Present economic resource

Held for use in

On a

Not for sale in

Classification of non-current (fixed) assets

T. non-current (fixed) assets

I. non-current (fixed) assets

Investments held long term

Intangible No substance.

P..

T..

D.

G..

Valuation of non-current (fixed) assets initially at cost

Subsequently choose either

at C. less A.D....

Also called N.. B. V.. (NBV)

or depreciated cost

Financial Accounting

Asset is recorded at

Usually applied to ..

Revaluation is a .. for the company.

If used, revaluations must be updated .

What is cost?

What is depreciation?

P. of an asset plus the .. it for use

(legal costs of acquisition and installation and commissioning costs).

Improvement expenditure may result in:

. the assets annual output capacity;

its economic life;

. associated running costs;

. the quality of its output).

Costs incurred to improve on the assets original condition:

These costs should be added to the original cost of the asset and depreciated over the remainder

of its useful life.

.......

Financial Accounting

DEPRECIATION

There are many views as to the nature of depreciation.

Accounting takes a limited view:

Non-current (fixed) assets are . in providing goods and

services over time.

The purpose of accounting depreciation is to of a non-current

(fixed) asset over its expected useful life.

Depreciation is a method of cost.

It achieves a .. costs against the related revenues.

In historical cost (traditional) accounting:

The net book value (NBV) of a non-current (fixed) asset is the result of a calculation:

Original cost minus A.. D

It is not intended to represent the assets .

Year Assets minus Liabilities equal Ownership

interest

Each year that a non-current (fixed) asset is in use, a portion of its cost is deducted from the

value shown in the statement of financial position (balance sheet). That portion of cost is

matched against the revenues of that year. This gives the

.

(income statement/profit and loss account).

Financial Accounting

Calculation of depreciation requires three items of information:

the .of the non-current (fixed) asset;

the estimated and

the estimated . (the value remaining at the end of the useful life).

The . depreciation of the non-current (fixed) asset is equal to the .of the

non-current (fixed) asset minus the estimated …

(a) ... method

(b) method

Those who believe that a non-current (fixed) asset is usedover time

apply a method of calculation called straight-line depreciation.

The formula is:

____________________________________

Example

A non-current (fixed) asset has a cost of £1,000 and an expected life of 5 years. The expected

residual value is nil. The calculation of the annual depreciation charge is:

_________________________ = £per annum

The depreciation rate is sometimes expressed as a ..

In this case, the company would state its depreciation policy as given below:

Accounting policy:

Depreciation is charged on a straight-line basis at . per

annum.

Financial Accounting

The phrase straight line is used because a graph of of the

asset at the end of each year produces a straight line.

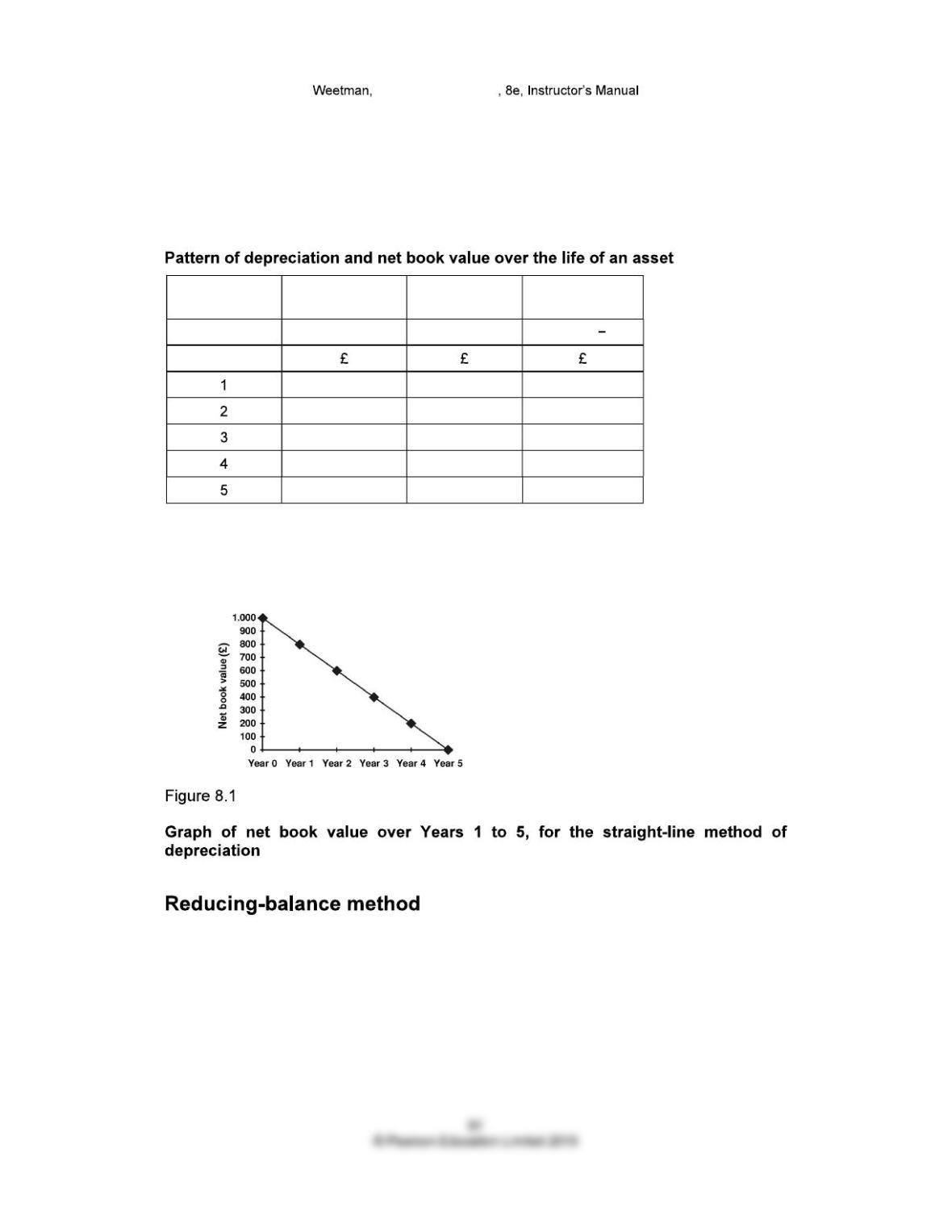

Pattern of depreciation and net book value over the life of an asset

End of year Depreciation of

the year

Total

depreciation

Net book value

of the asset

(b) (c) (£1,000 c)

Straight-line method of depreciation: graph of net book value over

years 1 to 5

Those who believe that a non-current (fixed) asset depreciates in the

.years of its life would calculate the depreciation using the formula:

..

