Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

chapter

8

Receivables

______________________________________________

OPENING COMMENTS

Chapter 8 presents the accounting issues related to accounts receivable and notes receivable. The chapter

opens with the common classifications of receivables. While presenting those classifications, you will

need to make a clear distinction between accounts receivable and notes receivable.

Accounting issues related to uncollectible receivables are covered next. Both the allowance and direct

write-off methods are presented. If class time is scarce at this point, coverage of the direct write-off

method (theoretically unacceptable because it violates the matching concept) may be omitted without

disrupting the flow of the text. Simply omit coverage of Objectives 3 and 5.

The last part of the chapter presents a Financial Analysis and Interpretation section that discusses

financial ratios related to receivables: the accounts receivable turnover and the number of days’ sales in

receivables.

After studying the chapter, your students should be able to:

2. Describe the accounting for uncollectible receivables.

4. Describe the allowance method of accounting for uncollectible receivables.

6. Describe the accounting for notes receivable.

7. Describe the reporting of receivables on the balance sheet.

8. Describe and illustrate the use of accounts receivable turnover and number of days’ sales in

receivables to evaluate a company’s efficiency in collecting its receivables.

KEY TERMS

accounts receivable

accounts receivable turnover

aging the receivables

Allowance for Doubtful Accounts

allowance method

bad debt expense

direct write-off method

dishonored note receivable

maturity value

net realizable value

notes receivable

number of days’ sales in receivables

receivables

STUDENT FAQS

• Why should we have to learn the direct write-off method of recording bad debts when we cannot use

it with the accrual basis of accounting?

• How accurate are companies with their estimates (guesses)?

• Isn’t estimating bad debts a way of manipulating net income?

• How does a company keep control on these estimates?

• How does one go about determining if uncollectible receivables are within a reasonable range?

• How can Allowance for Doubtful Accounts have a debit balance? Does that mean the company did

something wrong? Can Allowance for Doubtful Accounts have a debit balance at the end of the year

after adjustments have been made?

Chapter 8 Receivables 147

OBJECTIVE 1

Describe the common classes of receivables.

SYNOPSIS

Receivables include all money claims against other entities and may be a significant part of the current

assets. There are two different classes of receivables discussed. An account receivable is created when a

customer receives merchandise but does not pay when they receive the goods. The amount that they owe

Key Terms and Definitions

• Account Receivable - A claim against the customer created by selling merchandise or services

on credit.

• Notes Receivable - A customer’s written promise to pay an amount and possibly interest at an

agreed-upon rate.

• Receivables - All money claims against other entities, including people, business firms, and other

organizations.

SUGGESTED APPROACH

The purpose of this objective is to familiarize students with terms related to receivables. Hints for your

review of those terms follow.

LECTURE AID—Classification of Receivables

The common classifications of receivables are the following:

2. Notes Receivable — credit granted through a formal credit instrument known as a promissory note.

Notes are often used for credit periods of more than 60 days and involve payment of interest.

3. Other Receivables — such as interest receivable or receivables resulting from loans to officers or

employees.

Trade receivables are receivables resulting from the sale of merchandise or services on credit. Both

accounts receivable and notes receivable can be classified as trade receivables.

148 Chapter 8 Receivables

Students generally have the most difficulty distinguishing between accounts receivable and notes

receivable. Remind them that an account receivable results from a credit sale on an open account, such as

Three things generally distinguish a note receivable from an account receivable:

2. Notes typically require a formal written agreement stating due date and interest rate.

3. Notes typically involve interest being paid.

OBJECTIVE 2

Describe the accounting for uncollectible receivables.

SYNOPSIS

One issue not yet discussed is that some customers will not pay their accounts. These accounts become

uncollectible. Some retailers shift this responsibility to other companies. If a business accepts only cash or

Key Terms and Definitions

• Allowance Method - The method of accounting for uncollectible accounts that provides an

expense for uncollectible receivables in advance of their write-off.

• Bad Debt Expense - The operating expense incurred because of the failure to collect receivables.

