Chapter 8

Receivables

Review Questions

1. What is the difference between accounts receivable and notes receivable?

Accounts receivable represent the right to receive cash in the future from customers for goods sold

2. List some common examples of other receivables, besides accounts receivable and notes receivable.

3. What is a critical element of internal control in the handling of receivables by a business? Explain

how this element is accomplished .

A critical element of internal control is the separation of cash-handling and cash-accounting duties.

4. When dealing with receivables, give an example of a subsidiary account.

5. What type of account must the sum of all subsidiary accounts be equal to?

6. What are some benefits to a business in accepting credit cards and debit cards?

The benefits to a business of accepting credit cards and debit cards include the ability to attract more

8-2

7. What occurs when a business factors its receivables?

When a business factors its receivables, it sells its receivables to a finance company or bank (often

8. What occurs when a business pledges its receivables?

In a pledging situation, a business uses its receivables as security for a loan. The business borrows

9. What is the expense account associated with the cost of uncollectible receivables called?

10. When is bad debts expense recorded when using the direct write-off method?

11. What are some limitations of using the direct write-off method?

Limitations of the direct write-off method are that it violates the matching principle and is not

12. When is bad debts expense recorded when using the allowance method?

13. When using the allowance method, how are accounts receivable shown on the balance sheet?

14. When using the allowance method, what account is debited when writing off uncollectible accounts?

How does this differ from the direct write-off method?

15. When a receivable is written off under the allowance method, how does it affect the net realizable

value shown on the balance sheet?

16. How does the percent-of-sales method compute bad debts expense?

The percent-of-sales method computes bad debts expense as a percentage of net credit sales.

17. How do the percent-of-receivables and aging-of-receivables methods compute bad debts expense?

In both the percent-of-receivables method and aging-of-receivables method, the business determines

18. What is the difference between the percent-of-receivables and aging-of-receivables methods?

In the percent-of-receivables method, the business uses only one percentage to determine the balance

19. In accounting for bad debts, how do the income statement approach and the balance sheet approach

differ?

The income statement approach focuses on the amount of expense, Bad Debt Expense, that is

20. What is the formula to compute interest on a note receivable?

21. Why must companies record accrued interest revenue at the end of the accounting period?

The interest revenue earned on the note up to year-end is part of that year’s earnings. Interest

8-4

22. How is the acid-test ratio calculated, and what does it signify?

23. What does the accounts receivable turnover ratio measure, and how is it calculated?

24. What does the days’ sales in receivables indicate, and how is it calculated?

Days’ sales in receivables, also called the collection period, indicates how many days it takes to

8-5

Short Exercises

S8-1 Ensuring internal control over the collection of receivables

Learning Objective 1Consider internal control over receivables collections. What job must be withheld

from a company’s credit department in order to safeguard its cash? If the credit department does perform

this job, what can a credit department employee do to hurt the company?

SOLUTION

The company’s credit department should not take customer payments or have any other cash-handling

S8-2 Recording credit sales and collections

Learning Objective 1

Record the following transactions for Summer Consulting. Explanations are not required.

Apr.

15

Provided consulting services to Bob Jones and billed the customer

$1,500.

18

Provided consulting services to Samantha Cruise and billed the

customer $865.

25

Received $750 cash from Jones.

28

Provided consulting services to Regan Taylor and billed the

customer $625.

28

Received $865 cash from Cruise.

30

Received $1,375 cash, $750 from Jones and $625 from Taylor.

8-6

SOLUTION

Date

Accounts and Explanation

Debit

Credit

Apr. 15

Accounts Receivable—Jones

1,500

Service Revenue

1,500

S8-3 Applying the direct write-off method to account for uncollectibles

Learning Objective 2

Shawna Valley is an attorney in Los Angeles. Valley uses the direct write-off method to account for

uncollectible receivables.

At April 30, 2018, Valley’s accounts receivable totaled $19,000. During May, she earned revenue of

$22,000 on account and collected $15,000 on account. She also wrote off uncollectible receivables of

$1,100 on May 31, 2018.

Requirements

1. Use the direct write-off method to journalize Valley’s write-off of the uncollectible receivables.

2. What is Valley’s balance of Accounts Receivable at May 31, 2018?

Accounts Receivable—Cruise

Service Revenue

Cash

Accounts Receivable—Jones

Accounts Receivable—Taylor

Service Revenue

Cash

Accounts Receivable—Cruise

Cash

1,375

Accounts Receivable—Jones

Accounts Receivable—Taylor

8-7

SOLUTION

Requirement 1

Date

Accounts and Explanation

Debit

Credit

May 31

Bad Debts Expense

1,100

S8-4 Collecting a receivable previously written off—direct write-off method

Learning Objective 2

Spring Garden Greenhouse had trouble collecting its account receivable from Steve Stone. On June 19,

2018, Spring Garden Greenhouse finally wrote off Stone’s $600 account receivable. On December 31,

Stone sent a $600 check to Spring Garden Greenhouse.

Journalize the entries required for Spring Garden Greenhouse, assuming Spring Garden Greenhouse

uses the direct write-off method.

SOLUTION

Date

Accounts and Explanation

Debit

Credit

2018

Jun. 19

Bad Debts Expense

600

Accounts Receivable—Stone

600

Accounts Receivable—Stone

600

Bad Debts Expense

600

Cash

600

Accounts Receivable—Stone

600

Accounts Receivable

1,100

15,000

1,100

S8-5 Applying the allowance method to account for uncollectibles

Learning Objective 3

The Accounts Receivable balance and Allowance for Bad Debts for Signature Lamp Company at

December 31, 2017, was $10,800 and $2,000 (credit balance), respectively. During 2018, Signature

Lamp Company completed the following transactions:

a. Sales revenue on account, $273,400 (ignore Cost of Goods Sold).

b. Collections on account, $223,000.

c. Write-offs of uncollectibles, $5,900.

d. Bad debts expense of $5,200 was recorded.

Requirements

1. Journalize Signature Lamp Company’s transactions for 2018 assuming Signature Lamp Company

uses the allowance method.

2. Post the transactions to the Accounts Receivable, Allowance for Bad Debts, and Bad Debts Expense

T-accounts, and determine the ending balance of each account.

3. Show how accounts receivable would be reported on the balance sheet at December 31, 2018.

SOLUTION

Requirement 1

Date

Accounts and Explanation

Debit

Credit

2018

a.

Accounts Receivable

273,400

Sales Revenue

273,400

Cash

223,000

223,000

c.

Allowance for Bad Debts

8-9

S8-5, cont.

Requirement 2

Accounts Receivable

Dec. 31, 2017, Bal.

10,800

223,000

Collections

Net credit sales

273,400

5,900

Write-offs

Dec. 31, 2018, Bal.

55,300

Requirement 3

SIGNATURE LAMP COMPANY

Balance Sheet−Partial

December 31, 2018

Current Assets:

Accounts Receivable

S8-6 Applying the allowance method (percent-of-sales) to account for uncollectibles

Learning Objective 3

During its first year of operations, Fall Wine Tour earned net credit sales of $311,000. Industry

experience suggests that bad debts will amount to 3% of net credit sales. At December 31, 2018,

accounts receivable total $44,000. The company uses the allowance method to account for

uncollectibles.

Requirements

1. Journalize Fall Wine Tour’s Bad Debts Expense using the percent–of-sales method.

2. Show how to report accounts receivable on the balance sheet at December 31, 2018.

2,000

Dec. 31, 2017, Bal.

Write-offs

5,200

Adj.

1,300

Dec. 31, 2018, Bal.

Bad Debts Expense

Adj.

Dec. 31, 2018, Bal.

8-10

SOLUTION

Requirement 1

Date

Accounts and Explanation

Debit

Credit

2018

Requirement 2

FALL WINE TOUR

Balance Sheet−Partial

December 31, 2018

Current Assets:

Accounts Receivable

S8-7 Applying the allowance method (percent-of-receivables) to account for uncollectibles

Learning Objective 3

The Accounts Receivable balance for Lake, Inc. at December 31, 2017, was $20,000. During 2018, Lake

earned revenue of $454,000 on account and collected $325,000 on account. Lake wrote off $5,600

receivables as uncollectible. Industry experience suggests that uncollectible accounts will amount to 5%

of accounts receivable.

Requirements

1. Assume Lake had an unadjusted $2,700 credit balance in Allowance for Bad Debts at December 31,

2018. Journalize Lake’s December 31, 2018, adjustment to record bad debts expense using the

percent-of-receivables method.

2. Assume Lake had an unadjusted $2,400 debit balance in Allowance for Bad Debts at December 31,

2018. Journalize Lake’s December 31, 2018, adjustment to record bad debts expense using the

percent-of-receivables method.

Dec. 31

Bad Debts Expense ($311,000 × 3%)

8-11

SOLUTION

Requirement 1

Accounts Receivable

Dec. 31, 2017, Bal.

20,000

325,000

Collections

Net credit sales

454,000

5,600

Write-offs

Dec. 31, 2018, Bal.

143,400

Dec. 31

Bad Debts Expense

Dec. 31

Bad Debts Expense

8-12

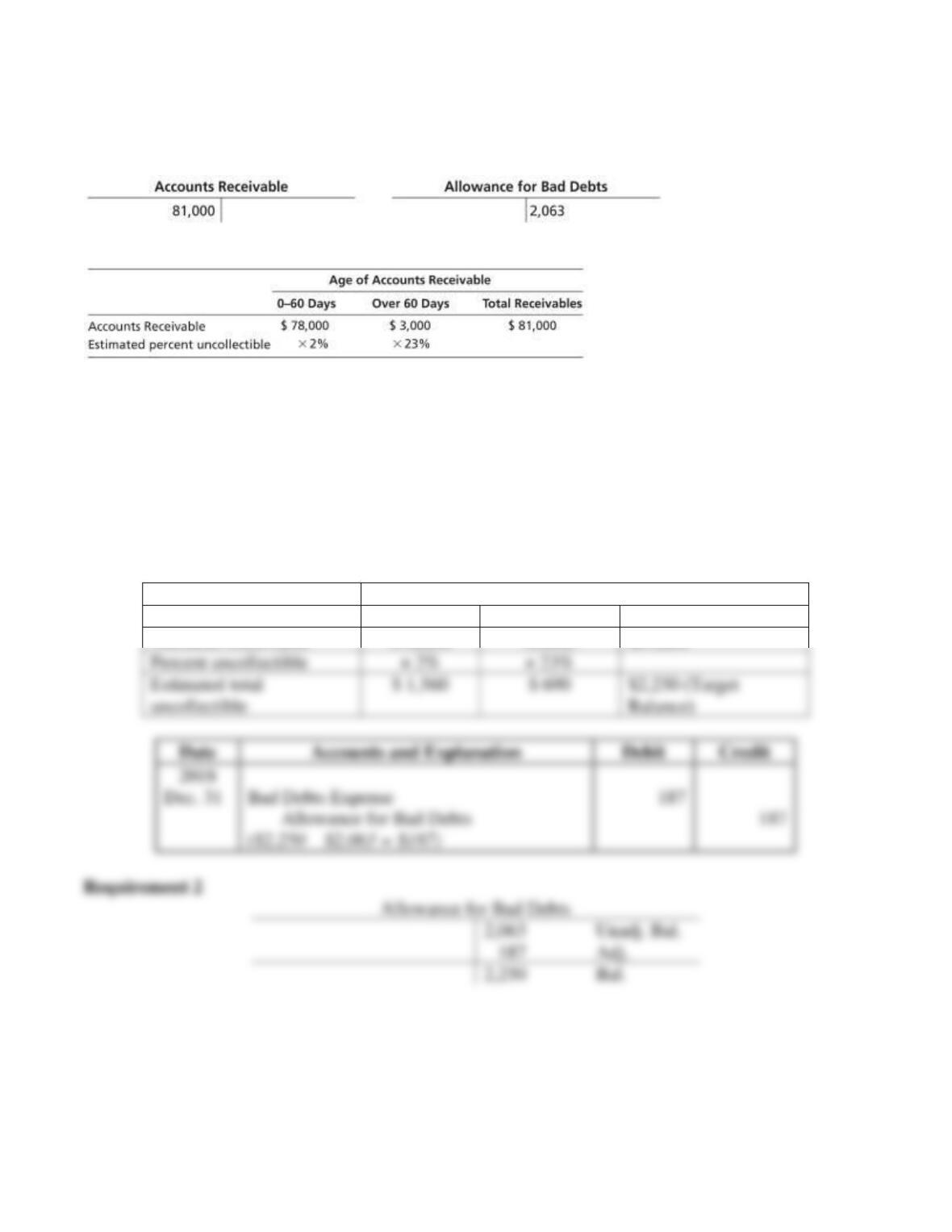

S8-8 Applying the allowance method (aging-of-receivables) to account for uncollectibles

Learning Objective 3

Surf and Sun had the following balances at December 31, 2018, before the year-end adjustments:

The aging of accounts receivable yields the following data:

Requirements

1. Journalize Surf and Sun’s entry to record bad debts expense for 2018 using the aging-of-receivables

method.

