Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

8–35 Ch. 8—Problems

Problem 8-6, Continued

Mary Company and Subsidiaries John Company and Joan Company

Worksheet for Consolidated Financial Statements

For Year Ended December 31, 2018

(Concluded)

Consoli-

Eliminations Consolidated Controlling dated

Trial Balance

and Adjustments Income Retained Balance

Mary John Joan Dr. Cr. Statement NCI Earnings Sheet

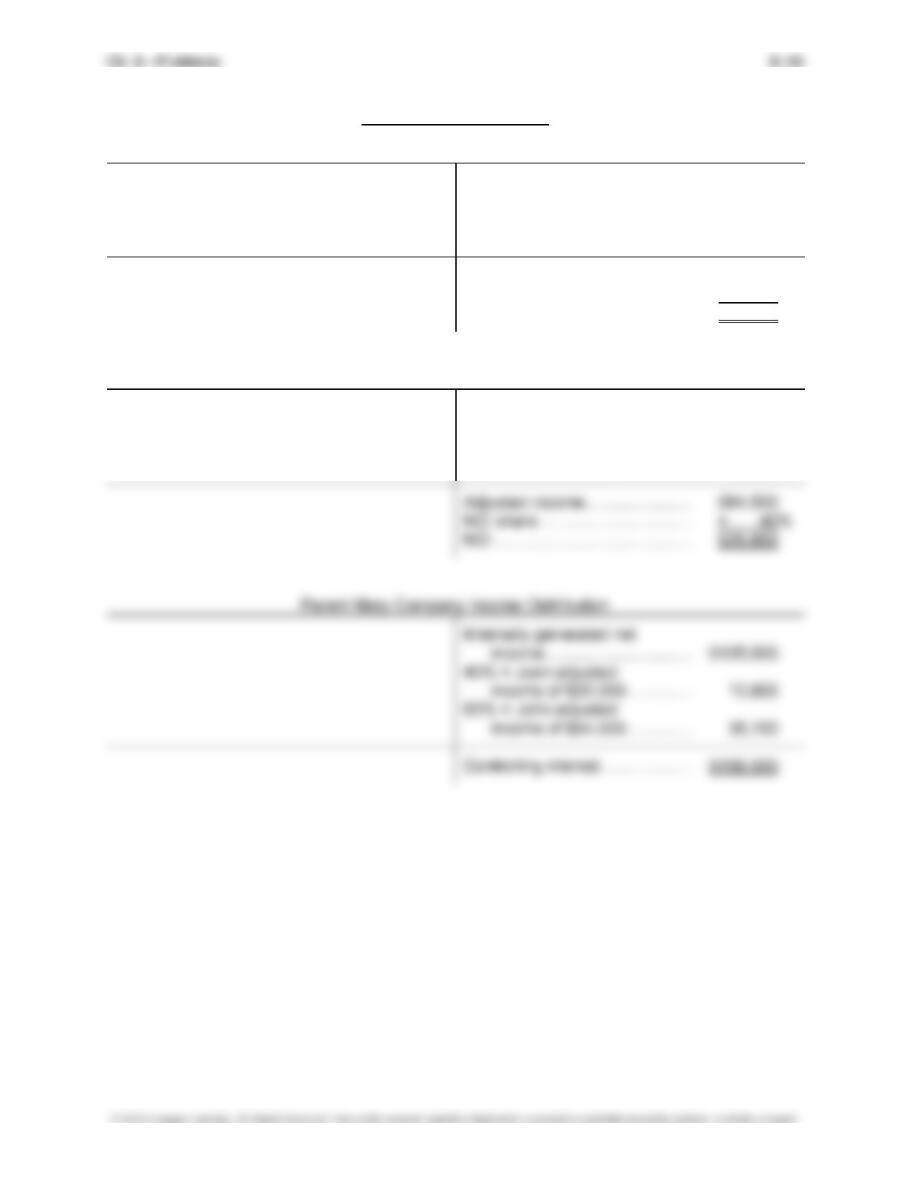

Consolidated Net Income .................................................................................................................................................... (185,500) ............. ............. ...............

To NCI (John and Joan) (see distribution schedule) ...................................................................................................... 29,000 (29,000) ............. ...............

Eliminations and Adjustments:

(CY1) Eliminate current-year entries for Mary’s investment in John. Income: $70,000 × 60% = $42,000.

