CHAPTER 8

SOLUTIONS TO EXERCISES—SET B

EXERCISE 8-1B

1. Establishment of responsibility. The counter clerk is responsible for

handling cash. Other employees are responsible for making the food.

2. Segregation of duties. Employees who make the food do not handle cash.

3. Documentation procedures. The counter clerk uses your order invoice

(ticket) in registering the sale on the cash register. The cash register

produces a tape of all sales.

EXERCISE 8-2B

(a)

(b)

Procedure

Weakness

Principle

Recommended

Change

1.

for cash with

a specific clerk.

register codes

for each clerk.

Inability to

establish

Establishment

of responsibility.

There should be

separate cash

EXERCISE 8-2B (Continued)

(a)

(b)

Procedure

Weakness

Principle

Recommended

Change

3.

Cash is not

independently

counted.

Independent

internal

verification.

A cashier office

supervisor should

count cash.

handle cash.

take vacations.

controls.

either take vacations

jobs and shifts.

EXERCISE 8-3B

(a)

(b)

Procedure

Weakness

Principle

Recommended

Change

1.

The approval

and payment

of bills is done

by the same

individual.

Segregation

of duties.

The store manager

should approve bills

for payment and the

treasurer should sign

and issue checks.

is not

independently

prepared.

verification.

responsibilities

should prepare the

bank reconciliation.

a secure area.

storage area.

EXERCISE 8-3B (Continued)

(a)

(b)

Procedure

Weakness

Principle

Recommended

Change

4.

Checks are not

prenumbered.

Documentation

procedures.

Checks should

be prenumbered

and subsequently

accounted for.

bill from being

paid more than

once.

payment.