2. Prepare a T-account to compute the ending balance of Allowance for Bad Debts.

SOLUTION

Requirement 1

Age of Accounts Receivable

0 – 60 Days

Over 60 Days

Total Receivables

Accounts Receivable

$78,000

$3,000

$81,000

Percent uncollectible

uncollectible

Balance)

Dec. 31

Bad Debts Expense

2,063

187

2,250

8-13

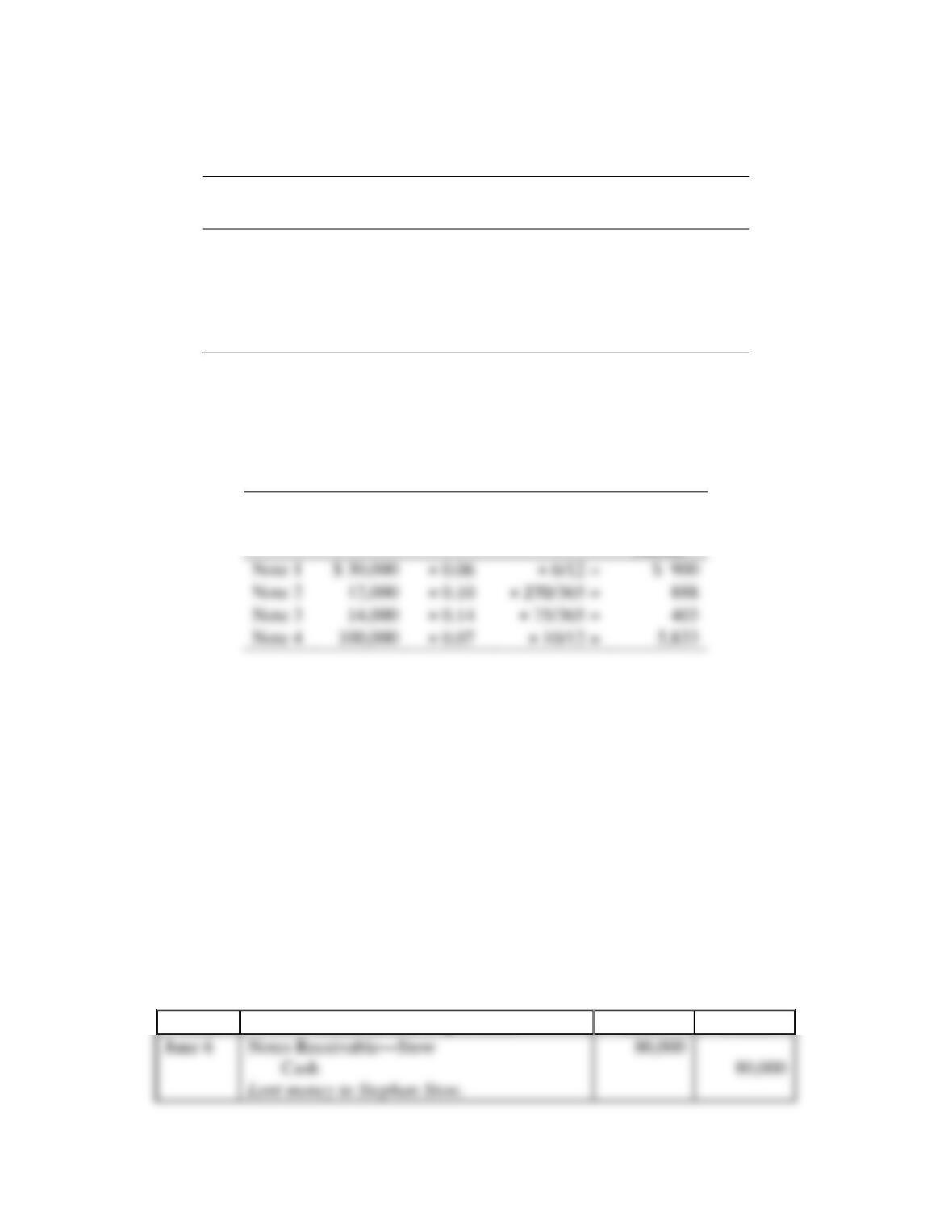

S8-9 Computing interest amounts on notes receivable

Learning Objective 4

A table of notes receivable for 2018 follows:

Principal

Interest Rate

Interest Period During

2018

Note 1

$ 30,000

6%

6 months

Note 2

12,000

10%

270 days

Note 3

14,000

14%

75 days

Note 4

100,000

7%

10 months

For each of the notes receivable, compute the amount of interest revenue earned during 2018. Round to

the nearest dollar.

SOLUTION

Principal

Interest

Rate

Interest

Period

Interest

Revenue

Earned

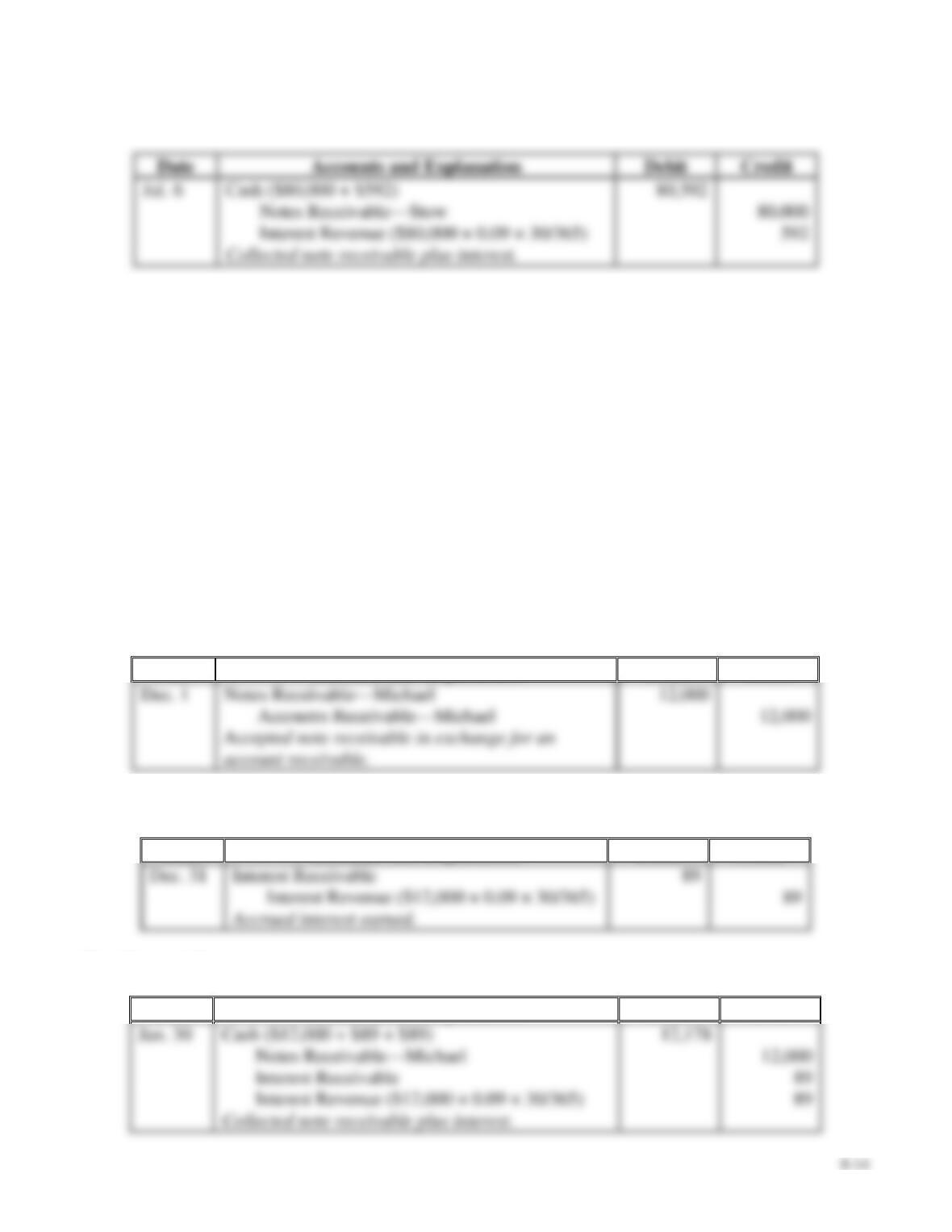

S8-10 Accounting for a note receivable

Learning Objective 4

On June 6, Lakeland Bank & Trust lent $80,000 to Stephan Stow on a 30-day, 9% note.

Requirements

1. Journalize for Lakeland the lending of the money on June 6.

2. Journalize the collection of the principal and interest at maturity. Specify the date. Round to the

nearest dollar.

SOLUTION

Requirement 1

Date

Accounts and Explanation

Debit

Credit

Date

Debit

Credit

S8-10, cont.

Requirement 2

S8-11 Accruing interest revenue and recording collection of a note

Learning Objective 4

On December 1, Kyle Corporation accepted a 60-day, 9%, $12,000 note receivable from J. Michael in

exchange for his account receivable.

Requirements

1. Journalize the transaction on December 1.

2. Journalize the adjusting entry needed on December 31 to accrue interest revenue. Round to the

nearest dollar.

3. Journalize the collection of the principal and interest at maturity. Specify the date. Round to the

nearest dollar.

SOLUTION

Requirement 1

Date

Accounts and Explanation

Debit

Credit

Requirement 2

Date

Accounts and Explanation

Debit

Credit

Requirement 3

Date

Accounts and Explanation

Debit

Credit

8-15

S8-12 Recording a dishonored note receivable

Learning Objective 4

cKale Corporation has a three-month, $18,000, 9% note receivable from L. Peters that was signed on

June 1, 2018. Peters defaults on the loan on September 1.

Journalize the entry for McKale to record the default of the loan

SOLUTION

Date

Accounts and Explanation

Debit

Credit

2018

Sep. 1

Accounts Receivable—Peters

S8-13 Using the acid-test ratio, accounts receivable turnover ratio, and days’ sales in receivables to

evaluate a company

Learning Objective 5

Silver Clothiers reported the following selected items at April 30, 2018 (last year’s—2017—amounts

also given as needed):

Accounts Payable

$ 328,000

Accounts Receivable,

net:

Cash

573,720

April 30, 2018

$ 11,000

Merchandise Inventory:

April 30, 2017

165,000

April 30, 2018

250,000

Cost of Goods Sold

1,200,000

April 30, 2017

210,000

Short-term Investments

148,000

Net Credit Sales

Revenue

3,212,000

Other Current Assets

100,000

Long-term Assets

350,000

Other Current

Liabilities

188,000

Long-term Liabilities

130,000

Compute Silver’s (a) acid–test ratio, (b) accounts receivable turnover ratio, and (c) days’ sales in

receivables for the year ending April 30, 2018. Evaluate each ratio value as strong or weak. Silver sells

on terms of net 30. (Round days’ sales in receivables to a whole number.)

SOLUTION

a) Acid-test ratio = (Cash including cash equivalents + Short-term investments + Net current

receivables) / Total current liabilities

Exercises

E8-14 Defining common receivables terms

Learning Objective 1

Match the terms with their correct definition.

Terms

Definitions

1. Accounts receivable

2. Other receivables

3. Debtor

4. Notes receivable

5. Maturity date

6. Creditor

a.

The party to a credit transaction who takes on an

obligation/payable.

b.

The party who receives a receivable and will collect cash

in the future.

c. A written promise to pay a specified amount of money at

a particular future date.

d.

The date when the note receivable is due.

e. A miscellaneous category that includes any other type of

receivable where there is a right to receive cash in the

future.

f. The right to receive cash in the future from customers for

goods sold or for services performed.

SOLUTION

1.

F

2.

E

3.

A

4.

C

5.

D

6.

B

8-18

E8-15 Identifying and correcting internal control weakness

Learning Objective 1

Suppose The Right Rig Dealership is opening a regional office in Omaha. Cary Regal, the office

manager, is designing the internal control system. Regal proposes the following procedures for credit

checks on new customers, sales on account, cash collections, and write-offs of uncollectible receivables:

• The credit department runs a credit check on all customers who apply for credit. When an

account proves uncollectible, the credit department authorizes the write-off of the accounts

receivable.

• Cash receipts come into the credit department, which separates the cash received from the

customer remittance slips. The credit department lists all cash receipts by customer name and

amount of cash received.

• The cash goes to the treasurer for deposit in the bank. The remittance slips go to the accounting

department for posting to customer accounts.

• The controller compares the daily deposit slip to the total amount posted to customer accounts.

Both amounts must agree.

Recall the components of internal control. Identify the internal control weakness in this situation, and

propose a way to correct it.

SOLUTION

The internal control weakness is that the credit department receives incoming cash from customers.