(EL1) Eliminate Mary’s interest in John’s equity.

(CY3) Eliminate current-year entries for John’s investment in Joan, $40,000 × 50% = $20,000.

(EL3) Eliminate John’s interest in Joan’s equity.

(F2) Adjust depreciation on the machine for 2018.

(IS) Eliminate intercompany sale of goods from John to Joan.

Problem 8-6, Concluded

Subsidiary Joan Company Income Distribution

Gain on sale of machine ............... $10,000 Internally generated net

income ................................ $40,000

Gain on machine realized

through use ......................... 2,000

Adjusted income ....................... $32,000

NCI share ................................. × 10%

NCI ........................................... $ 3,200

Subsidiary John Company Income Distribution

Gross profit in ending Internally generated net

inventory .................................. $1,500 income ................................ $50,000

50% × Joan adjusted

income of $32,000 .............. 16,000

8–37 Ch. 8—Problems

PROBLEM 8-7

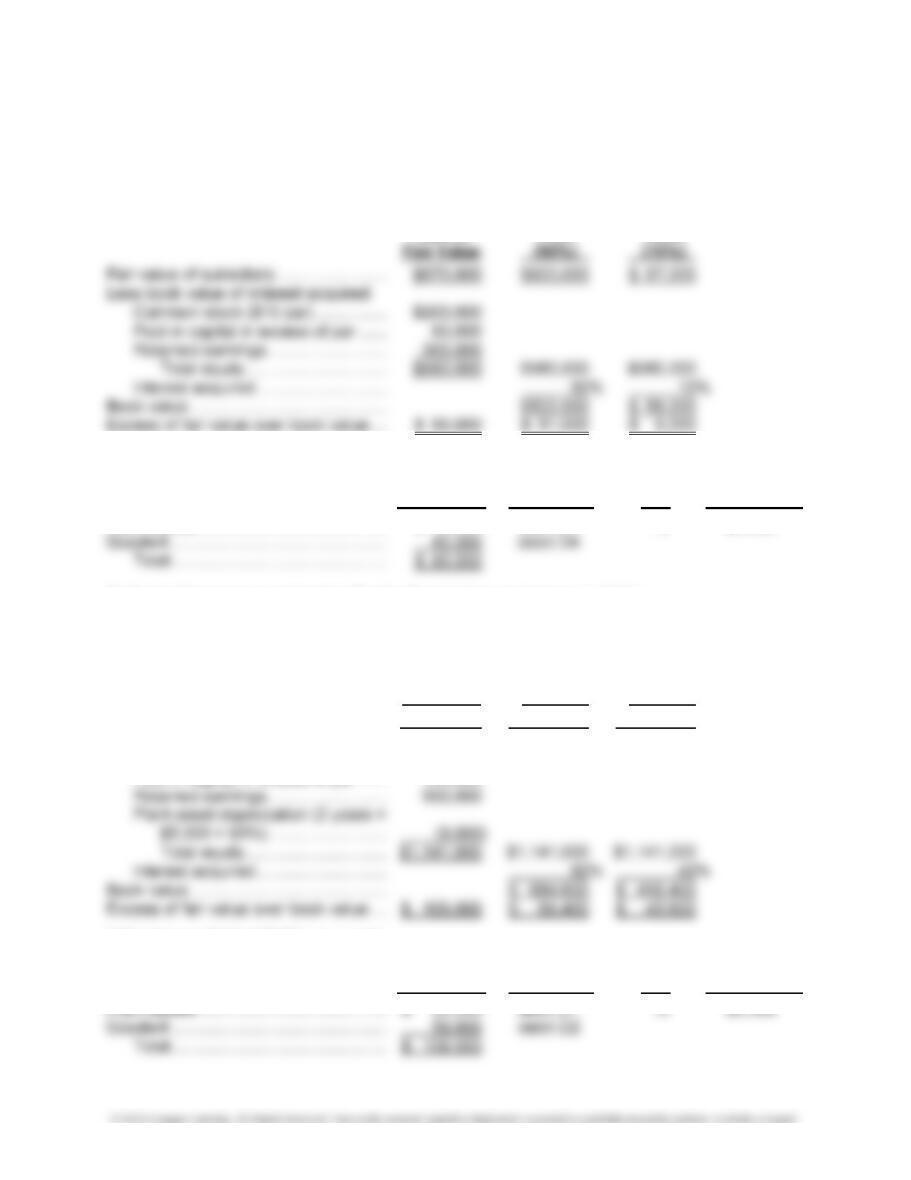

Shelby investment in Borner Company on January 1, 2015:

Determination and Distribution of Excess Schedule

Company Parent NCI

Implied Price Value

Adjustment of identifiable accounts:

Worksheet Amortization

Adjustment Key Life per Year

Plant assets ......................................... $ 50,000 debit D3 10 $5,000

DeNoma Company investment in Shelby Corporation on January 1, 2017:

Determination and Distribution of Excess Schedule

Company Parent NCI

Implied Price Value

Fair Value (60%) (40%)

Fair value of subsidiary ........................ $1,250,000 $ 750,000 $ 500,000

Less book value of interest acquired:

Common stock ............................... $ 500,000

Paid-in capital in excess of par ...... 150,000

Adjustment of identifiable accounts:

Worksheet Amortization

Adjustment Key Life per Year

Problem 8-7, Continued

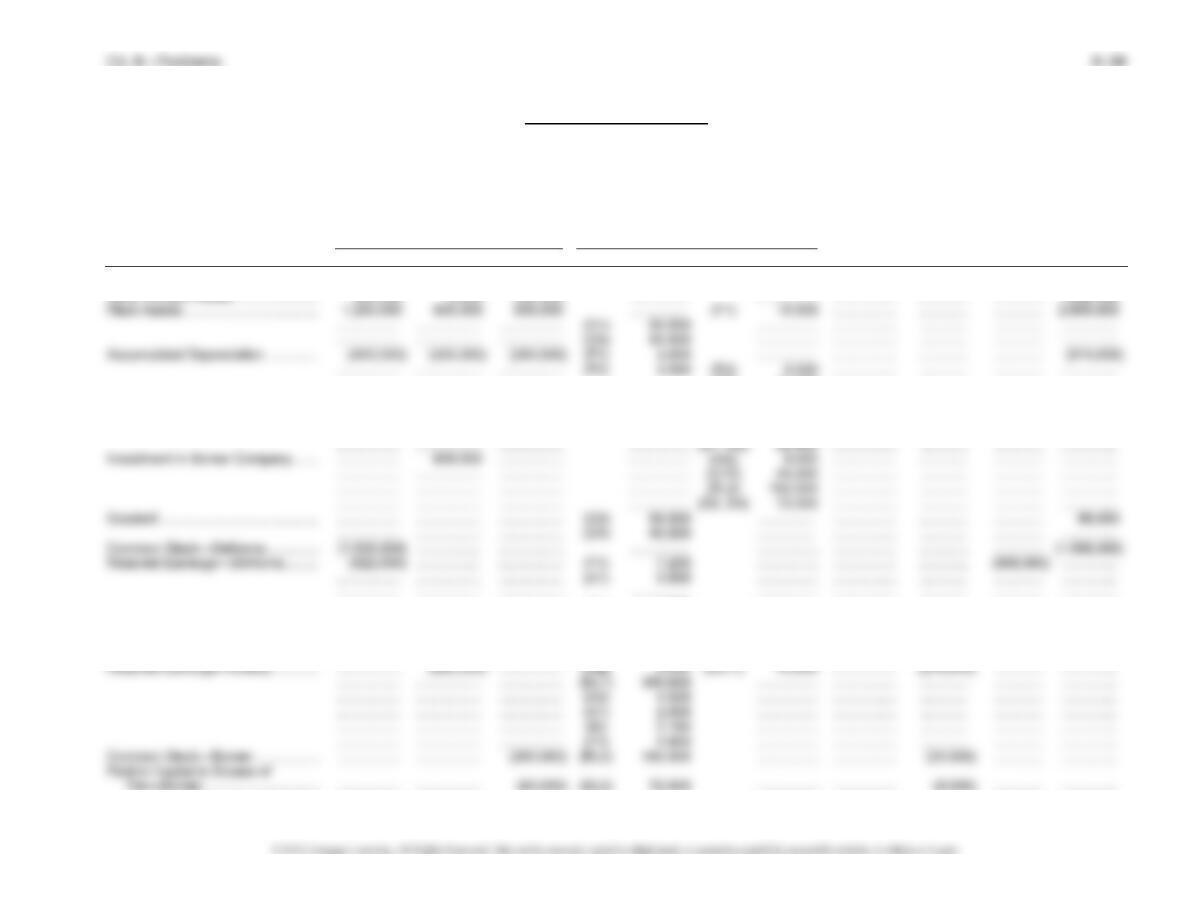

DeNoma Company and Subsidiaries Shelby Corporation and Borner Company

Worksheet for Consolidated Financial Statements

For Year Ended December 31, 2018

Consoli-

Eliminations Consolidated Controlling dated

Trial Balance

and Adjustments Income Retained Balance

DeNoma Shelby Borner Dr. Cr. Statement NCI Earnings Sheet

Inventory ......................................... 75,000 60,000 40,000 ............... (EI) 8,000 ................. ............. ............. 167,000

Other Current Assets ...................... 900,000 2,000 390,000 ............... ................ ................. ............. ............. 1,292,000

................. ................. ................. ................ (A3) 11,000 ................. ............. ............. ...............

................. ................. ................. ................ (A1) 10,000 ................. ............. ............. ...............

Investment in Shelby Corporation ... 894,000 ................. ................. ................ (CY1) 72,000 ................. ............. ............. ...............

................. ................. ................. ................ (EL1) 756,600 ................. ............. ............. ...............

................. ................. ................. (BI) 3,240 ................ ................. ............. ............. ...............

Common Stock—Shelby ................. ................. (500,000) ................. (EL1) 300,000 ................ ................. (200,000) ............. ...............

Paid-In Capital in Excess of

Par—Shelby ............................... ................. (150,000) ................. (EL1) 90,000 ................ ................. (60,000) ............. ...............

Problem 8-7, Continued

DeNoma Company and Subsidiaries Shelby Corporation and Borner Company

Worksheet for Consolidated Financial Statements

For Year Ended December 31, 2018

(Concluded)

