well with startups and estab-

lished companies

• Factoring financing lines can be setup in a few days

(b) Factoring rates range between 1.5% and 3.5% per month. The two major

variables considered when determining the rate are: (1) the size of the

transaction, and (2) the credit quality of the company’s clients .

(c) The first installment is paid within a couple of days and is typically

90% of the invoice amount. After customers pay the invoice amount

to the factor, the second installment (10%) is paid, less a fee for the

transaction.

BYP 8-6 DECISION MAKING ACROSS THE ORGANIZATION

(a)

2014 2013 2012

Net credit sales ……………………………. $500,000 $600,000 $400,000

Credit and collection expenses

Collection agency fees ………….. $ 2,900 $ 2,600 $ 1,600

Salary of accounts receivable

clerk……………………………….. 4,400 4,400 4,400

Uncollectible accounts …………. 8,000 9,600 6,400

Billing and mailing costs ………. 2,500 3,000 2,000

Credit investigation fees ……….. 1,000 1,200 800

Total ………………………………. $ 18,800 $ 20,800 $ 15,200

Total expenses as a percentage

of net credit sales …………………. 3.8% 3.5% 3.8%

(b) Average accounts receivable (5%) … $ 25,000 $ 30,000 $ 20,000

Investment earnings (10%) ………….. $ 2,500 $ 3,000 $ 2,000

Total credit and collection expense

per above …………………………….. $ 18,800 $ 20,800 $ 15,200

Add: Investment earnings* …………. 2,500 3,000 2,000

Net credit and collection expense …. $ 21,300 $ 23,800 $ 17,200

Net expenses as a percentage

of net sales ………………………….. 4.3% 4.0% 4.3%

*The investment earnings on the cash tied up in accounts receivables

is an additional expense of continuing the existing credit policies.

(c) The analysis shows that the credit card fee of 4% of net credit sales will

be higher than the percentage cost of credit and collection expenses in

each year before considering the effect of earnings from other invest-

ment opportunities. However, after considering investment earnings,

the credit card fee of 4% will be less than or equal to the company’s per-

centage cost.

BYP 8-6 (Continued)

Finally, the decision hinges on (1) the accuracy of investment earnings,

(2) the expected trend in credit sales, and (3) the effect the new policy

will have on sales. Nonfinancial factors include the effects on customer

relationships of the alternative credit policies and whether the Falcons

want to continue with the handling of their own accounts receivable.

BYP 8-7 COMMUNICATION ACTIVITY

To: John Doe, President

From: Mary Jane, Student

Re: Improving debt-paying ability

Date: September 14, 2014

The first step that should be taken to improve your company’s debt-paying

ability is to accelerate collections of your accounts receivable. The current

credit policy (i.e., “pay when they can”) encourages slow payment from credit

customers. Most companies have a 30-day credit period with finance charges

applied on late payments. You may also want to consider adopting a discount

period which allows customers a reduction in the amount owed if payment

is made within a specified time period.

Measuring success in improving collections can be done by monitoring

collections and evaluating the receivables balance. Monitoring collections

is done by preparing an accounts receivable aging schedule on a monthly

basis. Evaluating receivables is accomplished by computing an accounts

receivable turnover and an average collection period.

Another step that can be taken with receivables to ease your company’s

liquidity problems is to sell the receivables to another company for cash.

Selling receivables to another company (called a factor) shortens the cash-

to-cash operating cycle. It should be pointed out that factors normally

charge a commission of 1% to 3%.

Hopefully this memo addresses the questions you have on improving your

company’s debt-paying ability. Please contact me if you have any questions

or need additional information.

BYP 8-8 ETHICS CASE

(a) The stakeholders in this situation are:

The president of Ortiz Corp.

The controller of Ortiz Corp.

The stockholders of Ortiz Corp.

(b) Yes. The controller is posed with an ethical dilemma—should he/she

follow the president’s “suggestion” and prepare misleading financial

statements (understated net income) or should he/she attempt to stand

up to and possibly anger the president by preparing a fair (realistic)

income statement.

(c) No. Ortiz Corp.’s growth rate should be a product of fair and accurate

financial statements, not vice versa. That is, one should not prepare

financial statements with the objective of achieving or sustaining a

predetermined growth rate. The growth rate should be a product of

management and operating results, not of creative accounting.

BYP 8-9 ALL ABOUT YOU

(a) There are a number of sources that compare features of credit cards. Here

are three: www.creditcards.com/, www.federalreserve.gov/pubs/shop/,

and www.creditorweb.com/.

(b) Here are some of the features you should consider: annual percentage

rate, credit limit, annual fees, billing and due dates, minimum payment,

penalties and fees, premiums received (airlines miles, hotel discounts etc.),

and cash rebates.

(c) Answer depends on present credit card and student’s personal situation.

BYP 8-10 FASB CODIFICATION ACTIVITY

(a) Receivables represent contractual rights to receive money on fixed or

determinable dates, whether or not there is any stated provision for

(b) The conditions under which receivables exist usually involve some

degree of uncertainty about their collectibility, in which case a contin-

gency exists.

Subtopic 450-20 requires recognition of a loss when both of the

following conditions are met:

a. Information available prior to issuance of the financial statements

b. The amount of the loss can be reasonably estimated.

IFRS8-1 IFRS CONCEPTS AND APPLICATION

FASB and IASB have both worked toward reporting financial instruments at

fair value. Both require disclosure of fair value information in notes to

financial statements and both permit (but do not require) companies to

record some types of financial instruments at fair value.

IFRS8-2 INTERNATIONAL FINANCIAL REPORTING PROBLEM

(a) Zetar indicated that a later Easter contributed to a £5.9m increase in

receivables due from customers compared to the previous year.

(b) Note 3.14 states that loans and receivables are non-derivative financial

(d) Note 18 indicates that the provision for impairment of receivables was

£65 or 0.3% of trade receivables for 2011. In 2010, the provision was