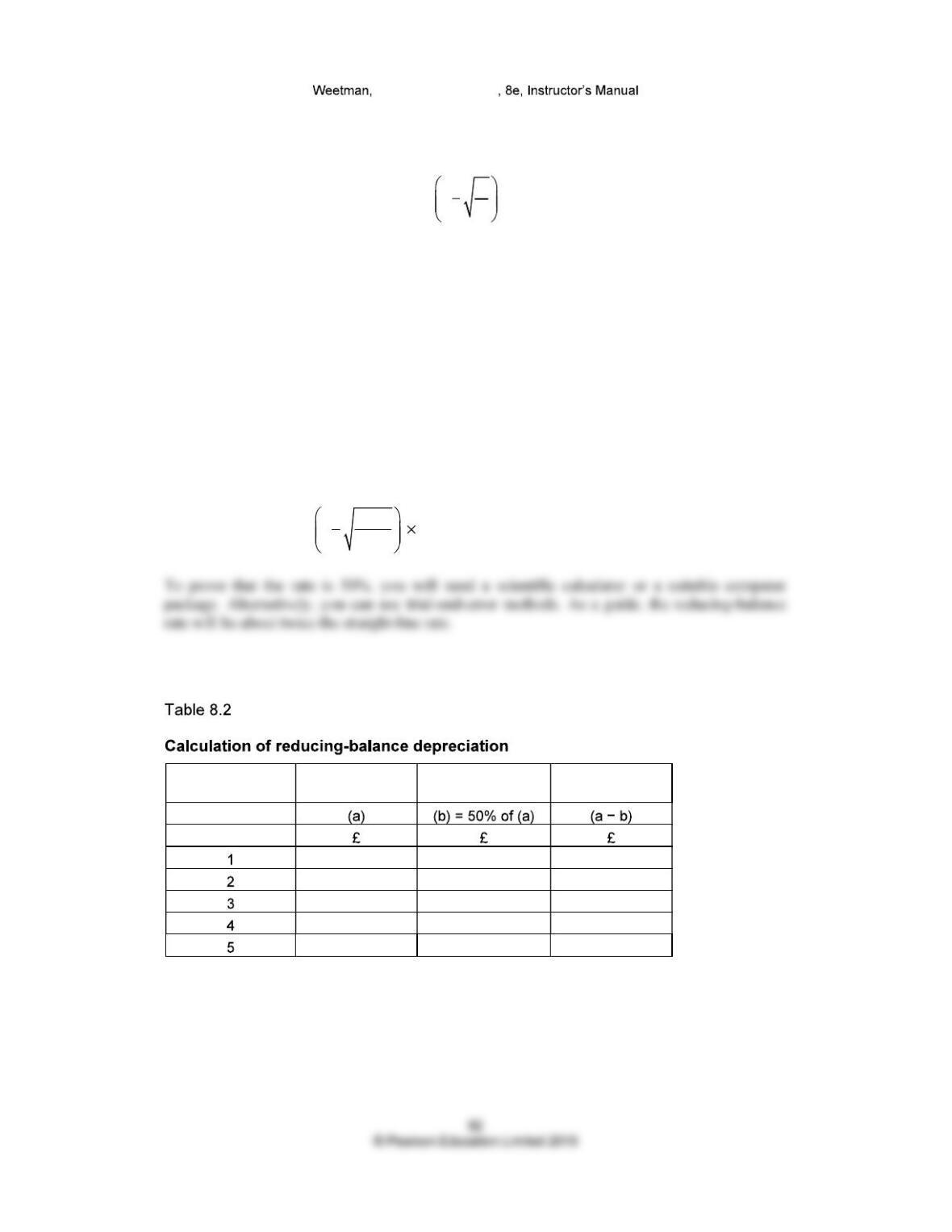

What is the fixed percentage?

Financial Accounting

The rate of depreciation to be applied under the reducing balance method of depreciation may

be calculated by the formula:

rate = 1 nR

C × 100%

where n = .

R = .

C = .

For the asset costing £1,000 with a 5-year life and small residual value (say £30):

n = 5 years

C = £1,000

R = £30 (The residual value must be of reasonable magnitude. Using an amount of nil

for the residual value would result in a rate of 100%).

rate = 530

11,000 100% = approx 50%

Calculation of reducing-balance depreciation

Year Net book value

at start of year

Annual

depreciation

Net book value

at end of year

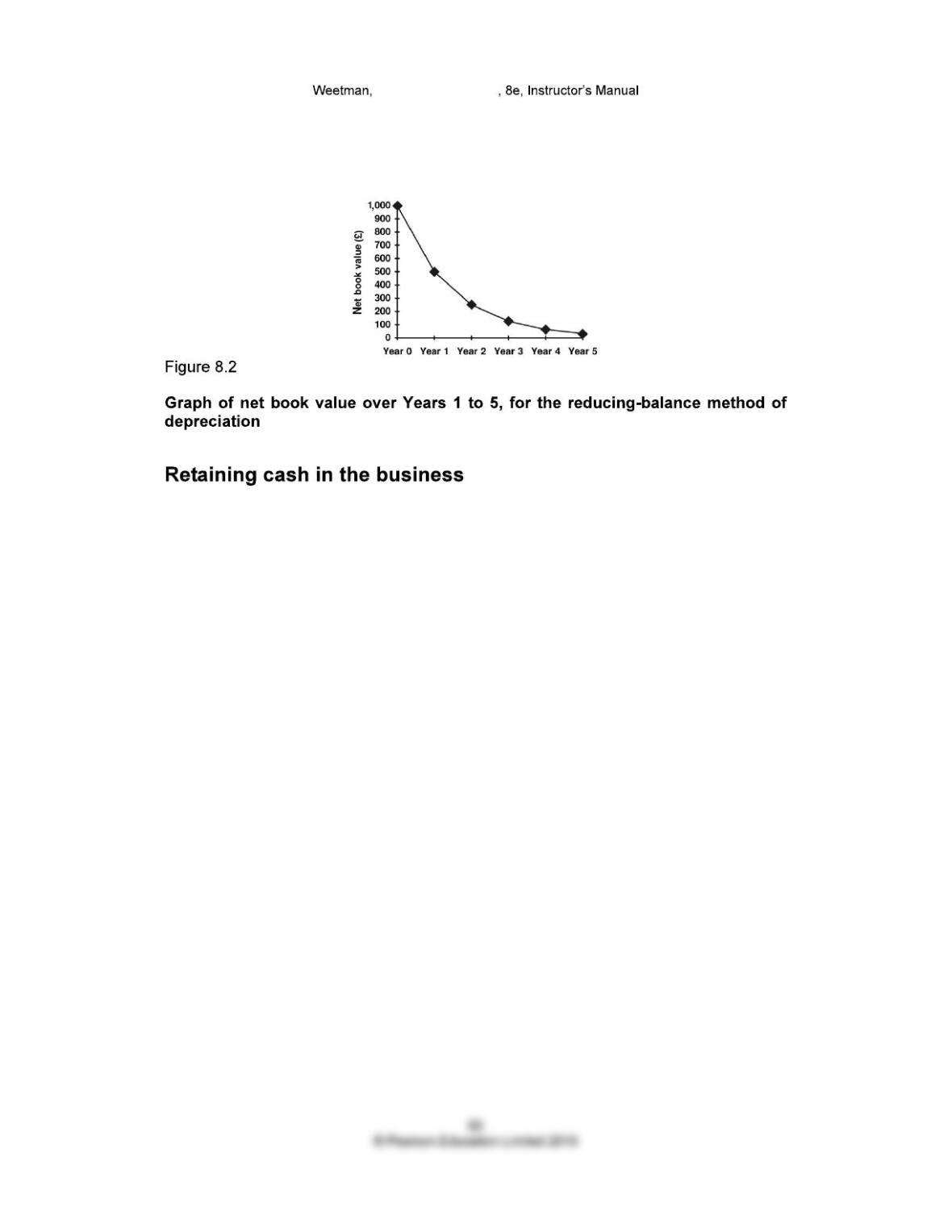

The steep slope at the beginning shows that the net book value declines rapidly in the early part

of the assets life and then less steeply towards the end when most of the benefit of the asset has

been used up.

Financial Accounting

Reducing-balance method of depreciation: graph of net book value over

years 1 to 5

Fee income, £120,000; pay wages and other costs, £58,000; depreciation calculated as £10,000

How much may the owner take in drawings?

Cash available is £..

But if that is taken for personal use, there is

Take cash of £.. leave..