Consoli-

Eliminations Consolidated Controlling dated

Trial Balance

and Adjustments Income Retained Balance

DeNoma Shelby Borner Dr. Cr. Statement NCI Earnings Sheet

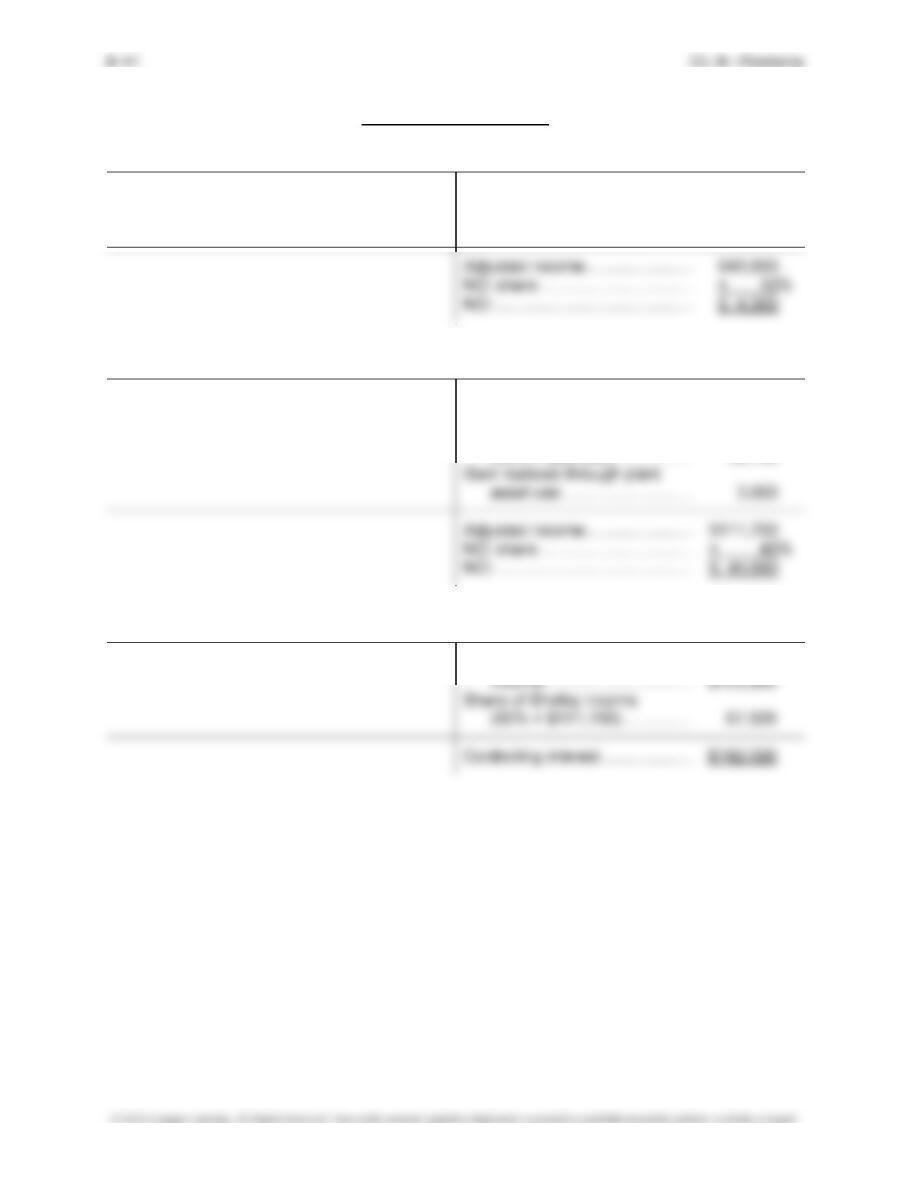

Retained Earnings—Borner ............ ................. ................. (500,000) (EL2) 450,000 (NCI2) 9,000 ................. (56,900) ............. ...............

................. ................. ................. (A3) 1,500 ................ ................. ............. ............. ...............

................. ................. ................. (BI) 600 ................ ................. ............. ............. ...............

Sales ............................................... (900,000) (700,000) (600,000) (IS) 125,000 ................ (2,075,000) ............. ............. ...............

Problem 8-7, Continued

Eliminations and Adjustments:

(Adj) Adjust Investment in Borner Company and Retained Earnings—Shelby for

(A1) Amortize the excess for the current and past years:

Depreciation: Current Prior Total

(A3) Amortize excess as follows:

Borner retained earnings, 3 years × 10% × $5,000 ..... $1,500

Shelby retained earnings, 1 year (2 years are in the

adjustment), 90% × $5,000 .................................... 4,500

Expense ....................................................................... 5,000

(IS) Eliminate the current-year intercompany merchandise sale.

(BI) Eliminate Borner’s gross profit contained in Shelby’s beginning inventory. The

correction of retained earnings must be prorated between noncontrolling and

controlling interests:

$7,500 × 80% = $6,000

(EI) Eliminate the intercompany profit contained in Shelby’s ending inventory,

$10,000 × 80% = $8,000.

(F1) Adjust to remove gain on intercompany sale of assets, reduce accumulated

depreciation by the prior-year amortization of the gain, and reduce Shelby’s

Problem 8-7, Concluded

Subsidiary Borner Company Income Distribution

