CHAPTER 8

UNDERSTANDING THE ISSUES

1. The stock dividend will result in the following entry being made by the subsidiary:

Retained Earnings (10,000 shares × $50 per share) ………………. 500,000

Common Stock ($1 par, 10,000 shares × $1) …………………….. 10,000

2. The parent shares in any equity increases from the excess of the current book value of $40 per

share ($4,000,000/100,000 shares) that the subsidiary receives. The parent does not record as in-

3. The subsidiary is selling the additional shares at $45 each, which is in excess of the current book

value of $40 per share ($4,000,000/100,000 shares).

(a) If the parent buys less than its current ownership percentage of shares, it will increase its equity

4. Control, in this example, is a “chain link” process. If A controls B and B, in turn, controls C, then all

three are under common ownership, and B and C are controlled by A.

5. The 2% holding in Company P shares, owned by Company S, is treated as treasury stock. This ap–

proach views the subsidiary as the parent’s agent in purchasing parent company shares. As treasury

8–3 Ch. 8—Exercises

EXERCISES

EXERCISE 8-1

(1) Retained Earnings (3,000 × $40) …………………………………………….. 120,000

Common Stock …………………………………………………………………. 30,000

Paid-In Capital in Excess of Par ………………………………………….. 90,000

To record stock dividend distributed on July 1, 2015.

(2) Memo: Investment in Lego Company now includes 2,700 (30,000 × 90% × 10%) additional

shares for a total of 29,700 shares.

Cash ……………………………………………………………………………………. 14,850

(3) Subsidiary Income …………………………………………………………………. 108,000

Investment in Lego Company ……………………………………………… 93,150

Dividends—Leego Company ………………………………………………. 14,850

Exercise 8-1, Concluded

Determination and Distribution of Excess Schedule

Company Parent NCI

Implied Price Value

Fair Value (90%) (10%)

Fair value of subsidiary …………………… $900,000 $810,000 $ 90,000

Less book value of interest acquired:

Common stock ($10 par) ……………. $300,000

Paid-in capital in excess of par …… 150,000

Retained earnings …………………….. 200,000

EXERCISE 8-2

Investment in Trailer …………………………………………………………………… 57,750

Subsidiary Income …………………………………………………………………. 57,750

Calculation:

90% × first 6 months’ income of $35,000 ………………………………….. $31,500

75%* × second 6 months’ income of $35,000 ……………………………. 26,250

Total …………………………………………………………………………………………. $57,750

8–5 Ch. 8—Exercises

EXERCISE 8-3

Maintain Increase Decrease

Interest

Interest Interest

Shares purchased by parent ……………………………….. 8,000 9,000 5,000

Total shares owned by parent after purchase ………… 24,000 25,000 21,000

Total subsidiary shares outstanding after issue ……… 30,000 30,000 30,000

Subsidiary equity after sale ($450,000 + $60,000

Parent’s ownership percent before purchase ………… × 80% × 80% × 80%

Parent’s equity interest before purchase ………………. $ 448,000 $ 448,000 $ 448,000

Price paid ($60 per share) ………………………………….. 480,000 540,000 300,000

Total investment ………………………………………………… $ 928,000 $ 988,000 $ 748,000

Net adjustment ………………………………………………….. $ 0 $ 21,333 $ (64,000)

Maintain ownership percentage interest:

Investment in Calco Company ……………………………………………… 480,000

Cash …………………………………………………………………………….. 480,000

EXERCISE 8-4

Investment in Nolan …………………………………………………………………. 81,360

Retained Earnings—Tarman ………………………………………………… 81,360

To convert investment from cost to equity for income.

Income equity adjustment:

Jan. 1, 2015 to Jan. 1, 2017 increase in retained earning ($42,000 × 60%) $25,200

Jan. 1, 2017 to Jan. 1, 2019 increase in retained earnings ($78,000 × 72%*) 56,160

Total …………………………………………………………………………………………….. $81,360

EXERCISE 8-5

(1)

Company A’s Books Company B’s Books

December 31, 2015 Cash …………………………………. 4,000

Investment in B …………………… 12,000

Subsidiary Income—B ………. 16,000

December 31, 2016 Cash …………………………………. 4,000 Cash ……………………………………. 3,000

Investment in B …………………… 32,000 Investment in C ……………………… 12,000

Subsidiary Income—B ………. 36,000 Subsidiary Income—C ………. 15,000

(2)

Company A’s Books Company B’s Books

December 31, 2015 Investment in C ……………………… 7,000

Subsidiary Income—C ………. 7,000

December 31, 2016 Cash ……………………………………. 3,500

Investment in C ……………………… 14,000

Subsidiary Income—C ………. 17,500

EXERCISE 8-6

(1)

Determination and Distribution of Excess Schedule

Company Parent NCI

Implied Price Value

Fair Value (60%) (40%)

Fair value of subsidiary …………………… $4,500,000 $2,700,000 $1,800,000

Less book value of interest acquired:

Common stock …………………………. $ 400,000

Adjustment of identifiable accounts:

Worksheet Amortization

Adjustment Key Life per Year

Cain Company equipment ………………. $ 80,000 debit D1

*NCI of Cain Company is also increased by $40,000.

