CHAPTER 8

SOLUTIONS TO PROBLEMS: SET B

PROBLEM 8-1B

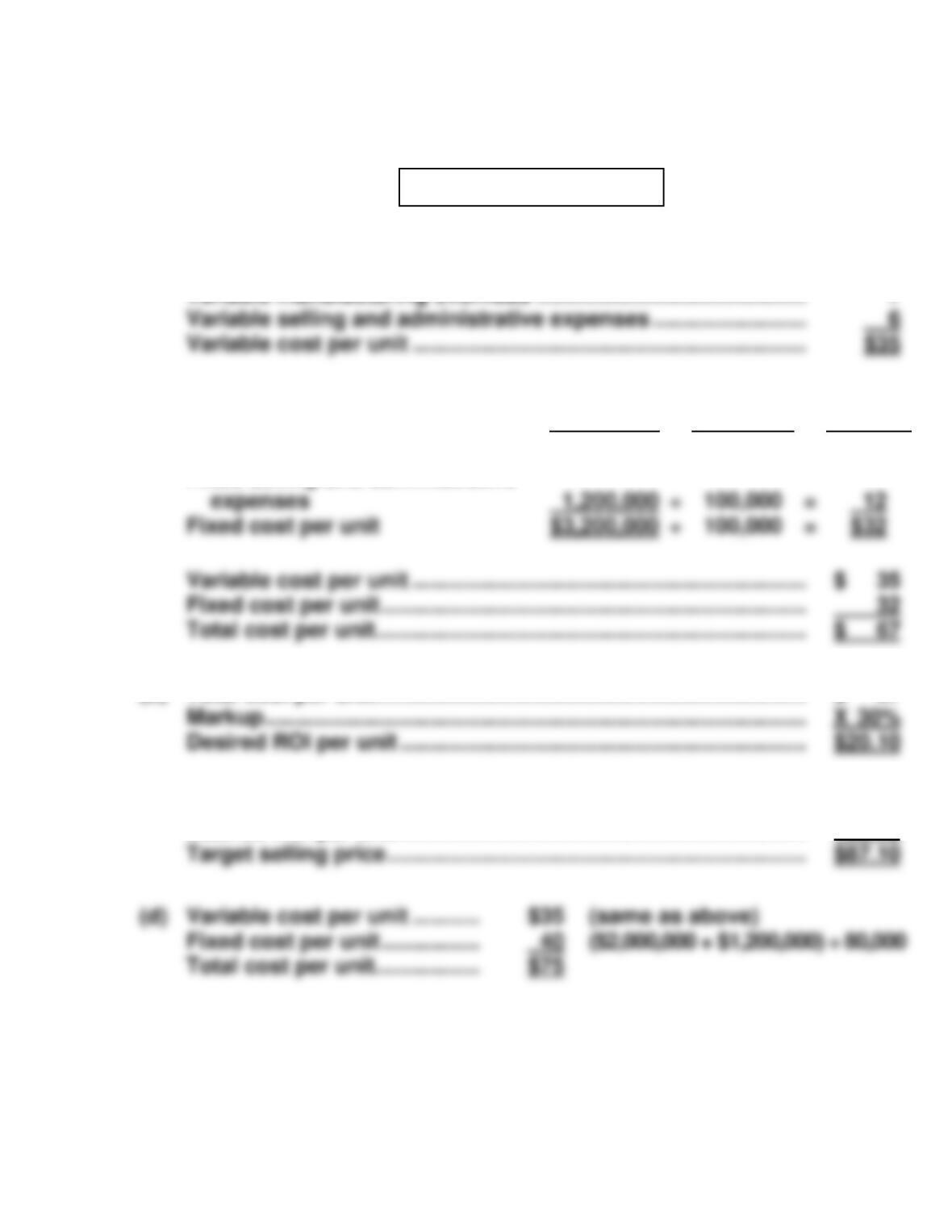

(a) Direct materials ……………………………………………………………….. $ 8

Direct labor ……………………………………………………………………… 14

Variable manufacturing overhead …………………………………….. 7

Total

Costs

÷

Budgeted

Volume

=

Cost

Per Unit

expenses

Fixed cost per unit

1,200,000

÷

100,000

=

Fixed manufacturing overhead

Fixed selling and administrative

$2,000,000

÷

100,000

=

$20

(b) Total cost per unit ……………………………………………………………. $ 67

(c) Total cost per unit ……………………………………………………………. $67.00

Desired ROI per unit ………………………………………………………… 20.10

PROBLEM 8-2B

(a) Direct materials ………………………………………………………………. $30

Direct labor …………………………………………………………………….. 20

Total

Costs

÷

Budgeted

Volume

=

Cost

Per Unit

expenses

Fixed cost per unit

÷

100,000

100,000

=

=

Fixed manufacturing overhead

$2,500,000

÷

100,000

=

$25

Desired ROI per unit

=

30% X $3,000,000

=

$9

100,000

(b) Variable cost per unit ……………………………………… $75 (same as (a))