Ending inventory profit .................. $8,000 Internally generated

Depreciation on excess ................. 5,000 income ................................ $50,000

Beginning inventory profit ......... 6,000

Subsidiary Shelby Corporation Income Distribution

Depreciation on excess ................. $5,000 Internally generated

income ................................ $ 75,000

Share of Borner income

(90% × $43,000) ................. 38,700

Parent DeNoma Company Income Distribution

Internally generated

PROBLEM 8-8

Determination and Distribution of Excess Schedule

Company Parent NCI

Implied Price Value

Fair Value (80%) (20%)

Fair value of subsidiary ........................ $562,500 $450,000 $112,500

Less book value of interest acquired:

Common stock ($10 par) ................ $ 50,000

Adjustment of identifiable accounts:

Worksheet Amortization

Adjustment Key Life per Year

8–43 Ch. 8—Problems

Problem 8-8, Continued

Parson Company and Subsidiary Salary Company

Worksheet for Consolidated Financial Statements

For Year Ended December 31, 2016

Eliminations Consolidated Controlling Consolidated

Trial Balance

and Adjustments Income Retained Balance

Parson Salary Dr. Cr. Statement NCI Earnings Sheet

Inventory ........................................................ 170,000 120,000 ................. (EI) 4,800 ................. ................. ................. 285,200

Long-Term Liabilities ...................................... (250,000) (100,000) ................. ................. ................. ................. ................. (350,000)

Common Stock ($10 par)—Parson ................ (100,000) ................. ................. ................. ................. ................. ................. (100,000)

Dividends Declared—Salary .......................... ................. 10,000 ................. (CY1) 8,000 ................. 2,000 ................. .................