(2) Eliminations and Adjustments:

Retained Earnings—Able ($12,000 × 80% × 60%) ………………….. 5,760

Retained Earnings—Baker ($12,000 × 80% × 40%) ………………… 3,840

8–9 Ch. 8—Exercises

EXERCISE 8-7

Companies A, B, and C

Consolidated Income Statement

For Year Ended December 31, 2015

Sales [($300,000 + $400,000 + $100,000) –

intercompany sales of $75,000] ………………………………………. $725,000

Cost of goods sold [$200,000 + $300,000 + $60,000 –

Subsidiary Company C Income Distribution

Unrealized profit in ending Internally generated net

inventory ……………………………. $6,000 income ……………………………. $30,000

Adjusted net income ………………. $24,000

Subsidiary Company B Income Distribution*

Internally generated net income . $70,000

60% × Company C adjusted

income of $24,000 ……………. 14,400

Gain realized through

*There is no impact shown for the ending inventory held by Company C since the gross profit was written down to

zero under LCM.

Parent Company A Income Distribution

Unrealized profit in ending Internally generated net

inventory ……………………………. $720 income ……………………………. $ 40,000

EXERCISE 8-8

Determination and Distribution of Excess Schedule, Ace Acquisition of Bell

Company Parent NCI

Implied Price Value

Fair Value (60%) (40%)

Fair value of subsidiary …………………… $700,000 $420,000 $280,000

Less book value of interest acquired:

Common stock ($5 par) ……………… $200,000

Paid-in capital in excess of par …… 100,000

Adjustment of identifiable accounts:

Worksheet Amortization

Adjustment Key Life per Year

Carter inventory (80% …………………….. $ 16,000 debit D1 1 $16,000

EXERCISE 8-9

(1) Company N’s books:

Cash …………………………………………………………………………….. 2,000

Investment in Company O ……………………………………………….. 14,000

Subsidiary Income (40% × $40,000) ……………………………… 16,000

Company M’s books:

Cash …………………………………………………………………………….. 9,000

Investment in Company N ……………………………………………….. 86,400

8–11 Ch. 8—Exercises

Exercise 8-9, Concluded

Subsidiary O Company Income Distribution

Unrealized gross profit in Internally generated income ….. $40,000

ending inventory …………………. $6,000 Realized gross profit in

beginning inventory …………. 4,500

Adjusted income ………………….. $38,500

NCI share …………………………… × 40%

NCI ……………………………………. $15,400

Subsidiary N Company Income Distribution

Unrealized gross profit in Internally generated income ….. $ 90,000

Parent Company M Income Distribution

Internally generated net

income ………………………….. $200,000

EXERCISE 8-10

(1)

Determination and Distribution of Excess Schedule

Company Parent NCI

Implied Price Value

Fair Value (60%) (40%)

Fair value of subsidiary …………………… $580,000 $348,000 $232,000

Less book value of interest acquired:

(2) Myles Corporation and Subsidiary Downer Corporation

Consolidated Income Statement

For Year Ended December 31, 2017

Sales ……………………………………………………………………………………………… $1,150,000

Less cost of goods sold …………………………………………………………………….. 840,000

Gross profit ……………………………………………………………………………………… $ 310,000

Subsidiary Downer Corporation Income Distribution

Equipment depreciation ……………. $1,500 Internally generated net income .. $30,000

Adjusted net income ………………. $28,500

NCI share ……………………………… × 40%

NCI ………………………………………. $11,400

8–13 Ch. 8—Problems

PROBLEMS

PROBLEM 8-1

Wells Corporation booked entries for adjustments to investment in Towne Company:

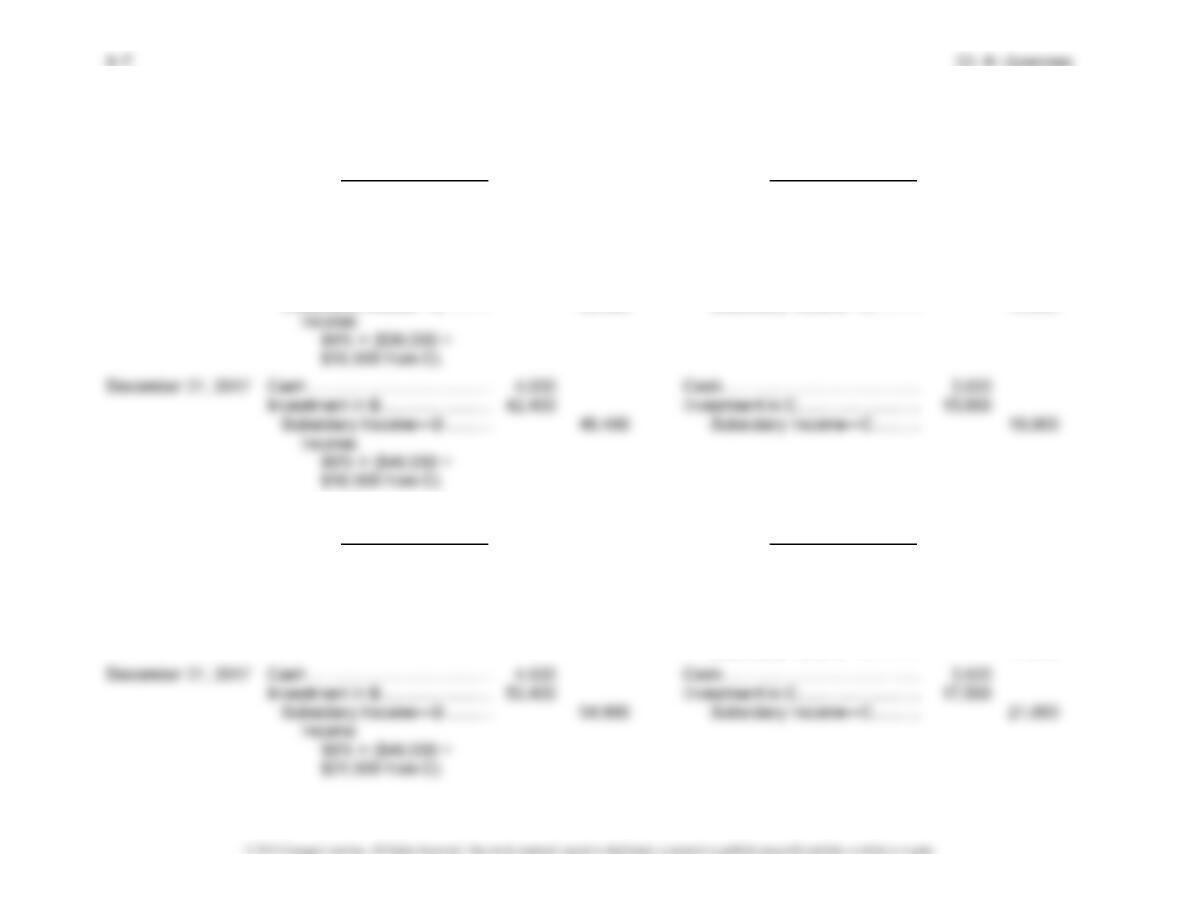

2015

(1)* December 31 Investment in Towne (80% × $50,000) …………… 40,000

(2)* Memo: All calculations are now based on 8,800 shares.

2016

(3)* July 1 Investment in Towne …………………………………… 14,400

Paid-In Capital in Excess of Par ………………. 14,400

(4)* December 31 Investment in Towne …………………………………… 16,000

Subsidiary Income …………………………………. 16,000

Problem 8-1, Continued

Wells Corporation booked entries for adjustments to investment in Sara Company:

