b. Inventory subsidiary ledger records:

(1) Specific identification method:

Date Units Unit Cost Total Units Unit Cost

Cost of

Goods Sold

Units Unit Cost Balance

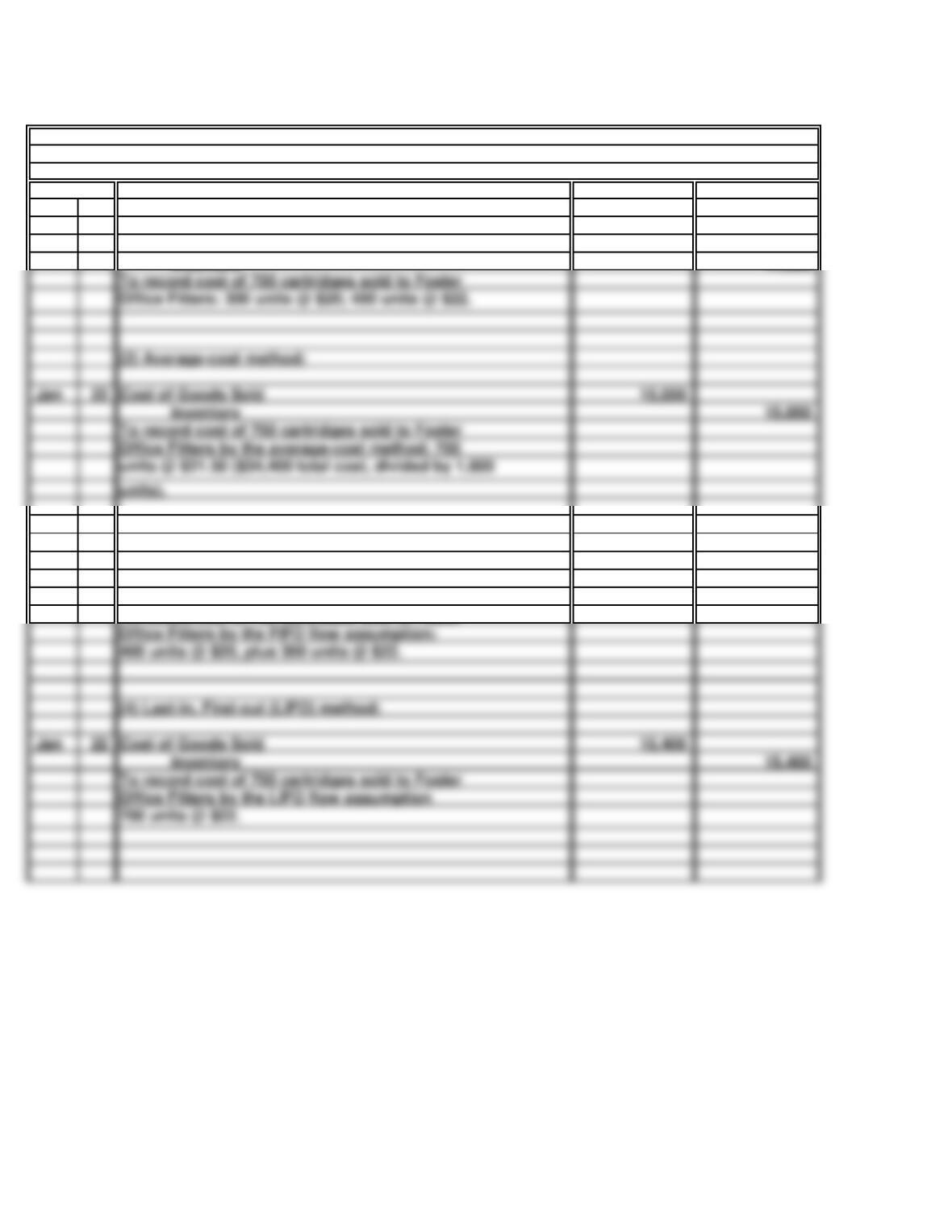

(2) Average-cost method:

Date Units Cost Total Units Cost

Cost of

Goods Sold

Goods Sold

(4) Last-in, first-out (LIFO) method:

Cost of

Goods Sold

SOLD

BALANCE

PURCHASED

Units Cost Balance

Dec 12 600 29$ 17,400$ 600 29.00$ 17,400$

Jan 09 900 32 28,800 1,500 30.80 46,200

Jan 15 1,000 30.80$ 30,800$ 500 30.80 15,400

* $46,200 total cost ÷ 1,500 units = $30.80 average unit cost.