Treasury Stock ............................................... .................

................. (TS) 100,000 ................. ................. ................. ................. 100,000

Totals .......................................................... 0 0 707,300 .... 707,300 ................. ................. .................

Consolidated Net Income ........................................................................................................................................ (175,200) ................. ................. .................

Problem 8-8, Concluded

Eliminations and Adjustments:

(CV) Convert to the simple equity method as of January 1, 2016.

(CY1) Eliminate the current-year dividend income of Parson against dividends declared

by Salary.

(EL) Eliminate 80% of the Salary Company equity balances at the beginning of the

year against the investment account.

(D) Distribute the $122,000 excess of cost over book value and $30,500 NCI ad-

justment to goodwill.

Subsidiary Salary Company Income Distribution

Internally generated net

income ................................ $60,000

NCI share ................................. × 20%

NCI ........................................... $12,000

Parent Parson Company Income Distribution

Ending inventory profit .................. $4,800 Internally generated net

PROBLEM 8-9

Determination and Distribution of Excess Schedule

Company Parent NCI

Implied Price Value

Fair Value (75%) (25%)

Fair value of subsidiary ........................ $148,000 $111,000* $ 37,000

Less book value of interest acquired:

Common stock ($5 par) .................. $ 20,000

Adjustment of identifiable accounts:

Worksheet Amortization

Adjustment Key Life per Year

Goodwill ............................................... $ 6,000 debit D

*Last purchase at $51,800/1,400 shares = $37 per share. Fair value = 3,000 shares × $37 =

$111,000

Adjustment to fair value:

Problem 8-9, Continued

Heckert Company and Subsidiary Aker Company

Worksheet for Consolidated Financial Statements

For Year Ended December 31, 2017

Eliminations Consolidated Controlling Consolidated

Trial Balance

and Adjustments Income Retained Balance

Heckert Aker Dr. Cr. Statement NCI Earnings Sheet

Cash ............................................................... 38,100 29,050 ................. ................. ................. ................. ................. 67,150

Marketable Securities ..................................... 33,000 18,000 ................. (TS) 18,000 ................. ................. ................. 33,000

................. ................. ................. (D) 4,500 ................. ................. ................. .................

Patents ........................................................... 35,000 ................. ................. ................. ................. ................. ................. 35,000

Goodwill ......................................................... ................. ................. (D) 6,000 ................. ................. ................. ................. 6,000

Dividends Declared—Aker ............................. ................. 4,000 ................. (CY1) 3,000 ................. 1,000 ................. .................

Sales and Services ........................................ (850,000) (530,000) (IS) 182,000 ................. (1,198,000) ................. ................. .................

Dividend Income ............................................ (3,000) ................. (CY1) 3,000 ................. ................. ................. ................. .................

Other Income ................................................. (9,000) (3,700) (F1) 800 ................. (11,900) ................. ................. .................

8–47 Ch. 8—Problems

Problem 8-9, Continued

Heckert Company and Subsidiary Aker Company

Worksheet for Consolidated Financial Statements

For Year Ended December 31, 2017

(Concluded)

Eliminations Consolidated Controlling Consolidated

Trial Balance

and Adjustments Income Retained Balance

Heckert Aker Dr. Cr. Statement NCI Earnings Sheet

Gain on investment ........................................ ................. ................. ................. (Adj) 11,200 (11,200) ................. ................. .................

Eliminations and Adjustments:

(Adj) Adjust investment account for gain on prior investment, $11,200.

(CY1) Eliminate intercompany cash dividends.

(CY2) Eliminate intercompany dividends on shares of Heckert owned by Aker,

1,500 × $0.50 = $750 against the dividends payable account.

(EL) Eliminate 75% of subsidiary equity against the investment account.

Problem 8-9, Concluded

Subsidiary Aker Company Income Distribution

Gain on sale of equipment ............ $ 800 Internally generated net

Unrealized profit in income ................................ $ 38,000

ending inventory ...................... 5,400 Gain on investment in Heckert . 11,200

Parent Heckert Company Income Distribution

Internally generated net