2015

(5)* July 1 Investment in Sara ………………………………………. 12,000

Subsidiary Income …………………………………. 12,000

(6)* July 1 Investment in Sara ………………………………………. 85,900

Retained Earnings (decrease in equity) …………. 6,600

(7)* December 31 Investment in Sara ………………………………………. 12,400

Subsidiary Income …………………………………. 12,400

(8)*January 1 Retained Earnings ………………………………………. 13,950

(9)* December 31 Investment in Sara ………………………………………. 28,933

Subsidiary Income …………………………………. 28,933

Problem 8-1, Concluded

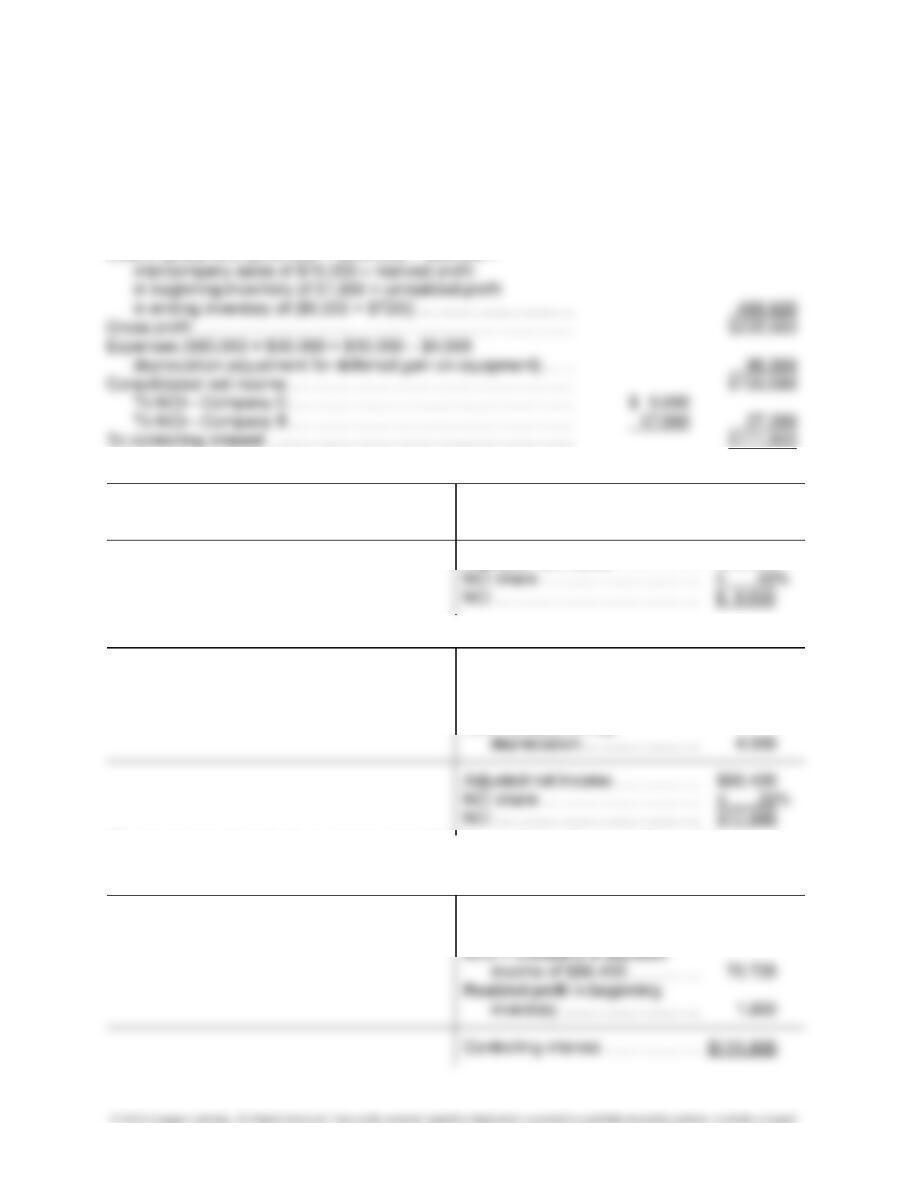

Schedules to Determine Wells Corporation’s Adjustments to Its Investment

Total Change in Total Controlling Change in

Subsidiary Parent’s Parent’s Subsidiary Subsidiary Share of Controlling

Shares Shares Interest Equity Equity Equity Investment

Towne

January 1, 2015, Balances ……… 10,000 8,000 80% ……….. $220,000 $176,000 …………

2015 Income …………………………. 10,000 8,000 80 $50,000 270,000 216,000 (1) $40,000

December 31, 2015, Stock

dividend …………………………… 11,000 8,800 80 ……….. 270,000 216,000 …………