8-19

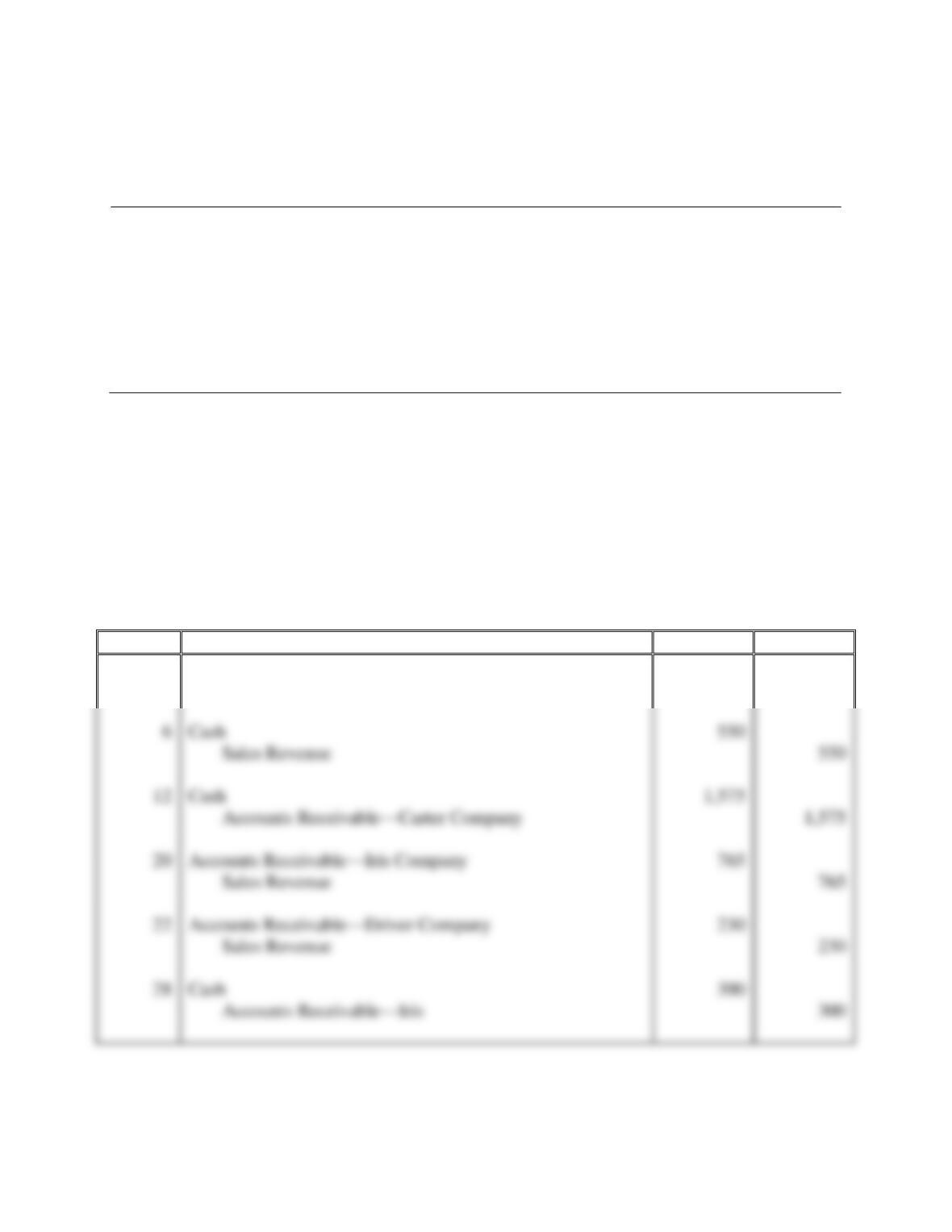

E8-16 Recording credit sales and collections

Learning Objective 1

3. $695

Steller Corporation had the following transactions in June:

Jun. 1

Sold merchandise inventory on account to Carter Company, $1,575.

6

Sold merchandise inventory for cash, $550.

12

Received cash from Carter Company in full settlement of its accounts receivable.

20

Sold merchandise inventory on account to Iris Company, $765.

22

Sold merchandise inventory on account to Driver Company, $230.

28

Received cash from Iris Company in partial settlement of its accounts receivable, $300.

Requirements

1. Journalize the transactions. Ignore Cost of Goods Sold. Omit explanations.

2. Post the transactions to the general ledger and the accounts receivable subsidiary ledger. Assume all

beginning balances are $0.

3. Verify the ending balance in the control Accounts Receivable equals the sum of the balances in the

subsidiary ledger.

Requirement 1

Date

Accounts and Explanation

Debit

Credit

Jun. 1

Accounts Receivable—Carter Company

1,575

Sales Revenue

1,575

Cash

Sales Revenue

Cash

1,575

Accounts Receivable—Carter Company

1,575

Accounts Receivable—Iris Company

Sales Revenue

Accounts Receivable—Driver Company

Sales Revenue

Cash

Accounts Receivable—Iris

8-20

Requirement 2

GENERAL LEDGER

SUBSIDIARY LEDGER

Cash

Accounts Receivable—Carter

Jun. 6

550

Jun. 1

1,575

1,575

Jun. 12

12

1,575

Bal.

0

Requirement 3

Control Account—Accounts Receivable

$ 695

Subsidiary Ledger:

$ 0

$ 695

E8-17 Journalizing transactions using the direct write-off method

Learning Objectives 1, 2

On June 1, 2018, Best Performance Cell Phones sold $21,000 of merchandise to Anthony Trucking

Company on account. Anthony fell on hard times and on July 15 paid only $5,000 of the account

receivable. After repeated attempts to collect, Best Performance finally wrote off its accounts

receivable from Anthony on September 5. Six months later, March 5, 2019, Best Performance

received Anthony’s check for $16,000 with a note apologizing for the late payment.

Requirements

1. Journalize the transactions for Best Performance Cell Phones using the direct write-off method.

Ignore Cost of Goods Sold.

2. What are some limitations that Best Performance will encounter when using the direct write-off

method?

28

300

Bal.

2,425

Jun. 22

230

Bal.

230

Jun. 1

1,575

1,575

Jun. 12

20

765

300

28

22

230

Jun. 20

765

300

Jun. 28

Bal.

695

Bal.

465

1,575

Jun. 1

550

6

765

20

230

22

3,120

Bal.

Use the following information to answer Exercises E8-18 and E8-19.

At January 1, 2018, Hilltop Flagpoles had Accounts Receivable of $28,000, and Allowance for Bad

Debts had a credit balance of $3,000. During the year, Hilltop Flagpoles recorded the following:

a. Sales of $185,000 ($164,000 on account; $21,000 for cash). Ignore Cost of Goods Sold.

b. Collections on account, $135,000.

c. Write-offs of uncollectible receivables, $2,300.

SOLUTION

Requirement 1

Date

Accounts and Explanation

Debit

Credit

2018

Jun. 1

Accounts Receivable—Anthony Trucking Company

21,000

Sales Revenue

21,000

Record sales on account.

Cash

Accounts Receivable—Anthony Trucking Company

Bad Debts Expense

16,000

Accounts Receivable—Anthony Trucking Company

16,000

2019

Accounts Receivable—Anthony Trucking Company

16,000

Bad Debts Expense

16,000

Cash

16,000

Accounts Receivable—Anthony Trucking Company

16,000

Requirement 2

Best Performance will encounter limitations with the direct write-off method because it violates the

matching principle. The matching principle requires that the expense of uncollectible accounts be

8-22

E8-18 Accounting for uncollectible accounts using the allowance method (percent-of-sales) and

reporting receivables on the balance sheet

Learning Objectives 1, 3

2. AR, Dec. 31 $54,700

Requirements

1. Journalize Hilltop’s transactions that occurred during 2018. The company uses the allowance

method.

2. Post Hilltop’s transactions to the Accounts Receivable and Allowance for Bad Debts T-accounts.

3. Journalize Hilltop’s adjustment to record bad debts expense assuming Hilltop estimates bad debts as

3% of credit sales. Post the adjustment to the appropriate T-accounts.

4. Show how Hilltop Flagpoles will report net accounts receivable on its December 31, 2018, balance

sheet.

SOLUTION

Requirement 1

Date

Accounts and Explanation

Debit

Credit

2018

a.

Accounts Receivable

164,000

Cash

21,000

Requirement 2

Accounts Receivable

Jan. 1, 2018, Bal.

28,000

135,000

Collections

Net credit sales

2,300

Write-offs

Dec. 31, 2018, Bal.

3,000

Jan. 1, 2018, Bal.

Write-offs

700

Unadj. Bal.

185,000

Cash

135,000

135,000

c.

Allowance for Bad Debts

E8-18, cont.

Requirement 3

Date

Accounts and Explanation

Debit

Credit

2018

Dec. 31

Bad Debts Expense

4,920

4,920

3,000

Jan. 1, 2018, Bal.

Write-offs

700

Unadj. Bal.

4,920

Adj.

5,620

Dec. 31, 2018, Bal.

Jan. 1, 2018, Bal.

Adj.

Dec. 31, 2018, Bal.

Requirement 4

HILLTOP FLAGPOLES

Balance Sheet−Partial

December 31, 2018

Current Assets:

Accounts Receivable

8-24

E8-19 Accounting for uncollectible accounts using the allowance method (percent-of-receivables)

and reporting receivables on the balance sheet

Learning Objectives 1, 3

3. Bad Debts Expense $4,770

Requirements

1. Journalize Hilltop’s transactions that occurred during 2018. The company uses the allowance

method.

2. Post Hilltop’s transactions to the Accounts Receivable and Allowance for Bad Debts T-accounts.

3. Journalize Hilltop’s adjustment to record bad debts expense assuming Hilltop estimates bad debts as

10% of accounts receivable. Post the adjustment to the appropriate T-accounts.

4. Show how Hilltop Flagpoles will report net accounts receivable on its December 31, 2018, balance

sheet.

SOLUTION

Requirement 1

Date

Accounts and Explanation

Debit

Credit

2018

a.

Accounts Receivable

164,000

Requirement 2

Accounts Receivable

Jan. 1, 2018, Bal.

28,000

135,000

Collections

Dec. 31, 2018, Bal.

3,000

Jan. 1, 2018, Bal.

Write-offs

700

Unadj. Bal.

Cash

185,000

Cash

135,000

135,000

c.

Allowance for Bad Debts

E8-19, cont.

Requirement 3

Date

Accounts and Explanation

Debit

Credit

2018

Dec. 31

Bad Debts Expense

3,000

Jan. 1, 2018, Bal.

Write-offs

700

Unadj. Bal.

4,770

Adj.

5,470

Dec. 31, 2018, Bal.

Jan. 1, 2018, Bal.

Adj.

Dec. 31, 2018, Bal.

Requirement 4

HILLTOP FLAGPOLES

Balance Sheet−Partial

December 31, 2018

Assets

Current Assets:

Accounts Receivable

$ 54,700

$ 49,230

8-26

E8-20 Accounting for uncollectible accounts using the allowance method (aging-of-receivables)

and reporting receivables on the balance sheet

Learning Objective 3

2. Allowance CR Bal. $25,360

At December 31, 2018, the Accounts Receivable balance of GPS Technology is $200,000. The

Allowance for Bad Debts account has a $24,110 debit balance. GPS Technology prepares the following

aging schedule for its accounts receivable:

Age of Accounts

1–30

Days

31–60

Days

61–90

Days

Over 90

Days

Accounts Receivable

$ 65,000

$ 50,000

$ 40,000

$ 45,000

Estimated percent

uncollectible

0.4%

3.0%

5.0%

48.0%

Requirements

1. Journalize the year-end adjusting entry for bad debts on the basis of the aging schedule. Show the T-

account for the Allowance for Bad Debts at December 31, 2018.

2. Show how GPS Technology will report its net accounts receivable on its December 31, 2018, balance

sheet.

SOLUTION

Requirement 1

Age of Accounts Receivable

1 – 30

Days

31 – 60

Days

61 – 90

Days

Over 90

Days

Total Receivables

Accounts

Receivable

$ 65,000

$ 50,000

$ 40,000

$ 45,000

$200,000

Percent

uncollectible

Estimated total

uncollectible

$ 1,500

$ 2,000

$ 21,600

$ 25,360 (Target

Balance)

Dec. 31

Bad Debts Expense

Requirement 2

Allowance for Bad Debts

Unadj. Bal.

24,110

49,470

Adj.

25,360

Bal.

Current Assets:

Accounts Receivable

$ 174,640

E8-21 Journalizing transactions using the direct write-off method versus the allowance method

Learning Objectives 1, 2, 3

During August 2018, Lima Company recorded the following:

• Sales of $133,300 ($122,000 on account; $11,300 for cash). Ignore Cost of Goods Sold.

• Collections on account, $106,400.

• Write-offs of uncollectible receivables, $990.

• Recovery of receivable previously written off, $800.

Requirements

1. Journalize Lima’s transactions during August 2018, assuming Lima uses the direct write-off method.

2. Journalize Lima’s transactions during August 2018, assuming Lima uses the allowance method.

SOLUTION

Requirement 1

Date

Accounts and Explanation

Debit

Credit

2018

Aug.