(3) First-in, first-out (FIFO) method:

Cost of

PROBLEM 8.1A

PURCHASED

SOLD

BALANCE

SPORTS WORLD (continued)

PURCHASED

SOLD

BALANCE

PURCHASED

SOLD

BALANCE

c.

PROBLEM 8.1A

SPORTS WORLD (concluded)

No. As shown in part a, the LIFO method resulted in the highest cost of goods sold figure, whereas

30 Minutes, Strong

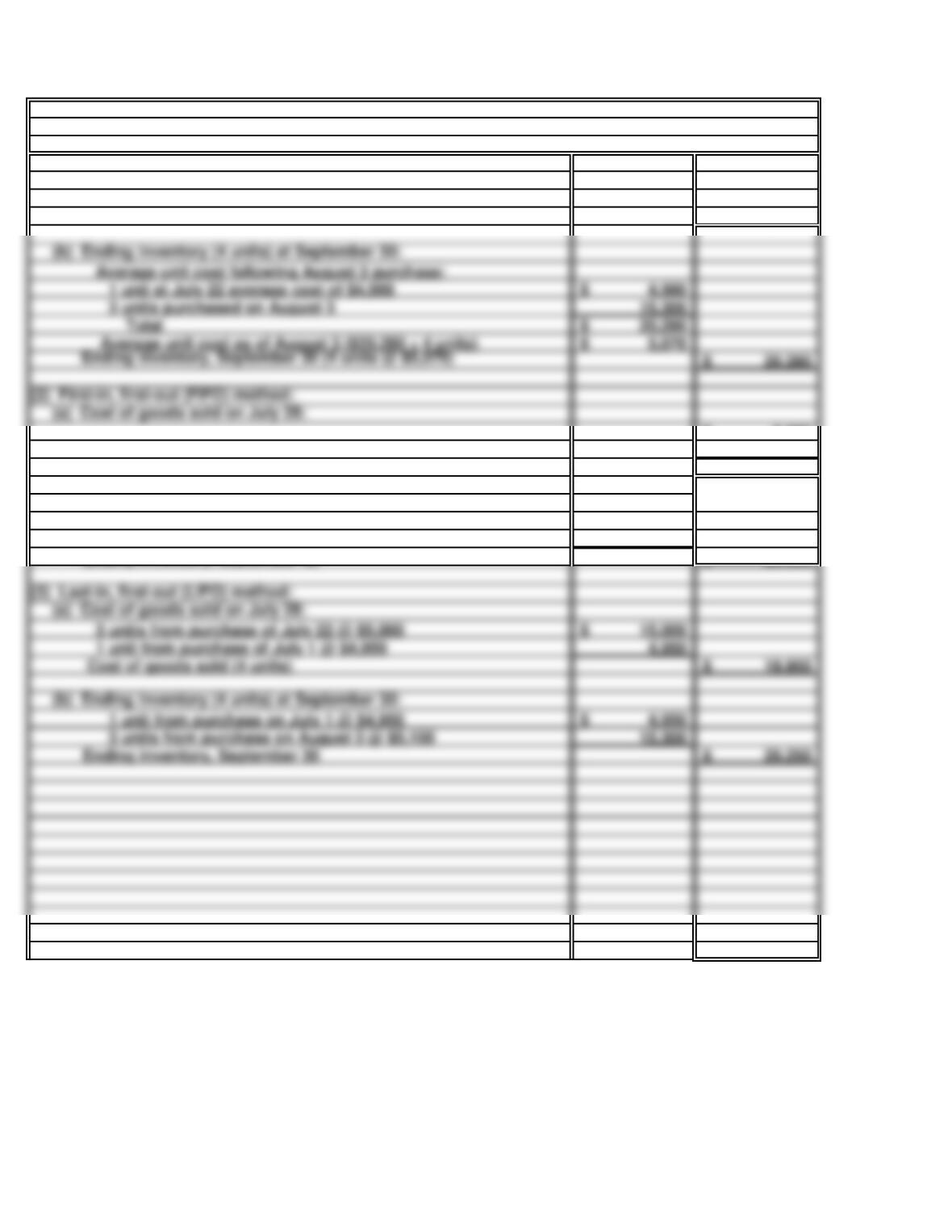

(1) Average-cost method:

(a) Cost of goods sold on July 28:

4,980$

19,920$

9,900$

10,000

19,900$

(b) Ending inventory (4 units) at September 30:

5,000$

15,300

20,300$

(3) Last-in, first-out (LIFO) method:

(a) Cost of goods sold on July 28:

19,950$

(b) Ending inventory (4 units) at September 30:

4,950$

15,300

20,250$

1 unit from purchase on July 1 @ $4,950

Cost of goods sold (4 units)

3 units from purchase of July 22 @ $5,000

1 unit from purchase of July 1 @ $4,950

3 units from purchase on August 3 @ $5,100

Ending inventory, September 30

Cost of goods sold (4 units)

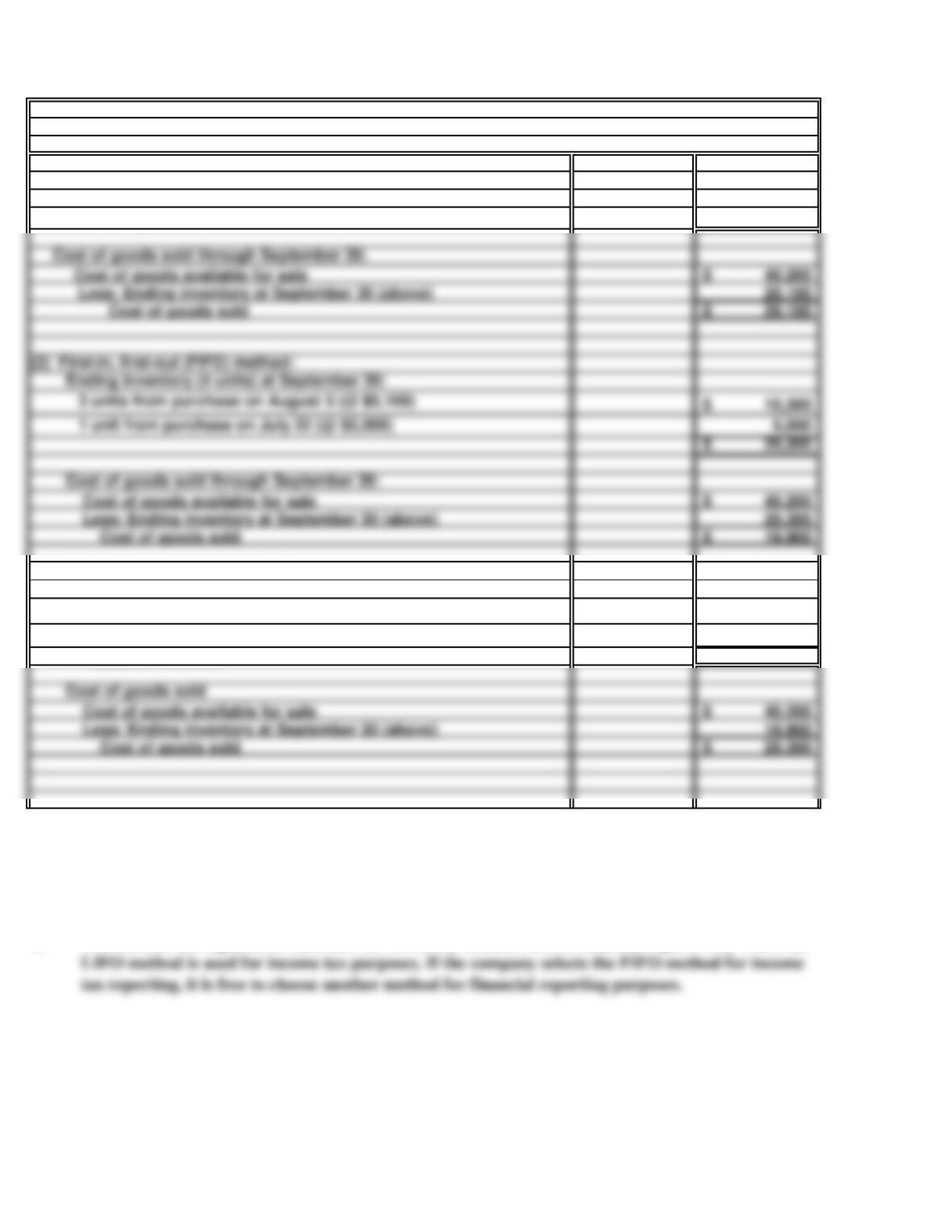

PROBLEM 8.2A

a. Cost of goods sold and ending inventory

SPEED WORLD CYCLES: PERPETUAL SYSTEM

Average cost (as of July 22; $24,900 ÷ 5 units)