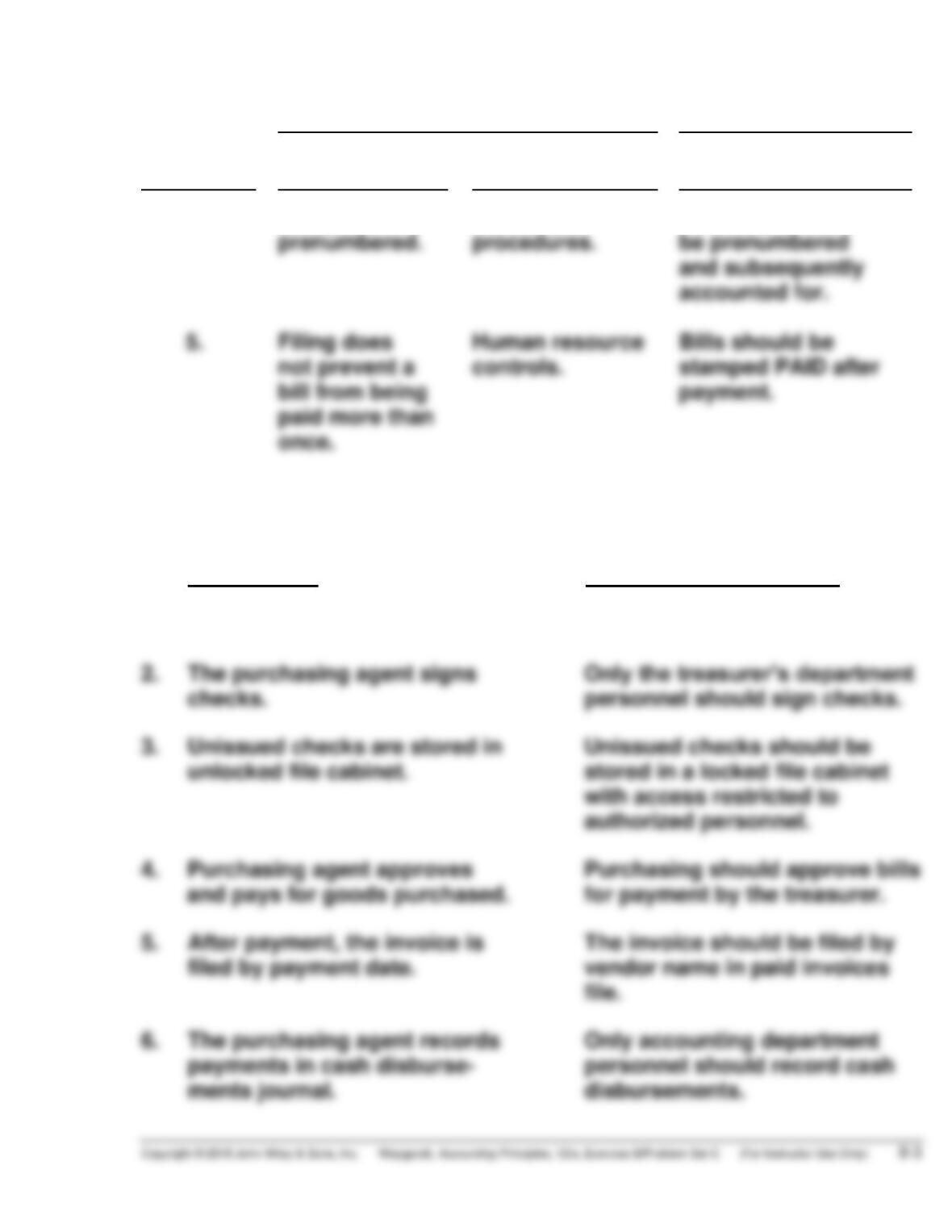

EXERCISE 8-4B

(a) Weaknesses

(b) Suggested Improvement

1. Checks are not prenumbered.

Use prenumbered checks.

2. The purchasing agent signs

checks.

Only the treasurer’s department

personnel should sign checks.

stored in a locked file cabinet

with access restricted to

4. Purchasing agent approves

and pays for goods purchased.

Purchasing should approve bills

for payment by the treasurer.

5. After payment, the invoice is

filed by payment date.

The invoice should be filed by

vendor name in paid invoices

file.

ments journal.

disbursements.

EXERCISE 8-4B (Continued)

(a) Weaknesses

(b) Suggested Improvement

7. The treasurer records the

checks in cash disbursements

journal.

Same as answer to No. 6.

bank statement.

An internal auditor should

reconcile the bank statement.

(b) To: Treasurer, Noble Company

From: Accounting Student

I have reviewed your cash disbursements system and suggest that you

make the following improvements:

1. Noble Company should use prenumbered checks. These should

be stored in a locked file cabinet or safe with access restricted to

authorized personnel.

EXERCISE 8-5B

Procedure

IC good or weak?

Related internal control principle

1.

Good

Establishment of Responsibility

2.

Weak

Independent Internal Verification

3.

Good

Segregation of Duties

4.

Weak

Segregation of Duties

5.

Weak

Documentation Procedures

EXERCISE 8-6B

Procedure

IC good or weak?

Related internal control principle

1.

Weak

Human Resource Controls

2.

Good

Establishment of Responsibility

3.

Good

Segregation of Duties

4.

Weak

Independent Internal Verification

5.

Weak

Physical Controls

EXERCISE 8-7B

May 1 Petty Cash ……………………………………………… 200.00

Cash ……………………………………………… 200.00

June 1 Delivery Expense ……………………………………. 69.30

Postage Expense ……………………………………. 75.50

EXERCISE 8-8B

Mar. 1 Petty Cash ……………………………………………………….. 150

Cash ……………………………………………………….… 150

15 Postage Expense ……………………………………………… 35

Freight-out ……………………………………………………….. 19

EXERCISE 8-9B

(a) Cash balance per bank statement ………………. $4,714.60

Add: Deposits in transit …………………………... 730.00

5,444.60

Less: Outstanding checks ………………………… 914.00

(b) Accounts Receivable …………………………………. 630.00

Cash ………………………………………………….. 630.00

EXERCISE 8-10B

The outstanding checks are as follows:

No.