Problem business may spend .on other aspects of business, such as:

Financial Accounting

On 1 January Year 2, Electrical Instruments purchased a three-year lease of a shop for £60,000.

The accounts over the next three years would include the following items related to the lease:

Income statement

(profit and loss account)

Statement of financial position

(balance sheet

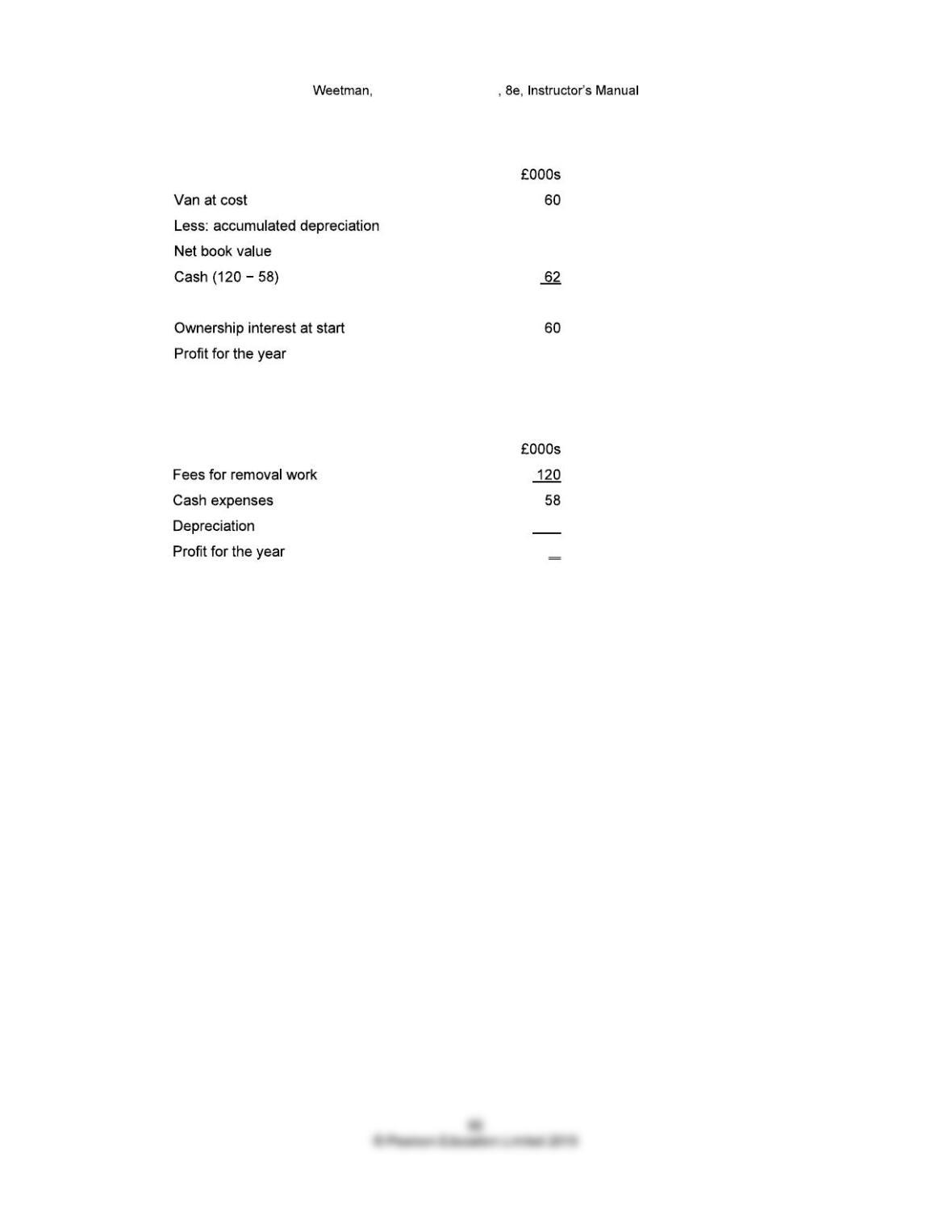

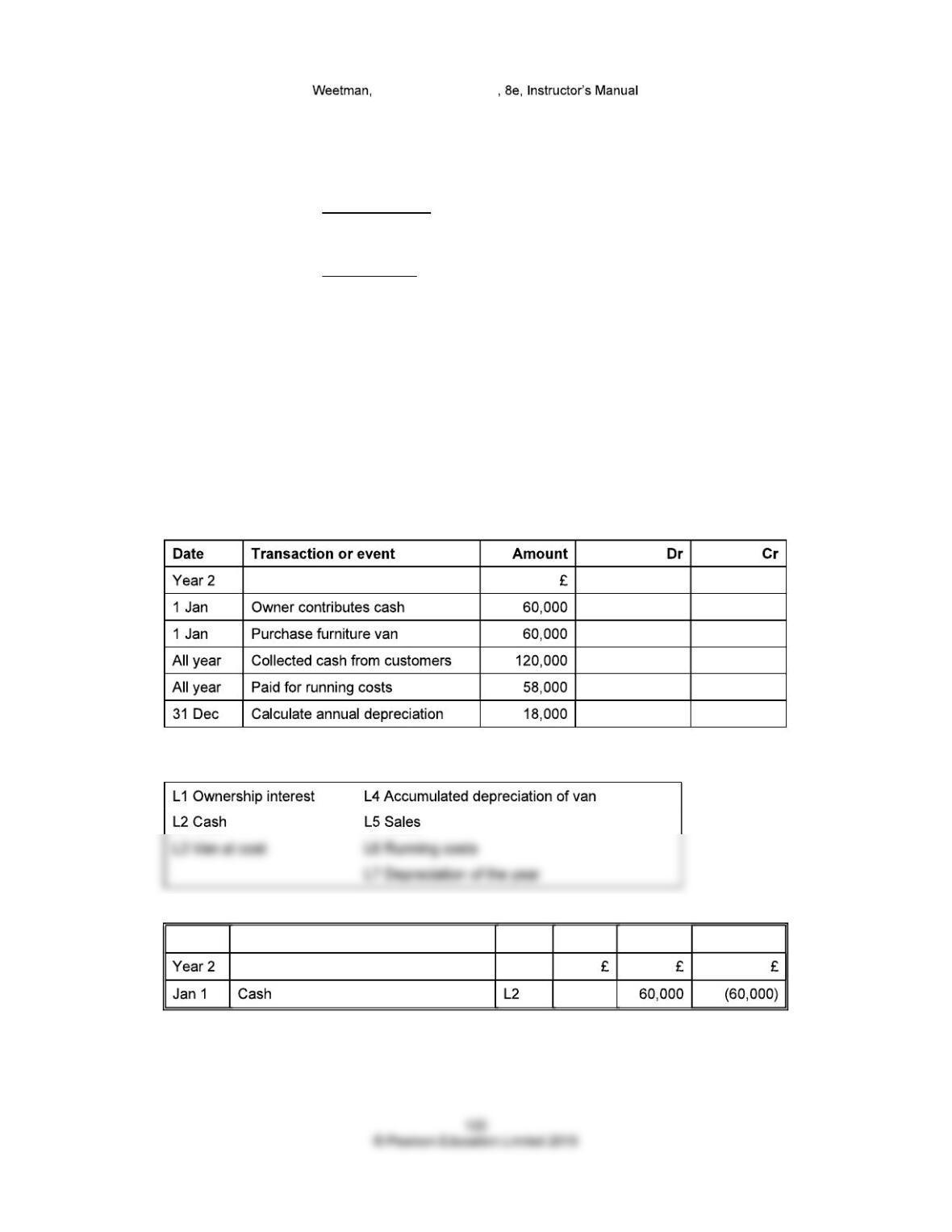

The Removals Company was set up on 1 January Year 2, purchased a van for £60,000 and

started to trade.