• Direct Write-Off Method - The method of accounting for uncollectible accounts that recognizes

the expense only when accounts are judged to be worthless.

SUGGESTED APPROACH

Objective 2 reminds students that a business incurs an expense when customers fail to pay. Three

common account titles used to record this expense are (1) uncollectible accounts expense, (2) bad debts

Chapter 8 Receivables 149

There are two methods of recording uncollectible accounts: direct write-off method and allowance

method. When introducing the two methods of recording uncollectible accounts, you will want to stress

OBJECTIVE 3

Describe the direct write-off method of accounting for uncollectible receivables.

SYNOPSIS

If using the direct write-off method, a company waits until a customer’s account is determined to be

worthless and then writes off that customer’s account. Bad Debt Expense is debited, and Accounts

Receivable is credited. If for some reason the account is later collected and payment is received, the

previous entry is reversed by debiting Cash and crediting the receivable. This method is used by

businesses that have a small percentage of their assets in receivables.

Relevant Example Exercises and Exhibits

• Example Exercise 8-1 Direct Write-Off Method

SUGGESTED APPROACH

Under the direct write-off method, the expense of an uncollectible account is recognized when the

company decides that further collection efforts on a delinquent account are useless. This method,

LECTURE AID—Direct Write-Off of Uncollectible Receivables

Under the direct write-off method, the following occur:

1. Uncollectible Accounts Expense is recorded when an account is written-off.

2. If an account that has been written-off is collected, the account is reinstated before recording

the payment received.

150 Chapter 8 Receivables

2. The amount of uncollectible accounts is immaterial.

TM 8-3 presents five transactions to be recorded under the direct write-off method. Ask your students to

work in small groups to journalize these transactions. TM 8-4 shows the solution to this exercise.

OBJECTIVE 4

Describe the allowance method of accounting for uncollectible receivables.

SYNOPSIS

If using the allowance method, a business estimates the uncollectible accounts receivable at the end of the

accounting period. The entry to Bad Debt Expense is an adjusting entry recorded at the end of the period.

Since this entry is an estimate of the total amount uncollectible, specific accounts cannot be credited. It is

recorded by debiting Bad Debt Expense and crediting Allowance for Doubtful Accounts, a contra asset

account. When a specific account is identified as worthless, it is removed from both Allowance for

The basis for the adjusting entry at the end of the period is the estimate of the amount uncollectible. The

two methods that are commonly used are the percent of sales method and the analysis of receivables

method. Since the accounts receivable is created by credit sales, the uncollectible amount can be

estimated as a percentage of sales. After calculating the amount that you want in Allowance for Doubtful

Accounts, you need to check the current balance of the account. After writing off the past period’s

worthless accounts, the account may have either a debit or credit balance at the end of the period. If the

account has a credit balance, it must be subtracted to determine the amount of the adjustment. If the

Key Terms and Definitions

• Aging the Receivables - The process of analyzing the accounts receivable and classifying them

according to various age groupings, with the due date being the base point for determining age.

Relevant Example Exercises and Exhibits

• Example Exercise 8-2 Allowance Method

• Example Exercise 8-3 Percent of Sales Method

SUGGESTED APPROACH

It is helpful to open your discussion of the allowance method by proving the need to estimate

uncollectible accounts. The following lecture notes will assist you in relating the allowance method to the

matching concept.

The allowance method of accounting for uncollectible receivables asks the accountant to estimate the

accounts that will not be collected and to record this expense before customers actually fail to pay. This

method adheres to the matching concept by recognizing the expense of uncollectible accounts in the same

was written off. This is also a good time to discuss the meaning of a debit or credit balance in the

allowance account prior to the adjusting entry. 2) The second area involves how the adjusting entry

amount is determined. There are two options: the percentage of sales method and the analysis of accounts

receivable method. If you break the text content into these two distinct areas, it can minimize the fact that

there is a lot of material in this one objective.

152 Chapter 8 Receivables

LECTURE AID—Uncollectible Accounts and the Matching Concept

The following explanation may help you present the need to estimate and record uncollectible accounts.