Amount

255

$ 510

EXERCISE 8-11B

(a) TIM’S DVD COMPANY

Bank Reconciliation

July 31

Cash balance per bank statement ……………………………… $2,542

Add: Deposits in transit ………………………………………….. 825

3,367

Less: Outstanding checks ……………………………………….. 207

Adjusted cash balance per bank …………………………..…… $3,160

(b) July 31 Cash …………………………………………………………. 621

Miscellaneous Expense ……………………………… 15

EXERCISE 8-12B

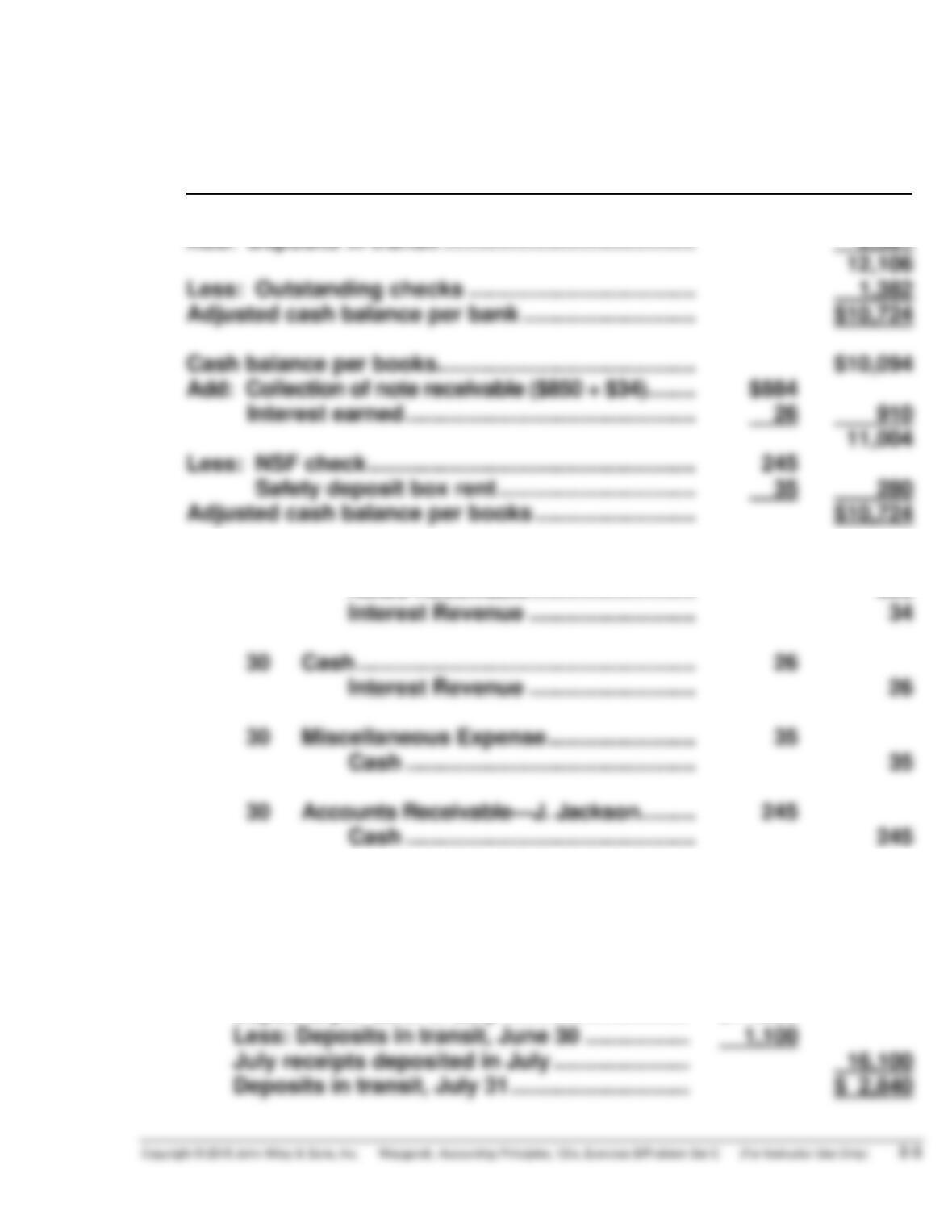

(a) MORSE COMPANY

Bank Reconciliation

September 30

Cash balance per bank statement …………………….. $ 9,525

Add: Deposits in transit ………………………………….. 2,581

12,106

(b) Sept. 30 Cash ………………………………………………. 884

Notes Receivable ……………………… 850

Interest Revenue ……………………… 34

30 Cash ………………………………………………. 26

Interest Revenue ……………………… 26

EXERCISE 8-13B

(a) Deposits in transit:

Deposits per books in July ……………………….. $18,940

Deposits per bank in July …………………………. $17,200

EXERCISE 8-13B (Continued)

(b) Outstanding checks:

Checks per books in July …………………………... $17,850

Less: Checks clearing bank in July ……………. $17,050

(c) Deposits in transit:

Deposits per bank statement in September …. $25,400

Add: Deposits in transit, September 30 ……… 1,900

Total deposits to be accounted for ……………… 27,300

(d) Outstanding checks:

Checks clearing bank in September ……………. $22,800

Add: Outstanding checks, September 30 …… 3,200

EXERCISE 8-14B

(a) Cash and cash equivalents should be reported at $37,400.