Accounts Receivable

122,000

Cash

11,300

Sales Revenue

133,300

Recorded sales for the month.

Cash

106,400

106,400

Bad Debts Expense

Accounts Receivable

Cash

8-29

E8-21, cont.

Requirement 2

Date

Accounts and Explanation

Debit

Credit

2018

Aug.

Accounts Receivable

122,000

Cash

11,300

Sales Revenue

133,300

Record sales for the month.

Cash

106,400

106,400

Allowance for Bad Debts

Accounts Receivable

Cash

E8-22 Journalizing credit sales, note receivable transactions, and accruing interest

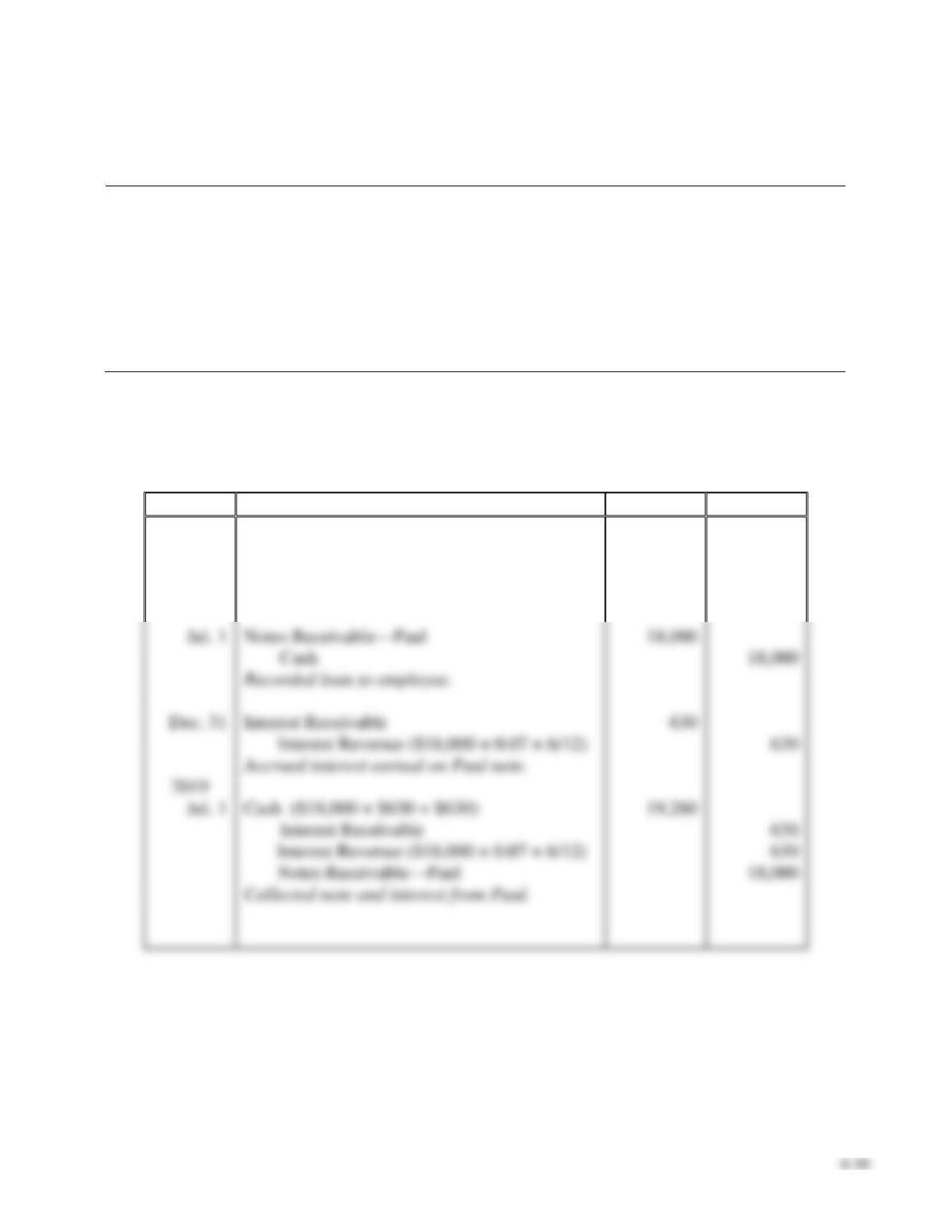

Learning Objectives 1, 4

Endurance Running Shoes reports the following:

2018

May 6

Recorded credit sales of $102,000. Ignore Cost of Goods Sold.

Jul. 1

Loaned $18,000 to Jerry Paul, an executive with the company, on a one-year, 7% note.

Dec. 31

Accrued interest revenue on the Paul note.

2019

Jul. 1

Collected the maturity value of the Paul note.

Journalize all entries required for Endurance Running Shoes.

SOLUTION

Date

Accounts and Explanation

Debit

Credit

2018

May 6

Accounts Receivable

102,000

Sales Revenue

102,000

Recorded credit sales.

Jul. 1

Notes Receivable—Paul

Interest Receivable

Interest Revenue ($18,000 × 0.07 × 6/12)

2019

Jul. 1

Cash ($18,000 + $630 + $630)

Notes Receivable—Paul

E8-23 Journalizing note receivable transactions including a dishonored note

Learning Objective 4

On September 30, 2018, Team Bank loaned $94,000 to Kendall Warner on a one-year, 6% note. Team’s

fiscal year ends on December 31.

Requirements

1. Journalize all entries for Team Bank related to the note for 2018 and 2019.

2. Which party has a

a. note receivable?

b. note payable?

c. interest revenue?

d. interest expense?

3. Suppose that Kendall Warner defaulted on the note. What entry would Team record for the

dishonored note?

SOLUTION

Requirement 1

Date

Accounts and Explanation

Debit

Credit

2018

Sep. 30

Notes Receivable—Kendall Warner

94,000

Cash

94,000

Recorded loan to Kendall Warner.

Interest Receivable

2019

Sep. 30

Cash ($94,000 + $1,410 + $4,230)

99,640

Interest Revenue ($94,000 × 0.06 × 9/12)

94,000

8-32

E8-23, cont.

Requirement 2

a.

note receivable

Team Bank

Requirement 3

Date

Accounts and Explanation

Debit

Credit

2019

Sep. 30

Accounts Receivable—Kendall Warner

E8-24 Journalizing note receivable transactions

Learning Objective 4

Jul. 1, 2019 Cash DR $17,280

The following selected transactions occurred during 2018 and 2019 for Baltic Importers. The company

ends its accounting year on September 30.

2018

Jul. 1

Loaned $16,000 cash to Bud Shyne on a one-year, 8% note.

Sep.

6

Sold goods to Lawn Pro, receiving a 90-day, 6% note for

$11,000. Ignore Cost of Goods Sold.

30

Made a single entry to accrue interest revenue on both notes.

?

Collected the maturity value of the Lawn Pro note.

2019

Jul. 1

Collected the maturity value of the Shyne note.

Journalize all required entries. Make sure to determine the missing maturity date. Round to the nearest

dollar.

note payable

Kendall Warner

c.

interest revenue

Team Bank

interest expense

Kendall Warner

8-33

SOLUTION

Date

Accounts and Explanation

Debit

Credit

2018

Jul. 1

Notes Receivable—Shyne

16,000

Cash

16,000

Recorded loan to Bud Shyne.

Notes Receivable—Lawn Pro

11,000

Sales Revenue

11,000

Interest Receivable

Cash ($11,000 + $43 + $119)

11,162

Interest Receivable

Interest Revenue ($11,000 × 0.06 × 66/365)

11,000

2019

Jul. 1

Cash ($16,000 + $320 + $960)

17,280

Interest Receivable

Interest Revenue ($16,000 × 0.08 × 9/12)

16,000

E8-25 Journalizing note receivable transactions

Learning Objective 4

Oct. 31 Cash DR $18,355

Professional Steam Cleaning performs services on account. When a customer account becomes four

months old, Professional converts the account to a note receivable. During 2018, the company

completed the following transactions:

Apr. 28

Performed service on account for Parkview Club, $18,000.

Sep. 1

Received an $18,000, 60-day, 12% note from Parkview Club in satisfaction

of its past-due account receivable.

Oct. 31

Collected the Parkview Club note at maturity.

Record the transactions in Professional’s journal. Round to the nearest dollar.

SOLUTION

Date

Accounts and Explanation

Debit

Credit

2018

Apr. 28

Accounts Receivable—Parkview Club

18,000

Service Revenue

18,000

Notes Receivable—Parkview Club

18,000

Accounts Receivable—Parkview Club

18,000

Cash ($18,000 + $355)

18,355

Interest Revenue ($18,000 × 0.12 × 60/365)

18,000

8-35

E8-26 Evaluating ratio data

Learning Objective 5

Abanaki Carpets reported the following amounts in its 2018 financial statements. The 2017 figures are

given for comparison.

2018

2017

Balance sheet—partial

Current Assets:

Cash

Short-term Investments

Accounts Receivable

Less: Allowance for Bad Debts

Merchandise Inventory

Prepaid Insurance

Total Current Assets

Total Current Liabilities

Income statement—partial

Net Sales (all on account)

$ 64,000

(7,000)

$ 5,000

25,000

57,000

194,000

2,000

283,000

105,000

742,400

$ 77,000

(6,000)

$ 11,000

14,000

71,000

190,000

2,000

288,000

107,000

730,000

Requirements

1. Calculate Abanaki’s acid–test ratio for 2018. (Round to two decimals.) Determine whether Abanaki’s

acid-test ratio improved or deteriorated from 2017 to 2018. How does Abanaki’s acid-test ratio

compare with the industry average of 0.80?

2. Calculate Abanaki’s accounts receivable turnover ratio. (Round to two decimals.) How does

Abanaki’s ratio compare to the industry average accounts receivable turnover of 10?

3. Calculate the days’ sales in receivables for 2018. (Round to the nearest day.) How do the results

compare with Abanaki’s credit terms of net 30?

8-36

SOLUTION

Requirement 1

Acid-test ratio = (Cash including cash equivalents + Short-term investments + Net current

receivables) / Total current liabilities

2018

Requirement 2

Accounts receivable turnover ratio = Net credit sales / Average net accounts receivable

2018 = $742,400 / [($57,000 +$71,000) / 2]

Requirement 3

Days’ sales in receivables = 365 days / Accounts receivable turnover ratio

8-37

E8-27 Computing the collection period for receivables

Learning Objective 5

Unique Media Sign Incorporated sells on account. Recently, Unique reported the following figures:

2018

2017

Net Credit Sales

$ 594,920

$

602,000

Net Receivables at end of

year

38,500

47,100

Requirements

1. Compute Unique’s days’ sales in receivables for 2018. (Round to the nearest day.)

2. Suppose Unique’s normal credit terms for a sale on account are 2/10, net 30. How well does

Unique’s collection period compare to the company’s credit terms? Is this good or bad for Unique?

SOLUTION

Requirement 1

Accounts receivable turnover ratio = Net credit sales / Average net accounts receivables

2018 = $594,920 / [($38,500 + $47,100) / 2]

Requirement 2

8-38

Problems (Group A)

P8-28A Accounting for uncollectible accounts using the allowance (percent-of-sales) and direct

write-off methods and reporting receivables on the balance sheet

Learning Objectives 1, 2, 3

1. Bad Debts Expense $11,000

On August 31, 2018, Bouquet Floral Supply had a $140,000 debit balance in Accounts Receivable

and a $5,600 credit balance in Allowance for Bad Debts. During September, Bouquet made:

• Sales on account, $550,000. Ignore Cost of Goods Sold.

• Collections on account, $584,000.

• Write-offs of uncollectible receivables, $4,000.

Requirements

1. Journalize all September entries using the allowance method. Bad debts expense was estimated at 2%

of credit sales. Show all September activity in Accounts Receivable, Allowance for Bad Debts, and Bad

Debts Expense (post to these T-accounts).

2. Using the same facts, assume that Bouquet used the direct write-off method to account for

uncollectible receivables. Journalize all September entries using the direct write-off method. Post to

Accounts Receivable and Bad Debts Expense, and show their balances at September 30, 2018.

3. What amount of Bad Debts Expense would Bouquet report on its September income statement under

each of the two methods? Which amount better matches expense with revenue? Give your reason.

4. What amount of net accounts receivable would Bouquet report on its September 30, 2018, balance

sheet under each of the two methods? Which amount is more realistic? Give your reason.

SOLUTION

Requirement 1

Date

Accounts and Explanation

Debit

Credit

2018

Sep. 30

Accounts Receivable

550,000

Sales Revenue

550,000

Cash

584,000

584,000

Allowance for Bad Debts

Bad Debts Expense

584,000

4,000

5,600

11,000

12,600

8-40

P8-28A, cont.

