CHAPTER 8

SOLUTIONS TO EXERCISES—SET B

EXERCISE 8-1B

Jan. 6 Account Receivable — Chico Inc. ……………… 8,400

Sales Revenue ……………………………………. 8,400

EXERCISE 8-2B

Jan. 10 Accounts Receivable—McCarty ………………… 1,700

EXERCISE 8-3B

(a) Accounts Receivable …………………………………….. 780,000

Sales Revenue …………………………..……………. 780,000

EXERCISE 8-3B (Continued)

(c) Accounts Receivable ………………………………….. 2,000

Allowance for Doubtful Accounts ………….. 2,000

(d) Bad Debt Expense ………………………………………. 18,200

Allowance for Doubtful Accounts ………….. 18,200

Allowance for Doubtful Accounts

Beg. Bal. 9,000

(e) Accounts Receivable Allowance for Doubtful Accounts

Beg. Bal. 210,000 Collections 743,000 Beg. Bal. 9,000

(f) Net realizable value of receivables is $217,800 ($240,200 – $22,400)

EXERCISE 8-4B

(a) Dec. 31 Bad Debt Expense ……………………………. 600

Accounts Receivable—Elk Company 600

EXERCISE 8-5B

(a) Accounts Receivable Amount % Estimated Uncollectible

Current $60,000 2 $1,200

1–30 days past due 14,000 5 700

$9,500

(b) Mar. 31 Bad Debt Expense …………………………….. 6,900

(c) The total balance of receivables increased from 2013 to 2014. However,

of concern is the fact that each of the three categories of older accounts

EXERCISE 8-6B

December 31, 2013

Bad Debt Expense ………………………………………………….. 10,400

Allowance for Doubtful Accounts

[(10% X $90,000) + $1,400] …………………………... 10,400

EXERCISE 8-7B

Nov. 1 Notes Receivable ……………………………………… 90,000

Cash ………………………………………………….. 90,000

Dec. 11 Notes Receivable ……………………………………… 4,500

Sales Revenue …………………………………… 4,500

EXERCISE 8-8B

2013

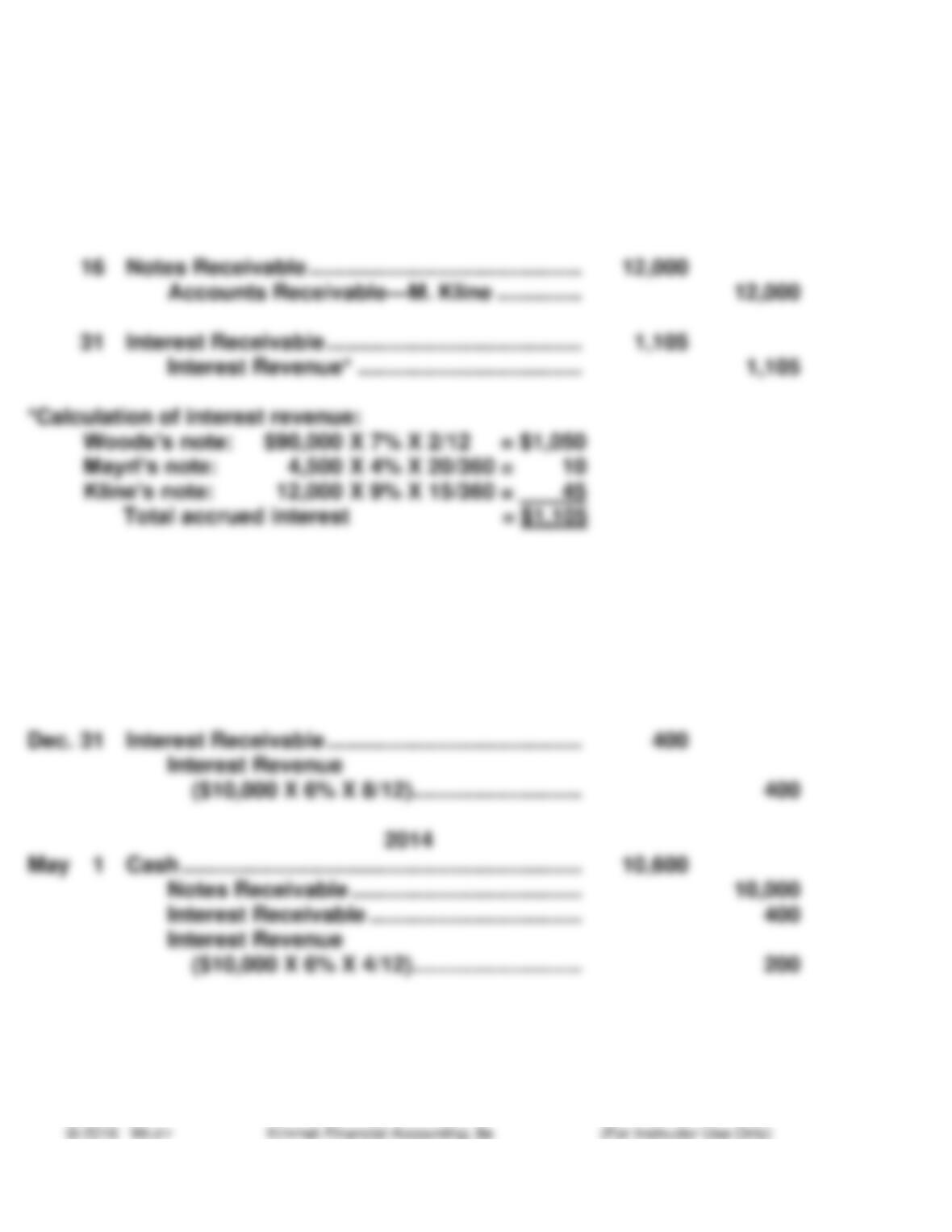

May 1 Notes Receivable ……………………………………… 10,000

Accounts Receivable—S. Doisey ………… 10,000

EXERCISE 8-9B

MORRIS CORP.

Balance Sheet (partial)

October 31, 2014

(in thousands)