Cash in bank ……………………………………………………….….. $20,000

(b) “Cash in plant expansion fund” should be reported as part of long–term

investments (a noncurrent asset). “Receivables from customers” should be

SOLUTIONS TO PROBLEMS—SET C

PROBLEM 8-1C

(a)

Principles

Application to Spotlight Theater

Establishment of responsibility.

Only cashiers are authorized to sell

tickets. Only the manager and cashier

can handle cash.

Segregation of duties.

The duties of receiving cash and admit–

ting customers are assigned to the

cashier and to the usher. The manager

maintains custody of the cash, and the

company accountant records the cash.

Documentation procedures.

Tickets are prenumbered. Cash count

sheets are prepared. Deposit slips are

prepared.

Physical controls.

A safe is used for the storage of cash

and a machine is used to issue tickets.

Independent internal verification.

Cash counts are made by the manager

at the end of each cashier’s shift. Daily

comparisons are made by the company

treasurer.

Human resource controls.

Cashiers are bonded.

(b) Actions by the usher and cashier to misappropriate cash might include:

(1) Instead of tearing the tickets, the usher could return the tickets to

the cashier who could resell them, and the two could divide the cash.

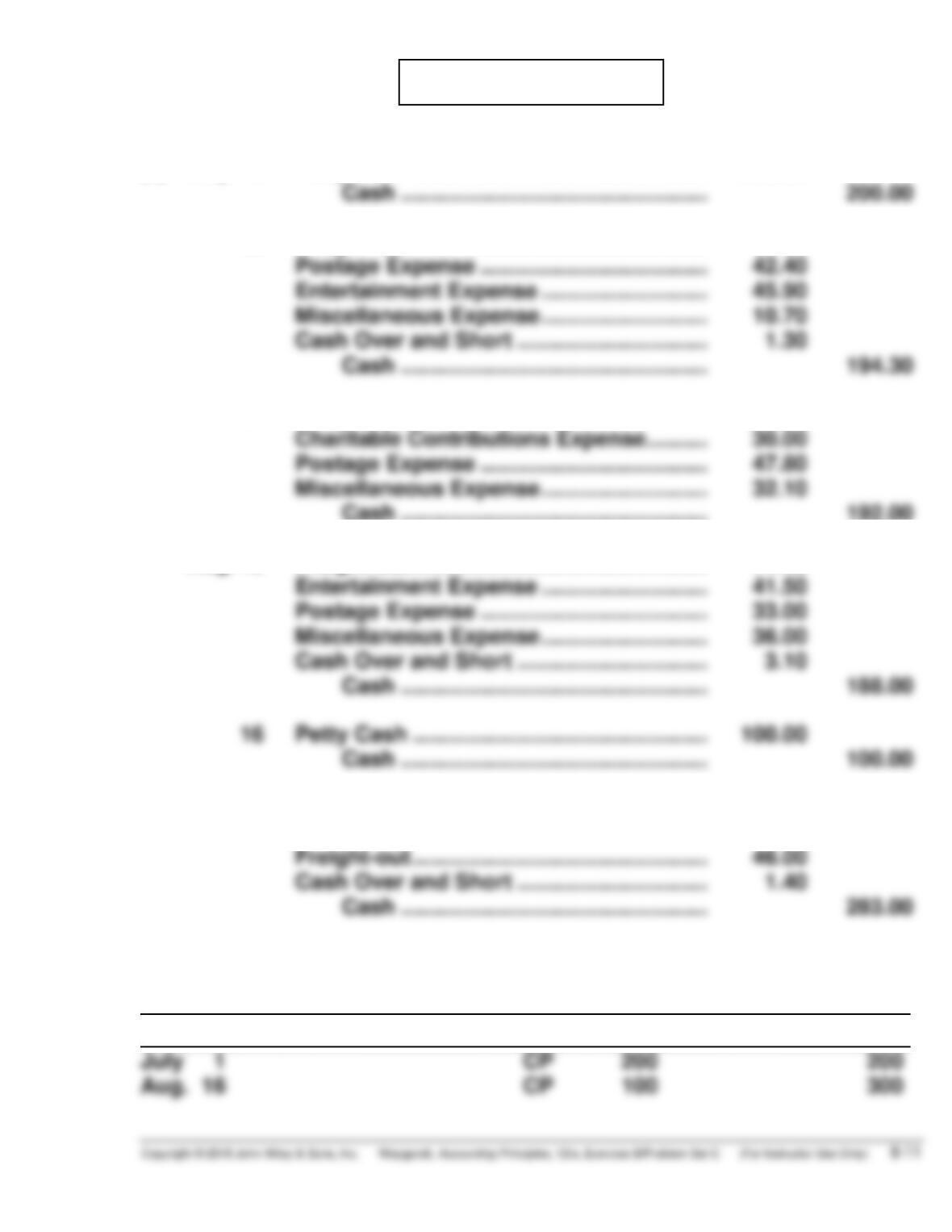

PROBLEM 8-2C

(a) July 1 Petty Cash ………………………………………… 200.00

Cash ………………………………………….. 200.00

15 Freight-out ………………………………………… 94.00

Postage Expense ………………………………. 42.40

31 Freight-out ………………………………………… 82.10

Charitable Contributions Expense ………. 30.00

Aug. 15 Freight-out ………………………………………… 74.40

Entertainment Expense ……………………… 41.50

Postage Expense ………………………………. 33.00

31 Postage Expense ………………………………. 145.00

Entertainment Expense ……………………… 90.60

(b)

Petty Cash

Date

Explanation

Ref.

Debit

Credit

Balance

PROBLEM 8-2C (Continued)