The manager estimates that:

the van will be used for 3 years and

at the end of that time, it will have a residual value of £6,000 (second hand or scrap value).

Net cost of the van (………...... ...………..) = £……………..

Net cost has to be …………………over…..………..years.

Financial Accounting

Statement of financial position (balance sheet) at 31 December Year 2

Income statement (profit and loss account) for Year to 31 Dec Year 2

Financial Accounting

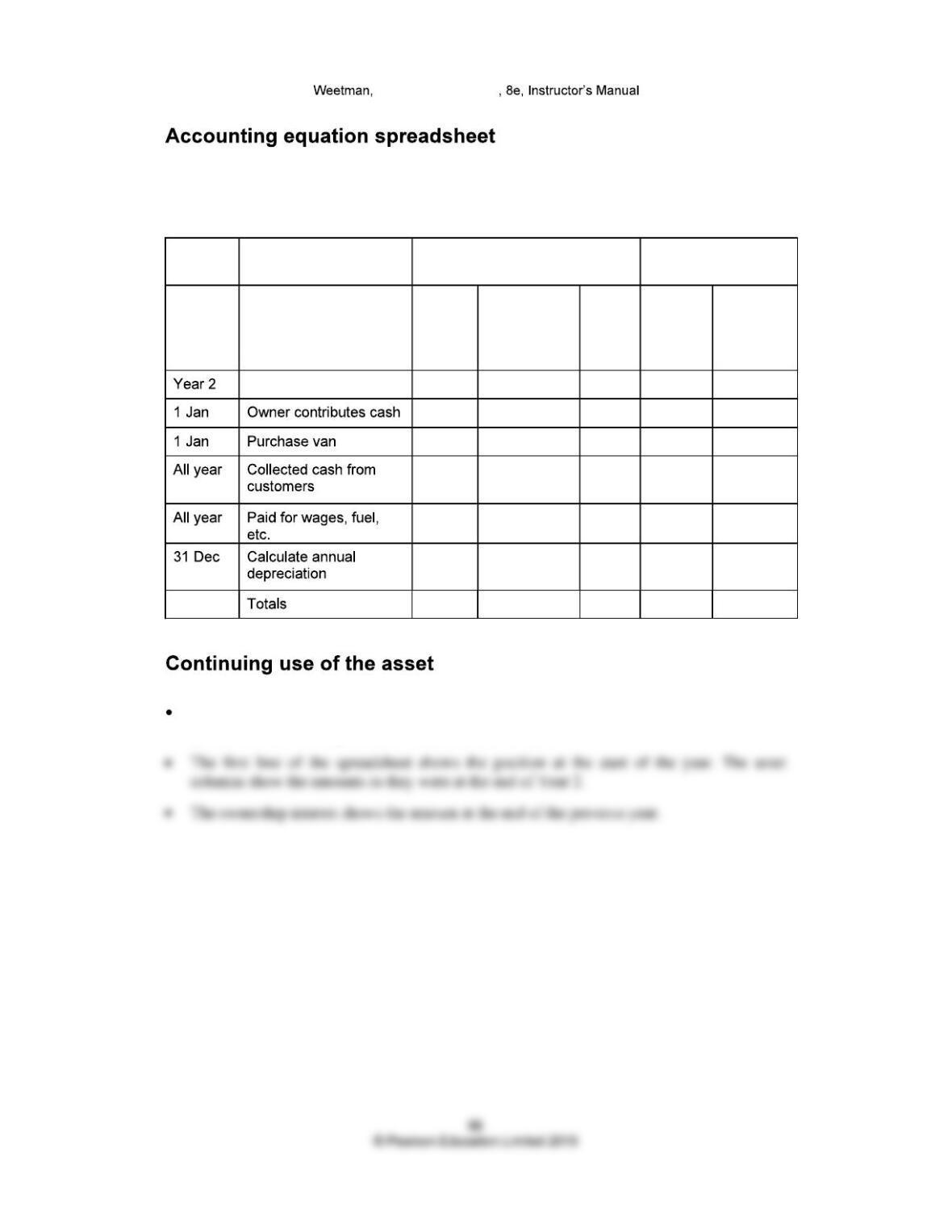

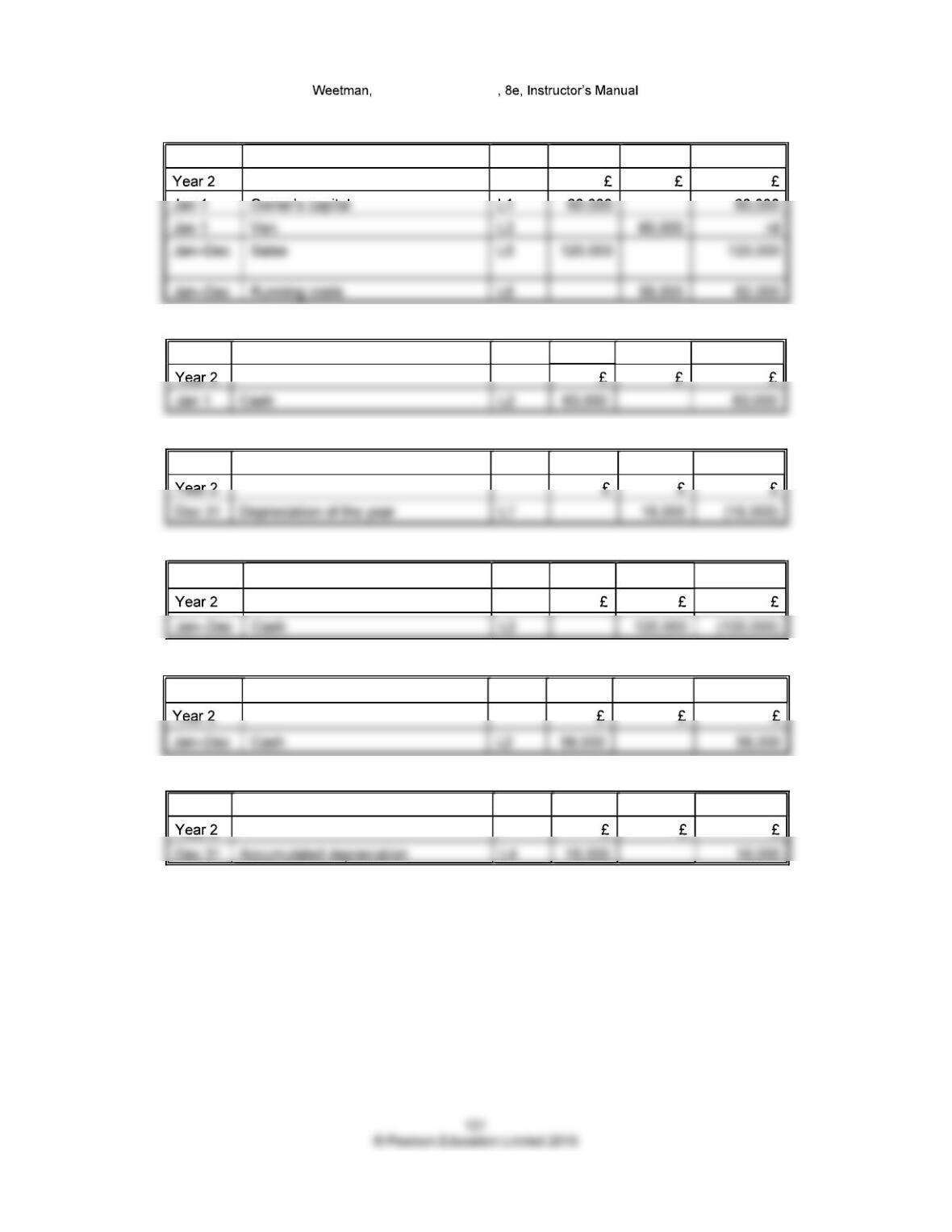

Spreadsheet analysis of transactions of The Removals Company, Year 2

Assets Ownership interest

Transaction or event Van at

cost

Accumulated

depreciation

of van