January–June 2016, Income ……. 11,000 8,800 80 25,000 295,000 236,000 (2) 20,000

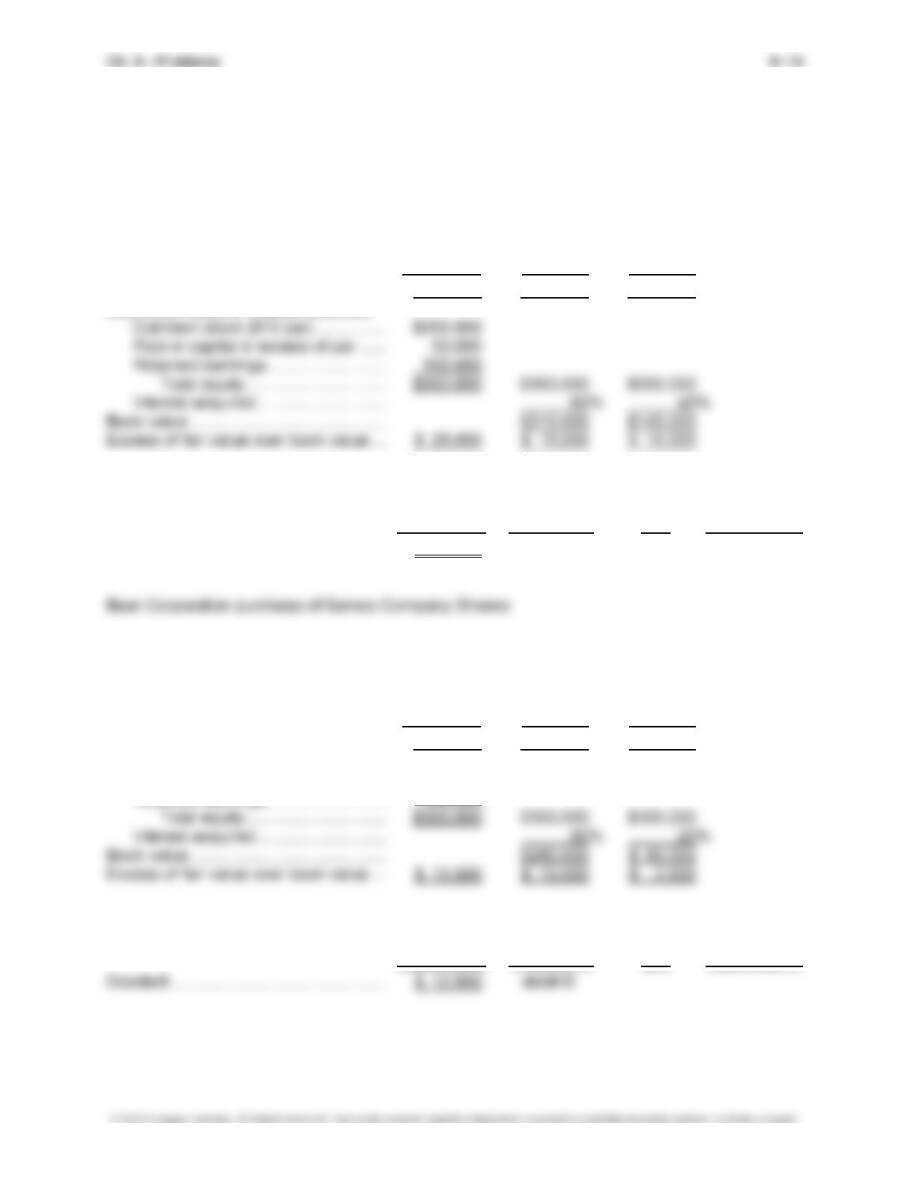

PROBLEM 8-2

Bear Corporation purchase of Kelly Company Shares:

Determination and Distribution of Excess Schedule

Company Parent NCI

Implied Price Value

Fair Value (60%) (40%)

Fair value of subsidiary …………………… $375,000 $225,000 $150,000

Less book value of interest acquired:

Adjustment of identifiable accounts:

Worksheet Amortization

Adjustment Key Life per Year

Goodwill ……………………………………….. $ 25,000 debit D

Determination and Distribution of Excess Schedule

Company Parent NCI

Implied Price Value

Fair Value (80%) (20%)

Fair value of subsidiary …………………… $312,500 $250,000 $ 62,500

Less book value of interest acquired:

Common stock ($20 par) ……………. $200,000

Retained earnings …………………….. 100,000

Adjustment of identifiable accounts:

Worksheet Amortization

Adjustment Key Life per Year

8–17 Ch. 8—Problems

Problem 8-2, Continued

*Entry to convert investment in Kelly Company to simple equity method as of December 31,

2017:

Investment in Kelly ……………………………………………………. 78,750

Additional Paid-In Capital in Excess of Par—Bear

Corporation ………………………………………………………….. 12,750

Retained Earnings ……………………………………………… 91,500

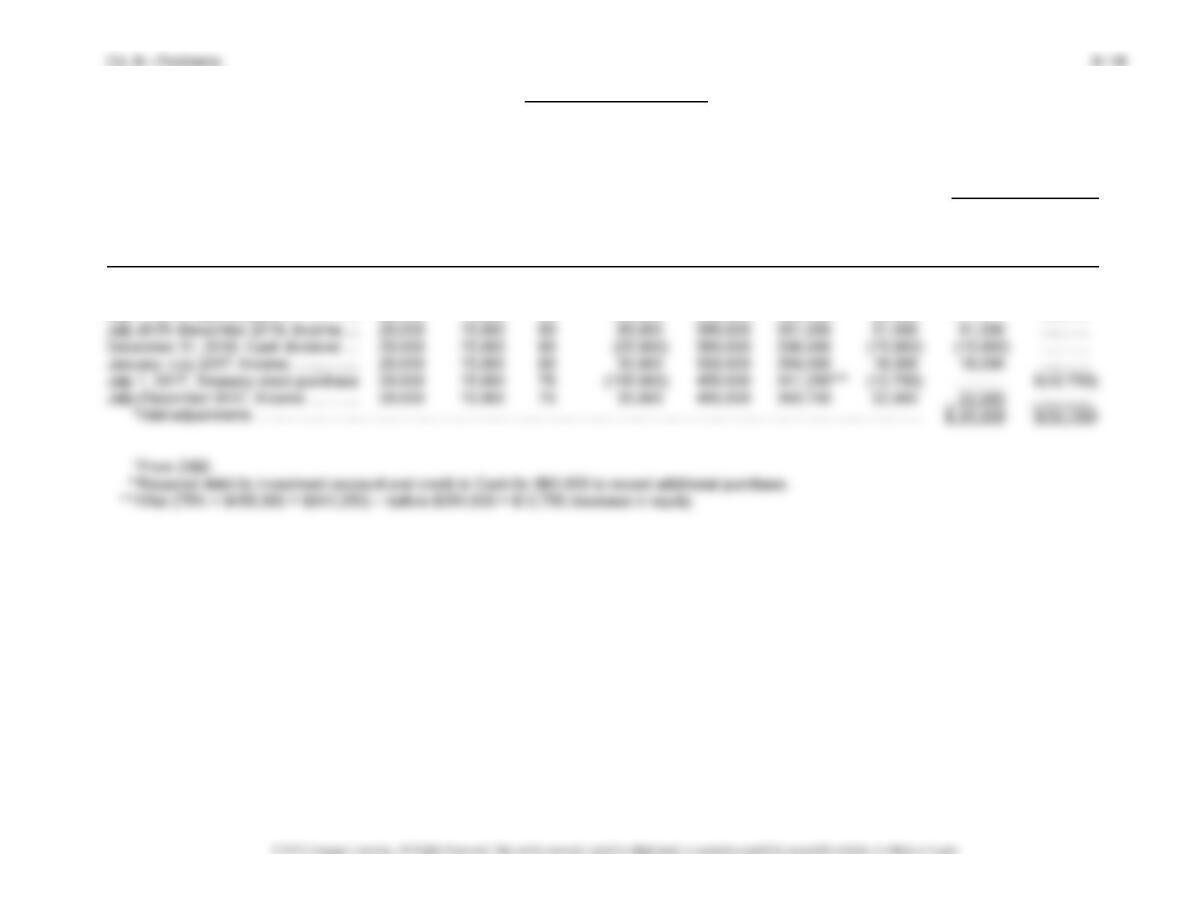

Problem 8-2, Continued

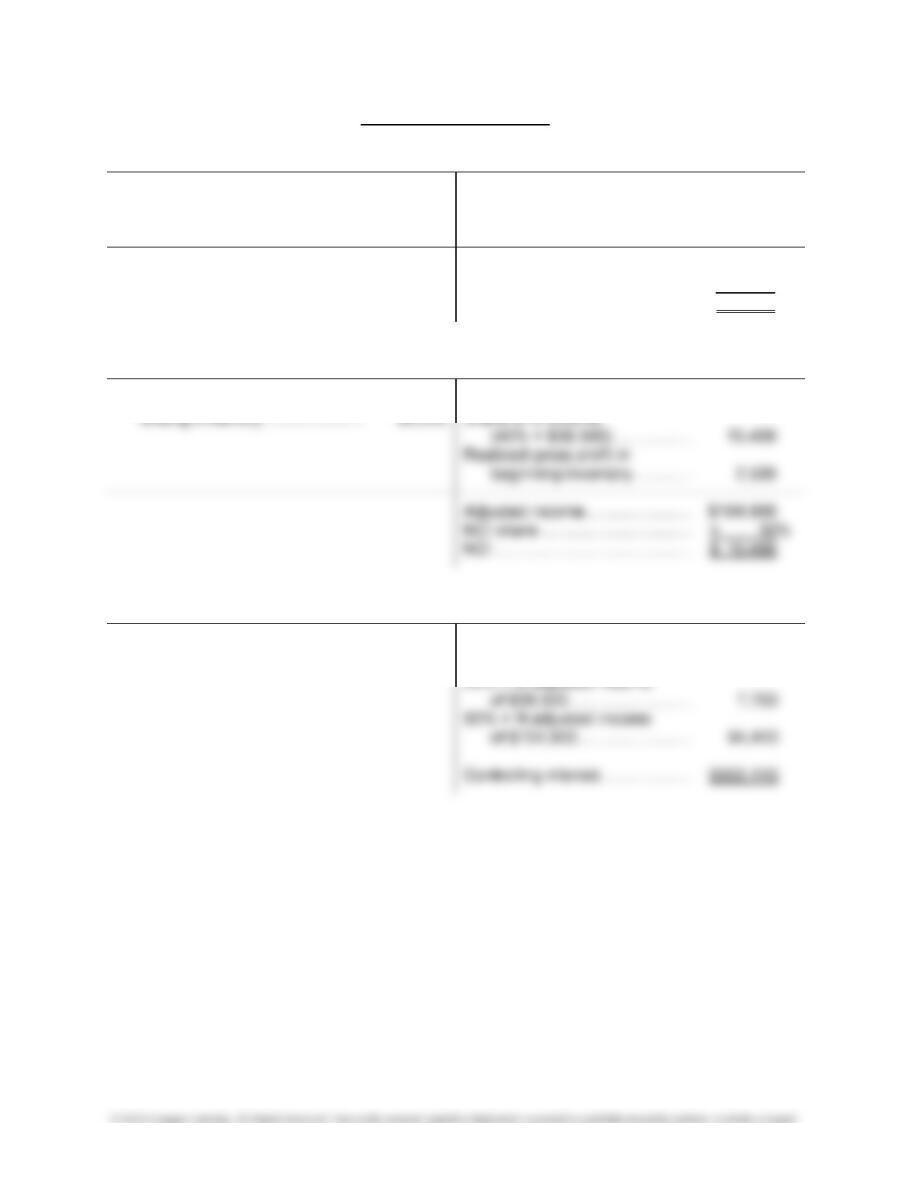

Schedules of Equity Adjustments for January 1, 2015–December 31, 2017

Adjustments

Reflected

an Increase to

Controlling Additional

Total Shares Increase in Total Share of Increase in Paid-In Capital

Subsidiary Held by Parent’s Subsidiary Subsidiary Subsidiary Controlling Retained in Excess

Kelly Common Stock Shares Parent Interest Equity Equity Equity Investment Earnings of Par

January 1, 2015, Balances………………. 20,000 12,000 60% ………….. $375,000* $225,000 ………….. ………… …………

January–June 2015, Income ……………. 20,000 12,000 60 $ 25,000 400,000 240,000 $ 15,000 $ 15,000 …………

July 1, 2015, Sale of stock ………………. 25,000 15,000 60 100,000 500,000 300,000 60,000** ………… …………