(c) The internal control features of a petty cash fund include:

(1) A custodian is responsible for the fund.

PROBLEM 8-3C

(a) EZY FERTILIZER COMPANY

Bank Reconciliation

May 31, 2017

Cash balance per bank statement ………………. $6,804.60

Add: Deposit in transit …………………………….. $1,436.15

Bank error—Bohr check ………………….. 600.00 2,036.15

8,840.75

Less: Outstanding checks ………………………… 515.25

Adjusted cash balance per bank ………………… $8,325.50

(b) May 31 Cash ………………………………………………………. 2,555

Miscellaneous Expense …………………………... 25

Notes Receivable …………………………….. 2,500

Interest Revenue ……………………………… 80

31 Accounts Receivable—Tyler Gricius ………… 934

Cash ……………………………………………….. 934

PROBLEM 8-4C

(a) LONBERG COMPANY

Bank Reconciliation

November 30, 2017

Balance per bank statement …………………….. $17,069.40

Add: Deposits in transit …………………………. 2,338.00

19,407.40

Less: Outstanding checks

No. 2451 …………………………………….. $1,260.40

No. 2472 …………………………………….. 503.60

Balance per books …………………………………… $10,846.90

Add: Note collected by bank

($2,400 note plus $120 interest

less $15 fee) …………………………..……… 2,505.00

13,351.90

PROBLEM 8-4C (Continued)

(b) Nov. 30 Cash …………………………………………………. 2,505

Miscellaneous Expense ……………………… 15

Notes Receivable ………………………… 2,400

Interest Revenue …………………………. 120

PROBLEM 8-5C

(a) STEINBRENNER COMPANY

Bank Reconciliation

August 31, 2017

Cash balance per bank statement ………………….. $25,932

Add: Deposits in transit (1) ………………………….. $ 8,590

Bank error ($278 – $275) ……………………… 3 8,593

34,525

Less: Outstanding checks (2) ……………………….. 6,393

(1) August receipts per books ……………………… $77,000

August deposits per bank ………………………. $72,410

Less: Deposits in transit, July 31 ……………. 4,000 68,410

Deposits in transit, August 31 …………………. $ 8,590

(2) Disbursements per books in

August……………………………….. $73,570

PROBLEM 8-5C (Continued)