The matching concept dictates that all expenses incurred in making a sale or providing a service are to be

In most cases, however, you don’t find out that an account receivable is uncollectible until several months

after the sale is made. Therefore, at the end of each accounting period, you must estimate your losses

resulting from sales to customers who will not pay and record this expense.

The journal entry to record uncollectible accounts:

Bad Debt Expense……………… XXX

Allowance for Doubtful Accounts……. XXX

DEMONSTRATION PROBLEM—Entries for Uncollectible Accounts

Kids-At-Play is a toy store that began operations this year. At the end of its first year of operations, Kids-

At-Play had accounts receivable totaling $50,000. The store’s manager estimates that $1,500 of those

receivables will not be collected.

Journal entry to record uncollectible accounts at the end of the year:

Bad Debt Expense……………… 1,500

Allowance for Doubtful Accounts……. 1,500

Chapter 8 Receivables 153

Many students will want to debit Bad Debt Expense when writing-off an account. Explain that Shirley

Smith’s $500 account was included in the $1,500 uncollectible accounts expense recorded at the end of

last year. Therefore, debiting the expense account now would record the expense twice.

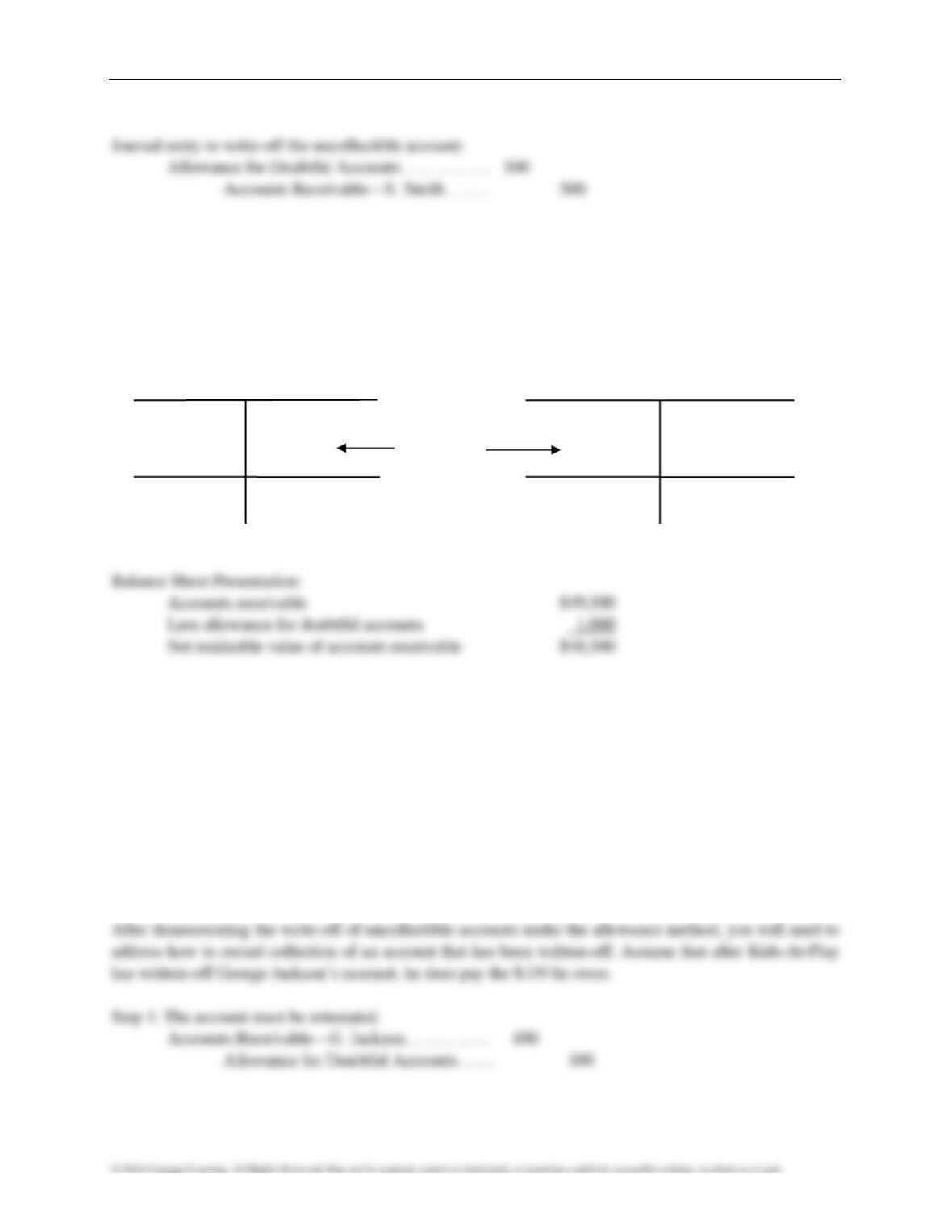

After writing-off the uncollectible account, the T accounts and balance sheet would appear as follows:

Accounts Receivable Allowance for Doubtful Accounts

Bal. 50,000 Entry to Bal. 1,500

500 Write-Off 500

Account

Bal. 49,500 Bal. 1,000

Point out that the net realizable value of accounts receivable did not change. Kids-At-Play still expects to

collect $48,500 of its receivables. All that has changed is that the company now knows that Shirley

Smith, who owes $500, is one credit customer who will probably not pay. There still is approximately

$1,000 in bad debts left to be discovered.

Ask your students to record the following journal entry in their notes: Kids-At-Play received notice that

another customer, George Jackson, will not be able to pay his $100 account receivable.

Allowance for Doubtful Accounts…………….. 100

Accounts Receivable—G. Jackson……. 100

DEMONSTRATION PROBLEM—Estimating Uncollectible Accounts Based

on Sales

When accountants estimate uncollectible accounts based on sales, they determine the amount of expense

to be recorded.