Total

Costs

÷

Budgeted

Volume

=

Cost

Per Unit

expenses

Fixed cost per unit

500,000

÷

80,000

=

PROBLEM 8-2B (Continued)

Variable cost per unit ………………………………………………………. $ 75.00

Fixed cost per unit …………………………………………………………… 37.50

Total cost per unit ……………………………………………………………. $112.50

PROBLEM 8-3B

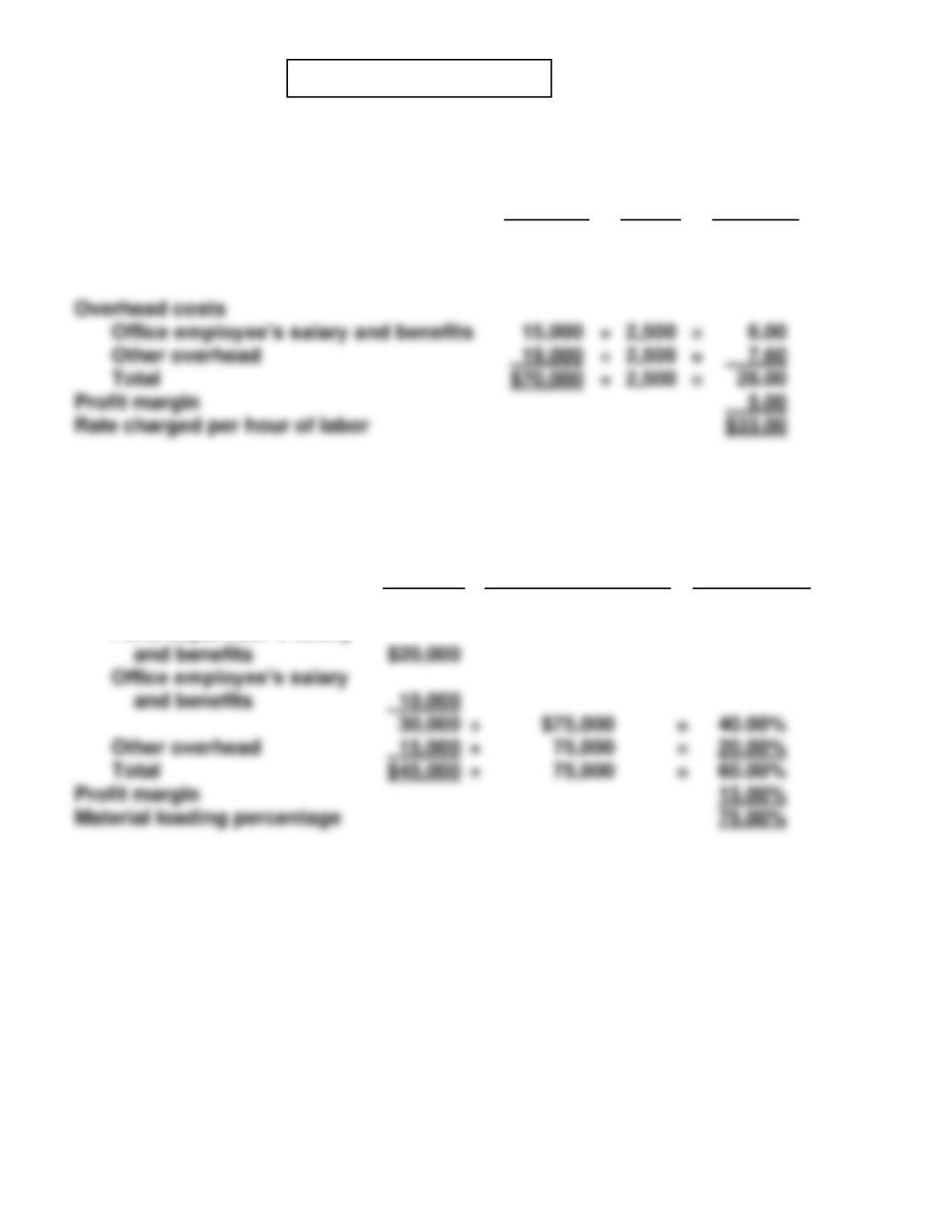

(a) Computation of time charge rate

Total

Cost

Total

Hours

Per Hour

Charge

Hourly labor rate for repairs

Shop employees’ wages and benefits

$36,000

÷

2,500

=

$14.40

(b) Computation of material loading charge

Material

Loading

Charges

Total Invoice Cost,

Parts and Materials

Material

Loading

Percentage

Total

Overhead costs

Parts supervisor’s salary

PROBLEM 8-3B (Continued)

(c) Price quotation for time and material

ARMSTRONG BIKE REPAIR SHOP

Time and Material Price Quotation

Job: Fix Superior Mountain bike

Labor charges: 4 hours @ $33 ……………. $132.00

PROBLEM 8-4B

(a) Assuming no available capacity, the printing operation’s variable cost

is $0.014 per page and its opportunity cost is $0.011 ($0.025 – $0.014)

(b) Assuming that the printing operation has available capacity, the print–

ing operation’s variable cost is $0.014 and its opportunity cost is $0.

The minimum transfer price would be $0.014 ($0.014 + $0). Therefore,

(c) The advantages of having all of the company’s printing done intern–

ally include: (1) ensuring that the company’s quality expectations are

met, (2) ensuring that all projects are completed on a timely basis, and

(d) The printing operation would lose:

($0.025 – $0.016) X 64 pages X 20,000 copies = ($11,520)

PROBLEM 8-5B

(a) The minimum transfer price is based on the variable cost of units

transferred internally, plus the opportunity cost of units sold externally.

(b) If the Peg Division rejects the offer, the Alto division will suffer a loss

of contribution margin, as well as the company as a whole. The amount

of this loss is calculated as:

Lost contribution margin by Alto Division:

Cost of buying externally, per Peg $0.28

Cost of buying internally, per Peg 0.26

Lost contribution margin by Peg Division:

Unit contribution margin on internal sales

($0.26 – $0.14) $0.12

Unit contribution margin on external sales

PROBLEM 8-6B

(a) Assuming no available capacity, and that the number of new units

produced would be equal to the number of standard units forgone,

variable cost of the special circuit board would be $50 ($30 + $20) and

(b) Assuming no available capacity, and that in order to produce the 200,000

circuit boards, 250,000 standard circuit boards would be forgone, the

minimum variable cost would be ($30 + $20) or $50 and the opportunity

cost would be:

(c) Assuming that the LT Division has available capacity, variable cost

would be $50 ($30 + $20) and the opportunity cost would be zero.

*PROBLEM 8-7B

(a) Absorption-cost pricing:

Computation of unit manufacturing cost and target selling price

Direct materials ………………………………………………………………. $ 50

Direct labor …………………………………………………………………….. 30

Variable manufacturing overhead ……………………………………. 13

(b) Variable-cost pricing:

Computation of total variable cost and target selling price

Direct materials ………………………………………………………………. $ 50

Direct labor …………………………………………………………………….. 30

Variable manufacturing overhead ……………………………………. 13

Variable selling and administrative expenses …………………… 7

*PROBLEM 8-8B

Absorption-cost pricing

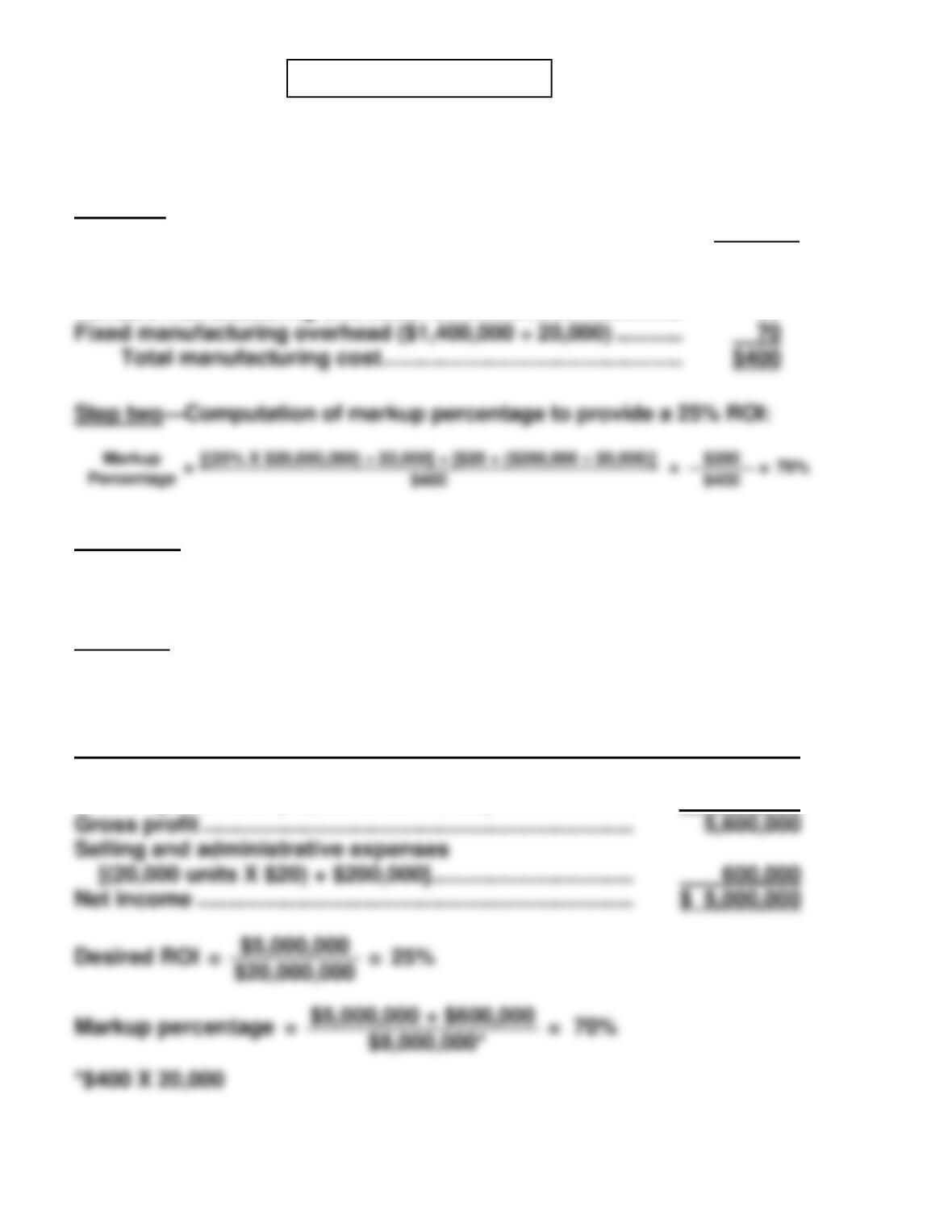

(a) Step one—Computation of unit manufacturing cost:

Per Unit

Direct materials ………………………………………………………………

Direct labor …………………………………………………………………….

Variable manufacturing overhead ……………………………………

$200

100

30

(b) Step three—Computation of target price:

Target price: $400 + (70% X $400) = $680

Step four—Proof of 25% ROI under absorption-cost approach:

GEORGIA GOULD BIKES INC.

Budgeted Absorption-Cost Income Statement

(Mountain Bike)

Revenues (20,000 units X $680) ……………………………….. $13,600,000

Cost of goods sold (20,000 units X $400) ………………….. 8,000,000

*PROBLEM 8-8B (Continued)

Variable-cost pricing

(c) Step one—Computation of unit variable cost:

Per Unit

Direct materials …………………………………………………………….

$200

(d) Step three—Computation of target price:

Target price: $350 + (94.3% X $350) = $680

GEORGIA GOULD BIKES INC.

Budgeted Variable-Cost Income Statement

(Mountain Bike)

Revenue (20,000 units X $680) ………………. $13,600,000

Variable costs (20,000 units X $350) ……… 7,000,000

Contribution margin …………………………….. 6,600,000

Fixed costs

*PROBLEM 8-8B (Continued)

(e) Both absorption–cost pricing and variable-cost pricing are used because

they have differing merits.

Absorption-cost pricing, especially when it includes full or all costs, is

preferred by some because in the long-run all costs plus a normal profit

margin must be covered. Using only variable costs, as the variable-cost

pricing does, is thought to encourage decision makers to set too low a