Cash OI

increase

Profit =

revenue

minus

expenses

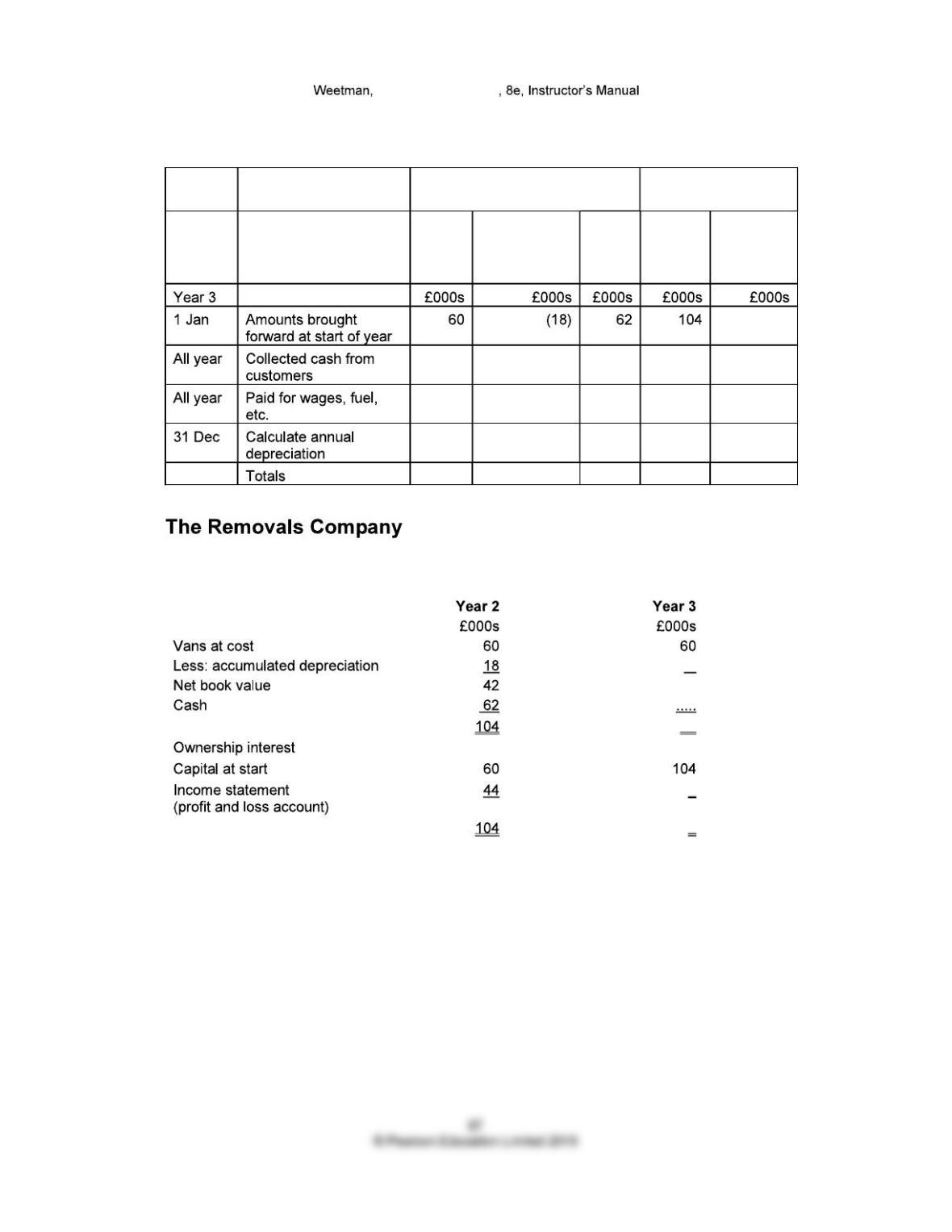

It is assumed that for Year 3, the amounts of cash collected from customers and the amounts

paid in cash for running costs are the same as for Year 2.

Financial Accounting

Spreadsheet analysis of transactions of The Removals Company, Year 3

Assets Ownership interest

Transaction or event Van at

cost

Accumulated

depreciation

of van

Cash OI at

start of

year

Profit =

revenue

minus

expenses

Statement of financial position (balance sheet) at 31 December

Financial Accounting

Income statement (profit and loss account) for Year to 31 December

Statement of financial position (balance sheet)