Assume that a business sold $750,000 worth of merchandise on credit. The business estimates that 2

percent of all credit sales are uncollectible.

Expense to be recorded = $750,000 2% = $15,000

DEMONSTRATION PROBLEM—Estimating Uncollectible Accounts Based

on Receivables

Break this explanation into three parts. First, use the series of exercises from the book to demonstrate 1)

calculating the due date of overdue accounts, 2) completing a spreadsheet to determine the amount of

estimated uncollectible accounts for the upcoming accounting period, and 3) recording the journal entry

to establish the Allowance for Doubtful Accounts adjusting entry.

Additional explanation of the adjusting entry execution is provided below.

based on the estimate of bad debts

The adjusting entry to record uncollectible accounts is:

Bad Debt Expense………………. 1,800

Allowance for Doubtful Accounts…….. 1,800

Assume that the accountant determines that $2,000 of the current accounts receivable will probably not be

Your students may question why the Allowance for Doubtful Accounts would have a debit balance. The

following T account explaining the entries that affect the Allowance will show that a debit balance occurs

when the amount of bad debts is underestimated and there are more actual write-offs than expected. In the

above example, bad debts from the previous period were underestimated by $200. Since the allowance

came up short, the entry to record bad debts in the current period is $2,200—the current expense of

156 Chapter 8 Receivables

Allowance for Doubtful Accounts

Actual Write-Off Adjusting Entry to

of Bad Debt Record Estimate of

Bad Debt

GROUP LEARNING ACTIVITY—Entries for Uncollectible Accounts

TM 8-1 presents entries for your students to prepare in small groups. This exercise asks them to estimate

uncollectible accounts based on receivables, make the adjusting entry for uncollectible accounts, and

write-off bad accounts. The solution to this exercise is shown on TM 8-2.

OBJECTIVE 5

Compare the direct write-off and allowance methods of accounting for uncollectible

accounts.

SYNOPSIS

Using the direct write-off method, there is no adjusting entry at the end of the period. At the end of each

period, the allowance method records an adjusting entry. These two approaches are compared in Exhibit

4, and differences are shown in Exhibit 5.

Relevant Example Exercises and Exhibits