Requirement 2

Date

Accounts and Explanation

Debit

Credit

2018

Sep. 30

Accounts Receivable

550,000

Sales Revenue

550,000

Requirement 3

Income Statement

Allowance

Method

Direct Write-

Off Method

Bad Debts Expense

$ 11,000

$ 4,000

Requirement 4

Balance Sheet

Allowance

Method

Direct Write-

Off Method

Accounts Receivable

Less: Allowance for Bad Debts

Accounts Receivable, net

Cash

584,000

584,000

Bad Debts Expense

584,000

4,000

4,000

4,000

8-41

P8-29A Accounting for uncollectible accounts using the allowance method (aging-of-receivables)

and reporting receivables on the balance sheet

Learning Objectives 1, 3

2. Allowance CR Bal. $8,482 at Dec. 31, 2018

At September 30, 2018, the accounts of Green Terrace Medical Center (GTMC) include the following:

Accounts Receivable

$ 145,000

Allowance for Bad Debts (credit

balance)

3,500

During the last quarter of 2018, GTMC completed the following selected transactions:

• Sales on account, $450,000. Ignore Cost of Goods Sold.

• Collections on account, $427,100

• Wrote off accounts receivable as uncollectible: Regan, Co., $1,400; Owen Reis, $800; and

Patterson, Inc., $700

• Recorded bad debts expense based on the aging of accounts receivable, as follows:

Age of Accounts

1–30 Days

31–60 Days

61–90 Days

Over 90 Days

Accounts Receivable

$ 104,000

$ 39,000

$ 14,000

$ 8,000

Estimated percent uncollectible

0.3%

3%

30%

35%

Requirements

1. Open T-accounts for Accounts Receivable and Allowance for Bad Debts. Journalize the transactions

(omit explanations) and post to the two accounts.

2. Show how Green Terrace Medical Center should report net accounts receivable on its December 31,

2018, balance sheet.

SOLUTION

Requirement 1

Date

Accounts and Explanation

Debit

Credit

2018

Accounts Receivable

450,000

Sales Revenue

450,000

Cash

427,100

Accounts Receivable

427,100

Allowance for Bad Debts

Accounts Receivable—Regan, Co.

Accounts Receivable—Owen Reiss

Bad Debts Expense

Age of Accounts Receivable

1 – 30

Days

31 – 60

Days

61 – 90

Days

Over 90

Days

Total Receivables

Accounts

Receivable

$104,000

$39,000

$14,000

$ 8,000

$165,000

uncollectible

Estimated total

uncollectible

$ 312

$ 1,170

$ 4,200

$ 2,800

$8,482 (Target Balance)

427,100

2,900

3,500

600

7,882

8,482

Percent

× 0.3%

× 3.0%

× 30.0%

× 35.0%

8-43

P8-29A, cont.

Requirement 2

GREEN TERRACE MEDICAL CENTER

Balance Sheet−Partial

December 31, 2018

P8-30A Accounting for uncollectible accounts using the allowance method (percent-of-sales) and

reporting receivables on the balance sheet

Learning Objectives 1, 3

2. Net AR $119,800

Delta Watches completed the following selected transactions during 2018 and 2019:

2018

Dec. 31

Estimated that bad debts expense for the year was 2% of credit sales of

$450,000 and recorded that amount as expense. The company uses the

allowance method.

31

Made the closing entry for bad debts expense.

2019

Jan. 17

Sold merchandise inventory to Mack Smith, $400, on account. Ignore Cost

of Goods Sold.

Jun. 29

Wrote off Mack Smith’s account as uncollectible after repeated efforts to

collect from him.

Aug. 6

Received $400 from Mack Smith, along with a letter apologizing for being

so late. Reinstated Smith’s account in full and recorded the cash receipt.

Dec. 31

Made a compound entry to write off the following accounts as

uncollectible: Cam Carter, $1,400; Mike Venture, $1,200; and Russell

Reeves, $400.

31

Estimated that bad debts expense for the year was 2% on credit sales of

$510,000 and recorded the expense.

31

Made the closing entry for bad debts expense.

Requirements

1. Open T-accounts for Allowance for Bad Debts and Bad Debts Expense, assuming the accounts begin

with a zero balance. Record the transactions in the general journal (omit explanations), and post to

the two T-accounts.

2. Assume the December 31, 2019, balance of Accounts Receivable is $136,000. Show how net

accounts receivable would be reported on the balance sheet at that date.

SOLUTION

Requirement 1

Date

Accounts and Explanation

Debit

Credit

2018

Dec. 31

Bad Debts Expense

9,000

Allowance for Bad Debts

9,000

(2% × $450,000 = $9,000)

Income Summary

9,000

Bad Debts Expense

9,000

2019

Accounts Receivable—Mack Smith

Allowance for Bad Debts

Accounts Receivable—Mack Smith

Accounts Receivable—Mack Smith

Allowance for Bad Debts

Cash

Accounts Receivable—Mack Smith

Dec. 31

Allowance for Bad Debts

3,000

1,400

1,200

Accounts Receivable—Russell Reeves

Bad Debts Expense

Allowance for Bad Debts

(2% × $510,000 = $10,200)

Income Summary

Bad Debts Expense

8-45

P8-30A, cont.

Requirement 1, cont.

Allowance for Bad Debts

0

Beginning Bal.

9,000

Dec. 31, Adj.

9,000

Dec. 31, 2018, Bal.

Bad Debts Expense

Beginning Bal.

0

Dec. 31, Adj.

9,000

Adj. Bal.

9,000

9,000

Dec. 31, Closing

Dec. 31, 2018, Bal.

0

Dec. 31, 2019, Adj.

Adj. Bal.

10,200

Dec. 31, Closing

Dec. 31, 2019, Bal.

0

Requirement 2

DELTA WATCHES

Balance Sheet−Partial

December 31, 2019

Assets

Current Assets:

Accounts Receivable

$ 119,800

Jun. 29, Write-off

400

Aug. 6, Reinstate

Dec. 31, Write-offs

3,000

10,200

Dec. 31, Adj.

16,200

Dec. 31, 2019, Bal.

8-46

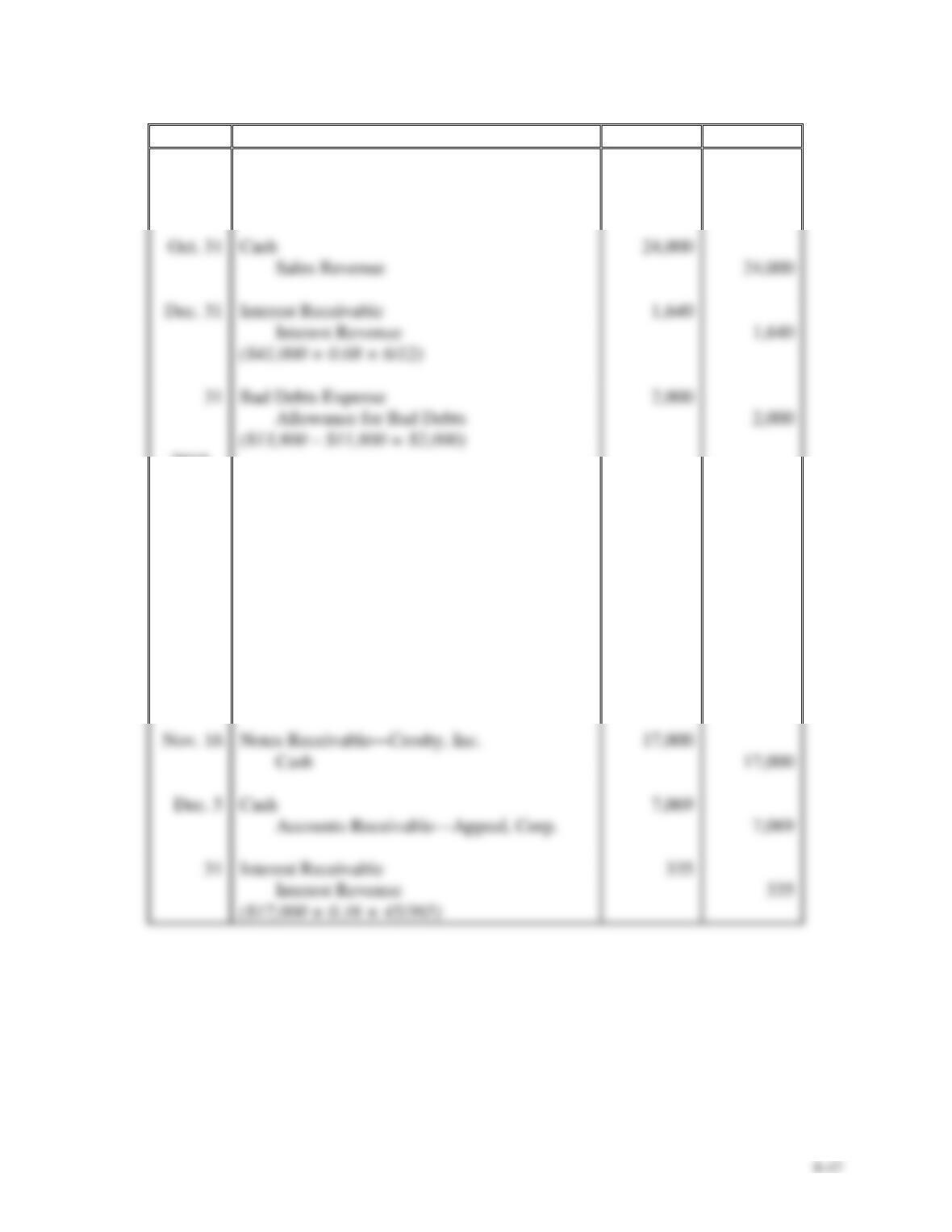

P8-31A Accounting for uncollectible accounts (aging-of-receivables method), notes receivable, and

accrued interest revenue

Learning Objectives 1, 3, 4

Dec. 31, 2018 Interest Receivable $1,640

Sleepy Recliner Chairs completed the following selected transactions:

2018

Jul. 1

Sold merchandise inventory to Stan-Mart, receiving a $41,000, nine-month,

8% note. Ignore Cost of Goods Sold.

Oct. 31

Recorded cash sales for the period of $24,000. Ignore Cost of Goods Sold.

Dec. 31

Made an adjusting entry to accrue interest on the Stan-Mart note.

31

Made an adjusting entry to record bad debts expense based on an aging of

accounts receivable. The aging schedule shows that $13,800 of accounts

receivable will not be collected. Prior to this adjustment, the credit balance

in Allowance for Bad Debts is $11,800.

2019

Apr. 1

Collected the maturity value of the Stan-Mart note.

Jun. 23

Sold merchandise inventory to Appeal, Corp., receiving a 60-day, 6% note

for $7,000. Ignore Cost of Goods Sold.

Aug.

22

Appeal, Corp. dishonored its note at maturity; the business converted the

maturity value of the note to an account receivable.

Nov.

16

Loaned $17,000 cash to Crosby, Inc., receiving a 90-day, 16% note.

Dec. 5

Collected in full on account from Appeal, Corp.

31

Accrued the interest on the Crosby, Inc. note.

Record the transactions in the journal of Sleepy Recliner Chairs. Explanations are not required. (Round

to the nearest dollar.)

SOLUTION

Date

Accounts and Explanation

Debit

Credit

2018

Jul. 1

Notes Receivable—Stan-Mart

41,000

Sales Revenue

41,000

Cash

24,000

Sales Revenue

24,000

Interest Receivable

1,640

Interest Revenue

1,640

Bad Debts Expense

2,000

Allowance for Bad Debts

2,000

2019

Apr. 1

Cash ($41,000 + $1,640 + $820)

43,460

Interest Receivable

1,640

Interest Revenue ($41,000 × 0.08 × 3/12)

820

Notes Receivable—Stan-Mart

41,000

Jun. 23

Notes Receivable—Appeal, Corp.

7,000

Sales Revenue

7,000

Aug. 22

Accounts Receivable—Appeal, Corp.

7,069

Interest Revenue ($7,000 × 0.06 × 60/365)

69

Notes Receivable – Appeal, Corp.

7,000

Nov. 16

Notes Receivable—Crosby, Inc.

17,000

Cash

17,000

Dec. 5

Cash

7,069

Accounts Receivable—Appeal, Corp.