Cost of goods sold (4 units @ $4,980)

2 units from July 22 purchase @ $5,000

1 unit from July 22 purchase @$5,000

Ending inventory, September 30

3 units from August 3 purchase @ $5,100

(b) Ending inventory (4 units) at September 30:

4,980$

15,300

5,070$

(2) First-in, first-out (FIFO) method:

(a) Cost of goods sold on July 28:

Average unit cost as of August 3 ($20,280 ÷ 4 units)

3 units purchased on August 3

Total

Average unit cost following August 3 purchase:

1 unit at July 22 average cost of $4,980

b. (1)

(2)

(3)

In this situation, the LIFO method will minimize income taxes, as it assigns the most recent

No. Speed World may not use FIFO in its financial statements and LIFO in its income tax

PROBLEM 8.2A

SPEED WORLD CYCLES: PERPETUAL SYSTEM (concluded)

The FIFO method will result in the highest net income, as it assigns the oldest (lowest) costs to

20 Minutes, Medium

(1) Average-cost method:

Ending inventory at September 30:

5,025$

20,100$

(3) Last-in, first-out (LIFO) method:

Ending inventory at September 30:

9,900$

10,000

19,900$

Cost of goods sold

Cost of goods available for sale

Less: Ending inventory at September 30 (above)

Cost of goods sold

b.

Yes. Income tax regulations influence the inventory method used in financial reports only when the

2 units from purchase on July 22 (@ $5,000)

Ending inventory

Note to instructor: Students may point out that ending inventory computed under LIFO is the same figure

as the cost of goods sold computed under FIFO. Likewise, the cost of goods sold figure computed under

LIFO is the same as the ending inventory figure computed under FIFO. The fact that these numbers are

the same is merely a coincidence.

PROBLEM 8.3A

a. Cost of goods sold and ending inventory

SPEED WORLD CYCLES: PERIODIC SYSTEM

Average cost ($40,200 ÷ 8 units)

Ending inventory (4 units @ $5,025)

2 units from purchase on July 1 (@ $4,950)

Cost of goods sold through September 30:

(2) First-in, first-out (FIFO) method:

Ending inventory (4 units) at September 30:

20,300$

Cost of goods sold through September 30:

Cost of goods available for sale

Less: Ending inventory at September 30 (above)

Cost of goods available for sale

Less: Ending inventory at September 30 (above)

Cost of goods sold

Cost of goods sold

20 Minutes, Medium

a. Shrinkage loss – 40 trees

1,000

Inventory 1,000

Inventory 3,370

(2) Write-down of inventory to the lower-of-cost-or-market:

Cost of Goods Sold

c.

(1) Average-cost method:

PROBLEM 8.4A

MARY’S NURSERY

b. Shrinkage loss and LCM adjustment

(1) Shrinkage loss, first-in, first-out (FIFO) method:

Cost of Goods Sold

The only unethical act in this situation was committed by the employee against his employer. There

Inventory 1,208

1,560

(2) Last-in first-out (LIFO) method:

Cost of Goods Sold

Cost of Goods Sold

25 Minutes, Easy

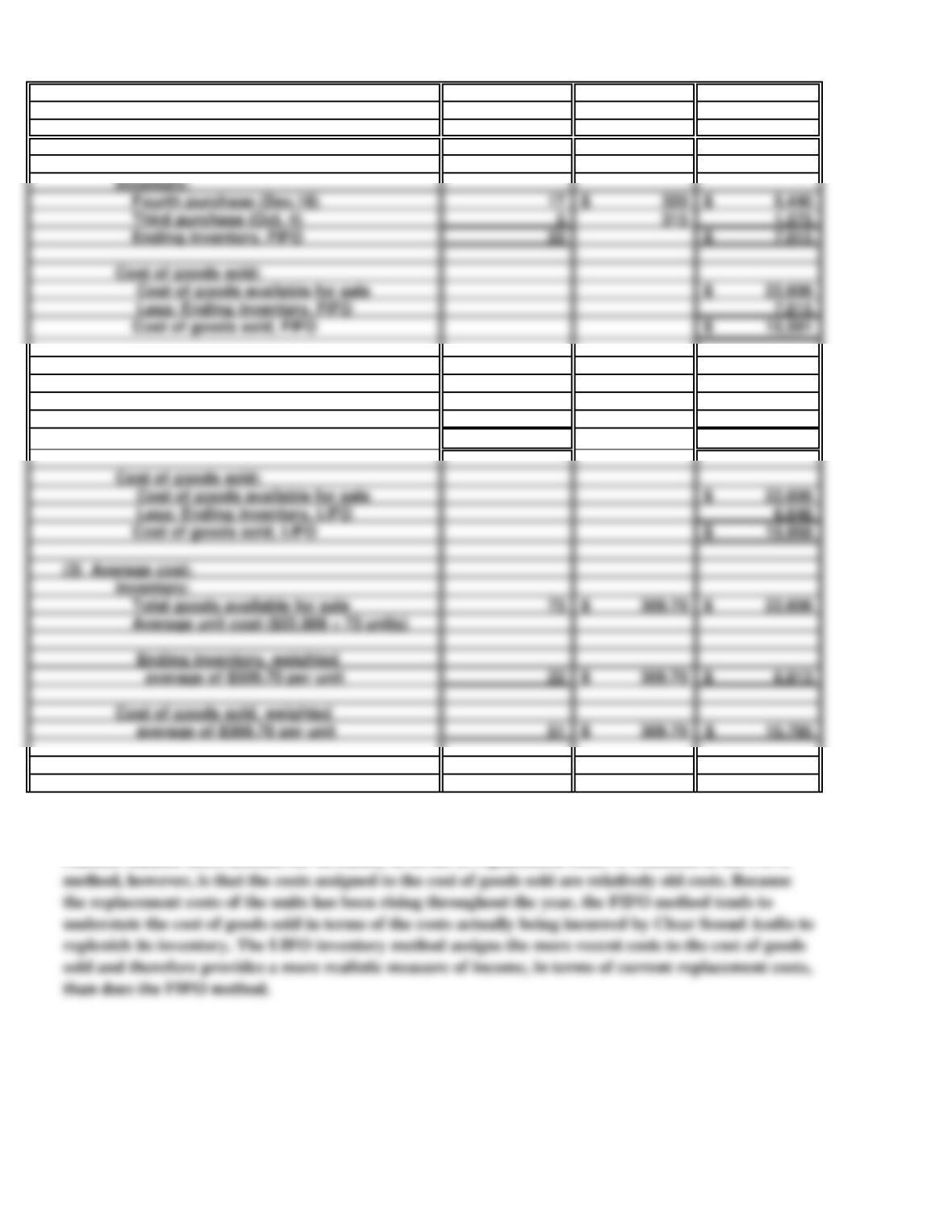

Units Unit Cost Total Cost

a. Inventory and cost of goods sold:

(1) FIFO:

(2) LIFO:

Beginning inventory 12 299$ 3,588$

First purchase (May 12) 10 306 3,060

Ending inventory, LIFO 22 6,648$

Cost of goods available for sale 22,606$

Less: Ending inventory, LIFO 6,648

(3) Average cost:

Average unit cost ($22,606 ÷ 73 units)

Ending inventory, weighted

average of $309.70 per unit 22 309.70$ 6,813$

b.

PROBLEM 8.5A

CLEAR SOUND AUDIO

Inventory:

The FIFO method, by assigning the costs of the most recent purchases to inventory, provides the most

realistic balance sheet amount for inventory in terms of replacement costs. A weakness in the FIFO

Fourth purchase (Dec.18) 17 320$ 5,440$

Third purchase (Oct. 4) 5 315 1,575

Ending inventory, FIFO 22 7,015$

Cost of goods available for sale 22,606$

Less: Ending inventory, FIFO 7,015

20 Minutes, Medium

a.

2018 2017 2016

Net sales 875,000$ 840,000$ 820,000$

Cost of goods sold 563,000 527,200 440,000$

b.