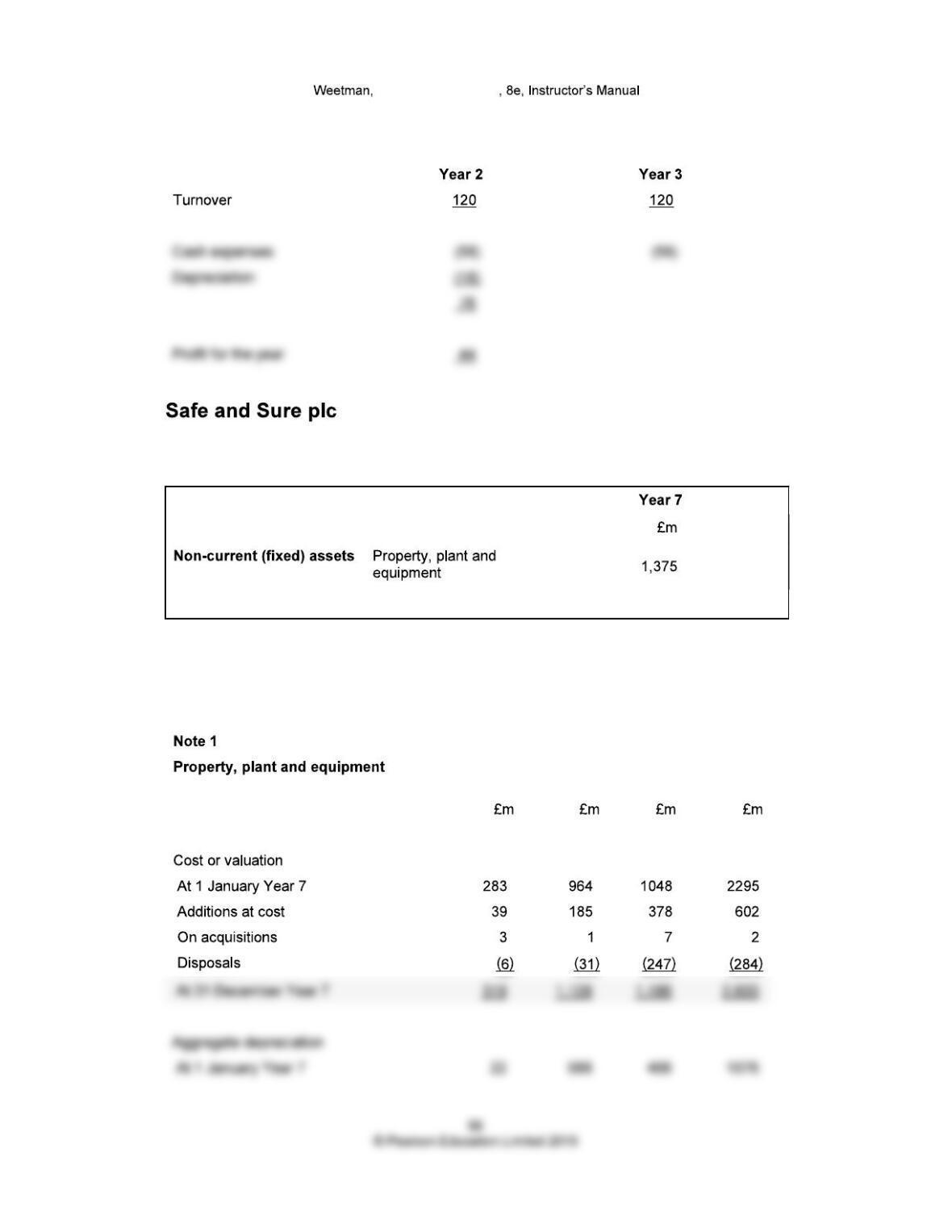

Notes Year 6

£m

1 1,219

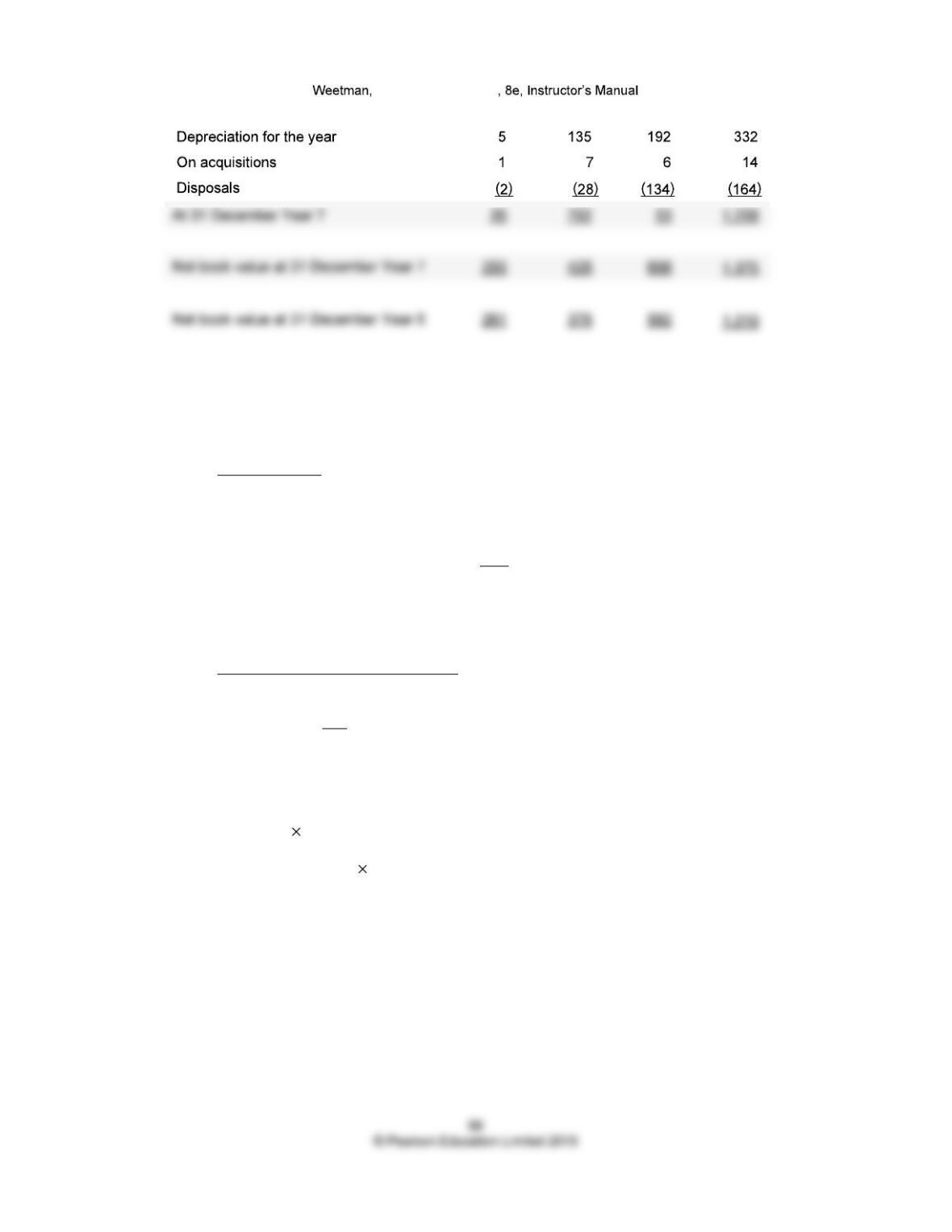

Notes to the statement of financial position (balance sheet)

In the notes to the statement of financial position (balance sheet), there is considerably more

information:

Land and

buildings

Plant and

equipment

Vehicles Total

Financial Accounting

What can we learn about the company from this information?

1. How up to date are the non-current (fixed) assets of the organisation?

(i) Average useful life of plant and equipment:

Cost at year end

.

Taking 31 December Year 7 £ m. = years

£ m.

(ii) Proportion of cost that has been depreciated:

………………………..………………………….

Cost at the year end

£ m = .

£ ……….. m:

(iii) Average age of plant and equipment

Average useful life proportion of cost depreciated.

………………… ………….………………. = .…………………………... years old

Financial Accounting

2. How efficiently are assets being used? (Fixed asset turnover)

We are told that turnover for Year 7 is £754.6 million (Year 6 £611.3 million)

Turnover (Sales)

£754.6 million = …………………..………

million.

OR £……….…………… sales are generated by each £1 of

……………………..………………………..………………

Compare this with the following:

(i) …..………………………………..………………………..…………………………….

(ii) ..………………………….………………………….…………………………………..