7,069

Interest Receivable

335

Interest Revenue

335

8-48

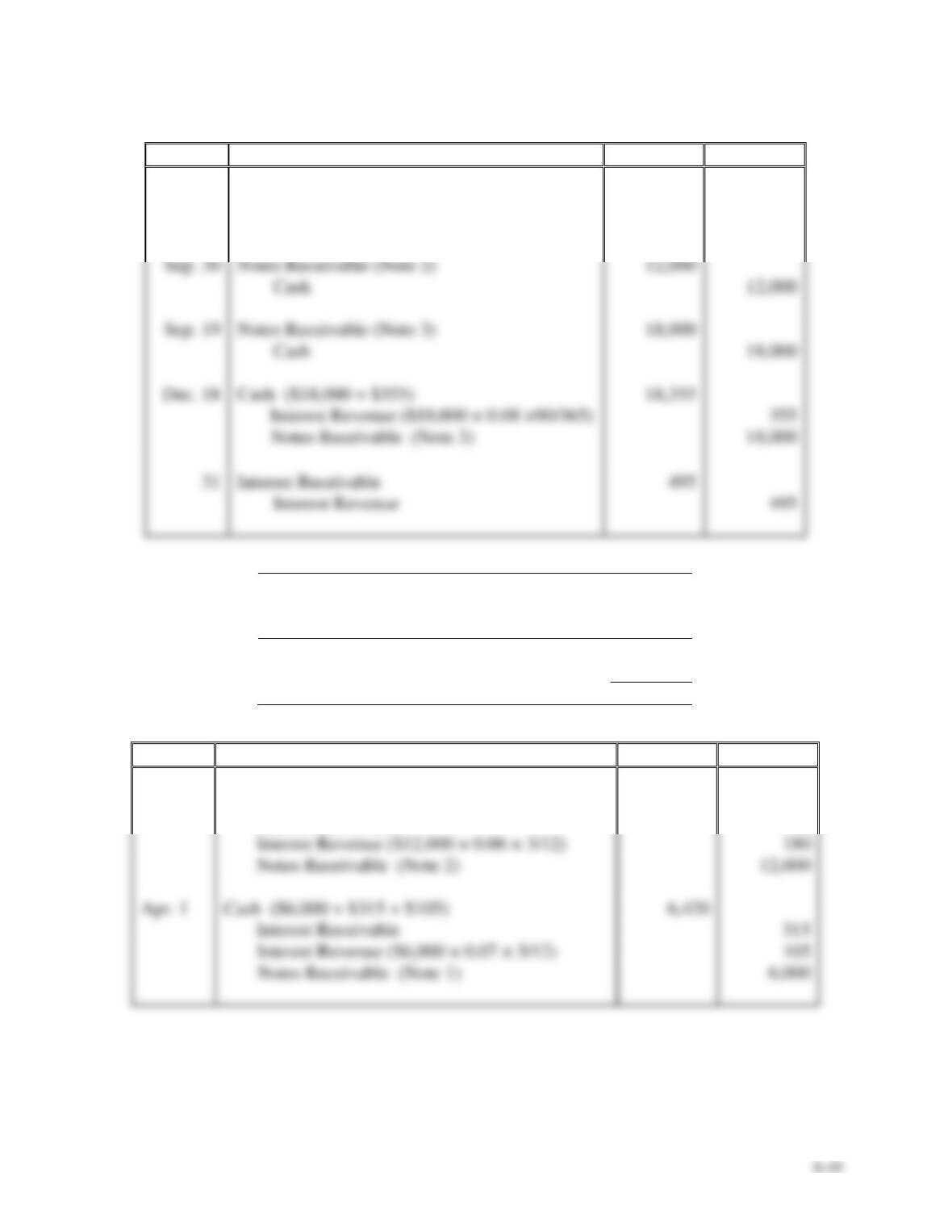

P8-32A Accounting for notes receivable and accruing interest

Learning Objective 4

1. Note 3 Dec. 18, 2018

Carley Realty loaned money and received the following notes during 2018.

Note

Date

Principal

Amount

Interest

Rate

Term

(1)

Apr. 1

$ 6,000

7%

1 year

(2)

Sep. 30

12,000

6%

6

months

(3)

Sep. 19

18,000

8%

90 days

Requirements

1. Determine the maturity date and maturity value of each note.

2. Journalize the entries to establish each Note Receivable and to record collection of principal and

interest at maturity. Include a single adjusting entry on December 31, 2018, the fiscal year-end, to

record accrued interest revenue on any applicable note. Explanations are not required. Round to the

nearest dollar.

SOLUTION

Requirement 1

Principal

Interest

Rate

Interest

Period

Interest

Revenue

Earned

Maturity

Value

(P + I)

Maturity

Date

$ 6,420

Note 2

× 6/12

Note 3

× 90/365

Dec. 18,

Requirement 2

Date

Accounts and Explanation

Debit

Credit

2018

Apr. 1

Notes Receivable (Note 1)

6,000

Cash

6,000

Notes Receivable (Note 2)

12,000

Cash

12,000

Notes Receivable (Note 3)

18,000

Cash

18,000

Dec. 18

Cash ($18,000 + $355)

18,355

Interest Revenue ($18,000 × 0.08 ×90/365)

18,000

Interest Receivable

Interest Revenue

Principal

Interest

Rate

Interest

Period

Interest

Revenue

Earned

Note 1

$ 6,000

× 0.07

× 9/12

$ 315

Note 2

12,000

× 0.06

× 3/12

180

$ 495

Date

Accounts and Explanation

Debit

Credit

2019

Mar. 30

Cash ($12,000 + $180 + $180)

12,360

Interest Receivable

180

Interest Revenue ($12,000 × 0.06 × 3/12)

180

Notes Receivable (Note 2)

12,000

Apr. 1

Cash ($6,000 + $315 + $105)

Interest Receivable

315

Interest Revenue ($6,000 × 0.07 × 3/12)

105

8-50

P8-33A Accounting for notes receivable, dishonored notes, and accrued interest revenue

Learning Objective 4

Dec. 31, 2018 Income Summary CR $74

Consider the following transactions for CC Publishing.

2018

Dec.

6

Received a $18,000, 90-day, 6% note in settlement of an overdue

accounts receivable from Go Go Publishing.

31

Made an adjusting entry to accrue interest on the Go Go Publishing

note.

31

Made a closing entry for interest revenue.

2019

Mar.

6

Collected the maturity value of the Go Go Publishing note.

Jun.

30

Loaned $11,000 cash to Lincoln Music, receiving a six-month, 20%

note.

Oct. 2

Received a $2,400, 60-day, 20% note for a sale to Tusk Music. Ignore

Cost of Goods Sold.

Dec.

1

Tusk Music dishonored its note at maturity.

1

Wrote off the receivable associated with Tusk Music. (Use the

allowance method.)

30

Collected the maturity value of the Lincoln Music note.

Journalize all transactions for CC Publishing. Round all amounts to the nearest dollar.

8-51

SOLUTION

Date

Accounts and Explanation

Debit

Credit

2018

Dec. 6

Notes Receivable—Go Go Publishing

18,000

Accounts Receivable—Go Go Publishing

18,000

Jun. 30

Notes Receivable—Lincoln Music

11,000

Cash

11,000

Oct. 2

Notes Receivable—Tusk Music

2,400

Sales Revenue

2,400

Dec. 1

Accounts Receivable—Tusk Music

2,479

Interest Revenue ($2,400 × 0.20 × 60/365)

79

Notes Receivable—Tusk Music

2,400

1

Allowance for Bad Debts

2,479

Accounts Receivable—Tusk Music

2,479

Cash

12,100

Interest Revenue ($11,000 × 0.20 × 6/12)

1,100

Notes Receivable—Lincoln Music

11,000

Interest Receivable

74

Interest Revenue ($18,000 × 0.06 × 25/365)

74

Interest Revenue

74

Income Summary

74

2019

Cash

18,266

Interest Receivable

74

Interest Revenue ($18,000 × 0.06 × 65/365)

Notes Receivable—Go Go Publishing

18,000

8-52

P8-34A Using ratio data to evaluate a company’s financial position

Learning Objective 5

1. Acid-test ratio (2018) 0.88

The comparative financial statements of Norfolk Cosmetic Supply for 2018, 2017, and 2016 include the

data shown here:

2018

2017

2016

Balance sheet—partial

Current Assets:

Cash

Short-term investments

Accounts Receivable, Net

Merchandise Inventory

Prepaid Expenses

Total Current Assets

Total Current Liabilities

Income statement—partial

Net Sales (all on account)

$ 70,000

140,000

280,000

355,000

70,000

915,000

560,000

5,890,000

$ 60,000

170,000

240,000

330,000

35,000

835,000

630,000

5,130,000

$ 50,000

120,000

260,000

310,000

35,000

775,000

640,000

4,210,000

Requirements

1. Compute these ratios for 2018 and 2017:

a. Acid-test ratio (Round to two decimals.)

b. Accounts receivable turnover (Round to two decimals.)

c. Days’ sales in receivables (Round to the nearest whole day.)

2. Considering each ratio individually, which ratios improved from 2017 to 2018 and which ratios

deteriorated? Is the trend favorable or unfavorable for the company?

8-53

SOLUTION

Requirement 1

a. Acid-test ratio = (Cash including cash equivalents + Short-term investments + Net current

receivables) / Total current liabilities

2018

b. Accounts receivable turnover ratio = Net credit sales / Average net accounts receivables

c. Days’ sales in receivables = 365 days / Accounts receivable turnover ratio

2018 = 365 days / 22.65

Requirement 2

The acid-test ratio improved from 2017 to 2018. This trend is favorable to the company.

8-54

Problems (Group B)

P8-35B Accounting for uncollectible accounts using the allowance (percent-of-sales) and direct

write-off methods and reporting receivables on the balance sheet

Learning Objectives 1, 2, 3

1. Sep. 30 Bal. Accounts Receivable $91,000

On August 31, 2018, Forget-Me-Not Floral Supply had a $140,000 debit balance in Accounts

Receivable and a $5,600 credit balance in Allowance for Bad Debts. During September, Forget-Me–Not

made the following transactions:

• Sales on account, $530,000. Ignore Cost of Goods Sold.

• Collections on account, $573,000.

• Write-offs of uncollectible receivables, $6,000.

Requirements

1. Journalize all September entries using the allowance method. Bad debts expense was estimated at 2%

of credit sales. Show all September activity in Accounts Receivable, Allowance for Bad Debts, and

Bad Debts Expense (post to these T-accounts).

2. Using the same facts, assume that Forget-Me-Not used the direct write-off method to account for

uncollectible receivables. Journalize all September entries using the direct write-off method. Post to

Accounts Receivable and Bad Debts Expense, and show their balances at September 30, 2018.

3. What amount of Bad Debts Expense would Forget-Me-Not report on its September income statement

under each of the two methods? Which amount better matches expense with revenue? Give your

reason.

4. What amount of net accounts receivable would Forget-Me-Not report on its September 30, 2018,

balance sheet under each of the two methods? Which amount is more realistic? Give your reason.

SOLUTION

Requirement 1

Date

Accounts and Explanation

Debit

Credit

2018

Sep. 30

Accounts Receivable

530,000

Sales Revenue

530,000

Cash

573,000

Accounts Receivable

573,000

Allowance for Bad Debts

Accounts Receivable

Bad Debts Expense

Allowance for Bad Debts

Accounts Receivable

Aug. 31 Bal.

140,000

573,000

Collections

Net credit sales

530,000

6,000

Write-offs

Sep. 30 Bal.

91,000

5,600

Aug. 31 Bal.

Write-offs

10,600

Adj.

10,200

Sep. 30 Bal.

Adj.

10,600

Sep. 30 Bal.

10,600

8-56

P8-35B, cont.

Requirement 2

Date

Accounts and Explanation

Debit

Credit

2018

Sep. 30

Accounts Receivable

530,000

Sales Revenue

530,000

Accounts Receivable

Aug. 31 Bal.

140,000

573,000

Collections

Net credit sales

530,000

6,000

Write-offs

Sep. 30 Bal.

91,000

Write-offs

Sep. 30 Bal.

Requirement 3

Allowance

Direct Write-

Cash

573,000

Accounts Receivable

573,000

Bad Debts Expense

Accounts Receivable

8-57

P8-35B, cont.

Requirement 4

Balance Sheet

Allowance

Method

Direct Write-

Off Method

Accounts Receivable

$ 91,000

$ 91,000

Less: Allowance for Bad Debts

(10,200)

Accounts Receivable, net

$ 80,800

Net accounts receivable under the allowance method is more realistic because it shows the amount of the

receivables that the company expects to collect.