(b) Aug. 31 Cash …………………………………………………….. 7,630

Notes Receivable ……………………………. 7,500

Interest Revenue …………………………….. 130

31 Cash …………………………………………………….. 32

Interest Revenue …………………………….. 32

PROBLEM 8-6C

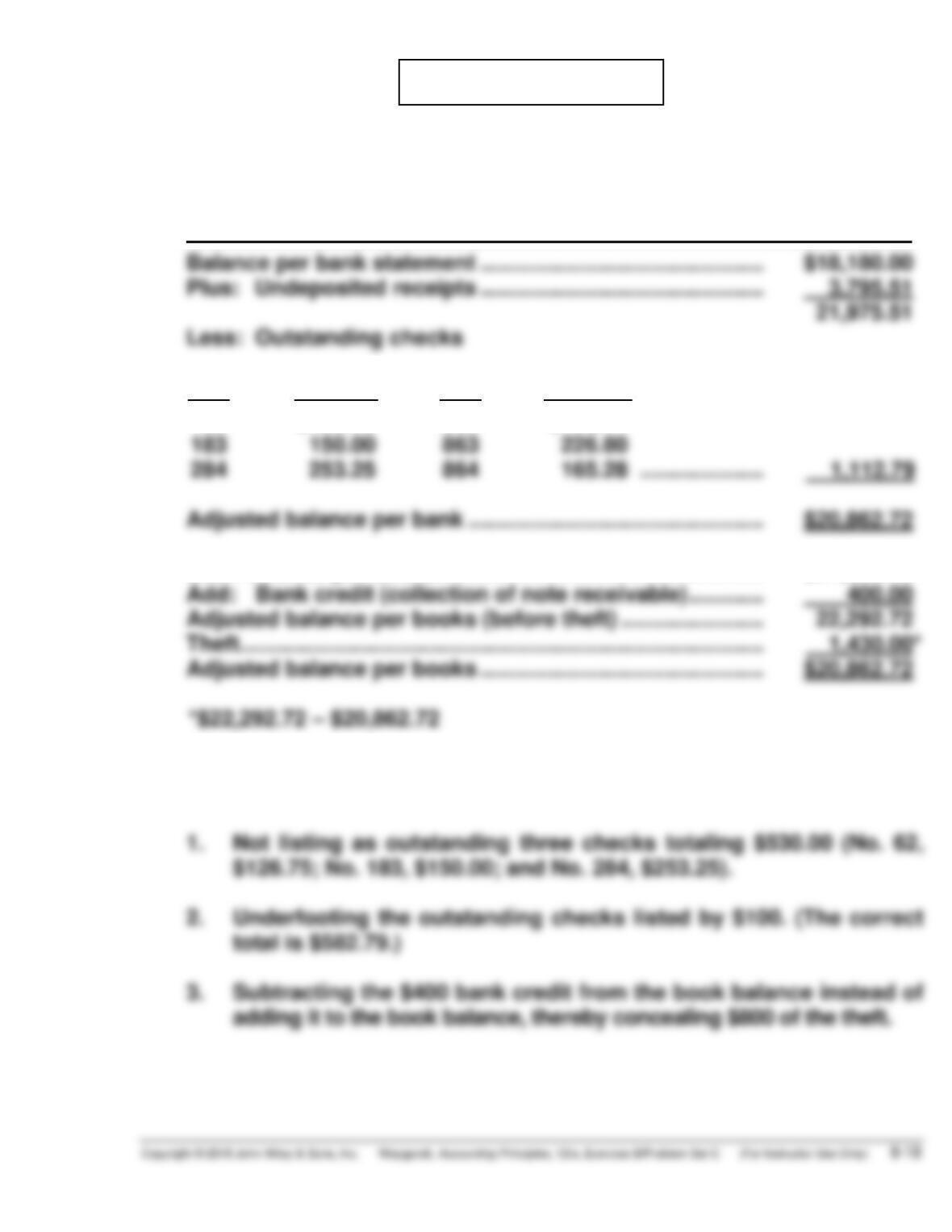

(a) TAVARES COMPANY

Bank Reconciliation

October 31, 2017

Balance per bank statement ………………………………………. $18,180.00

Plus: Undeposited receipts ………………………………………. 3,795.51

21,975.51

Less: Outstanding checks

No.

Amount

No.

Amount

62

$126.75

862

$190.71

Cash balance per books…………………………………………….. $21,892.72

Add: Bank credit (collection of note receivable) ………… 400.00

(b) The cashier attempted to cover the theft of $1,430.00 by:

1. Not listing as outstanding three checks totaling $530.00 (No. 62,

$126.75; No. 183, $150.00; and No. 284, $253.25).

PROBLEM 8-6C (Continued)

(c) 1. The principle of independent internal verification has been violated

because the cashier prepared the bank reconciliation.