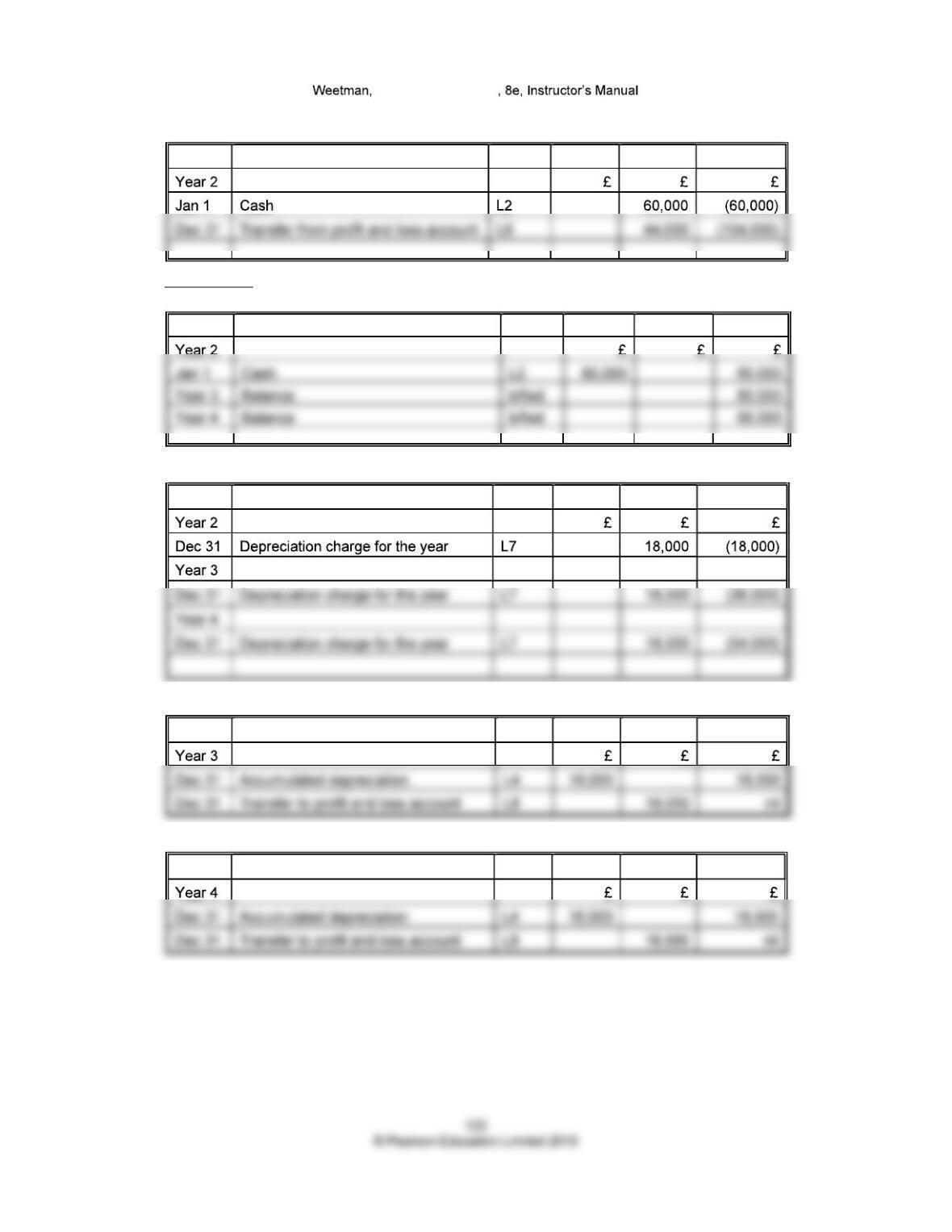

Analysis of transactions for The Removals Company, Year 2

Ledger accounts required to record transactions of Year 2

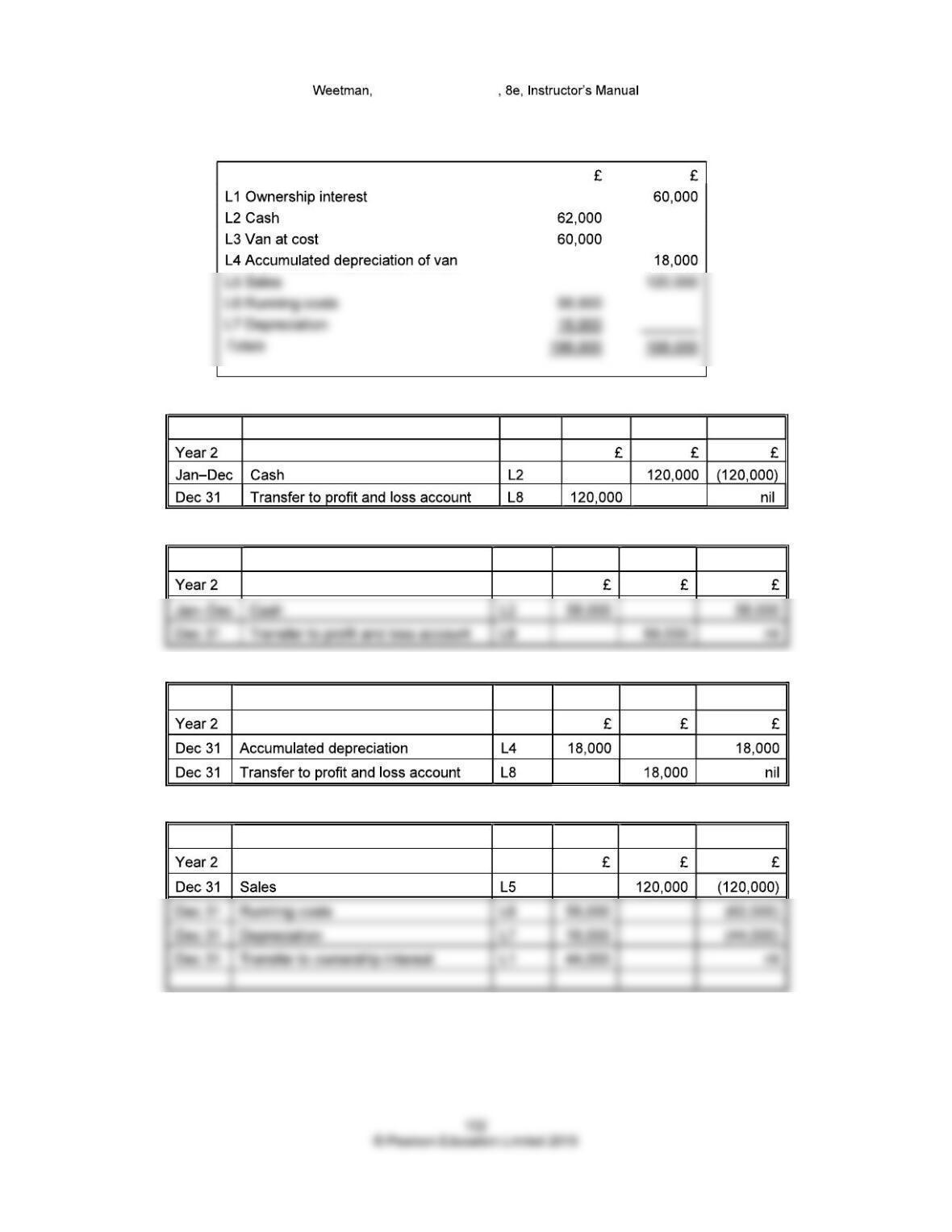

L1 Ownership interest

Date Particulars Page Debit Credit Balance

Financial Accounting

L2 Cash

Date Particulars Page Debit Credit Balance

L3 Van at cost

Date Particulars Page Debit Credit Balance

L4 Accumulated depreciation of van

Date Particulars Page Debit Credit Balance

L5 Sales

Date Particulars Page Debit Credit Balance

L6 Running costs

Date Particulars Page Debit Credit Balance

L7 Depreciation of the year

Date Particulars Page Debit Credit Balance

Financial Accounting

Trial balance at the end of Year 2 for The Removals Company

Ledger account title

L5 Sales

Date Particulars Page Debit Credit Balance

L6 Running costs

Date Particulars Page Debit Credit Balance

L7 Depreciation of the year

Date Particulars Page Debit Credit Balance

L8 Profit and loss account

Date Particulars Page Debit Credit Balance