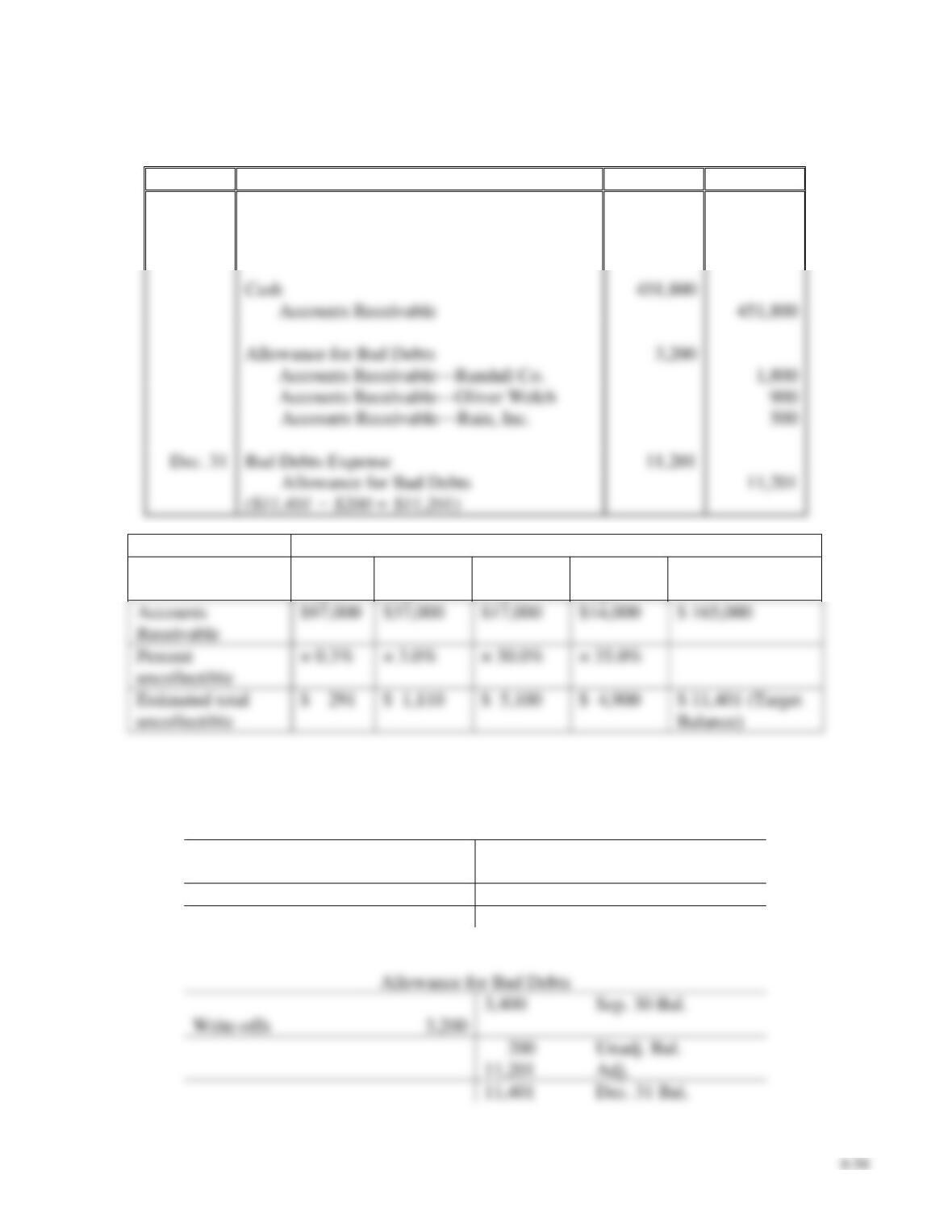

P8-36B Accounting for uncollectible accounts using the allowance method (aging-of-receivables) and

reporting receivables on the balance sheet

Learning Objectives 1, 3

2. Dec. 31, 2018 Allowance CR Bal. $11,401

At September 30, 2018, the accounts of Spring Mountain Medical Center (SMMC) include the

following:

Accounts Receivable

$145,000

Allowance for Bad Debts (credit

balance)

3,400

During the last quarter of 2018, SMMC completed the following selected transactions:

• Sales on account, $475,000. Ignore Cost of Goods Sold.

• Collections on account, $451,800.

• Wrote off accounts receivable as uncollectible: Randall, Co., $1,800; Oliver Welch, $900; and Rain,

Inc., $500

• Recorded bad debts expense based on the aging of accounts receivable, as follows:

Age of Accounts

1–30

Days

31–60

Days

61–90

Days

Over 90

Days

Accounts Receivable

$ 97,000

$ 37,000

$ 17,000

$ 14,000

Estimated percent

uncollectible

0.3%

3%

30%

35%

Requirements

1. Open T-accounts for Accounts Receivable and Allowance for Bad Debts. Journalize the transactions

(omit explanations) and post to the two accounts.

2. Show how Spring Mountain Medical Center should report net accounts receivable on its December

31, 2018, balance sheet.

SOLUTION

Requirement 1

Date

Accounts and Explanation

Debit

Credit

2018

Accounts Receivable

475,000

Sales Revenue

475,000

Cash

451,800

Accounts Receivable

451,800

Allowance for Bad Debts

Accounts Receivable—Randall Co.

Accounts Receivable—Oliver Welch

Accounts Receivable—Rain, Inc.

Bad Debts Expense

11,201

Allowance for Bad Debts

11,201

Age of Accounts Receivable

1 – 30

Days

31 – 60

Days

61 – 90

Days

Over 90

Days

Total Receivables

Accounts

Receivable

$97,000

$37,000

$17,000

$14,000

$ 165,000

Percent

uncollectible

× 0.3%

Estimated total

uncollectible

$ 291

$ 1,110

$ 5,100

$ 4,900

$ 11,401 (Target

Balance)

Requirement 2

Accounts Receivable

Sep. 30 Bal.

145,000

451,800

Collections

Net credit sales

475,000

3,200

Write-offs

Dec. 31 Bal.

165,000

3,400

Sep. 30 Bal.

Write-offs

200

Unadj. Bal.

11,401

Dec. 31 Bal.

8-59

P8-36B, cont.

Requirement 3

SPRING MOUNTAIN MEDICAL CENTER

Balance Sheet−Partial

December 31, 2018

P8-37B Accounting for uncollectible accounts using the allowance method (percent-of-sales) and

reporting receivables on the balance sheet

Learning Objectives 1, 3

1. Dec. 31, 2018, Allowance CR Bal. $12,300

Dialex Watches completed the following selected transactions during 2018 and 2019:

2018

Dec.

31

Estimated that bad debts expense for the year was 3% of credit sales

of $410,000 and recorded that amount as expense. The company

uses the allowance method.

31

Made the closing entry for bad debts expense.

2019

Jan. 17

Sold merchandise inventory to Marty White, $400, on account.

Ignore Cost of Goods Sold.

Jun.

29

Wrote off Marty White’s account as uncollectible after repeated

efforts to collect from him.

Aug. 6

Received $400 from Marty White, along with a letter apologizing

for being so late. Reinstated White’s account in full and recorded

the cash receipt.

Dec.

31

Made a compound entry to write off the following accounts as

uncollectible: Barry Krisp, $1,600; Maria Bryant, $1,100; and

Richard Renik, $400.

31

Estimated that bad debts expense for the year was 3% on credit

sales of $490,000 and recorded the expense.

31

Made the closing entry for bad debts expense.

Requirements

1. Open T-accounts for Allowance for Bad Debts and Bad Debts Expense, assuming the accounts begin

with a zero balance. Record the transactions in the general journal (omit explanations), and post to

the two T-accounts.

2. Assume the December 31, 2019, balance of Accounts Receivable is $136,000. Show how net

accounts receivable would be reported on the balance sheet at that date.

SOLUTION

Requirement 1

Date

Accounts and Explanation

Debit

Credit

2018

Dec. 31

Bad Debts Expense

12,300

Allowance for Bad Debts

12,300

(3% × $410,000 = $12,300)

Income Summary

12,300

Bad Debts Expense

12,300

Accounts Receivable—Marty White

Allowance for Bad Debts

Accounts Receivable—Marty White

Accounts Receivable—Marty White

Allowance for Bad Debts

Cash

Accounts Receivable—Marty White

Dec. 31

Allowance for Bad Debts

Accounts Receivable—Richard Renik

Bad Debts Expense

14,700

Allowance for Bad Debts

14,700

(3% × $490,000 = $14,700)

Income Summary

14,700

Bad Debts Expense

14,700

8-61

P8-37B, cont.

Requirement 1, cont.

Allowance for Bad Debts

0

Beginning Bal.

12,300

Dec. 31, Adj.

Bad Debts Expense

Beginning Bal.

0

Dec. 31, Adj.

12,300

Adj. Bal.

12,300

12,300

Dec. 31, Closing

Dec. 31, 2018, Bal.

0

Dec. 31, 2019, Adj.

14,700

Adj. Bal.

14,700

14,700

Dec. 31, Closing

Dec. 31, 2019, Bal.

0

Requirement 2

DIALEX WATCHES

Balance Sheet−Partial

December 31, 2019

Current Assets:

$ 112,100

12,300

Dec. 31, 2018, Bal.

Jun. 29, Write-off

400

Aug. 6, Reinstate

Dec. 31, Write-offs

14,700

Dec. 31, Adj.

23,900

Dec. 31, 2019, Bal.

8-62

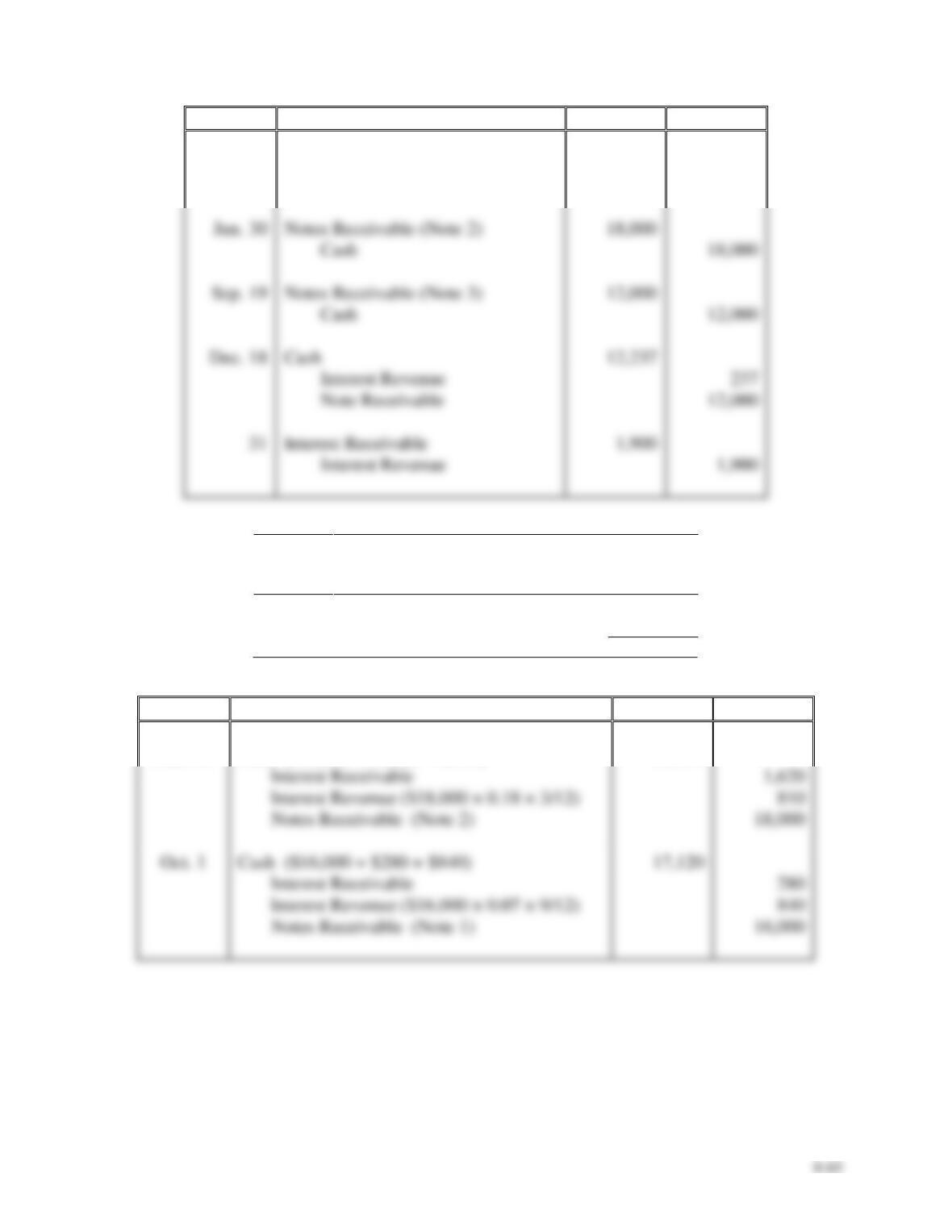

P8-38B Accounting for uncollectible accounts (aging-of-receivables method), notes receivable, and

accrued interest revenue

Learning Objectives 1, 3, 4

Dec. 31, 2018 Bad Debts Expense $4,200

Relax Recliner Chairs completed the following selected transactions:

2018

Jul. 1

Sold merchandise inventory to Go-Mart, receiving a $43,000,

nine-month, 16% note. Ignore Cost of Goods Sold.

Oct. 31

Recorded cash sales for the period of $23,000. Ignore Cost of

Goods Sold.

Dec. 31

Made an adjusting entry to accrue interest on the Go-Mart note.

31

Made an adjusting entry to record bad debts expense based on an

aging of accounts receivable. The aging schedule shows that

$14,900 of accounts receivable will not be collected. Prior to this

adjustment, the credit balance in Allowance for Bad Debts is

$10,700.

2019

Apr. 1

Collected the maturity value of the Go-Mart note.

Jun. 23

Sold merchandise inventory to Allure, Corp., receiving a 60-day,

6% note for $7,000. Ignore Cost of Goods Sold.

Aug. 22

Allure, Corp. dishonored its note at maturity; the business

converted the maturity value of the note to an account receivable.

