PROBLEM 8-2A (Continued)

(d)

$2,500,000 – $50,000

($563,000* + $763,000**) ÷2=$2,450,000

$663,000 =3.7 times

PROBLEM 8-3A

(a) Dec. 31 Bad Debt Expense ……………………………….. 34,400

Allowance for Doubtful Accounts

($42,400 – $8,000) ……………………….. 34,400

(a) & (b)

Bad Debt Expense Allowance for Doubtful Accounts

12/31 34,400 2013 12/31 Bal. 8,000

(b) 2014

(1) Mar. 1 Allowance for Doubtful Accounts ……. 600

Accounts Receivable ……………….. 600

(2) May 1 Accounts Receivable ………………………. 600

Allowance for Doubtful

PROBLEM 8-4A

(a) $37,000.

(b) $30,600 [($840,000 X 4%) – $3,000].

PROBLEM 8-5A

(a) Dec. 31 Bad Debt Expense ($10,200 – $1,500) …… 8,700

Allowance for Doubtful Accounts …… 8,700

(b) Dec. 31 Bad Debt Expense ($10,200 + $1,500) …… 11,700

Allowance for Doubtful Accounts …… 11,700

PROBLEM 8-6A

Jan. 5 Accounts Receivable—Ross Company ……… 4,000

Sales Revenue ……………………………………. 4,000

Feb. 2 Notes Receivable ……………………………………… 4,000

Accounts Receivable—Ross Company .. 4,000

Apr. 5 Notes Receivable. …………………………………….. 5,200

Accounts Receivable—Meachum Co …… 5,200

12 Cash ($12,000 + $200) ……………………………….. 12,200

Notes Receivable ……………………………….. 12,000

Interest Revenue

($12,000 X 10% X 2/12) ……………………… 200

June 2 Cash ($4,000 + $120) …………………………………. 4,120

PROBLEM 8-7A

Transaction

Current

Ratio

(2:1)

A

ccounts

Receivable

Turnover

(10X)

Average

Collection

Period

(36.5 days)

1. Recorded cash sale. I NE NE

2. Recorded bad debts

PROBLEM 8-8A

(a) July 5 Accounts Receivable ………………………….. 4,500

Sales Revenue ………………………………. 4,500

14 Cash ($600 – $18) ……………………………….. 582

Service Charge Expense ($600 X 3%) ….. 18

Sales Revenue ………………………………. 600

20 Cash …………………………………………………. 6,120

Notes Receivable …………………………… 6,000

31 Interest Receivable ……………………………. 50

Interest Revenue

($10,000 X 6% X 1/12) ………………….. 50

(b)

Notes Receivable Interest Receivable

Accounts Receivable

PROBLEM 8-8A (Continued)

KOLTON COMPANY

Balance Sheet (Partial)