The current owners of this business have no basis for being enthusiastic about the trend of gross profit

PROBLEM 8.6A

HEALTH FOODS

25 Minutes, Medium

a.

b.

84,480$

55%

46,464$

52,800$

6,336$

744,000$

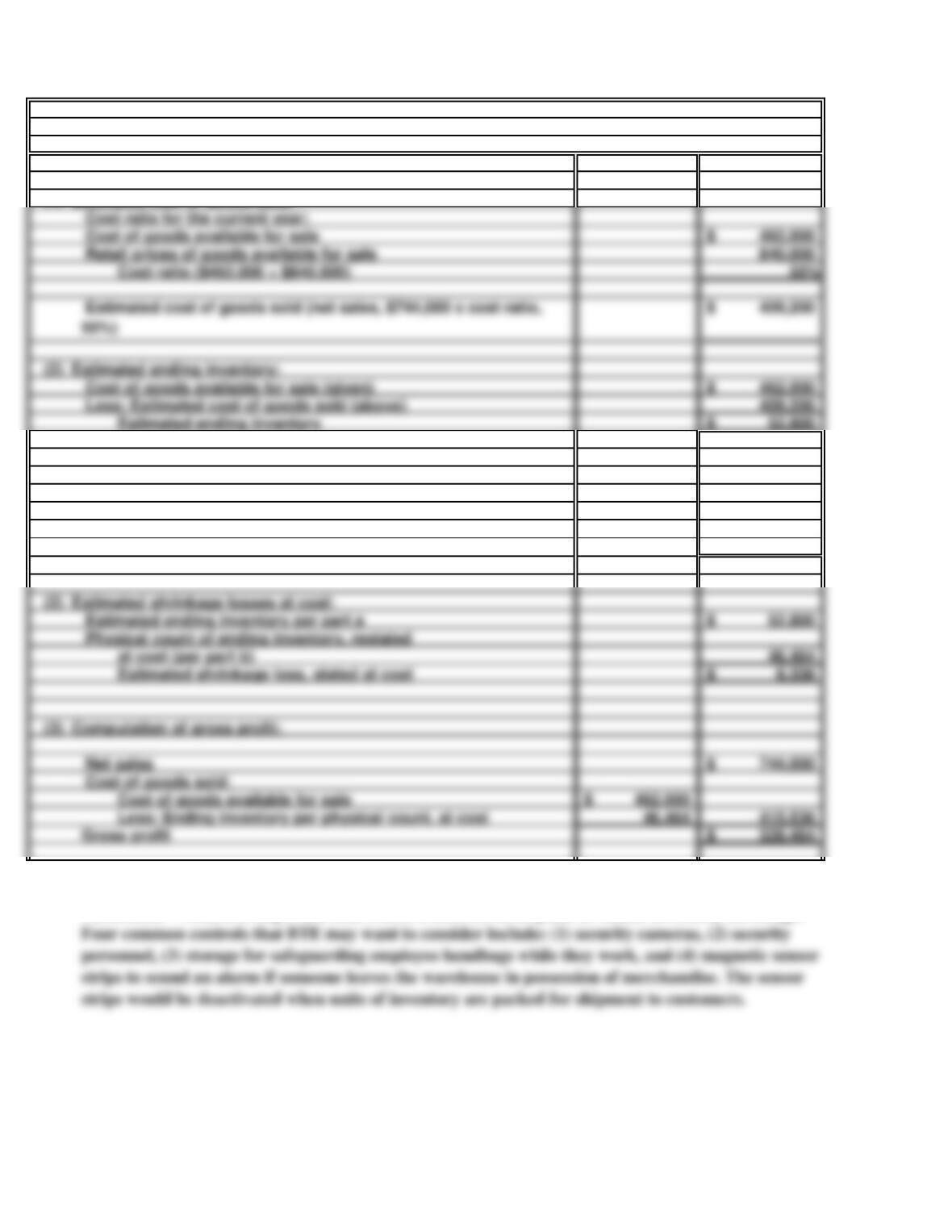

462,000$

46,464 415,536

Gross profit 328,464$

Cost of goods available for sale

(3) Computation of gross profit:

Estimated shrinkage loss, stated at cost

at cost (per part b)

Net sales

Cost of goods sold:

Less: Ending inventory per physical count, at cost

(2) Estimated shrinkage losses at cost:

Estimated ending inventory per part a

Physical count of ending inventory, restated

c.