Nov. 16

Loaned $20,000 cash to Tench, Inc., receiving a 90-day, 8% note.

Dec. 5

Collected in full on account from Allure, Corp.

31

Accrued the interest on the Tench, Inc. note.

Record the transactions in the journal of Relax Recliner Chairs. Explanations are not required. (Round to

the nearest dollar.)

SOLUTION

Date

Accounts and Explanation

Debit

Credit

2018

Jul. 1

Notes Receivable—Go-Mart

43,000

Sales Revenue

43,000

Cash

23,000

Sales Revenue

23,000

Interest Receivable

Interest Revenue

Bad Debts Expense

Allowance for Bad Debts

2019

Cash ($43,000 + $3,440 + $1,720)

48,160

Interest Receivable

Interest Revenue ($43,000 × 0.16 × 3/12)

Notes Receivable—Go-Mart

43,000

Notes Receivable—Allure, Corp.

Sales Revenue

Accounts Receivable—Allure, Corp.

Interest Revenue ($7,000 × 0.06 × 60/365)

Notes Receivable—Allure, Corp.

Notes Receivable—Tench, Inc.

20,000

Cash

20,000

Cash

Accounts Receivable—Allure, Corp.

Interest Receivable

Interest Revenue

8-64

P8-39B Accounting for notes receivable and accruing interest

Learning Objective 4

1. Note 2 Maturity Value $20,430

Logan Realty loaned money and received the following notes during 2018.

Note

Date

Principal Amount

Interest Rate

Term

(1)

Oct. 1

$ 16,000

7%

1 year

(2)

Jun. 30

18,000

18%

9 months

(3)

Sep. 19

12,000

8%

90 days

Requirements

1. Determine the maturity date and maturity value of each note.

2. Journalize the entries to establish each Note Receivable and to record collection of principal and

interest at maturity. Include a single adjusting entry on December 31, 2018, the fiscal year-end, to

record accrued interest revenue on any applicable note. Explanations are not required. Round to the

nearest dollar.

SOLUTION

Requirement 1

Principal

Interest

Rate

Interest

Period

Interest

Revenue

Earned

Maturity

Value

(P + I)

Maturity

Date

Requirement 2

Date

Accounts and Explanation

Debit

Credit

2018

Oct. 1

Notes Receivable (Note 1)

16,000

Cash

16,000

Notes Receivable (Note 2)

18,000

Cash

18,000

Sep. 19

Notes Receivable (Note 3)

12,000

Cash

12,000

Cash

12,237

Interest Revenue

Note Receivable

12,000

Interest Receivable

Interest Revenue

Principal

Interest

Rate

Interest

Period

Interest

Revenue

Earned

Note 1

$ 16,000

× 0.07

× 3/12

$ 280

Note 2

18,000

× 0.18

× 6/12

1,620

$ 1,900

Date

Accounts and Explanation

Debit

Credit

2019

Mar. 30

Cash ($18,000 + $1,620 + $810)

20,430

Interest Receivable

Interest Revenue ($18,000 × 0.18 × 3/12)

18,000

Cash ($16,000 + $280 + $840)

17,120

Interest Receivable

16,000

8-66

P8-40B Accounting for notes receivable, dishonored notes, and accrued interest revenue

Learning Objective 4

March 6, 2019 Interest Revenue $128

Consider the following transactions for TLC Company.

2018

Dec.

6

Received a $8,000, 90-day, 9% note in settlement of an overdue

accounts receivable from Forest Music.

31

Made an adjusting entry to accrue interest on the Forest Music note.

31

Made a closing entry for interest revenue.

2019

Mar.

6

Collected the maturity value of the Forest Music note.

Jun.

30

Loaned $14,000 cash to Washington Music, receiving a six-month,

12% note.

Oct. 2

Received a $1,000, 60-day, 12% note for a sale to ZZZ Music. Ignore

Cost of Goods Sold.

Dec.

1

ZZZ Music dishonored its note at maturity.

1

Wrote off the receivable associated with ZZZ Music. (Use the

allowance method.)

30

Collected the maturity value of the Washington Music note.

Journalize all transactions for TLC Company. Round all amounts to the nearest dollar.

8-67

SOLUTION

Date

Accounts and Explanation

Debit

Credit

2018

Dec. 6

Notes Receivable—Forest Music

8,000

Accounts Receivable—Forest Music

8,000

Interest Receivable

49

Interest Revenue ($8,000 × 0.09 × 25/365)

49

Interest Revenue

49

49

2019

Cash

8,177

Interest Receivable

49

8,000

Notes Receivable—Washington Music

Cash

Notes Receivable—ZZZ Music

1,000

Sales Revenue

1,000

Dec. 1

Accounts Receivable—ZZZ Music

1,020

20

1,000

Allowance for Bad Debts

1,020

Accounts Receivable—ZZZ Music

1,020

Cash

8-68

P8-41B Using ratio data to evaluate a company’s financial position

Learning Objective 5

1. Days’ sales in receivables (2018) 18 days

The comparative financial statements of Newton Cosmetic Supply for 2018, 2017, and 2016 include the

data shown here:

2018

2017

2016

Balance sheet—partial

Current Assets:

Cash

$ 80,000

$ 50,000

$ 30,000

Short-term investment

150,000

170,000

125,000

Accounts Receivable, Net

310,000

260,000

220,000

Merchandise Inventory

360,000

335,000

330,000

Prepaid Expenses

50,000

30,000

35,000

Total Current Assets

950,000

845,000

740,000

Total Current Liabilities

530,000

630,000

670,000

Income statement—

partial

Net Sales (all on account)

5,850,000

5,110,000

425,000

Requirements

1. Compute these ratios for 2018 and 2017:

a. Acid-test ratio (Round to two decimals.)

b. Accounts receivable turnover (Round to two decimals.)

c. Days’ sales in receivables (Round to the nearest whole day.)

2. Considering each ratio individually, which ratios improved from 2017 to 2018 and which ratios

deteriorated? Is the trend favorable or unfavorable for the company?

SOLUTION

Requirement 1

a. Acid-test ratio = (Cash including cash equivalents + Short-term investments + Net current

receivables) / Total current liabilities

2018

c. Days’ sales in receivables = 365 days / Accounts receivable turnover ratio

2018

= 365 days / 20.53

= 18 days (rounded)

2017

= 365 days / 21.29

= 17 days (rounded)

Requirement 2

The acid-test ratio improved from 2017 to 2017. This trend is favorable to the company.

8-70

Using Excel

P8-42 Using Excel for Aging Accounts Receivable

The Lake Lucerne Company uses the allowance method of estimating bad debts expense. An aging

schedule is prepared in order to calculate the balance in the allowance account. The percentage

uncollectible is calculated as follows:

1–30 Days

1%

31–60 Days

2%

61–90 Days

5%

91–365 Days

50%

After 365 days, the account is written off.

Requirements

1. Calculate the number of days each receivable is outstanding.

2. Complete the Schedule of Accounts Receivable.

3. Journalize the adjusting entry for Bad Debts Expense.

SOLUTION

The student templates for Using Excel are available online in MyAccountingLab in the Multimedia

8-71

Continuing Problem

P8-43 Accounting for uncollectible accounts using the allowance method

This problem continues the Canyon Canoe Company situation from Chapter 7. Canyon Canoe

Company has experienced rapid growth in its first few months of operations and has had a

significant increase in customers renting canoes and purchasing T-shirts. Many of these customers

are asking for credit terms. Amber and Zack Wilson, stockholders and company managers, have

decided it is time to review their business transactions and update some of their business practices.

Their first step is to make decisions about handling accounts receivable.

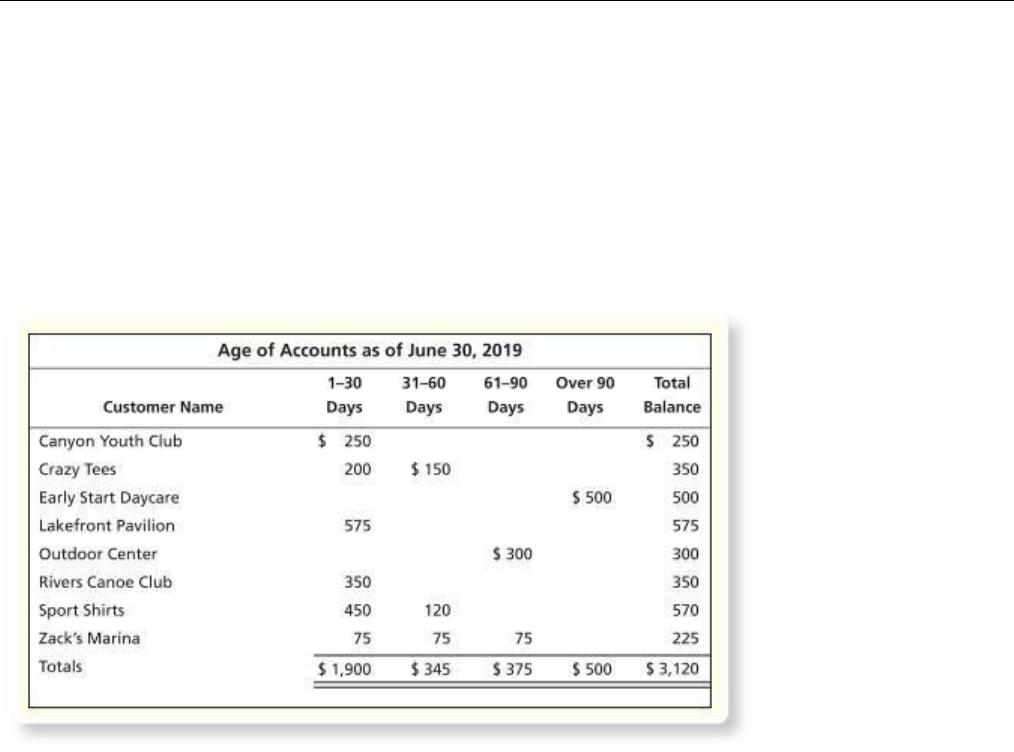

So far, year to date credit sales have been $15,500. A review of outstanding receivables

resulted in the following aging schedule:

Requirements

1. The company wants to use the allowance method to estimate bad debts. Determine the estimated

bad debts expense under the following methods at June 30, 2019. Assume a zero beginning

balance for Allowance for Bad Debts. Round to the nearest dollar.

a. Percent-of-sales method, assuming 4.5% of credit sales will not be collected.

b. Percent-of-receivables method, assuming 22.5% of receivables will not be collected.

c. Aging-of-receivables method, assuming 5% of invoices 1–30 days will not be collected, 20%

of invoices 31–60 days, 40% of invoices 61–90 days, and 75% of invoices over 90 days.

2. Journalize the entry at June 30, 2019, to adjust for bad debts expense using the percent-of-sales

method.

3. Journalize the entry at June 30, 2019, to record the write-off of the Early Start Daycare invoice.

4. At June 30, 2019, open T-accounts for Accounts Receivable and Allowance for Bad Debts

before Requirements 2 and 3. Post entries from Requirements 2 and 3 to those accounts.

Assume a zero beginning balance for Allowance for Bad Debts.

5. Show how Canyon Canoe Company will report net accounts receivable on the balance sheet on

June 30, 2019.

8-72

SOLUTION

Requirement 1

1a. Percent-of-sales method:

Bad Debt Expense

=

4.5% of credit sales

=

4.5% × $15,500

=

$698

1c. Aging-of-receivables method:

Age of Accounts as of June 30, 2019

Customer Name

1-30

Days

31-60

Days

61-90

Days

Over

90

Days

Total

Balance

Bad Debt Expense

=

Target Balance – Unadjusted balance in Allowance for Bad Debts

=

$689 – $0

=

$689

Target Balance

=

22.5% of Accounts Receivable

=

22.5% × $3,120

=

$702

Bad Debt Expense

=

Target Balance – Unadjusted balance in Allowance for Bad Debts

=

$702 – $0

=

$702

P8-43, cont.

Requirements 2 and 3

Date

Accounts and Explanation

Debit

Credit

2019

Jun. 30

Bad Debt Expense

698

Allowance for Bad Debts

500

Requirement 4

Accounts Receivable

Allowance for Bad Debts

Balance

3,120

0

Balance

500

Jun. 30

Jun. 30

500

698

Jun. 30

Balance

2,620

198

Balance

Requirement 5

CANYON CAONOE COMPANY

Balance Sheet−Partial

June 30, 2019

Current Assets:

Accounts Receivable

8-74

Practice Set

P8-44 Accounting for uncollectible accounts using the allowance method and reporting net

accounts receivable on the balance sheet

This problem continues the Crystal Clear Cleaning problem begun in Chapter 2 and continued through

Chapter 7.

Crystal Clear Cleaning uses the allowance method to estimate bad debts. Consider the following

April 2019 transactions for Crystal Clear Cleaning:

Apr. 1

Performed cleaning service for Debbie’s D-list for $13,000 on account

with terms n/20.

10

Borrowed money from First Regional Bank, $30,000, making a 180-