July 31, 201X

(c) Current assets

Notes receivable ………………………………………… $10,000

PROBLEM 8-9A

Nike Adidas

Accounts receivable

a2,873.7 – 78.4

Average collection period 365

SOLUTIONS TO PROBLEMS—SET B

PROBLEM 8-1B

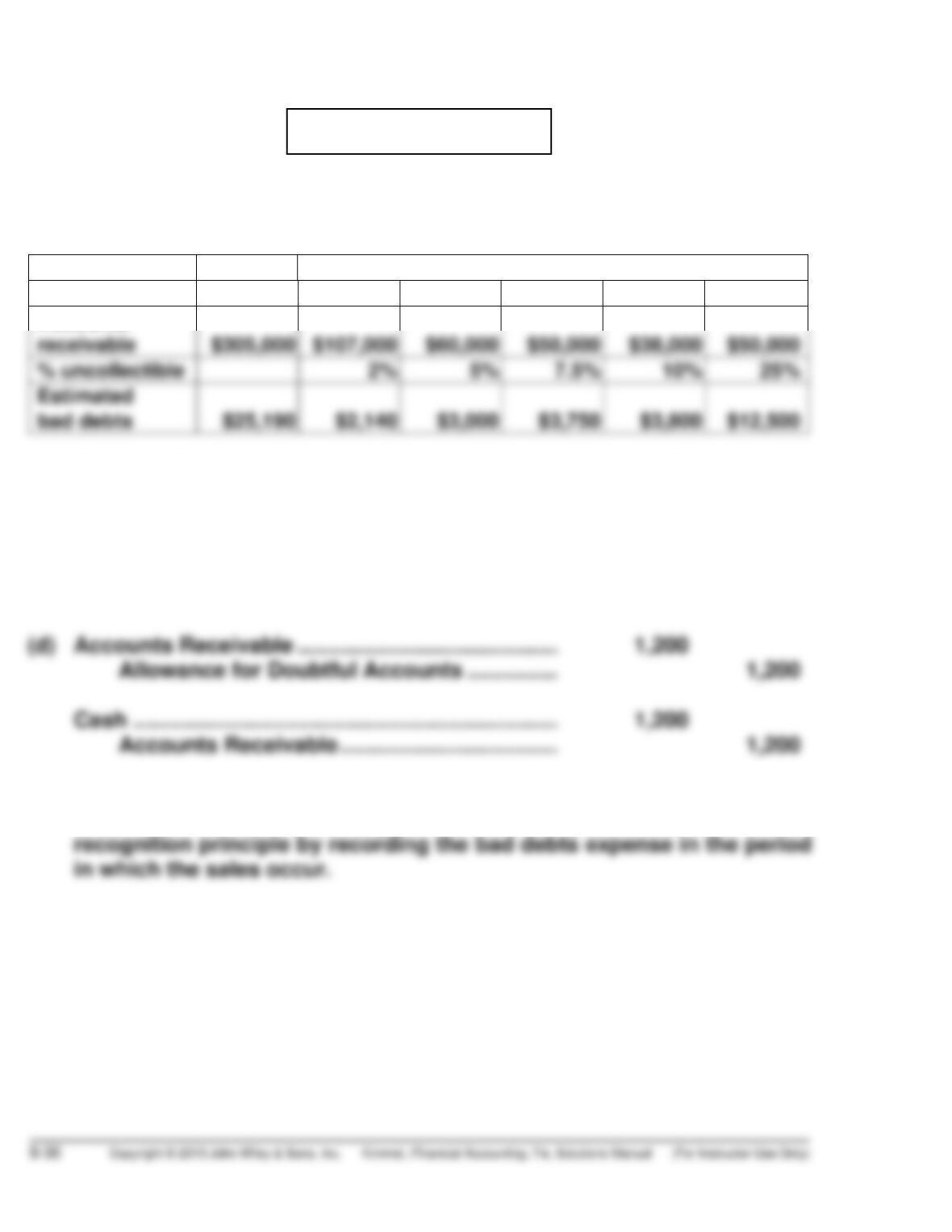

(a) Total estimated bad debts

Number of Days Outstanding

Total 0–30 31–60 61–90 91–120 Over 120

Accounts

(b) Bad Debt Expense ………………………………………… 18,190

Allowance for Doubtful Accounts

[$25,190 – $7,000] ………………………………… 18,190

(c) Allowance for Doubtful Accounts ………………….. 2,600

Accounts Receivable ……………………………… 2,600

(e) When an allowance account is used, an adjusting journal entry is made

at the end of each accounting period. This entry satisfies the expense

PROBLEM 8-2B

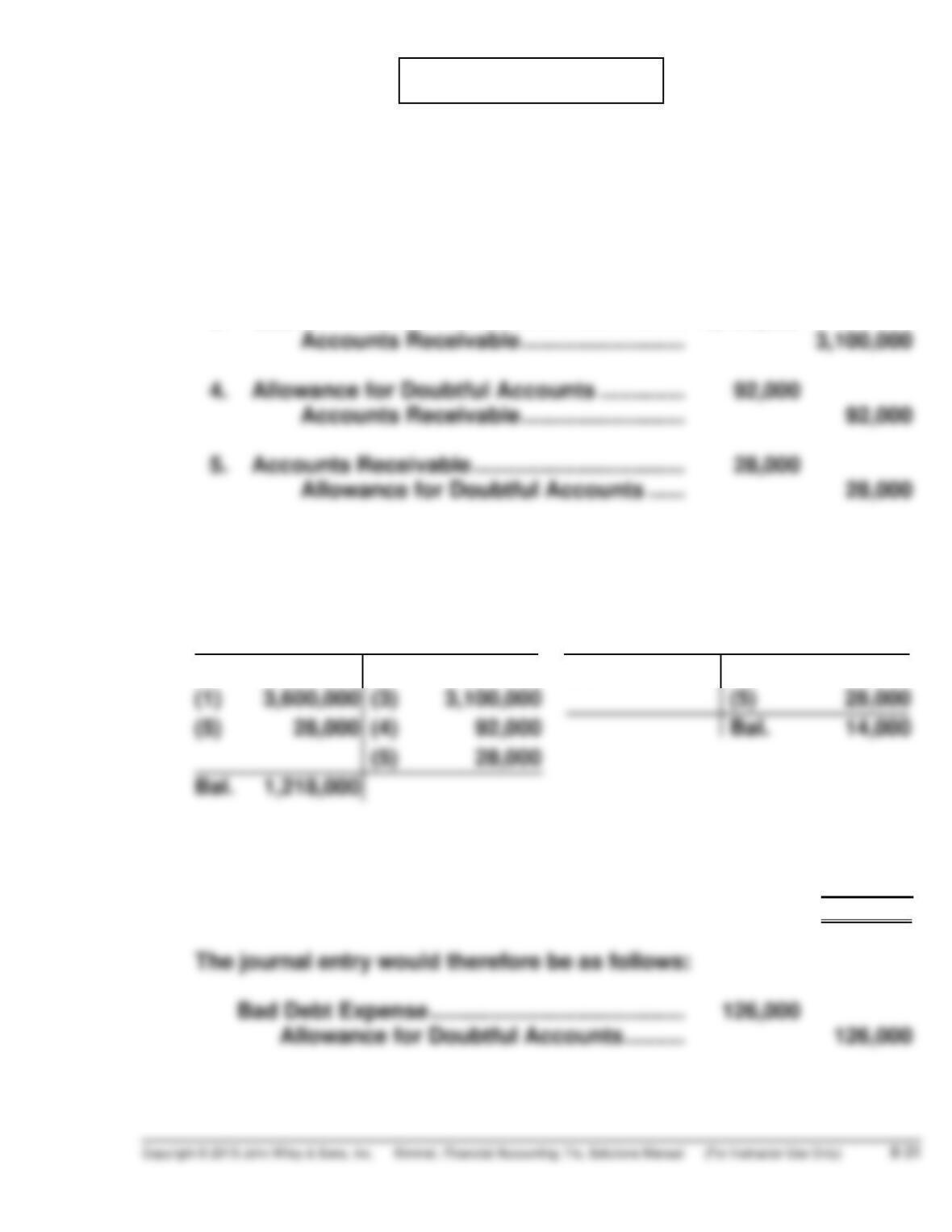

(a) 1. Accounts Receivable ……………………………. 3,600,000

Sales Revenue ……………………………….. 3,600,000

2. Sales Returns and Allowances ………………. 150,000

Accounts Receivable ……………………… 150,000

3. Cash …………………………………………………….. 3,100,000

Cash …………………………………………………….. 28,000

Accounts Receivable ……………………… 28,000

(b) Accounts Receivable Allowance for Doubtful Accounts