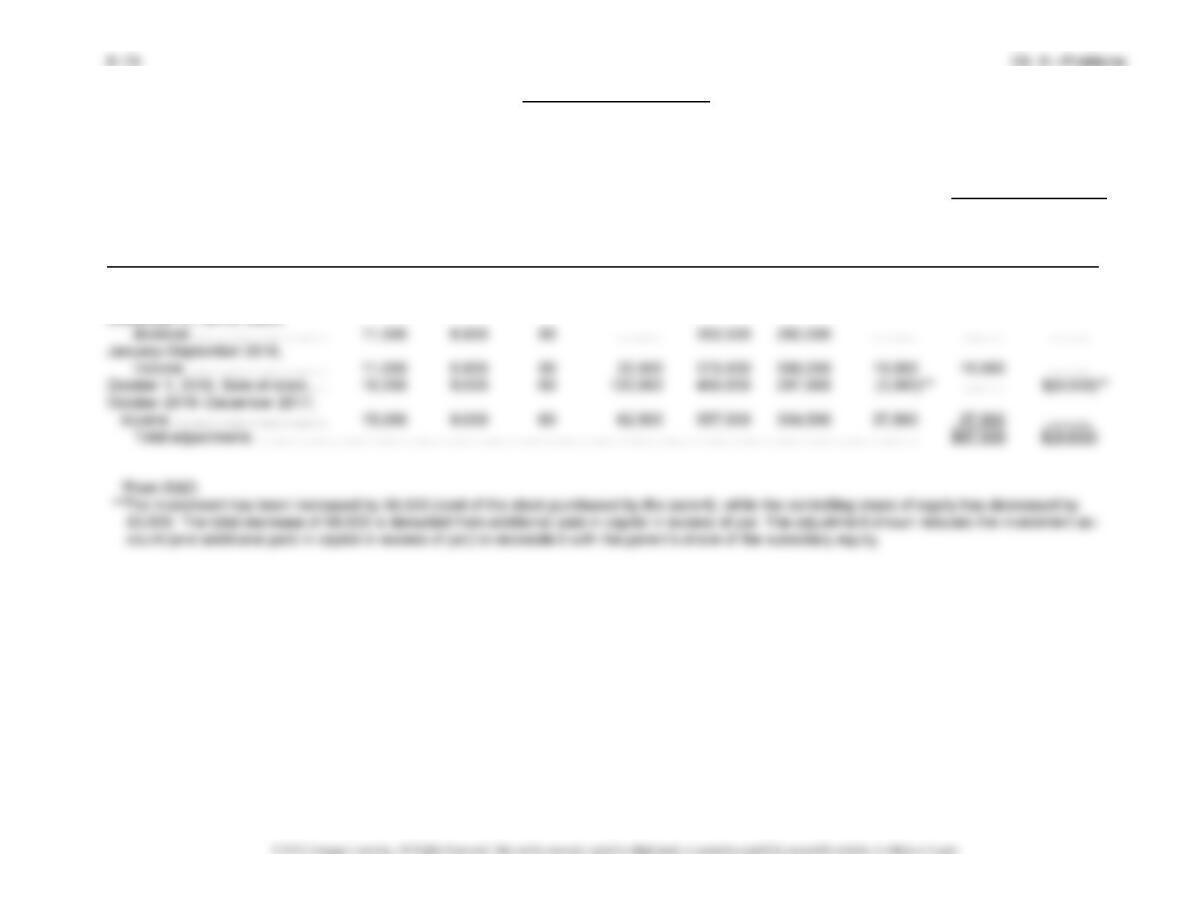

Problem 8-2, Concluded

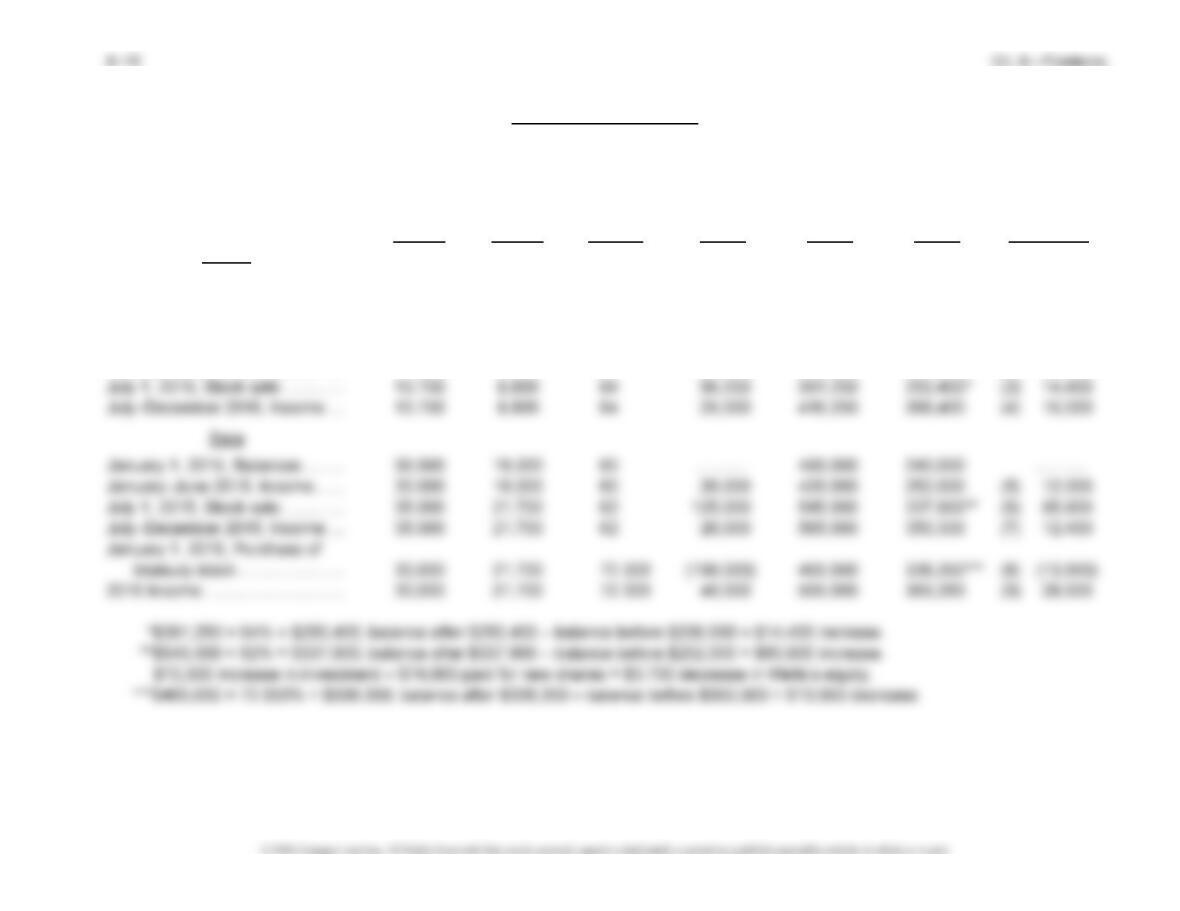

Schedules of Equity Adjustments for January 1, 2015–December 31, 2017

Adjustments

Reflected

an Increase to

Controlling Paid-In

Total Shares Increase in Total Share of Increase in Capital

Subsidiary Held by Parent’s Subsidiary Subsidiary Subsidiary Controlling Retained in Excess

Samco Common Stock Shares Parent Interest Equity Equity Equity Investment Earnings of Par

January 1, 2015, Balances……….. 10,000 8,000 80% ……….. $312,500* $250,000 ……….. ………. ………

Income, 2015 …………………………. 10,000 8,000 80 40,000 352,500 282,000 $32,000 $32,000 ………

December 31, 2015, Stock

PROBLEM 8-3

Determination and Distribution of Excess Schedule

Company Parent NCI

Implied Price Value

Fair Value (80%) (20%)

Fair value of subsidiary …………………… $875,000 $700,000 $175,000

Less book value of interest acquired:

Common stock ($2 par) ……………… $200,000

Adjustment of identifiable accounts:

Worksheet Amortization

Adjustment Key Life per Year

Building ………………………………………… $ 80,000 debit D1 20 $4,000