CDs and recorded music in other formats can easily fit into someone’s pocket and “walk out of the

warehouse.” Thus, it is important that effective controls be in place to reduce inventory shrinkage.

(1) Restating physical inventory from retail prices to cost:

Physical inventory stated in retail prices

Cost ratio (per part a, above)

Ending inventory at cost ($84,480 x 55%)

(1) Estimated cost of goods sold:

PROBLEM 8.7A

BETWEEN THE EARS

462,000$

840,000

55%

462,000$

409,200

52,800$

Cost ratio for the current year:

Less: Estimated cost of goods sold (above)

Estimated ending inventory

(2) Estimated ending inventory:

Cost of goods available for sale (given)

Cost of goods available for sale

Retail prices of goods available for sale

Cost ratio ($462,000 ÷ $840,000)

20 Minutes, Strong

a. Computations based on LIFO valuation of inventory:

(1) Inventory turnover rate:

Cost of Goods Sold = 365,086$ 8.11 times

c. You would expect the ratios to be different under FIFO as follows:

the year.

PROBLEM 8.8A

WAL-MART

Average inventory 45,000$

(2) Current ratio:

Current Assets = 63,278$ 0.97 : 1

Current Liabilities 65,272$

(3) Gross profit rate:

Net Sales 482,229$

35 Minutes, Medium

Jan 22 14,800

Inventory 14,800

Jan 22 14,600

Inventory 14,600

Jan 22 15,400

Inventory 15,400

(4) Last-in, First-out (LIFO) method:

Cost of Goods Sold

To record cost of 700 cartridges sold to Foster

Office Fitters by the FIFO flow assumption:

Office Fitters by the LIFO flow assumption

SOLUTIONS TO PROBLEMS SET B

PROBLEM 8.1B

DOBBINS SUPPLY, INC.

Cost of Goods Sold

a.

2018

General Journal

(1) Specific identification method:

(3) First-in, First-out (FIFO) method:

Cost of Goods Sold

To record cost of 700 cartridges sold to Foster

Jan 22 15,050

Inventory 15,050

Cost of Goods Sold

Office Fitters by the average-cost method: 700

To record cost of 700 cartridges sold to Foster

To record cost of 700 cartridges sold to Foster

(2) Average-cost method:

b. Inventory subsidiary ledger records:

(1) Specific identification method:

DOBBINS SUPPLY INC. (cont.)

Date Units Unit Cost Total Units Unit Cost

Cost of

Goods Sold

Units Unit Cost Balance

Dec 12 400 20$ 8,000$ 400 20$ 8,000$

400 22 14,800$ 800 22 19,600

(2) Average-cost method:

Date Units Cost Total Units Unit Cost

Cost of

Goods Sold

Units Cost Balance

Dec 12 400 20$ 8,000$ 400 20.00$ 8,000$

Jan 16 1,200 22 26,400 1,600 21.50 34,400

Jan 22 700 21.50$ 15,050$ 900 21.50 19,350

* $34,400 total cost ÷ 1,600 units = $21.50 average unit cost.

(3) First-in, first-out (FIFO) method:

Goods Sold

Dec 12 400 20$ 8,000$ 400 20$ 8,000$

Jan 16 1,200 22 26,400 400 20

1,200 22 34,400

Jan 22 400 20$

300 22 14,600$ 900 22 19,800

(4) Last-in, first-out (LIFO) method:

Cost of

Dec 12 400 20$ 8,000$ 400 20$ 8,000$

Jan 16 1,200 22 26,400 400 20

1,200 22 34,400

Jan 22 700 22$ 15,400$ 400 20

500 22 19,000

PURCHASED

SOLD

BALANCE

Cost of

PROBLEM 8.1B

PURCHASED

SOLD

BALANCE

PURCHASED

SOLD

BALANCE

PURCHASED

SOLD

BALANCE

Jan 16 1,200 22 26,400 400 20

1,200 22 34,400

Jan 22 300 20$ 100 20

c.

PROBLEM 8.1B

DOBBINS SUPPLY, INC. (concluded)

Yes. As shown in part a, the LIFO method resulted in the highest cost of goods sold figure, whereas