Bal. 960,000 (2) 150,000 (4) 92,000 Bal. 78,000

(c) Balance needed …………………………………………….. $140,000

Balance before adjustment [see (b)] ………………. (14,000)

Adjustment required ……………………………………… $126,000

PROBLEM 8-2B (Continued)

(d)

$3,600,000 – $150,000

($882,000* + $1,078,000**) ÷2=$3,450, 000

$980,000 =3.5 times

*$960,000 – $78,000

PROBLEM 8-3B

(a) Dec. 31 Bad Debt Expense …………………………….. 24,480

Allowance for Doubtful Accounts

(a) & (b)

Bad Debt Expense Allowance for Doubtful Accounts

12/31 24,480 2013 12/31 Bal. 9,000

(b) 2014

(1) Feb. 1 Allowance for Doubtful Accounts …… 900

Accounts Receivable ……………… 900

(2) July 1 Accounts Receivable …………………….. 900

Allowance for Doubtful

PROBLEM 8-4B

(a) $15,000.

(b) $16,300 [($500,000 X 4%) – $3,700].

PROBLEM 8-5B

(a) Dec. 31 Bad Debt Expense ($7,600 – $2,800) ……. 4,800

(b) Dec. 31 Bad Debt Expense ($7,600 + $2,500) ……. 10,100

Allowance for Doubtful

Accounts ……………………………….. 10,100

(c) Allowance for Doubtful Accounts ………………………. 750

(e) The advantages of the allowance method over the direct write-off

method are:

(1) It attempts to match bad debt expense related to uncollectible

PROBLEM 8-6B

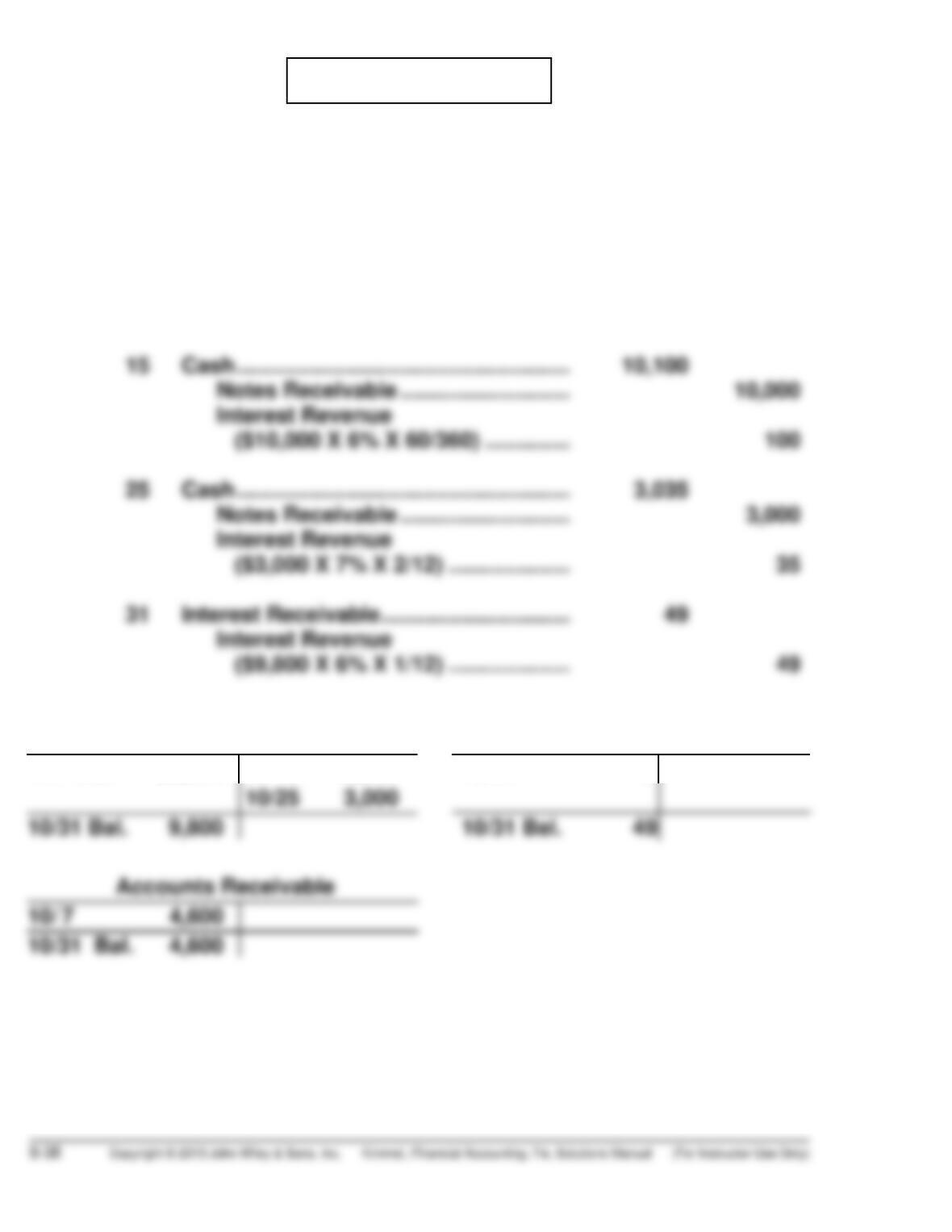

Jan. 5 Accounts Receivable—Flynn Company ……… 10,000

Sales Revenue ……………………………………. 10,000

20 Notes Receivable ………………………………………. 10,000

Accounts Receivable—

30 Cash ($12,000 + $360) ……………………………….. 12,360

Notes Receivable ………………………………… 12,000

Interest Revenue

($12,000 X 9% X 4/12) ……………………….. 360

PROBLEM 8-7B

Transaction

Current

Ratio

(2:1)

Accounts

Receivable

Turnover

(10X)

Average Col-

lection Period

(36.5 days)

1. Recorded sales on account. I D I

PROBLEM 8-8B

(a) Oct. 7 Accounts Receivable ……………………… 4,600

Sales Revenue ………………………….. 4,600

12 Cash ($600 – $18) …………………………… 582

Service Charge Expense

($600 X 3%) ………………………………….. 18

Sales Revenue ………………………….. 600

(b)