Financial Accounting

L1 Ownership interest

Date Particulars Page Debit Credit Balance

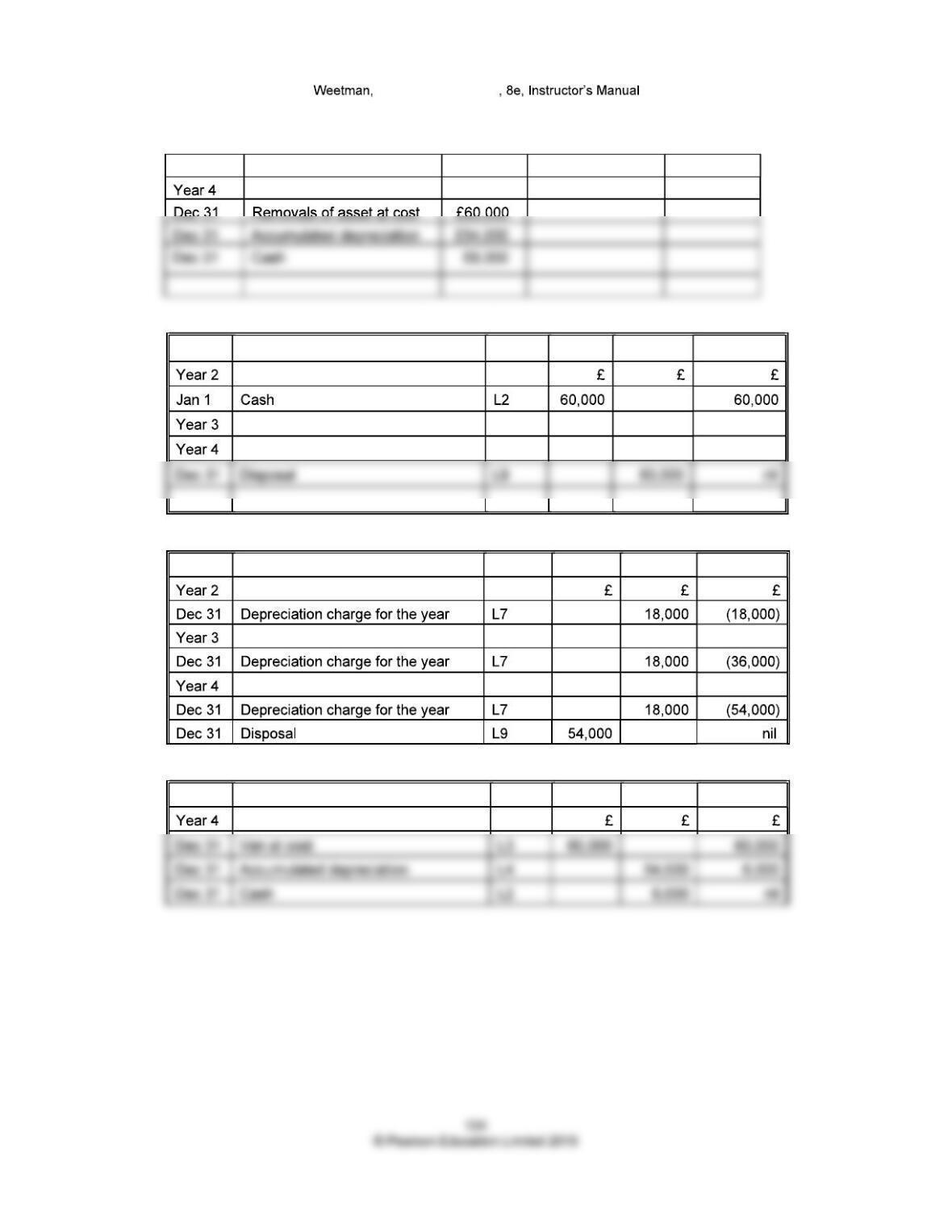

Years 3 and 4

L3 Van at cost

Date Particulars Page Debit Credit Balance

L4 Accumulated depreciation

Date Particulars Page Debit Credit Balance

L7 Depreciation of the year

Date Particulars Page Debit Credit Balance

L7 Depreciation of the year

Date Particulars Page Debit Credit Balance

Financial Accounting

Disposal of the asset

Date Transaction or event Amount Dr Cr

L3 Van at cost

Date Particulars Page Debit Credit Balance

L4 Accumulated depreciation

Date Particulars Page Debit Credit Balance

L9 Non-current (fixed) asset disposal account

Date Particulars Page Debit Credit Balance

Financial Accounting

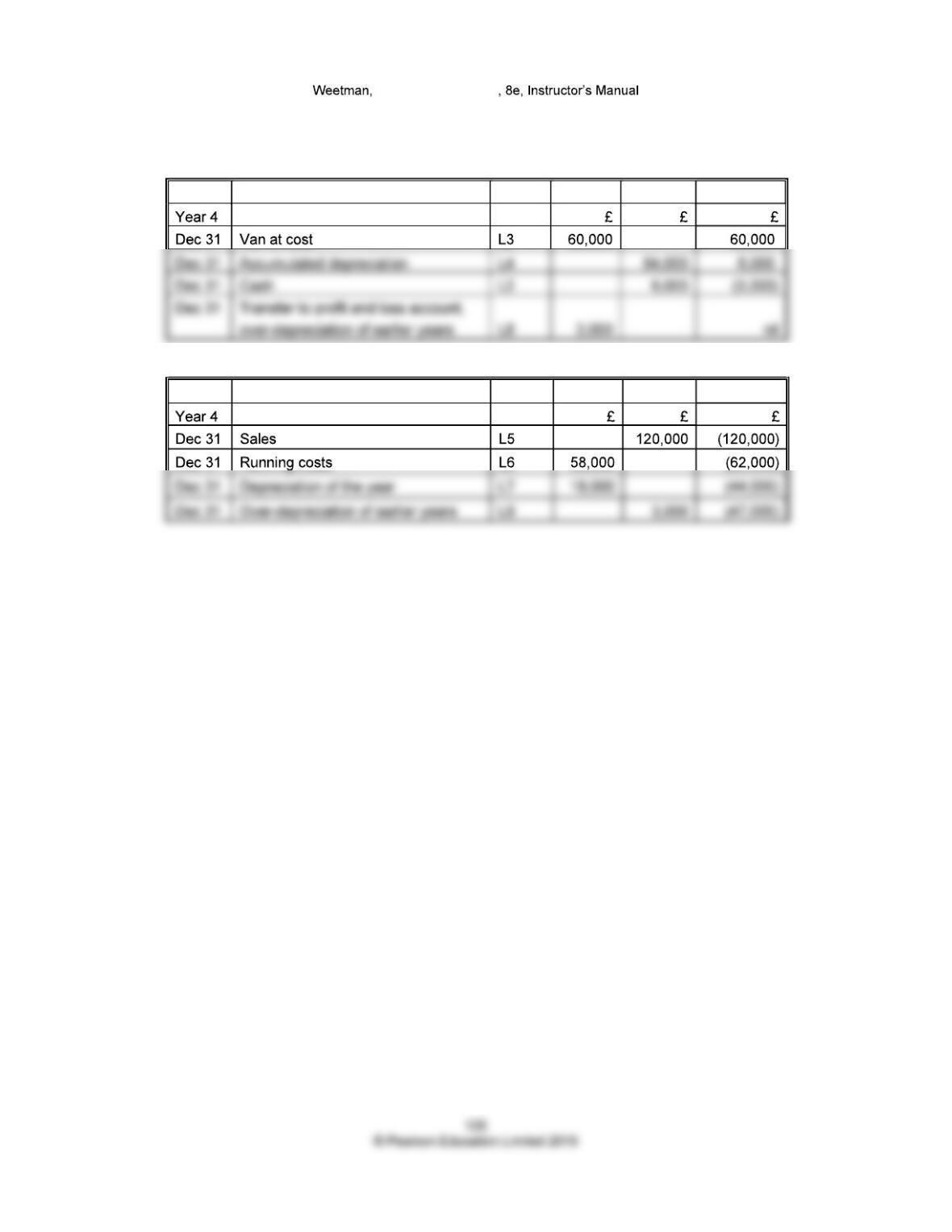

Sale for an amount greater than the net book value

L9 Non-current (fixed) asset disposal account

Date Particulars Page Debit Credit Balance

L8 Profit and loss account

Date Particulars Page Debit Credit Balance