Receivables

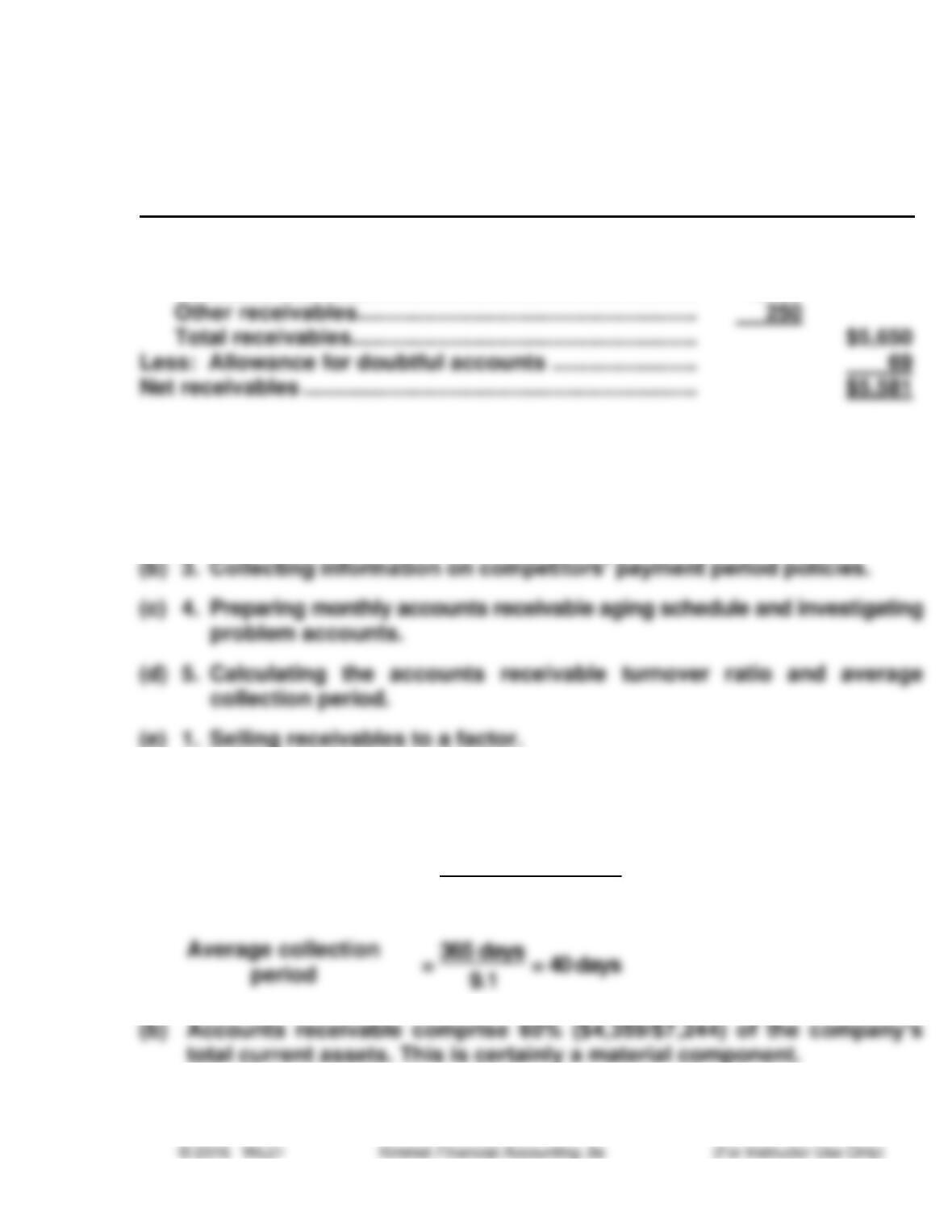

Notes receivable ………………………………………………… $2,000

Accounts receivable …………………………………………… 3,400

EXERCISE 8-10B

(a) 2. Reviewing company ratings in the Dun and Bradstreet Reference Book

of American Business.

EXERCISE 8-11B

(a)

Accounts receivable

turnover

=$37,953

($4,359+ $3,942)/2 = 9.1 times

EXERCISE 8-11B (Continued)

(c) The balance in the allowance account increased $22 million ($158 – $136)

while its accounts receivable increased $439 million ($4,517 – $4,078).

As a result, the allowance for uncollectible accounts increased from

EXERCISE 8-12B

(a) At first glance it appears that Gordon’s liquidity had deteriorated over

the past year since the company’s current ratio has fallen from 1.5:1 to

1.3:1. However, it is taking the company less time to collect its

accounts receivable as evidenced by the higher accounts receivable

(b) Changes in the turnover ratios do not directly affect profitability. However,

improvements in turnover generally indicate that the company is better

(c) There are several steps that Gordon might have taken to improve its

receivables and inventory turnover:

Receivables

– The company could limit credit to only the best customers,

however, this could negatively affect sales.

EXERCISE 8-12B (Continued)

Inventory

– The company could limit the amount of inventory by improving its

purchasing relationships with suppliers. If inventory could be pur-

chased more frequently, required inventory levels could be reduced.

EXERCISE 8-13B

Mar. 3 Cash ($900,000 – $36,000) …………………………. 864,000

EXERCISE 8-14B

One possible reason Auto-Shed chose to sell its receivables may have

EXERCISE 8-15B

May 10 Cash ($2,500 – $95) …………………………………… 2,405

EXERCISE 8-16B

July 4 Cash ($300 – $12) ……………………………………… 288

EXERCISE 8-17B

(a)

Accounts Receivable

Beg 48,000

(b) The quality of earnings ratio is net cash provided by operating activities

divided by net income. If accrued sales exceed cash collections, then net

(c) If the company relaxed its credit requirements it should increase its esti-