Notes Receivable Interest Receivable

10/1 Bal. 22,800 10/15 10,000 10/31 49

PROBLEM 8-8B (Continued)

DURHAN COMPANY

Balance Sheet (Partial)

October 31, 2014

(c) Current assets

Notes receivable ……………………………………………… $ 9,800

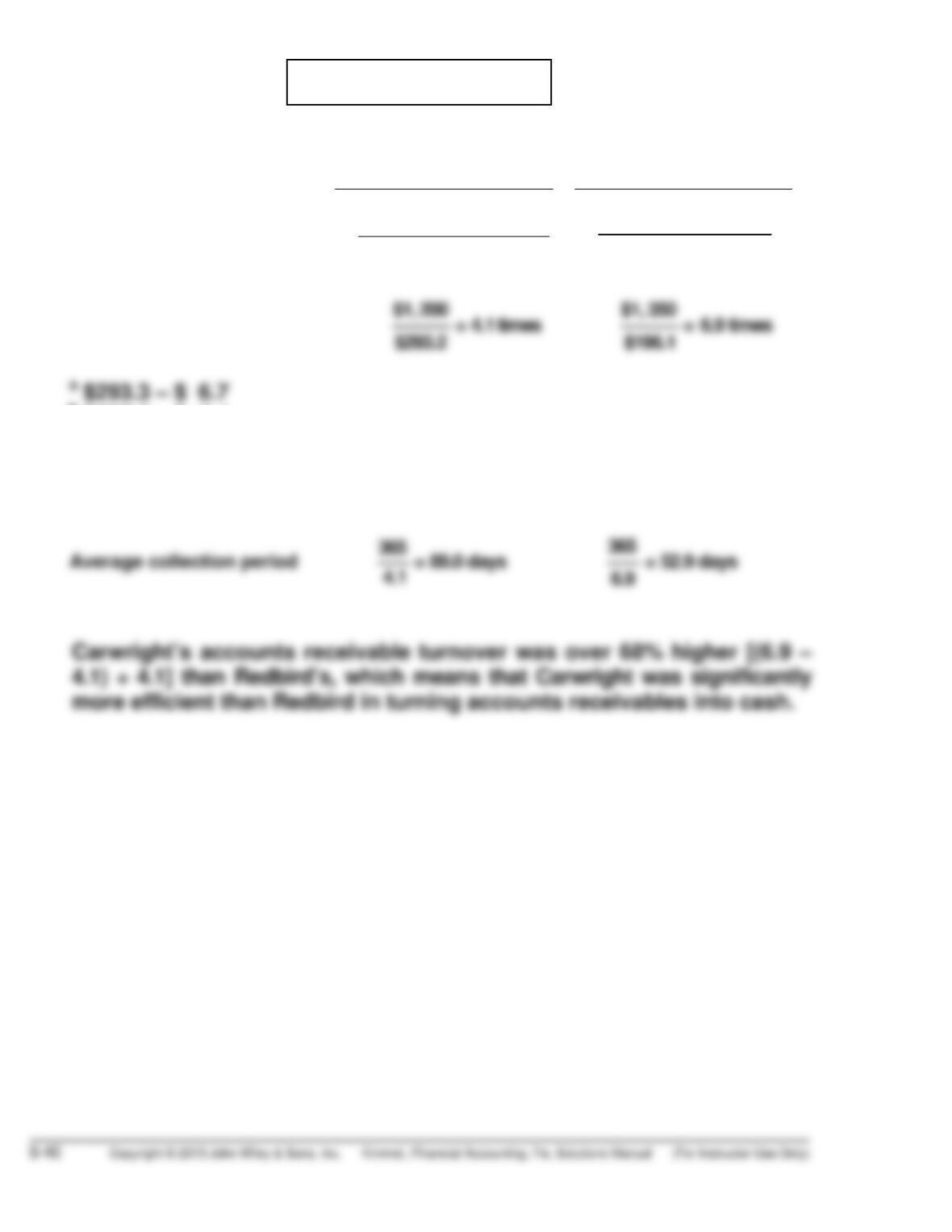

PROBLEM 8-9B

Redbird Sportswear Carwright Company

Accounts receivable turnover ab

$1, 200

($286.6 + $299.8 )/2 $1, 350

($204.0c+ $188.1d)/2

b

$307.2 – $ 7.4

c $216.5 – $12.5

d $202.9 – $14.8